A narrative gets debunked. The affordability crisis remains.

By Wolf Richter for WOLF STREET.

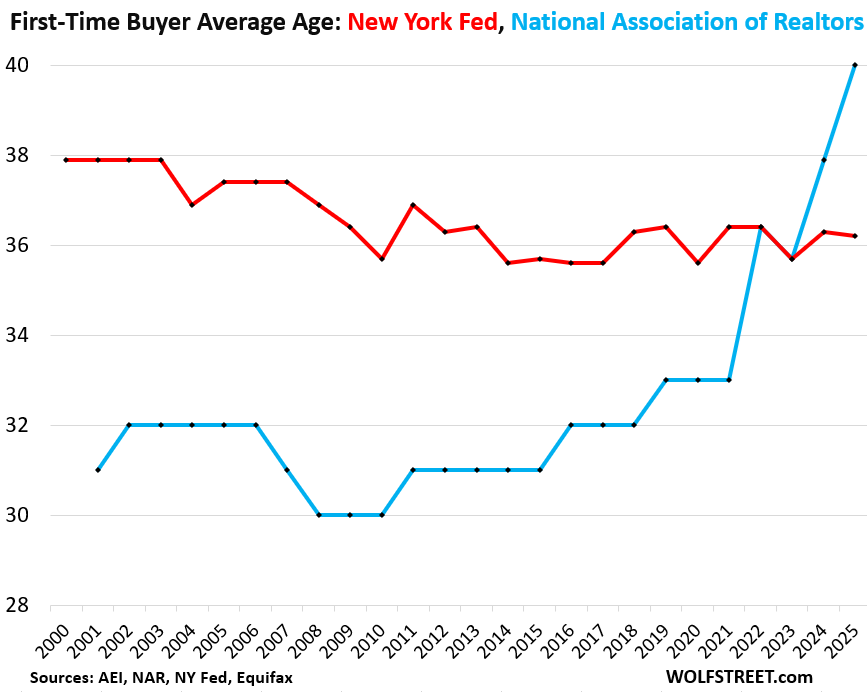

The National Association of Realtors (NAR) claimed in its annual report on homebuyers, based on survey results, that the typical age of first-time buyers (FTBs) had spiked to 40 years in 2025, up from 37.9 years in 2024, and up from 33 years in 2021. This spike in the age of first-time buyers caused a lot of handwringing and heavy breathing in the media and social media.

But the New York Fed, based on its Consumer Credit Panel/Equifax (CCP) data, has debunked this narrative of the surging age of first-time buyers. In August, it released a report with data through 2024.

And I reported on it, republishing the charts from the NY Fed, and I summarized:

“The average age of first-time home buyers has essentially not changed since 2012, and compared to the early 2000s, it has declined marginally.”

Now, Edward J. Pinto and Joseph S. Tracy at the AEI Housing Center have published a new report with updated CCP data from the NY Fed through 2025 (they thanked economic research advisor at the NY Fed, Donghoon Lee, for his assistance in updating the NY Fed’s data analysis). And they compared the NAR’s data and methods to the NY Fed’s data and methods:

Per the New York Fed’s CCP, the average age of first-time buyers edged down in 2025 to 36.2 years and remains roughly unchanged since 2009, and lower than in 2008 and prior years (red line in the chart).

Per NAR, the typical age in 2025 spiked to 40 years, from 33 years in 2021, 32 years in 2018, and 31 years in 2015… a stunning nine-year increase in a decade (blue in the chart):

Why the difference? Who is closer to accurate?

The AEI’s Pinto and Tracy dig into the methods. From their report:

“NAR’s statistics are based on their annual survey of homebuyers and sellers. For the 2025 report, covering from July 2024 to June 2025, 189,750 surveys were mailed to a ‘representative sample’ of buyers and sellers. However, only 6,103 completed surveys were received, indicating a response rate of just 3.5%, with only 21%, or 1,281, being FTBs.

“The [NY Fed’s] CCP, by contrast, is based on a 5% random sample of all credit reports, which reports provide both borrower age and home buying history.”

And they add:

“Digging deeper into the NAR and CCP results yields helpful distributions by age bins. While both have nearly identical shares for age 35-44, the NAR’s under age 35 groups are underrepresented by 17 percentage points and the aged 45 to 74 buyers are overrepresented by 18 percentage points respectively, compared to the CCP.

“The NAR bias to a higher age is perhaps not surprising given that it is a mail survey with 120 questions, which doesn’t lend itself to a high response rate by Millennials and GenZ-ers.

