Slowly unwinding a phenomenon that wrecked the housing market.

By Wolf Richter for WOLF STREET.

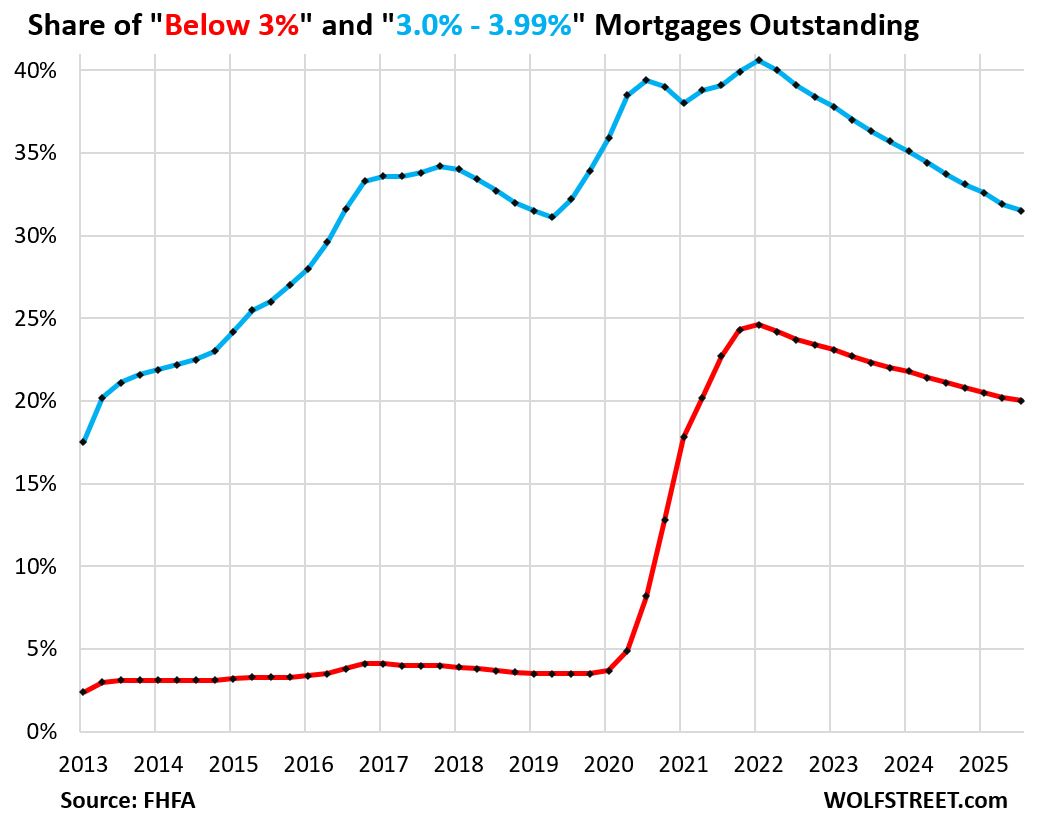

The share of below-3% mortgages outstanding, by number of mortgages, declined to 20.0% of all mortgages outstanding in Q3, the smallest share since Q1 2021, and down from a share of 24.6% at the peak in Q1 2022 (red in the chart), according to data by the Federal Housing Finance Agency (FHFA).

The share of below-3% mortgages had exploded from early 2020 through Q1 2022 when the Fed’s interest rate repression – via trillions of dollars of asset purchases, including mortgage-backed securities (MBS) and 0% policy rates – created a tsunami of homeowners refinancing their homes to get these new ultra-low interest rates.

The share of 3% to 3.99% mortgages declined to 31.5%, the smallest share since Q3 and Q2 2019, and beyond that, the smallest share since Q2 2016 (blue).

All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.

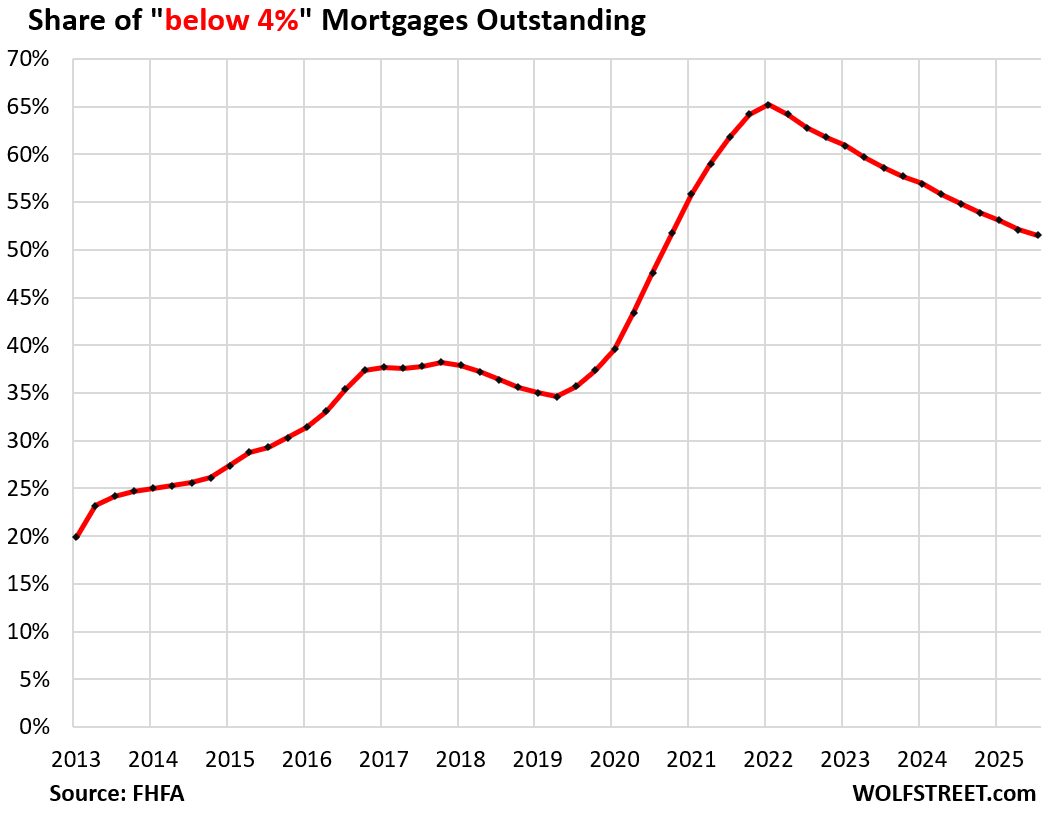

Combined, the share of below 4%-mortgages dropped to 51.5% of all mortgages outstanding, the lowest since Q4 2020, as homeowners, facing changes in life – new job in a different city, divorce, growing family, death, etc. – ever so reluctantly sell their home and thereby let go of these ultra-low interest-rate mortgages.

At the peak in Q1 2022, over 65% of all mortgages outstanding had interest rates below 4%.

