Shareholders got wiped out, noteholders take losses and get the company, banks appear to be largely unscathed.

By Wolf Richter for WOLF STREET.

Here is an example of who is taking the losses from the office meltdown in commercial real estate: Office Properties Income Trust, a publicly traded office REIT that owns 122 office properties with a combined 17.1 million in rentable square feet of office space, filed for Chapter 11 bankruptcy on Thursday – the first office REIT to file for bankruptcy.

The US government is the largest tenant at its properties. The occupancy rate across all properties has dropped to 77%, according to the company’s Business Plan released in August.

The properties themselves are managed by a property management company, The RMR Group. Office Properties Income Trust is just the owner.

So who took the losses?

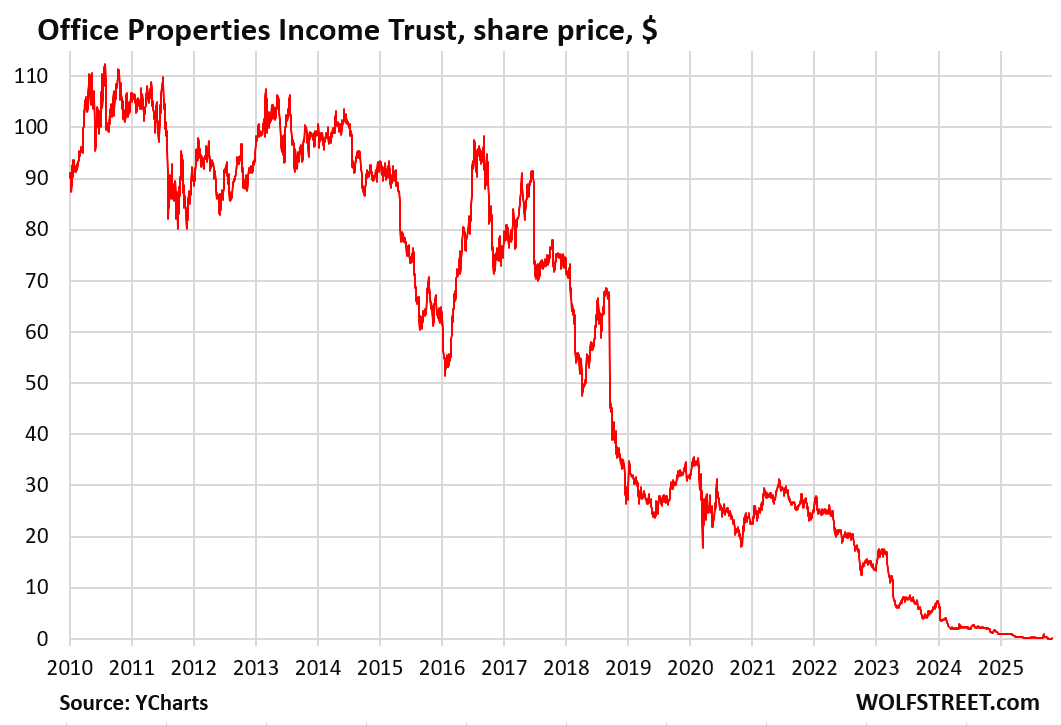

Stockholders first: And that started years ago. In 2017, market capitalization of the REIT was nearly $2 billion. After the total collapse of the shares since then, market cap is now essentially zero, with the delisted shares trading Over the Counter for 2 cents, down from over $110 in 2010.

So over the past 8 years, $2 billion of the losses were taken by stockholders collectively – a near 100% loss that could become a total loss, as the company warned in its SEC filing about the bankruptcy: “The Company expects that holders of Company’s common shares of beneficial interest could experience a significant or complete loss on their investment, depending on the outcome of the Chapter 11 Cases.”

The REIT listed $2.42 billion in debt in its bankruptcy disclosure with the SEC, not including unpaid interest. This debt is composed of: Two mortgage loans totaling $177 million (UBS and JPM), secured by specific properties; and eight note issues totaling $2.24 billion, some secured, others unsecured.

The noteholders. Of this $2.24 billion in bonds, $280 million mature in 2026. But as of June 30, the company had only $78 million in unrestricted cash and $14 million in restricted cash. In Q2, it booked a net loss of $87 million. Losses in Q3 likely ate further up the cash cushion, and out of cash, the company filed for bankruptcy.

When OPI filed for bankruptcy, it also entered into a restructuring agreement with holders of its secured notes – so a pre-packaged bankruptcy filing. The agreement, which still needs to be approved by the bankruptcy court, calls noteholders to give up $1.1 billion collectively, in exchange for equity in the restructured company.

