After the debt ceiling, the shutdown: government checking account (TGA) sucks up $700 billion in four months.

By Wolf Richter for WOLF STREET.

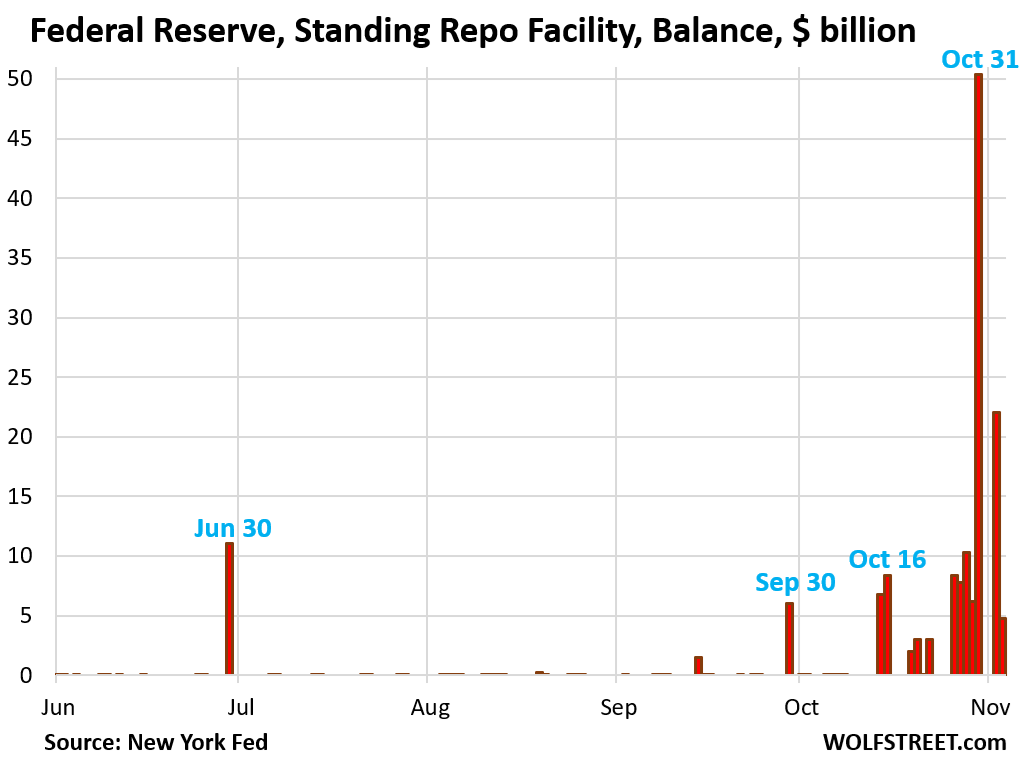

The uptake at the Fed’s Standing Repo Facility (SRF) plunged to $4.8 billion today: $2.8 billion at the morning auction and $2.0 billion at the afternoon auction. The approved counterparties at the SRF are big banks and broker-dealers.

This was down from $22.0 billion on Monday, and from $50.4 billion on Friday, which had been a record of this new facility that the Fed revived in July 2021.

These repos (“overnight repurchase agreements”) will mature on Wednesday, when the Fed gets its $4.8 billion back and the banks get their collateral back. The collateral is Treasury securities and government-guaranteed “agency MBS.” The $50 billion in repos taken on Friday matured on Monday, when the Fed got its $50 billion back and the banks got their collateral back. So that liquidity that these repos provided on Friday got reversed on Monday. Then on Monday, $22 billion in new repos were taken, and that liquidity was reversed today. And today’s $4.8 billion in liquidity will be reversed tomorrow. The total balance outstanding at the SRF is now $4.8 billion.

The purpose of the SRF is to provide liquidity to banks and dealers so that they can lend to the repo market. This is a profitable trade when repo market rates are significantly higher than the Fed’s rate at the SRF (currently 4.0%). And repo market rates have been higher in recent weeks.

