This is precisely what this overpriced and frozen housing market needs.

By Wolf Richter for WOLF STREET.

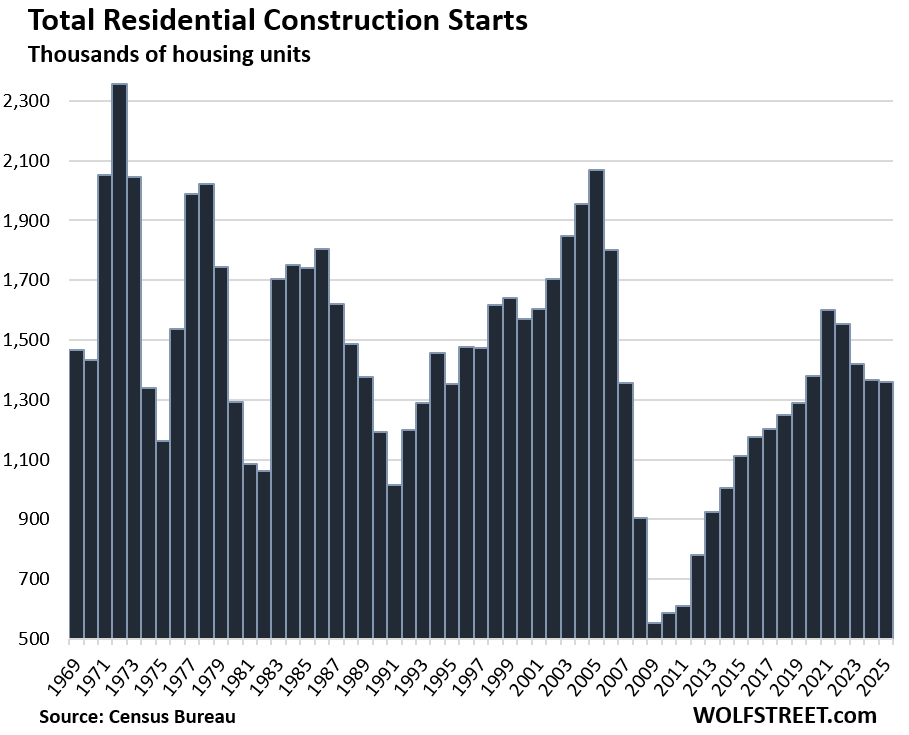

In 2025, construction was started on 1.36 million privately owned housing units, down just a hair from a year ago: 943,000 single-family housing units and 416,000 multifamily housing units (condos and rental apartments), according to Census Bureau data today.

About 2.3 people occupy a housing unit on average. So the 1.36 million housing units that were started in 2025 would provide a home, when completed, for 3.1 million additional people. But the US population increased by only 1.78 million people in the 12 months through mid-2025; and for the 12 month through mid-2026, it is projected to grow by only 756,000 people; and growth might further decline in the following years, according to the Census Bureau’s estimates.

In the years before 2009, the US population grew by 2.5-2.8 million people per year. In the 12 months through mid-2025, population growth was half that. For the 12 months through mid-2026, population growth will be between one-third to one-quarter of that. This continued flood of new housing supply amid dramatically slowing population growth is precisely what this overpriced and frozen housing market needs.

