The Fed’s weekly balance sheet on Thursday will show a substantial drop in total assets.

By Wolf Richter for WOLF STREET.

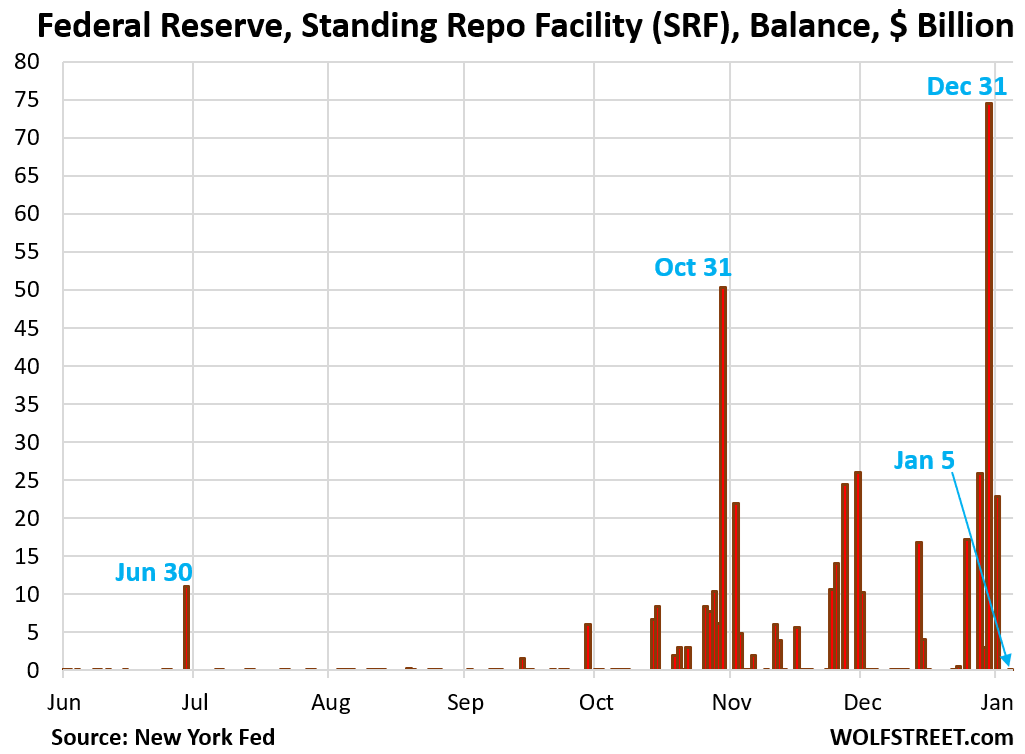

The balance at the Fed’s Standing Repo Facility (SRF), an asset on the Fed’s balance sheet, fell back to zero today, with all repos from Friday unwinding, and zero new repos being taken up at the two auctions today, as expected.

The SRF had spiked to $75 billion on December 31 as part of the year-end liquidity shifts, from zero before Christmas, and that $75 billion had been the largest factor in the $104 billion spike of the Fed’s weekly balance sheet as of the close of business on Wednesday, December 31.

But this spike has now completely reversed; and the Fed’s next weekly balance sheet, to be released on Thursday, will show a substantial drop in total assets.

