Banks are mostly off the hook this time; risks were shifted to taxpayers and investors.

By Wolf Richter for WOLF STREET.

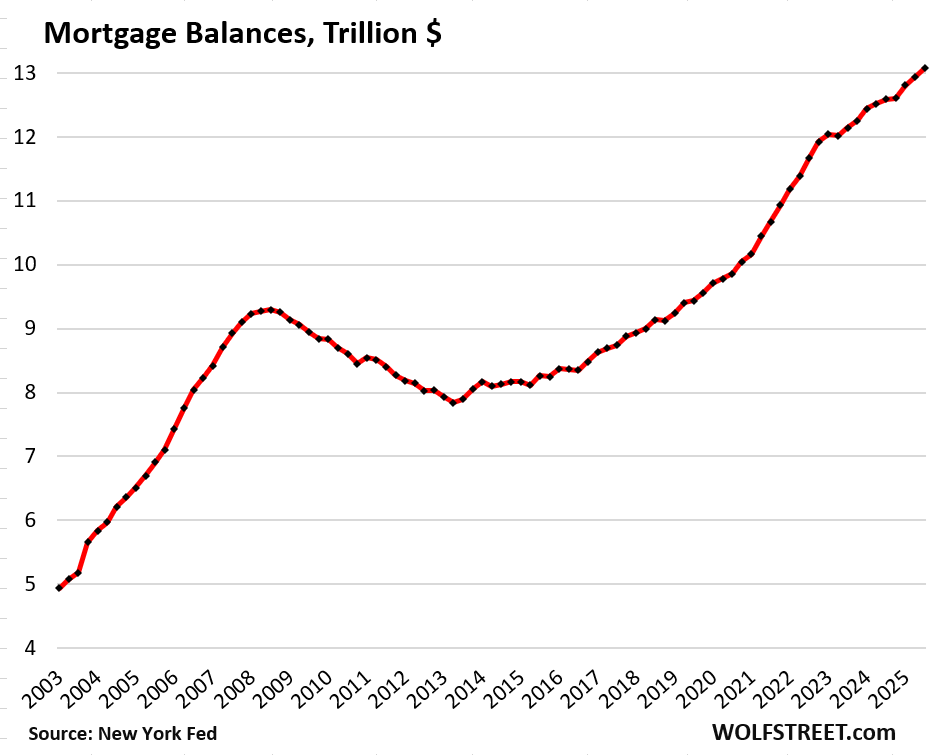

Mortgage balances rose by $137 billion (+1.1%) in Q3 from Q2, and by $482 billion (+3.8%) year-over-year, to $13.1 trillion, according to the Household Debt and Credit Report from the New York Fed, based on Equifax credit report data.

Growth in mortgage balances is a net of several factors, a significant one being the growth of the housing stock when buyers finance the purchase of newly constructed homes. Mortgage balances also increase, in terms of existing homes, by the difference between buyers’ new mortgages and sellers’ paid-off mortgages, if any (many sellers don’t have mortgages); balances also increase by the cash-out portion of newly refinanced mortgages and by new second-lien mortgages.

Conversely, mortgage balances are reduced by the principal portion of mortgage payments and other mortgage paydowns or payoffs; and by mortgage wrecks that cause mortgage balances to be written off – few of them currently, but a lot during the Mortgage Crisis:

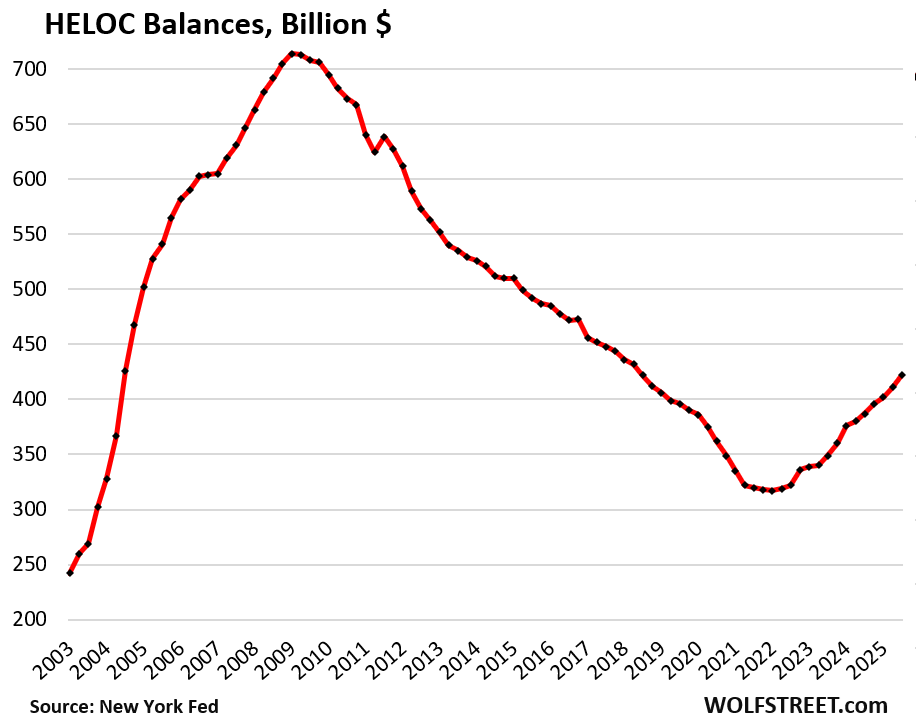

Here come the HELOCs: +33% since Q1 2021.

Balances of Home Equity Lines of Credit jumped by 2.7% quarter-to-quarter, and by 9.0% year-over-year, to $422 billion. Since the low point in Q1 of 2021, HELOC balances have surged by 33%.

HELOCs did some damage during the Housing Bust, and lessons were learned about their risks. But more importantly, mortgage rates plunged ever lower through 2021, and cash-out refinancings dominated the equity-extraction industry. As a result, HELOC balances declined for 13 years.

Despite the 33% surge off the 2021 bottom, HELOC balances are still relatively low. HELOCs are lines of credit, and many of them are unused, just sitting there as a standby source of funding. But the balances here are actual balances drawn on HELOCs:

The risks of HELOCs involve that second lien they put on the home. If homeowners default on the HELOC while keeping the first-lien mortgage current, they can still end up in foreclosure.

Also HELOCs are full recourse even in the 12 states, including California, where nonrecourse mortgages are standard, and where lenders, after a foreclosure sale, cannot pursue former homeowners with deficiency judgements on the first-lien mortgage. But they can pursue former homeowners for the balance of the HELOC.

And HELOCs come with higher interest rates as lenders face the additional risks that come with second-lien mortgages, as the holder of the first-lien mortgage gets paid first in a foreclosure sale, and often there is nothing left over for the second-lien holder.

On the plus side for the borrower: HELOC interest rates are a lot lower than interest rates on credit cards or personal loans, and can even be lower than unsubsidized auto loans.

And homeowners can use it as a stand-by line of credit with no balance and no interest cost (though fees may apply), to have instant access to the cash, if suddenly needed, at a lower cost than borrowing on their credit cards. This includes people with substantial investments who don’t want to sell those investments to fund other projects.

The burden of housing debt: Housing-debt-to-Income Ratio.

The debt-to-income ratio is a common way of evaluating the burden of a debt. With households, we can use the debt-to-disposable-income ratio.

“Disposable income,” released by the Bureau of Economic Analysis, includes income from all sources except capital gains, minus payroll taxes: So income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc. It roughly represents cash flow after payroll taxes that is available to spend on the costs of living and debt service.

Due to the government shutdown, the BEA has not yet released disposable income for September. To get Q3 disposable income, we can use the data for July and August and estimate September based on average growth year-to-date.

