The bond market went back to work on Monday.

By Wolf Richter for WOLF STREET.

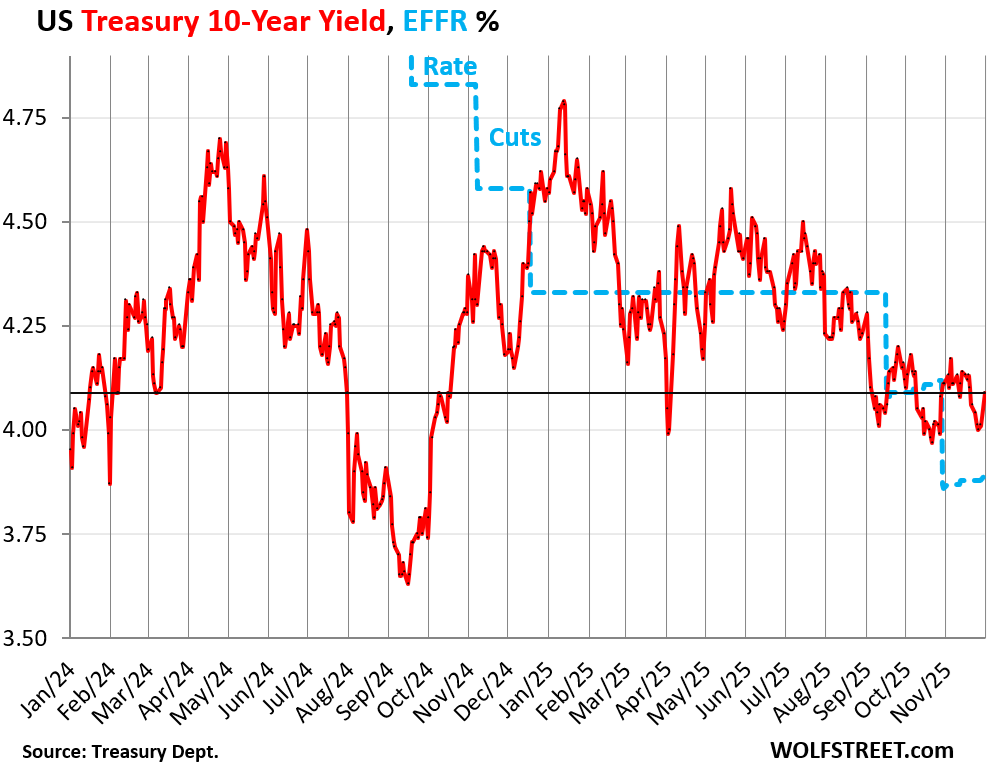

The 10-year Treasury yield jumped by 8 basis points on Monday, to 4.09%, where it had been on November 20, wiping out in one day the entire decline of last week.

Long-term yields are largely driven by fears of future inflation and fears of future supply of new Treasuries that the bond market has to absorb. The Fed’s short-term policy rates and hopes for rate cuts have little impact on the long end of the bond market.

The Effective Federal Funds Rate (EFFR), an overnight rate at which banks lend to each other, and which the Fed targets with its five monetary policy rates, shows the rate cuts. But it has been drifting up ever so slightly starting in September as liquidity is getting tighter in the market (dotted blue line).

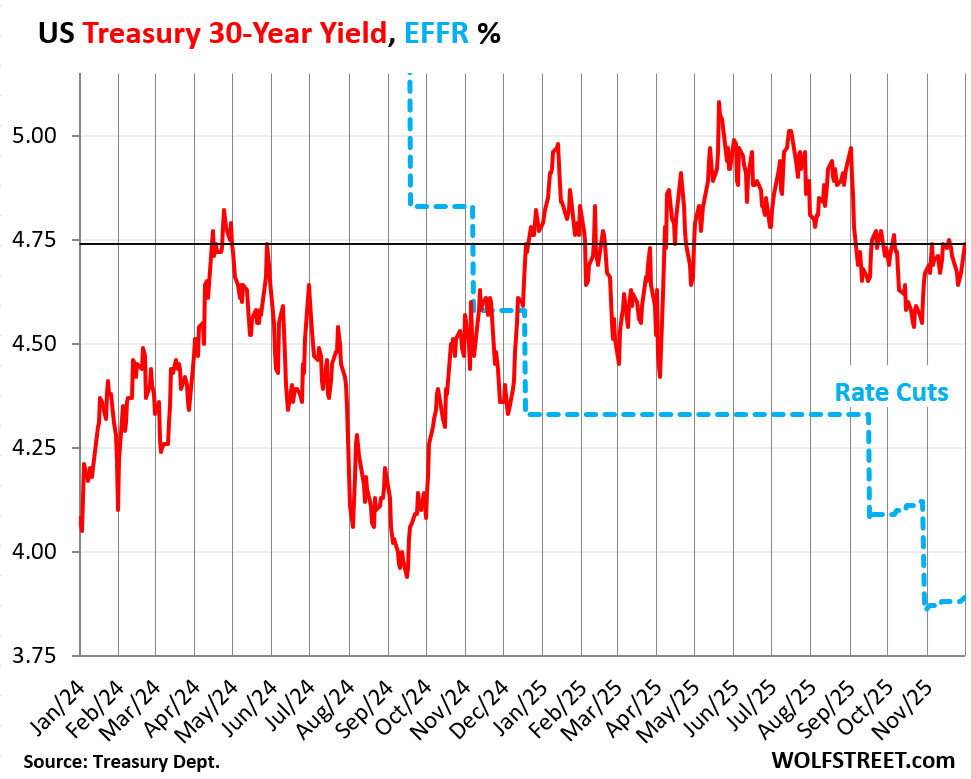

The 30-year Treasury yield jumped by 7 basis points to 4.74%, wiping out more than the drop last week. All year it has remained in a fairly narrow range between 4.5% and 5.0%, only briefly piercing both of them a couple of times.