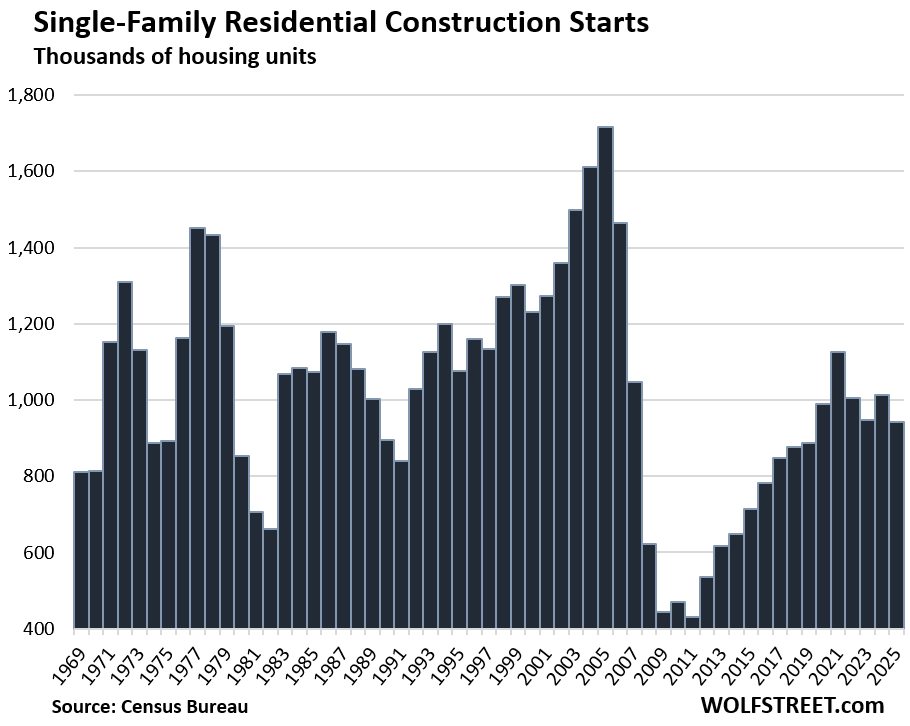

Single-family housing units.

Construction starts of privately owned single-family housing units, at 943,000 in 2025, were down by 6.9% from 2024 but roughly on the same pace as in 2023, as homebuilders pulled back amid very high inventories of new homes for sale and falling prices.

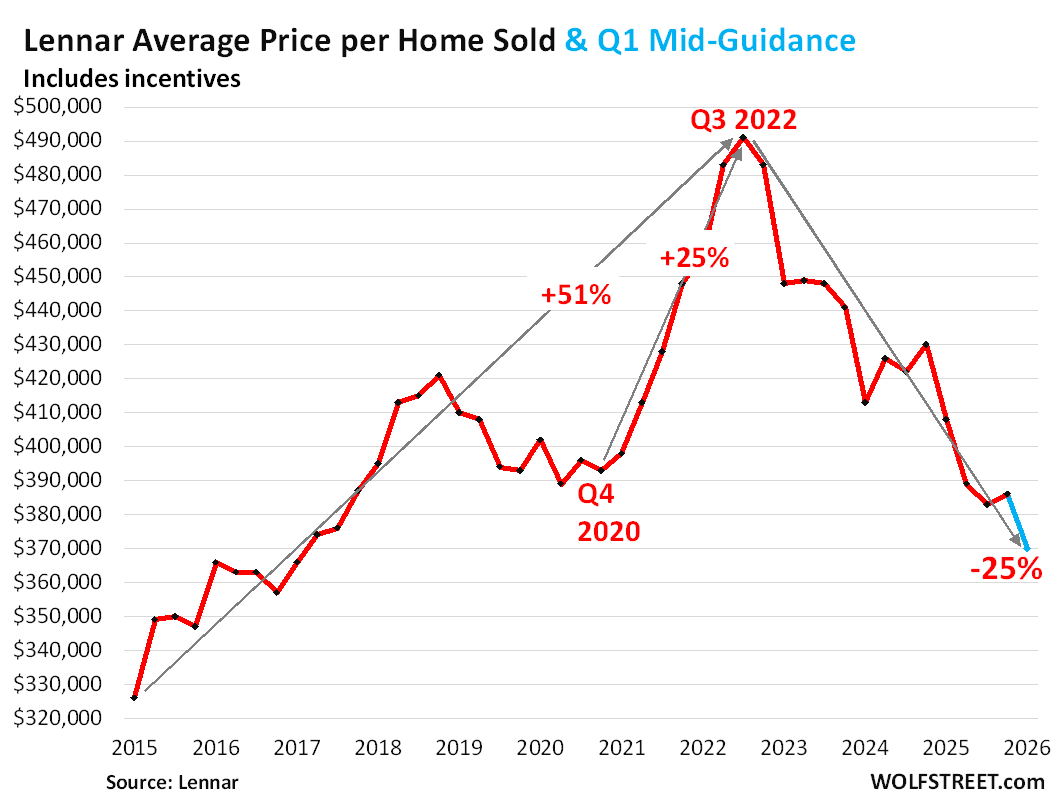

Falling prices of new single-family homes: For example, Lennar, one of the largest homebuilders in the US, has been trying to maintain its sales volume by piling on incentives, cutting prices, giving up a substantial part of its big-fat pandemic-era profit margins, and building at lower costs.

