The “rate check” on Friday to put a floor under the yen was the latest step.

By Wolf Richter for WOLF STREET.

On around midday Friday came the latest step, a “rate check,” with which Treasury Secretary Scott Bessent attempted to put a floor under the yen that had plunged against the dollar, and push back down long-term US Treasury yields that had surged, as he saw the turmoil in the Japanese bond market, and the plunge of the yen, bleeding over into the US.

The New York Fed, at the request of the Treasury Department and acting as fiscal agent for the Treasury Department, asked its primary dealers what exchange rate they would get if the NY Fed started buying yen through them. This “rate check” was a signal that the US government is ready to intervene in the currency market to support the yen against the USD.

As soon as this happened around midday Friday, the USD began to plunge against the yen, and the yen jumped from 159.2 yen to the USD to 155.7 by Friday evening (hourly chart via Investing.com):

On Wednesday, Bessent had blamed the surging long-term US Treasury yields on the bond-market meltdown in Japan, during which the 30-year Japanese Government Bond yield spiked by 42 basis points in two days and drove it to 3.91%, the highest since the 30-year bond was introduced in 1999. The crucial 10-year JGB yield surged by 15 basis points in two days. And the yen re-plunged against the dollar. The trigger had been Prime Minister Sanae Takaichi’s call for increased government spending with simultaneous tax cuts.

The 10-year US Treasury yield had surged to 4.30% on Wednesday morning, up by 17 basis points in a week, even as the Trump administration is trying to get mortgage rates to come down. But mortgage rates track the 10-year Treasury yield, with a varying spread. And this surge of the 10-year yield caused mortgage rates to jump back to 6.20%, from 6.01% a few days earlier, according to the daily measure of 30-year fixed mortgage rates by Mortgage News Daily. And Bessent blamed that on the bond market meltdown in Japan.

“It’s very difficult to disaggregate the market reaction from what’s going on endogenously in Japan,” Bessent told Fox News at the time. And he said that he’d gotten in touch with Japanese officials, and said that he is “sure that they will begin saying the things that will calm the market down.”

With this two-step three-day jawboning — first on Wednesday when Bessent said he “got in touch” with Japanese authorities, and then on Friday, with the “rate check” — the 10-year yield dropped from 4.30% to 4.23% (hourly chart via Investing.com).

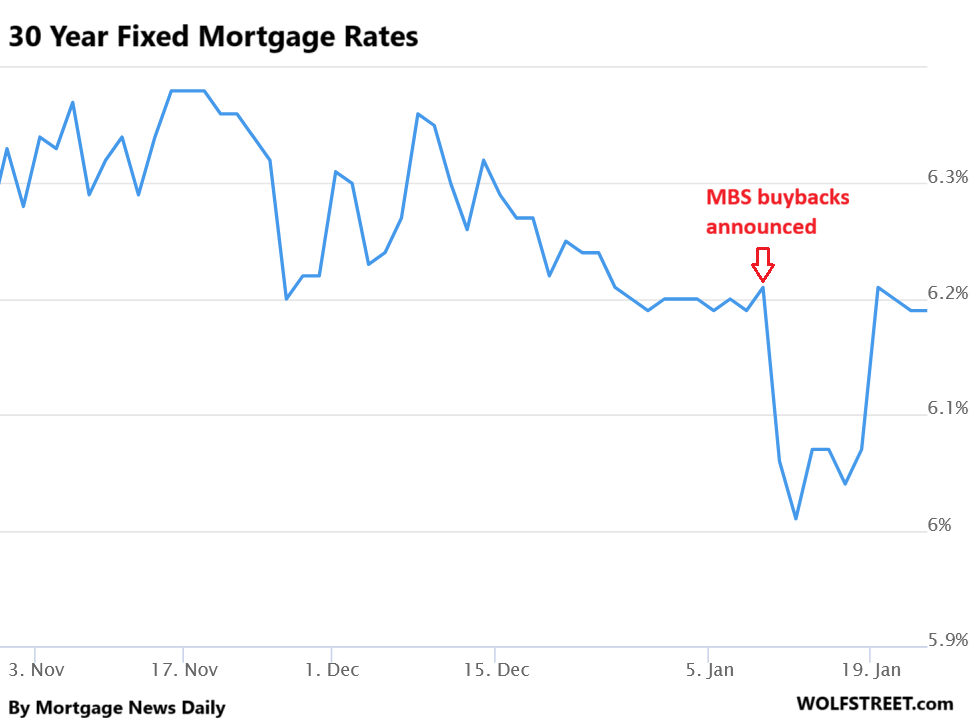

To help push mortgage rates down, the Government Sponsored Enterprises Fannie Mae and Freddie Mac started buying back some of the MBS they’d issued. This started in 2025. But on January 8, this was moved to the front pages when Trump directed Fannie and Freddie to buy back $200 billion in MBS, about the maximum they can buy back under current legal limitations.

But they don’t have the available cash to do that, they only have enough available cash to buy some MBS. They could also issue bonds and then use the cash proceeds to buy those MBS, but that would put further pressure on the bond market. So whatever.

This announcement was a masterful if temporary stroke of jawboning down mortgage rates, which plunged by 20 basis points combined on Friday January 9 and Monday January 12.

