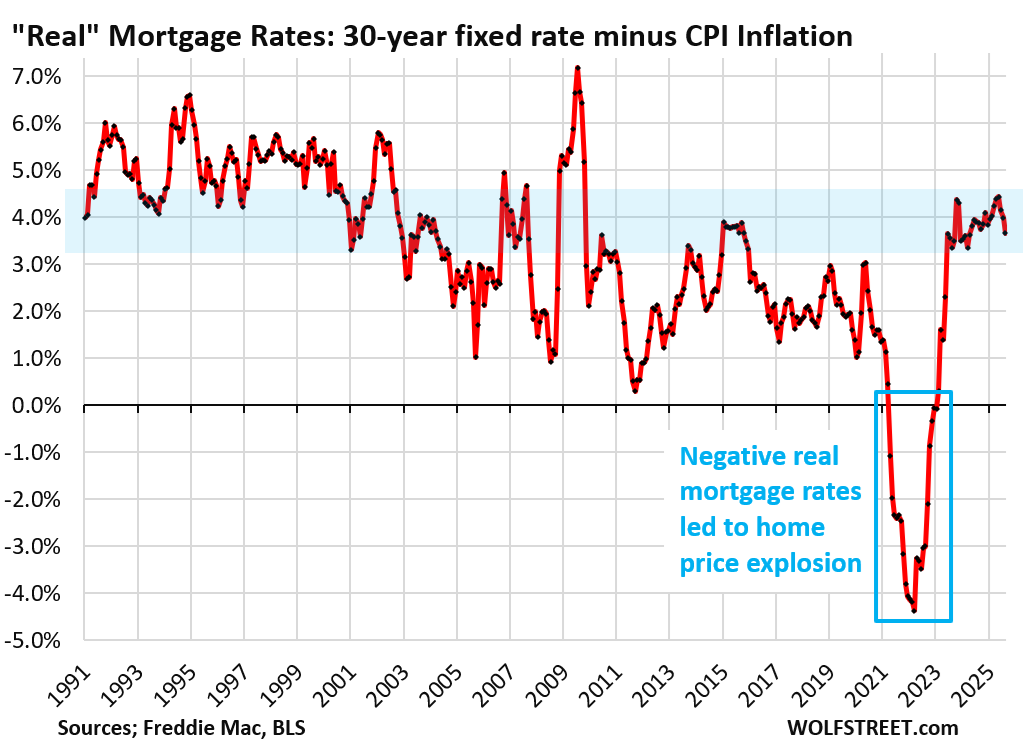

So mortgage rates are not the problem; they’re at the low end of the pre-QE historical range. Those exploded prices are.

By Wolf Richter for WOLF STREET.