As a result, the average price of the homes that it sold has plunged; and for Q1 2026, it guided the average price down further, to a range of $365,000 to $375,000 net of incentives. The mid-point ($370,000 blue in the chart) would be the lowest sales price since Q1 2017, and down by 25% from the peak in Q3 2022 ($491,000).

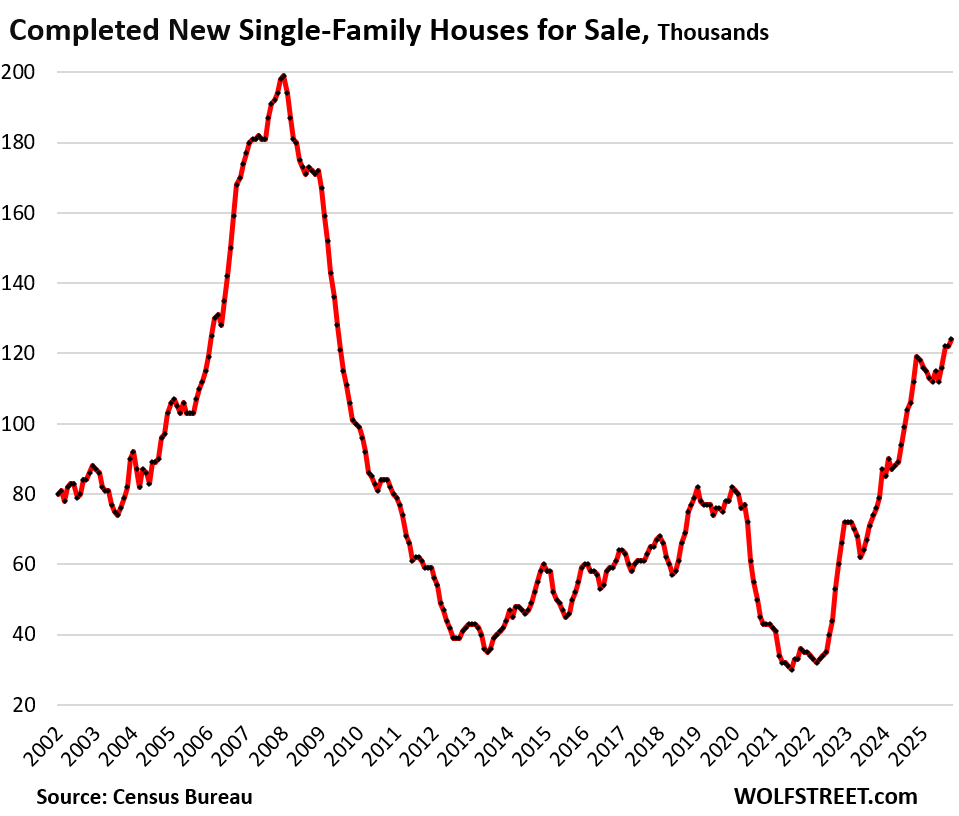

Soaring inventories of new single-family homes: Inventories of completed single-family homes for sale by homebuilders have piled up to the highest level since 2009, to 124,000, per the Census Bureau’s latest data available through October. And homebuilders are responding to it with lower average selling prices. Bring on the supply!