It didn’t last long, however. By Wednesday January 20, mortgage rates where right back where they’d been on January 8. They’d just done a big U (daily chart via Mortgage News Daily).

Obviously, Bessent wouldn’t blame the surging long-term Treasury yields on the ballooning US deficit and the flood of new supply of bonds coming on the market that investors will have to absorb, and he wouldn’t blame it on inflation that accelerated further and that worries the bond market. Jawboning is a lot easier to do than to address those issues.

The bond market might not be happy for long with this jawboning. Inflation is a big issue for bond investors as bonds lose purchasing power due to inflation, and yield is supposed to compensate for the loss of this purchasing power, plus some. But long-term yields are too low to compensate investors for hotter inflation in the future.

And inflation keeps moving further away from the Fed’s target, amid government policies of prodigious deficit spending and Trump’s pressure on the Fed to cut short-term interest rates. They want to run the economy “hot,” meaning higher growth and more inflation, which provides fertile ground for inflation to bloom. Given this scenario, the bond market is still very sanguine, surprisingly sanguine, despite the recent ripples.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Still waiting to buy any bond beyond 2 years. I suspect there will be a bear market in bonds for quite a while, no sign of serious deficit reduction. When the administration wants to run the country hot, one doesn’t want to buy bonds.

I was around in the late 1970s in a professional role, it got very ugly for bonds there at the end until Volcker, Reagan and the populace got serious about curtailing Inflation.

If you really want a safe long term bet, it looks like despite all safe deposit box costs and insurance, physical Gold outshine all fiat based government bonds.

Gold plunged by 50% over a span of 3 years starting in late 2011. In its history, gold had huge surges and plunges = risk.

Yep,but to stackers holding for the long run feel tis a good asset to have in the basket along with silver,in hand of course.

I have done very well in that regards recently after holding for years but see no need for fiat at moment.That said,you have a big expense that needs being taken care of feel soon perhaps sell and take some profit.

Gold and silver are both screaming higher every week, and traders will put their money where it gets the best treatment. The Gold and silver ETFs (GLD, SLV) are seeing absolutely enormous call option volume week after week, as they continue to climb relentlessly with no sign that they are topping out, so they are apparently not concerned at all with risk (yet.) GLD went from $421 to $458 last week in 4 trading days, a $445 call option was –get this– a 130 bagger (!!!) So they just keep pumping it in with the call options, and will continue to do so until the metals fever breaks. Then, lookout below.

I’ve sold 30% of my total silver holdings recently. It will be 40% by tomorrow if my limit order makes it through.

When I got my bachelor’s in economics from a no-name university in California… banking and interest were the most confusing topics by far. Not sure the professors even understood them. Test scores of us students showed that *we* certainly didn’t.

Didn’t get clarity on these topics until I got a sales job working for billionaire-founder J. Paul Reddam of Ditech Mortgage fame: he said simply that US consumers get their best deal on house prices when interest rates are high. After purchasing at high mortgage rates, however, first-time home buyers should pray for lower rates and refinance ASAP when it makes sense.

The other people in the room nodding to in agreement to Dr. Reddam’s proclamation were his executive directors, many of whom were soon indicted by the FBI for extortion, so take that above advice as you will.

Muff Marauder, that’s a good strategy. As good as “buy low, sell high” and equally easy to implement.

Please make sure you understand that tax implications of holding gold. It is not treated the same as securities.

Volcker never learned a lesson. He injected too many legal reserves again in 1983.

He solved the problem….

Bernanke Yellen and Powell kicked the problem.

LOL! Let me guess, another idiot that thinks regulation is bad. You want to see a truly unregulated, capitalist market? Move to Afghanistan.

Volcker had the balls to do what was require to save the FRN. All that followed have essentially committed treason and violated the Fed’s contract with CONgress. Unfortunately, congress is also complicit and fully owned by the corporations.

Interesting times.

Bear market?

lol.

The bear market for bonds was 2022

The 60/40 did excellent in 2025, almost as good as the S&P

This reminds me of my comment on bull/ bear from the other day.

A “secular” bull or bear market would be a lasting trend, generally considered 5 years to decades.

For example the US stock market has been in a secular bull market since the GFC recovery (post the lost dot-com decade: possibly a “secular bear market”).

The COVID crash could be considered an entry into bear market territory, but in any long term view: a 1-month pullback is NOT a trend.

The performance of the treasury bond market is a perfect example of: not everything goes to heck in a straight line.

I think the 10-year will yield 6%, before it yields 2%.

Excellent article that focuses on what your paragraph proclaims:

“The New York Fed, at the request of the Treasury Department and acting as fiscal agent for the Treasury Department, asked its primary dealers what exchange rate they would get if the NY Fed started buying yen through them. This “rate check” was a signal that the US government is ready to intervene in the currency market to support the yen against the USD ”

The currency has been trashed by that nitwit president that America elected

Difficult environment for me as an investor approaching retirement. Will Gold go to $10,000 ounce and S&P 500 go to 8000? Will any type of bond return be a real risk with inflation but having short term investments not outpacing inflation. Does international investment make sense given exchange rate risk and so on. The answer as usual is diversification but feels like even the simple guidelines are blowing up. The challenge I think is we are at a pivotal time in the world where much of the assumptions we might make today will be very different in perhaps as short as 10 to 20 years. That said, humans are super terrible about predicting the future, but not even sure history can be a guide anymore.

