Lower prices & lots of new supply. Deliveries & backlog rose. Profit margins, profits, & shares plunged.

By Wolf Richter for WOLF STREET.

Lennar, one of the largest homebuilders in the US – it targets the mass market and not the high end – is addressing the housing affordability crisis and the huge amount of new supply in the housing market in its own way as it keeps adding to supply and pushing sales volume, rather than cutting back. It is building more homes, but targeting lower price points, helped by a “decrease in construction costs, reflecting the Company’s continued focus on cost-saving initiatives,” and it’s selling more homes, but at much lower prices, including lower prices per square foot, and in doing so, is giving up an ever-larger slice of its profit margins and net profits that had gotten obscenely fat in 2021 and 2022 when free-money-besotted buyers were stepping all over each other to pay whatever. Now Lennar is cutting prices to where the newly sober buyers are.

In its earnings report yesterday evening for its fourth quarter, ended November 30, Lennar said that deliveries rose by 4% year-over-year to 23,034 homes and that the backlog rose by 18% to 20,018 homes, despite a litany of lamentations about the tough housing market, “constrained by affordability challenges, as well as weak consumer confidence.” Incentives needed to make those deals remained at 14% of revenues per home sold – “to address continued market declines,” as it said.

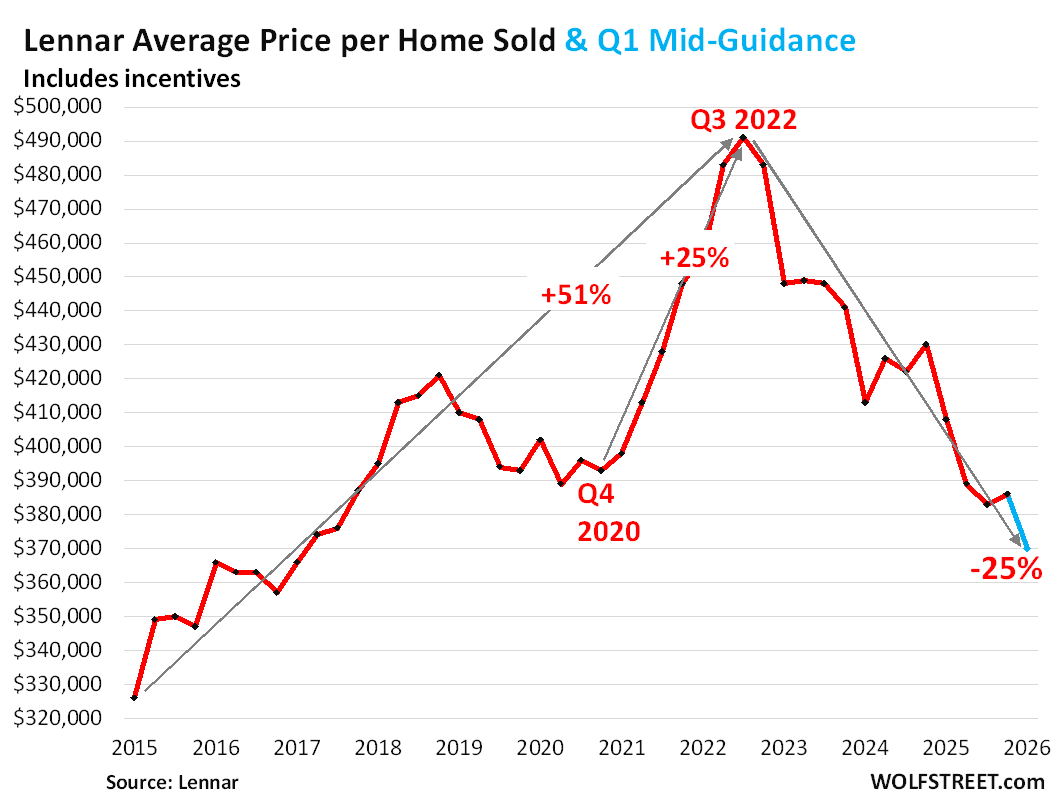

So the average sales price per home sold plunged by 10% year-over-year to $386,000. Lennar guided for an average sales price in Q1 2026 of $365,000 to $375,000. The mid-point ($370,000 blue in the chart) would be the lowest sales price since Q1 2017, and down by 25% from the peak in Q3 2022 ($491,000).

Lennar, like all big homebuilders, figures the cost of incentives and mortgage-rate buydowns into the average sales price per home sold.