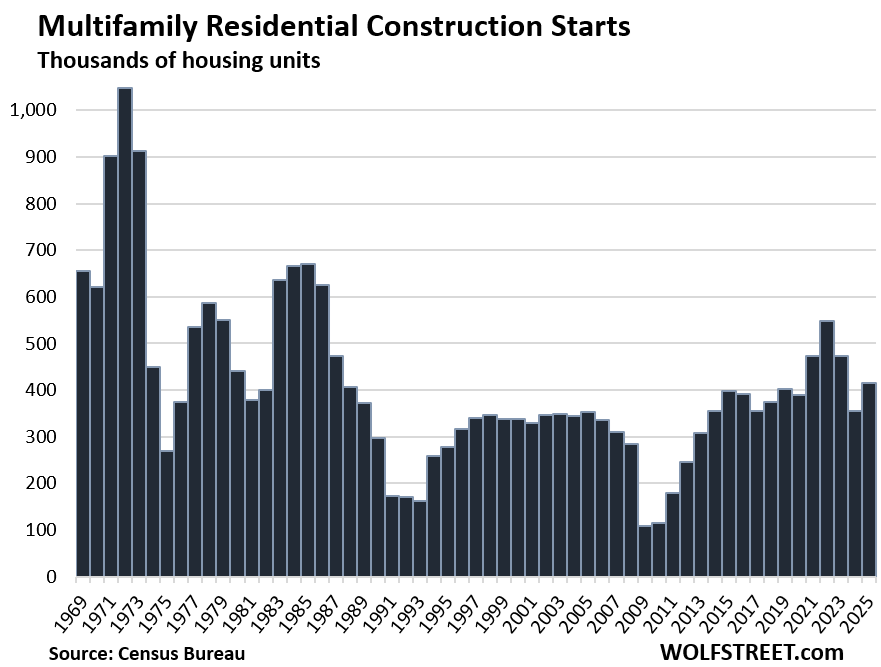

Multifamily housing units.

Construction starts of privately owned multifamily housing units (rentals and condos in buildings of 2 or more units) rose by 17.4% to 416,000 units in 2025.

Outside of the years 2021-2023, the 2025 pace was the highest since 1986. Bring on the supply!

In many markets, there has been a flood of higher end rental apartments and condos coming on the market. The bigger projects take years to plan and build. Vacancies have been rising as these units came on the market. Many projects that had been planned but not started became stalled due to lack of financing as the CRE depression spread around. Asking rents have been edging down in some of those markets (but rising in others). There have already been a number of large multifamily defaults, and the multifamily CMBS delinquency rate has surged to over 7%, from 1% in 2024.

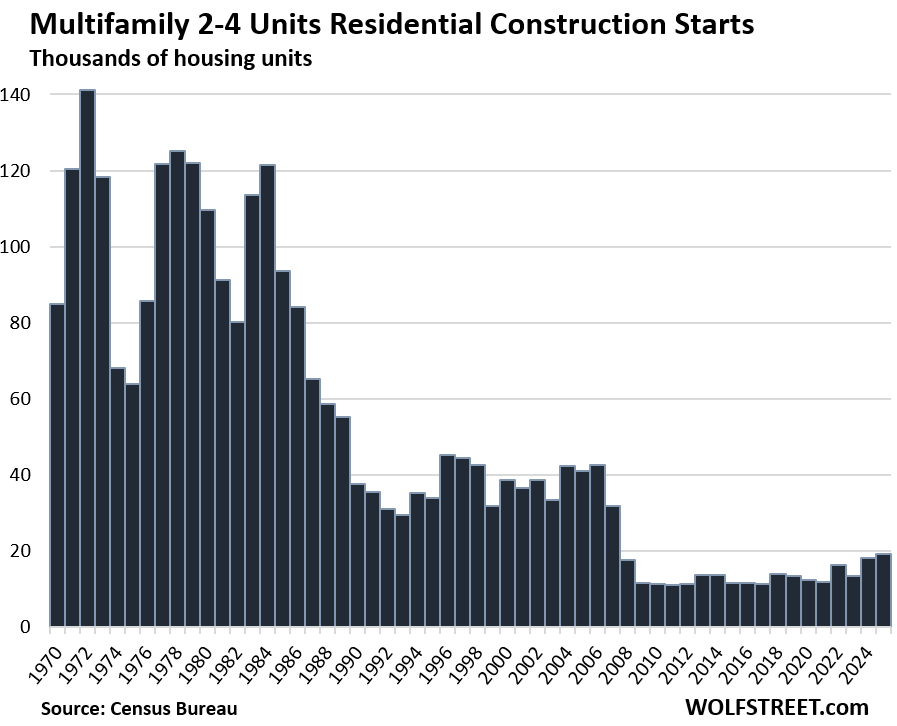

About 95% of these multifamily housing units were in buildings with 5 or more units. Only about 5% were in small buildings with 2-4 units.

Construction starts of housing units in small multifamily buildings with 2-4 units accounted for just 5% of all multifamily construction starts, at 19,100 starts in 2025.

But the pace has accelerated by 66% since 2015 (11,500 starts), sort of a rising-from-the-ashes moment, after that segment had nearly vanished in 2008. This is a playground that is accessible to mom-and-pop developers and landlords.

In densely populated urban cores, higher-end multifamily housing units (condos and apartments) are about the only type of housing that is getting built.