The 30-year yield is particularly driven by fears of future inflation. Since the first rate cut in September last year – the 50-basis-point monster cut – the 30-year yield has risen by 80 basis points.

Rate cuts by the Fed do not automatically translate into lower long-term rates.

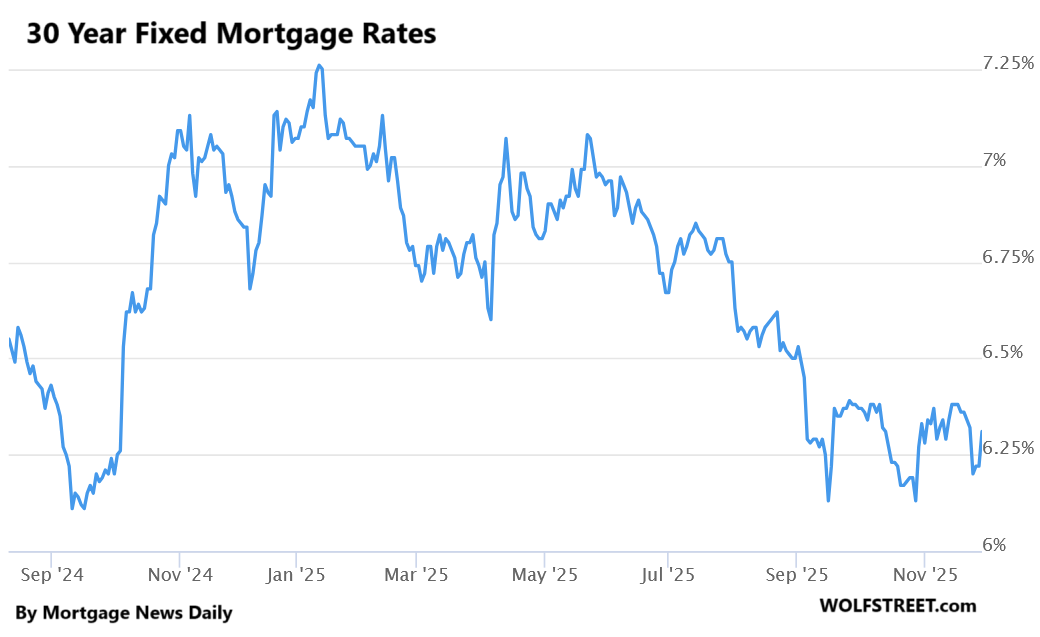

Mortgage rates also jumped on Monday. The daily measure of the average 30-year fixed mortgage rate by Mortgage News Daily jumped by 9 basis points, to 6.31%, also wiping out the drop last week.

The average 30-year fixed mortgage rate roughly tracks the 10-year Treasury yield, but is higher, and this spread varies over time. The average life of a 30-year mortgage is less than 10 years as mortgages get paid off prematurely via refis and sales of the homes (it was about 7 years before the arrival of the 3% mortgages).

The average 30-year fixed mortgage rate is higher than it was before the monster rate cut in September last year.

Here too: Rate cuts by the Fed do not automatically translate into lower 30-year fixed mortgage rates.

These mortgage rates of 6% to 7% are not high by historical measures; they’re only high compared to mortgage rates during the era of QE, which started in 2009. The problem in the housing market is not those historically normal mortgage rates, but the 40-70% home price explosion from mid-2020 to mid-2022, caused by the Fed’s mega-QE that created the below 3% mortgage rates even as inflation was surging toward 9%, which resulted in steeply negative “real” mortgage rates (mortgage rates minus CPI inflation).

These negative real mortgage rates were better than free money and caused the craziest home-buying behavior ever, and home prices exploded — and those prices are the problem in the housing market today: Mortgage Rates Are Not Too High. What’s too High Are Home Prices that Exploded by 40-70% in 2 Years, Creating the “Affordability Crisis”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Risk (trust) continues to be repriced, globally. The faster the Fed lowers the FFR, the faster real interest rates will rise. An irresponsible congress and administration certainly doesn’t help.

Interesting times.

Home prices need to come down 50% in this economy. If we go in to a recession they will go down 70%. If we go into a depression home values will totally tank. We can’t lie our way out of this one. Pucker up buttercups.

What does the standard of living do when we have a economic contraction?

True that! :)

Will a 211k or less weekly unemployment report this Thursday change the Fed futures? On the charts 209k is support this week. Less than that it breaks lower in the weeks ahead. Charts were invented to predict rice yields way back, they work great for unemployment claims too. FYI 205k is the 52 week low. O Yeah, ADP is expensive we switched to paycorp after 2008. People who use ADP have extra money to spend my point is ADP data isn’t what it used to be to be.

Unemployment claims broke support, 191k!! Back test is 209k, next support to fall 182k it’s crazy that the news isn’t covering this. This should change fed futures for Dec. the inflation unemployment inversion is coming Inflation is going above the unemployment rate in 27 or late 26.

Despite everything, the argument that interest rates are high and should fall is propagated all over the world. Prices never fall and should not fall, and politicians come up with all sorts of things to maintain this delusion.

Perhaps those shouting the loudest have the most to lose when refi time comes.

