One thing is clear: a bond market as strung out as Japan’s doesn’t want to hear about spending increases accompanied by tax cuts when inflation is already 3%.

By Wolf Richter for WOLF STREET.

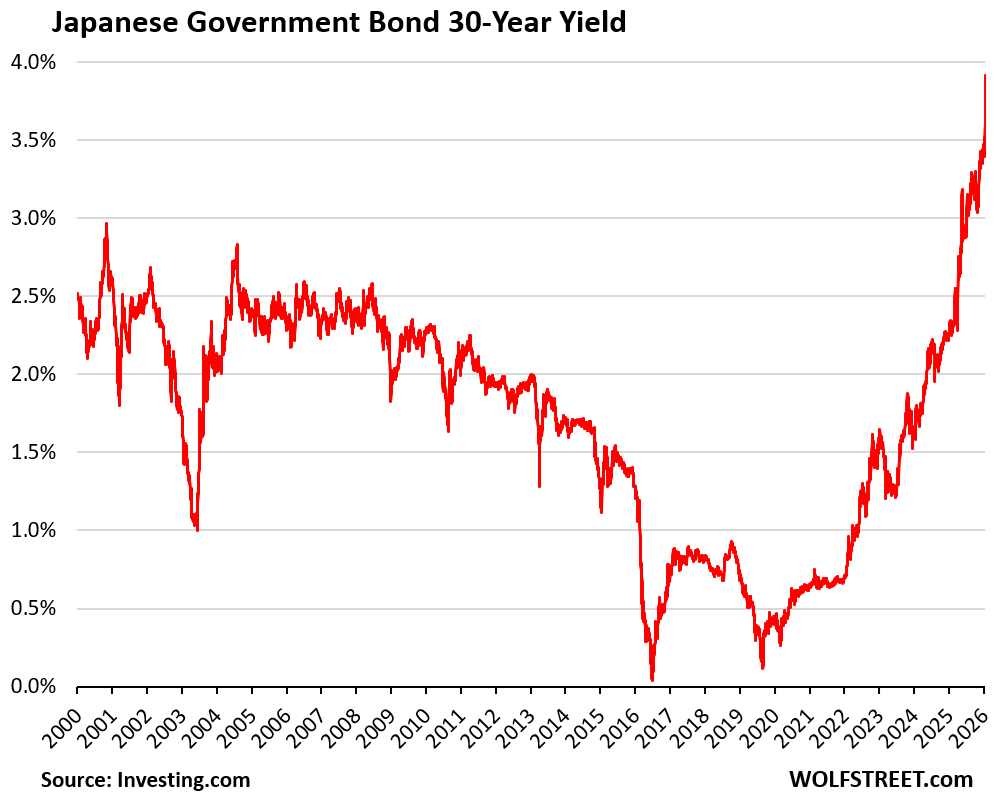

The 30-year yield of Japanese Government Bonds (JGBs) exploded by 30 basis points today and by 42 basis points over the past two days, to 3.91%, the highest since the 30-year bond was introduced in 1999, after Prime Minister Sanae Takaichi called for increased government spending with simultaneous tax cuts by pausing the 8% consumption tax on food purchases. And she announced snap elections — three months after taking office — to get the public support her party needs to push those plans through parliament.

Inflation in Japan has been around 3%. Japan’s debt-to-GDP ratio is the worst in the world, at 256% at the end of the last fiscal year, more than double what it is in the US. Japan’s credit rating by Fitch (‘A’) is five notches below ‘AAA’ while S&P’s rating (‘A+’) and Moody’s rating (‘A1’) are four notches below ‘AAA’ (my cheat sheet of bond credit ratings by rating agency).

And the bond market – what’s left of it since the Bank of Japan still holds more than half of all JGBs outstanding though it is now shedding JGBs – is getting a wee bit nervous.

Maybe the dreaded “bond vigilantes” – big institutional investors that refuse to buy government bonds because risks are too high and yields too low – are rising from their graves? Nah?

But apparently, hedge funds got caught on the wrong foot and were turned into forced sellers, and it was a mess.

Another trigger today was the 20-year JGB auction, which was marred by weak demand, not surprisingly. And in the secondary market, the 20-year yield spiked by 22 basis points today, and by 32 basis points in two days, to 3.48%, the highest since 1996.