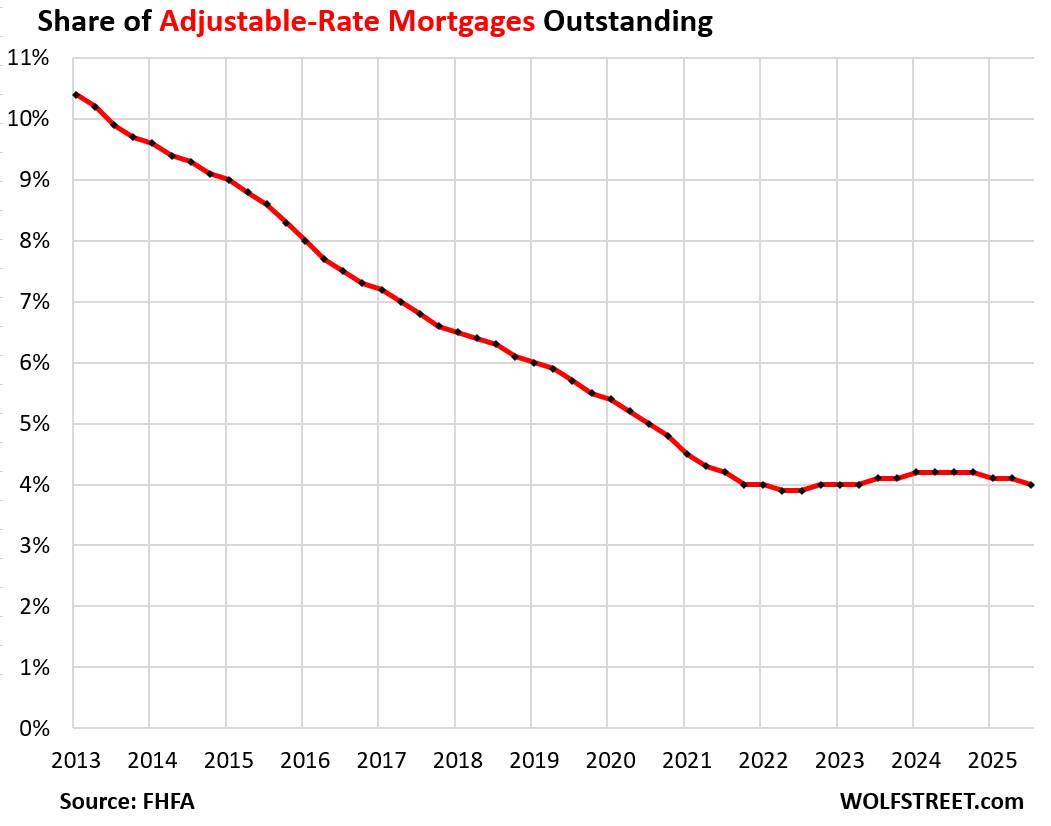

The share of Adjustable-Rate Mortgages has been hovering at low levels since 2021, and dipped in Q3 to 4.0%, down from over 10% in 2013, the extent of the FHFA’s data.

Some ARMs had rates below 3% even before 2020, which is one of the factors in why the below 3% mortgages (red line in the top chart) was between 2.5% and 4% before 2020.

Homeowners with ARMs that were originated when rates were low experienced payment shock when their mortgage rates adjusted as rates began to rise in 2022. But that payment-shock phase has mostly passed by now.

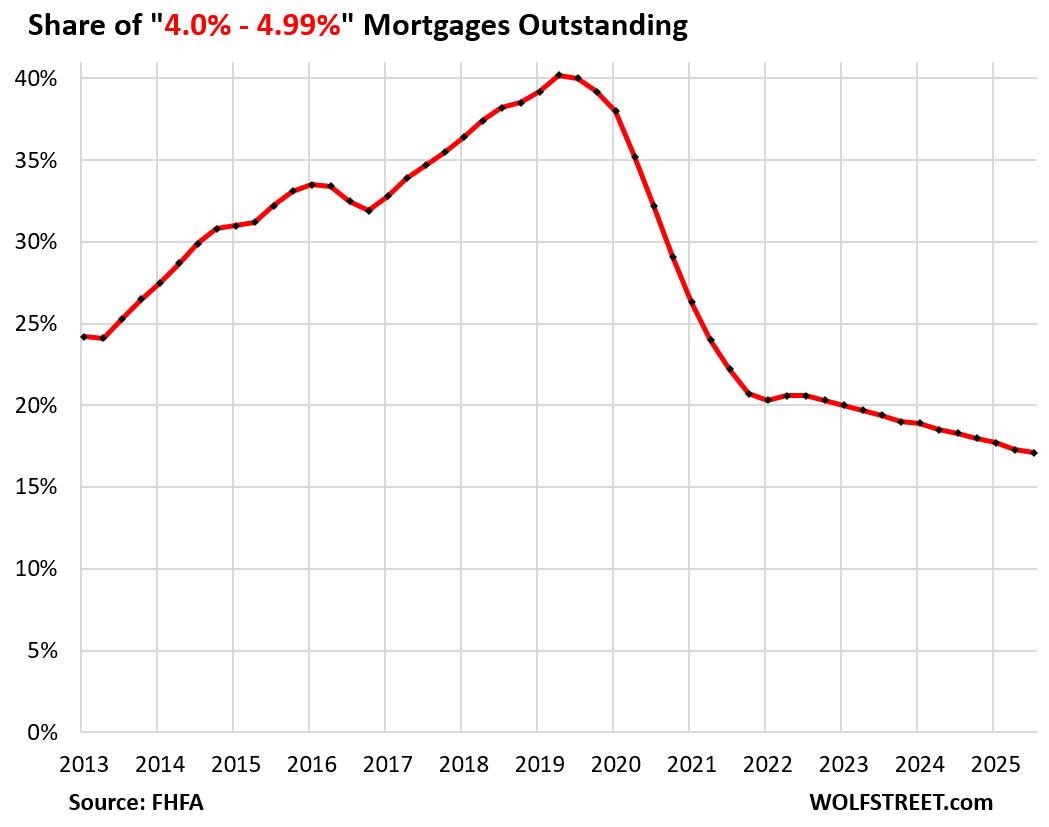

The share of 4.0% to 4.99% mortgages declined to 17.1%, the lowest share in the FHFA’s data going back to 2013, and down from the peak in 2019 of 40%.

When mortgage rates plunged in 2020, massive numbers of homeowners refinanced their mortgages into lower-rate mortgages – but not everyone could get a below-4% mortgage.

Homeowners who had qualified for mortgage rates between 4.0% and 4.99% before 2020 refinanced into the lowest-rate categories. But homeowners who had 6% or 7% mortgages before 2020, due perhaps to a tarnished FICO score, also refinanced into mortgages with sharply lower rates, but the lowest rates they might have had available were in this 4% to 5% range.

In other words, many homeowners refinanced out of this category in 2020-2022 and into lower rates, while a smaller number of other homeowners refinanced from higher rates into this category over the same period.

