The bond market faces the duo of Inflation and Supply.

By Wolf Richter for WOLF STREET.

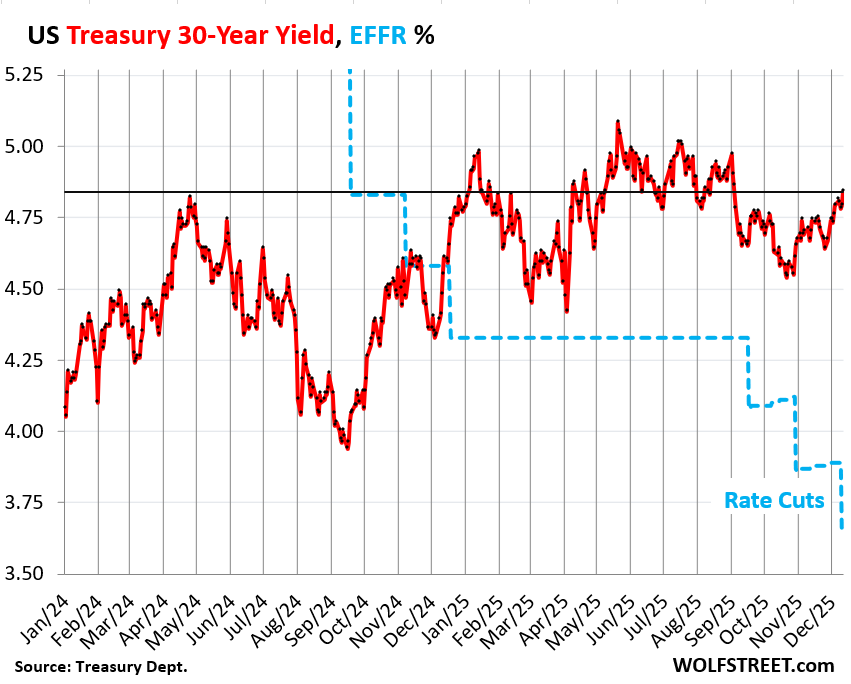

The 30-year Treasury yield has risen by 19 basis points since September 16, while the Fed cut interest rates by 75 basis points. It closed on Friday at 4.84%, while the Effective Federal Funds rate (EFFR), which the Fed targets with its policy rates, has dropped by 75 basis points (blue in the chart).

The spread between the 30-year Treasury yield and the EFFR has now reached 120 basis points. Since October 2023, the 30-year yield has pierced the 5%-line several times.

The 30-year Treasury yield reacts to bond-market issues, such as expectations of future inflation and expectations of supply of new bonds that have to be absorbed; it is not particularly influenced by the Fed’s short-term policy rates.

But the short-term yields react to the Fed’s current and expected future policy rates. And those yields have dropped roughly along with the Fed’s rate cuts. With long-term yields rising and short-term yields falling, the yield curve steepened sharply over this period and has almost uninverted.

