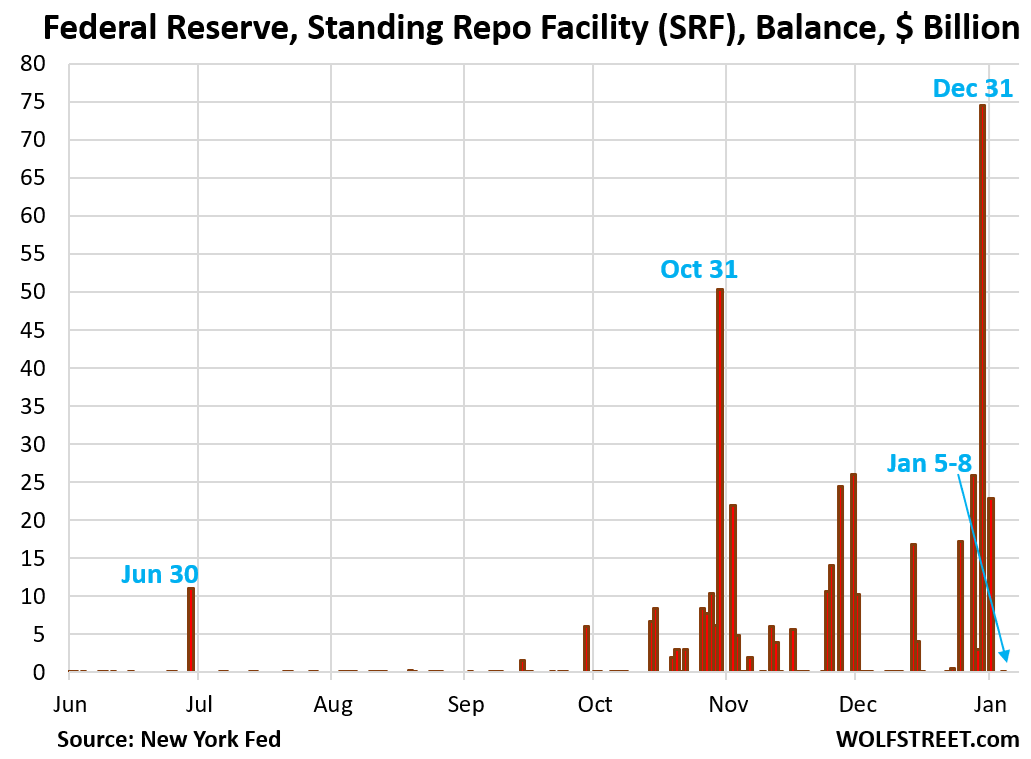

Standing Repo Facility -$75 billion to zero, Reserve Management Purchases +$8 billion: The year-end liquidity shifts have settled down.

By Wolf Richter for WOLF STREET.

Total assets on the Fed’s weekly balance sheet dropped by $67 billion from the prior week to $6.57 trillion as of Wednesday, according to the Fed today. The drop, which was expected, reversed a big part of the $104 billion spike in the prior week when Wednesday, the cut-off for the Fed’s balance sheet, was December 31, the point of maximum year-end liquidity shifts.

That drop of $67 billion was caused by the Standing Repo Facility (SRF), whose balance dropped from $75 billion on December 31 to $23 billion on Friday January 2, and to zero on January 5 and stayed at zero through today.

The SRF is an asset on the Fed’s balance sheet, and that $75 billion uptake on December 31 happened on the day of the Fed’s weekly balance sheet, and so it increased the Fed’s total assets for one day by $75 billion. And that has been completely unwound.

These repos (repurchase agreements) at the SRF unwind the next business day, when the Fed gets its money back and the banks get their collateral back. Then the counter parties can take up new repos for another business day. But there has been no uptake since January 2.

The 43 or so approved counterparties at the SRF, mostly big broker-dealers and banks, can borrow overnight at the SRF via repos at 3.75%. The idea is that these counterparties will keep repo market rates from blowing out during liquidity shifts by lending to the repo market when rates in the repo market exceed the SRF rate and earn a quick profit from the spread.

On December 31, rates in the portion of the repo market that SOFR tracks rose as high as 4.0%, so banks borrowed $75 billion at the SRF for two days (including January 1) and lent to the repo market at higher rates, and profited from the spread. As rates in the repo market dropped below the SRF rate, the spread vanished, and banks unwound the SRF repos.

