Is it finally time to bottom-fish this stock? Or is it a falling knife?

By Wolf Richter for WOLF STREET.

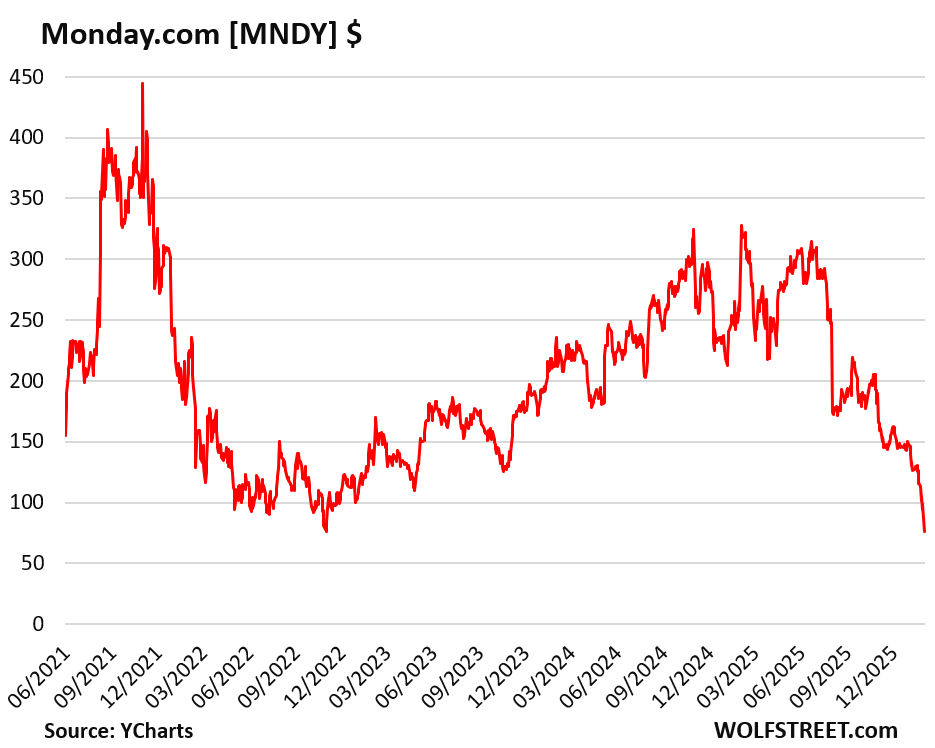

Amid the general repricing of providers of enterprise Software as a Service (SaaS) in recent months, cloud-based collaborative work-management platform with “Agentic AI products,” monday.com, reported earnings this morning, upon which its shares [MNDY] plunged by 22%, to about $76.70 at the moment. If it closes at this price, it will be a record-low closing price.

Since the all-time high in November 2021 ($444.70), the stock has now plunged by 82%, and thereby has become eligible for our pantheon of Imploded Stocks, for which the minimum requirement is a plunge of 70% from the more or less recent all-time high.

The company went public in June 2021 at an IPO price of $155 a share, amid the immense consensual hallucination at the time. Shares are now down by 51% from the IPO price.

In early November, when the stock traded at over $200, 80% of the 25 brokerage firms that cover the stock had a “strong buy” rating on the stock, 8.3% a “buy” rating, and 12.5% a “hold” rating, according to Zacks.

But none had the only rating that would have nailed it: “Sell.” Then, armed with these ratings, the stock plunged by 63% in three months. Why is anyone still paying attention to these ratings?

The stock is traded on the Nasdaq, the company is headquartered in Israel, and files its earnings reports (6-Ks) with the SEC as a “foreign issuer.”

Its Q4 revenues of $334 million, revenue growth of 25%, and adjusted profit of $1.04 per share beat the average of analysts’ expectations.

But its Q1 revenue guidance of $338-340 million fell short; its Q1 revenue growth guidance of 20% fell short; its Q1 guidance for operating income fell short; and its guidance for the full year metrics fell short.

GAAP operating income dropped to $2.4 million in Q4, from $9.6 million a year ago; GAAP operating margin dropped to 1%, from 4% a year ago.

Finally time to bottom-fish this stock? Or is it a falling knife?