“The CCP data appears to offer a better historical view of the current position of FTBs.”

But the affordability crisis remains.

Today’s first-time buyers face a huge affordability crisis in the US housing market, driven by the home price explosion from mid-2020 to mid-2022, of over 40% on average, and in many markets of 50%, 60%, or even 70% in just a couple of years, which was completely nuts.

In many of those markets, home prices have been skidding lower since then: Here are 14 bigger markets where single-family home prices have already sunk by 10% to 25%, and 24 bigger markets where condo prices have sunk by 12% to 29%. These lower prices, along with rising wages, are the market’s solution, and it has begun to whittle away at the affordability crisis.

But in other markets, prices have continued to rise, though at a slower pace, thereby still worsening the affordability crisis.

There is a solution to this affordability crisis – and it isn’t lower mortgage rates, which are in a historically normal range, given where inflation is. My analysis and why this mess happened: Mortgage Rates Are Not Too High. What’s too High Are Home Prices that Exploded by 40-70% in 2 Years, Creating the “Affordability Crisis”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Might the fact that some measures say that if you have not bought a home in say 5 years, you are considered a “new” home buyer?

Not these two measures here. What you’re talking about is sometimes used for things like subsidies for first-time buyers, such as by HUD.

The Mortgage Bankers Association (MBA) came out with an article and its “Chart of the Week” on Dec 5, showing just how far out there in no-man’s land the NAR is with its 40-year first-time buyer age nonsense.

Red marks are mine. The NY Fed CCP/Equifax date are the columns on the right.

Wolf states this: “ Today’s first-time buyers face a huge affordability crisis in the US housing market, driven by the home price explosion from mid-2020 to mid-2022, of over 40% on average, and in many markets of 50%, 60%, or even 70% in just a couple of years, which was completely nuts,” leaving us wonder ‘Was this some organic, spontaneous event, or was it caused by something / someone – i.e. ‘some boogeyman.’

i’m going with the boogeyman hypothesis, but Wolf doesn’t report on boogeymen.

Click on the link in the last paragraph, and you will find out in color and detail.

You’re right. The boogeymen are alive and well; they reside in the Eccles Building. Why was it a good idea to give friends of Don or Joe the power to drop interest rates to zero. Since when is money free?

I mean, it’s “free” for governments which issue their own currency.

But that doesn’t mean there aren’t consequences.

they should rename it

1st time home renters – since you never really own it given the govt property taxes they keep grifting

our 2 sons each bought their homes

1st – age 24 (right after graduating college/1st job)

2nd – age 20(never went to college and worked for living)

now he’s building new home at 27

Remember not too long ago some of the experts were predicting negative interest rates?

I was so looking forward to borrowing money for a house and having the bank pay me the interest for the loan. Sigh….

Crazy times but not Weimar times.

On a side note which may help free up homes for sale, all Treasuries are now paying less than 4% except the 10, 20, and 30 year bonds. If you have a 3% mortgage, less than 4% ( less than 3% after almost 25% federal taxes), you are no longer making safe money holding on to your mortgage.

As people approach retirement:

1) You can now pay off your mortgage and live in safety. The banks can’t take your house and you are motivated to pay off the loan (per Dave Ramsey ideals) to be debt free.

2) You can sell your house and downsize.

3) You could gamble and put the money into equities for a higher return. IMHO, you might have better odds in Vegas.

4) You could take the money you had stashed in Treasuries to pay off the house, and treat it as a low cost HELOC to improve your house being in forever debt.

People haven’t had to make this decision in 5 years. Change is coming.

we have 15 year 3.35% mortgage – going on year 6

since we can’t walk it over to different home

we’re stuck here in our little 2700sf home

maybe in 5 years we’ll be close enough, but I doubt at 70 we’re gonna move

“Crazy times but not Wiemar times.”

I feel we are getting very close there in many ways.

Well, I had my first 3.25% mortgage while Obama was President. But I get your drift, a choice was made to avoid deflation, to reinflate and to monetize us out of a long term economic malaise. Did it work? For many it’s been great… but aren’t so many talking about the unhoused? The massive deficits? Our inability to compete with a low cost nation such as China? Perhaps deflation might have helped a bit with some of this? But it’s so much easier to paper over things with inflation.

Perhaps inflation is the boogeyman. Housing prices may be like gold prices. They go along quietly for years and then suddenly make up for ten years or more of inflation in 12 months. If I had a chart of housing prices, one of golf prices, and one of inflation from 1900, I would bet they would all show lines up and to the right.