Prices are “sticky downwards” but do fall (eventually) when warranted. Interest rates, however, aren’t “prices” and are driven by extreme competition, liquidity, and fungibility so change easily.

Interest rates are the price of borrowing money.

Both the price of housing and the price of borrowing money are governed by who shows up to the market to trade at any given moment and what they agree on based on what time pressure respective sellers and buyers are under to close a deal.

Free money is the best money 🤣

Bond traders are fighting the real estate market. They will lose. Real estate will benefit from a diminished dollar. Mist here want the bond market to win. I say real estate will win and bond traders will eat dust.

As a landlord I am going to only add that the potential wrench in your hypothesis will be the cost to maintain real estate and the cost of utilities. Especially as more data centers suck up electricity and water.

For the investor, if ROI goes negative, we sell, period. Even for a homeowner who has paid off their property, if the maintenance and utility costs get high enough, then they will look to downsize.

The liquidity injection that followed 2008 and covid was obscene the distortion that this has had on “markets” is yet to be fully felt. The correct response would have been to let all the bad actors in banking and finance fail and experience a prolonged recession to clear out the bad actors and reset prices to reality. But that isn’t the path that was chosen.

Certainly NOT CLEAR as of this posting.

Wolf refrains from predictions for a very very good reason backed with tons of data.

Real estate is already losing if you read up WRs articles.

You tack inflation on top and other expenses and it is losing big time .

The delusion is strong in this one…

“Real estate is already losing if you read up WRs articles.

You tack inflation on top and other expenses and it is losing big time .”

I am only one small landlord, but my rental properties are still very profitable and my vacancy has never been above 2-3%, but then again, I have very little debt on these properties. Seems to me, it’s the folks who lever up that get crushed in the “rinse cycle” of the fed’s wash and rinse regime.

The political problem is from nominal prices falling. Real price of housing has been falling for years, even in markets where nominals are sticky or rising.

The new Fed Chair will make it worse if he tries to make DJT happy and ignore the realities.

Wolf, I still think the demand for money and the activity at in the SOFR and the SRF are an indication that rates are NOT restrictive but attractive. IMO.

Your thoughts.

Realities?

Real estate wins.

“Real estate wins”

The 14 Bigger Cities & Counties with the Biggest Price Declines of Single-Family Homes (-10% to -25%) from Peak to October

The 24 Bigger Cities where Condo Prices Have Dropped by 12% to 29% through October

I agree that current rates are NOT restrictive.

Nominal rates are pre-tax, but CPI inflation is after-tax.

For most market participants, after-tax interest rates are below real-world inflation rates.

P.S. Mortgage lending is being discouraged by high-and-falling real estate prices, not high interest rates.

My old mothers property taxes have gone up so much after this fake price appreciation she is having problems staying in her house of 60 years… She and my father bought it for 30k in 1964. Prop tax is now the same as what they bought it for all those years ago. If she can’t afford it she loses 30% to capital gains just to move.

That’s one thing California got right….

restricting and capping real estate taxes.

BUT, by the same stroke, this is why Pacific Palisades and other effected areas wont rebuild. New construction comes with the new assessment.

Living in California, no this wasn’t a good move. It’s one of the reasons real estate is overpriced here. The market cannot stabilize because people can pay a tax rate that isn’t remotely connected to the reality of the current market and prices. This in turn forces newer buyers, usually younger generations, into paying for it via inflated real estate prices and subsequent taxes. It’s another form of forcing one select group, newer buyers and usually younger generations, to pay for another groups, older generations and those who are lucky enough to be able to buy during recessions, benefits in the form of reduced tax rates/burden. If taxes matched prices, the market would come down and spikes would not be as crazy as the increased tax would tamper artificially created demand. The people who think it’s great are those are people who picked up real estate cheap and those who invest in real estate for rentals of some form. Plus, really, if a 1 to 1.3% tax is going to make or break your budget to the point you can’t afford a home anymore something is off. 1.15% on a 300,000 dollar value increase is an increase of 287$ a month to your payment. Really, that is the thing that’s destroying peoples budgets in todays hyper inflation world? I have a hard time believing that. But hey, asset owners always seem to love being subsidized by everyone else, if it’s through money printing or advantageous tax structures like this one.

Agree 100%. The solution to property taxes increasing with abandon is to cut back on local governemnt spending, not to shift the costs to new buyers.

Good points.

But, how affordable is it to have an annual real estate bill of about 3% of the assessed value? (like a few other Blue states)

Sure the price tag drops, then they bleed you to death with the real estate taxes.

The law in question was never really about helping elderly homeowners stay in their homes, as there are far less distortionary means of accomplishing the same objective. It was always about creating a sweetheart deal for landlords, who have been its biggest promoters since the very beginning.

Prop 13 has favored corporate landlords the most. The property stays owned by a shell corporation so the property taxes never go up much, even though both the tenants and de-facto owners (of the shell corporation) change quite a bit.

It is crazy how a person can be taxed on unrealized gains such as “fake price appreciation” in real estate. A person can have not much of anything, except a roof over their head and potentially be taxed as if they were a millionaire.

Awhile back they were floating ideas about taxing unrealized gains in stocks. I cannot wrap my head around taxing people on unreal numbers.

I understand the tax when someone sells or buys “though I don’t especially care for it”. I just cannot understand taxing that which is unreal and does not exist yet. Which is why I though it was called Unreal Gains.

Real money paid against fake imaginary money that may or may not be there later….. (mind bending).