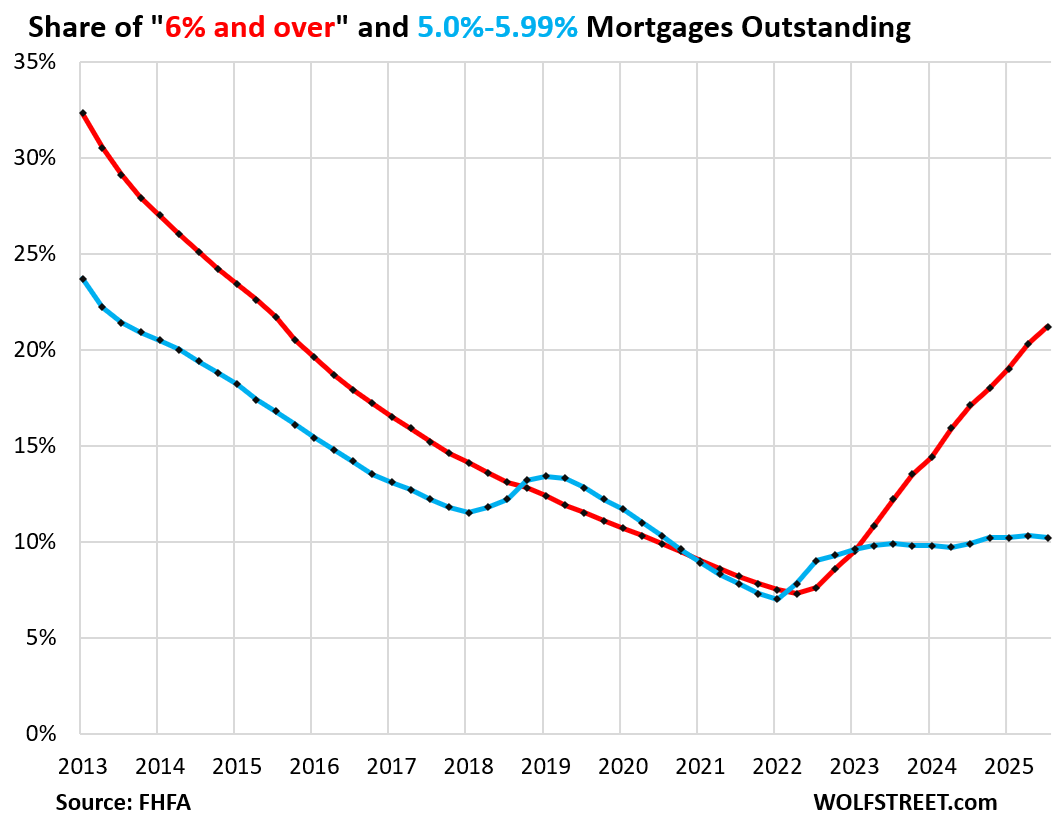

The share of 5.0% to 5.99% mortgages has remained roughly stable in 2023-2025, near 10% of all mortgages outstanding (blue in the chart below).

There are currently lots of fixed-rate mortgages offered in this range. For example, the interest rate of the average conforming 15-year mortgage was 5.44% in the latest week, according to Freddie Mac, but 15-year mortgages are not very popular.

The share of 6%-plus mortgages rose to 21.2% of all mortgages in Q3, the highest since Q3 2015, up from a share of 7.3% at the low point in Q2 2022 (red in the chart).

“Locked in” by Free Money. Below 3%-mortgages are free money in real terms because inflation is currently running at about 3%, and if borrowing costs run at the rate of inflation or below, it’s the equivalent of borrowing money at no cost … free money.

These ultra-low mortgages were a result of the Fed’s reckless monetary policies that caused home prices to explode in many markets by 50% and much more in just two years through mid-2022.

Those too-high home prices and ultra-low-interest-rate mortgages have now locked up part of the housing market – with those homeowners not selling and therefore not buying because they don’t want to finance a more expensive home with much higher interest rates.

This “lock-in effect” has haunted real-estate brokers, mortgage brokers, and mortgage lenders– as transactions and mortgage originations have plunged, and therefore income from commissions and fees has plunged, triggering waves of mass-layoffs and voluntary departures since late 2021.

Nevertheless, life happens – new job, return-to-the-office mandate, divorce, family additions, death, natural disasters, whatever – and so some of those “locked-in” homes with ultra-low-interest-rate mortgages get sold anyway, and the mortgages get paid off, and their share shrinks slowly, unlocking the housing market bit by bit.

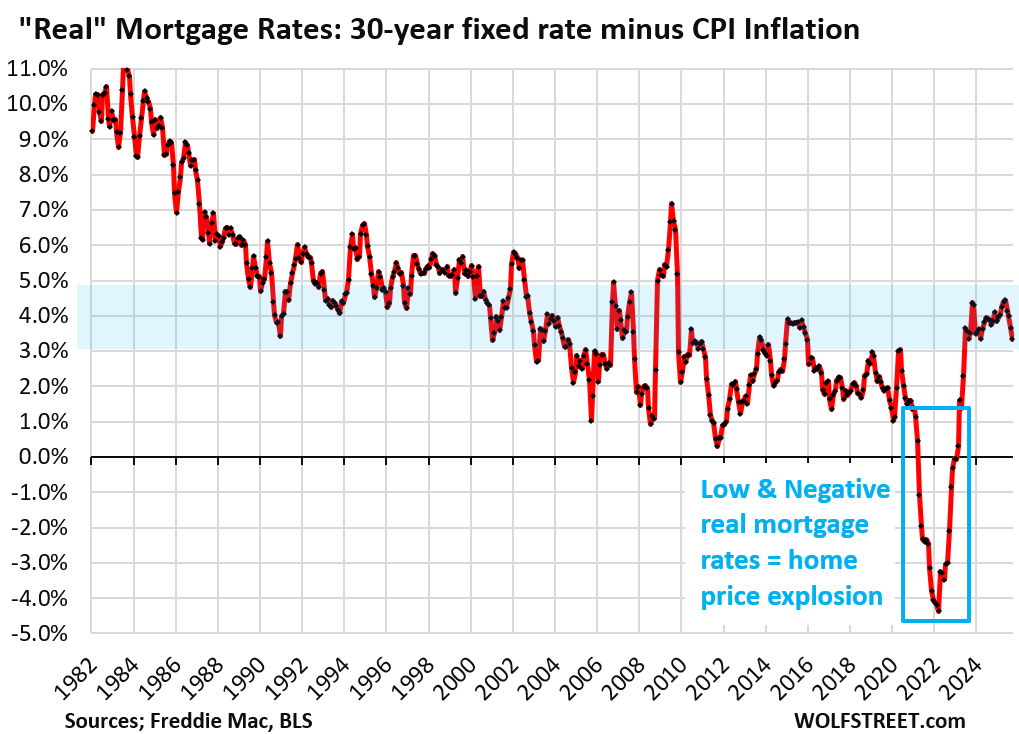

Just how crazy were those ultra-low mortgage rates? Between early 2021 through 2022, the average 30-year fixed mortgage rate was below CPI inflation – negative “real” mortgage rates – free money!

At the peak of the Fed’s craziness, “real” mortgage rates were 4 percentage points below CPI, with the average 30-year fixed mortgage rate below 3% and CPI inflation exceeding 7%.

Those were the craziest times ever in the mortgage market, and in the housing market, and those negative real mortgage rates wrecked the housing market through a historic home price explosion (now being unwound in many markets).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Excellent article. I see this pandemic related distortion dominating the Real Estate Sales market for at least another decade, or until the bottom falls out of the prices because of a recession or depression. So any new buyer is almost guaranteed to lose money. Most holders of these free money mortgages will hold on until a major life event forces them to sell. They will rent their property in the event of a job change which forces a move. There are 45,000 real estate agents here in the state of Maryland. They are leaving the business in droves. 3,000 left last year alone.

I have heard that a lot around here (“If it doesn’t sell for my price, I’ll just rent it out.”). Then they list it for rent and it sits.

The demand to rent single-family homes isn’t as high as these people think it is, at least not at the rents they’re asking.

I’ve heard good stories & I’ve heard nightmare stories.

I believe most landlords are like a lamb accidently stumbling into the Lions den.

The entire industry is built for amateur hour with no warning signs.

Being greedy in a housing

bear market is astonishing.