The housing debt for this ratio includes mortgage debt and HELOC debt.

The housing-debt-to-disposable income ratio in Q3 inched up to 58.6%, just a hair higher than in Q2, which had been the lowest on record, except the four quarters during the pandemic when stimulus funds distorted household incomes into absurdity.

It’s glaringly obvious what led to the Mortgage Crisis that was a big part of the Financial Crisis: Households overindebted themselves with housing debt. By Q1 2007, the housing-debt-to-income ratio exceeded 90%!

Who’s on the hook this time?

Among the most important changes resulting from the Financial Crisis was the transfer of mortgage risk from banks to taxpayers. There won’t be another mortgage crisis for banks. They’re largely off the hook.

Banks and credit unions are on the hook for $2.7 trillion in mortgages, HELOCs, and second-lien mortgages, according to Federal Reserve data on bank balance sheets. That amounts to only 19.7% of the $13.5 trillion in mortgage and HELOC debt.

The government is on the hook for $9.1 trillion of single-family mortgages that were securitized into MBS and sold to investors, according to Ginnie Mae data. If borrowers default, the government eats the loss. For investors, these MBS have a similar near-zero credit risk as Treasury securities. The investors include bond funds, pension funds, the Federal Reserve ($2.1 trillion and shrinking), banks, mortgage REITs, etc.

And subprime-rated mortgage debt is insured by the government through the FHA.

The share of government-guaranteed single-family mortgages outstanding:

- Fannie Mae: 38.6%

- Freddie Mac: 33.1%

- Ginnie Mae: 28.3%

Investors are on the hook for $1.7 trillion of residential mortgages, such as jumbo mortgages that didn’t qualify for government backing. These mortgages have been packaged into “private label” MBS and sold to institutional investors around the globe, such as pension funds and bond funds. It’s these investors that carry the credit risk for those mortgages. Banks are off the hook.

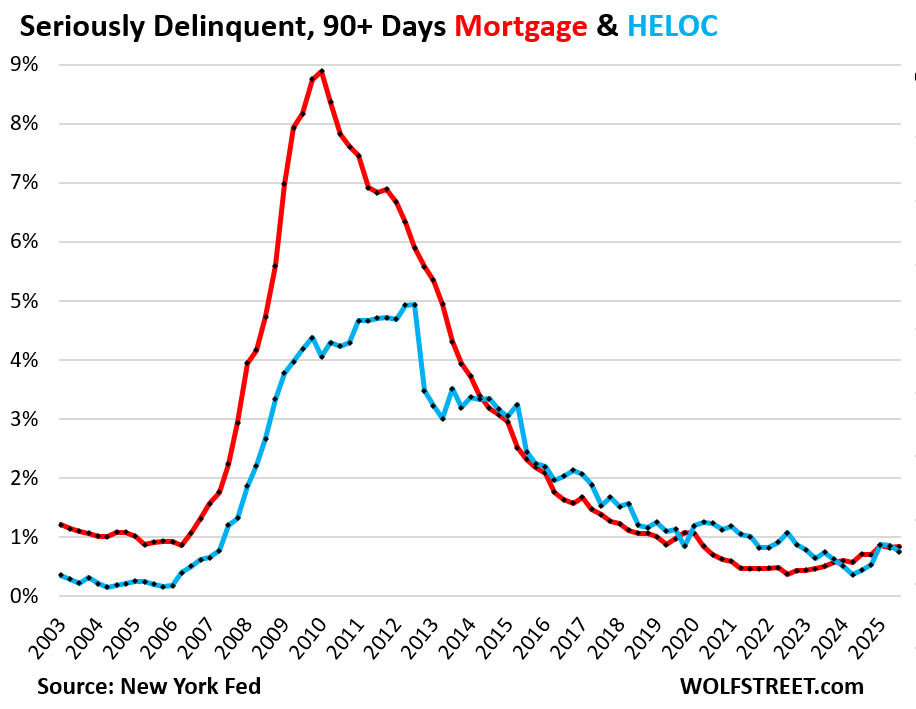

Delinquencies and foreclosures dipped and are low.