Inflation is.not under control, and probably never will be so the dollar is constantly losing purchasing power and housing prices go up and down but mostly up.

If you sell your home for 2or3 times what you paid for it and have held it for over ten years, considering the loss of dollar purchasing power, capital gains taxes, real estate costs, property taxes, insurance costs, repair cost and opportunity cost of original investment, your ‘biggest’ investment might just brake even.

Perhaps the new American Dream is renting not buying.

Reasons:

1. Mass illegal immigration causes high rents making it impossible to save.

2. Cost of vehicle so high also making it impossible to save.

3. High tax on single earners.

4. Transaction costs.

5. High interest rates.

6. Lack of stability in most employment scenarios.

7. Crazy high property taxes, maintenance costs, and sky high utility bills.

8. Student loan payments.

Solutions:

1. Force government to allow for more smaller housing sizes.

2. Force real estate transaction costs to be reduced.

3. Allow for tax free saving for down payment.

4. Make down payment extremely low on small homes.

end all property taxes

setup Federal(I KNOW) catastrophic insurance and everyone has to participate – $100 year

then have insurance companies cover normal insurance

they will then have NO EXCUSE for high priced policies and if they write in 1 county they MUST write in all counties of state

It’s a weird how the illegal aliens set rental rates and not landlords.

Some of the illegal aliens probably are landlords.

Where I live some of the rentals are foreign owned. Neighbor says his rental is owned by someone jn Saudi Arabia and he bought 11 other local homes as rentals as well. Mine is owned by immigrant that leverages all the properties like crazy, can’t pay for maintenance and just wants to brag about his 6000sqft house. Zero upkeep on his properties.

MW: Treasury market logs worst weekly rout since April, in a bad sign for borrowers

America homeowners hold record levels of home equity, exceeding $34 trillion collectively, with the average mortgage holder having around $300,000+, driven by rising home values, though growth has recently slowed and some areas see declines. This substantial equity acts as a financial cushion, though many homeowners are paying down mortgages rather than tapping it via loans (HELOCs, cash-out refis), leading to a rise in fully owned homes, notes Marcus by Goldman Sachs.

Key Figures & Trends (as of mid-to-late 2025):

Total Equity: Over $34 trillion.

Average Equity: Around $300,000 – $307,000 for mortgage holders.

Equity-Rich Status: Nearly half of mortgage holders have at least 50% equity.

Shifting Behavior: More homeowners are paying down mortgages, increasing outright ownership, and using less home equity debt.

– You are either in the club or out the club regardless of age. Wolfs drunken sailors updates really drive’s these points home. If you add on interest bearing MMA’s, CD’s, and T Bills. Americans are just too rich to fail.

You can’t eat household equity. As I tell my kids – that equity looks great as long as someone is around to buy your home when the time comes to sell. I am keeping an eye of Wolf’s reports on HELOC rates – one sign that people are trying to tap into that “equity” without actually having to sell their home.

I’ve had heloc now for over year

think I have to pay annual fee

and if I don’t use down road they charge like $500 at end

currently massive 8.5% rate

I have it for projects and when I buy another rental

use it wisely or it will eat you

Too late, the “no one can buy a home until 40” meme has taken hold. And it is very difficult to ever meaningfully change minds.

Late 80’s first time home buyers ages 36 & 40 yo, barely could afford with 2 professional salaries….mortgage rate was 14%. So, not much has changed…this isn’t some new affordability crisis…its always been tough out there! And for the plandemic era housing price surge, they printed gobs of money, lots of inflation, so no wonder prices soared off the charts… And look at the increased building & maintenance costs…doubt that prices are going to collapse…but I’ve been wrong before…

But famed NAR economist Lawrence Yun said it’s a great time to buy a house.

… Again.

Sounds reasonable, the mind weakens with the age, I was smart at 32 and started loosing my mind in my 40s, and you should be out of your mind to buy something now..

The NAR also said the median age of all buyers, first time and repeat, was 59. That is a fascinating statistic if true. According to NAR, only 21% of sales are by first time buyers. Repeat buyers drive the transactions.

According to NY Fed/Equifax data, the average age of repeat buyers is 48. The NAR data really seems to skew high.

In 1980, my wife and I bought our first home (me aged 22) for the, scary at the time, sum of $35,000. Along with the excitement was trepidation but the $325/mo 30-year mortgage payment was a scratch less than the $350/mo we were paying rent. It was doable.