I don’t have answers here, only some observations: With GAAP earnings per share in 2025 of $2.24, and even at the current collapsed share price, the stock still has a trailing 12-month P/E ratio of 34.

That’s high for a company that is dialing down its revenue growth rate to 20%, and maybe dialing-down more later amid a whirlwind of software industry challenges, including from AI, perceived or real. The company also continues to issue new shares and thereby continues to dilute existing shareholders: In 2025, its share count increased by 3.1% year-over-year.

At the current price, the stock has a market cap of about $4 billion. The company does sit on $1.62 billion in cash and marketable securities, and it still has revenue growth, though at a slower rate, and those revenues grew to $1.2 billion in the year 2025. And short interest amounts to about 10% of its float, which could make for some fireworks when these folks cover their short positions.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Ironic, on a Monday. Heh. Our IT staff uses this software. The name Monday always causes confusion.

The stock has a case of the Mondays…sorry couldn’t help myself.

We use Monday. I hate it. It’s at least better than Asana. Imploded because it’s crap.

anyone that is waiting for the next crash seems to be firstly focused on a scenario whereby humanity, the obvious invasive species …

We use Monday as well.

I agree, the name “Monday” is very confusing for our team, and they picked the worst day. Could’ve picked “Friday” or maybe “Happy Hour” at least…

Our experience is that it’s better than using spreadsheets to track workflow, but it’s nonintuitive and was clumsy to implement.

Our company uses this software, it’s like a mural board and an Excel spreadsheet had a baby.

If used properly, I could see it being semi-useful (though probably not worth its cost), but no one uses it correctly so most of the alleged savings are never realized.

I deployed Monday.coms project management tools shortly after their IPO at a state agency that implemented it across all projects. As a consultant with 20+ years of PM experience, I was required to use it along with 10 other PMs.

Their implementation was a disaster and a complete waist of time. After 25 years of IT project managent, it was like using a toy in a professional setting. Everyone was asking if they had a ‘professional” version!

The company is run by amatures with good political connections I’m guessing.

I’m sure for just PM and large complicated projects Microsoft Project Management and other systems could/would be better. Based on Q4 they are serving a niche client base well.

MS Project was great but then again really only had teams of less than 20 to coordinate.

What

Foreign entity having domestic contracts. Must be spies .

No facts to back up accusations but hey sounds great.

BS ini –

Quick – name a few successful startups that do not have political connections! Nothing to do with international intrigue…

Panic was what I experienced when I arrived at work as the main engineer and finding that a another engineer had taken the liberty of changing all of the 2 Billion dollar project drawings including renumbering the streams, the basic components of the mass, heat, and energy balances

I was told about one year ago that using two AI packages in conjunction together allows creation of a website with backend database management for capturing and managing inquiries from the website very easy, and free. No upfront fees or monthly subscriptions.

I was told this by a young man, who had no degree in Comp. Sci. but who does have high IQ and naturally strong math skills. Probably the average person would have problems with the process of using the two AI packages, but eventually, everyone will be doing that.

Yeah, maybe software is becoming obsolete.

AI can create a website frontend no problem, and it can create a content management system.

But no one in their right mind is going to replace the software layers that are at the core of a company with an AI generated vibe site. If you do that, you have no idea what vulnerabilities are in this setup. You have no idea how it will scale. You have no guarantee that it won’t lose or corrupt all your data, including your customer and payroll data, etc. If it’s just a toy website to have fun with, no biggie. But if it’s a bigger operation, no way.

But you can create pieces of software with AI, you can fix software issues with AI (my developer did that on my site when the theme, which is no longer supported, ran into trouble; saved me a lot of money), you can do all sorts of things with AI.

But no big corporation is going to replace the layers of software that represent the beating heart of the company with some AI-created vibe site. That would be fatal for the company in no time.

Wolf – this is a very grounded take and I agree completely. As a software engineer at a large (bureaucratic) firm, i despise using tools like Salesforce, Monday.com etc … however, I doubt these softwares will vanish as soon as the market seems to think. No tech leadership will dump them in favor of something to be built and maintained internally – it is far too much work.