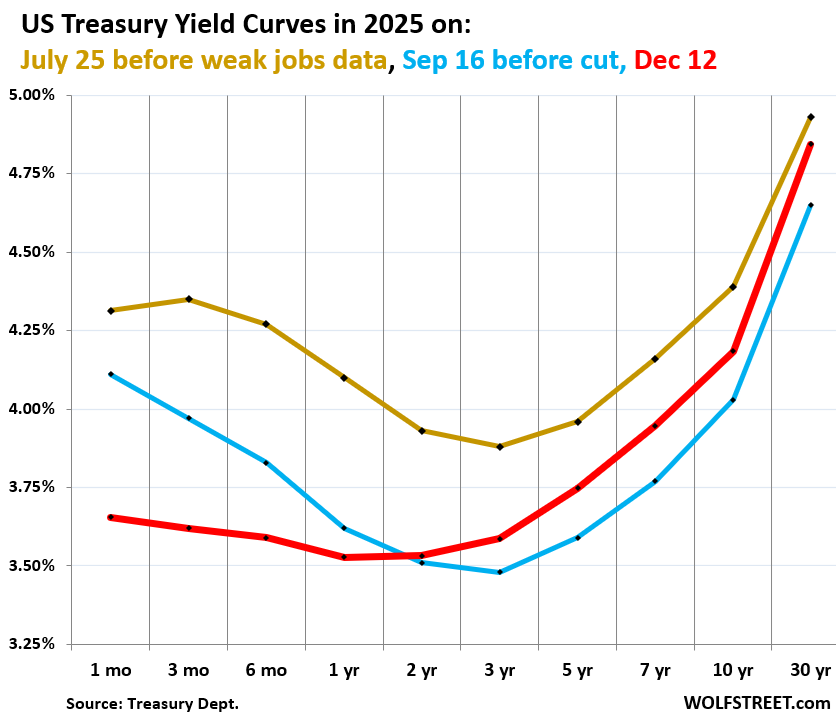

Treasury yields from 1 month to 6 months are right at or a little above 3.60%, with the 1-month yield at 3.66% and the 6-month yield at 3.59%

But there is still this sag in the middle, if barely, formed by the 1-year yield (3.53%) and the 2-year yield (3.53%) marking the lowest part of the yield curve. And then yields rise from there.

The yield curve has sharply steepened since September 16, just before the Fed’s first rate cut.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates in 2025:

- Red: Friday, December 12.

- Blue: September 16, just before the Fed’s first rate cut in 2025.

- Gold: July 25, before the labor market data turned sour.

You can see how everything from the 2-year yield and longer has risen since that September rate cut, defying hopes and predictions that long-term rates, including mortgage rates, would decline when the Fed cuts its policy rates:

And they rose for several very solid reasons: fears of future inflation, and fears of future supply that the market will have to absorb.

The 1-month yield (3.66%) is bracketed by the Fed’s policy rates (3.50%-3.75 % since the December rate cut) and closely tracks the EFFR (3.64%), and it was pushed down in line with the 75 basis points in rate cuts since mid-September. The 3-month through 1-year yields were also pushed down by the rate cuts, but less so, with the three-month yield still dropping substantially, and the 1-year yield barely.

Every yield from 2 years on up has risen since the 75 basis points in rate cuts:

But the yield curve is still inverted in the 3-month through 3-year range, with those yields being lower than the 1-month yield. That’s the sag in the middle. But it has become shallow, and almost straightened out, from the deep trench it had formed previously.

This now shallow sag in the middle shows that the bond market has walked back expectations of rate cuts next year.

The bond market faces a problem: The Fed cut rates three times this year while inflation has accelerated. CPI inflation, when last measured, was 3.0%, which was the September reading. And the only reason it wasn’t higher was the outlier plunge in Owners Equivalent of Rent (OER), the largest CPI component, weighing 26% in overall CPI, 33% in core CPI, and 44% in core services CPI (my analysis is here). Something went awry, but CPI was cobbled together by hastily recalled staff during the shutdown, and that was that.

Cutting interest rates in this inflationary environment can spook the bond market. It’s already worried about the onslaught of new supply of Treasury securities to fund the ballooning government deficits. And it fears a lackadaisical Fed when inflation is out of the bottle.

Inflation destroys the purchasing power of long-term bonds; and the yield has to be high enough to compensate investors for this destruction of purchasing power, and for the other risks investors are taking.

Inflation is not to be trifled with. It’s not just the bond market where yields can blow out; it’s consumers and voters. They hate inflation, and they hate high prices, and they express their feelings about inflation at the polls.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“….fears of future inflation….”

And for good reason. They are stoking inflation now instead of fighting it.

“Deflation is to rich people what inflation is to everybody else.”

We badly need deflation. MASSIVE deflation. We need a wipeout of 80%+ in the wealth of all these billionaire a-holes.

BUY TIPS!

Buy TIPS & I bonds .

Right on Depth Charge.