The homebuilder is on the right track in terms of addressing the problems of this screwed-up housing market after the price explosion in the years through 2022.

“Lower revenue per square foot and higher land costs year over year” were largely responsible for the year-over-year decline in gross margin, “partially offset by a decrease in construction costs, reflecting the Company’s continued focus on cost-saving initiatives,” it said.

Its gross margin on home sales dropped to 17.0%, from 22.1% a year ago and from 28% in Q4 2021.

Lennar’s shrinking gross margins on home sales:

- Q4 2025: 17.0%

- Q4 2024: 22.1%

- Q4 2023: 24.2%

- Q4 2022: 24.8%

- Q4 2021: 28.0%

In its guidance for Q1 2026, it projects further declines in its gross margin to 15.0% to 16.0%.

Due to lower average sales prices, revenues from homebuilding fell 6.9% year-over-year despite the increase in deliveries – selling more homes at lower prices.

Operating earnings from homebuilding plunged by 52% year-over-year, net income plunged by 55%, and earnings per share plunged by 52%.

And its shares [LEN] have plunged by 39% from the peak in mid-October 2024, the moment when it finally dawned on the stock market that the housing market boom was cooked.

“Even as interest rates moved slightly lower in our fourth quarter, the overall market remained challenged,” it said.

“Even as market conditions softened, we prioritized providing supply for a healthier housing market, while driving down costs to support affordability. Our strategy remains consistent and clear: maintain volume, adapt to evolving conditions, reduce costs, and support housing affordability,” the report said.

Homeowners who want to sell their homes are losing buyers to the homebuilders, especially in markets with lots of new construction. Sales of new single-family homes have held up, even as sales of existing homes have plunged by 25% or more.

In case you missed it: The Most Splendid Housing Bubbles in America: Price Drops & Gains in 33 Large Expensive Metros in November 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

May be they just built smaller homes. Should be price / sqft

1. Read the article more carefully: Per square-foot prices dropped again (first paragraph and further down).

2. No, should not be per square foot because people buy a home with a price and a mortgage payment, not per square foot.

Wolf, there’s something not right here.

If you check out Lennar’s web site, you’ll see for instance Woodstock Plan 4055 in Surprise AZ to be around 370K. This is a 1250sqft house on a 4800sqft lot. That’s a representative home in an “up and coming” areas in the Valley, like Surprise, meaning the best deal you can find in Phoenix area.

Around 2021 for this price you could have bought about 2400sqft house on a lot at least 7000sqft. I know, I’ve bought and sold some at that time in the same area.

For a family looking for shelter, these prices are catastrophically high. It’s hard to imagine (though not impossible) a family looking seriously at 1250sqft. I’ve toured these homes. There’s no living room to speak of. Tiny, tiny. That’s more of a condo square footage packed into a “house”. 2400 sqft on the other hand is a nice home.

I am looking at this chart you have, and it’s just not reflecting reality the way a typical buyer would see it. This chart shows optimism, but that’s not the reality out there. Kind of like Trump’s speech tonight, or as they say where I’m from “all hat and no cattle”. Just my 2/100.

1. Read the article. READ IT. Don’t just look at the pictures. Average sales price includes all incentives and discounts, including mortgage rate buydowns. You don’t see that in an example house.

2. An up-and-coming area of Phoenix is not a representative area for Lennar’s nationwide business. Phoenix is much more expensive than most other markets where Lennar is active, such as the suburbs in Texas and Florida, and in the South. Phoenix is the “West.” Lennar’s average sales price in the West is nearly $600,000. These are Lennar’s average sales prices by region:

East: $359,000

Central: $361,000

South Central: $224,000

West: $596,000

Other: $611,000

3. anecdotal stuff — like “this one house I’m looking at”– is always BS.

Amusing how people and perceptions change over time. 1250 sq/ ft is considered tiny, tiny now.

I raised my family in a 1400 sq/ft 1957 year home, 3 bed 2 bath, that I remodeled in the early 2000’s.

In 1957 it was considered large for the time and the location.

It was not huge by any means, but not tiny, tiny, and definitely more than comfortable enough for a family of 4.

Definitely a house affordability problem, don’t get me wrong.

But some people may need to also lower their expectations to meet their own reality. Don’t have a champagne appetite on a beer budget.