I suppose on some level might have to be happy to not lose money relative to inflation but be happy with break even. OpenAI, for example, has moved into what it said it would only do in desperation, sell ads. They even lose money with that unless the cost of processing words comes way down. OpenAI collapsing of course doesn’t mean the end of AI but it would send a strong signal.

I hear you, totally in the same boat, about 12 months from retirement.

If you are about to retire, take bill Bernsteins advice and be safe.

Firstly, you are unlikely to be at least half as vigorous as you are now in ten years.

OpenAI ads is the realization of profit, not the whispers of doom imho

The music stops when people start looking at the training data sourcing, the impact of systemic opinion suppression on that good ole non-biased target we all agreed was pretty useful, and we scratch our heads and start wondering if we’ve made a research and processing tool or shiny new “toys for boys”…

I am afraid that AI, a flawed facsimile of creativity is nothing but a forgery IMO. I could be wrong. I am only referring to the mathematics of it without prejudice;

As always, there are intelligent ways to do things and stupid ways to do things. The fact is that America has been rewarding bad behavior, at all levels of society, for 50+ years. The response to the great financial fraud of 2008 should have made that clear to everyone. I mean look at the way this administration is behaving. As a result, the rest of the planet is voting with their wallets and repricing risk and trust. Not sue about $10,000, but $8,000 is a lock. Moreover, unless there is going to be a massive drop in the world population, then there will continue to be plenty of demand for energy and commodities. Buy well run utilities and well run miners. Many of these companies have been abused by the financiers for decades.

I think ( agree with your apparent premise that Americas wealth has been squandered by the politicians at the behest of the merchant class which Adam Smith specifically warned the voting public to never elect the merchant class to make policy. They might not value the status quo as emotionally as the general public including their own mother is the inference.

God bless America

Not even our Jizz Coins and monkey pictures are safe anymore! What is going on!?

Not even negative nominal interest rates will extricate the government’s largess from the present morass of a cumulative debt > 33 trillion dollars.

I think that we have been living in a world of negative interest rates since the criminal bank bailout, the advent of Bernanke’s QE

A world in which skyrocketing asset prices are not considered inflation.

I have an alternative hypothesis based on the consideration that asset price inflation is the primitive source.

What we measure is a derivative of the discounted cash flow cost of ownership of the asset

President Richard Nixon’s move of devaluing the dollar would work great to raise the value of the yen. Then follow that with Nixon’s famous wage and price controls. Federal Reserve Chairman Burns, I mean Powell, should know how to do this.

Nixon was similar to Trump in that inflation was the least of his worries

He figured he would be long gone when the corruption was manifest in America’s philosophical defeat

I suppose Bessent has dislocated his jaw to be able to open his mouth so wide… Stormy Daniels might be impressed.

I’m sure Mr. Bessent’s husband, John Freeman might be impressed.

Both replies Epic!

The problem is debt and inflation. No one in Goverment is willing to admit what the problem is.

Even recession will increase spending and make the issue worse.

All the chatter about hard assets and our strong economy is just that. It is a big world and we will no longer control the price of anything.

Open trade was the best thing that ever happened for the average person! While we play silly games, the world will finds ways to prosper without us.

Incorrect, Open trade was a raw deal for the “average person” It was a boon for capital owners as you could arbitrage low wages in part of the world against prices in another. Free trade hollowed out the jobs that “average people” had- generally paid well and provided benefits.

I surmise that you meant to say that the free trade paradigm has been determined to be fraudulent, Free trade, hardly, humbug

I wonder if the US treasury buyback for liquidity went over the plan 2B on Friday by full magnitude(factor of 10). You think we will find out? The exact amount?

10x I am guessing it took 20b to push down the yield on Friday with the US dollar being down ,9% on that day.

Wolf FYI~ 22b, last Friday, 11x plan

https://treasurydirect.gov/instit/annceresult/press/preanre/2026/BBR_20260122184000.pdf

8b Thursday 2X plan

https://treasurydirect.gov/instit/annceresult/press/preanre/2026/BBR_20260121184000.pdf

You’re looking at the wrong line 🤣🎉🎇

You’re looking at “Total Par Amount Offered” — that’s the amounts that primary dealers offered to sell to the Treasury Department.

You need to look at the line below, “Total Par Amount Accepted” which is the amount that the Treasury actually bought back.

In the auctions you linked, the amounts it bought back were $2 billion and $2.8 billion respectively.

Also note the prices it paid: $2 billion at 63.3 and 83.3 cents on the dollar. And $2.8 billion at 93.7 to 101.3 cents on the dollar. These are market values. The bonds with a haircut are those whose yields are lower than today’s yields. The bonds with a premium are those whose yields are higher than today.

When I reported on it under Biden, there was a week of $8 billion accepted. I don’t look at them every week because the amounts are minuscule and don’t matter, so there could be have been bigger weeks than $8 billion.