Sure, but my larger point is that a lot of people, who say are willing to pay $5,000/mortgage, taxes, etc. are not going to be willing to pay that amount, or even close to it, for rent. So the math in these people’s minds doesn’t math, as they say.

These landlords are under the assumption that nobody wants to move, so they can command whatever they want. Truth is, with remote work, lack of family formation, and subscription model to everything in life, it’s only getting easier to move.

well well, say it ain’t so

WE would like to down size from our small 2,700SF home

but with 3.35% mortgage and less than 10 years to pay it off

not going to

have different plan(since we actually know how to rent property)

no not planning on renting this 30 year home – we’ll sell when time is right and take tax free cash home with us

of course our new home will be MORTGAGE FREE instead

deleverage folks – new motto

We have a lot of those in Denver atm.

I’ve also heard horror stories about properties getting trashed and the fixes costing more than what they made it rent. A coworkers tenant burst a pipe and didn’t tell him, instead just moved out so he didn’t find out until he was inspecting the property after she left.

Even without horror stories, simple wear and tear and age beats up a property and it’s associated systems (HVAC, plumbing, appliances, etc) over time that is almost never accounted for by rookie landlords. That furnace is going ot have to be replaced and nobody is accounting for that. They rent it out for 3 years, and now go to sell it and now they need some appliance replaced, the floors are trashed, the water heater is leaking oh and the roof needs to be done.

Yeah…

I know a couple people who were hosed by terrible tenets. Especially during Covid.

An old couple I know were hosed by tenets who did not pay rent because the government said they did not have to pay.

The tenets were still working and making same wages, but said they would not pay rent because Covid said they did not have to.

The government said that they would make the Landlords whole, but 2 years of no rent payments were never realized. Hosed for 2 whole years rent.

These old asset holders worked their whole life to pay for a house. They invested in a retirement plan, and then government and society changed the rules and said they were evil asset holding greedy landlords…

So they lost. Lost it all.

Is getting a renter in 2-3 months w/in normal time frame ?

if priced right for neighborhood

A lot of this is local. As our host has pointed out recently, there are still some very hot rental markets, and in these places such landlords are likely doing well. But in many other places, they just sit.

@MS and @CHS I’ve been renting property for more than 40 years and time to rent depends on the type of peoperty and the rent in relation to the conpetition. If you have the nicest 2 bedroom apartment in town at the lowest rent it will rent quickly since lots of people want a 2 bedroom apartment. If you have a 6 bedroom home on 6 acres 6 miles out of town it will take a lot longer to rent since not many people want a home that big, on a lot that big that far out of town even it the rent was the same as a 4 bedroom home in town.

funny thing is TODAY I have several larger homes getting top $$ with 3 generations of tenants living together

the 1 bedroom ones I manage for others are having bigger vacancies

only been doing this for 30 years here

Based on my son’s observations, he is paying 40% less in rent than what the Zillow payments(PITI) if he bought the same or similar house in the same neighborhood today. That’s not even counting repairs typically required with owning a house.

His landlord is making money because he bought before 2015.

My son is paying current going rent for the area so I suppose anybody who decides to rent out their house at going rates and purchased before 2015 with a fixed 3% mortgage, may be able rent it without much loss (barring a destructive tenant).

It doesn’t make financial sense to buy now with a 40+% spread between renting and owning costs per month. He’s waiting for Wolf’s awesome chart of Price vs rent to intersect again like 2010-2013. Rents almost always go up with inflation (currently 3-5% per year) except in overinflated markets (Austin, Oakland). There is a long way to go before the intersection and cost parity. Houses are too expensive to buy.

Meanwhile, he saves and waits.

In San Diego, I saw a home for rent for $1700 but it’d take $4000 per month to buy the home with 20% cash down.

In the Great Recession, realtors left the market in droves then too.

only top 5% make decent $$

I have friend who is only closing 2 per month now

used to be 5-8 during covid

others I know are NOT MAKING IT, spouse works otherwise they’d be on streets

I chose simpler lower paying route to manage and buy/remodel/rent our own

no pension these days anyway

Luckily Maryland is close to NJ where they are advertising jobs for Gas station attendants. NJ is the only state in the US that will not let you pump your own gas. They are paying $18/hour. So the RE Agents who have lost their jobs because of the moribound RE market in the DC Metro area may want to head up I-95 and start a new career.

Very good summary. Thank you.

I agree an excellent presentation of the official data that is mathematically expected too lag the measured occurrence.

The mortgage market is moribund because the housing asking prices are as much as 50 pct too high in some markets. Speculation is an expectation that the shit wont hit the fan as much as a bet on the future value of the asset.

Affordability is an excellent word that captures the zitgiest of reality between income and expense.

Of course, given the number of billionaires among us, one would think that the tax revenue from the insufferable assholes was substantial while the growth in the national debt plainly showed who picked up the check.

Thanks wolf

IMHO – The inflation-adjusted mortgage interest rates are going down to 2%-5% in 2027. Absolute interest rates won’t go down, or maybe even up much, but with the Fed now printing money to pay the interest on the debt, inflation is sure to increase. People who continue to see U.S. Treasuries as a safe harbor are going to get fleeced. You know who they are, big pension funds, insurance companies, big ‘safe’ investment funds such and so forth, run by risk-adverse bean counters with no imagination and no spine, and they all deserve to go to jail for lying to their policy-holders, beneficiaries and investors, just to hold on to their jobs for a few more years, while they march their policy-holders, beneficiaries and investors off the cliff.

Buying other currencies is no safe harbor because all currencies are going down in comparison to precious metals, and the big financial guys are nearly all prohibited from PMs.

And single family residences won’t go down much in terms of absolute dollars nationwide, only in select markets. But that shipped has sailed in making big inflation-adjusted returns from SFRs, for the next 10-15 years.

There will be winners and there will be losers. The safe harbor bean counters will be the biggest losers, with negative returns adjusted for inflation.

This will be the big come-uppance of the skeptics against the believers in the institutions.

Looking forward to the next 5-8 years. I will be laughing all the way to the bank.

I have more degrees than a person should be allowed to get, and that’s how I became a disbeliever in the system. I realized that most fundamental theories in our social systems, including economics, are self-referential (no fundamental truth). Look at what is going on in MN for example. My first 2 degrees were from MN, and I despise those people. They thought they could re-define reality, just like the architects of our financial system.

You lost me at mortgage rates going down 2-5%. Tell me, what defines the 10 year and what is the 30 year represent? If inflation kicks up, then expect a 7% mortgage indefinitely. If the money printer continues to run (which it will), dollar weakens, and asset prices go up to replace lost value. In this case, you don’t need demand to force price increases. If the FED is rolling off MBS, they are trying to lower prices. The problem: They can’t lower prices faster than they print. I agree with the haves and have not case. The problem is how you see it. If debt to gdp increases, this will fuel further lost trust in the dollar, spiking long term debt.

IMHO – mortgage rates adjusted for inflation are going to 2-3%, mainly because Trump will be pushing mortgage down this summer when Powell’s replacement is installed. That’s my prediction.

I expect mortgage rates to go down before inflation kicks in.

I see your objection. My difference is in the timing of these events. That’s all.

Not trying to force my opinion anyone, just interested in seeing if anyone can poke holes in my theories.

You aren’t from around here, are you?

So you’re telling me(us) that the FED lowering their rate will magically begin to move mortgage rates down? With debt levels and deficit still rising–amidst increasing geopolitical concerns?