Start a service charge against the Reds and the Blues for each inside trade gain, since we can’t seem to hold our elected officials accountable for their blatant, in your face corruption toward the people they were elected to represent. That might help a bit.

Sorry this ended in a slight rant, delete this as you deem fit.

Haha.

You can borrow real money from that “fake price appreciation” through a HELOC or a margin loan.

Yeah…

I know, and I have done that to my benefit.

But my point was that it does not make sense to me, to tax it until it does become that real money…..

Just my thoughts.

You can borrow real money backed by nothing at all. See credit cards, student loans, etc.

Huck

How about they tax you on an assessed value…..

then you go to sell and get a price below that assessment.

Do you get a refund? You should.

I suppose I really have no true say in any of it.

I just don’t believe that the government should have a realized gain on a tax payer’s unrealized gain.

People can demonize asset holders, but what about the guy that saves to buy a couple hundred $ in stocks, or an ounce of silver/gold, or a dumpy empty city lot to try and get ahead…They will fall in the same bucket of demon asset holders, punished for prudence.

Either way, I will just play by the rules they give me….not necessarily the ones I wish I had…..or even maybe should have.

I learned long ago… if you are playing by baseball rules on the football field….

Gonna lose for sure.

She doesn’t “lose” 30% to capital gains. She gets taxed on 30% of the gains minus $250,000 or $500,000.

It’s amazing what running a 6-7% GDP government deficit will do to mortgage rates.

Mortgage rates will got over 7% in early 2026. The housing market will dominated by foreclosures.

Optimist! A 7% mortgage was normal for a very long time…

…back when we actually marked to market.

Back-to-back 1.8 trillion-dollar fiscal deficits don’t help.

Back to back? They’ve been in the trillion or two range since 2020. The only other time they were that bad in my living memory was after 08.

Wolf, all of us at our company read your newsletter every day. your newsletter is excellent an dead-on accurate. Your newsletter is easy to read, is loaded with the most current information in each issue, supported by historical data. I don’t know how you produce such important economic data each day without a huge staff. We love everything you publish and support you with voluntary donations. Congratulations and thank you for such a great newsletter. Steve Marks, CEO, Tower Investments, LLC.

Thank you, Steve!!

I agree, Wolf finds great data. But the data is there to be found. St Louis Fed is maybe the best single resource.

What sets Wolf apart are the explanations of market operations that no one else has and that I wouldn’t have a clue about on my own. Examples are: why did the repo market blow out a few years ago and how did the Fed redesign its tools to keep it from happening again? Or how did Silicon Valley Bank mismanage its interest rate risk and blow itself up mismatching long term assets with short term obligations? These are the types of analysis I haven’t found elsewhere.

I agree. Wolf uses reliable sources, what I wonder is how much off-balance sheet or outright lies are out there, especially in the commercial real estate space. I know of at least one 100+ million dollar property that is sitting vacant, yet the bank holding the note still claims the 100+ million dollar asset. How is this possible?

Until “mark to fantasy” dies, I don’t think anybody trusts anyone else’s books.

I believe banks can adopt an accounting system that allows them to mark assets at cost. I think they use this especially with bonds and notes, I assume they use it with real estate as well.

BTW, the Fed has “special” accounting procedures….

curious that GAAP are cast aside when inconvenient.

I stand to be corrected, perhaps Wolf can confirm or deny.

J J Pettigrew,

This is the second time I reply to your statement about the Fed and GAAP. The first time was on Nov 30. if you post the same statement a third time, I’m going to delete it.

Here is the copy-and-paste version from the first time:

Yes, by definition, the Fed cannot use GAPP because the Fed does not have a “cash” account, unlike all other companies. It does not need one because it creates money when it pays for something and destroys money when it gets paid for something, every second of every day.

GAAP is for companies. Companies have a cash account and have to take money out of their cash account to pay for something and put money into their cash account when they get paid for something. GAAP is not for central banks that create and destroy money instead of taking it out of or putting it into a cash account.

Yes, by definition, the Fed cannot use GAPP because the Fed does not have a “cash” account, unlike all other companies. It does not need one because it creates money when it pays for something and destroys money when it gets paid for something, every second of every day.

GAAP is for companies. Companies have a cash account and have to take money out of their cash account to pay for something and put money into their cash account when they get paid for something. GAAP is not for central banks that create and destroy money instead of taking it out of or putting it into a cash account.

Wolf,

Was he talking about the 4000 some US banks or the Fed itself?

As you point out the Fed has its own unique policy objectives, perogatives, powers, and – not inconsequentially – persistent failures.

So, perhaps GAAP is inappropriate for use by the Fed *itself*.

But that doesn’t necessarily apply to the 4000 some banks *regulated* by the Fed.

A different case would have to be made as to why GAAP should not be fully applied to *them*.

COMPANIES borrow off-balance-sheet, and that came up when two of them collapsed (Tricolor and First Brands). And they use GAAP accounting.

Neither the banks nor the Fed borrow off-balance-sheet. The Fed doesn’t do anything off balance sheet; even the Fed’s loans to the SPVs during the pandemic were on its balance sheet, and it reported what the SPVs had bought in detail. Banks don’t borrow off-balance sheet either, they don’t need to. But they might lend off balance sheet in certain complex structures.

Lower rates will lead to higher standards, unless we go back to free money policy. Which would lead to higher prices.

Either way you lose unless you grow up and live within your means.

I hope the experiance generation has found memories of their dinning out when they will never have an option of retirement.

You can play with your numbers all you want, but business investors wants certainty. We do not have that and all may change again with the next election.

