Long-term Treasury yields under pressure, amid large auctions of notes and bonds, despite shift to T-bills.

By Wolf Richter for WOLF STREET.

This week, despite being shortened by Veterans Day when the bond market is closed, the government sold $694 billion in Treasury securities spread over 9 auctions on three days.

Of these auction sales, $549 billion were Treasury bills with maturities from 4 weeks to 52 weeks, including $110 billion of 4-week bills, and $101 billion in 6-week bills.

| Type | Auction date | Billion $ |

| Bills 6-week | Nov-10 | 101.1 |

| Bills 13-week | Nov-10 | 91.5 |

| Bills 17-week | Nov-12 | 69.2 |

| Bills 26-week | Nov-10 | 81.8 |

| Bills 4-week | Nov-13 | 110.3 |

| Bills 8-week | Nov-13 | 95.3 |

| Bills | 549.1 |

And $144 billion of the auction sales this week were notes and bonds, including $48 billion of 10-year notes and $29 billion of 30-year bonds.

| Notes & Bonds | Auction date | Billion $ |

| Notes 3-year | Nov-12 | 67.0 |

| Notes 10-year | Nov-12 | 48.5 |

| Bonds 30-year | Nov-13 | 28.9 |

| Notes & bonds | 144.4 | |

| Total auction sales | 693.5 | |

The note and bond auction sales replaced some maturing notes and bonds, and added a lot of new debt, and this is where the debt grows in leaps and bounds. For example:

The $48.5 billion of 10-year Treasury notes sold at auction this week at a yield of 4.07% replace $24.1 billion of 10-year notes that were issued in November 2015 at a yield of 2.30% and mature now: The issue amount doubled, and the yield is 1.77 percentage points higher, on double the principal!

T-bills mature constantly in huge volume and have to be replaced with new sales just to stay level. The $101 billion of 6-week T-bills sold on November 10 will mature on December 26 and will be replaced via new auction sales, plus whatever amounts will be added to the auction to fund the ongoing deficits.

The $82 billion of 26-week T-bills sold this week will mature on May 14, 2026, and will have to be refinanced then via a new issue, plus whatever new funds will be needed to fund the additional deficits.

As the T-bill pile grows, the auctions get larger and larger as maturing T-bills will have to be refinanced, on top of the issuance needed to fund the ongoing deficits with new T-bills. So the already huge T-bill auctions will become gigantic.

But so far, so good. These T-bill auctions are well-oiled machines. Investors, including big companies, often use T-bills on automatic rollover to manage their cash, like they would use money market funds.

The Fed is also preparing to replace maturing MBS with T-bills after QT ends in December. MBS will continue to come off the balance sheet after QT ends until they’re gone. At the current rates at which MBS come off the balance sheet, the Fed would buy $15-19 billion in T-bills a month. The market has to continue to absorb that amount of MBS. The Fed has already shed $670 billion of MBS since QT started, but still holds $2.1 trillion that it will replace with $2.1 trillion in T-bills as these MBS come off over the next few years. And investors are going to have to absorb an extra $2.1 trillion in MBS.

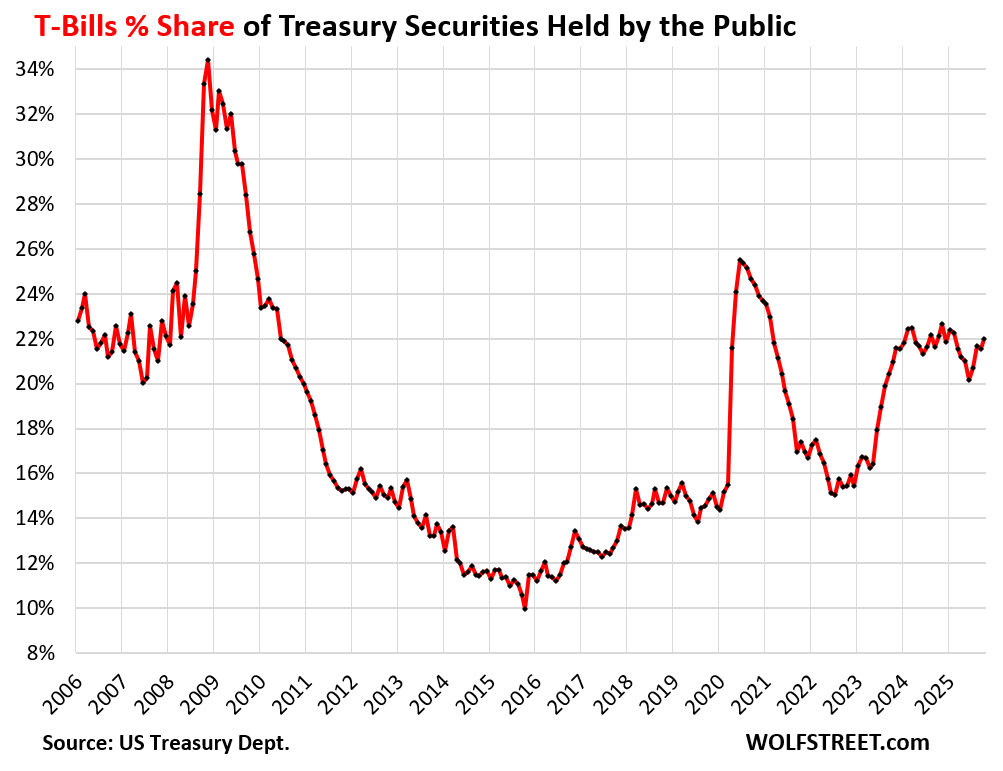

T-bills outstanding ballooned to a record $6.59 trillion by the end of October, but notes and bonds outstanding ballooned too, and so the share of T-bills of the overall marketable debt isn’t setting records:

T-bills’ share of the $30.0 trillion in marketable Treasury securities (= total debt minus securities “held internally,” such as by government pension funds) at the end of October rose to 22.0%, which is high, but well below the two recent crisis dates.

During crisis events, the government issued huge amounts of T-bills quickly to fund its sudden stimulus and bailout expenditures, which for short periods causes T-bills’ share of the total to spike, such as to a 34.4% share in November 2008 during the Financial Crisis, or to a 25.5% share in June 2020. During those times, the Fed became a huge buyer as part of its QE program.