The only way The Fed influences mortgage rates to get down to 2-3% is if it starts to purchase MBS again and forces rates down artificially as it starting in 2009 and especially 2020-2022.

I don’t understand why so many think Trump can magically make a 2-3% mortgage happen just by appointing a new fed chair. Perpetual hopium

he inflation-adjusted mortgage interest rates are going down to 2%-5% in 2027.

Well, given the 6.3 mortgage rate, just noodling, and the actual rate of inflation the mortgage rate is not the problem. The normalized mortgage rates are probably a guardian angel preventing the next generation from listening to the nesting instinct

The problem is that the price is too high by a lot, on the order of 40 pct ot more

I agree that price is too high.

If mortgage rates go to half of what they are now (before the next bout of inflation kicks-in), that will greatly improve affordability.

For example, with one of my mortgages, that will cut my monthly payment by nearly 40% (including tax and insurance).

That alone is a huge improvement in affordability.

But that’s not how it works for homebuyers — which is where the affordability issues are. If mortgage rates drop to 3%, home prices might spike by 50% again and homebuyers will be SOL again, in a much worse way than now. Low mortgage rates are toxic for affordability because prices adjust upward to them. These 3% mortgages CAUSED the current affordability issues. I’m not sure why this is so hard to grasp.

To piggyback on Wolf’s comment.. the cost to entry for the current market is the problem. The increases in home prices has created a situation where a first tine homebuyer needs a very large nut compared to historical levels. The market has created a smaller pool of possible buyers, and it shows in the activity. You are going to end up in a situation where its asset owners trading with asset owners.

This problem is worse in America. There are cultures where people still focus more on the actual price. Many Americans only care about the monthly payment, whether it’s a house or a financed car. That’s why the 3% mortgage rates caused prices to skyrocket. Had people exercised a modicum of self-control, things wouldn’t have gotten so out of hand.

MS also lost ME at “mortgage rates adjusted for inflation will go down to 2-5%.”

I guess I am confused as to how that “adjustment” is considered?

Aren’t mortgage rates currently in that range?

If inflation is 3% and mortgages are 6-7% (even up to 8?) AND 8-3=5 (still)…. Then I remain confused.

If inflation spikes or even meanders up by 100 bps (or more?), it may change the “inflation adjusted mortgage rate,” and cause prices to rise?

This story sounds familiar….

Well, I expect inflation to increase, while the Fed lowers interest rates.

Wish I could respond to all of the posts here criticizing my post, but most of those posts don’t have a “reply” button.

No here seems to consider the effects of the illegals on the housing market. One of my properties in TX in a lower income neighborhood has gone down in price by 20%, way more than average decrease in TX. Right now, an usually high number of properties in that market are sitting empty, that have been remodeled.

We will lose a lot more illegals in the next 3 years, and that will have a huge effect on housing pricing, even in better neighborhoods, such as my 3000 ft. property that has 4 illegal adults and their 7 children. When they are deported (which is almost certain) I will have to rent that out to others putting more downward pressure on that neighborhood.

Wolf even said “These 3% mortgages CAUSED the current affordability issues. I’m not sure why this is so hard to grasp.”

with no consideration on how the massive amount of illegals during the Biden years affected housing prices.

I seriously doubt that interest rates had much effect since nearly all houses during 2000-2022 were cash sales. I couldn’t buy anything then because I couldn’t find any properties that would accept a mortgage. Where did all of this cash come from ? It must have been fraudulent Paycheck Protection Program (PPP) money that had been given out and was trying find a place to “land”.

So, IMHO mortgage interests were not any serious factor in housing prices going up, the big drivers were PPP cash and illegals.

But, now that sellers will contract with buyers who mortgage, mortgage interest rates are now important, and will have an effect, so lower mortgage interest rates will help keep housing prices from decreasing much in response to deportations and PPP cash drying up, and inflation generally going up as we approach the debt crisis will also help too.

I don’t know why we all forgot about the flood of illegals and the PPP cash.

MS

“I seriously doubt that interest rates had much effect since nearly all houses during 2000-2022 were cash sales.”

LOL, that — “nearly all houses during 2000-2022 were cash sales” — is ignorant BS. Cash sales were around 20%-25% of existing home sales during that time. In June 2021, for example, they were 23% of total sales (NAR data).

Look at the boom in PURCHASE mortgage origination at that time… mortgages taken out to PURCHASE a home:

There is a lot of other nonsense in your comment that I won’t spend my time on. But I just want to add one item:

“One of my properties in TX in a lower income neighborhood has gone down in price by 20%, way more than average decrease in TX.”

In the Austin-Round Rock area, home prices are down 23%, after hugely spiking. They haven’t even undone half of the two-year spike; and that spike came on top of already very high prices.

The home-price explosion we saw in 2021-2022 is a disease that now damages the economy in many ways. Let the market heal that disease by allowing home prices go down and incomes to rise until that combo makes sense again:

I know ARMs have dropped as a percentage of outstanding mortgages, but even at a reduced percentage, every outstanding ARM is seeing their rates drastically increase.

Furthermore, I think lenders learned their lesson with ARMs. It is definitely anecdotal, but I know of two people who had did ARMs during the pandemic whose rate adjustments are going higher than standard 30 year mortgage rates. The language in the ARM was such that they are seeing 7 or 8% rates now.

Now they have to decide if it is worth paying the friction (i.e. closing costs) to refinance.

The payment shock for ARMs is by now behind. Most ARMs adjust to SOFR, which rose to 4.3% in Dec 2022, topped out at 5.3% in July 2023, stayed there until Sep 2024, and has been dropping since then. SOFR is currently 3.87%.

When SOFR started dropping, ARMs adjusted DOWN, and payments got smaller. That’s the phase they’re in now: adjustments to lower payments.

Right, but ARMs have an initial lock period where the rates stay low. Generally 5 years, but I have seen 3 or 7 as well. An ARM with a seven year lock signed in 2019 is going to be unlocking next year. An ARM with a 5 year lock signed in late 2020 just unlocked recently.

So my point was, ARMs signed with locks during the COVID craziness are becoming more expensive right about now (plus or minus 12 months). I am guessing that a lot of those ARMs were cheap (low rate) initial mortgages, but after they unlock they are getting higher rates. I am guessing they are moving from the “sub 4%” or “sub 5%” bucket to the “higher than 6%” bucket.

Also, what I meant by mortgage lenders got smart about ARMs is that although they are tied to the SOFR, it is typically SOFR plus a number that makes them a higher rate than a standard 30 mortgage rate now that they are unlocked.

For example, while I do not remember the exact numbers my acquaintance said, the gist of his complaint was that he had signed an ARM with a 5 year rate lock in 2020 around 4% (i am guessing 3.875% or so). When the lock expired in August or September of this year, his adjustable rate is going to climb to just over 7% if SOFR does not change.

It is a higher rate than the standard 30 year, but not so significantly higher that would make it obvious choice to pay the friction costs to refinance.

“It is a higher rate than the standard 30 year, but not so significantly higher that would make it obvious choice to pay the friction costs to refinance.”