“Certainty” requires a rules-based system where all the players are subject to the same rules and bad behavior suffers real consequences. The response to 2008 should have made it clear to every small business owner that this model no longer exists in America.

Interesting times.

The personal savings rate, percentage of disposable personal income, is well below the historical average.

because interest rates have been way too low for way too long.

Just as these low rates deter saving, they DO NOT deter govt spending.

The Fed used to be concerned with low savings , now they seem delighted to have forced people into the markets and real estate.

What’s your source for this? I feel like everything I read is the opposite.

Not OP, but: https://fred.stlouisfed.org/series/PSAVERT

Savings rate has been dancing around 5% for 20 years now, so I wouldn’t say ‘well below the historical average’, but it’s definitely embarrassingly low (you can’t retire saving 5% a year).

Thank you!

It’s almost like it matches the level up to where a company will do a 100% match in your 401k. I assume 401k’s are counted in the savings rate?

The savings rate is basic math: (total income from all sources minus total spending) divided by (total income from all sources).

In other words, the money not spent divided by the money earned.

interesting wolf regarding short-term rates trending up due to liquidity pressures. I also noticed yesterday that SOFR is up to 4.12, which is a relatively large spread vs the EFFR.

Real Interest rates should reflect recent real inflation. Artificially low interest rates created by fed gimmicks, QE, TALF, TARP, operation twist, etc. recently in the past choked off the savers living on fixed incomes because asset prices sky rocketed but incomes didn’t.

In otherwords since house prices went up 25% compounded YOY like they did in the not so distant past, posted fed interest rates should have reflected this. They didn’t, hence the current conundrum. This is not rocket science. The people that pulled the levers, tried to the cheat the math. Math won.

yappy

never a discussion about the “acceptable” 2% annual inflation rate trend line……which from 2021 is well below where we currently are.

An honest Fed would admit this is “unacceptable”. They don’t. They arent.

Thanks wolf

It’s been 3 years roughly and I still see the same “rate cuts tomorrow” slop from mainstream media. It’s so obvious, the manipulation.

The market can stay illogical longer than I can stay solvent though, but damn I was hoping to buy a house this year but the rate propaganda is holding everything up by the nerves and joints it seems like

Petulant bond market children….

In 2026 the spanking will come.

Economics dont really matter.

Super charged economy powered by those who make money in spite of bond traders.

Oh well the bond traders can go to other countries lololololololol on that idea.

Just stop. It’s painfully obvious how openly you’re shilling here for rate cuts and mass speculation that got the US economy into this self-destructive mess in first place, you’re even worse than the pivot-mongers on the financial news channels. Wolf has already posted up multiple charts and posts on why, in fact American homes are already seeing massive price drops in both big and small markets. And no longer just in the south and west. And these are nominal price drops, real value deterioration for housing (adjusted for inflation and actual costs for ex. homeowner’s insurance, property taxes, repairs) means even more real estate investors are massively in the red and underwater.

The pro-speculation fiscal and monetary policy you keep droning on about is a big reason the US birth rate has plunged so fast and young couples even with high incomes more and the more can’t buy a good home and start families, and fuels a lot of the inflation also causes things like daycare, care for seniors, healthcare, college, cars and even groceries to also be too expensive. The reckless Fed policy of QE and ZIRP, and reckless Covid over-stimulus from Congress (with all the PPP fraud) is direct cause of the Everything Bubble and cost-of-living disaster hundreds of millions of Americans are now facing. And this disaster policy from Greenspan and Bernanke all the way to JPow’s Fed is caused by what you’re advocating, too much coddling and moral hazard of speculators instead of focussing on price stability.

The longer this bubble in the USA is foolishly kept inflated, the worse eventual reckoning will be because of all the misallocations and excess liquidity and debt. Soon followed by the collapse of the US dollar itself as a reserve currency, then things get really ugly. We’re already seeing record auto repo’s and student loan debt, rising defaults and delinquencies on other debt and who even knows how much for BNPL and other forms of debt. This is what easy money policy leads to, it’s time to end it, take the hard medicine and move into healthier and more realistic valuations.

Inflation money making is an art in itself

Copper just set a new record high. Cu is perhaps the least volatile of all commodities. That may be because it is the element that underlies all industrial civilization.

Bond traders be damned

You sure appear to have it in for the bond traders. But you must agree that the only market that makes any sense is the BOND MARKET!

The world is no longer rational. Natural forces are not able to thwart the perversion of how economics actually occur. Using the old school methodology ignores other realitities.

1. Americans hate hate hate inflation and high prices. They have a history of voting governments and parties out of office under which this occurs. If inflation continues to rise, Republicans are sunk. They ran on inflation and won. Now it’s their baby. Everyone knows this. And they, egged on by DJT’s social media posts, will scramble over to the Eccles Building and beg the Fed to jack up rates to get inflation under control, and DJT will threaten to fire the new head of the Fed if he cannot get inflation back down 🤣

2. Long-term rates and mortgage rates are determined by inflation fears. Watch them blow out if inflation takes off.

Wolf is correct about the GOP. Personally, I think they’re already done — their attitude now is “either inflation is basically gone or it doesn’t matter anyway”. Have fun losing the midterms with that!

I didn’t expect this level of stupidity especially since Harris & others primarily lost in 2024 because of inflation. Did they think voters would give them a pass for what they voted against the DNC for?

DJT is the main game in town. I would not bet against him no matter how you feel about him.