Fast forward 45 years and the home (not in a HCOL environment) most recently transacted (2022) for $175,000. As for the apartment where we once lived? It rents today for $1650/mo.

Meanwhile, at retirement as an engineer, I earned a scratch over 5X more (with 45 years experience) than I did as kid with an entry level engineering job. Grade school math shows I’ve merely stood still economically (whilst delivering far more value) thanks to our Federal Reserve and the acceptance of 2% inflation.

Of course, I can buy a 75″ television for about 5X more than I paid for a 19″ Sony Trinitron back in the day, so there’s that – but – ground beef on sale is no longer 88¢ a pound (for 80% because money was tight whereas these days we’re paying $7.10 but buying ground chuck.

And I know this, not from memory but because my better half recently came across a Kroger receipt, which had been used as a page marker. We sat together and walked down memory lane.

Sigh.

I’m glad you brought up the cost of tvs.

Perhaps Wolf has a thought on this.

As flat screen tv costs go down, as the manufacturing improves, this shows up as a deflationary input. From 2k down to $500, for example.

BUT, when tvs went from Black and White $500 to flat screen $2K, did that show as an inflation?

I did a quick look and the domestic television hardware market size (in the US) continues to experience strong revenue growth – driven by an increase in number of units per household and shortening purchase cycles. So you can cut your revenue per unit if people buy more units, more often – particularly if those revenue cuts are driven by corresponding cuts in production costs. That is why the “deflation” fear is just that – fear. Deflation with static consumer behavior might be bad, but consumers rarely remain static and will change their behavior based on economic factors – like cost per unit.

Curious whether NAR had some incentive to misreport the average age of 1st time buyers. Any agenda there?

FredW

Nah. They have sent out the same huge long paper survey for decades, and the response rate by the younger generation has dropped even more than the response rate by the older generation. The response rate is now minuscule… less than 4%. A survey like this should be scuttled.

JustAsking

So this was a 30-year journey. Some period after a new product comes up, such as flat-panel TVs and computer screens, they are added to the CPI basket, initially at a very low weight since few people are buying them and not much consumer spending goes into them. As sales increase, while prices fall, their weight in the basket increase.

So the $2,000 price at the beginning had a very low weight, and so it didn’t matter much. The very first $7,000 plasma screens weren’t in the basket at all because so few of them were sold. So when their prices plunged, it had no impact on CPI. But as prices dropped and sales increased and became a mass-market product, flat-panel screes were added at a low weight, and therefore had little impact. When prices fell further and sales increased further, their weight in the basket increased in proportion to the amount of consumer spending that went into them (but spending on something with falling prices means that the unit sales increase will have to be high just to maintain sales, and therefore the weight).

Over the same period, vacuum-tube TVs and computer screens also became bigger and cheaper, and people continued buying them because they were a lot cheaper than early flat-panel screens. But as flat-panel screens became competitive on price and quality with vacuum tube screens, sales shifted to flat-panel, and vacuum-tube screen sales declined, and as they declined and got cheaper along the way, their weight in the basket also declined. At some point, vacuum-tube products essentially vanished from shelves, and their weight in the consumer spending basket was near zero, and they were pulled out of the CPI basket.

So the journey from a $2,000 screen to $300 screen didn’t have a lot of impact on CPI because the weight of the early $2,000 screen was minuscule and didn’t matter. Vacuum-tube screens getting cheaper and bigger over those years had a bigger impact because they initially had bigger weight in the CPI basked, and their price drops mattered more.

Thanks for that.

Affordability

My Generational observations

Used to be to raise a family you only needed one parent working, now it seems to me BOTH must hold jobs. Then the cost of day care. This keeps the birth rate down. Delays the ability to afford a house.

Used to be a starting salary out of college, with a degree, was about 4 times the yearly tuition. Now about 2 to 1.

“Used to be to raise a family you only needed one parent working, now it seems to me BOTH must hold jobs.”

I’ve been hearing this at least since the early 2000s. It wasn’t true for my family, first kid born in the early 2010s, one middle-class income from then to now. The recent insane run-up in house prices and rent may have rendered it finally true. I hope it’s a temporary aberration.

Yes, when women entered the workforce the price of housing went up to take their income as well.

After 50+ years of various types of market manipulation, enabled by the Fed, are any of us really that surprised by the lack of true price discovery in so many “markets”, including the housing market? I am certainly not. Especially considering the levels of debt. With regard to housing, either prices need to continue to fall or wages need to rise. Place your bets!