You are right. I looked at the wrong line I was going to ask you not to post, but the bid to cover was 11x on the 2b and that is a record reverse bid to cover, that should get peoples attention. I am curious what the bid to cover will be on the next 10 year auctions. That’s a bad sign for such a high ratio of people offering to sell vs buyers. At least in my mind that’s something to pay attention too going forward.

If I recall correctly, the Fed has a huge amount of notes and bonds coming due in 2026, something like $9T+. Since US deficit spending is unlikely to be curtailed, most, if not all, of the maturing debt will be financed by new issuance. This figure is just for existing debt and does not include new debt that must be financed.

At what point will supply outstrip demand? And what about the political damage being done, how many of our former allies start selling their UST holdings and start boycotting treasury auctions? Given this backdrop, it’s hard to believe that rates beyond the 2-year will be heading lower. Best guess the 10-yr UST will be priced to yield between 5% to 5.25% by the end of 2026.

I doubt there will be immediate selling on the part of foreign governments and especially pension or sovereign wealth funds as they would show up as a very embarrassing immediate loss. Much preferable for them to hold until maturity even with low yield bonds as then there is no loss to report.

Then buy anything other than long yield treasuries. This is going to be a long term problem, slowly until it goes fast. Perhaps 10 or 20 or even 30 years in the future, but does anyone here expect the USD to escape intact until the year 2100? Gold will still be around, but will the US be around?

Your thoughts?

Under normal circumstances I would agree with you. However, these are not normal circumstances when the US invades sovereign nations at will while threatening other allies with tariffs and other punitive measures. I would rather take a 15% or 20% hit now versus having an unstable president order the Dept of Treasury to block large foreign accounts from repatriating their money. Not only that, but USD for now is declining in value, meaning that there could be greater currency losses upon conversion from USD back to the account’s native currency. Why gamble when the potential negatives are far worse than acting now?

There is another theory of thought that global governments are all printing. This actually increases the money supply. This money has to find a place…anyplace.

Thus sure, lots of assets will go up in price but bonds yields may go down. Look at MMF charts. Yields have been dropping for 6 months yet MMF are still seeing an increase of assets.

The thought is all this excess liquidity will smother yields. Think about it. Do I want to put my money in stocks that have PEs of 30 to 50 or 80 and P/S of 20 or 30. Do I want to buy a stock today at a price that is reflecting its next 10 or 20 years of revenue growth and hope it grows for the next 10 to 20 years. Because if it does not…then it could drop 30% or 50%. Or do I want to play it safe with a MMF at 3% or 4%.

That AI only has part of the truth.

Look at the experience of Turkey. Argentina. Zimbabwe.

There is a point beyond which excess money supply triggers a collapse of trust in the currency, resulting in excess inflation and higher interest rates.

Well 5.25 is the minimum that I would demand for buying any credit instrument.

I keep watching a number of things. E.g. 1) the crosses of the 3 largest traded currencies (EUR, USD and Yen). 2) the US 10 and 3) US 30 year yield. If these yields and the USD “go ballistic” then it’s time to “enter the lifeboats”.

I am curious to see where all the US yields go when the market(s) has/have peaked. I actually still expect US yields to go lower for a (short ? long(er) ?) while.

I assume that the falling USD/Yen is a sign the yen carry trade is “vulnerable” (to put it friendly). For the time being I don’t worry too much.

Would you worry if the yen rate dropped to 140 in the coming months? Or would you feel better if it went to 170? Where do you think it should be without manipulation?

Unfortunately, 165 yen per dollar resistance is a very nearby line in the sand that the BOJ and the Fed are trying to avoid breaking.

From Gemini AI:

Takeshi Fujimaki, a former JPMorgan star trader and Japanese opposition lawmaker, has for over a decade consistently predicted a major devaluation of the Japanese yen (potentially to 180–200+ per dollar).

The specific mention of a “free fall” to a figure over 200 has gained traction in recent presentations and macro reports during the January 2026 World Economic Forum (Davos) and recent investor summits.

Something has to give. That looks like long-standing carry trade. If the Caymans based carry trade begins to unspool in a less than controlled manner, IMHO bonds likely to rocket higher and dollar potentially plummet. This is magnified by potential for other countries to begin treating US like 21st century pariah state.

Do you mean bond prices or bond yields will rocket higher?

Bondholders have little leverage here. They have nowhere to go. Other assets such as stocks and RE are probably even more overvalued, and if bondholders do revolt, the Fed can probably QE or twist them again with full support of Wall Street.

1. You’re still pursuing your favorite hobby here of QE mongering. Are you never going to give up? You’ve been doing it for so long.

2. Bonds mature constantly. SOME current bond holders can decide to sit out some of the auctions, and SOME new investors might demand higher yields and wait for those, and that would be enough reluctance on the margins to push up yields. Treasury securities are not a fixed sum, but a constantly growing sum that constantly gets rolled over.

3. Putting cash on hold still pays over 3.5%. There are plenty of safe short-term options if you want to wait for yields to rise.

Wolf, you are smart and open-minded, but when somebody suggests the Fed might do QE again for some reason you fly off the handle.

We’re talking about a Fed that pushed a QE cycle for a decade, repressed rates to zero for six years straight, continued to buy MBS after RE rose 50-100%, let inflation hit 9%, ended QT early, just recently came up with a new idea to justify more balance sheet expansion, and is pursuing ST rate reductions while inflation has been way over target the last five years.