Serious delinquency rates – 90 days or more delinquent – were unchanged for mortgages at 0.8% (red in the chart below) and edged down for HELOCs to 0.8% (blue). These are very low delinquency rates.

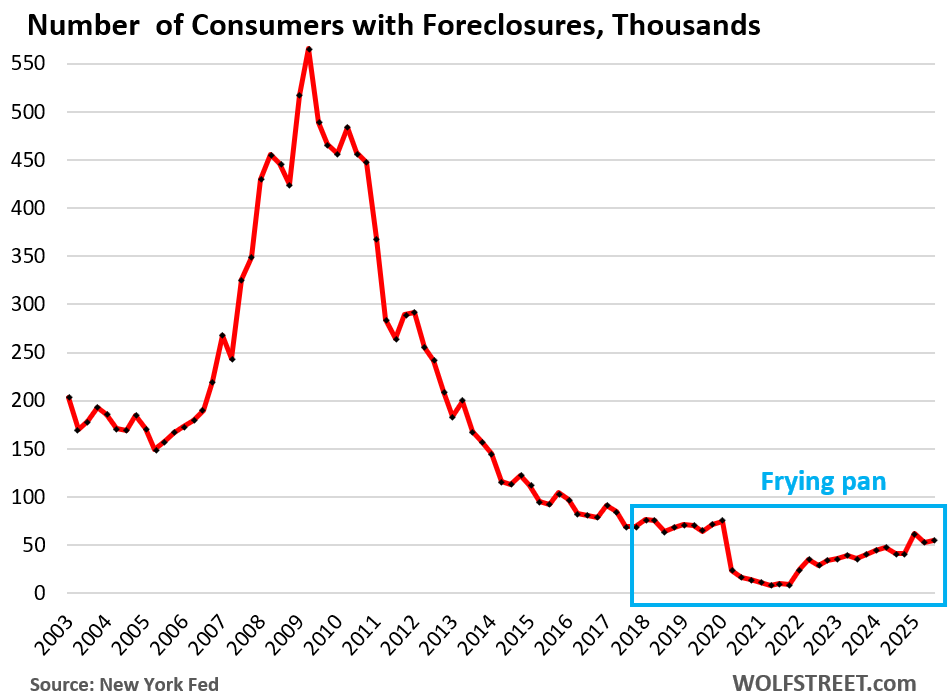

Foreclosures are very low. The number of consumers with foreclosures in Q3 rose to 54,760, well below the low end of the 65,000-to-90,000 range of the Good Times in 2018-2019, and far below the number of foreclosures in prior years.

The infamous frying-pan pattern, as we call it here, was formed as a result of the era of mortgage-forbearance and foreclosure bans, when foreclosures were essentially impossible and foreclosures fell to near zero; and then, as rules loosened, foreclosures began to edge higher from those near-zero levels but remain well below the prior times. The resulting line of this drop and then the rise looks like a frying pan. This frying-pan pattern has cropped up in a lot of delinquency charts as well.

And in case you missed it yesterday: Household Debts, Debt-to-Income Ratio, Delinquencies, Collections, Foreclosures, and Bankruptcies of our (not so) Drunken Sailors in Q3 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good report. We know how this story will end. There are already almost half a million 1-4s underwater. When the correction really gets rolling, there will be millions.

People who have a 3% mortgage or even an under 4% mortgage don’t really care about being underwater on price. They’re going to protect that mortgage like a gift from God.

It’s the people who bought at a high price with a high rate over the last two years… and there aren’t all that many of them. But even they will keep making their mortgage payments unless they lose their jobs for a long time and run out of money. And we aren’t there yet.