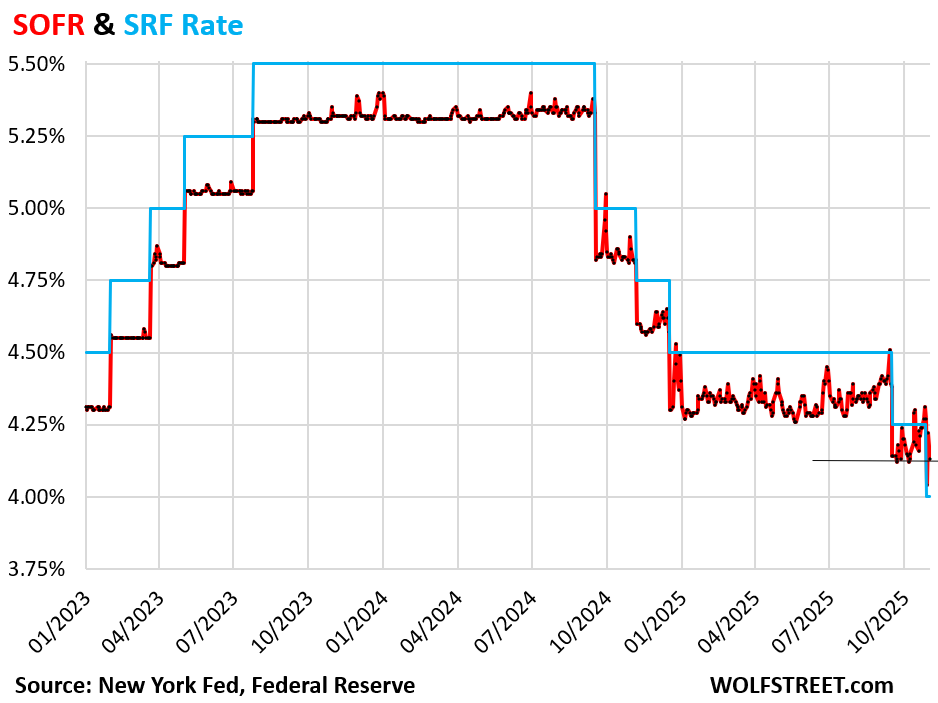

Repo rates. The Secured Overnight Funding Rate (SOFR), which tracks a $3-trillion-a-day segment of the repo market, declined to 4.13% on Monday, from 4.22% on Friday (the NY Fed will release today’s rate tomorrow).

While 4.13% is a drop from Friday, it’s where it was in late September and early October after the September rate cut. But last week there was another rate cut!

The rate at the SRF (blue in the chart below) is now lower than SOFR (red), when normally it is higher. The SRF rate is one of the Fed’s two ceiling rates. When repo market rates go above it, banks are expected to pile into the SRF, grab a bunch of money at the SRF rate, and lend it overnight to the repo market at the higher market rate. That new supply of liquidity brings market rates back down, at which point banks lose interest, and activity at the SRF goes back to sleep.

When repo market rates blew out in September 2019, the Fed did not have the SRF; the Fed had scuttled its repo facility in 2009 under QE.