I’m just trying to be realistic. I hate QE and think it’s a disastrous idea, but relying on the Fed to exercise good judgement and restraint is not prudent, given the history.

With your incessant QE mongering, YOU are eagerly spreading market manipulation BS on my site. That’s how that shit works. People like you do this across the internet to serve their own interests. Do that BS market manipulation somewhere else.

You can get plane ticket to Ireland or many countries open a bank account and transfer money, buy a home abroad, etc it’s all normal and acceptable to diversify pay taxes here in the USA from returns overseas. Bitcoin is down 3% today when futures open it may be deep red. limit down day tomorrow morning? Will find out shortly. Selling will pickup as the night goes on. The world is paying attention to our affairs, a Vote of no confidence is coming!!!

Yen open 2.3%higher, US dollar is getting crushed at opening of the FX markets. Euro is up .86%. Get ready for the equity futures. Let’s go Broncos!! Let’s go Seahawks!

Sorry, FXstreet and .Yahoo posted the wrong %, for some reason maybe they were comparing tonight to Thursday instead of Friday currency values. Bloomberg has the yen up .62% and euro up .54%. Made big difference with opening futures :) $gold is up over 5k milestone price. sorry for posting so much I am taking break for few days but will be reading content. cheers.

I sold off my bitkorn. Reported this to the IRS, Form 8949 and Schedule D (along with various other forms and schedules). I still do my own taxes—on paper—since I enjoy doing paper dumps on the IRS.

If the Fed resumes QE, watch the bond market REALLY revolt.

Waiting for US debt to top 40 trillion. Probably before the end of the calendar year. 45 trillion plus in Jan 2029 as Trump’s term ends.

Hard Assets – what all does that include? Recent article posturing that US small businesses are doing great, but I disagree. I help insure many Midwest small businesses and their reported assets or those available to use as collateral are leveraged at least X2 just to meet operating budgets and payroll. US small businesses are in the black but only on paper and if they start missing loan payments; well good luck to the banks on figuring out who’s in first position to collect because their underwriting standards are less than credible.

That’s how small business has always been. Nothing new. Try starting a restaurant. Something like 90% of restaurants shut down within 5 years after being started. Nothing to do with economic times. That has always been that way. Small business is not for the faint of heart. It can be great and fulfilling, but it has always been fraught with existential risks, revenues are precarious and hard to come by and can vanish in a moment, and getting capital has always been very tough, through most of history a lot tougher than now, and the cost of capital is very high. That has always been that way. If you cannot handle those risks, don’t start a small business. Get a job.

You are correct. About 50% of new businesses fail within 5 years. Except restaurants of which it’s 50% in 1 year and 90% in 5.

I am told our Golf Course in NW Florida needs money. Perhaps it is a good investment. Better than tokenized assets.

Bond markets can get very ugly.

The buyer of Japanese govt. bonds at the Low of the cycle faces big price declines today. The 10 year down to the low 70s the 30 year in the low 40s

and yes there ar 40 year bonds. Price today in the 30s.

Not pretty for the owners of those bonds.

3 thoughts:

1) Japan is having their own Liz Truss moment due to rising inflation and perceived fiscal irresponsibility. Meanwhile, the US is acting as if it is immune to bond market seizures. It’s interesting to see the US trying to talk down the currency and yields of a nation as big and indebted as Japan, as if we believe we have that much fiscal power. We will see about that, or perhaps we already did: The results of Bessent’s experiment suggest that the best the US can do is create a very brief fluctuation in yields and exchange rates, at its own expense. The USD and treasury holders paid the price for this effort, and it yielded little to nothing that will endure. Perhaps instead of trying to prop up its currency with political interventions, the US should consider why such maneuvers should even be necessary? Why don’t we trust the free market to set the proper prices for debts and currencies? Is it because we know we’re not doing the right things with monetary or fiscal policy? Whatever the cause, I think we can expect the interventions to soon expand from political rhetoric to the spending of very large sums on currency defense. It is the endgame of this sorry saga, but we will eventually learn that it is impossible to defend a structurally weak currency for more than short periods of time.

2) What is the motive for US policy to keep yen-denominated bond yields low and to keep the yen from rising against the dollar? Is it fear that rising rates in Japan might transfer to US treasuries? Or is it fear that the combination of a falling USD and rising Japanese yields could lead to an exodus from US treasuries? Japan seems an unlikely destination for the money fleeing US treasuries, because most of the reasons to flee US treasuries exist there too (high debt/GDP, rising deficits, long-term future is murky). I also wonder how China plays a role in this? How much wealth could China suck out of US/Japanese markets if one day they suddenly floated their currency and dropped currency controls?

3) Conservatives have a tendency to blame scapegoats who are foreign or different (and, yes, liberals scapegoat the rich). Bessent’s use of the Japanese to explain why people in the US can’t have low mortgage rates might reflect more than rhetorical thinking. It might be a product of a groupthink environment where it is unspeakable to think of the true underlying causes, like cutting rates into a rising inflationary trend or suddenly expanding deficits with a tax cut bill. If that’s the case, US policymakers are oblivious to the actual influences, and are focused on the wrong things, like Japan. This insight might not matter much today, but when a crisis hits it will be worth keeping in mind as we try to predict the next moves. E.g. if slowing economic growth is met with calls for ever-higher tariffs or currency controls, because it’s the fault of foreigners, then Scott Bessent might as well be the reincarnated ghost of Andrew Mellon.