Mr. Trump will hire a Fed Chairman who will follow his orders to get “interest rates back down to 1 percent or lower.

Maybe. But the Bond Vigilantes may arise as they did in the late 70s into the early 80s. Gold is speaking. Is anybody listening?

Happy Holidays.

B

I agree that if they succeed in forcing down rates that much, we will see a return of the bond vigilantes. I don’t know what they are thinking – the last thing anyone should want is a reprise of 1980-81, but with the idiocy of recent years it looks more likely now.

I’d take a stable money supply

A. We need people that know the difference between the supply of money & the supply of loan funds.

B. know the difference between means-of-payment money & liquid assets.

C. know the difference between financial intermediaries & money creating institutions.

D. that recognizes that interest rates are the price of loan-funds, not the price of money

E. that recognizes that the price of money is represented by the various price (indices) level.

F. that realizes that inflation is the most important factor determining interest rates, operating as it does through both the demand for and the supply of loan-funds.

“inflation is the most important factor determining interest rates,”

Disagree. It’s the Federal Reserve.

Inflation went to 9%, did interest rates go there?

BECAUSE THE FED STILL DID QE (buying long-term bonds and MBS) WHICH FURTHER ACCELERATED INFLATION TO 9%. QE has been finished since early 2022.

But didnt the Fed suppress interest rates with QE?

Yes they did control the rates…and still do. IMO

Spencer,

You would make a great Fed chair.

The inflation is killing us & must stop. I no longer know what groceries are supposed to cost.

“Deflation is to rich people what inflation is to everybody else.”

1) Perhaps. In general, I think it might be more accurate to say that deflation does in *leveraged speculators* – who would have to repay their (frequently ill-considered) loans with *more expensive* dollars under deflation.

2) That said, it is a bit hard to see why the hell the US government has seen fit to hew almost everything to the interests of leveraged speculators for 20 years (the long night of ZIRP – those obscene 2002 and 2012 and 2022 MSM “news” pieces about how deflation – notwithstanding the history of, say, computers – is somehow the devil incarnate beyond question).

3) My guess is the half-wits at the Fed would say that “leveraged speculation” is essentially the equivalent of “growth” – “any borrowing is good borrowing so they took what they could get, yes they took what they could get – and you ain’t seen nothing yet.”

4) Per #3, somehow 25 years of economic derangement has failed to penetrate the “big dome” skulls at the Fed with the insight that they have funded a sh*t-ton more secondary-market speculation than primary-market asset creation (see, housing inflation and housing production shortfalls). Of course, this only could have been discovered by, say…2004.

Cas127, that’s a great post. I think it’s going to take someone with common sense, and more importantly, huge ba**s, to turn things around. We can hope.

Massive deflation and I keep my job and my pay stays the same? That sounds dreamy, but when has that ever happened?

1930s. My grandfather, and it was dreamy. His family lived quite well.

I think both sides of the aisle would agree with you.

Yep, and now the Fed is starting to expand the balance sheet. 40 billion already in the works. Look for inflation to return to Biden levels. The next Fed chief will be a sock puppet.

The 5 yr inflation expectation is about 2.2%, according to FRED, leading to a question of what the expectation of the expectation number will be when next measured.

Higher, I’d wager…

5 year inflation expectations are measured daily. It’s the yield on the 5-year Treasury less the yield on the 5-year TIPS. FRED has that data too.

For anyone in the upper income tax brackets, the real return on any Treasury or TIPS is negative after taxes and inflation. This is one source of the current speculative fever in the stock and gold markets.

This right here! If I own any type of gov’t bond, I’ll lose purchasing power.

Although a steeper yield curve reflects heigtened inflation expectations and budget defecit concerns, I think it’s a healthy development financial markets. It means bonds are now a viable asset class. For serveral years when even long duration bonds were yielding close to nothing, they didn’t make sense as an alternative to other asset classes.

I agree. These low-yielding bonds before 2022 were just another distortion from QE.