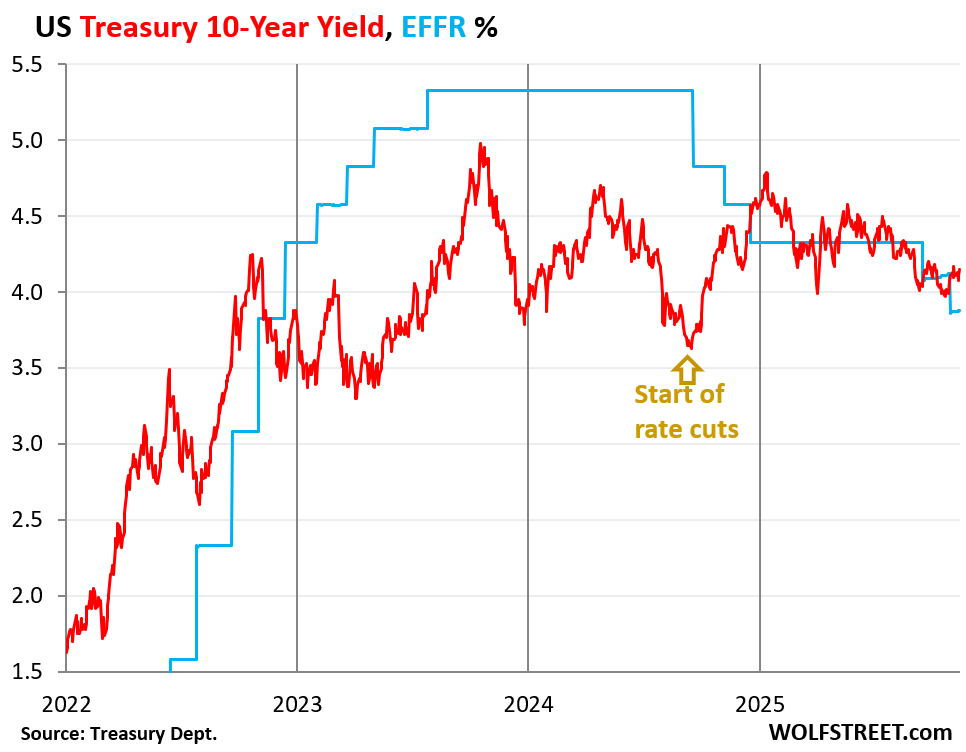

Long-term yields are under pressure, despite the rate cuts by the Fed. The 10-year Treasury yield rose today by 4 basis points to 4.15% currently, after having dipped below 4% just before last rate cut.

The 10-year Treasury yield (red) is now 27 basis points above the EFFR (blue). In normal credit markets, long-term yields, such as the 10-year Treasury yield, are quite a bit higher than short-term yields, such as the EFFR:

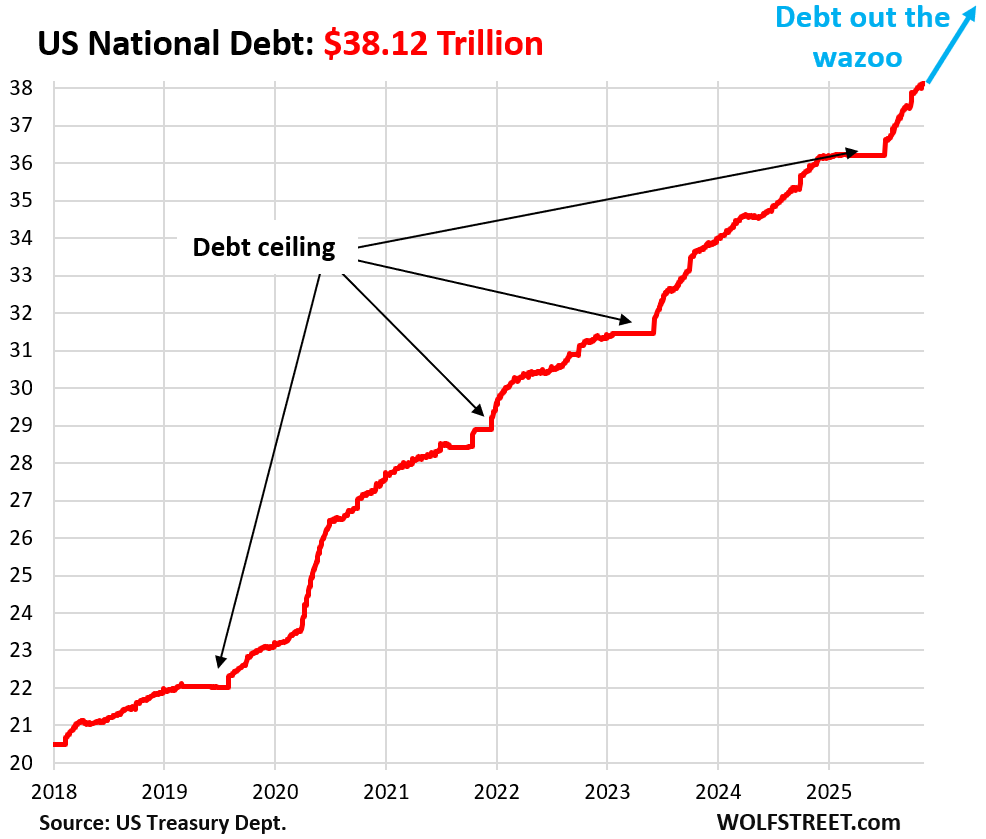

The ballooning federal debt hit $38.12 trillion as of November 13. The portion of the issuance that replaces maturing debt does not add to the US government debt. But the additional issuance to fund the new deficits adds to the amount of the debt.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

$38 Trillion, if you print it all in 1 dollar bill, is there enough to cover the entire landmass of United States? We throw around T like it’s nothing but…

Btw, things are going in wrong direction, but good to see at least 10 yrs is heading higher if it means giving fixed income investor a fighting chance at TINA and also keep mortage rates higher so RE agents can STFU about 30yrs rates dropping soon…

“Long-term yields are under pressure. The 10-year Treasury yield rose today by 4 basis points to 4.15% currently.”

I wonder how much debt must the U.S. have for buyers of U.S. Treasuries to start worrying that the U.S. gov’t won’t pay back their Treasuries, or worry that the Fed will be printing so much money that the inflation rate will be higher than the interest rate on the Treasuries.

Everyone is now Alfred E. Neuman saying “What, me worry?”.

If you knew that amount / date, you could make a lot of money.

I sincerely believe things start to fall apart in the next 5 years.

We will be into the final push of Boomer retirements with GenX retirements starting to ramp up.

The SSTF will most likely move forward from a 2032 insolvency date to 2030.

It hard to imagine we don’t have a recession sometime in the next five years, which means there will be a big increase in debt.

AI job losses will be in full swing.

Thinking outside the box:

The US government could attempt to issue long term zero bounds, say 30-50 years. Then, we remove in government accounting all the interest paid of $1-1.5T annually. Might temporarily balance budget. GAAP accounting requires amortization of annual interest on the discount, but government accounting does not. How large would face amount of new bonds be? Someone with present value calculator using today’s 30 year rate could compute.

So you say no one would buy them? Because they would not trust the US government to have capacity in 50 years to pay them?

Well, that is what we have today? The government only “ pays” interest annually by borrowing the same amount? Not really paying.

Think about it , IF my equalization comparison holds water(?), then what rate would investors

/buyers demand?

Next, and separate out of the box thought, what if the FED BOUGHT all $38T outstanding US Treasury debt tomorrow, grew their balance sheet and injected $38T cash DOLLARS into the world and US economy. That money starts out in the hands of the big institutional bond holders. Where would it go next?

TOO MANY DOLLARS CHASING THE SAME ASSETS?

Okay, so all asset values skyrocket. Is that good or bad? I thought FED wanted inflation (3% ). Let’s look at the assets closest to the consumer like food and homes. Both go up substantially. But, if a consumer can never again buy a house , what does happen in a few years when no working man can ever buy a house? Does price end up dropping?

Alright, that’s enough. Just showing what really going on by accelerating time frames. Hopefully a smart reader or Wolf can analyze results.