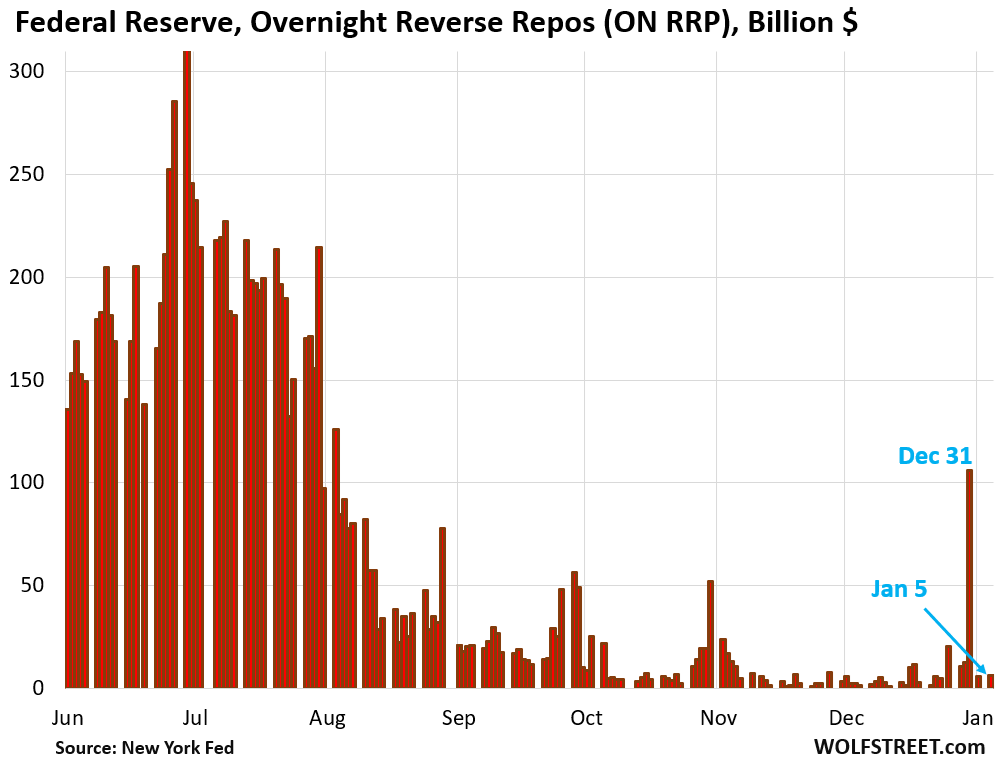

At year-end, massive amounts of liquidity shifted around markets, causing tight spots in some places, as reflected in the spike of repo market rates, such as SOFR, and excesses in other places, as reflected in the spike at the Fed’s overnight reverse repos (ON RRPs) which drain liquidity from the markets.

The tight spots showed up in repo market rates, such as those tracked by SOFR, which surged at the end of December, with some transaction rates as high as 4.0% on December 31. On that day, SOFR – a calculated median for the day’s rates – jumped to 3.87%.

This spike in repo rates made it profitable for banks to borrow $75 billion at the SRF on December 31 at 3.75% and lend to the repo market at higher rates through the holiday until Friday morning.

On Friday, January 2, as repo market rates dropped – the high was down to 3.87%, and SOFR was down to 3.75% – that profit opportunity vanished, and banks unwound most of their repos at the SRF on Friday, and unwound the rest today, and the balance went back to zero today.

But the Fed’s weekly balance sheet, which shows balances as of the close of business on Wednesday, had booked that $75 billion one-day-wonder spike at the SRF that had occurred on Wednesday, and that had been the primary factor in the $104 billion spike of the Fed’s total assets on its balance sheet released on Friday.

But the Fed got its $75 billion back, and the counterparties got their collateral back, and that $75 billion has now been completely unwound and vanished from the Fed’s assets.

The excess liquidity that had occurred in other parts of the market on December 31 showed up at the Fed’s overnight reverse repo facility (ON RRPs). And it has been unwound nearly entirely.

That excess was reflected in the spike to $106 billion at the Fed’s ON RRP facility on Wednesday, December 31.

ON RRPs mostly reflect excess cash that money market funds have put on deposit at the Fed; they in essence lend their excess cash to the Fed and earn 3.5% on it. The Fed owes them this cash, and so ON RRPs are a liability on the Fed’s balance sheet.

On Friday January 2, the ON RRP balance plunged to $6 billion, from $106 billion on December 31. Today it remained at $6 billion. So this too has settled down, as expected.

These two facilities at the Fed – the SRF and ON RRPs – are part of the Fed’s system of control of short-term interest rates to keep them in the range of its monetary policy rates, currently 3.5% to 3.75%.

The SRF rate acts as a ceiling rate – one of the tools to keep overnight rates from surging too far above the Fed’s top end of the range (3.75%).

The ON RRP rate acts as a floor rate – one of the tools to keep short-term rates from dropping too far below the Fed’s bottom end of the range (3.5%).

And the counterparties of these two facilities are not the same, and so the rates affect different parts of the market: The counterparties of the SRF are 43 big banks, broker-dealers, and a credit union (I posted the updated list in the comments below). The counterparties of the ON RRPs are mostly money market funds.

After three years of QT removed $2.43 trillion in liquidity from the markets, these kinds of brief liquidity shifts are going to show up on key dates during the year, such as year-end, quarter-end, month-end, and particularly on Tax Days, such as around April 15.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The updated list of the 43 approved counterparties at the SRF:

Ally Bank

Bank of America, National Association

Banco Popular de Puerto Rico

Banco Santander, S.A., New York Branch

Barclays Bank PLC, New York Branch

BMO Bank N.A.