1. Americans hate hate hate inflation and high prices. They have a history of voting governments and parties out of office under which this occurs. If inflation continues to rise, Republicans are sunk. They ran on inflation and won. Now it’s their baby. Everyone knows this. And they, egged on by DJT’s social media posts, will scramble over to the Eccles Building and beg the Fed to jack up rates to get inflation under control, and DJT will threaten to fire the new head of the Fed if he cannot get inflation back down 🤣

2. Long-term rates and mortgage rates are determined by inflation fears. Watch them blow out if inflation takes off.

When Powell is gone DJT will shine in all his glory….

Economics be damned….lol

1. Americans hate hate hate inflation and high prices. They have a history of voting governments and parties out of office under which this occurs. If inflation continues to rise, Republicans are sunk. They ran on inflation and won. Now it’s their baby. Everyone knows this. And they, egged on by DJT’s social media posts, will scramble over to the Eccles Building and beg the Fed to jack up rates to get inflation under control, and DJT will threaten to fire the new head of the Fed if he cannot get inflation back down 🤣

2. Long-term rates and mortgage rates are determined by inflation fears. Watch them blow out if inflation takes off.

I’d actually argue the opposite. The bond market trades largely based on what should happen without Fed intervention. The stock market trades based on the assumption of Fed intervention to support asset prices.

Who is right? So far, there is a clear winner. The Fed has consistently done “what it takes” in response to unemployment threats, including asset price drops.

I don’t think the Fed as been responsible in that regard. They should be thinking more about long-term sustainability, as opposed to short term recession avoidance.

“They should be thinking more about long-term sustainability, as opposed to short term recession avoidance.”

I think they learned their lesson regarding QE.

ShortTLT, we’ll see soon if they learned anything. They did let stocks drop 20% when tariffs were announced, without a response. That’s a good sign. But Hoenig thinks they’ll buckle under pressure if long rates rise.

They also let the market drop in 2022.

The bond market can punish the Fed for doing QE just like it has for cutting rates. The Fed can’t keep buying bonds forever to make the problem go away… they’re not trying to copy the BoJ.

I’m puzzled why the equity markets generally view rate cuts as so bullish, as I gather they do, despite the tenuous effect of the cuts on long-term rates, which I gather have a large impact on economic growth. What might I be missing? Is it that rate cuts do reduce short-term rates, and those reductions often increase corporate earnings, and generally stimulate economic growth? Thanks for peoples’ advice on this.

What you’re missing is that fundamentals don’t matter to markets. Rate cuts being bullish is just a media driven narrative to make people hit the buy button.

Constant examples of how fundamentals don’t matter… Recently Nvidia reversal a couple weeks ago and last week a 4% rally on a holiday Thanksgiving week with no news. Government shutdown and reopening market movement…etc

I can explain. A rate hike is bullish because the economy is doing great. A rate cut is bullish because, obviously, money is cheaper. Rates unchanged are bullish because we are in a goldilocks zone. Learned all of this on CNBC.

in addition to amdy’s astute observations, i think there are a non-zero amount of people that view equities (assets) as an inflation hedge

“These mortgage rates of 6% to 7% are not high by historical measures”

That’s true, are the living costs normal by historical measures? In 1970 one graduated and could afford to have a family. The 1970’s person today lives at home and likely can’t afford a car.

I think it’s time the Unites States consider that it has made some kind of colossal blunder that may have stripped an entire generation of making a life. And it is headed down doing the same for it’s very elderly.

The Fed speaks of a cut down to the 3.5 . 3.75 range….

do they not see the scramble for money at or over 4% in the SOFR ?

It would be interesting to read your views on trends in TIPS yields and prices. Is the small size of the market–under 10 % of total Treasury debt–the reason for this omission?

I have discussed TIPS in the comments a bunch of times, including how they’re different from other bonds, how they work, what the tax implications are, that we bought some, etc. Big detailed posts, starting last summer. Just because you missed them doesn’t mean I didn’t write them.

One cold, foggy wintery day, Uncles Donnie and Jerome woke up and discovered that they don’t actually control interest rates. Some unknown, powerful force overpowers even them. it was on that day that they realized they were mere mortals.

The “king” really does have no clothes.

Michael Burry gave a podcast interview today – and said he thinks the neutral rate is probably around 4%. The fed shouldn’t be cutting and he actually thinks we should get rid of the fed, that they’ve done more harm than good since their inception. I have never agreed with anything more.

A neutral rate of 4%? 😳. Yeah, sure! Do you think since 2020 inflation has been 4%? Not on my street it hasn’t.

CPI inflation, as per the BLS, increased by 27% since 2020. But that’s over nearly five years.

Having politicians directly in control of the monetary levers does not sound like a good idea to me. A truly independent Fed would be a good thing IMO. Unfortunately, as 2008 revealed, the Fed is NOT independent, but rather the greatest enabler of bad behavior the world has ever known.

More and more big names are starting to talk about a return to QE as not only possible, but likely. This system is rotten to the core.

That is terrifying. That won’t make housing affordable – that will make it take off again. As well as cause massive inflation. Have they not seen what inflation has done to other countries?

Does trump not realize that he won the election because people were pissed off about inflation? Bring inflation back above 5% and we’ll have a democrat in office in 2028. I’m not sure why he’s pushing so hard for lower rates. At first I thought it might be just PR while secretly hoping they stay high to kill inflation, but no he definitely wants the cuts for some reason.

I also wouldn’t be surprised to see a lot of Democrats elected in the interims either. People are still pissed off about everything being expensive…. the general public is fickle.