CountryBanker,

Along the lines of what you are saying, I believe that Chile(?) and a handful of other nations have previously attempted to stop capital flight/currency crises/force down domestic interest rates by *compelling* national pension funds/etc (basically any institutional investor) to hold some significant fraction of their portfolios in domestic government securities.

(Thereby accomplishing what the Fed has – so far – been able to do in the US – force down interest rates artificially – by printing money. Compelled Treasury Buyers = Lower Domestic Treasury Rates.

Other countries have to be much much much more careful about money printing – many have destroyed their economies this way because the domestic real asset base was much much smaller than the US’ historic real asset base…leading to wildfire inflation compared to the US…so far).

Let’s see… A dollar is ~16 square inches. That’s 9 dollars per square foot, which makes for 4.22 trillion square feet, or 150K square miles. But the US is 3M square miles, so we’re not even 10% of the way there. We have a lot more debt to go!

That is the correct way to evaluate the seeming illogic of the trajectory of the best of the best. The cream that has risen to the top.

The Ivy league.

“But the US is 3M square miles, so we’re not even 10% of the way there. We have a lot more debt to go!”

LOL, I think you’re on to something, this might be the way to measure our debt level and instead of the scary digital debt clock, our national debt is only less than 10% of total land mass…fantastic, we’re doing well/

This reminds me of the pond scum story. It doubles coverage every day and took all summer to cover half of the pond. When will it cover the pond entirely?

tomorrow.

Exponential functions are a bear.

@b bj, tomorrow.

Washington DC is only 68 square miles.

The national debt should be piled up there.

150K square miles of debt, divided by 68 square miles… DC would be papered over, repeatedly, more than 2000 layers deep.

Given the thickness of a dollar bill (0.0043 inches), DC is mired about a foot deep, in fact.

No wonder everyone there is trying to get some of that money to stick to themselves!

P.S. Don’t forget all the state, county and municipal debts, the corporate debts and real estate mortgage debt… already all over the U.S. the nation would be about 50% covered. Not including ufunded mandates, fraud and bezzle…

$38 trillion in dollar bills laid flat would be about 152,000 square miles. That is almost enough to cover the state of California. If laid end to end, they would reach the average distance from the Sun to Pluto or 3.7 billion miles.

Surely the debt situation is unsustainable? Grow economy through increased productivity, cut spending, default or default through high inflation.

Wolf, what is your prediction?

I think that the world’s governments will pull out the monetary stops to avoid a recession.

A normal economic event that occurs in the capitalist cycle, generally considered, necessary, like the fall and the winter.

This government is flirting with an inflationary policy that will accumulate ownership unto the class that hates taxes.

Yeah……taxes are now pretty much equated with many other things that are largely considered “evil” in the USA, at least by those who have any say in running the country.

The only people who would like even a modest increase (much less the beautiful 1960 tax tables with MANY brackets) are branded as lacking moral character…..to “work hard”, I guess.

Including yours truly….

I still believe a better Gov’t-Private balance can be achieved……but the big money says, “Absolutely NO! Wrong direction!”

3-5% CPI inflation with occasional flareups and 3%+ economic growth will keep the debt more or less under control. If economic growth slows, it would take more inflation.

But then we’re back to the debasement trade, and iirc you recently wrote an article about how debt holders still weren’t ready to subscribe to that hypothesis as they were buying debt at the current yields.

At some point someone will have to be wrong. Either stock holders get rinsed or debt holders, or both.

“Or both,” maybe even all 3: the folks who neither hold stocks nor bonds but are simply trying to live while using the USD?

The US commands 34.5% of global government debt, over twice the next guy (China). The total government debt is about $111 Trillion. Global GDP is about $111 Trillion.

The USD is involved in between 60-90% of global transactions.

I see the equivalent of paying the bills with a payday loan, and taking out more loans, to cover the payday.

We’re approaching an event horizon (which we had a preview of) of uncontrollable global inflation.

The timeline and magnitude are unknown as is the resolution (change of currency, one world government/ “IMF intervention” type scenario, or war; kinetic or financial).

Interesting times indeed.

Wolf,

1) How does that, say 4%, annual CPI inflation compare to the average for the 50’s/60’s/etc.?

(I know it is borderline annoying to foist uncompensated work on you, but the CPI inflation data might be fairly easy to get/post.)

My broader implied point is that *sustained* 4% CPI inflation may be something outside of US living memory (and ugly as sin to boot).

4% *sounds* lowish, but the miracle of compound interest becomes a curse in the context of inflation. My semi-educated guess is that post-70’s we’re maybe talking about a 2% inflation average.

2) Occasional “flare-ups” sounds scary as hell given what happened in 21-22.

Was inflation the only real fix that the powers that be ever really had to “fix” the relentless macro failures of the last 50 years (fiscal/trade deficits?)

3) Consider the irony of 20 years of inflation-baiting ZIRP followed by inflation as a policy “fix”…

On one level, perfectly predictable (although continuously denied by the powers that be).

On another level…madness (2012-2020 – zero rates, 2022+ lucky to avoid high single/low double digits (I exaggerate but not by much…)

4) In retrospect, those “deflation is the devil” pieces pumped out in 2002 are truly, truly disgusting.

Imagine what might have have occurred had not the “best minds of the commanding heights” pushed that particular line of self-serving baloney.

From consumers “could have shared in the China price” to “only inflation can save the country” in just 20 years.

“1) How does that, say 4%, annual CPI inflation compare to the average for the 50’s/60’s/etc.?”

Look up annual CPI rates anywhere that has CPI rates, including FRED. You’ll see what annual inflation was in any time period going back to the 1040s. I have posted charts like that too

I post charts like that this, all you have to do is look at them, most recently Feb 2025:

2. “My broader implied point is that *sustained* 4% CPI inflation may be something outside of US living memory (and ugly as sin to boot).”

Depends how young you are. Between 1968 and 1992, annual CPI rates were mostly higher than 4%, and in 1980, over 3x as high. So that’s within my own “living memory.” Before my own living memory, there were also periods like that.

Thanks for the chart.

Knew the 70’s were bad – but it really is interesting why exactly an oil price supply shock (admittedly hugely inflationary for *gasoline*) would have such a huge knock-on effect for the entire CPI (how much could gasoline possibly make up of the CPI that its price would skew the entire index?)

And…in contrast, we have 2003-2008 – with oil going from $30 to $100 – and yet the CPI overall increase is maybe 4% on average – a small fraction of the 1970’s madness.

I know there are complicating factors (housing cost explosion in 70’s as well…but why? Doesn’t seem enormously gasoline linked…and aughts saw China price help offset oil prices to restrain indices).

Chart is useful but it really does make me wonder about the constituent parts of the CPI and how their weights really seem to change over time.

The dominating drivers for inflation (or lack thereof) really do seem to vary over time by quite a bit (70’s – oil, aughts – China to allowed degree…, 20’s – housing).

To a degree it makes sense, but the knock-on effects sometimes seem awfully unpredictable.

The aggregate number doesn’t reflect the reality of debt servicing ability. So far so good. Just pray there is no recession. Inflation is still here. It looks like debt holders are screwed. Why do they buy long bonds with such low rate is puzzling.