I think probably the point I was failing to make is that for some multi-million dollar ARMs the amount of borrowing is so extreme that even a small increase in the rate comes to thousands of dollars a month more in interest. I am just thinking out loud if these borrows were really stretching to get those loans in the first place in a gamble that rates would be more favorable about 7 or 10 years. And if they are not, what will be the result of the interest rate increases. For example, I personally know of a 4 million loan at 3.25% on a 10 year ARM. It will float free in another 4 years. In the mean time the taxes have increased on this home by 30% in in 6 years to 64k annual which is eye popping. The monthly mortgage may well increase from 18k a month currently to 24k a month in the first two years the ARM is allowed to float (2% max increase). The individual that owns this home is starting to struggle even now. There are others in a similar situation that gambled with large loans. Why the banks or non-banks made these loans is a whole other question. But from a macro economic perspective these loans may be insignificant. However, from a regional bank loan perspective as was the case with this loan the losses may be significant.

There’s a also a lot of 2 year rate buy downs expiring

I personally know of several jumbo ARMs on homes in my area that are set on a 10 year ARM with 4 to go. These are 2 to 5 million dollar mortgages. So although many 2, 3 and 5 year ARMs have adjusted there are still some rather large 10 year ARMs out there. The percentage might be insignificant as I have no data on it.

One would think that ARM’s seem to presently not be competitive with the fixed rate mortgage.

There is an aspect to this that I have long talked about but that generates very little enthusiasm amongst others because it is counterintuitive. That is, it doesn’t necessarily hurt to refinance your primary residence even at these higher interest rates.

As inflation drives the price of everything higher and people find themselves needing to improve their monthly cashflow, then those who have significant equity built up in their house can benefit from a refi and reduce the “nut” (i.e. the fixed monthly mortgage payment) by shifting the balance of their debt into a new 30-year term.

I think this trend is only going to accelerate and those low-rate mortgages will steadily get eaten up people looking to improve their balance sheets by extending their term structure.

Your comment is equivalent to “Cutting your throat to blow your nose”. I “ll get rid of my 2.5% rate at 30/yrs to refinance @5.5 or 6.0%. That’s is Nuts. Never mind the increase in taxes and insurance we’ve seen across America. If you are not forced to sell or drowning in debt. Your best decision is to stay the course, and pass that rate down to the kids or grandkid’s. Even renting to extended family better option than refinancing.

Most definitely

I read Bessent wants ZIRP-NIRP back.

He sees the Fed rate at 1% in one year from now.

I also hear all you have to do while being interviewed for the Fed chairs job is to grovel at bessents & trumps feet.

I can grovel for power.

I also heard the Oracle of Omaha didn’t like the idea of bills going 1% & threatened to buy Japanese bonds. Buffet has $384 billion in T-bills. Not even Wolf has that much 🙂

Without any context beyond ‘I read’ or ‘I heard’ isn’t the most accurate response to any comment of this nature, so what?

Especially when AI says U.S. Treasury Secretary Scott Bessent has not explicitly called for a return to a Zero Interest Rate Policy (ZIRP) or Negative Interest Rate Policy (NIRP). Instead, his public comments and policy actions indicate a focus on lowering current interest rates through economic growth and fiscal policy changes, rather than Federal Reserve action, which he sees as constrained by a high neutral rate.

Who is going to buy a 1 percent t-bills when inflation is over 5 percent?. For that matter, over 2 percent. Buy some gold, land, a business, etc. This countries finances are a blatant mess.

Well, *somebody* (if only the Fed…) bought trillions of zirp’ed US Treasuries from 2002 to 2022 (more or less).

I can grovel for power.

You have captured the concept and translated it too everyman

I don’t like Trump, but i find it funny all the people here who scream about him wanting 0% rates. Obama had 0% for seven years with one increase of .25%. Partisan people never fail to amaze or not annoy.

And how was the inflation?

“And how was the inflation?”

Not nearly as bad Cory R. But the question you should be asking yourself is why is that different now? Not the gotcha you think you had my man

Cory R, in assets, it was major.

Rates should never be held at 0 for 7 years, regardless of who is in office.

I can’t find evidence for that, but unfortunately this administration’s economic policies have left a lot to be desired. Particularly on interest rates and deficit spending. They appear to want to bring back the reckless days of 2021 to “juice” the economy. It is the wrong way.

Were you replying to me that you can’t find evidence of rates at 0% from 2008 until 2015? You think Wolf would have let that comment thru without him tearing someone a new one if it was untrue?

I lived it, it happened, and if you can’t remember then i don’t know what to tell you. Its funny how everyone here thinks the stock market money they’ve “earned” is from some kind of intelligence. Every gain you’ve made since 08 has been on the back of savers and those who don’t gamble.

@CSH

Disregard my comment. You were not responding to me, my apologies.

I agree.

Add in college tuition, remodels, emergencies, etc…Current Helocs start at 8% plus so if you need a lot of funds then a cash out refi is the only real option.

I have 50% equity in my house and a sub-3% rate. I just checked and my payment would go up by 20% if I refinanced into a current 30 year.

That’s it, I’m thinking that I could refinance my houses and end up with the hot potato, cash

Hmm, what to do with cash at my age, Philanthropy

I understand this happening if a major household expense is needed. My neighbor got a quote for a new roof for 150K. Roof inflation is terrible. He doesn’t have this cash so he will likely cash-out refi from his 3% rate for another 30 years.

He doesn’t have much left on his original mortgage since he refi’d around 200K 5 years ago on a 15 year loan. It is not optimal but you gotta do what you gotta do.

The refi rate is around 6%. The HELOC rate is over 8%

Not knowing any details at all, 150K is way way too much for a standard residence.

Is it a mansion with platinum roofing..

They saw him coming.

This based on me being a roofer for way longer than I wanted to be.

Huck, thanks for your input. I hope he is getting more quotes.

It’s a mini-mansion with tile roof. I think he has expensive tastes in tile.

My point is that the roof is likely a major expense that happens every 20-25 years. Houses built before 2005 fall into this category. Homeowners need to find the money for the largest maintenance expense of a house to avoid potentially much more expensive water and mold damage if it is ignored. Even if it is 50K for a smaller shingle house, do people have that money available?

A cash-out refi at 6% may be the cheapest option.

It’s going to take a long time for the distortions in the house and condo market to return to normal. Meanwhile, most young Americans will not be able to afford a house. My house, according to Zillow, is worth 11 times more than I paid for it. That’s how bad inflation has been. Money printing, especially cheap money with low rates, corrupts the money, corrupts prices, corrupts the economy. There are no zero rates in capitalism. In 2020 our central bank drove down rates to stimulate buying of homes, cars, appliances, etc. But in 2 years price inflation in houses was 60% to 100%. It was a terrible decision. And we have $38.5 trillion in federal debt going to $50 trillion in 10 years. Interest on that debt is about $1.3 trillion per year. Total Debt divided by GDP is horrendously high.

Got news for ya, Jeff. $50 trillion in debt will be here well before 100 years. A lot closer to 5 years.

Yep, since we are increasing in net, debt by about $3 tril/ year, total debt will be about $50 tril in 4 years.

The debt has increased at a rate of about $2.2 trillion a year in 2024 and 2025, and by $2.6 trillion in 2023.

Hi Wolf – I wanted to respond and say, that I stand corrected, then we won’t get to $50 tril in debt until 2031, but your reply has no “Reply” button.

I knew this would happen.

This is America. The land of irresponsible YOLO spending and showing off on social media. Did anyone think that people were going to get a 3.0% mortgage and never refinance or move again in their lives?

If activist types were Economics majors, they would be marching on Constitution Avenue.

Or they might ‘assume a march’….