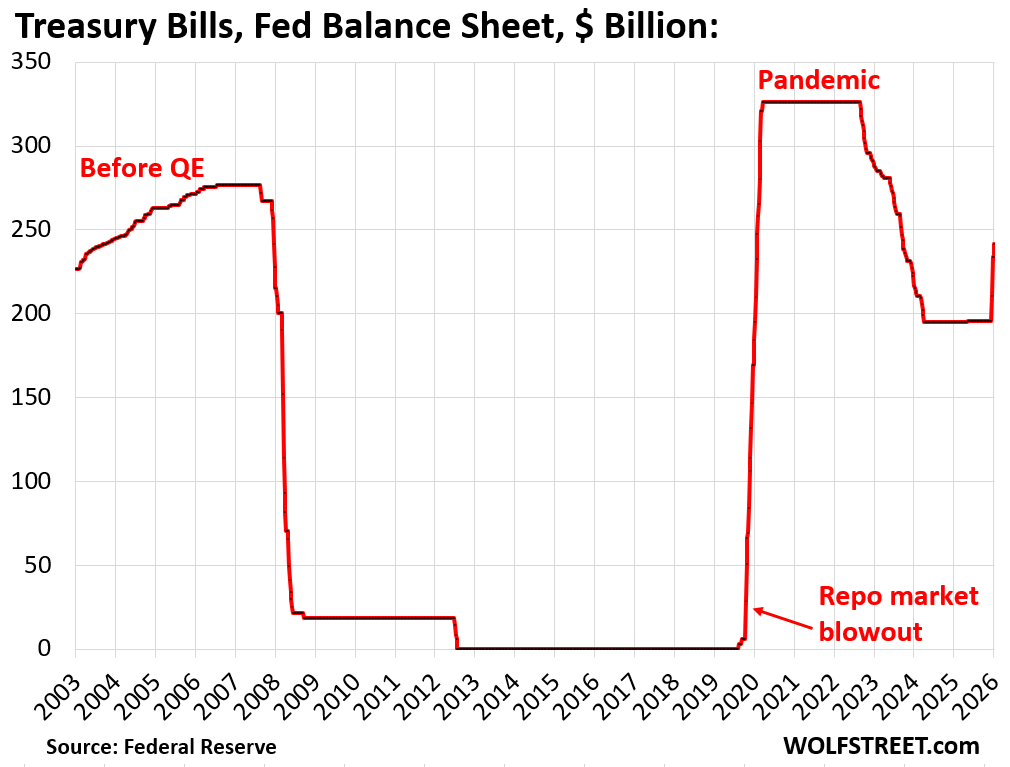

Treasury bill purchases. T-bills on the Fed’s balance sheet rose by $8 billion from the prior week, to $241 billion. T-bills are short-term Treasury securities with terms of 1 month to 1 year.

In December, the Fed started adding T-bills for two purposes, within its new effort to shift the composition of its balance sheet toward T-bills:

- Replace the MBS that come off its balance sheet to reach its goal of shedding all of its MBS over time;

- “Reserve Management Purchases” (RMPs) to increase reserve balances (bank cash on deposit at the Fed) as needed for reserves to remain at “ample” levels.

Until December, the Fed held only $195 billion in T-bills – only 3.0% of its total assets at the time. The only reason it had any T-bills at all was the repo market blowout in late 2019 when it purchased T-bills in addition to engaging in repos to bring that back under control. Before the repo market blowout, T-bills were at zero.

On December 12, the Fed started buying T-bills for RMP purposes and to replace MBS that come off the balance sheet.

Since then, the Fed added $46 billion in T-bills:

- $15 billion replaced MBS that came off its balance sheet

- $31 billion for RMP purposes.

When the Fed made that announcement in December, it said that RMPs for the month from December 12 to January 12 would amount to $40 billion.

The Fed will announce in a few days the amount of the RMPs to be purchased during the next 30-day period. The amounts will vary by season. The Fed is currently frontloading for April 15 Tax Day, when big liquidity strains are expected. After that it will slow the RMPs, it said.