“2) What is the motive for US policy to keep … the yen from rising against the dollar?”

You got this question backwards. It should read:

“What is the motive for US policy to keep … the yen from plunging further against the dollar.”

The yen had plunged against the dollar, and then the US intervened with the rate check, to end the plunge of the yen and to cause the yen to rise against the dollar.

The motive for the “rate check” is potentially the yen carry trade. It is basically free money for US investors, who get a “free” credit in Japan and pay it back with even less USD. It accounts for over $1 trillion in US liquiditiy (according to Google). The credit only works with a positive rate spread UST vs. JGB and if the JPY is stable or falls. If the JPY and/or the JGB rate rise too high too fast (compared to the USD and UST rates), the whole thing collapses, because investors can no longer borrow for free.

Japan is facing high inflation, high debt and a serious devaluation of their currency. They are a small step ahead of the “crowd” (US, EU, China), instead of going alongside. My guess is that the US must support the carry trade, because an end to this free money (liquidity) for US investors would mean a collapse of US assets (shares, bonds). Japan is the single largest holder of US bonds. If the Japanese govt. wants to support the JPY and thereby tame inflation, they have to sell UST (!) in order to buy JPY. If they overdo it, the JPY goes too high and kills the carry trade. And the economy. If they don’t buy enough JPY, the JPY falls further, (imported) inflation will rise and also kill the Japanese economy. Tricky situation. Japan cannot reduce inflation by raising the interest rate – because even higher interest payments would make everything worse. Best would be to keep USD/JPY and the JGB rate stable, but the market wants Japan to pay for their formerly free lunches.

Summary: the Japanese and US government chose to support the JPY just enough (“rate check”, i.e. a friendly invitation to buy JPY) without killing the carry trade. The carry trade ends if the JPY rises too hard too fast. Then, some US investors may be panicking and the liquidity fiesta in Japan may be over. Right now it is only dying slowly, but nobody wants to leave just yet. Which is actually a good thing. That’s my take on this story.

All central banks want to keep the party going – but have to do it simultaneously (stable FX, corresponding rates, etc.). It will lead to higher debt, rising long-term interest rates, higher inflation. This is happening now in Japan, just earlier than in other countries. Bad luck. A positive scenario would be unexpected global economic growth and stable national debts.

Just kidding. :o]

We may be seeing the party die in real time: BTC, bonds and stock markets have lost in real terms over the last couple of months, whereas some precious metals have doubled in value. Fresh money is already going to the next party. I asked both Gemini and ChatGPT – same answer: financial repression (inflation) is eventually the base scenario. Gold and only a few stocks (e.g. energy, mining) may secure your wealth. But who knows? The BRICS chose to buy gold – according to rumors for their new currency.

Disclaimer: I am 75% invested in gold, silver and mining stocks. I just love your leader’s creativity. Every new idea makes me richer. For now…

Cheers from Europe

Andy,

You offer a very good explanation.

An end to the carry trade due to high rates in Japan OR expectations for the yen to fall could reduce demand for US treasuries, leading to a rate spiral in the US.

Then if Japan sells US treasuries to stabilize the yen, that adds even more treasuries to an already soaked market, further raising US rates.

Can it last? Well, to some extent the carry trade has already lasted for decades. But that was before the US’s indebtedness deteriorated to the point of some worst-case-scenarios from 20-30 years ago. It was also before Japan finally defeated deflation and became a more normal economy.

As Wolf’s charts show, if the US pushes down on the yen it now sinks its own dollar. Maybe that wasn’t the case decades ago, when the US debt/GDP ratio was only 70%.

So perhaps Bessent’s experiment revealed that the US would have few good options to arrest a collapse in the yen and an unwinding of the carry trade. If the US government buys yen, it will only sink the US dollar and make a temporary blip in rates. If the US government jawbones about it, as Bessent did, it still sinks the USD and makes only a temporary blip in rates!

Given that neither government is interested in pivoting to fiscal moderation, I suspect we can see more episodes like this. Perhaps the lesson Bessent took away from the U turn in rates is that actual yen-buying would be necessary to create a sustained change in the trend of investors dumping the yen. That could be the next step, but what will he conclude when yen-buying is followed by investors dumping the USD?

Our leader may be creative, but I suspect some of the demand for precious metals may be due to a worldwide trend toward such creative leaders. In Europe, such parties are perhaps one election away from demolishing the political middle, as happened in the US with help from Russia.

“as happened in the US with help from Russia.”

LOL! You were doing well until the propaganda line.

The underlying problem is unsustainable government debt. Supporting the Yen and artificially pushing down long duration JGB yields is only a temporary solution, at best.

Gee, it’s almost like maybe Congress and the President should work together to reduce spending and therefore deficits or 10 year bond yields will rise. Who would have thunk it?

Reducing spending is extremely unpopular. Every one of those dollars ends up in someone’s wallet. Government spending is basically vote buying, and no one wants to lose.

i.e. we voters are too dumb to resist it.