“2400 sqft on the other hand is a nice home”

ehhhh…from the late 1940’s through the 90’s plenty of 2/3/4 person American families were perfectly content with 1250-1750 sf homes.

2400 sf on the other hand, starts edging into the lower-end McMansions for McMorons territory – only made possible/juiced up because the depredations of ZIRP (brought to you by the Geniuses of the Fed -TM) expropriated basically 20 years of savers in order to slice mtg rates in half.

2400 sf for 2 people?

For the 2.2 member families of today?

4 and 5 member families of the 50’s, 60’s, and 70’s were perfectly fine with 1500-1750 sf homes.

It was only due to the money-manipulating Fed turning the housing market into a speculative casino (with complementary psychotic booms and busts) that created the 2500 sf “normal house.

And thanks to special-interest infected zoning laws, that 2500 sf house is *required* to have a *much* bigger lot than the plain old 1500-1750 sf’er – greatly restricting the supply/growth in supply of new homes – further juicing the SFH speculative frenzy/frenzies.

We’re been through 2-3 very destructive rounds of Fed-abetted housing speculation/stupidity – and some people are pushing for round 4.

Houses have been getting smaller by 1.25%/year for a dozen years. So perhaps a 5% drop in the last 4 years is due to a smaller house is valid, but it certainly does not explain a 25% drop.

we’d love to get smaller newer home(ours is ’68 just 2,700sf)

but we can’t walk our 3.35% loan over(10 years left)

so we’ll stay

looking at foreclosure’s but they haven’t repriced quite enough

need couple more rentals

raising cash via cash flow

I diverge from Wolf in thinking this is still valuable to think about, but it still aligns with the point of the article. You can run this calculation on FRED yourself using:

Median Sales Price for New Houses Sold in the United States (MSPNHSUS)

and

New Privately Owned Housing Completions in the United States, Average Square Feet of Floor Area for One-Family Units (COMPSFLAA1FQ)

to get the $/sq foot in of houses sold and completions (not entirely apples to apples, not all completions are sales in the same time period). But we commenters love our hand-waiving!

If you do this, you’ll see that while this shot up during the early post-covid boom, it has reversed and *decreased* 2022-and-on as buyers pulled back. Remember this is *before* all the incentives that Wolf details that just further decrease this $/sq ft in terms of what Lennar is actually getting.

So in aggregate new houses are getting smaller [Wolf has pointed this out, it crested in the 2010’s], but they’re also getting more-than-correspondingly-cheaper in aggregate across the country. It’s the only lever homebuilders have to pull to steal buyers from existing homes!

The Census figure for new home prices that you cite:

1. does NOT include incentives and mortgage rate buydowns — I’ve discussed this here a million times. In Lennar’s case, that’s 14% of revenues per home sold (see article).

2. represents contract signings, and does not net out cancellations. So contracts that later get canceled are still included. This was a huge problem when lots of high-priced contracts were canceled in late 2022, but stayed in the Census figures, thereby inflating them. And then Census later made a huge adjustment, knocking down a big part of the price increase it had shown, and reducing the price declines since then.

So the median sales price per Census is not meaningful.

3. the square foot data of completed homes you cite:

— actually ROSE (to 2,386 sf), from the low point in Q2 2024 (2,326 sf)

— had dropped from the high in Q2 2015 (2,698 sf) to the low in Q2 2024 (2,326).

Does Lennar’s key markets align with the markets that have seen the largest drops in prices, like Austin and the Sun Belt generally?

Looks like Lennar’s gross margin ranged between 11-14% through the 2010s. Is that where we should expect to see it fall to before calling the housing deflation largely over, or will it overshoot into the single digits like after the housing bust?

“Looks like Lennar’s gross margin ranged between 11-14% through the 2010s.”

No, you’re looking at “operating margin” = “gross margin” minus “S,G&A expenses” (Selling, General, & Administrative expenses)

“Gross margin”:

2014: 25.4%

2013: 24.9%

2012: 22.7%

search for “gross margin” until you get to the table with it:

https://www.sec.gov/Archives/edgar/data/920760/000162828015000218/len-20141130x10k.htm

Wolf: Just one more example of why I LOVE Wolfstreet, and send you at least a century every year to support your work.

I cannot remember how many folx, good hard working folx to be sure, that I have had to explain the sometime VAST delta between ”gross” and ”net” or even ”triple net.”

Many of these people should really have known better, but they clearly did not,,, and some of them could not make the mental adjustment between, ”We made a million dollars last year,,, And the hard fact that they actually made less than 10% of that after ALL expenses.”