QE and Operation twist made Bond prices distorted for long period 2008-2022. Now they are market driven upto certain extent. Slowing and Stopping QT stabilized them I feel. Otherwise we would have seen 6-8% on 30 yr by now.

As of now FED is still holding large % in Long term compare to Treasury issuance. If FED would have invested all excess roll over into T-Bills during QT time, we would have much higher rates on Long term.

The Fed doesn’t want 30Y rates anywhere near 6-8%. If they get that high, something is on the verge of breaking.

“The Fed doesn’t want 30Y rates anywhere near 6-8%. If they get that high, something is on the verge of breaking.”

Care to elaborate on what would be affected (and how) by an 8% 30y beyond vague references to “something breaking” ?

Isn’t margin investing influenced by short term rates? Doesn’t this just incentivize more margin investing and a high risk profile for the country (shifting to short term purchases to lower debt servicing for the government is all gravy minus the whole increased re-investment risk).

If you’re margin investing with a Shiller PE over 40, good luck to you!

May the melt up be with you. Haha

^^^^ Exactly. But I question how many people will understand what you wrote… or accept it even if they understand it. Hubris is the rule of the day.

You can live pretty good for lucky people who have 5 million in bonds at 4 to 5%.

Unsustaable.

“Deflation is to rich people what inflation is to everybody else.”

Dispersed costs to many (inflation) for the concentrated benefit of a few (asset holders)

BTW, who has ever seen deflation? Disinflation would be welcomed. And a touch of deflation also.

We are told cutting rates is to help main street and the economy. Yet inflation steals the value of saved money, saved from previous labor. Does that help “main street”?

But the powers point to a 4.4% unemployment number as reason to cut, but actually to just keep the market “party” going.

One can expect more Fed purchases if the yield curve gets out of their control, and it will be justified so as to accommodate an expanding economy. But if the economy is expanding, why the rate cuts?

The powers seem to seek higher and higher markets to accrue political benefit. Yet as they do, the societal bifurcation will expand. Recent elections indicate such.

r/e prices in my hood in phoenix deflated about 70% from top in 2006 to 2011 roughly. that was great for me, as i was long metals and bought properties in 2011 and 2012 with 20% caprates. no debt needed to purchase. i also was clearing all my trades with bear stearns and sold bear stearns stock at the high in summer of 2007 when their mortgage funds started smoking from the toxic waste. my family profited in great depression in the early 1900s. PS. we aren’t ruthless. i helped many homeless and out of work neighbors……..as did my grandparents……

Question is has the Fed been able to navigate a soft landing and is the bond market an indicator of midterm or does midterms even matter in a 30 year outlook.

Inflation sure makes the deficit look smaller as a percentage of GDP.

Tariffs are making an impact on the economy with reduced demand from government for the deficit spending which should keep longer term rates lower and asset prices higher and I think inflation lower. Manufacturing returning to the USA is happening . Looks to me as if we are headed in the right direction if we can just get our inflation headed lower not higher in the 2 percent target rate range.

Massive LNG buildout and increased NG production should really help GDP. Wolf’s analysis of the energy export market and future LNG exports would help. Have not seen that update for awhile .

Texas legislature and ERCOT in 2025 have approved expansion of the Texas High Voltage grid with a planned doubling of ERCOTs ability to transport electricity efficiently throughout the state . Which implies a doubling of the power generation capacity from power stations. Power demand is a key component to driving increased manufacturing and consumption .

I don’t see deflation happening when we have large manufacturing buildouts ongoing . All of these major public and private industrial expansions need to be financed which will bring more demand for the longer end of the yield curve.

Higher yields should bring about lower inflation . Rates appear to be headed higher. This data presentation supports the notion of higher long term rates and I think the 30 year rate has a 10 percent change of exceeding 5.5 percent next year. Check out the 2025 ERCOT power expansion approvals.

All were needed to accommodate the approvals of LNG export permits that had been put on hold in 2024.