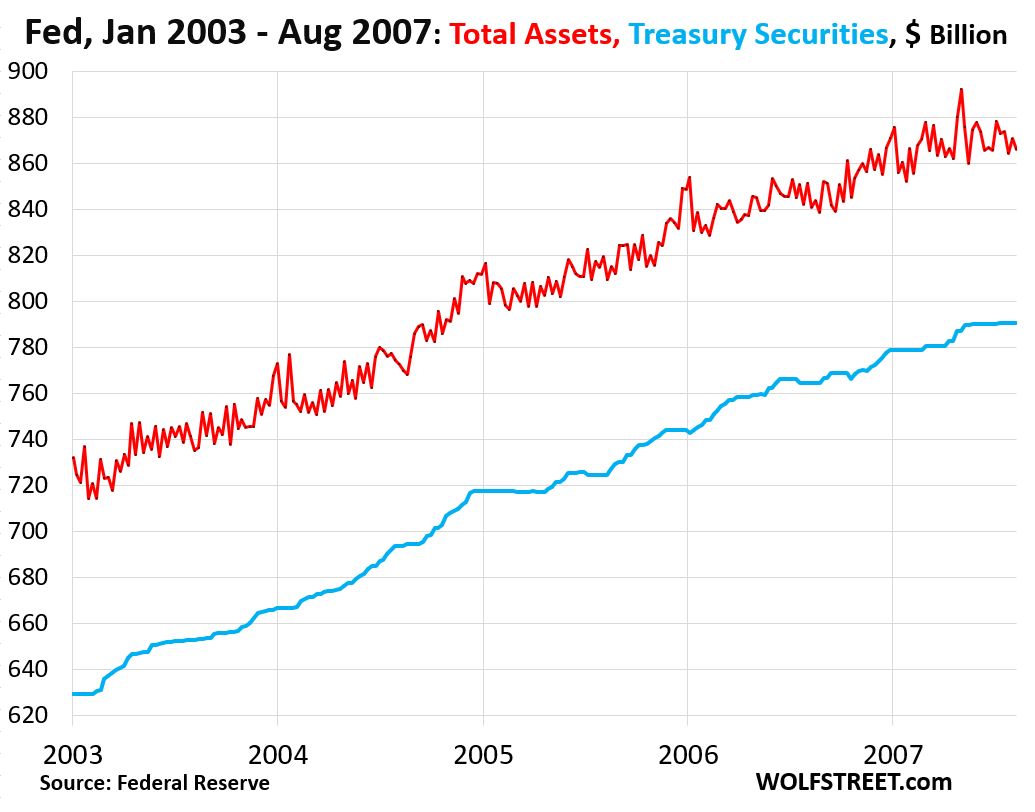

Before 2008 and before QE, the Fed always let its balance sheet grow roughly with the nominal economy (at the time, largely a function of currency in circulation and inflation). It did so by purchasing T-bills and Treasury securities, and by engaging in repos. QE changed that in 2008, when the Fed suddenly began to balloon its balance sheet out of all proportion.

Note the growth of the Fed’s T-bill holdings before 2008 QE. This pre-QE method of letting the balance sheet grow roughly with nominal economic growth and shifting more of its assets to T-bills is what the Fed is reverting to.

From January 2003 to August 2007, the Fed’s total assets increased by 18%. That was not QE but standard balance sheet management, to keep the balance sheet in line with the economy.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Think the 2nd paragraph should be December 31st.

Always appreciate your reporting efforts!

Thanks!

“President Trump said he was directing the purchase of $200 billion in mortgage bonds, which he framed as his latest effort to bring down housing costs ahead of the November midterm election.”

In response, the Fed should seize on this opportunity to sell $200 billion of mortgages on its balance sheet.

Trump will have to issue $200 billion in additional Treasuries to fund the purchases of the $200 billion in MBS. It may reduce the spread a tiny bit between MBS and 10-Year Treasury yields, but it will cause the government, in one form or another, to issue $200 billion in additional debt. And that might push the 10-year yield up a little. So it might reduce the spread a little, but to a higher 10-year yield. And then mortgage rates might not change much.

What that is actually doing is loading up Fannie and Freddie with MBS and mortgages, which was exactly what blew them up in 2008 when they carried $1.5 trillion in mortgages and MBS that went sour. They’re the mortgage insurer/guarantor. They carry all of the risk of those mortgages and MBS.

What duration do you think those “treasuries” will be Wolf? Smart money would guess T-bills?

Treasury has already said that it will further increase issuance of notes and bonds because they cannot fund all this new debt with T-bills. This means that the SHARE of T-bills will increase, but the amount outstanding of notes and bonds will also increase, just not as fast as T-bills.