1. “The aggregate number doesn’t reflect the reality of debt servicing ability.”

The economy will do just fine with 1 million mortgage default (there were over 10 million during the mortgage crisis). The banks will do just fine no matter what because they’re not on the hook anymore – the federal government is. If you look the homeowners who bought during the peak of prices, those mortgages are at risk if prices plunge, but they’re a relatively small number. How often do you want me to re-re-re-explain this? Anecdotal feel-sorry-for stuff is just nonsense when it comes to the overall economy. Go to a social justice blog to get your fill. The only thing that matters to the overall economy is “aggregate numbers.”

2. “Why do they buy long bonds with such low rate is puzzling.”

Agreed. Buying long-term Treasuries is fine if yields are high enough. I don’t think yields are high enough. TIPS are different though. Their return goes up faster than CPI inflation, guaranteed for the term of the security.

“but they’re a relatively small number. How often do you want me to re-re-re-explain this?”

It is because the Fed “wealth effect” black magic makes it very, very easy to have misleading impressions as to how the *whole* housing market is doing.

Sure, maybe only 5 or 6 million RRE transactions went off during during peak Pandemic stupidity – for a cumulative 11(?) million out of a total base of 85(?) million SFH.

But that ain’t the way the “median” prices for peak 2021/2022 got reported – the reports were/are for “the housing market” which makes it sound like the whole 85 million enchilada.

That is the “wealth effect” reality distortion field the Fed wants (when prices go up…) and that is mostly what the Fed gets.

But the inevitable result is that the publc gets mind-screwed with incorrect impressions as to how many SFH traded at peak pandemic prices.

(The same reality distortion dynamic surrounds hazy discussions of an equity’s “market cap” – just because *today* 1% of shares went off at X dollars, doesn’t mean that 100% could…but that is what “market cap” implies).

I wonder when do buyers of U.S. Treasuries start to worry that the U.S. gov’t won’t pay back their Treasuries, or worry that the Fed will be printing so much money that the inflation rate will be higher than the interest rate on the Treasuries. How much debt does that have to be ?

The Federal Reserve is doing QT to reduce funds outstanding and are not increasing any funds to buy more US Treasuries and that will continue to be the case for the foreseeable future and is the opposite of inflationary.

Incorrect. J-pow has halted QT. A truly independent Fed would continue QT and leave the FFR where it is, forcing CONgress to be fiscally responsible.

Incorrect: J-Pow WILL halt QT on Dec 1 (today is Nov 15).

Close enough. Not much is going to roll off in the next two weeks. The point stands. The Fed is NOT “independent” and should continue QT until CONgress balances the damn budget.

About $16 billion in MBS will come off and about $4 billion in Treasuries, for $20 billion combined. Other things are coming off too — I mentioned two of them in my last balance sheet article on Nov 6. So my next balance sheet article, which will cover November, could show a decline in the $30 – $40 billion range compared to the prior month.

The only unknow is the SRF. Month-end November could show a run-up in the SRF, which would begin to abate on Dec 1. The weekly balance sheet that covers the end of November will be as of close of business on Dec 3. By then the SRF might have totally settled back down, or maybe not. So that’s the unknown.

QE and purchase of MBS was especially corrupt and simply rewarded bad behavior.

Either way this will be a default. Default or pay back with worthless dollars. All the same. Just a matter of time. Our politicos do not appear to be aware of this.

Gunning up for an unnecessary war with whoever the identify as the enemy (Nigeria Venezuela) with borrowed money. What a waste.

Many of our politicos will be dead before any doomsday scenario happens most likely.

Many already appear to be so, at least from the neck up (Meatheads)

AB here.

ZERO chance of that happening. A country that controls its own currency cannot default on debt issued in its own currency because the central bank can always print enough to support that debt. So get that off your worry list.

Inflation should be on your worry list, 3-5% inflation with occasional bigger flareups.

It is on MY worry list, but what’s alarming is that neither the central bankers nor the legislative and executive branches seem to care much at all. There was a token attempt to contain inflation but they wrapped that up by 2024 at the latest. For the rest of us, it is very dangerous how cavalier these people are.

It’s easy to blame the government, but the real blame falls on the American people, who aren’t willing to actually tolerate any austerity that would get the deficit and spending under control.

So inflation it is.

TSonder: The American people don’t have much say in what we do/ don’t “tolerate.”

I was greatly alarmed, and did not want to “tolerate” the pandemic blanket free money that was directly deposited into my account (they have my digits and didn’t ask).

I foresaw a myriad of negative repercussions, including a potential wave of inflation. Should I have voted for the 6th party candidate?

The concept that there’s no possibility of inflation, without QE or whatever, or if I tighten my belt or pray or something to that effect is just not realistic.

If I had a Trillion for every year I have been alive (clearly: shame on ME)….

I think J-Pow and some of the others are secretly, or not so secretly, VERY worried about inflation. They have seen the monster they created and they are scared of it, but they are also under immense pressure from their big banker buddies and now the administration to avoid a come down that sucks everything and everyone down a black hole we can’t crawl out of. I console myself with the idea that we are very adaptible as a species.

Brendan,

Re: They have seen the monster they created and they are scared of it..

Bernanke got Nobel prize for releasing QE-Frankenstein. He also wrote a book “Courage to Act”. They are not scared. The firemen are also the arsonists.

TSonder305,

“It’s easy to blame the government, but the real blame falls on the American people, who aren’t willing to actually tolerate any austerity that would get the deficit and spending under control.”

That is a false statement. The blame does not fall on the American people. The blame falls on the two-party political power structure that rules the Legislative and Executive branches of government.

“American people” are powerless to change anything in a quick or meaningful manner. We have a vote every November, yeah, that is so. But the people, the masses who do vote every year, like I do, really have no option on the ballot. The UniParty controls things.

TSonder305, I call bullshit on your comment. I am an American person. The deficit spending and national debt in the USA is not my F-ing fault!

The Struggler and Prairie Rider,

Obviously I’m not referring to all people, as individuals, but the American people, as a whole.

Korzybski also stressed that sanity requires the awareness that “whatever you say a thing is, it is not”, because anything expressed through language is not the reality it refers to: language is like a map, and the map is not the territory……Hence, the widespread assumption that we can grasp reality through language involves a degree of insanity.

“There is no evil, only misunderstanding”. -Socrates

“Evil” is also known by the terms “right and wrong”

But I’m not saying to quit trying to make this ongoing “book” of Wolf’s interesting….not at all…..keep it up.

Think 91B20 used the analogy of Wolf as a bartender of sorts…..running an excellent establishment, or something.

Weimar Republic would like a word….

Wolf, so with inflation on my worry list, do I go with T-bills, or 10-year TIPS (when I also care about monthly income)?

1m t-bill rolling over 6 months will give me about twice as much monthly income as 10-year TIPs 6-month payment. Do I have this right?

The “inflation part” of interest is not paid until maturuty, correct? I’ve never actually tried TIPS.

Thank you.

“1m t-bill rolling over 6 months will give me about twice as much monthly income as 10-year TIPs 6-month payment. Do I have this right?”