“Wolf’s analysis of the energy export market and future LNG exports would help. Have not seen that update for awhile”

Thanks. I do these annually, with the annual data (less volatile than the monthly stuff), which the EIA releases at the end of February. So in about 2.5 months, it will come. Here is the last one from March 2, 2025:

https://wolfstreet.com/2025/03/02/drill-baby-drill-for-20-years-us-natural-gas-production-and-exports-via-lng-pipeline-rose-to-new-records-in-2024/

“… has the Fed been able to navigate a soft landing..”

Soft landing? How many years has that been talked about. Look, over there….Big Foot!

There has been no “landing” of any type.

“Check out the 2025 ERCOT power expansion approvals.” Yes, lets check them out. These are approvals for power usage from AI centers, not for new generating capacity:

“More than 220 gigawatts of big AI projects have asked to connect to the Texas electric grid by 2030. That’s more than twice the Lone Star State’s record peak summer demand this year of around 85 gigawatts, and it’s total available power generation capacity for the season of around 103 gigawatts”

“The number of big AI projects requesting a connection has nearly quadrupled this year”

Nothing to see here folks. It is absolutely NOT a bubble! Right?

What could possibly go wrong?

If this ever comes to pass, it will be great news for natural gas producers in Texas and nearby states.

Texas has an effectively infinite supply of natural gas. Time for E&P companies to start focusing on the high gas/oil ratio wells they’ve been ignoring.

The moving average for bonds is now higher and higher all next year.

Madness….just madness. As I told everyone two years ago…..buy yellow metal. Buy silver metal.

Best advice today….same only 2x.

The crazies have taken over and are lowering rates in spite of deficits exploding.

The AI crowd is slowly starting to understand the money they are expending will never be profitable….much less paid back.

Protect yourself. TIPS are OK if you believe and trust the calculation of the CPI in the hands of the very crowd that lead you here.

Fiat currencies are just credit…. money is yellow.

All the modern monetary nonsense will never change that.

I will say the new solid state batteries that will use a fair amount of silver seems to have helped push up the prices,stacked for a long time but ads always would be happy to see me metal values go down if we could have fiscal sanity……..,one can dream.

I of course agree with respect to gold. While it may currently be “overvalued” (if you believe in charts, which I do, as they prophesied the price downturn after a run up for nine consecutive weeks) it is also very much “under-owned”.

Consider just one item: At least three Asian countries have recently allowed their insurance companies to allocate up to 5% of their assets to gold, up from 0%.

For more reasons go to Kitco for both gold and silver.

Isn’t it interesting to watch people fire sell crypto to buy gold?

This isn’t a “fire sale” for crypto. So far it’s a routine dip. Maybe an asset-class rotation.

Actual Fire Sales occur when people need to sell All Their Investments to stay solvent.

And at that point, they aren’t using the proceeds to “buy gold”, they are scrambling just to cover debts.

Social Security COLA for 2025: 2.5%. Social Security COLA for 2026: 2.8%. Nuff said.

It’s a bizarre economic paradox: while the Social Security Administration confirms the annual Cost-of-Living Adjustment (COLA) continues to increase benefits for current recipients, the government simultaneously warns that the trust fund will be depleted, requiring reduced payouts in just over a decade. It feels like we are collectively accelerating the car towards the stop sign: we’re boosting the benefits right now, even while acknowledging that the long-term system is heading toward an inevitable reduction of payments

Do you really believe that recalculating a payment to counterbalance the decline in value of the currency it’s paid in is “boosting the benefits”?

My parents will be happy to hear that they’ll be able to buy a lot more stuff with their “boosted benefits”. Of course a big chunk of that is being redirected to inflation-adjusted Medicare premiums before it even touches their bank account. I guess the government giveth and the government taketh away.

“Mongo only pawn in game of life.”

^Not only that – how much of that COLA is going right out the door from increased property taxes?

“Back to1% or lower”

At that point will the dollar be just below the rupee or just above the paso ?

I’ve gone full in on the Argentinian Peso.