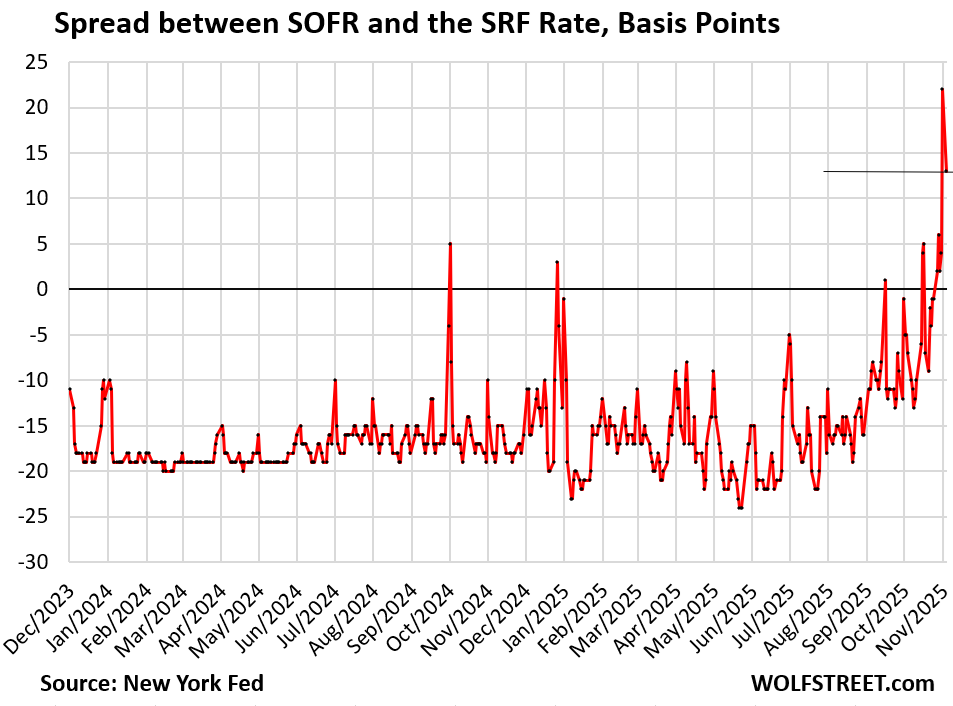

The spread between SOFR and the SRF rate widened on Friday to +22 basis points, the widest in the short life of the new SRF (born July 2021). On Monday, the spread narrowed to +13 basis points, the second widest in its short life.

Normally, the spread is negative, with SOFR below the SRF rate.

Why these liquidity pressures?

Over three years of QT have wrung out a lot of excess liquidity. Now, two major factors came together to put liquidity pressure on the repo market, where large amounts of liquidity have to move around, and yields signal where these amounts need to go, and higher yield help the flow of liquidity to where it is needed. But it takes some time.

1.Month-end, quarter-end, and tax days, and the days surrounding them are pressure points, when massive liquidity flows put pressures on the market and cause SOFR to rise. October 31 was on Friday, which saw the big spike in SOFR to 4.22%.

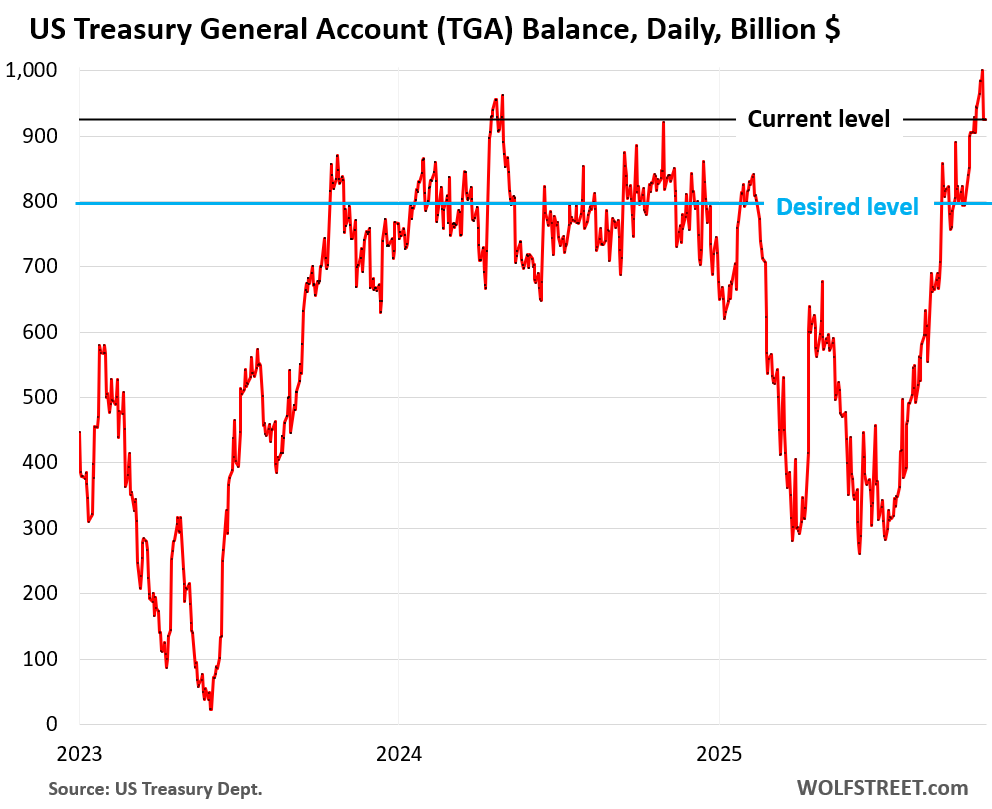

2. The balance in the government’s checking account, the TGA (Treasury General Account) has ballooned over the past three weeks as the government halted paying for some of its operations and salaries due to the shutdown, while still selling Treasury securities and collecting taxes, fees, and tariffs. So cash is still coming in, but the cash outflow has been temporarily slowed, and the checking account balance has ballooned.