So yes, if you expect to use all the interest from your investment to live on, TIPS are not for you. TIPS are designed for long-term investor seeking to hedge inflation risk. But with 6-month T-bills you get the interest every six months. To get interest monthly, you can either go for 1-month T-bills or stagger T-bills, such as buying six sets of 6-month T-bills each in a different month.

Also note, if there is a recession, and the Fed cuts interest rates to 1% for a six month period, your interest income will collapse during the low-interest-rate time period. But if inflation spikes, and the Fed hikes its policy rates, your income will balloon out the wazoo (not exactly out the wazoo maybe, but it will be higher).

So I just did a little math here.

1. Your 6-month T-bill rate changes every six months when your T-bills roll over. Who knows what it will be in the future. The 6-month auction next week will likely come with a yield of just over 3.8% (on Friday the trading yield was 3.83%). If you buy $1,000 of T-bills, you will pay a smaller amount (discount), and when it matures in six months, you’ll get $1,000, the difference being the interest you earned. Then the rollover process will buy new T-bills with a new yield. Note that the interest portion will not be reinvested, and you can use it to live off or to reinvest.

If the Fed cuts rates, the 6-month yield will decline ahead of the rate cuts. If the Fed hikes rates, the yield will rise ahead of the rate hikes. But the yield will be pretty close to the Fed’s expected policy rates a month or two hence.

2. The 10-year TIPS going through the auction next week has a coupon interest payment of 1.875%. The auction determines the price of the TIPS. If the price for $1,000 of TIPS is $999.30, your yield will be slightly higher than 1.875%. If it sells at a premium, your yield will be lower.

But wait… since the TIPS principal grows with the inflation protection that is added to the principal (see below), the 1.875% coupon is calculated on the new principal every six months, including inflation protection throughout the life of the TIPS. So if you buy $1,000 of 10-year TIPS, and 5 years later, inflation protection has added $300 to the principal, the 1.875% for that 6-month time period will be applied to the $1,300 (=$12.19 for the six month period in five years). So the coupon rate remains fixed, but the interest amount in dollars goes up because TIPS pay interest on the accumulated inflation protection amount.

The inflation protection is calculated daily with CPI. The Treasury Dept. publishes tables where you can look up the accumulated inflation protection for TIPS you bought (by CUSIP number). For example, if you bought $1,000 of TIPS at auction in mid-July, your TIPS would now be worth $1,010.16 ($1,000 plus inflation protection of $10.16).

Coupon interest will be paid in January, and the coupon rate will be applied to the total principal of maybe $1,015 (estimate, depending on CPI until then). And your 6-month interest payment will be half of the coupon rate (=0.937%), so $9.51 for six month. So in total, over the first six months, these TIPS will earn you $15 in inflation protection (estimate depending on CPI until Jan), paid at maturity, plus $9.51 in interest paid cash in January. This makes for a return of about 2.45% for six months. If CPI stays at 3% for another six months, you’re just under 5% return. If it goes to 2%, the return will be less; if it goes to 4%, the return will be higher.

But in January you will only get the coupon payment of $9.51.

Unpleasant Taxes: The yield and the inflation protection are both taxable income every year (so you pay taxes on the inflation protection every year, but you don’t get cash income from it until maturity). For this reason, I personally don’t like TIPS except in tax-deferred accounts, such as an IRA or SEP IRA where you don’t worry about taxes until you take the money out.

Thanks so much, Wolf.

You are better at financial details than Google AI and ChatGPT combined. Your last point about saving TIPS for tax-deferred accounts is well-taken. For that same reason I loaded up on Nvidia puts in my IRA account; don’t wanna pay tax on the boatload of money I’m going to make 😅 (this is not a financial advice to any of the readers, clearly. Only gamblers anonymous)

What about the foreign central banks selling off their US bonds and buying gold Firing up the $ printing press i.e monetizing debt can only lead to dollar losing value which equals inflation Wealth can’t be created by printing money

They’re NOT selling their US Treasuries, they’re ADDING US Treasuries, but they’re adding also other stuff, such as bonds in other currencies and gold.

I detail it every quarter. You should read these articles. Here is the last one:

https://wolfstreet.com/2025/09/18/the-foreign-investors-who-bought-the-recklessly-ballooning-us-treasury-debt-and-why-theyre-so-important/

Sounds like your post comes directly from MMT and

Warren Mosler . If you are correct , then the door is open to ever increasing budget deficits . And then the logical conclusion is to absorb the Federal Reserve directly into the Treasury , since the Fed will be the only entity buying US debt. Although the underlying conditions in the US are completely different than the German or Hungarian hyperinflations , we could be

approaching a South American inflation .

At the very least , there is a high probability of failed auctions in the coming years

I bet you have made that same comment all over socials once a week for decades.

Weimar America as the Trillion Dollar Coin “fix”…

I know, I know – “just 4%” ain’t Weimar.

But look at the macro policy competency/results of the last 50 years…why would many people have faith in the judgment of the powers that were/be?

Prob better to worry about the sun not coming up.

Cuz neither is ever even remotely likely to happen.

10 mile wide meteor you mean (etc)

I’ve had my own business for 30 years and I’ve had a net loss just one year. The Federal Government has had a net loss in 50 of the last 54 fiscal years. Absolutely pathetic track record. I won’t touch US Bonds. They’re not good for it IMO.

And yet these bonds get paid out every month without fail. Sure, they’re technically in the hole, but they can print and tax, whereas you and I cannot.

T Bills may be a comparatively safe way to go in an ugly inflationary enviroment.

1) Avoid insane, laughably thin ice, hyper-valuations of many/most assets and “leading” stocks…

2) Avoids duration risks/losses as much as is possible in Treasury world.

You know you will get your money back at something resembling par (cp a Mag 7 PE collapse from 40 to 20…) and *in theory* the continuous nature of those T Bill auctions *should* somewhat keep pace with inflation.

(Although T Bills during the long night of ZIRP almost definitionally failed to reflect clearly threatened inflation for years. Of course, so did 10 and 30 yr T *bonds* – that also got absolutely destroyed by 2022+ unZIRP – duration effect with an unprecedented viciousness.)

It is very hard to escape from the belly of a dying/rotting whale.

When the s hits the fan, the US government should consider a Value Added Tax to keep things going. Otherwise the FED will just have to buy the bills and print the money and retire the bought bills. At 100 percent inflation the debt will retire itself annually if necessary.

Mr. Pepper, why add a V.A.T. tax to all the taxes that wage earners already pay. Bad idea in my opinion.

Why not just start taxing the top 10% at the same rates that wage earners pay ? ?

In the end, things are likely to end up so frigging ugly that “all of the above” will likely have to be invoked.

“twenty centuries/years of stony sleep

Were vexed to nightmare by a rocking cradle/ZIRP”

“Why not just start taxing the top 10% at the same rates that wage earners pay ? ?”

Because if we did that we’d really really really be broke.

The top 10% pays roughly 75% of all taxes collected, and despite the propaganda pays a much higher rate than the lower tiers. Taxing them at the same rate would give them a HUGE tax cut.

The US has zero chance of default unless it’s willful. All the Fed has to do is say $38T exist and it’s paid for. Too bad a gallon of milk will cost $100.

Huh?

He means: The Fed could type a few numbers and generate $38T to pay back the entire debt but this would cause massive inflation.