Also, and I have discussed this in my articles: In December, for example, the $39 billion of 10-year Treasury notes sold at the auction replaced the $21 billion of 10-year notes that were issued in December 2015 and had matured. That’s how you need to look at it. $21 billion in 10-year notes matured and were replaced with $39 billion in new 10-year notes.

You should read these articles – I now do them monthly, after the 10-year and 30-year auctions:

https://wolfstreet.com/2025/12/12/us-government-sold-602-billion-of-treasuries-this-week-10-year-treasury-yield-bounces-back-to-4-20-30-year-yield-to-4-86-highest-since-sep-4-after-fed-cuts/

Will do Wolf. For those of us interested, are you keeping these reports under a specific tab/section on your front page?

This is a new feature, and I’ve done only three of them so far, one a month, around mid-month. You will recognize them by the headline, which will say something like: “Government Sold $X billion in Treasury Securities this week…”

You will be able to find the past ones in the category “Debtor Nation” where all my government-debt articles are (list of categories is in the left sidebar on your laptop, so just click on Debtor Nation):

https://wolfstreet.com/category/all/debtor-nation/

On your smartphone, there is a hamburger menu in the upper left corner. Tap it, which opens the menu, scroll down to Debtor Nation and tap it.

Wouldn’t that require Congress to appropriate the funds for Fannie, and then Treasury issues the new debt?

I realize that Mike Johnson is just a puppet, and it could pass, and the Constitution is merely a suggestion to Trump. But it would take time.

Raiding Fannie’s balance sheet seems like another alternative. I have no idea though whether that is feasible.

Good idea, especially since that would only be 10% of the Feds enormous $2 trillion in MBS, but I’m doubtful that they will because I don’t know how much that would push down rates for the MBS on the market, if at all, since it wouldn’t seem to create any extra demand for the MBS on the market. But the whole scheme to add more to our already huge national debt to try and alleviate interest rates, which are a result of the too high debt, seems like another illogical and bad idea to me. The fed has printed two thousand billions of dollars to artificially suppress mortgage rates, but they are still too high?

Reinforcing your comments, extract from AI

Quote:

the Fed’s shift from mortgage-backed securities (MBS) to Treasury bills (T-bills) while managing its balance sheet can support dollar stability by providing market liquidity, reducing uncertainty, and aligning its holdings with operational needs, ensuring smoother market functioning and reinforcing confidence in U.S. financial markets, which underpins dollar strength.

Unfortunately, with plans to increase military spending to 1.5 trillion, purchasing Greenland, buying MBS, and all kinds of crazy spending that does nothing for the average American, that’s going to be a massive T-bill issuance. LOL!

It’s almost as if there is an intentional plan to destroy the Federal Reserve Note…

CONgress is completely disconnected from the real economy. I wonder who will prevail? Place you bets…

We , the USA is NOT buying Grenland, nor are we taking it by military. We WILL negotiate for increased military bases and mineral rights.

LOL! So you admit the president is an idiot. It’s either that or you don’t understand sarcasm. YES, we already have several bases in Greenland and their government has said as much. Do you have anything useful to actual add that relates to my comments?

America’s DEBT is the problem, and the rest of the world knows it. We will not be able to bully other countries for much longer. The real economy knows this, but CONgress and this president continue to rob the treasury. The ONE hope I had for complete republican control was a balanced budget. I was wrong and it simply confirms we really have one party of grifters.

@WB,

He said no such thing about the prez (and I’ll leave that part at that).

This is all bluster to “negotiate a better deal”, whatever he imagines that to mean. I don’t think having title to the land is any more useful than putting bases wherever he wants, which he can for free.

Although, it is entirely possible that having been told no, laughed at, etc., it’s now an ego thing and he really wants that title to prove he can do it. So who knows?!

WB you should look to NATO spending as the closest comparison for the Greenland topic.

Trump floated leaving NATO (with no serious plans of leaving) and magically more and more NATO nations started meeting their commitments.

Bases and other assurances along those lines are far better than actually holding Greenland. The EU losing their minds is sending them on a fools errand and is walking right into what Trump actually wants.

That would be consistent with he past approaches as well.