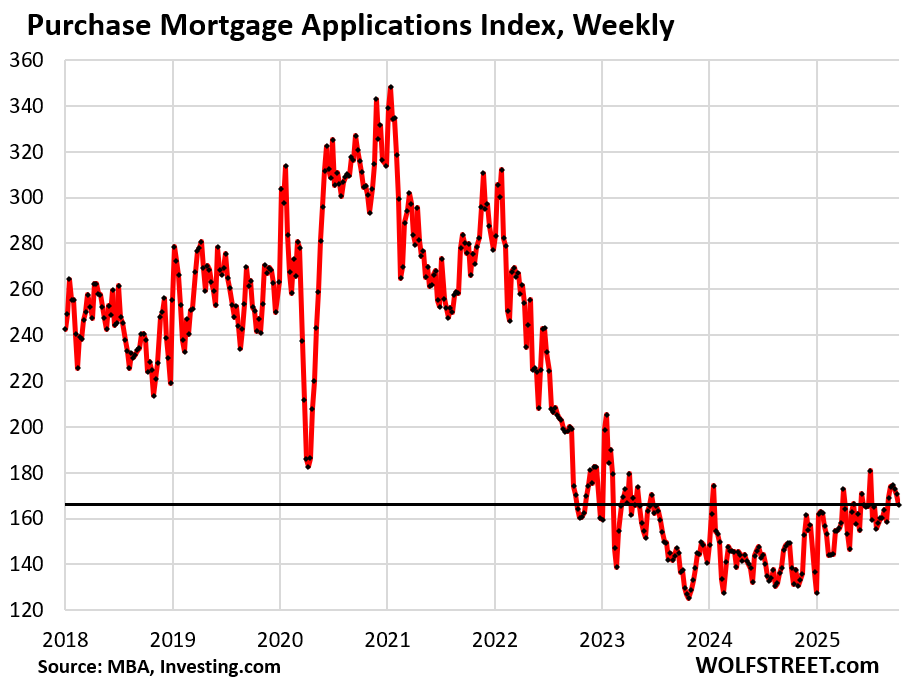

Despite slightly lower mortgage rates, demand for homes by homebuyers who need a mortgage dropped further in the latest reporting week, the third weekly decline of purchase mortgage applications in a row, according to data from the Mortgage Bankers Association today. Compared to the same week in 2019, purchase mortgage applications were down by 34%.

Demand in the housing market plunged three years ago, after home prices had exploded over the preceding two-year period of a mega-FOMO-driven frenzy, fueled by mortgage rates the Fed had recklessly repressed via QE to way below the rate of inflation. So mortgage rates are not the problem; those exploded prices are.

These applications for mortgages to purchase a home are a measure of demand that may become actual home sales in the future and are therefore an indicator of future home sales. And they remain dismal.

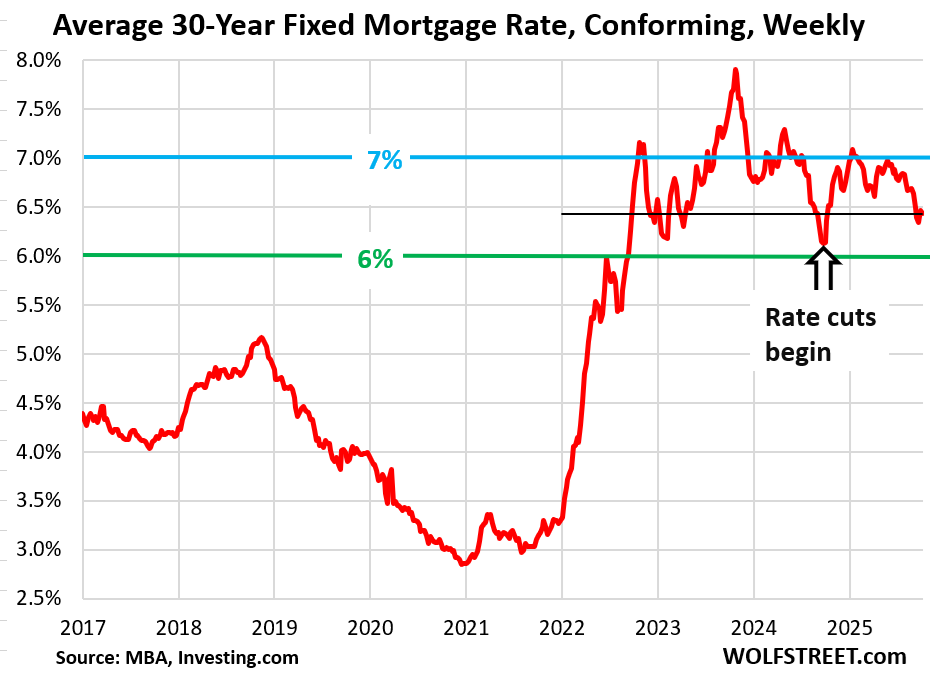

The average weekly mortgage rate for conforming 30-year fixed mortgages declined a hair to 6.42%, according to the MBA today. This measure bottomed out last year in September and early October 2024 at 6.13%, just before the Fed started cutting interest rates.

Last year from mid-September through mid-December, the Fed cut its policy rates three times, by a total of 100 basis points despite re-accelerating inflation. The bond market, including the mortgage market, got spooked about a lax Fed in light of re-accelerating inflation, and went the opposite way. From mid-September 2024 through early January 2025, mortgage rates jumped by 100 basis points.

After that episode, the Fed talked hawkish and put rate cuts on hold to keep a lid on the bond market. Even now, as rate cuts have started again, the Fed is talking about “careful” rate cuts, and being “concerned” about the “rising inflation,” and “watching it closely,” etc. etc., while reacting to labor-market weakness. The last thing they want is another spike in long-term yields.

The Fed’s reckless policy of pushing mortgage rates far below the rate of inflation via QE, including the purchase of mortgage-backed securities, pushed mortgage rates below 3% even as inflation was raging toward 9%, thereby creating the most negative “real” (inflation adjusted) mortgage rates ever.