Canadian Imperial Bank of Commerce, New York Branch

Capital One, National Association

Charles Schwab Bank, SSB

Charles Schwab Premier Bank, SSB

Charles Schwab Trust Bank

Citibank, N.A.

Citizens Bank, N.A.

Comerica Bank

Credit Agricole Corporate and Investment Bank

East West Bank

Fifth Third Bank, National Association

First-Citizens Bank & Trust Company

First Horizon Bank

Goldman Sachs Bank USA

HSBC Bank USA, N.A.

JPMorgan Chase Bank, N.A.

KeyBank National Association

Manufacturers & Traders Trust Company

Mizuho Bank, Ltd., New York Branch

Morgan Stanley Bank, N.A.

Morgan Stanley Private Bank, National Association

MUFG Bank, Ltd., New York Branch

Natixis New York Branch

Navy Federal Credit Union

PNC Bank, National Association

Regions Bank

Royal Bank of Canada, Three World Financial Center Branch

State Street Bank and Trust Company

Sumitomo Mitsui Banking Corporation, NY Branch

The Bank of New York Mellon

The Huntington National Bank

The Norinchukin Bank, New York Branch

Truist Bank

USAA Federal Savings Bank

U.S. Bank National Association

Wells Fargo Bank, N.A.

Zions Bancorporation NA

Interesting that Canadian and other foreign banks are on the list. As an outside observer, I assumed that the list would be limited to US banks…

Canadian Imperial Bank of Commerce, NEW YORK BRANCH ;-)

These are US operations, regulated by US regulators, of foreign banks.

Is that the list of “Too Big To Fail” bros who the Fed will always rush in to bail out when they screw things up?

No, as we have seen, big regional banks, such as Silicon Valley Bank, Signature Bank, and First Republic Bank, are not too big to fail. Those three were taken out the back and shot, their executives got fired and sued, and investors lost everything. Only the depositors got bailed out. There may only be a handful of TBTF banks on this list of 44 banks.

“Only the depositors got bailed out.”

Wayyyyyyyyyyyyyyy over the FDIC limit i might add. But hey, why have rules right?

“Ninety-four percent of SVB’s deposits were above the FDIC’s $250,000 insurance limit, according to S&P Global Market Intelligence data from 2022, meaning the bank held one of the country’s highest shares of uninsured deposits when it collapsed.”

“For my friends, anything. For my enemies, the law!”

Citizens United is the newest Amendment to the Constitution, Mr House.

Yes, and bailing out uninsured depositors stopped the run on other banks uninsured deposits which prevented a disaster.

So you could say it was a “to big to fail “ situation.

“So you could say it was a “to big to fail “ situation.”

Which will continue to happen until you let them fail. How have you guys not noticed its essentially looting of the public treasury at this point? We live in a Banana Republic, but most are too greedy to admit it until their rice bowl gets broken.

Initially I was against the bailout of the SVB depositors. I believe in the rule of law and thought that they should suffer the consequences of their negligence.

However, I have come to learn that after all was said and done, the depositors would have likely been made whole anyway. The banks assets would have been sold off and the depositors would have been first in line and likely been made whole anyway. It would have just taken a long time.

If guaranteeing the depositors money upfront prevented an unnecessary run on similar banks, it didn’t really change anything, so I am ok with it.

Going through the whole selling off assets and reimbursing depositors would have taken a long time and caused a lot of pain to people whose only fault was they assumed their bank was safe

I understand that there is a segment of people who enjoy seeing unnecessary pain in others.

They would have been made whole anyways, so bail them out? Help me understand that logic. Sooooo many apologists, like i said greed for your stocks, your 401k, sacrifice your children to moloch and high asset prices. Seeing pain in others for gambling in a bank that failed, so the public should pay because i may have lost some money. You guys are all gorden gecko, no wonder this country is failing at an accelerating rate.

Moral hazard is real. Will we fade the knee jerk reaction from the weekend events starting tomorrow? Broadening attempt is underway, will its legs run out of steam tomorrow? Googl and NVDA are setup for the downtrend, will it lead everything else? 3 day rule for new highs is intact for a reversal, will see soon enough

If RMPs are seasonal, then stocks fall about the 3 week in Jan.

What was Bernanke thinking when he eliminated the REPO facilities?

It seems to work very well.

Did the 2008 financial crisis just overwhelm it?