With higher-end apartments, builders are targeting “renters of choice” – people who could afford to buy a house out in the suburbs, but want to live in a modern high-rise in a central location with all the amenities and conveniences, a short commute, possibly an easy social life, and the feeling of being the middle of things, topped off by the flexibility that rentals provide.

Developers cannot target lower-income tenants or buyers because the construction costs just don’t pencil out, unless the buildings are subsidized, and there is that too.

Renters with less stellar incomes generally have to make do with renting apartments or condos in older buildings in less desirable areas, sometimes in run-down buildings with five decades of deferred maintenance.

Single-family construction has been spreading further out from urban cores – the urban sprawl that is everywhere. This includes “build to rent” single-family developments, designed and built specifically as rentals mostly for “renters of choice” by large single-family landlords or by builders that then fill the developments with tenants and sell the income-producing project to large landlords, pension funds, and other funds.

These build-to-rent developments have common amenities, a leasing and maintenance office, and are more efficient to manage for the landlord than individual houses scattered across their market, and they’ve been selling those scatter units here and there at sky-high profits for the past two years. Read… The Biggest Single-Family Rental Landlords and Multifamily Landlords in the US: Big Shifts Underway

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf what’s your take on this post GFC underbuilding / housing shortage narrative in general? It seems convincing on its face but I am skeptical… lots of speculators out there.

It has been the most cited real-estate industry propaganda whose sole purpose is to manipulate up home prices by rationalizing them.

And after manipulating up home prices for years, they’re too high, and there IS a shortage of reasonably priced homes, thanks to all these efforts to manipulate up prices.

But if you have enough money, you can buy 100 homes a day, which proves that there is no housing shortage, but prices are too high.

Lots of new supply for years to come with slow population growth is exactly what the real estate industry needs. Bring on the new supply! Construction is a big contributor to the economy.

There were 15 million vacant housing units in Q4, 11.6 million were vacant year-round, according to the Census Bureau.

I know you are talking nationwide, but even with the price increases of 2001-2003, in north Fort Worth, suburban areas have 3000 sq, ft houses available for $340,000, an 8 mile section of highway was recently upgraded to 6 lane freeway.

That’s not overpriced, especially since employers continue to move employees to the DFW area.

MS,

That 340k number is interesting – and a bit surprisingly low (thank god) if accurate.

But this is a good example of how the housing market is still a bit opaque/fragmented (relative to other financial mkts – and 20 years of Fed ZIRP policies financialized the absolute crap out of housing mkts).

The $340k development in FtW would be findable with a focused geocentric search (because, in the *final* analysis, housing mkts are local.).

But idk if there is a widely known, *nationally aggregated* database that is capable of shooting out all new build communities currently selling…sorted by *ascending price*, across the entire US.

Because that isn’t how RRE has been traditionally marketed – instead the focus is almost entirely on local geo mktg.

But we need *nation-wide* price signals, broadly disseminated to help unfreeze a frozen mkt.

True nationwide New build info/prices, broadly disseminated, would influence business siting decisions, job taking decisions, etc.

And *those* shifts would help unfreeze the housing mkt.

We have a nationwide price signal, called the median price of new homes sold. It’s reported monthly. And I report on it pretty frequently with a chart. But it’s not very useful because it only includes the contract prices, and not the incentives. As in the auto business, much of the price cutting happens via incentives, including interest rate buydowns.

But you can go to all the builders’ websites and see what they’re selling and where. For example, you can to Lennar’s site and search in your city, such as Dallas, and it puts up a list of its new homes for sale, with a map too. This goes by development. So then you go to the specific development you’re interested in (click on the icon on the map), and then you get real asking prices per home, and with the price cuts from the prior price, and how many homes are available in that development. Lennar now has lots of SFHs in the Dallas area below $300K.

Or you can read the articles I post on this site where I give you a chart of Lennar’s average price of homes sold per quarter across the US, which I take from its quarterly financial report. And sometimes I also post DR Horton’s average home price chart.

Wolf, I don’t really hear anyone talking about the number of vacant homes being an issue.

In the markets I’m familiar with, small cool touristy markets across the country, they all have one thing in common: tons of housing stock sitting empty 11 months out of the year.

I’m in Oxford, MS and we have roughly 5000 vacant units that are second homes.

“Year-round” vacant means year-round vacant, not “11 months” vacant.

There is serious price discounting in nearly all ski areas in the West. I see it every day in my daily searches in from realtor.com and zillow.com.