For homebuyers, the steeply negative real mortgage rates were better than free money, and when money is free, prices don’t matter, and homebuyers went nuts. During this period I called it the Most Reckless Fed Ever. And as we now know, its recklessness has done enormous long-lasting damage to the housing market.

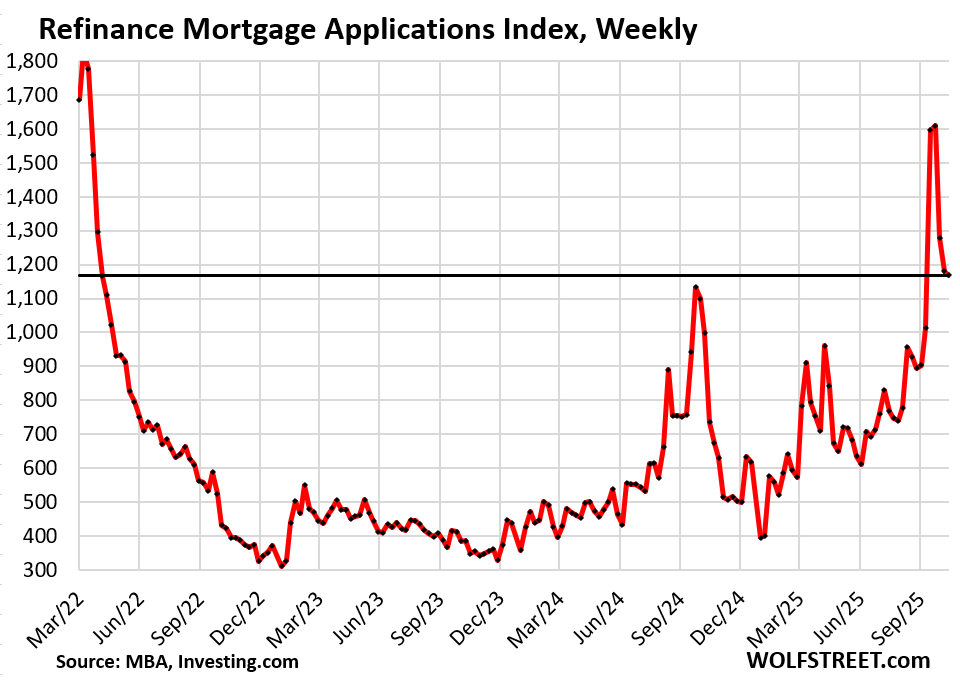

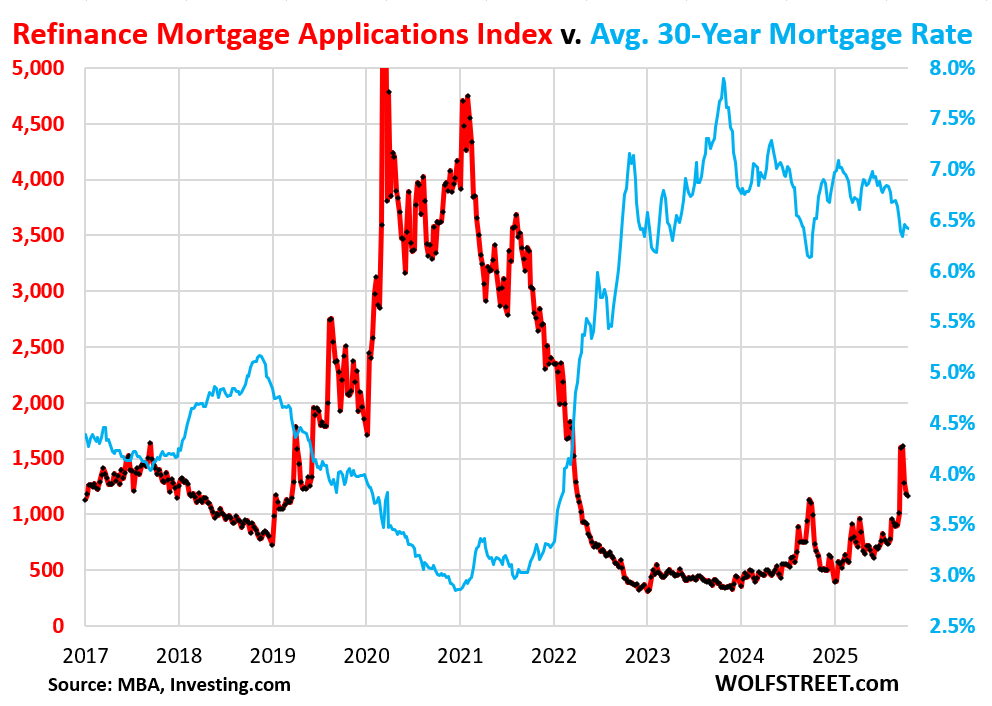

A funny thing happened with refis. That small drop in mortgage rates in mid-September by just a few basis points apparently pierced a magic line, and a bunch of homeowners suddenly refinanced mortgages, causing a spike in refi applications, but it lasted only for two weeks, and then it was over again.

Refi applications edged down further in the latest reporting week, after having plunged over the prior two weeks from the two-week-wonder spike.

It seems a bunch of homeowners had been sitting on the edge of their chairs waiting for rates to inch down to a magic level, and then they pounced, and there were no more people left sitting on the edge of their chairs?

It’s funny because mortgage rates barely moved over those six weeks.