Nice one.

Now built on a foundation that is a USD 20 billlion currency swap from the US Treasury.

It’s turtles all the way down.

In that scenario real turmoil wouldn’t be from the dollar dropping in forex markets – it would be a failed treasury auction.

Usually if the dollar goes down so do the rupee, peso and everything else.

All the global currencies are intertwined. None of the big-enough ones ever fall too far out of line. Plenty of recorded historical documents showing how central banks juggled local rates to keep the equilibrium.

One mainstream account of the Great Depression says it was triggered in part by the Federal Reserve lowering rates to aid France, a policy error resulting in excess borrowing and speculation in the U.S. Credit Bubble followed by inevitable bust. But maybe the motivation was different, say the 1928 election, or something else.

One wonders whether the current U.S. rate-lowering might be similarly motivated, with similar consequences?? At this point it hardly maters, the speculative balloon is just waiting for a pin.

Hey Wolf,

The “(my analysis is here)” link at “Owners Equivalent of Rent (OER), the largest CPI component, weighing 26% in overall CPI, 33% in core CPI, and 44% in core services CPI (my analysis is here)” is returning a 404

Thanks, fixed.

Here is the link:

https://wolfstreet.com/2025/10/24/massive-outlier-in-owners-equivalent-of-rent-pushed-down-cpi-core-cpi-core-services-cpi-something-went-awry-at-the-bls/

Will unemployment rate be revised lower last month and come in lower than expected tomorrow? Inflation higher than expected later in the week. That combination will equal neutering the Fed from keeping the bubbles intact and being team Risk On.. I read in Barrons or

WSJ 1.71 trillion of imports were carved out from receiving any Tarrifs. So half of all imports coming in have zero tariffs, no wonder tariffs hasn’t played a big role in inflation data yet. Today 2Yr/10Yr Spread are .68 that’s a high going back a couple of years. Party hats for all the earnings growth coming? I don’t think so. Happy Hanukkah for those who are lighting candles. :)

I don’t think the Fed is going to do QE again. They’re moving towards pre-2008 balance sheet management.

Medium and long-term yields are still far too low to compensate for the risk. Who’s buying these things?

Agree. Not touching 10-yr below 5%.

When it hits 5%, what causes it to rise to that level will make you not want to take it at that rate either. It’s always going to look expensive on a risk-adjusted basis.

2% term premium for a 10y is totally normal. For whatever reason (carry trades and “free money”??) people haven’t accepted 3% inflation will dominate the majority of the next decade. That’s fine, I can get similar real returns at a similar risk profile elsewhere.

I think the answer is twofold:

1) the Ex-US economy is growing even faster than the US, and that creates demand for US dollars as the somehow-still reserve currency, and all those dollars create demand for treasuries.

2) Hourly wages have been growing faster than inflation for a couple of years now. Drunken sailors are spending much of it, but some of those wages go into treasuries via the 401k plans of fearful workers and the banking system.

These factors are pushing yields down even before we talk about the government’s operations.

What did these countries have in common and what was the outcome?

The Weimar Republic

The Nationalist Government of China

Yugoslavia (early 1990s)

Zimbabwe (late 2000s)

Venezuela (2010s-present)

USA please beware.

Ryan

You forgot to add in Austria Hungary, Wolf’s home country.

Ahhh yes correct. I guess that almost every country has suffered the effects of inflation, the worst resulted in regime change

Trump’s support for a loose money policy at the Fed reminds me of Nixon’s nomination of Arthur Burns to head the Fed in 1970. Burns agreed to support a loose monetary policy to help Nixon’s re-election campaign in 1972. A decade later, the US had to deal with double digit interest rates.

Wolf, you say, “(consumers and voters) hate inflation, and they hate high prices, and they express their feelings about inflation at the polls.” This is likely true, and it should be this way. At the same time, the US economy is hooked on inflation. So, my best prediction for the next 30 years is a compound inflation rate of 3.5%, about the same as it has been since 1945. Thus, I think that the 30-year bond should pay close to 7%, to compensate for taxes and inflation.