In this article, there is the notion that the Fed has an undemocratic and independent power, e.g. “…the Fed’s reckless monetary policies” and “At the peak of the Fed’s craziness…” But the Fed’s money comes from debt, and that debt has to be approved by Congress, correct, i.e. the “debt ceiling”? In other words, for the Fed act in a crisis, e.g. a pandemic, Congress presumably has to approve the additional debt issued (and there need to be buyers of that debt, as well; if the Fed was being so stupid, why would the market buy the debt?). Was it truly the Fed being reckless, or should the analysis be that the system is reckless, with the Fed playing its role?

Maybe the government went too far with “free money” but it was solving a nonlinear, i.e. difficult to model, social (and political) problem that was alleviated by making money available. Hypothetically, suppose the government had done nothing in response to the pandemic, and just told people to rely on their emergency funds? How would that have worked out? Not well.

“But the Fed’s money comes from debt, and that debt has to be approved by Congress,”

No… some conceptual confusion here.

The Fed (Federal Reserve) created massive amounts of money out of nothing during QE and bought trillion of dollars of securities (debt) with it.

The Treasury Dept. issues (sells) the securities (debt) to fund the expenditures that Congress passed into law and told the Treasury Dept to fund.

“Hypothetically, suppose the government had done nothing in response to the pandemic, and just told people to rely on their emergency funds? How would that have worked out? Not well.”

I think you are wrong.

Wealth concentration and unaffordability are at highs. Inflation skyrocketed to 9% at peak, 20% over 4-5 years. Trust in government has been lost. People feel the system is rigged more than ever. That’s your “not well” ending.

The alternative was a well deserved drop in asset prices from unsustainable levels, which might have temporarily increased unemployment. Look to past recessions to see how free market forces quickly resolve that problem.

Why do some people quickly lose confidence in themselves and others, then look to governments for bailouts and freebies? It creates unnecessary dependency.

Maybe the government went too far with “free money” but it was solving a nonlinear, i.e. difficult to model, social (and political) problem that was alleviated by making money available.

Hardly. That model was solved several hundred years ago,

I’m not sure what is meant as non-linear model ? Like developing a general model of the graphical data Wolf presents.

The free money era has been an exercise in desperation in preventing the wealthy from losing money by sticking it to the everyday bloke to bail their entitled asses out

Stymie, this is a nonsensical false choice. There was a lot of middle ground between “do nothing” and “borrow trillions and hand it out with no consideration as to whether it was targeted well or not.”

The federal government should have done three things. 1) Increase funding for treating and testing for COVID, so hospitals and states didn’t get overwhelmed, 2) increase unemployment benefits for people out of work because of COVID, and 3) compensated businesses that were forced (either directly or de facto) to close because of COVID. That is ALL it should have done.

Handing out $600/week to people who made much less was stupid. Handing out a trillion in PPP loans to small businesses that not only didn’t lose a dime of revenue, but boomed, was idiotic. Handing out $2,000 checks to people who didn’t lose their jobs was idiotic. Handing out tens of billions to schools and colleges with no strings attached so that they could upgrade their fitness facilities (this did happen!) was stupid.

Massive inflation from handing out $5 trillion to compensate for $1.5 trillion in lost activity was obvious and foreseeable.

Any way to know how much of the ratio change is due to people paying off the 3% versus the rise in >6% originations?

Percentage of 3% could decline even if none are paid off, as an extreme scenario.

It looks like the majority of mortgages in America are fixed, mainly 20 to 30 years, while in Canada, the mortgage rates are variable (or ARM as they say in America).

Would that mean that an American in 2021 who took on a 30-year mortgage at 2% pays that rate for the rest of the mortage?

Because in Canada, the 0.99% 5-year fixed mortgages have to be renewed at current rates from 2026 and beyond. Which explains why it feels like Canada is undergoing a consumer slowdown right now, in addition to a population decline of approximately 80,000 people.

Yes, “fixed rate” means fixed for the entire life of the loan.

I’m less worried about housing and more about inflation. I think a given deficit won’t be reined in by Congress. That combined with countries that will slowly utilize the dollar less and less as reserves. Who is going to buy short term treasuries at 3-4% when inflation is at 8%? Obviously this isn’t next year type of stuff but end of decade possible imo. Not suggesting everything changes overnight or even anything goes away but not hard to create a solid argument that we are witnessing changes that people alive today have not seen before. It isn’t like the US hasn’t inflated debt away before so playbook is there. Problem is we aren’t the king of industry anymore.

There is no doubt that the deficit is unlikely to be reigned in by this milk toast Congress afraid of their own shadow willing to sell their constituents down the river at the behest of a foreign government that claims to be a proponent of the old testament.

It is funny how predictable this looks. Almost straight lines. Like the amount of MBS running of the Feds balance sheet. It is basically same for every month in the long run.

Makes me think of psychohistory in the Foundation by Isaac Asimov.

I mean, I’m not giving up my 2.875% anytime soon

I wouldn’t either. In fact, I resisted the urge to take a mortgage out on a property in 2021 just for the low rate. Oops. I won’t make that mistake again. The next time we have a pandemic and the Fed crushes rates to 0%, I’m borrowing!

I mean, you probably are happy in the house you have.

I’ve known multiple people who have given up their sub-3% rate because they’ve outgrown their 1,400 square foot starter home and don’t want to raise 2 kids in one.

Wolf,

Good stuff, as usual.

But how about the share of SFH that has *no* mortgage (paid off)?

When I looked into this 7 or 8 years ago, I think about 33% of the owner-occupied SFH market had no mortgage – so the “lock in” dynamics would be quite different for them.

About 40% of the homeowners have no mortgage. Quite a few people with money have been paying cash in recent years rather than paying 6-7% interest on a mortgage. If you have Treasuries and money market funds and don’t see good low-risk places to put that money, you might as well put that cash into your own home — and you can self-insure then, saves a ton on interest and insurance. You’d have to buy junk bonds to get that kind of return at a far higher risk.

No one should be self insuring.

See I think munger is wrong on this.

None of us are rich enough to self insure.

You would need $50 million to be in that ballpark.

Even then you’re going to need insurance to protect your $50 million, cuz everyone wants it. 🎯

Self insuring is a huge blind spot IMO

Sufferin,

Hmmm…I don’t get where you are getting $50 million from in order to “safely” self-insure.

1) Say I buy a used car for 10K.

2) Rather than pay $2500 per year for outside insurance…

3) I just “reserve” $10k in a safe interest-earning account to *completely* replace the used car if something catastrophic goes wrong.

4) By self-insuring, I

a) Save $2500 in annual insurance outlays,

b) Earn perhaps $500 in annual “reserve” account interest.

That seems like a 30% ROI by simply keeping $10k in “reserve” savings rather than paying an outside insurance agency.

Obviously, the more expensive the asset (like a house) the more difficult it is to accumulate the necessary “reserve” savings (although that is a good indication that people are spending way too much on risk-exposed assets…)

But, as a general principle, self-insuring (when and where possible) seems like a *very* sensible thing.

What am I missing?

Whether Auto or Homeowners, there’s the first party part and third party liability part.

Shiloh1,

Good point about potential injury liability exposure – I was primarily focused on asset replacement.

Still, I think the general principle holds – although likely at a lower ROI.

Liability coverage is more prudent – but would only be part of the (estimated) $2500 annual premium.

For pure asset replacement/repair, I think the initial layout of the dynamics still likely applies.

I own my home free and clear but it still costs me about $2,000/month when you look at property taxes, insurance, maintenance, utilities, etc. and it keeps getting more expensive every year.

From a purely conceited and greedy perspective, I see nothing wrong with a 2% mortgage.