Interesting times.

Good Start WE:

How some ever, it has actually been the entire 112 YEARS of ”market manipulation” by the communist central planning bureau AKA federal reserve board!

Thus, WE, in this case the workers and savers WE, have paid through the nose for the vast and continuing market manipulations AKA central planning of the FED since 1913, when the FRB was started BY and FOR the banksters.

Recently, while declaiming loudly their foucs is to provide ”stable prices” etc., etc., so that the naive and as usual generally uninformed non ”financially” aware, AKA suckers believe that the FED has our interests mandated, the FED, as always over the last 112 years, protects the rich and richer at our expense…

FREE MARKETS are SO Clearly the ONLY long term option for the workers and savers that it is truly amazing that the FED is still in operation…

And to be more clear, yes WE need the FDIC and other GUVMINT oversight of the banks and bankster, but only because that industry, other than politicians are the most corrupt group, maybe next to lawyers that has ever been.

Good Luck and God Bless ALL on here to see Wolf’s wonderful analyses of what can be known of the financial world.

A stock market wipeout of 90%, followed by 30 years of no gains, is what’s needed.

Out here in flyover, my children are home owners. The youngsters I see on my job sites own homes.

They do alot of their own handyman work. If they don’t know how, they have friends or family.

No HOA, or 3000ft2 homes.

Not all doom and gloom.

Flyover country is different. On the Coasts, many (if not most) people couldn’t afford the homes they are living in at today’s prices. It’s definitely true in Seattle, where rental cost is less than half the ownership cost in many neighborhoods.

Good one Bobber, and thanks for your local POV:

Here in the saintly part of the TPA bay area, the house behind us, NEW in August, just closed at $1,050,000.00, very close or possibly below the final cost of construction; it had started listing at $1.6M, but, as Wolf has said, ”builders” are very clear about what’s happening and willing to deal.

Others in good shape in this hood that is above flood and evacuation levels continues to be popular, with one neighbor just decided to demo her old house of 20 years and have the best local builder build a new one on the same lot; very interesting, indeed…

INVHO, the rental versus owning situation in Seattle, similar to many locations, indicates where the market, IF and ONLY IF left alone by the central planning appartus, will settle THIS TIME…

And WE, in this case ALL the elder worker and saver WE, can only hope that our younger similar folx will receive the benefit of the next crash as they always did previous to the FRB, (clear description in comment earlier/above.)

Where I live on the West Coast a lot of my Boomer friends and acquaintances feel like the only way their kids will get houses (and maybe grandchildren…cross fingers) is for them to either be gifted (full or part) or inherit a house. I don’t think it’s that grim but I do see this happening often.

I would imagine passing homes down to kids via trusts and other gimmicks is the course of action out west. (CA)

This non change of ownership I assume allows one to escape being reassessed and getting the prohibitive tax bill

That assumes the kids stay in the same location and want the home. Big assumption.

If kids need affordable housing, won’t most of them move out to more affordable areas before parents pass on?

It’s complicated as we are going through this right now in California and we just had this discussion with a tax attorney. If you pass down a home to kids in California, the kid needs to make it their permanent home w/in one year of the transfer, otherwise it is reassessed at current market value (e.g. non-primary home). This would assume the kids want to live in the home and that there are also no other heirs, etc to split it with (not sure how this works if you had to buy out a sibling, etc). Also, if the home has experienced great appreciation (>$1M), the amount above the “exclusion” amount will be added to the property’s new taxable value. I am by no means an estate expert so trying to navigate all of these stipulations is mind numbing :)

Yes, a house transferred in a trust needs to be the primary residence of the trustee to avoid reassessment, but with the parent.child exemption the ‘exclusion’ is not applicable.

I hope that by the time I pass into great beyond that my kids will already have settled into a career and a location with their own houses. They likely won’t have any interest in living in my deferred maintenance 50+ year old house so they will sell it to pay off their current houses.

CA has a good law that allows the transfer of the property taxes to the kids if they decide to live there. I know several families who have special needs children living at home or who have children living at home taking care of their elderly parents who would greatly and justly benefit from this.

CA closed the loophole for kids who inherit their parents’ Prop 13 houses with very low taxes and decide to rent them for market rate exorbitant rents. If the kids don’t live in the house, then the taxes are re-assessed. That’s fair IMHO.