A 30-year bond is incredibly risky in this environment. the yield would have to be nosebleed high before I’d be interested, and then I might be too scared from all the blood in the streets to buy it.

If inflation has been understated because of shutdowns, partisan BLS, whatever, then unemployment is understated. The fed knows unemployment is understated. It’s like the fed is trying to get ahead of unemployment while ignoring inflation. You can’t convince me they don’t know inflation numbers are higher than stated.

The government said it “removed” 2.5 million illegal immigrants from the US this year (many of them through self-deportation). If true, that would be a huge number. Many of them were likely either looking for a job or were working – so they should have been in the labor force and in total employment. Now these people are gone… there are fewer workers, and fewer people looking for jobs – so this is a supply issue. No one has any kind of handle on how this is impacting employment data.

This, just like in 2005 the economic status quo is broken. We are out into the unknown, hoping we are not going to hit a rock. Our fiscal bonzo gummint repressing interest rates is nuts. Scaring out millions of workers will have consequences, and the fiscal cliffs are real. Apres moi, les deluge.

Indeed, the next fed chair will play the part of Arthur Burns. We just have to stagger on to the next Whiskey Bar, and hope they take our money.

Oddly enough, if people truly believe huge inflation is coming, they should be buying property, not paper or electronic beanie babies.

I’ve been waiting for a lower participation rate from deportation to bring down the unemployment rate but the opposite is happening, “ people in their prime working years, between age 26 and 54, the labor force participation rate edged up to 83.8 percent, nearing a recent high of 83.9 reached last year. (The highest rate was 84.6 percent in 1999.)”, I don’t understand why the participation rate isn’t falling and bringing down the unemployment rate.

It’s not like immigrants were filing jobs that most Americans are willing to do, or that have enough skilled labor to fill them. You aren’t finding any meaningful number of Americans to fill the farming jobs. Same for low skill hospitality work. Construction jobs were already maxed out on skilled American labor. The problem areas I see right now are tech which another big company announces layoffs every month, and retail which is nervous as heck and looking to cut it’s workforce to maintain profitability. Offshoring maybe picking up again and that would offset the number of people that have left (how much, I’m not sure anyone knows right now)

Cole,

A lot of those jobs would be filled by Americans if employers were willing to hire Americans and pay wages and offer working conditions Americans are willing to accept. Institutions that defend illegal immigration are part of a vast conspiracy to repress wages and employer costs.

There are programs in place for seasonal legal immigration for farm work, BTW.

I believe many of the tech layoff workers are getting new jobs during their severance package period. They are not showing up in weekly unemployment numbers or haven’t yet. Appears to be a disconnect with Challenger corporate layoff data and people collecting unemployment benefits. Unless is all a time lag from generous severance packages. Maybe?

@Wolf, “would be filled by Americans if employers were willing to hire Americans and pay wages and offer working conditions Americans are willing to accept…”

….and if American consumers would be willing to pay more for those goods to cover at least some of those added costs. Based on America’s love for cheap Chinese stuff on Amazon or whatever, that willingness is pretty soft currently.

Yes, people might have to pay a little more to get their lawns cut and trees trimmed, and they might have to pay a little more for nannies, and they might have to pay a little more for restaurants meals and hotels, etc.

I was at the bar the other night with my drinking buddy and we were drinking the bourbon like it was kool aid. When we were both three sheets to the wind, I told my buddy “I have a ‘friend’ named Wolf”. He said “What kinda name is that?”I replied “I dunno, but that’s his name! Anyway, I’ll bet you dollars to donuts that Wolf gets a monthly stipend from the Fed.” We left that place howling like a couple coyotes.

That Wolf man is a mysterious creature.

you clearly were and still are totally plastered. The bourbon must have been good! 🤣

Diego bud, good times, thank you!

The President just came out with his affordability plan, shrinkflation, telling US car manufacturers they should make smaller cars that cost less.