And that’s w/o any serious economic problems. Imagine what the discounting would look like if we had a serious recession.

Wolf, all this talk of ideas to adjust the housing market to tilt towards families instead of investors has left out one important, and I think, huge elephant in the room. Allowing depreciation for an appreciating investment. One simple change to the tax code with a phase in and perhaps a housing unit limit would have a dramatic effect on the investment component to rental housing. Your thoughts?

So you can’t depreciate the value of the land, only the improvements (buildings, fixtures, etc.). In theory, much of the appreciation we’ve seen in the past has been on the land, so depreciation isn’t permitted on the portion appreciating the most.

In practice, I suspect that in many cases, too much value is being ascribed to the improvements and too little to the land, but I don’t have any data to back that up, it’s just an instinct.

There’s also a decent argument that the prescribed useful lives (27.5 years for residential properties and 39 years for commercial properties) are too short. The useful life estimation means that, in theory, the residual value is 0 at the end of that period. For an office printer, as an example, it’s considered 5 years. Given how much technology has gotten cheaper, that’s probably about right. How much would you pay for a 5-year-old printer? Probably pretty close to 0.

A house, built today, and again, just the value of the house, NOT the land, is not worth 0 at the end of 27.5 years, unless it isn’t maintained at all and has to be razed.

But that’s what the IRS considers it. I don’t know what the right number is.

The tax code should be modified to allow only one home + 1 additional home to be depreciated. This will get rid of all the speculators and free up more homes for families.

@Wolf thanks for pointing out that that “real-estate industry propaganda whose sole purpose is to manipulate up home prices by rationalizing them” (few people know this).

I may have missed it, but have you ever posted about the (almost all developer funded) YIMBY groups that push for more development (and usually higher developer profits with increased density and reduced parking).

P.S. I’m no expert on Census Data (I did have a guy renting for me working for the Census in 2020), but I was always told that the Census marks a home as “vacant” if it is “vacant” the time they visit (and they don’t make any effort to see if it has been “vacant” for a full year) Google found this:

Yes, the U.S. Census Bureau considers many summer or seasonal rentals as vacant if they are not the primary, year-round residence of the occupants at the time of the survey. These units are classified under “Vacant – Seasonal, recreational, or occasional use” because the residents have a usual home elsewhere.

You’re understanding of the Census Bureau’s determination when a housing unit is vacant is not correct (BTW, the determination is not by “visit” but by “interview”). And note the difference between vacant and year-round vacant. The Census Bureau has a long list of reasons why a housing unit is vacant, including “held off the market.” It’s a 14-page document and you have to read the whole thing all the way down, and not just ask AI for a summary. Start on page 5:

https://www.census.gov/housing/hvs/files/currenthvspress.pdf

It’s not that ho.es are so expensive, its that our dollars are worth so much less than just five years ago.

When the (not) federal reserve prints 40% of all US dollars into existence over the last several years, its inevitable that the other 60% of dollars lose an incredible amount of value.

Hence, housing prices reach insane levels, like what we’ve seen recently ..

YMMV….

Yes, but also no.

Real estate markets are still ultimately set by supply and demand. Inflation or no, people have to buy up the homes for sale, or prices will fall so they do.

RE investors who think they are guarding against inflation should perhaps consider how real estate does in places with high inflation like Turkyie or Russia. Who wants to buy a house in a broke country?

How do you see this playing out amid a weakening dollar and low FFR but relatively high long rates?

You fail to mention that going back to the year 2000, on average 700,000 to 1,400,000 residential units are demolished or destroyed each year. Thats an important component to realize. When taking this into account – pace of new construction appears to be on par leading to further housing shortage.

good lordy. those figures are totally nuts. The number of housing units removed is a minuscule percentage. Where do you come up with this stuff? Who’s circulating this stuff?

In 2025, 1.471 million net housing units were added: new construction minus removals. This includes privately owned housing units — the type I discussed in this article — plus public housing units. Chart #1 below

In 2024, 1.411 million housing units were added, see Chart #1 below. The recent peak was 2022, when 1.605 million units were added.

At the end of 2025, there were 148.7 million total housing units, up by 1.471 million year-over-year obviously. Chart #2

Over the past 10 years, the total housing stock on net rose by 13.2 million housing units (new construction minus removals).