The previous sudden spike in demand for refi mortgages occurred a year ago in September 2024, when the MBA’s measure of the average weekly 30-year fixed mortgage rate dropped as low as 6.13%, before surging again:

Refi mortgage applications (red in the chart below) and mortgage interest rates (blue) are in an inverse relationship. The below-3% mortgage rates while inflation was raging toward 9% caused not only an explosion of home prices but also a historic refinance boom when a huge number of mortgages were refinanced.

That spike of refi mortgage applications a few weeks ago was small compared to the boom years of negative real mortgage rates, but exceeded the volume in 2017, 2018, and early 2019.

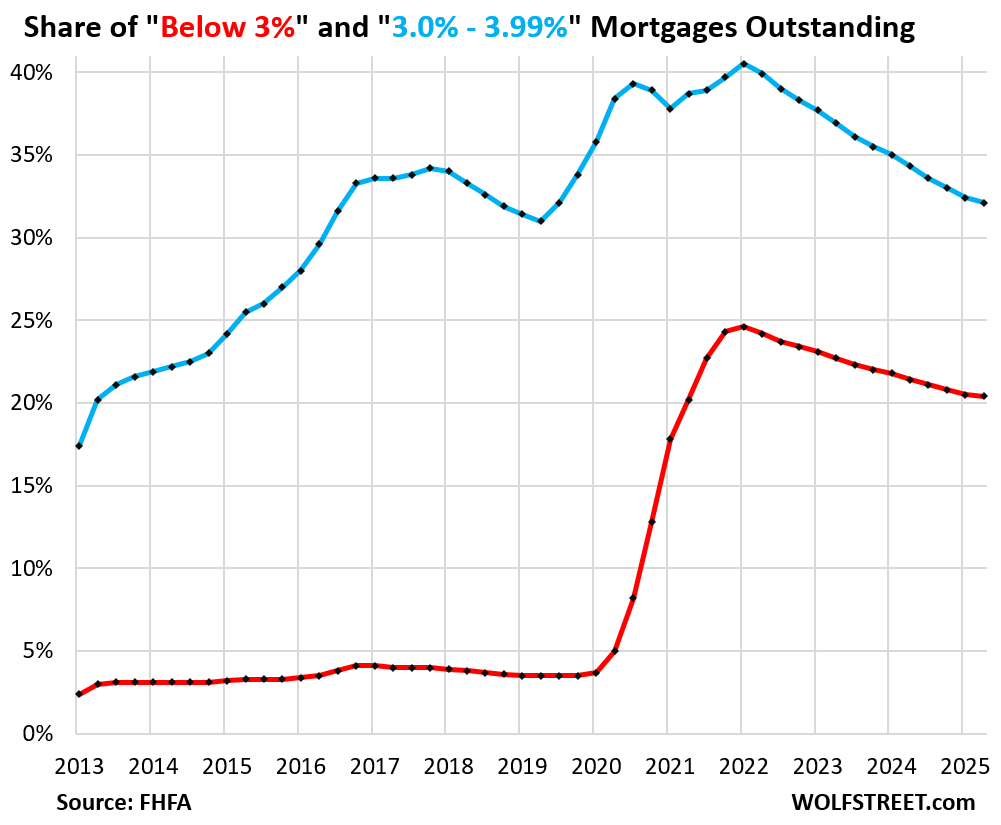

This refi boom in 2020-2021 caused a large portion of mortgages to carry very low interest rates, and homeowners now cling to these low-interest-rate mortgages as if they were valuable assets. Nevertheless, life happens, and homeowners are gradually getting out of these mortgages and loosening the phenomenon of the “lock-in effect.”