The imminent collapse of the Russian economy (their oil terminals are being taken off-line almost nightly these days) may lead to a peace dividend. US military spending cuts could help reduce the deficit.

The US could have decreased defense spending after the Berlin wall fell. There was always an excuse to keep spending.

why concentrate on cutting defense when China has telegraphed they’re building up for a rukus? 90% of the Farm Bill is for food stamps, and 23% of them go to California, where 48% of the people living there weren’t born in America… Stupid giveaways to people not willing to hustle their own living needs to stop.

California you mean the California that’s the fourth largest economy in the world? That California? Or do you mean the California that’s been a donor State most likely funding your state for the last decade? No maybe it’s the 275 billion that we will over contribute to the feds.. let me restate that we will receive as a state $275 billion dollars less than we contribute to the federal government. That california? We would love nothing more than to separate from States like Texas which by the way is half the state we are in contributions to the federal government.. people who grabbed up California either can’t afford to live here or just like being racist.. perhaps you’re a fan of our current president? Perhaps the Epson files are not relevant to you because you think it’s a hoax LOL LOL LOL.. hope you don’t have children and if you do I hope someone’s looking out for him.

Whoa there Scotty.. down boy.. One can make an economic point with a little less blathering, hah.

Why are words like racism and nazi thrown around so nonchalant these days to describe people and things ?

The seriousness of words like that seems to be very diluted now. Kind of disappointing.

Besides, I thought this site was supposed to be about business and money and stuff.

TDS?

The “donor state” versus “taker state” meme is really getting old.

Scott,

Your state pays the Feds nothing. Your state collects taxes from it’s citizens, US citizens, and delivers them to the Fed government.

My parents…..and then I have remained here for the Land and the Climate since moving here in 1953…..father moved here several years before WW2.

It has/had an economic value….but maybe not so much now, I’m pretty old.

It’s very well known California is a net contributor to federal funds

https://usafacts.org/articles/which-states-contribute-the-most-and-least-to-federal-revenue/

Lol. It is always so easy to spot someone who gets their information from sources that take advantage of their ignorance.

It is entertaining, but unfortunately it is destroying the country.

The best part about such people is that their ignorance is taken advantage of on both ends. You say “Stupid giveaways to people not willing to hustle their own living needs to stop.” Later you will say something like the people from elsewhere are taking jobs that should go to Americans. Yet you won’t see the contradictory nature of those statements.

Easy to say Jim what about people that are unable to work because of extreme pain . Until u live it your just talking shit frankly. Try going from working from age 15 till your injuries prevent you from walking then a giant group of aholes throw you in a shit pot to be stird up at ur weakest point of ur life n blame it on you because easier that taken any heat ur self for your contribution. Right the government gives 711 away to people that blow up our federal buildings now is that intelligent.idk I’m ignorant

Hello Tom,

Your numbers are so shocking that I had to research it myself, and I discovered that your data was inflated. My research found that a stunning 80% of the Farm Bill went toward all nutrition programs including SNAP. Hopefully it will be spent on US produced food products, which will indirectly help the farmers, just like USAID bought billions of dollars of US crops to be distributed around the world.

California has 5.3 million of the 42 million on food stamps and other programs, which is only 12.6% of the total recipients. Since 11.5% of the US population lives in California, their beneficiary total is in line considering that they also have the biggest homeless population. Then only 27.7% of them are foreign born. Your number includes those born in other US states, which makes your total misleading.

Thank you for sharing some interesting data

Thank you for calling out Tom Slick’s BS

Every one of those numbers is made up and incorrect.

“Debt out the wazoo”…that aptly sums up just about everything!

But some how….

Some way….

We keep soldiering along, shuffling around complex numbers in complex webs to keep it working.

The Debt does not seem to matter, until someday, maybe it does.

The Fiat Money, Economic Collapse Doomsters say it should have all ended long ago, and that none of it is real.

With that said, I would fair to bet that if you had a time machine and sent average Americans from today back to year 1900….most of them would probably be sad.

The more I learn on this site, the more I realize that I don’t understand how we keep it all this working.

Anyways….

It will all probably be fine.!!

Still learning…

Thanks Wolf.

“The Debt does not seem to matter, until someday, maybe it does.”

How did you come to live in Weimar?

Slowly…then all at once.

The 10-year Treasury yield rose today by 4 basis points to 4.15% currently….

IMO, the ten year should be at least 25 bpts higher, or more.

I think that the economic tight rope that we are walking is not stable.

Nice to see 10-year US Treasury long term interest rates hit 4.15% today.

Only 4.15% ? That does not seem like enough, considering my local Credit Union is paying 4.25% on their checking accounts,

“ChaChing™ Checking: 4.25% APY on balances up to $15,000 and 0.15% APY on balances over $15,000, provided monthly qualifications are met.” (The qualification seems to be having direct deposit).

There really is no way out of the decline. A multipolar world is here and in a few decades or less we will not even be the favored partner. The real answer lies in a paradigm shift but our political system essentially makes that impossible. Not like the writing hasn’t been on the wall for most of this century but clearly written in some alien language yet to have a Rosetta Stone. Perhaps Americans will rediscover civil disobedience but seems like a vacuum at the moment.

“There really is no way out of the decline. A multipolar world is here and in a few decades or less we will not even be the favored partner. ”

Scary but probably true.

America’s Asian allies are/are going to be more tightly bound to Chinese production/consumption and the whole Yuan eco-system over time (the Yuan becoming Asia’s reserve currency despite political distrust – the economic interlacing of exports/imports with China will be too profound for the Asian countries to not center on the Yuan)

The US might be left with Europe (equally senile economically) and Latin America (history of hating US guts with only some justification and basket cases of their own accord anyway).

That ain’t a great split of the world for US interests – the huge productive efficiency winners of this world are Asian.

Better factor in our (now split more, IMHO) standard of living. Ostensibly, many kids of my generation were protecting it….somehow.

Thanks as always, Wolf for the timely analysis. We owe you a debt of gratitude.

Off topic but current: the guy who got Trump to speculate about 50 year mortgages may be heading to political Siberia. The down votes are pretty much unanimous across party lines. ‘Absurd’ is the reaction.

I don’t think there will be any tears anywhere when he finally gets fired. The vultures are circling.

The Wikipedia bio of William (Bill) John Pulte is fun reading. He was born in 1988 and is the grandson of national home builder William Pulte. A 2021 Detroit Free Press interview estimated his net worth as $100 M. Politico has described him as one of Trump’s few friends in the administration and he is the Director of the Federal Housing Finance Agency (FHFA) and Chairman of Fannie Mae and Freddie Mac since 2025. Pulte appears to have politicized his agencies to go after opponents of Trump. This is detailed in a Wednesday (11/12) article in real estate publication TheRealDeal. Fannie Mae’s ethics investigators probed whether Pulte improperly got the mortgage records of several officials and Trump opponents including NY AG Letitia James leading to her indictment. The investigations of Pulte followed complaints that officials of the agency improperly asked workers to access mortgage documents, and if Pulte had the authority to obtain the documents. Pulte has made criminal mortgage fraud referrals for Sen. Adam Schiff and Federal Reserve governor Lisa Cook who Trump has tried to fire. After the investigations dozens of ethics and investigator staff were fired or pressured to step down. Pulte had previously claimed to us tips and public records to support his mortgage fraud allegations.