If the goal is negotiation l then the idiot in chief is going all about it backwards (no surprise to anyone with an IQ greater than tap water). Up until a year ago, Greenland loved having U.S. military bases on it’s soil. It would have let the U.S. put as many bases almost anywhere they wanted to. If the U.S. wanted to spend hundreds of million building a radar and missile base in the middle of nowhere, Greenland would have been ecstatic with that.

Now that the Moron in Chief has threatened their sovereignty, they will probably have second thoughts about allowing any more U.S. troops on their land.

Just watched a yearly roundup over at fidelity, interestingly one of the people mentioned that MBS are real hot right now.

Something about blah blah the high rated ones.

So we’re plowing THAT field again huh?

Let’s not forget that the EOQ and EOY repo spikes we’ve seen on 6/30, 10/31, and now 12/31 indicate that somebody somewhere (or a lot somebodies) wants to show more cash on their books on accounting day.

There’s almost no repo usage absent EOQ/EOY deadlines. And $75B can hide a lot of leverage.

Wolf,

Because all the major broker-thieves have access to the SRF, do you think the SRF plays a role in keeping the SPAC market juiced? And to a lesser extent, the RMP’s as well? I mean, if the reserve requirement is zero, let those “ample” reserves drain.

SRF balance = ZERO = “ZERO.” How can it keep anything juiced with $0? They were $75 billion for just ONE DAY. And then back to zero. Since Jan 2, NO ONE has been borrowing at the SRF, and everything has been paid back. Look at the chart!

Any comments on the latest Trump edict?

As the Fed allows MBSs to mature and run off the balance sheet, Fannie and Freddie to buy $200 Billion of MBSs.

“Any comments on the latest Trump edict?”

All you have to do is READ it:

My reply to JeffD yesterday, just above your comment:

“Trump will have to issue $200 billion in additional Treasuries to fund the purchases of the $200 billion in MBS. It may reduce the spread a tiny bit between MBS and 10-Year Treasury yields, but it will cause the government, in one form or another, to issue $200 billion in additional debt. And that might push the 10-year yield up a little. So it might reduce the spread a little, but to a higher 10-year yield. And then mortgage rates might not change much.

What that is actually doing is loading up Fannie and Freddie with MBS and mortgages, which was exactly what blew them up in 2008 when they carried $1.5 trillion in mortgages and MBS that went sour. They’re the mortgage insurer/guarantor. They carry all of the risk of those mortgages and MBS.“

Apologies…but I posted prior to Jeff and was delayed awaiting approval from moderator

“Trump will have to issue $200 billion in additional Treasuries to fund the purchases of the $200 billion in MBS”

Is this accurate? General reportage made it sound like Fannie/Freddie have $200B+ in retained earnings that would pay for this.

“General reportage” is frequently wrong but I thought it worthwhile to ask for confirmation.

Kinda matters because 1) paying for it out of F/F retained earnings doesn’t add to money supply but 2) paying for it out of new issue Treasuries has much greater probability of necessitating money supply growth at some point (Fed acting as perpetual money-printing backstop for perpetual fiscal deficit increasing Treasury…)

1. “retained earnings” (stockholder equity) don’t matter. That’s just an accounting entry. Do they have $200 billion in “cash” that they can use to buy securities with?

Fannie Mae’s Q3 financials (10-Q):

$3.9 billion quarterly net income

$12 billion in cash

$27 billion in “restricted” cash that it cannot use

$61 billion in repos

But it needs lots of cash to operate because it buys mortgages with cash, holds them for a while, pools them into mortgage pools, and sells the MBS to investors, when it gets that cash back, to buy more mortgages with.

It had $4.08 trillion in mortgages in those mortgage pools (an asset on its balance sheet)

It had $4.08 trillion in debt (the other side of the MBS it issued) associated with those mortgage pools.

Total stock holder equity is $105 billion, for $4.23 trillion in liabilities. Fannie is among the most leveraged entities out there.

2. The GSEs had been remitting all of their cash profits to the government; and the government used it as revenues to pay for its outlays. This was changed in 2019, and since then, the GSE have been allowed to keep some of their profits to build capital. So any cash that the GSEs don’t send to the government will have to be replaced by new debt that the government issues. There is no way around it.

Given the complete disconnect and irresponsible behavior by this administration and congress, the fed is quickly becoming irrelevant.

Hedge accordingly.

Add in, Congress just approved the extension of temporary Covid subsidies to Obamacare on to top of the existing Obamacare subsidies. 17 Republicans went along with the Dems. No one cares about the deficit anymore.