The share of below-3% mortgages outstanding declined in Q2 to 20.4% of all mortgages outstanding, the smallest share since Q2 2021 (red in the chart below). And the share of 3%-3.99% mortgages declined to 32.1%, the smallest share since Q3 2019 (blue). More on the slowly fading phenomenon: The “Lock-in Effect” and Mortgage Rates: Update on Unwinding a Phenomenon that Wrecked the Housing Market

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“and homeowners now cling to these low-interest-rate mortgages as if they were valuable assets”

I think on this point we disagree. A sub 3% mortgage IS a asset, just like an 8% guaranteed CD for 10 years would be considered an asset. These 3% mortgages are now paying off principal over 50% every month just 3 years in.

I would say Prop 13 in California is a similar “asset” or at least an asset enhancer.

Let’s see what happens when Trump’s slash in capital gains takes effect next year. That could bring a surge of homes onto the market. Mainly in the affluent areas, to be sure. but that is where the greatest disparity in home wealth gap effect in concentrated. Trump is also raising the tax brackets.

“low-interest-rate mortgages as if they were valuable assets”

I get that a mortgage is technically a liability, but I kinda see it the same way.

Rationally, it makes no sense to pay extra principle towards a 2.7% mortgage when other fixed-income products (T-bills etc.) accrue interest faster.

Principal*

Time to finish coffee.

But you should also factor in that you can get rid of INSURANCE once your house is paid off. For people who don’t plan on burning their house down anytime soon, this should be something you get rid of.

Trump’s proposal to eliminate the capital gains tax on housing was not serious, and is not going to take effect. Congress has to approve, and they won’t.

Even if it did happen, it will have zero effect on demand.

People don’t consider the demographic shifts happening and their effect on demand either.

From an accounting point of view the mortgage is a liability account and the measurable difference between current market and any fixed rate carried could be carried as asset, or a contra liability account, all blue sky or goodwill or of course.

It certainly is true around here where thousands of smallish (cheaply built) homes are going up like roaches crawling out of a damaged sewer pipe.

The builders (name brands) are offering 3.99% fixed for 30 years (PMI on the buyer with $5K down) and the homes are still sitting. Also, recently builders are knocking 5 – 10% off the list price to get action and PAYING a real estate agent who brings a buyer through closing a $5,000 bonus on top of the 3% fee. The new houses are priced at $150/170 sq, ft. depending on location and options.

A few years ago, these were $100/sq. ft. homes.

Dollar debasement, inflation, fed buying MBS in excess, and investment firms buying properties are factors to why prices appreciated the way they did. At the same note of token, those who bought post 22 accepted 6.5 average refis. Buydowns only work if lenders can keep their prices listed. They absorb a tok of loss, which is why Lennar and Dr Horton are mentioning lower revenue. The last administration pressed the GTFO button on spending and now we are here. Interest rate cuts, or even rolling out MBS won’t address the problem, rather exacerbate rates. Time to accept rates aren’t going to drop and time to accept currency devaluation got prices stuck where they are at.

I think in the fantasy land camp talking points from RE agents, when it’s implied lower interest rate will bring the sizzle back to the housing market, most of them are probably thinking of the once in a lifetime <3% 30 yrs mortgage rate as the savior, not the current barely noticeably still above 6% 30 yrs…I am sure whoever still pumping the low interest rates narrative will likely say that as their defense and continue to dope out hopes we will be back there again one day, so buy now and don't miss out, cause if you wait until then, it will be bidding over asking, lines out the corner at showing when we're at ultra low rates again…blah blah.