The publicly volatile DJT is much more predictable than the media would have you think. The man values and respects two things, money and power. Fellate his ego and you win, pad his pockets and you win.

Why does he want the rate down? It personally benefits him. His money is real estate, after all. It’s the same reason he overheated the economy right before COVID, same song and dance.

Depth Charge

Growing the balance at the same rate as the economy grows is NOT QE, it’s how the Fed has always done it before QE.

Don’t spread BS here.

It’s when the balance sheet grows faster than the economy, that QE is involved. Everyone knows that, but some people twist everything into “QE” for manipulative purposes.

We’ve discussed the details here MANY times, including this chart:

Wolf, you don’t think Thomas Hoenig, a former FED official, knows what QE is? He said “Are we going to go back to QE? The odds are that we will.” I am not spreading BS, this was a frightening thing to hear from somebody like him. It seems no lessons were learned. I am starting to believe that we have nothing but rapaciously greedy, deranged narcissistic lunatics intentionally destroying the country to take every last morsel for themselves.

1. He is not a “big name,” as you said. He was mouthing off in a podcast. Like anyone else in a podcast. He has no insights into the future whatsoever. That guy is 80, been retired from the Kansas City Fed for 15 years, and now says whatever.

2. If there is a catastrophe, such as Covid, or a financial crisis like we had in 2008, the Fed will use QE to deal with it. But it likely won’t be long-term QE. That’s very different from your statement “More and more big names are starting to talk about a return to QE as not only possible, but likely. This system is rotten to the core.” which implies QE coming soon, which is twisted BS.

3. You’re QE mongering on my site. People get blacklisted for that.

“You’re QE mongering on my site. People get blacklisted for that.”

I’m not QE mongering. I absolutely despise QE. And I despise those people who are constantly hyping that QE is right around the corner again. I don’t think there should ever be QE again, Ever. The damage from it is still occurring.

2028 will be a watershed. A lot of people thought an “outsider” would save them from the corruption of the two major parties. They’ve now discovered that the outsiders are just as corrupt as the insiders they replaced. Being mired in corruption is the only way to raise the sheer amount of money required to obtain power in the US.

Historically, the stage is set for a major change as all the viable options are equally corrupt. Retirement of the Boomers will clear the way for something else.

The chair now recognizes Marjorie Taylor Green and Alexandria Ocasio Cortez for 5-minutes, Mr. Speaker.

Don’t get your hopes up.

AMZN, NVDA, Googl and AMD chips will cannibalize each other. Wafer

Quantum chips, produce like semiconductors, will cannibalize the

winner within 3/5 years.

When is Congress going to do its job and pass the appropriation bills that were suppose to be done by Oct 1st 2025? I hear they are now planning another recess for the holidays. They have no plan to pass anything before the the next CR, Jan 31st 2026, which could trigger another shutdown.

And would another shutdown would be no economic data again?

The GDP calculations include govt spending.

Govt spending increases as the borrowing increases. Borrowing is uncurtailed when rates are too low and the Fed too accommodative.

When the Fed is loose, the Govt spending expands, the GDP gets a bump, and the Fed has reason to meet the expanding economy with loose policy. Rinse, repeat.

There is something circular here.

It used to be the Fed expanded things to meet the expanding economy.

Now it seems the Fed expands things to make it seem the economy (GDP) is expanding, which then gives them reason to further expand…..round and round.

Somewhere along the line, probably 2009, the cart went before the horse. IMO

No, GDP does not include “government spending.” It includes only “government investment and consumption.” Lots of government spending is not included in GDP, including interest expense and salaries of government employees.

I love this site- Wolf maintains a sharp focus on economics without getting too political. (even if the comments stray into the weeds a bit, as above)

I also find myself going down rabbit holes on Substack- with Michael Burry, Charles Huge Smith, Adam Taggert, John Rubino, and even fringe authors like Jim Stewartson- wow! Krugman is on there, and Michael W Green has been addressing poverty, inflation and some very prescient socioeconomic issues. I don’t know how the Substack algorithm works for what bubbles up in your feed- but it’s been feeding me a lot of fascinating rhetoric.

One story floating around in particular is political with severe economic implications- Trump’s peace proposal for Ukraine and European response and posturing: in a nutshell, the EU and possibly Canada together have a red line- any deal that cedes Ukrainian territory to Russia, they are threatening, will trigger massive liquidation of their US treasuries. This would cause economic chaos here. If true, it would indicate the EU has had it’s surfeit of appeasing and boot licking Trump’s giant ego. I don’t know what to make of this story- perhaps it’s yellow press. If true, and if we continue to see so much idiotic, belligerent behavior it would be quite interesting if the rest of the world were to play this card. Should something like this come to pass I will enjoy Wolf’s take on it. This would be economic warfare waged upon us by our allies.

As for mortgage and long term treasury rates jumping, this is no surprise as the informed readers of this site know. Massive treasury dumping by foreign countries would be a surprise, and have even more profound effect than short term cuts.

Curious if anyone thinks something like this is likely in our future?

Norway, Qatar, now Cyprus among some other places, in fact the gas fields discovered recently for Cyprus are some of biggest in the world. Other fields in the Baltic and Mediterranean too, some recent discoveries. And despite all the FUD headlines (and being fair some mis-steps before) the EU has developed it’s renewables sector very well and fast, not as aggressively as China but still enough to steady reduce gas reliance. And China is moving so fast on renewables it’s also reducing it’s own gas dependence so global supplies can go elsewhere.