😝

Or you could just be dumb like me and pay off your 3% mortgage rather than keep that amount invested.

I still believe that over the next two years, 2026-27, we will see a significant decrease in the Fed’s MBS holdings as those having a sub 4% mortgage run up against the IRS requirement that you reside in the home for 2 of the past 5 years in order to claim the one time capital gains exemption on sale of a home.

The Fed MBS roll-off is interesting.

The Fed is rolling off MBS but government controlled Fannie and Freddie are buying back almost as much as the Fed roll-off. The MBS market and mortgages shouldn’t be affected by the Fed roll-off while Fannie and Freddie are buying. That makes sense to me.

I haven’t seen Wolf comment on this yet. I’d like to hear his expert thoughts.

That was from a Bloomberg report on Dec 15. Below are excerpts from the report on Realtor.com on Dec 15. Note that Fannie and Freddie had $1.5 trillion in mortgages and MBS on their balance sheet before the financial crisis, and now it’s $234 billion.

Also note:

1. they cannot print money; they can only use their own capital (they’re very profitable) or borrowed money;

2. to increase their pile, they can retain mortgages and MBS instead of selling them to investors, and so their own holdings increase over time by holding on to mortgages and MBS.

Quoted from the article:

Since May, Fannie and Freddie have added more than $55 billion in mortgage principal balances to their combined holdings, an increase of more than 30%.

That’s taken their combined mortgage holdings to a whopping $234 billion, the highest in four years, and analysts tell Bloomberg, which first reported the move, that Fannie and Freddie’s holdings could expand an additional $100 billion next year….

The two companies, which have been under federal control since 2008, may be boosting their mortgage holdings in preparation for a public stock offering, a move that President Donald Trump has teased for months.

On the other hand, or additionally, the move could be aimed at engineering lower mortgage rates, another long-standing goal of the Trump administration.

…

The two companies inevitably hold some MBS on their balance sheets, whether as part of the pipeline prior to sales, or as a supplement to cash flow by collecting interest payments directly, instead of through guaranty fees paid by lenders.

Prior to 2008, Fannie and Freddie ballooned their combined holdings to more than $1.5 trillion as a way to juice earnings, by borrowing heavily at low interest rates and plowing the money into high-yield debt and increasingly risky assets.

That strategy backfired in the subprime mortgage crisis, which blew up their balance sheets with large valuation and credit losses, necessitating the federal bailout that landed Fannie and Freddie in conservatorship.

Under the strict rules of conservatorship, Fannie and Freddie were forced to shrink their retained portfolios and rebuild capital.

By the 2020s, both enterprises had much smaller retained portfolios relative to precrisis levels, but much larger outstanding guarantee books, reflecting a shift from leveraged investment companies toward capital‑constrained credit guarantors.

Now, however, growing their retained portfolios may help Fannie and Freddie juice their earnings before a public share offering, making them more attractive to potential investors.

“The move comes during a period when Fannie and Freddie are being considered for an IPO,” says Berner. “Expanding their income streams to include more direct interest payments could help them show off how profitable they could be under public ownership and attract investors.”

Meanwhile, Trump has also focused on lower mortgage rates as the centerpiece of his affordable housing agenda, meaning that easing rates may be a happy side effect of the balance sheet expansion.

Thank you, Wolf for providing more depth and clarity.

It was my original understanding that Fannie and Freddie were buying MBS at roughly the same rate of the Fed roll-off. That should lessen any impact on mortgage rates increasing.

Also, the Fed is not buying as many 10 year Treasury Bonds to replace the MBS roll-off and the Treasury is limiting 10 year bond offerings. There is less demand and supply for the 10 year. Will this suppress 10 year rates and thereby suppress mortgage rates?

Any bond vigilantes won’t have any leverage if the 10 year bond supply is low.

This all seems like a planned strategy to lower mortgage rates.

Thanks again!

Looks like we’re in for another 10 years of frozen housing, as the sub 4% mortgages decrease at a snail’s pace

Chunkymunky,

I 100% agree.

Also … inflated home and Condo prices.

MW: Stock market goes ballistic as Wall Street makes huge bet on Trump’s Venezuela raid

Donald Trump announced plans to take control of Venezuela’s oil industry and said American companies would revitalize it after capturing President Nicolás Maduro.

Buy gold( I know you will )!

Why would you buy for any amount more than $20 per pound?

Thank you again for this very interesting data, Wolf.

Your points on reasons why this is happening make sense to me anecdotally based on my co-workers and family.

1) A new job in a different city (I know a few that had been laid off and now are moving since WFH for new hires is more difficult. I couldn’t hire anyone remotely last year. They all had to be at corporate offices even though their field jobs were not there. Zoom was the answer to that.)

2) The Return To Office is slowly being implemented due to attrition. New hires to replace layoffs and retirements of senior people are all at corporate offices.

3) Sadly, about 50% of my co-workers are on their 2nd or 3rd marriage due to divorce which is the national average. Divorce is very expensive and typically involves selling the house at my age.

4) I noticed in the obits this week that more Boomers (1945-1950) are passing than the previous Silent Generation. 1950, 75 year olds still think they are young. 1945, 80 year old Boomers are starting to pass.

When safe Tbill rates are now 3.6%(about 2.7% after taxes), it doesn’t make as much financial sense to hold onto a 3% mortgage if you are retiring. Peace of Mind and cash flow become more critical.

I will likely to still hold the 3% mortgage even after the slight after-tax loss to see where long term rates go. Equities still make enough return but with much greater risk than just paying off the mortgage.

I am no longer TBilling and chilling.

I will just have to make sure I keep out enough cash for major expenses like a new roof. I’d hate to swap out a 3% mortgage and have to take out a 6-8% loan for a major expense.

I still think the Fed irresponsible low interest policy could be thought of as genius.

There are still 50+% of mortgage holders who are proud of their sub-4% mortgages and will likely not panic and walk away like they did in Housing Bubble I.

The Fed gave them meaning to stay as long as they can and not run causing another crash.

The Fed has so far avoided Great Recession II from their results of Housing Bubble II. The cost has been the current generation not being able to afford a house today. That will slowly go away without a devastating crash and recession.

Taking wealth from a lower wealth group and handing it to a higher wealth group does not help the economy. It hurts it. There is absolutely no genius there. Just stupidity.

Bobber, I 100% agree with you.

However, I’d argue a job loss recession like 2008 hurt the lower wealth group more than the higher wealth group. After the lower wealth group lost their jobs, foreclosed on homes, and cashed out their retirement stock accounts at lows to survive, the higher wealth group swooped in and bought the houses and stocks at steeply discounted prices, waited a few years, and sold at tremendous profits to become an even higher wealth group.

Recessions hurt everyone but mostly the lower wealth group who need jobs to survive. I was lucky to keep my job in 2008 with a 15% temporary pay cut, but not wealthy enough to buy at all-time lows. I treaded water while my unemployed peers dropped.

Controversially, I’d also argue that affordable housing and food are rights but owning a house is not.

This time, wage inflation and rent inflation have tracked closely. House imflation is out of whack.

From a long line of lower wealth group members, I recommended to my son to not buy a house, bitcoin, AI stocks until either wages go up more or prices become more sane.

That’s one slow unwind.

Less than 4% mortgages do the slow unwind. Just like the Edsel’s 3 year run that sold 84,000 units. Eventually like < 4% mortgages, they all faded from view.

Sorry, folks, I just couldn't resist the look back comparison.