Personally, I pray we will never see ultra low mortgage rate make a return in my lifetime, it was not needed and created problems that will lingering for many years that F over future generations. I would rather see price drop 30-50% and mortgage rates at 10% so for large downpayment or cash buyers, they are not force to overpay and rely on the magic formula of housing can only go up mindset, plus it might actually condition to people to save money for bigger downpayment in an effort to avoid paying interest…

It’s a combination of interest rates and prices. If either went down alot, sales volume would go up alot.

not if prices do not fall… they are horribly bloated! Middle class and entry level people just cannot do it.. this also drives rents up.. There are no entry level homes.. 350k is not anything but a cheap ass mobile .maybe or a POS trashed home, that needs major work, STILL over priced. I see homes sitting for months with no price change in Carson city, Reno.. and nothing under 1 million with one acre , its laughable.. California cheaper with lots of price drops.. but the taxes and fire insurance are driving that.

But there is nothing wrong with mortgage rates. And if inflation rises a little further, they’re going to be too low.

I’m not disagreeing with you on that, I agree with your whole take on it. Its the prices! The agents also drive that train too. If a house sits for 30 days with no offers, it’s priced too high. Sellers get stuck in the “HOPE” .3 offers in the same price range should tell you that’s market value. I know because I have made offers and not low ball, and the homes are still sitting months later with no price reduction. Minden, Carson, Genoa, anything by Kingsbury Grade, anything green and not desert, insane price.. my agent is blown away. My own home is over a million, but not really, more like 700K (if it was listed at that it would be bid up!).. its NOT a million dollar home at all. But it’s in Sparks ranch land with huge build up around it.. NV has gone nuts.. you really should include Reno and Carson area in your research… $$$$ anyway, I digress..

“you really should include Reno and Carson area in your research”

Reno is included in my research, all you have to do is click on the headline:

Condo Prices Dropped by 12%-27% in these 25 Bigger Cities through August: Condo Bust Update

And the Las Vegas metro is included here, so click on it:

The Most Splendid Housing Bubbles in America, Aug 2025: Price Drops & Gains in 33 Large Expensive Metros. Overall US Home Prices Fell YoY

Why would you want to see housing sales go up at all?

I have heard it said: The housing market is the economy.

Obviously it’s not everything, but it’s home services (everything from the transaction to the maintenance and remodel), construction and a sign of household formation.

It’s not just the construction guys, banks, realtors and economists all like to see a vibrant market.

First thought: Homeowners with low down payments have more invested the longer this goes on which, in theory, should help to lower defaults and losses when the inevitable recession arrives.

Second: Many are married to the rate and want to divorce the house due to issues such as insurance, HOA frustrations, boredom, job opportunities. Those dating the rate, in realtor parlance, have more opportunity.

Eventually the accidental landlords will come off of their prices and move the market a bit.

Either way I stick to my position that prepayments of mortgages will accelerate in 2027.

Not enough housing in popular areas, and those owning rentals, both private and corporate are content to hold on. Rents have not dropped enough to convince them to sell. Have a relative in CA, they will stay until the die (locked in by Prop 13) and the like where they are at. Their two kids, representing pent up demand for additional housing are outa luck. No signifiant new construction in their area for years. Their only option is to move away, but they need to find the combo of a good job plus low cost housing…

And more states have now passed laws to cap property tax increases regardless of home value change. Politicians have no incentive to allow market forces to drop housing values. That’s why the only political solution we hear from officials is “build more housing!”

If property taxes were allowed to freely vary like home values do, that would be a force against housing inflation.

Property taxes being fixed at transaction value means that municipalities are forced to build more since they can’t block construction and get more taxes.

This means that California is in better shape than it would be if not for Proposition 13.

That being said, Cali is infamous for godawful anti-business policies, and so new construction can’t really happen. That’s why people are leaving that state. When you adjust for cost of living California is poorer than Mississippi if you’re unfortunate enough to have to buy a house.

Arbitrarily fixing property taxes is grossly unfair. To have a neighbor literally paying twice as much, or more, makes no sense. Generally more wealthy owners pay less than newer less heeled owners. The incentive is backwards. If anything, do the reverse. The longer one is in a home, generally the more wealthier they get and are able to pay more taxes. But the sane for all would be the most fair.

“..and so new construction can’t really happen.”

That’s an exaggeration. California has been building about 110,000 housing units per year. Over the past five years, it built 550,000 housing units. If the average occupancy is 2.3 per home, it creates homes for 1.26 million people in a five-year span. There is quite a lot of inventory on the market now.

“Arbitrarily fixing property taxes is grossly unfair.”

Taxing people base on FAKE bubble prices is grossly unfair.

What is the opposite of an anti-business policy. Would that be a pro-business policy. Owning a home is a business for me. So I don’t get the point of anything going on here. I and my kids have a great business here. Actually we have cornered the market.