Believing low interest rates are a gift from god shows just how delusional people are these days. Bragging about paying interest on something you can’t really afford, such idiotic clowns.

Seems like folks can afford these mortgages given the low foreclosure rates.

Given the very low foreclose rate, seems like people can afford their homes.

I didn’t see short’s post above mine a few minutes ago. Please delete mine above.

No. Nailed twice holds better.

Wonder what the debt to income looks like for just households who bought since mortgage rates went back to normalish.. have to imagine that’s the forward looking picture at this point. Well offset currently by purchases pre 2023.

Some households have zero debt and some households have lots of debt and some household have moderate amounts of debt. And there are always some who default on their mortgages. That’s always the case and not new. It’s only the household with lots of debt that are at risk. That has always been the case.

But when you want to know whether something can damage the economy overall, you need to look at the aggregate debts and aggregate incomes. And you can see that the economy overall was getting pushed into trouble in 2005-2007 by this explosion of mortgage debt that far outran income growth.

So when housing price went up 40% in 5 year period while income only went up 25% (15%? I am not 100% on this # based on the stats I read), is this an indicator of pre-trouble phase? We all know it is housing bubble 2.0. The question is when it will burst.

It is said that 62% divorce rate in 🍊 county CA. # of married couple vs # of homes they own is 1:2 ratio. I wonder whether two homes for each married couple & divorcee are the reason home purchase (demand) has sustained so far aka price has not only sustained but also gone up 🧐

This housing bubble was so fast and furious (50%+ in many markets in 2 years) that actually most homeowners bought before it and benefited from the high prices and still own those homes; and only a relatively small number of buyers bought afterwards at high prices.

Home prices are going to come down because they’re too high and don’t make sense. And as they come down, incomes rise, and after some years, maybe lots of years, they start making sense again.

So it’s only the relatively small number of buyers who bought during and after the price explosion that are at risk, and most of them will be fine. And the banks are not on the hook. So that’s not a scenario that will take down the economy or the banks.

According to the YouTube, everyone is just going to pay off their 30 yr in 3-5 years by getting a HELOC and using some razzmatazz known as velocity banking. What could possibly go wrong with that?

Maybe people whom own houses but have SNAP will have to stop paying their mortgages to buy food.

Also not sure if Walmart has had their earnings call or not recently, but no SNAP and Walmart earnings are going to be abysmal.

While there are homeowners with mortgages on SNAP for sure, primarily they are renters. That doesn’t dismiss there may be earning impacts but of course need to figure out where the courts settle on that matter and how society supports the most needy while an inept government fails them.

Wolf – how, in a sane world, could ‘entity A’ engage in a financial transaction, and transfer the RISK to ‘entity B’ (Tom, Dick, Harry and Sally).

In this case, entity B is all of us working people.

We had NO PART in the financial transaction and did NOT sign up for this. I call foul ‼️‼️‼️

This IS going to translate into real world losses.

Have you looked into your 401k, or pension, rights? When you sign the papers to allow financial analyst to control your return – you signed up for those very decisions.

Ah! The illusive “investors”…

“Americans had $12.2 trillion invested in 401(k)s and $16.8 trillion in IRAs in the first quarter of 2025, according to the Investment Company Institute. “

Tidbit: Allan Merrill, CEO of Beazer Homes, said in a recent interview: “Speaking on a panel at ResiDay, a residential real estate conference hosted by ResiClub, Merrill talked to the outlet’s editor, Lance Lambert… [Merrill] thinks the market has to “grind back … I think it’s a multi-year period of sort of trying to get back to a more normalized affordability environment.””

I’m a little skeptical of the debt to disposable income charts. The Fed used to have something called the FOR (Financial Obligation Ratio), defined as “Household debt service payments and financial obligations as a percentage of disposable personal income; seasonally adjusted.”

They discontinued it in 2024, but always also warned about it while publishing it: “The Board decided to stop publishing the FOR due to a lack of high-quality data on property tax and homeowners’ insurance payments. They still publish the household debt as a percentage of disposable income which is listed here.