If only the ones who oppose spending cuts couldn’t complain about inflation, because my guess is they’re mostly the same people. 99% of voters are voting for more inflation by voting for the deficit spending Republicans and Democrats. Its wanting to have your cake and eat it too.

So Japan started all this ZIRP and sopping up their own debt game back about 2000.

People said it was nuts and would collapse eventually.

And here we are…..DEFENDING their idiocies

And who are we to take on the fiscal troubles of another country, which is what this is.

See my dialogue with Andy above.

There seems to be a terror of contagion to the US market. It’s a well-founded fear because the US is in such a weak fiscal position.

We chose this path, where we are thinking about bailing out Japan’s currency to keep treasury buyers buying.

I find it strange that the futures bond market is wagging the cash bond market in Japan.

The actual holdings of Japanese government bonds is pretty much locked up with the BOJ, Japanese Banks, Japanese pension funds. Japanese life insurance companies holding about 90% of bonds issued.

Foreign holdings of Japanese government debt is around 6 to 7 % of outstanding issuance.

So the only place to really trade these instruments is in the various futures exchanges where some settle for cash (Singapore) and others for the underlying bonds.

And the total penalities for failure to deliver can be huge.

It’s not that simple. Interest rates are linked via spreads.

All the interest rates on all other yen-denominated debt are linked to the Japanese government bonds, and vice versa.

Furthermore, the banks lending to the Japanese government borrowed that money from other customers, who might choose to withdraw.

That credit market in Japan is much larger than just Japanese government bonds. It includes the infamous Yen Carry Trade: borrow in yen at low rates, invest overseas, and get a further bonus from yen devaluation vs. other currencies. Yen Carry worked for a while and got too popular. When it unwinds things get complicated.

The US government could yet again get partially shut down this week if the Senate refuses to pass the spending bills by January 31, 2026.

Perhaps call off the dogs?

FED can step in as a last resort if demand are lackluster for US bonds! BOJ started the printing press long before the FED. BOJ now owning the largest share of JGB without any doomsday hyperinflation sweeping through the country. So, the music will continue.

What both countries have now that they didn’t have back then is INFLATION. Doing QE in an inflationary environment is asking for inflation to explode, like it did in 2021, it went to 9% in no time. So QE is essentially off the table, except to avert a government default — and both countries are far from that.

Didn’t you hear? “There is no inflation.”

You are correct, Wolf. It is / will be money printing to service debt.

But if QE pushes up on inflation, continuing to finance massive deficits like this pushes up on yields. It’s money printing either way.

Persistent inflation (and expectations) will eventually push up long term yields regardless of the jawboning or “operation twist” efforts. At some point the substance of a market outweighs the rhetoric, and countries can no longer bear the cost of direct currency manipulation games.

And inflation/devaluation is fine because the US dollar needs to lose about another 50% of its purchasing power to get the US back on a sustainable debt path. Efforts to prevent the slow decline of the dollar are more likely to create more acute instabilities. E.g. borrowing USD to buy yen will raise the US debt and raise US interest rates, imposing a cost in terms of dollars and stability.

This constant QE mongering is just nonsense. Moderate amounts of inflation (3-5%) and strong economic growth dimmish the burden of the debt. That’s how they’re doing it. That has already happened in Japan. Its debt-to-GDP ratio went from 258% in 2020 to 232% in 2025. Same process now going on in the US.

There isn’t going to be any QE. There is going to be moderate inflation (3-5%) and strong economic growth (“let it run hot”).

Surging yields? They go up they go down, but aren’t we down from a year ago and historically low (apart from the 1% free for all days)?

Is all this really a pressure cooker getting hotter, or are we right now slightly less getting better than we experienced since the way back days of September 2025?

If we did remove the Japan bond troubles – idk this doesn’t feel like the doom and gloom end times to me …

10 year rates yields trending down, overall market is up, gold also climbing…

We sure we got the causes pegged here appropriately?

“10 year rates yields trending down”

Bullshitter

Some of the patterns I see in the comments section get their own little names in my head. It’s evolving into a kind of argot.

I call this one “chartbombing”.

Pull a 100 year 10 year chart and ask yourself what’s the most common rate across America’s most successful growth period… here’s a quote

“the long-term average frequently cited around 4.25% or higher, reflecting a wide range of economic conditions over the past 100 years”

What are yall talking about? 4.25 is the gold standard of ten year rates.

Get your head out of the artificial easy money period post the Great Recession – you taught me that.

You can build a middle class on 4 and a quarter

Agreed, almost. Except that figure of 4.25% is too low because it includes the period of QE when the 10-year was artificially suppressed to as low as 0.5%. That period of 2009-2022 (the QE period) needs to be removed from the long-term average.

A better measure is inflation. The 10-year needs to be 2-3 percentage points above the rate of inflation. The economy works fine under those conditions.

And I think we’re there, unless we’re sending everyone home and shoveling out another $9tn

We shall see, but past evidence suggests good old American deficit spending doesn’t spike inflation (a lack of people producing while getting cash payments, on the other hand, very much does – especially when done worldwide).

Frankly, my BS detector is catching whiffs of a Neocon rebellion (not to be political)… nothing more. And that started with 986 and the GILTI tax, not 2025 Trump shenanigans.