Boy, I was sure that that Trump-as-FDR poster was going to be absolute crack cocaine for Trump’s personality.

A terrible idea…but that never stopped an ego-driven Trump concept before (his real business having long become licensing his fools-gold name to everything in sight with a checkbook).

Trump has some serious judgment issues when it comes to personnel, and he always has. Also, he seems to be getting senile of late (see for example his disastrous interview with Laura Ingraham).

Hard to run a team when the job entails non stop criticism from every decision .

These jobs all all temporary anyway as the economy changes and needs new guidance. Every four years there is a potential change so no job security for the executive branch thank goodness.

The reason for that is that so many people inside the government tried to undermine him in the first term.

So for his second term, he values loyalty above all else.

Ideally for him, he’d have loyalty and competence, but it’s a small group.

One thing I learned in business is that those that are perceived as loyal always get promoted over those that are competent. I think that competent people aren’t trusted because they are perceived as a threat.

Every CEO decision inherently involves some degree of uncertainty/potential for error.

The CEO personality type does not like to admit this – or the possibility of personal error.

So any dissenting opinion is psychologically reacted to as stupidity or disloyalty – even when it is *clearly* neither.

I never had a desk. My choice. I wanted to use hands, back, AND brains. So I was never a threat to any manager (maybe a pain in the ass, though). The more work I did, the more I was often given. Had to nip some of that in the bud, or just quit.

But there were a lot more interesting small and larger (mostly factory) tech and non-tech (2-1100 people and all in between) jobs for people like me back then……not so today……so except for trashed back, I was very lucky.

Wait a minute, he did an interview??

He must have a lot more to do to catch up with Biden.

Well, we’ve seen senility in the WH and, it ain’t Trump ! So, try some therapy for the TDS-it could help.

Wolf,

Thank you. On topic of MBS, have question. You mentioned

“At the current rates at which MBS come off the balance sheet, the Fed would buy $15-19 billion in T-bills a month. The market has to continue to absorb that amount of MBS. ”

For simplicity let’s say FED got paid 15B in MBS as part of monthly mortgage payments. Those Houses were not sold or refinanced. FED will invest that 15B in T-Bills. So Market has to absorb 15B “less” in that month as FED is picking up that much amount. In this this case, QT stopped. We don’t have QE or money printing. But its just getting moved from one place to other. But why it will impact on Markets as far MBS rolls off considered?

MBS get issued all the time. Old ones get called, pas-through principal payments shrink them, etc. and the pile is growing all the time. That process will go on no matter what the Fed does. As the Fed sheds MBS, rather than replace them by buying new ones, someone else has to step into the market and buy MBS because the pile keeps growing and the Fed is shedding. It’s not the Fed’s MBS that anyone needs to buy, but the amounts in $ that it is shedding.

That’s how ALL of QT has worked. That’s how anything works if there is a fixed amount out there, and someone is shedding, then someone else needs to buy.

“someone else has to step into the market and buy MBS because the pile keeps growing and the Fed is shedding”

Wolf,

Would it be fair to say that lower demand for MBS would (eventually) result in higher rates on newly-originated mortgages? Or is there not a direct correlation between rates on mortgages pre-securitization and the yields on MBS products?

Yes, I think slightly higher mortgage rates would be the result. There is a fairly tight relationship between rates of new mortgage and yields of MBS.

Let kids not born yet worry about paying back $38 trillion.

Beelzebub

The predetermined losers in the game of hot potato.

All empires fall when they go through the same cycle that we are in now.. At first, their currency becomes as good as good around the world where other nations use it and peg their own currencies to it. Then extravagant spending on domestic and military needs ensues, creating enormous amounts of debt. They proceed to print more currency and debase it by removing any intrinsic value or taking it off the gold standard. Nixon did this creating the petro-dollar based on the good faith of the US Government and might of the US military to back it up. Later on, immoral and reckless leaders take power sending the empire into a death spiral where foreigners begin to reject the empires currency and good faith, like with the BRICS countries and the cycle concludes with cataclysm effects.

This happened many times through out recorded history and America is in the ninth inning. The end of days for the American empire just needs another pandemic, momentous natural disaster or expensive war to tap it down into the pile of other failed empires. Maybe the upcoming Venezuelan War will do just that???

The so-called ‘gold standard’ was nothing but a very brief and totally failed 60 year experiment from 1873 until 1933 at which time it was completely abolished and the price of gold set at $35 per ounce. The Federal Reserve has been doing exactly the opposite of ‘money printing’ for the past several years with QT and its balance sheet has shrunk dramatically. There is no currency of any kind anywhere that can challenge the US Dollar in the foreseeable future. The US will have to both raise taxes and cut spending significantly across the board to deal with its massive debt challenges and prices will have to fall substantially.

SoCal, you’re right that the Fed has shifted from QE to QT recently, and that no single currency poses an immediate threat to the dollar’s role. But we’re seeing an increase in trade settlements in local currencies, not just between U.S. rivals, but also between large economies like China, Brazil, and even India. These moves aren’t just symbolic; they reflect growing geopolitical fragmentation and a desire to reduce reliance on USD-based systems, especially given how financial sanctions have been used as tools of statecraft.

As for the gold standard, yes, it was short-lived in modern form and ended for good in 1971. But the record gold purchases by central banks in recent years, especially outside the West, suggests that some countries are preparing for a more multipolar monetary system, even if not a return to gold per se.

Lastly, the U.S. fiscal position is becoming more difficult to manage. Sustained high deficits, rising interest costs, and political gridlock make it harder to assume the dollar’s dominance will remain unshakable forever. It’s not that the dollar will be replaced overnight, but the world may slowly transition toward a system where the dollar is “first among equals” rather than a monopoly.

The US went off the Bretton Woods quasi-gold standard in the early 1970’s because persistent trade and fiscal deficits made it impossible to preserve without US economic reform.

The subsequent 50 years has been nothing but a worse, accelerating deterioration in trade and fiscal deficits and an absolute refusal to even contemplate reform.

So the Keynesian “barbarous relic” was replaced with a gun in the mouth – which seems worse 50 years on?

There are less than 200,000 metric tonnes of gold ever produced and central banks have owned between 32,000 to 35,000 metric tonnes of it for decades which has not increased significantly at all Most gold is owned in the form of jewelry and that remains its primary useful purpose. If all of the gold were split up among all.of the world’s population people who only get 1/10 of once ounce each. Gold’s total value even at today’s prices is less than 1% of all global assets making it of zero financial relevance.

The US dollar will definitely have a role but it will continue to decline as a global reserve as it already has significantly over the last few decades. I don’t think anyone is suggesting it goes away but the power of it, and the abilities it gives the US will decline with it. For the world that is a good thing. For the US it will present challenges, that perhaps manifest in better debt management but perhaps higher interest rates. So I would say the future is very foreseeable at least if you talk in terms of decades or the lives of your children.