I see the ever increasing debt in the NY Fed report on household debt and credit; I know there are increasing households which might be a factor. But a rougher indicator (but also another angle) would be simply the ratio of total household debt to number of households. A number with less transformations to obtain and perhaps less error.

1. Your last paragraph: I explained to you where the increase in the debt comes from in paragraph #2 and #3. Do the math yourself. 1 million new single-family homes and condos per year. Plus the other stuff I said.

2. Debt-to-income ratios are a classic measure of debt sustainability, and it is one of the things used when qualifying for a mortgage.

3. The thing you cite “FOR (Financial Obligation Ratio)” IMPLODED because it was so bad, and the Fed stopped producing it. And then it came up with a new thingy recently, and maybe it’s better or maybe it’s even worse. It’s nearly impossible to measure debt service expenses accurately.

In addition: mortgage rates are mostly fixed in the US and so debt service expenses overall doesn’t change that much because only a small portion of homeowners get a new mortgage in a year. You can see how slowly the portion of 6%+ mortgage rates has risen in three years, and 5%-6% hasn’t changed at all.

https://wolfstreet.com/2025/09/29/the-lock-in-effect-and-mortgage-rates-update-on-unwinding-a-phenomenon-that-wrecked-the-housing-market/

I am curious as to the impact of baby boomers not selling unless they have too in the next ten years vis-a-vis these factors now evolving. It seems that things will not really get going until those in properties like mine will finally cash out. In Riverside, Ca the million dollar homes are not selling like my my neighbor at 999K. The competition is going even lower to compete which gives a whiff of coming desperation. The flippers showed up at the first open house and nothing more….

My mortgage is at about $2,300 everything included whereas my neighbor is selling a home that will cost 6K monthly with all included not factoring the huge landscaping bill to come with giant trees all over.

I am one who does not worry about price as in most scenarios I have other factors at play. It seems the real estate market is like when you go sailing in waters where the riptide changes the typical patterns of an area you sail often. You set tack but the rip tides rule…

Does anyone collect data on the aggregate amount of equity homeowners have? Or a distribution curve of equity? So, can we predict whether foreclosures would result in losses for taxpayers, investors, etc.?

I note that in 2007, the losses on the bonds were not due to foreclosures, but to foreclosures without sufficient value in the properties to cover the remaining debt.

If current homeowners have enough equity that the loans will be fully repaid after a foreclosure sale, then there is no society-wide crisis. The homeowners who lose their equity to losses will be upset, but none of the banks, taxpayers, or investors will be worried about a ~3% loan being repaid in full so they can reinvest at higher interest rates.

However, I don’t know where to find such equity information.

I’m still wondering just how many homes are having to be dumped in 25′ or 26′ over the forbearances coming due. There are a LOT of homeowners that took the forbearances during COVID and have to come up with $10k’s to pay year’s worth of interest to keep their mortgage in good standing. I’ve heard from some in realty that the savvy are house-swapping before the bill comes due because they can’t afford it and their only real option is going back to ‘zero’ in a new home. This could cause a ‘hiccup’ in foreclosures from Q4 25′-Q4 26′.

1. Covid forbearance is not an issue anymore. Nearly everyone existed covid forbearance by 2023 as most people refinanced into lower rates in 2021/2022, some with cash-out, given the spike in prices, and exited forbearance by paying off the old mortgage.

2. generally, accrued interest is added to the loan balance in most forbearance agreements, thereby increasing the remaining balance and lengthening the term of the loan. No lumpsum payments are needed.

3. Forbearance is a standard tool to deal with natural disasters, such as hurricanes, wildfires, etc. And there are always some mortgages in forbearance.

But what did happen during Covid was that these forbearance deals and foreclosure moratoriums caused foreclosures to drop to near zero. What’s hitting foreclosures now is not those old forbearance deals.