SaaS is oversold imo. These tools are more than their software products – they contain network effects, trusting customer bases, and are layered into the fabric of many large firms. No matter how prevalent AI becomes, firms will still need project management tools, CRMs, etc. In the years it might take to ditch these tools entirely, they will switch to consumption based pricing (vs seat based as they do now) and ride the new wave – if they are competent

Fast-forward to 2028 >> “Nasdaq joins our list of Imploded Stocks”

Classic!

I love investing in companies that will take 30+ years to pay me back.

I think I have more faith in my investment in my daughters lemonade stand. Similar YoY revenue growth, but she can pay back the table, chair, and sign in a matter of months.

All these SaaS companies can come knock on my door for money when trailing PE gets to 15. They are a dime a dozen, particularly in the productivity space. Companies are tightening the belt on subscription plans where the whole company gets charged a seat.

I have made more money over a 30 year horizon not being in the market

MNDY is a limited partnership….PITA come tax time. Pass.

MNDY: 1M: flop. 1W: flop. 1D: Lindsey Vonn.

But but but “It’s in the cloud!”

Many companies have spent huge amounts of money chasing the latest software fads when they never figured out to use what they had already invested/wasted lots of money and employee time trying to implement. Accounting systems became “ERP”.. of which many implementations failed or never reached the level of productivity they were supposed to provide.

Often these “next greatest software solution” are recommended by some consulting firm like Deloitte or PWC, etc. Consultants that were hired by clueless corporate executives who often knew very little about computers or software, they were token hires from the good old boys (and girls too) network. Somebody who knew somebody from “business school “. Double bonus- they pay the consultants to “implement “ the new software system the consultants recommended, and then the consultants outsource it to a bunch of inexperienced people in a third world or brought in on a H1-B visa. And then the company can lay off some of their own experienced employees who actually knew how the company worked.

This was repeated multiple times, and then the cloud came along and gave them all the chance to repeat the stupidity again. Consultants and salespeople got big bonuses, corporate managers got lots of steak dinners, corporate junkets, and liquid lunches. And if a manager got fired for a failed system purchase and implementation their buddies at the consulting firms helped them find well paying management job at another company where the whole process gets repeated again.

And now we get the same stupidity cycle with “AI” which will see a lot more money and effort wasted for minimal gains in productivity but plenty of more layoffs for workers and bonus checks for managers and consultants.

Smart companies were already doing a lot the big data analytics and efficiency gains that “AI” is supposed to provide, they just didn’t call it Artificial Intelligence “.

Now with big expenditures on “AI” things will be much faster, there won’t be a sucker born every minute, it will be a sucker born every second, and if you overpay for the next greatest chip free Nvidia it could be a sucker born every nanosecond!

Sounds like you’ve been around the block in business technology as long as I have. You nailed it. I have seen the same cycle repeat again and again. AI “experts” and “influencers” would have us believe “it’s different this time”. Guess again!

Yeah but someone’s getting rich aren’t they? Just track all those sales by insiders baby!

MW: Oracle’s stock soars as analyst predicts ‘pure upside’ ahead for the battered cloud provider

ORCL +9.54%

MNDY: 2025 was a very good year: $1.23B vol. up 27% y/y. Est growth for 2026: $1.45B/ $1,46B, or 18% up y/y. Non GAAP profit $14 on $100 vol. The number of large customers using our AI products is growing.

FX exchange: if the US dollar rises in 2026 so will profit.

USDX in precarious infection point.

Usdjpy exchange rate near 160+

Japs don’t like it above 160

Stock market runs on the carry trade

Somethings going to break, will the Japs tank the US equities market? Will the fed lower the rates even though inflation is raging to drop the USDJPY exchange rate? Or will they let the Nasdaq burn?

Join us for next weeks episode of Currency Avengers

IXIC: [1W] flop, [1D] flop.

fwiw my friend’s light manufacturing company uses it for project scheduling for construction and delivery as well as inventory management. Some clients now outsource their inventory management to them as well. For their particular industry it has allowed their entire team ( of 7) to see projects, schedules and pick inventory quickly. Probably still over valued stock price wise but they are serving a niche of clients well – based on also reading the Q4 summary.

I use it at my office, doing manufacturing and engineering scheduling and workflow. It does a great job for what we do, but they have been jacking up the price and adding tons of “features” that don’t add value. We even worked with them to help develop their tools early on.