We’re still essentially renting our house, even though the Mortgage is paid in full. Property taxes are now approaching $10,000/yr for a 1,450 sq foot house here in the Swamp. Add insurance, utilities, maintenance, etc and you get $2,000/month costs to live here in a bare bones single family home. What a scam to say you own your own home and you have made a lot of money with appreciation. That’s total bull s$it from the NAR and all the Real estate industry’s con artists to make people feel good when they are actually losing their shirts every day.

10k a year for 1450ft2!!

You need more planners and administrators to at least reach 20k.

If you buy a mid-tier single-family home in San Francisco today, your property tax bill is around $18,000 per year.

The annual LA County Assessor Property Tax Bill on a typical $2.5 million house in a reasonably decent LA suburb is right around $30,000 these days and I should note is due in a few days on December 10, 2025 for the 1st of 2 installments without incurring an additional 10% penalty.

Good one SC, and it is very likely that the current administration and the legislature in the flower state has exactly a similar situation in mind when, so far, there are four bills pending to either greatly reduce or totally eliminate ”property taxes”…

Some reduce, others eliminate ALL on elderly folx, and while all of these bills have Some good ideas, it is likely that at least old folx will see a serious reduction, or perhaps elimination of such taxes so that they, the old folx, can stay in their homes longer, a much less costly process than forcing them out as was the case before FL had the Save our Homes tax CAP similar to California, and sheparded in fact by the same dude.

I bought my first home 20 days before my 41st birthday this year, in a small irony.

Bought my first home in 2009 @ 33 years old.

It was very expensive for me at that time….

barely pulled it off.

Crazy insane expensive now. Just sold it to move…. but I could not afford to buy it for the amount they bought it for… could not even touch it. Crazy numbers out there. Hopefully it keeps mellowing out, because the up up up is definitely unsustainable.

hahaha. Thought so.

This week’s Fed meeting will highlight the central bank’s challenge: Preventing a recession while tackling inflation

Figures lie and liars figure. There are three kinds of lies: lies, damned lies and statistics.

Those are not my words, but this article is a great example of how numbers get manipulated to spread a message. My wife is a Realtor and she cringes when her industry publishes garbage like this.

On August 11, 2024 the Wall Street Journal had an article titled, “Boomers Buying Houses Had It Bad in the ’80s. Millennials Have It Worse.”

Let me guess … the Wall Street Journal is filled with BS you don’t want to hear about on your site?

“the Wall Street Journal is filled with BS”

is often correct. So let’s look at it.

From your statement it seems you don’t subscribe to the WSJ and therefore cannot read the articles, and you just drag headlines into here, without having read the article, because you imagine that you know what the article said? That is a stupid thing to do and is one of the seven sins of commenting. If you don’t read the article, do NOT drag the headline into here.

So let me help you: that WSJ article from August discussed “affordability” — which the article pointed out is composed of sky-high home prices (including a chart of sky-high median home prices, LOL), sky-high property taxes, sky-high insurance, and mortgage rates that have risen from record lows.

The article showed how sales of existing homes have plunged. It showed the median price to median income ratio with a chart. Etc.

So far, this is stuff I discussed in my articles.

With regards to the early 1980s, when young boomers were buying homes, the WSJ said: “Record-high mortgage rates [18%] sent home sales tumbling, but prices and incomes keep rising.” Now rates are 6-7%.

So far so good.

And then toward the bottom of the article, the WSJ cites the bullshit figures from NAR that I and everyone else (see the MBA chart in the comments above) have totally debunked – and I gave you the reasons why they’re bullshit numbers. Can you not even read my articles? They’re free.

Wolf, always great to read your “no BS tolerated” comments and to read how you set things straight.

I wish, I had more time to read all of your articles, but still have to slave on plantation every day.

A $1,000,000 assessment on a home in northern WY results in $2400/yr property insurance and $3800/yr in property taxes ( 2700 sq ft home on the nicest golf property in the state and near the Big Horn mountains ). But, ( here’s the rub ), you have to live in northern WY !

My assessment is less than half that and my annual prop tax bill is almost double.

As previously mentioned, Property Taxes in many areas are out of control.

Property tax collections rose about 38% nationwide over the last 10 years in the US, and inflation rose about 31%.

Add to that the cost of regulations and special assessments, and housing is now more expensive.

These are not the only causes, but ones that could be easily dealt with.

Isn’t this how the Chicago Tribune published “Dewey Defeats Truman” in the 1950s? I.e. they didn’t understand that their phone poll tended to reach the people who were voting for Dewey.