All data from the Census Bureau’s quarterly “Housing Vacancies and Homeownership.” All you have to do is look it up. It’s not a secret. Or you could just ask me, and I will tell you 🤣

Also a lot of flipping going on which I don’t think any of these stats capture. Flippers have made a lot of formerly decrepit housing inhabitable here in Indy.

Flipping has zero to do with this. We’re talking about new housing units being built and sold by construction companies and added to the total housing stock.

Flipping is when someone buys an existing housing unit, more less rehabs it, and resells it. Flipping does not add to or subtract from the housing stock. It has zero effect on the growth rate of the housing stock.

>Flipping does not add to or subtract from the housing stock.

When flippers are as I said turning formerly uninhabitable housing into habitable housing, that adds to the housing stock. There is a lot of that going on here.

Not to mention most demolished units are either immediately redeveloped or abandoned homes and wouldn’t have any impact anyway. Have you ever met someone who’s like “yeah I used to live downtown but they demolished my home”?

The greater Boston area needs at least a quarter million housing units over the next decade to keep up with demand. However most of these homes will be multi family since the area is already too densely populated to accommodate that many new single family homes.

The longstanding restrictions on multi family housing are mostly to blame for the area’s current crisis of too little housing at prices few people can afford. The problem was (and continues to be) so severe, the state legislature had to step in and force cities and towns across the region to build more multi family housing. Too little, too late unfortunately.

It’s a problem that crosses the political lines and few are willing or interested in solving.

I am surprised that employers didn’t step-in to ask the legislature to reduce the restrictions because the cost of housing and taxes makes the typical salary in Boston look very uncompetitive to other parts of the U.S.

I question whether places in the Northeast need more people living there. It’d be better for the American population to spread out a little bit.

Flipping affects the supply of housing in this way: Before the rise of the flipper-industrial complex, dilapidated houses in my formerly underappreciated town would get torn down by the city, often the lot was sold to a neighbor. Thus a reduction in housing stock. Now that almost never happens.

I would be interested to know if the teardowns continue in the rust belt cities.

We might also think of housing supply within customer segments. Flipping can take a house out of one segment and add it to another.

This is partly why we have a scarcity of starter homes. Some of what would have been starter homes have been flipped up into an “upgrade” home.

Which is emblematic of the American economy in general. As wealth stratification has grown, the car companies no longer want to make the $24,000 starter new vehicles, but the $60,000 luxury sedans. Same principle.

I like the term flipper industrial complex. To your point — flippers may have delayed demolition of a dilapidated house by a decade or two, but most flippers I’ve met are unskilled and unscrupulous. Most of the work can’t be considered restoration. Genuinely curious, what condition are the rehabbed homes currently in, and how long ago did the flippers work on them?

It’s called “facadomy.”

Make it shiny, ask top dollar: never answer a call from the buyer = PROFIT!

Boston will always have land issues because you can’t build in the Boston harbor. That plus all the NIMBYs make it an impossible market to grow.

I’ll buy a home when it’s cheaper to buy than rent, or once prices come down to a point where I don’t have to compromise my lifestyle. I have affordable rent considering my location in Bay Area CA.

Some truly hopeful news. Thanks for calling this out.

More multifamily housing is coming on the market, more private housing will too. US immigration is down about 80% and, thanks to that, the US is reaching its expected population cliff abruptly now rather than gliding into it over a half century to come. How will that work out? The way it has everywhere else. Look at smaller more heavily populated Europe and Japan. It will hit more thinly populated aging areas first and hardest. Population is changing overnight. It looks like models and calculations are still absorbing the impact. I think we will still experience a decline in rental and property value over the next couple decades due to abrupt shift in demographic arc.

The presumption that the current immigration environment will last beyond 2028 seems as unlikely to me as the presumption that the immigration environment of 2022 would persist beyond 2024.

Maybe not the current environment, but the border will probably be closed now for at least a decade.

Like him or not, Trump proved Biden wrong when Biden insisted he can’t close the border. It is an unwinnable issue now to open it back up.

Now as for immigration reform? Sure that may be on the books and probably necessary.

Most immigrants to America do not cross a physical land border–they arrive through an airport. The Trump administration has greatly reduced the issuance of immigrant visas, though the degree is hard to quantify as 2025 data is not available yet. But also application volumes have slowed significantly (especially from non-shole countries” in the face of exec branch rhetoric.

The last year may have soured both immigration and vacationing into the US for a generation. We shall see.