When bread is $50 a loaf, they might. When bread is scarce, they will. We are headed to the same place the former Soviet Union was in 1990. We are simply coming at it from a different direction.

This is what I have been saying, too. People have this blind spot that somehow the US is invincible to the very same forces that took other nations down. What the FED and US politicians have been doing over the past almost 30 years is destroying everything that was once good about the country, and hastening/guaranteeing its demise so that billionaires and hundred millionaires can own everything.

What’s diabolical is that it’s not even about the money within their little group, it’s about egos and bragging rights. They are destroying an entire nation as they play ego games with each other. I don’t think their skin bags are worth the price of dog food.

” anymore”

how far back are we going?

Wolf,

It may be prudent to remind your readers of the bank bail in provision of the Dodd Frank act, because that is how i believe they will handle the next crisis.

1. The banks have shed nearly all of the residential mortgage risk to the government. So there will not be a repeat of the mortgage-and-banking crisis. That is one of the biggest changes coming out of the financial crisis. So maybe there will be another crisis, somewhere else, private credit, etc.

2. Everyone knows that depositors are “unsecured” creditors, meaning they have no right to collateral if the bank fails. But depositors are “insured” within the limits of the FDIC.

So who got “bailed in” at the bank collapses in 2023? INVESTORS. That’s how it always should be. The FDIC takes over a bank, and shareholders and preferred shareholders lose 100%. It’s not their bank anymore. FDIC then instantly pays the insured depositors up to the insurance limits, sells all of the bank’s assets over time (loans, securities, buildings, etc.), and with the proceeds pays the uninsured depositors, who may or may not get a haircut of some sort, such as getting 80 cents on the dollar for their deposits.

What was new in 2023 is that ALL depositors got deposit insurance from the FDIC without limit. But investors were still bailed in 100% and lost everything, while depositors lost nothing.

I don’t like the way it was done, but I do think Congress should just remove the FDIC cap. I think it’s silly.

they can remove or not remove but what I want is the rules to be followed not arbitrarily benefitting rich people by not adhering to rules like what they did to SVN depositors.

” but I do think Congress should just remove the FDIC cap. I think it’s silly.”

Well Janet Yellen kind of removed it with the coverage given to the SVB payouts

Limits DO serve a purpose….risk management is one

Gotcha, good run down. Only thing i would add is a lot of the people at SVB were connected. Schlubs like us aren’t. I bet they honor anything up to 250k and confiscate anything beyond.

“a lot of the people at SVB were connected.”

Yes, the Silicon Valley billionaire class. Bailing them and their startups out was the scandal.

“What was new in 2023 is that ALL depositors got deposit insurance from the FDIC without limit.”

And you really believe this will continue? What are the total deposits in the American banking system today?

It didn’t continue. There were several small banks that failed since then, and deposit insurance was limited to the FDIC limits.

The key in my comment was this… you need to read it over and over again until you have it memorized:

“The FDIC takes over a bank, and shareholders and preferred shareholders lose 100%. It’s not their bank anymore. FDIC then instantly pays the insured depositors up to the insurance limits, sells all of the bank’s assets over time (loans, securities, buildings, etc.), and with the proceeds pays the uninsured depositors, who may or may not get a haircut of some sort, such as getting 80 cents on the dollar for their deposits.

” There were several small banks that failed since then, and deposit insurance was limited to the FDIC limits.”

Though I suspect you are correct, it is remarkable that those harmed by the limits did not sue based on the precedent set by Yellen.

Equal protection, etc.

“it is remarkable that those harmed by the limits did not sue based on the precedent set by Yellen.

Equal protection, etc.”

Exactly my point. Equal justice under the law or there is no justice.

It looks like Trump got what he wanted, which was a knee jerk reaction by the bond market algos to buy MBS. I guess the question is how long it lasts

Hello Wolf,

Is there any chance we will see reporting on the banks unrealized losses on long term treasuries again soon?

They’re not a concern anymore. They don’t bother anyone. The losses have been declining as those securities get closer to maturity amid lower yields. At maturity, the bank will be paid face value… with zero loss. Those 10-year notes issued in 2020 at 1% yield, now trade like 5-year notes with a 3.75% yield, instead of an 8-year note with a 4.7% yield a couple of years ago. Big difference in price. In 2030, those evil 10-year notes from 2020 will all mature, and banks will get all their money back with no losses.