Commenters here have been clamoring for small cheap cars for years, whereupon I tell them – having spent part of my career in the car business – that Americans don’t like to drive them, and only buy them in small numbers, and so volume is never high enough to make them work. Automakers all used to sell small barebones cars in the US, but gave up, including Toyota with its Yaris model. But they were real cars that were legal to drive on expressways. So it’s going to be a hoot to watch how two 250-pound 6.5 ft Americans squeeze into a tiny Japanese Kei car – the vehicle Trump was talking about — that aren’t even highway legal in Japan because they don’t have enough power and speed. These are cute baby-cars. They’re narrower than normal cars and have 660cc engines. Can you imagine these two Americans in their Kei car going about their business in Dallas or Phoenix or L.A. while staying off expressways? People need to go Japan and see why Kei cars are popular in Japan for local driving.

Those cars are for thee not me……………………………….

If you listen to the internet and to auto enthusiasts, we’d all be driving brown, manual transmission wagons (this is an old joke from Euro enthusiast car forums back in the day).

Joke aside, the truth is that auto enthusiasts and “journalists” who claim that Americans want cheap cars have no clue what the real market is.

Ask every automaker who offers an entry level, poverty model. They do it to hit a certain price point to attract people into the showroom. From that point, the *vast* majority of buyers self-select into a significantly more expensive, better optioned trim level or model altogether.

I worked in car sales back in the very late 90s, and the number of people who came in for a $15,000 manual transmission Jetta and left with a $27,000 fully loaded automatic Passat was legendary.

Until someone takes away the punchbowl, Americans will always self select into the more expensive trim/models. “Affordable” cars are just there to attract eyeballs, not buyers.

In my view, the biggest problem is the number of pickup trucks, especially driving recklessly, by people who have no legitimate need for them.

Buyers pay very high premiums to get manual transmissions on BMW cars and most BMW drivers have little to no interest in overlarge vehicles so a vehicle’s size has little to do with its price as you assert.

“Ask every automaker who offers an entry level, poverty model.”

This literally doesn’t exist anymore. Even a base model Corolla or Civic has a gazillion different modules on the CAN network. “Entry level” cars are just as sophisticated as the higher trims these days.

Parts quality can certainly still be described as cheap. My favorite thing in the world is warrantying out a part I just replaced two weeks ago because it already failed /s

japanese are very polite drivers. much as, in the rest of their lives.

I’m not sure what the kei cars look like, but we have some “karts” and mokis popping up around here.

They’re little EVs, not for highway use (basically glorified golf carts).

In my small town they’re great for getting to the ski lifts and carting around the family.

They are used in addition to the other huge SUVs and everything else.

I only see a small amount of people who have small vehicles as daily drivers (being in the mountains where a 70 mile daily commute is normal for half the workforce).

I think you meant “expressway-legal” when you wrote “highway-legal”.

Not so much of a problem in Japan as not as many expressways as in U.S., and AFIK they’re all tollways _very_ expensive by U.S. standards — about

$0.35-$0.40/mile at purchasing-power-parity of ~90 yen/$ (current market rate of 155 yen/dollar makes yen very undervalued).

Tokyo-Osaka is about 310 miles, toll about 11k yen.

As most driving in Japan is on roads with 54kph (31mph) speed limits, lack of power is no problem. Higher limits are uncommon, only some two-lane rural roads have 60kpn (~40mph) speed limits

I’m driving a small cheap car. A Mitzibushi Mirage. The car has a 1.2 leter engine and is under-powered. I hate to take on the Beltway because it gets blown all over the road. I use it for local travel only. It’s easy to park, easy to drive, has good visibility, and gets excellent gas mileage. I believe it was made in Thailand. Anybody can confirm this? Anyway American manufacturers don’t make any car like this.

MW: Stocks struggle as Wall Street ponders impact of latest jobs data on Fed’s interest-rate path

SPX -0.43%

DJIA -0.48%

COMP -0.17%