Don’t threaten me with a good time

The idea that anything from 2022 would be a pattern for the future–inflation, job market, WFH, crime–was ridiculous, yet we’re still seeing the echoes in popular perceptions.

That’s the “capitalist grift”!

Always make the most favorable comparison. Prices are crashing!

From a wacko bubble peak? Just an intraday move? Whatever comparison it takes to make it “THE time to buy!”

Timeframe and external factors matter.

Wolf, thanks for highlighting the drop in demand for new residential construction indicated by slower population growth. The overbuilding stats look even worse when measured against household growth–a more accurate predictor of demand. For 2025–2035, Harvard’s Joint Center for Housing Studies projects a “middle case” annual increase of roughly 860,000 households, and a “low case” annual increase of only 690,000 households if the recent huge decline in net inward migration continues. https://www.jchs.harvard.edu/blog/new-projections-anticipate-slowdown-household-growth-and-housing-demand

Will they bring back the liar or NINJA loans? Interest only mortgages? Pick-a-payment?

Banks back in the mortgage business? Mortgage backed securities. Credit default swaps? The good old days. Gut Dodd-Frank?

“ The Federal Reserve has announced plans to loosen capital requirements and supervisory rules for banks to encourage more mortgage lending. Regulators want to reduce barriers that have pushed mortgage origination away from banks and into lightly regulated non-bank lenders.”

The biggest mortgage lenders are now shadow banks, they have little regulation, and they’re huge, and they can blow up and do a lot of damage. That has happened because a specific formula regarding how securitized mortgages are handled in a bank’s capital formula pushed banks to pull back from the mortgage business. You need to read her entire speech to understand what is going on. I know it’s complicated, and it’s easier to make silly comments than to read a complicated speech.

Most of the mortgages are now and will be securitized by the US government anyway, and the credit risk is with taxpayers, not banks. So from a risk point of view, it doesn’t matter anyway.

As a retiree with a number of rentals, I plan to liquidate them all in the next 5 years or so. The point of this article is something I’ve been thinking for a long time – that demographics favor a housing surplus in the coming years. If nothing else, as those in my age bracket no longer need housing, those units will come to the market as they are sold by heirs. Personally, I think housing prices will be flat for some time until they become 20% cheaper or more in real terms. This is especially true in existing homes as they aren’t typically updated before being put on the market by non-investors.

I think that’s true for a lot of assets, including stocks. My belief is that we’ve just pulled demand forward. But nobody thinks an environment where stocks don’t return 8-10% per year over the next decade is possible.

Interesting times, as they say.

I had the same thought. However, they are paid off and I decided to just lower rents if need be. I recently had to drop one $100/mo and applications surged. First decrease in over 10 years. I keep par with our local military base’s BAH for E5 with dependents, but the market is shifting. Thousands of new townhomes built, but the city planners say we are still thousands of doors short due to rapid migration. This younger generation don’t seem to care about garages or yard space. They have bought into the own nothing and be happy, even without personal space for the same price. Interesting times.

“They have bought into the own nothing and be happy”

That’s like concluding the victim bought into the assault.

One must move forward and play the hand they’ve been dealt. A realistic analysis shows that affordability metrics have been slanting against the general population for a generation or two.

I don’t know your age, but I wouldn’t be surprised if your parents were able to afford a house, with space and to “keep up with the Joneses,” all on a single income. Just saying: neither of my Grandmothers had a 9-5.

I hope that the prophecy will one day be fulfilled, that housing prices will go down. It’s like waiting for the second coming.

“Capitalism”: noun. an economic system in which every participant competes to survive in a perpetual zero-sum housing crisis.

Capitalism: a system where people are free to trade goods and services as they wish.

I follow zillow in my zip code. 3 years ago anything under 200k would get snatched up and you see it selling several months later for 350k or more.

Now I am seeing livable homes for 200k and under. I say livable because you can tell someone is living there because of the clothes and stuff piled around. Not perfect of course but inhabitable. The flipped houses have price reductions.

A key element of the “housing bubble” as measured in large metropolitan areas is the massive decrease in crime that has occurred since the 1990s.

Now instead of fleeing cities to get away from crime, people are fighting like subway rats to live in big cities.

What isn’t measured so much is the price of non “metro area” housing in all those 1980s/1990s exurban developments where people were commuting an hour or more into the cities each day.