“Situation

Dollar Effect

Global risk aversion

⬆️ Stronger dollar

Investors flee to safety

⬆️ Stronger dollar

Global trade collapses

⬆️ Dollar shortage → stronger

Fed raises rates

⬆️ Stronger

Fed cuts deeply / QE

⬇️ Can weaken (late in recession)

World recovery begins

⬇️ Dollar weakens”

‘The gold standard ‘was completely abolished and the price of gold set at $35’

This is an internal contradiction. Setting the price of gold at $35 WAS a gold standard. The US $ was anchored at one thirty- fifth of an ounce of gold. This was not in 1933 but in 1944 at the Bretton Woods Agreement. Thus there was a limit to how many US $ could be printed. During the war in Vietnam it became apparent, first to the French, that the US wanted to pay for it without raising taxes, but by printing US$. So France started presenting lots of US $ and getting an ounce of gold for each 34 US$. Then Nixon ended convertibility and took the US$ off the gold standard.

Could the US have accumulated 38 US $ trillion in debt if it was those dollars were redeemable for gold at 35$ per ounce?

Strangling an economy with gold only makes sense to gold bugs who don’t care about anything other than the price of gold, and for today’s HUGE US economy, the price of gold would have to be billions of dollar an ounce. That’s the only reason gold bugs keep bringing it up.

Natural money creation in a growing economy via the banking system is demand based and is not inflationary. “Printing” money by a central bank is inflationary. Government debt is not a problem if it’s not excessive and grows no faster than the economy. But the US debt has risen far faster than the economy. This is politics.

The role of gold is an economic debate.

Asserting that: ‘The gold standard ‘was completely abolished and the price of gold set at $35’ is a problem with the English language.

see Who Really Killed the Gold Standard? | The National Interest

The charges on debt are related to a cumulative compounding figure; and since the multiplier effects of debt expansion on income, the ingredient from which the charges must inevitably be paid, is a non-cumulative figure, it would seem that the time will inevitably arrive when further debt expansion is no longer a practical or possible expedient, either to provide full employment or to keep debt charges with tolerable limits.

The ensuing rise in real yields will kill bitcoin.

Where art thou liquidity; “ New York Federal Reserve President John Williams met with Wall Street banks this week to discuss a key short-term lending facility, the Financial Times reported on Friday, amid signs of tighter market liquidity.” ~Willams knows the importance of feeding the master trading algorithm, if it’s input doesn’t change it will follow its orders to big sell off. It’s like Atlas “algo” will need more food “liquidity” to not drop the bubble from the sky high valuation. Watch out for falling knives this week!

This reads like quote from 1929 newspaper. In 1906 they went directly to JP Morgan I think.

“Finally it became plain that there was no use in waiting at the Post for money. There wasn’t going to be any. Then hell broke loose.”

– Reminiscences of a Stock Operator

The meeting was about the SRF, after the NY Fed and other Fed officials had expressed their disappointment that banks weren’t using it enough to quell repo market rate increases. We don’t know what was said in that meeting, but it followed these comments of disappointed by Fed officials with the banks. Maybe Williams told the banks to use the SRF or else?

Seems to be a strong demand at these rates.

Maybe the rates are too low?

Too low for me. But since there is strong demand at these rates, the rates are exactly right to attract enough demand. That stuff is sorted out by the market, that’s what markets are for.

Wolf, do you think the current spike in TGA balance is only related to the shutdown or does the increasing size of short term bill funding mechanically require higher TGA balances to manage the program efficiently ?

It’s related to the shutdown that slowed the cash outflow because stuff didn’t get paid. You’ll see the TGA draining by a good amount this coming week as catch-up payments are being made.

remember when more supply depressed prices (raised rates)?

I am wondering if the shift by the Treasury into shorter-duration bills is eventually going to cause the interest rates of 4-week, 6-week, and 8-week bills to rise. The Treasury has to issue these to cover expirations, further indebtedness, and the shift from long-term bonds. Eventually, demand should slacken and interest rates should rise. The key number to watch is the spread between the overnight rate and the 4-week bill.

The tools for managing the federal debt would seem to be:

1. Austerity

2. Taxes

3. Inflation

4. Currency devaluation

5. Debt default*

The pandemic starkly highlighted how the game works. The government handed out “free money” (a lot of which went disproportionately to the existing owners of capital, e.g. stockholders) and could have at the same time passed legislation designed to pay for the hand-out, but did not (why dilute the myth of “free money”). Were constituents outraged, writing Congress that they had not included a way to pay for the stimulus written into law? Is there any risk that Congress will pay a price at the polls for not having a plan to pay for the hand-out? It would seem that every time we have a crisis, or even a recession, the government is just going to ratchet up the debt with no explicit plan to pay for it, and it is the new economic reality, and the market is o.k. with this approach–there are no immediate consequences.

*On the point of debt default, it is an option, in that the U.S. could simply tell foreign holders of its debt that it is not paying, and deal with the fall-out (but covering debt held internally differently). Empires have defaulted on their debt (e.g. the Dutch), so thinking that this could not happen to the U.S. empire is magical thinking. When we say the U.S. cannot default on its debt, I think we are saying that as the U.S. empire stands now, it cannot default, but history would say that empires do not last forever, and the evidence is that the U.S. is post-peak as an empire, so the probability of default is non-zero, and likely increasing.

STYME: You left a very important tool off your list.

6. Tax the wealthy at the same rates that wage earners pay.

We could start with the F.I.C.A. and go from there.

“If you’re self-employed, you pay the combined employee and employer amount. This amount is a 12.4% Social Security tax on up to $176,100 of your net earnings and a 2.9% Medicare tax on your entire net earnings.”

The only tool, credit control device, at the disposal of the monetary authority in a free capitalistic system through which the volume of money can be properly controlled is legal reserves. Powell eliminated legal reserves in March 2020. And Powell also eliminated deposit classifications. Monetarism has never been tried.

I don’t think USA would ever default on its debt.

The only game in the town is inflation which basically leads to currency devaluation.

IN the last few decades, USD has lost 90% plus purchasing power.

Got gold hamsters?

Hey Wolf, are you on Trading View? If you ever happen to we write a book on macroeconomics, I’ll buy it. Have any suggestions on reads? Ty

Tony Robbins!

No just kidding.

I am being mean 😆

I love that guy! 🤣

Stage presence (acting) over slow boring (but well thought out) content.

Old as civilization….maybe much older.

1st time commenter, long time reader. Love your in-depth work and extensive knowledge & analysis as much as your candid replies to comments, LOL.

That being said, what differentiates a bond from a note or a bill?

Types of Treasury securities:

Bills: securities with 1 month to 1 year terms, no coupon interest paid, but sold at auction at a discount and redeemed at face value. Difference is interest payment.

Notes: securities with 2 year to 10 year terms, interest is paid every six month via coupon interest payments.

Bonds: securities with terms of 20 years and 30 years, interst paid every six months via coupon interest.

TIPS = Treasury Inflation Protected Securities come in 5 year, 10 year, and 30 year terms. See my long comment here in this thread about them:

https://wolfstreet.com/2025/11/14/government-sold-694-billion-of-treasuries-this-week-debt-hits-38-1-trillion-treasury-yields-rise-further-shift-to-t-bills-has-begun/#comment-661221

FRNs: Floating Rate Notes that have a variable rate of interest.

Plus a few other types of Treasuries that are not traded in the markets.

Thanks for your patience to reply this question which was easily available through quick google search.