Keep on keeping on Wolf, and may the chips and profits fall where they do.

Thanks for pointing me in the right direction.

Wolf, can I hire you to explain Gross Margin vs EBIT vs EBITDA at my company? I need full on RTGDFA Wolf to come out during our quarterly update meetings. I will pay you with some excellent beer.

🤣❤️

Where I live in the PNW new home builders are building townhomes at the cheaper price because the law allows it. Houses are still selling here but slower than before. Yes, down 5% off the top. Houses they sell are still way out in the boonies where land value is lower.

Something I am seeing in the southeast. First buying large tracts of land just a few miles out from the edge of mature suburbs presumably for lower land costs. In unincorporated areas with fewer rules and regulations. Then building small communities sometimes mixed with duplexes or quadplexes for lowered costs. Not very fancy, just all in all trimming a little expense off to sell at lower prices.

“Not very fancy”

Which is all to the good.

“Very fancy” McMansions (“Empowered by ZIRP”) brought us the 2008 implosion and the Pandemic Dope Bubble.

You can’t have median housing prices triple or quadruple over the same 20-25 years that median salaries have only (maybe) gone up 1.75 to 2 times (and that is with ZIRP-meth being mainlined into the economy).

I took a peek at the release to see if I could find some version of “completed, unsold inventory” but it eluded me.

I did however note that net margins are now around 9-10% and guidance is for around 5% for 2026. That’s not a lot of wiggle room. If input prices or interest rates move up a hair or demand contracts further, I wonder if they’ll continue pumping out supply at a loss or pause their building.

“That’s not a lot of wiggle room.”

Hmm.

Somehow these builders were magically able to construct $150k starter homes in 2002.

Then, apparently, 20 years of ZIRP caused this knoweldge to be lost to the memory of Man, “requiring” the $400k starter home.

I would venture a guess that ZIRP-exploitation played a pretty damn big role in determining the “possible” in terms of actual construction costs.

I hope other builders follow this.

Home ownership is a complex human engagement summed up into a couple of words,

Home builder stocks still trading many times pre COVID prices..wonder how long that can last!

Not long, sell the rally today at SPY $679.3 or right now at least that how the ALGO has previously acted.

We are seeing condo products coming back to life where I live in the city. Very slowly but interesting to see as that is perhaps a better option than apartment living and perhaps for some that don’t want to live in the ex-burbs just to buy a slab track home.

See HOA fees.

The ‘the average price per house sold’ graph shows ….2018,2029,2020….. on the x axis. Noting it just so you are aware of it.

The price of building materials since 2017 has doubled to quadrupled in price. Everyone points to lumber, as if that’s all a house is built with, but look at the price of windows, doors, siding, decking, shingles, cabinets, flashing and aluminum coil, romex wire, propress fittings, etc… not to mention the rising cost of labor.

I guess what I’m saying is, with the devalued dollar/inflated price of labor + materials, a $360k home built in 2017 can’t possibly be equivalent to a $360k home built in 2025/2026. Is there a “Home Quality Index” that measures or standardizes a baseline for home quality?

People always get confused with inflation and price of building homes.

What matters most is how much people afford when it comes to home prices and nothing else.

It would be interesting to see where those cost reductions came from. As a contractor, i haven’t seen that much deterioration in raw material cost. Most suppliers continue to increase prices, some are double-digit whether it’s justified or not. They recognize that higher prices are the easiet way to pump profitability. It seems possible Lennar’s overall lower average selling prices may be sales mix into cheaper markets.

“It seems possible Lennar’s overall lower average selling prices may be sales mix into cheaper markets.”

Don’t make up stuff. The article TOLD you why overall selling prices are lower:

First paragraph: …“decrease in construction costs, reflecting the Company’s continued focus on cost-saving initiatives”

Further down: ““Lower revenue per square foot and higher land costs year over year” were largely responsible for the year-over-year decline in gross margin, “partially offset by a decrease in construction costs, reflecting the Company’s continued focus on cost-saving initiatives,” it said.”

Nothing about a shift to cheaper markets.

I’d assume a bifurcation in that market. With little demand for construction, prices for all building products should see a lot of downward pressure. I’d expect to see that on the wholesale market where Lennar buys. On the other hand, with people not moving, there ought to be more DIY work and owner upgrades, keeping prices up on the retail market.