The crucial 10-year JGB yield rose by 7 basis points today and by 8 basis points on Monday, to 2.33%, the highest since 1999.

And yet, the 10-year JGB yield is still way below the rate of inflation (around 3.0%), when it should be significantly higher than the rate of inflation. So at those still too-low yields, those JGBs are still extremely unappetizing, and the fact that there are buyers at those yields at all is another sign that the bond vigilantes may still be dead.

Japanese government officials fanned out to calm down the markets, and even Bessent got in touch with Japan’s finance minister to discuss the situation, as Treasury yields in the US were also being roiled. So whatever.

But one thing is clear, a bond market as strung out as Japan’s doesn’t want to hear about spending increases accompanied by tax cuts when inflation is already at 3%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interesting. Also interesting: the real (inflation adjusted) yields have been negative since 2013, though for much of that they were between 0 and -1. They’ve only been drastically negative since 2021.

Still, by some combination of inflation and yield increase they will most likely revert to the 1-3% level they traditionally hold.

I was in Japan a year ago. Prices (at the then exchange rate for the dollar) for very high-end food in the Ginza department store markets were very low. These stores charge the highest prices. I could buy a large sashimi platter for about $12! If the equivalent was even available in the US, it would be closer to $75-$100. A friend of mine in Japan has stopped all international vacation travel because of the unfavorable exchange rates.

The spillover in the US Bond market is rather sharp. Isn’t it also rumors of a Denmark fund and the EU threatening to sell US Bonds?

“The Danish pension fund AkademikerPension, which said it will exit the market by the end of the month, holds only about $100 million of Treasuries. Still, its statement revived concerns about the financial consequences of US antagonism toward allies. Trump over the weekend escalated his pursuit of American control of Greenland, an autonomous part of the Kingdom of Denmark, threatening opponents with tariffs and even hinting at possible military action.”

Just my opinion, but when countries start seizing other countries financial assets, then the ripple effects can become quite deadly. The agreed upon world order is cracked. Repairs need to be made before the cracks worsen.

There may be some people reading this site that could sell more than $100 million in Treasuries. The Treasury market, the most gigantic bond market in the world, doesn’t even notice a portfolio of that size getting unwound.

Isn’t Japan’s 256% debt level a bit illusory? If half is owned by the central bank, hasn’t that half been monetized and extinguished from a practical standpoint? There is no way the central bank will sell that debt back into markets.

1. It’s being re-monetized through QT.

2. Sure, you could say that the debt doesn’t exist because the BOJ holds it, and in terms of interest expense that’s kind of true since the BOJ remits its income back to the government. And that’s exactly the same for the Fed.

https://wolfstreet.com/2026/01/06/bank-of-japans-qt-cuts-502-billion-from-balance-sheet-jgb-yields-surge-as-boj-steps-away-from-bond-market/

Exciting to finally see some solid movement in the last year(ish) on these long rates after such an unreal low rate period.

Hopefully inflation in Japan has now become ingrained and self reinforcing such that only a recession or high interest rates can break it. That should provide the fuel needed to get the 10y above 3% and bring some overdue fireworks to the global markets.

Are the US treasuries held by “Japan” all held by the BOJ or does that include those held by Mrs Watanabi? If not, I wonder what the total holdings of Japanese interests are and at what point might the holdings be unwound in favour of JPY debt?

So will this continue to make the basis trade less desirable? Would that negatively affect equities in the rest of the world? Or do we have a ways to go before that?

What is the interest expense on government bonds to receipts ratio for the Japanese government? Where would it be at 3% blended rate of interest on outstanding securities?

Current blended rate is less than 1% and even that is 24% of revenue. A doubling would take it to 50%. That’s when it gets serious.

I was just talking about the bond vigilantes as a possible scenario (albeit in America) on this site the other day. I don’t think we’re there yet. But this could definitely be an ominous sign of things to come.

US is still one of the cleanest shirts in the dirty laundry. That matters. But it can change quickly with our current leadership antics and actions.

Pretend and extend for the sovereign debt ends soon. No more free lunches!!!. Here in the USA; Bond vigilantes will square off with “My morality is my only check on my power”. Who will lose? Hint… the whole world. How much sovereign debt did the USA purchase from China and Russia? That answer may determine how much future debt the ROW will purchase from USA. Who will win.,..Russia! Shorting JGB was called the widow trade for decades. The times are a changing!