This agreement would reduce OPI’s outstanding debt from $2.4 billion currently, to $1.3 billion upon exit from bankruptcy. The new owners will mostly be the noteholders that received equity in exchange for the debt.

How much the debt holders will collectively lose depends on the outcome of the bankruptcy proceedings and the ultimate value of the equity in the restructured company that they will receive in exchange for the debt.

The banks: The filing listed a $54-million mortgage from UBS and a $123-million mortgage from JPM. It appears, the banks won’t have to endure a haircut or have to take the office buildings back as part of the bankruptcy, though the mortgages may be amended or restructured.

In case you missed it:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Stonecutters:

Who controls the British crown?

Who keeps the metric system down?

We do, we do!

Carl: Who leaves Atlantis off the maps?

Lenny: Who keeps the Martians under wraps?

We do, we do!

Who holds back the electric car?

Who makes Steve Guttenberg a star?

We do, we do!

Seymour Skinner: Who robs cave-fish of their sight?

Homer: Who rigs every Oscar night?

We do!

We do!

The Simpsons Take the Bowl

Who controls the British crown?

Who keeps the metric system down?

We do, we do!

Who keeps Atlantis off the maps?

Who keeps the Martians under wraps?

We do, we do!

Who holds back the electric car?

Who makes Steve Guttenberg a star?

We do, we do!

Who robs cave-fish of their sight?

Who rigs every Oscar night?

We do, we do!

Who gives their song an extra verse?

With no time to rehearse?

We do!

We do!

Average occupancy 77% and still you go under?

I would have thought that could keep ship afloat/give time to cut the real loss buildings and turn into build-able lots what have you.

I guess the purchase prices were way too high/just mismanaged.

It’s not the occupancy rate that pushed them into bankruptcy (though 77% doesn’t help). It’s the bonds that come due in 2026, and the company is out of money and cannot borrow more and cannot pay off those bonds and cannot afford to pay the current interest rates that deep-junk-rated bonds come with. There is no way around this without a debt restructuring.

Bad CRE is something the Federal Reserve should own; perhaps by trading MBS that has equity for the worthless CRE at face value. That would be a win-win in the losses being socialized while the MBS loss is never realized.

Sarcasm, I think?

Excuse me Gary, but I would very much appreciate my tax dollars to not be spent bailing out CRE bag holders based on their poor investment performance. I really hope your comment is sarcastic. Otherwise, you might get an earful from Depth Charge (I’d relish that).

The Fed prints it’s own money; it doesn’t use your tax dollars. If they owned this on their balance sheet, they could cancel it and their “assets” would be less, a graph Wolf has shown many times. (Note: I agree that the original comment is just sarcasm.)

Let’s get him, boys!

You want to own commercial properties?

-stay away from banks

-stay away from mortgage on property

-stay away from property management (they are clueless anyway)

-do maintenance yourself

-own the property free and clear

-make the tenants happy

And you’ll make mucho dinero…easy 10% NOI…

Two questions.

How do you accumulate the cash to buy f&c?

Is it a full-time job to manage and do maint?

1.I happened to accumulate the necessary cash after 32 years of working my butt out in different industries including construction…

2. Maintenance is determined by building repair need…I happened to remodel it from top down, including new parking lot, new roof, new electrical panel etc…

Due to my experience, maintenance is a walk in the park…

PS. Depending where you live, commercial building maintenance is prohibiting expensive…just to adjust a front door the guy wanted $2,200 …I’ve told him to get lost…

@truthseeking congratulations of you are getting a 10% NOI (aka ROE if you don’t have any debt) but few people (even those that do ALL the management and maintenance themselves) have seen a 10% cap for decades. Are you getting a 10% return on the “current” market value of your peoperty (you use “current” market value to calculate NOI not “purchase price”),

And have bought the building many years ago

So was the property management company and its management fees the way the monies got funneled to the right people instead of the bagholders? Or how does it work?

Yes. The question is whether the compensation was commensurate with the service provided or inflated to line their pockets? Eye of the beholder and all that.

How can the bank note holders be “largely unscathed” if they have to exchange debt for common stock in a bankrupt company?

As the article points out, the two banks hold mortgages (not notes) secured by specific properties, and the REIT is going to keep those properties and maintain the mortgages.

It is not just occupancy percentage, it’s also amount of the rents, which may have been declining to maintain the occupancy they have, and the prices paid by the REIT to acquire the properties, and the fees and commissions paid to set up and maintain the Reit.

Don’t forget that local governments will lose on property taxes, since the buildings’ valuations must also go down (if they haven’t already).