“The price of building materials since 2017 has doubled to quadrupled in price.”

Only during the worst of the Pandemic bubble…those prices have substantially fallen since then. Among many other speculative evils, ZIRP engorged commodity speculation – including in lumber.

And those building material prices have historically been influenced by the ZIRP-empowered highway robbery pricing that builders have gotten away with since 2002 – if some builder has been able to ZIRP-goose *his* pricing by 200% there is no way in hell his suppliers weren’t going to try and get *their* cut of that lucre.

Then the builder and the suppliers blame each other for the “impossibility” of building a starter home for less than $400k, when America was plastered with $150k starters in 2002 (pre ZIRP).

Apparently the American SFH market from 1950-2002 was some sort of unrepeatable miracle (and “Pay No Attention to that ZIRP Behind the Curtain!!”)

Apparently the knowledge of how to build cheaper homes (smaller, simpler houses with basic finishes) has been erased from the Memory of Mankind by ZIRP.

This company realizes that those old margins are history, they were a fluke.

Accept reality or be left behind by those who do.

Lennar building 2527 sq.ft ranch home in 80016 area code for $935,000. 4 Bd 3bath 3 car garage. I bought my first ever Lennar home Nov/2014 for $335,000 4bd 3.5 bath, 3 car garage (2400 sq.ft) 2 story. The wife now wants the new Lennar ranch home and the $600k of inflation that comes with it. I will say that Lennar builds a good home, as it has withstood to 80-90 mph wind gust the past 11 years here at the beginning of the eastern plains. 15 miles SW of Denver airport. I have noticed continued price drops in the more affluent 55 and over golf course communities nearby existing homes, but none beating Lennar pricing. Buyers facing that new car vs old car conundrum. After seeing my homeowners insurance renewal go from $2800 to $5800 last month and never filing a claim in 11 years. I think the fix is in. 166% increase. I might as well be living in Boulder, CO. Property Taxes and Insurance are the silent killers in this market.

“Property Taxes and Insurance are the silent killers in this market.”

Sure…but they are based off the SFH purchase price too.

So if anybody willing goes from paying 335K to 935k in a decade (when median salaries have *maybe* gone up 1.3 to 1.5 times..,maybe), then the property tax/insurance rogering is kinda among the lesser problems.

Less than 25 years ago, million dollar homes (outside of CA/NY) were mainly the province of rich celebrities.

25 years of ZIRP brainwashed too many people into thinking that crazy levels of housing inflation were remotely “normal”.

The next 5-10 years for single family ownership will be interesting. More and more people are renting (even with this concessionary environment) and build-to-rent is becoming more and more popular due to affordability issues and renters by choice.

Hell, I’d consider renting a good house from a national landlord if I had the choice.

“Its gross margin on home sales dropped to 17.0%, from 22.1% a year ago and from 28% in Q4 2021.”

Guess what their overall gross margin was from 2014-2018? About 12-15%.

I’m not sure what it was purely from home sales, but probably not much higher. It’s overall gross margin peaked at 22.34%. So these fat little suckling piggies aren’t making a shit ton anymore, just a nice ton.

No, you’re looking at “operating margin” = “gross margin” minus “S,G&A expenses” (Selling, General, & Administrative expenses)

“Gross margin”:

2014: 25.4%

2013: 24.9%

2012: 22.7%

search for “gross margin” until you get to the table with it:

https://www.sec.gov/Archives/edgar/data/920760/000162828015000218/len-20141130x10k.htm

ah thanks wolf! I appreciate it.

Pretty handy for LEN that when they need to sell a house for less, they make a house for less. Takes a forced sale to get regular people to be ok selling for less. Maybe being greedy and bidding up to buy places for short-term rentals during everyone’s revenge travel phase was only meant to be a short-term thing

14% of $386K is $54,040 to incentivize buyers with rate buydowns, seller provided payments to a buyer’s agent and probably closing costs assistance. 17% of 386K is $65,620 which should exclude seller’s marketing payment to an agent, correct?

When added together, that’s more than $119K, so I would say there’s a whole lot of downward price movement still needed. To me, the question is when does the money available for massive incentives go away and where are rates at that moment?

At what point do companies pack up? This might be what the housing market needs but there is likely a minimum margin needed for the effort of running such a business. I’m guessing 17% is still well above that level but it would be need to be more than 7%.

Lennar is still profitable.

There are lots of companies that are not profitable, many of them for years, no problem.