To be fair, when the REPO facilities were eliminated, the crisis they were facing was big enough that the REPO facilities couldn’t handle it anyway. They knew they needed alternatives and what they settled on fixed the problem. The error though was they thought it was magic. They thought it was a better way all around so they abandoned old ways.

Unfortunately they made the classical mistake that has been made over and over again. They time mismatched assets and liabilities. They were using a long term asset (an instrument based on 30 year mortgages) to solve a short term liquidity problem.

It was an absolutely dumb mistake, but one made when facing a much bigger problem (systemic collapse of the banking system).

Bernanke conducted the most contractionary monetary policy since the GD. It turned safe assets into impaired ones.

Those surges in interest rates must be how the oligarchs make money; analogous to the Duke brothers’ pork bellies at Christmas in the movie: “Trading Places.”

Add Coconuts, Monkey Business, How to Stuff a Wild Bikini, Wall Street, Jumanji, Girls Go Wild videos etcetera, etcetera, etcetera. Then get Hollywood to focus on the rising metal mania and we’ll have an entire collection of films related to what happens when you introduce bi-pedal bloated monkees to hallucinogens. They go apesh*t coo-koo! Far too many puppy uppers before the doggy downers arrive. Sit Fido. Calm boy. Now fetch. Just what the masters ordered.

Actually it is the opposite.

It is nothing more than a mechanism allowing the market to quickly respond to a minor imbalance in supply and demand.

Why will spikes be expected leading up to Tax Day?

Because on tax day, the government collects huge amounts of cash in form of tax payments, and this cash comes out of regular personal and corporate checking accounts (cash in bank) and goes as tax payments into the government’s checking account, the Treasury General Account (TGA), which is at the New York Fed, and when the Fed receives any cash, it destroys it as a matter of routine (the Fed does not have a cash account). So for a few days, huge amounts of liquidity are drawn from the banking system into the Fed via the TGA. This cash is then slowly put back into the banking system as the government spends it. So you have these huge cash flows into and out of the TGA that massively impact market liquidity.

There was a time before the Financial Crisis, when the government had checking accounts at commercial banks, which didn’t cause this problem because the cash stayed in the banking system. But during the Financial Crisis, the government’s checking accounts were moved to the New York Fed.

Wolf,

1) I’m glad that you laid out,

“These two facilities at the Fed – the SRF and ON RRPs – are part of the Fed’s system of control of short-term interest rates to keep them in the range of its monetary policy rates, currently 3.5% to 3.75%.”

because that statement *explains* why people should care about the operation of particular Federal Reserve actions/metrics.

In fact, I think it would be very helpful for your readership if you put these sort of “why it matters/why I should care” explainers towards the *top* of your Fed-related posts – otherwise these kind of posts can pretty much baffle 90% of your readership (me frequently included – until I mull and mull and mull…). A more casual reader isn’t likely to grasp the significance of what you are trying to say otherwise – and if not, your efforts are being largely wasted,

2) On a semi-related note, the bigger picure (why these things matter *more*) is that because – at least on the loosening end of things – the Fed isn’t a MUTPD (Magical Unicorn That Poops Diamonds) – it can only engage in these sort of interest-rate-restraining operations by *printing incrementally unbacked money* (ie, creating inflation – either somewhat benign or dangerously toxic, but inflation regardless and inescapable).

*That* dynamic (on the gross scale, over decades, of the Fed *having to* print money/create inflation in order to keep US interest rates from exploding to a level much more reflective of being the World’s Most Enormous/Leveraged Debtor).

That massive/dangerous tradeoff – relentless inflation (in real goods/”assets”/what have you) in order to temporarily avoid the consequences of perpetual deficits (trade/fiscal) and ever more engorged debt levels, **is the absolute core dynamic of why *any of this* matters to the country as a whole**.

That can’t be emphasized, repeated, or explained enough.

It is the poisoned seed of America’s relentless relative/longitudinal decline – and *that* can’t be repeated/explained/put up top enough either.

You might not agree with the magnitude/proximity of the macro problem (although I think you have been moving that way over the years) but the important thing is for the debate to be held in the context of relaying various Fed metrics – and explaining *what they imply and why it matters* – up top.

Hammer looking for a nail.

I truly belive that inflation is at a very dangerous tipping point right now, however the reasons have nothing to do with the SRF.

You are looking for reasons to ignite inflation which is causing you to look in places that have nothing to do with inflation.

Good ideas.