The TGA is with the New York Fed. As the TGA balance rises, it removes liquidity from reserves and the market.

On October 30, the TGA balance reached $1 trillion, over $200 billion more than on October 10 before the shutdown began changing the cash flow.

On November 3, the balance dropped to $925 billion, still $125 billion more than on October 10. If the balance continues to decline, it would send this liquidity into reserves and the market.

In the four months between the end of the debt ceiling – when the TGA was down to $300 billion – and October 30, the TGA has sucked up $700 billion in liquidity, part of which came out of banks’ reserves at the Fed.

This type of large and sudden move of liquidity out of the market into the TGA, when liquidity had already tightened up after three years of QT, was the reason the Fed cited when it slowed QT in June to preempt too much pressure on bank reserves, and thereby on the repo market because, when reserves are tight, banks don’t lend their reserves to the repo market, and repo rates surge, which is when the SRF is supposed to kick in. And it did.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I went to Subway yesterday. The $5 footlong is now $16.

If the tariffs are essentially doubling corporate taxes, they will hustle to cut costs and push prices to the limit.

Was that sandwich imported from China? (obviously not because it’s made in front of you by US labor). Was the bread imported? (no, it’s baked on location). Was the labor tariffed? (no the labor is right in front of you and at headquarters and is not tariffed). Were the rent and utilities imported and tariffed? (come on, give it try). Were the transportation and cold-storage costs in the US tariffed? (nope). The cold cuts and cheese? (unlikely, most of this stuff is made in the USA from US beef, pork, and milk). Were the few pieces of greenery imported? Maybe some, others not. So maybe 2 cents in tariffs on four slices of tomatoes and a few morsels of peppers and olives.

So how do you blame a $16 price on a few cents of tariffs – if any? You people are hilarious.

And why did you troll this article on the repo market with your sandwich-tariff hilarity? Trying to start the comments out with a good laugh?

I learned from Google AI recently that California, accounting for 1% of the U.S. farmland, produces something like 75% of the U.S. veggies, fruits, and nuts. Everywhere else they pretty much grow corn, potatoes, and soybeans. And of course Cali is the biggest producer of milk (ahead of Wisconsin). All in all, California produces 8% of the nation’s food supply.

Why did you buy it???

I am confused why SOFR would ever go above the upper limit of the FFR if SRF is there to provide better rates?

Do banks rather pay an extra in order to avoid tapping the SRF? Perhaps there is stigma associated with using it?

“Section 11 of the Federal Reserve Act, as amended by section 1103 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, requires that detailed operational results, including counter-party names, be released two years after each quarterly transaction period.”

And there is no liquidity shortage, there is a trust shortage. Liquidity can be had, just not at the cheap price the banks want.

I expect SFR being tapped more and more, and while we saw a dip in amount today, would not be surprised to see that go back up, ‘until moral improves’ aka QE w/vengeance.

“Do banks rather pay an extra in order to avoid tapping the SRF?”

No, banks LEND to the repo market. Repo market rates jumped because banks didn’t lend their reserves in sufficient amount to the repo market. Banks sit on $23 trillion in cash from depositors, and their $3 trillion in reserves at the Fed are an excess of that. They don’t need to borrow in the repo market. The $7 trillion in money market funds are the other big lenders to the repo market.

What is the impact of the tariff proceeds? I thought those inflows went to the TGA. Does it help? And by how much?

I mentioned that in the article. They’re part of the cash inflow into the TGA, along with fees and taxes.

Well, with the Treasury now full, the U.S. government could almost afford to buy a quarter of Nvidia stock. To put the above in perspective, what Nvidia makes in a year, the U.S. government spends in four days. There is a two orders of magnitude mismatch right there, but draw your own conclusions.

This is a great article explaining the dynamics of the Repo rate over the last week or so. Thank you.