So there’s less reliance on nat gas in general and even less on imported. And what does need to be imported a lot of it can come from sources above, even before Cyprus’ supplies come fully on-line. LNG prices in fact have been dropping so clearly there’s a lot of global supply with weakening demand, so it’s false to assume particular suppliers have some kind of magical ability to apply any kind of pressure. Our LNG is one source in the mix but one of many, and suppliers don’t have the luxury of just letting their product sit without selling even at a discount when needed. Just strange in general some of the comments assuming some kind of big chess match with suppliers of resources trying to make demands, in the real world sellers have to sell. It’s the same reason home-builders in the US don’t have the luxury of just sitting around with over-priced homes and have to lower the price even if it means smaller profit, if they don’t do that they go under and lose everything. There now more sellers of LNG and other sources of natural gas for Europe, they have to sell and supply and that’s what they’re doing.

LNG is a global commodity in oversupply. There are other large LNG exporters out there that would love to get that business, including Australia and Qatar.

“in a nutshell, the EU and possibly Canada together have a red line- any deal that cedes Ukrainian territory to Russia, they are threatening, will trigger massive liquidation of their US treasuries. ”

That story is a mix of idiotic bullshit and braindead market manipulation, spread by some moron bloggers that are short Treasuries and YouTubers trying to get clicks or sell financial services to scared people? And people just swallow that idiotic BS hook, line, and sinker? the internet never ceases to astound me.

“the internet never ceases to astound me.”

Give it another 5 years worth of AI clanker proliferation.

I read an article claiming that Bessent and Miran (both FX traders in past) are pushing for lower short term rates in order to lower hedging costs for foreign treasury buyers (since hedging costs are a function policy rates gaps between central banks). Lowering short term rates would enable more hedged treasury buyers which is good for US manufacturing (less upwards pressure on the dollar) and long term yields. The article is by Michael McNair in his substack.

the kinds of BS circulating out there in the wild is just astounding.

In response to the idea that real estate prices need to go down how would that affect bank balance sheets in respect to downgrade of asset value? It seems you want a wholesale drop of all asset values to a substantial level. If so how do you deal with this reality?

genosurfbr

🤣❤️ You haven’t been paying attention for 15 years. You need to read the articles here. They explain: Only a very small portion of residential mortgages are on bank balance sheets. A large majority have been bought and securitized by government entities, and these “agency MBS” were sold to investors, and they’re guaranteed by the government and trade similarly to Treasury securities. An additional chunk of mortgages that didn’t qualify for government guarantees (“nonconforming”) were securitized and sold to investors (“private label MBS”), and investors carry those risks. Banks are mostly off the hook. That is one of the biggest changes that came out of the Financial Crisis, and you missed it?

I have been detailing this for years in my housing articles and comments, most recently in this article from Nov 7. This passage is quoted verbatim from the article:

https://wolfstreet.com/2025/11/07/here-come-the-helocs-mortgages-housing-debt-to-income-ratio-serious-delinquencies-and-foreclosures-in-q3-2025/

Who’s on the hook this time?

Among the most important changes resulting from the Financial Crisis was the transfer of mortgage risk from banks to taxpayers. There won’t be another mortgage crisis for banks. They’re largely off the hook.

Banks and credit unions are on the hook for $2.7 trillion in mortgages, HELOCs, and second-lien mortgages, according to Federal Reserve data on bank balance sheets. That amounts to only 19.7% of the $13.5 trillion in mortgage and HELOC debt.

The government is on the hook for $9.1 trillion of single-family mortgages that were securitized into MBS and sold to investors, according to Ginnie Mae data. If borrowers default, the government eats the loss. For investors, these MBS have a similar near-zero credit risk as Treasury securities. The investors include bond funds, pension funds, the Federal Reserve ($2.1 trillion and shrinking), banks, mortgage REITs, etc.

And subprime-rated mortgage debt is insured by the government through the FHA.

The share of government-guaranteed single-family mortgages outstanding:

Investors are on the hook for $1.7 trillion of residential mortgages, such as jumbo mortgages that didn’t qualify for government backing. These mortgages have been packaged into “private label” MBS and sold to institutional investors around the globe, such as pension funds and bond funds. It’s these investors that carry the credit risk for those mortgages. Banks are off the hook.

The bond market really doesn’t know what to do at this point. An administration and Congress recklessly cutting taxes and increasing spending (on wasteful items). Borrowing at a rate that has never been seen before. Trying to take away essential services and deporting people that actually contribute to the economy without benefiting from government programs. An administration that won’t produce numbers, calls them into question, and puts in people that can’t be trusted to provide accurate numbers. A fed that doesn’t seem to be too independent anymore. A fed that missed the mark big time twice already.

I’m surprised rates aren’t higher than what they are. The ultra rich controlling this poop show must be real confident in the mess they have created.

The mortgage on my home has 6.8% interest rates in 2007. I have a near perfect credit rating score. The current rate is not very high.

I see the 10 year Treasuries, which tend to drive mortgage rates, are back above 4.14%. Trump does not seem to understand that when the Fed lowers interest rates, over the past year or so, long-term Treasuries react by going higher, because they are worried about inflation. Bessent and the rest of Trump’s staff are probably afraid to tell Trump this.

Back in September 23, 2024, a week after the Fed started the current cycle of rate cutting the 10 year Treasury yield was 3.94%. After two rate cuts, and the market pricing in another next week, the yield is 4.14%. The numbers for 20 year Treasuries are more impressive: 4.13% in September of 2024, and 4.72% today. I would not be surprised a week or so after the Dec 10 2025 cut, the 20 year yield goes up to 5%.