Textbook enshittification, gather a bunch of customers with cheap fees, lock them into the system, then jack up the price and collect rent.

We are going to build a spreadsheet tool in house and jump ship on monday.com here soon. If it were 30% the price, it would be a good deal.

Adding another IT related comment, as someone who spent 28 years in the field in various roles. Clients that use your software, especially as a service, have 10x more reasons to stay so long as the cost is reasonable, they suffer little downtime and the staff like/trained on the platform. We could turn the AI story around and say that Monday has a good solid existing client base and they could churn out new modules/features quicker with AI perhaps – rather than a few AI savvy coders simply whipping up something to put them out of business. Time will tell.

This is a very specific case so they were really beaten . Someone at CNBC built a working Monday.com clone in under 60 minutes using Anthropic’s Claude Code AI tool, spending just $5-15 in compute credits according to the hands-on experiment

With a gazillion holes to get attacked, no guarantee that it will scale, a good possibility that data will get corrupted, and a host of other issues. It’s easy to build a good-looking vibe app. Kids can do that. But that’s not a functional enterprise level tool that customers and money depend on.

A small cross-team of a few AI Engineers and business experts can clone a SaaS product. There’s no need to vibe-code. Only to decompose a large problem into smaller, manageable parts.

White-box, verified, at a tiny fraction of what it cost two years ago. Hard to believe it took this long for the market to price it properly.

> But none had the only rating that would have nailed it: “Sell.”

But then they wouldn’t have been able to sell the stock to their clients, LOL.

> Why is anyone still paying attention to these ratings?

Major firm analyst ratings do generate stock price action. You know the analyst firm will be busy at work finding new buyers for the stock to earn that $ after issuing a buy rating, very nice for anyone who bought in before the re-rating.

> Finally time to bottom-fish this stock?

In the value world there are much better value picks than this. Maybe at $30/share if they hold on to their cash pile and stop acting like they DGAF about shareholders.

During the Lehman financial crisis, a new website emerged called fvckedbanks, or something like that. It would list the names of banks that went belly-up each day. I would go to those bank’s websites before the websites were taken down and read how they are wonderful and outstanding banks. It was amusing.

Software companies are a buy:

1) They’ve got a nice moat. It’s difficult to switch to a competing software package.

2) With most software on the cloud, the marginal cost of making a new sale is very small. I can’t think of any other business which has better operating leverage.

3) AI programming tools will reduce development costs.

4) They’re cheap based on the absurd notion that anyone now can develop a competing software package. It’s not going to happen. The incumbents have a huge advantage over new entrants.

Analyst’s for Monday.Com are so funny. What did they miss??

This was going to happen sooner or later, we don’t need 100 different SaaS products doing the same thing. We will see lots of losers and some winners in the coming years. Monday has a somewhat weak data moat and isn’t as necessary anymore (if agentic workflows really work, which I think they can sort of, the economics are still being worked out). There are some SaaS companies that will come out of this alive (mostly those with strong data moat), but most won’t. Maybe a helpful way to think about is if you removed all people from the workflow, would the software still matter? So whoever owns execution wins.

Monday’s problem is that once Copilot works out their messy interface and other issues, Monday becomes increasingly irrelevant as you can get the same work done natively in MS products. I was testing out integration with PowerPoint earlier today and Copilot autonomously went right into all our project folders, read the previous decks, looked at the strategy docs on SharePoint and suggested slide content based on the context I gave it around client needs and what we wanted to present.

I’m going to set up my first agent this week and build out workflows, some of which involve project management tasks.

It ain’t soup yet, but I’d bet that within a year it will be and Monday then serves no point.

I liked that its name gave it away as a good short. The dot com, as in dot com bust version 2

Falling knives I might catch include Salesforce, Adobe, and Google. I’ll pass on this one.

These are almost approaching value stock territory on a forward earnings basis. And who do people think are going to implement all this AI wizardry to upsell their trapped clients?

Bad case of the Mondays.

Our company uses this software, it’s like a mural board and an Excel spreadsheet had a baby.

If used properly, I could see it being semi-useful (though probably not worth its cost), but no one uses it correctly so most of the alleged savings are never realized.