Think about it!

Also thanks for chatting love your work. We can disagree and respect – much respect!!!!

Ahhh so glad that these fed lawsuits and pressure have brought down U.S. borrowing costs… oh wait!… awkward

Jawboning is the government’s favorite move trying to talk the market into behaving. By controlling the narrative, officials can nudge the economy in the right direction, dodge political blame, and keep investors calm when things get dodgy.

Thanks for this update, illuminating.

I’m no pro at this, but I’d guess that even international jawboning wouldn’t be enough if the PM has her way with the snap elections. Still, I for one like that Trump’s goal of lowering the 10-year rate aligns with strengthening the dollar against the yen. Another lever to pull.

Bessent is a good guy. One of the best in the administration. He wrote the op-ed in the WSJ calling out the wealth effect. Unfortunately, Trump is too much of a lover of debt. He thinks debt is good. That is how he ran his businesses. Bessent has to deal with his boss.

Many of us do not share that opinion at all regarding Bessent who has shown himself to be very stupid and clueless.

Let’s see, last Treasury Secretary under Biden was brilliant ( Janet Yellen )! Speaking of clueless and stupid. Another TDS post from SoCal ( go purchase some gold ). LOL

Good guy my ass. This guy wants to protect those poor people with 15 rental houses rather than allow affordable housing for first time buyers.

DXY 9:15 today

96.99

-0.61 -0.63%

Right, wait until the rate decision, and look at the weekly chart (after the weekly close).

I suspect that this may have put in THE bottom of the year-long “bottoming” of the DXY.

I wouldn’t be surprised to see a weekly green candle, and a DXY that doesn’t revisit a 90-something handle for… a while. Also: the 160 Yen:USD level is deemed a “breaking point,” and the point of this whole exercise/ article.

Of course, financial markets are highly volatile and manipulated. It’s not usually a geopolitical preference that drives large money flows, but rather a decision regarding profits and safety.

MW: Michael Burry flags risks from Japanese yen to U.S. stocks as ‘rate check’ stirs debate

MAJOR reset in asset valuation is desperately needed to finally tame inflation below 2%. Overvaluation in asset prices and loose fiscal policies (deficit overspending) causes more inflationary spending both in consumer and government budgets. From bitcoin, gold, houses, stocks, cars and everything else, there needs to be a pricing adjustment led by a Federal Reserve that values price stability over inflationary grease to keep overvaluation from continuing, even if that means a mild recession or zero growth for industry to catch up to consumer and government demand in spending.

“There isn’t going to be any QE. There is going to be moderate inflation (3-5%) and strong economic growth (“let it run hot”)”

“A better measure is inflation. The 10-year needs to be 2-3 percentage points above the rate of inflation. The economy works fine under those conditions.”

So the 10 year needs to be 5 to 6 or 7 to 8 ?

“ It would crush housing, hit stocks, strain government finances, and likely force a major policy response.”

“It would … strain government finances, and likely force a major policy response.”

It would NOT strain government finances any more than they already are — that’s an ignorant or manipulative BS statement — because not many long-term bonds roll over every month, so the higher long-term rates don’t make it noticeably into interest expense until years after inflation took down the purchasing power of those bonds that are redeemed.

Short-term rates make it into interest expense very quickly. But that’s not what your statement is talking about; it’s talking about long-term rates. So total clueless BS.

The ignorant manipulative bullshit being spread by these QE mongers has no end. That’s why I crush or block them here. This has been going here in the comments since late 2021 when QE was being tapered. The flow of BS never stops. The bigger the BS, the bigger the flow.

Great post, taught me some things about the yen rate check that no other media outlets had.

I’ve been hoping you’ll do one on gold (and silver). It’s going up so fast it makes me wonder if they know something we don’t. I see your last post on gold was in July 2025 and attributed it to USD value erosion and central banks buying gold. So it seems you forecasted it very well – GLD has gone up ~50% since!

But is that much really attributable just to dollar value and foreign bank purchasing? Or does it look more like future inflation expectations and/or a speculative bubble (and can we say how much of an influence those are? I guess that’s the million dollar question)

Agree with Wolf, but: Inflation in Japan is different to the US. In Japan, inflation has been imported (lower JPY led to rising exports, higher real GDP but also (real) productivity losses: J-curve effect). Yield curve control (YCC) works because JGB debt is held domestically. Japan has bought some time, but not a solution for the future.

In the US, structural inflation is created domestically (wages, rents, tariffs). The US has been leveraging the debt (govt. spending + AI investments), which is a risky bet, but working so far. The US can sustain the debt in the future, if the AI investments lead to broad productivity growth in all sectors. AI alone will not feed the whole population (unless the wealth is somehow distributed, as Musk suggests).

YCC and USD devaluation do not work in the US, because the US depend on foreign UST buyers – and trust in the USD. A USD debasement would lead to higher long-term rates (UST, mortgages, car loans) and imported inflation. Real growth could become negative.

As long as the USD remains stable and real GDP growth is positive, all good in the US economy. If inflation strangles the middle-class and becomes political, the govt. will cap private interest rates (CC rates, mortgage rates) or send money (e.g. US military).