@4hens:

Building more housing is definitely needed. I don’t think that enough will be built to address pent-up demand.

I suspect that we will see maybe a 5% increase in housing units, and that this will not be enough.

Then, the media yak-yaks will say “SEE? We built more housing and it didn’t work!”

I am still on strike,a cash buyer that wants a modest home with 20 acre minimum,will finish the rest of property to my needs.

I am not looking for bottom feeding pricing(though would take it!)just more reasonable pricing then what I see…….,sigh.

The entire housing market is a SCAM.

That’s my editorial/PhD thesis.

Nobel Prize in literature coming up?

I hope it wasn’t too wordy, or confusing.

SCAM, Ponzi or rugpull, take your pick. Even people that bought just 2 years ago are now asking 20% more often without doing anything and expect to pawn it off to the next bag holder. Boomers that bought eons ago that want to sell are now trying to unload to future generation and cash out their golden ticket….The whole thing kind of stink, do remind me of some elements from ponzi and Crypto rugpull, get the top dollar and before too the last one out the door

Trump set for unprecedented Supreme Court attendance: ‘The most important case in history’

President Donald Trump said Wednesday he would likely make the highly unusual move and head to the Supreme Court to watch cases related to his tariffs be argued.

I’ve been watching house prices in many areas in the Mountain West and Sunbelt. I’ve also been looking at Airbnb monthly rental rates in the same areas. Both are extremely exaggerated. $3000 barely gets a guest suite or a small studio in most of the US. And, almost all listings on Zillow are at 2021-22 levels. People have lost their minds. When the market finally gives into price pressure, there will be blood.

“It seems a bunch of homeowners had been sitting on the edge of their chairs waiting for rates to inch down to a magic level, and then they pounced, and there were no more people left sitting on the edge of their chairs?

It’s funny because mortgage rates barely moved over those six weeks.”

We all got frantic calls from our loan officers telling us rates were finally coming down and asking us to refi.

Has anyone seen those listings just a little over $1.25M for a gorgeous looking SFH 3B5B of 3,124 sf with spectacular ocean views in La Jollo or Newport Beach? It is 1/8 of the ownership (co-ownership) 😂 how does this even work? Gosh how many homeowners are out there out of their mind?! 🤯 guess even worse? One house in La Jollo were sold for $1.35M twice – once on 12/09/2024 & once on 09/20/2025. Oh my gosh 😂 are these people mentally considered normal or healthy? How do they even divide the # of days stay for each of these 8 owner groups? Who gets X’mas & who gets 🦃? 4th? SoCal housing markets has some really bizarre things going 🫢

Time shares have been around forever (for vacation homes). Trying to sell your share can be very difficult and involve big losses. Only the developers of times shares make money.

Back in 2005, I was fresh out of high-school and was setting modular homes. Whole neighborhood ghost towns were built. All on the speculation of future demand while systematically subduing borrowers. I drove passed a suburb freshly built yesterday, not a soul buying, saw another which was primarily investment rentals suddenly put the whole neighborhood for sale. In the end they’ll say poor people didn’t pay the rent, when in fact it is those drunken sailors greed that sank their ship.

I noticed there are so few listings on the market here in the DC Swamp that even total crap is selling if it is priced right. However, becasue of the frozen market, and buyer’s strike, many realtors have let their real estate licenses expire as there is no activity. They cannot even pay their license renewal fees. There are at least 50 Realtors for every listing. The whole Real estate career field has turned into another Amway ponzi scam, where they extract all kinds of fees to enter a career where there is no business.

Seeing an increasing number of “sell for 1%” for sale signs here in the midwest. Long may it continue.

… one place where almost no-one will moan about the impact of automation.

Be interesting the impact should the employment picture change significantly. My gut feel is not that much unless it cuts really deep and that isn’t expected.

Real median household income has barely budged since 2019.. Go check FRED. Where are the buyers going to come from at these high prices?

You cannot use inflation-adjusted income and not-inflation-adjusted prices. That’s apples and oranges. You need to use nominal income and nominal prices.

I think the jump in refi applications are those that had 3, 2, 1 buydowns at 8 plus percent. As someone with a 7% mortgage, it makes no financial sense until rates are nearly 5% given the thousands in refi fees. My payback period on those fees even at 6% is longer than I want to stay in my current home.