The bond market has taken the opposite bet, and the dollar has strengthened.

By Wolf Richter for WOLF STREET.

A hot theme widely bandied about to pump up cryptos, gold, silver, and even stocks is the so-called “currency debasement trade.” The idea is that enough traders rally behind a common theme to move prices in their direction for long enough to make a serious buck and generate fees from the trading.

This debasement-trade theme is a bet that government borrowing and money printing will erode the value of the US dollar dramatically and quickly, and that therefore enough investors will pile into cryptos, gold, silver, and even stocks, to cause prices of those instruments to explode. And they did.

But the huge bond market has taken the opposite bet, led by the $29-trillion Treasury market, the $11-trillion corporate bond market, the $9-trillion residential MBS market, the $4-trillion municipal bond market, plus the other segments of the bond market, where yields have fallen this year and have been in the same relatively narrow range for the past three years.

These bond investors bet that inflation will cool further over the longer horizon, and that the relatively low yields they get on their securities will therefore adequately remunerate them for inflation and for the risks they’re taking, and that the cooling of inflation will cause yields to decline further in the future, thereby pushing up prices of bonds that had been issued earlier at higher yields.

If the bond market were fearing a rapid and substantial debasement of the US dollar – the theme being hyped by the debasement trade promoters – it would demand much higher yields. But that hasn’t been the case.

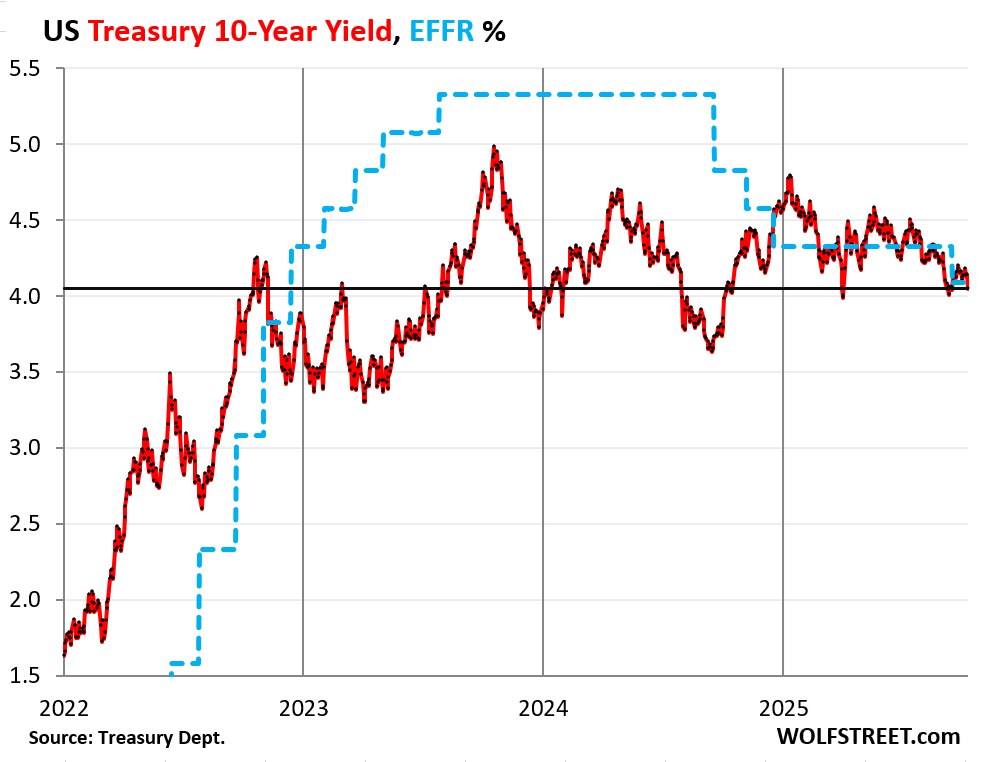

The 10-year Treasury yield, for example — now barely above 4% as of Friday evening (bond markets are closed today) — has been on a downtrend this year and has been roughly in the same range for three years:

But, but, but, the US dollar…. The dollar’s drop during the first half of 2025 has been falsely promoted in clickbait headlines and by braindead manipulative talking heads on TV, as “the steepest decline in more than a half a century,” or whatever.

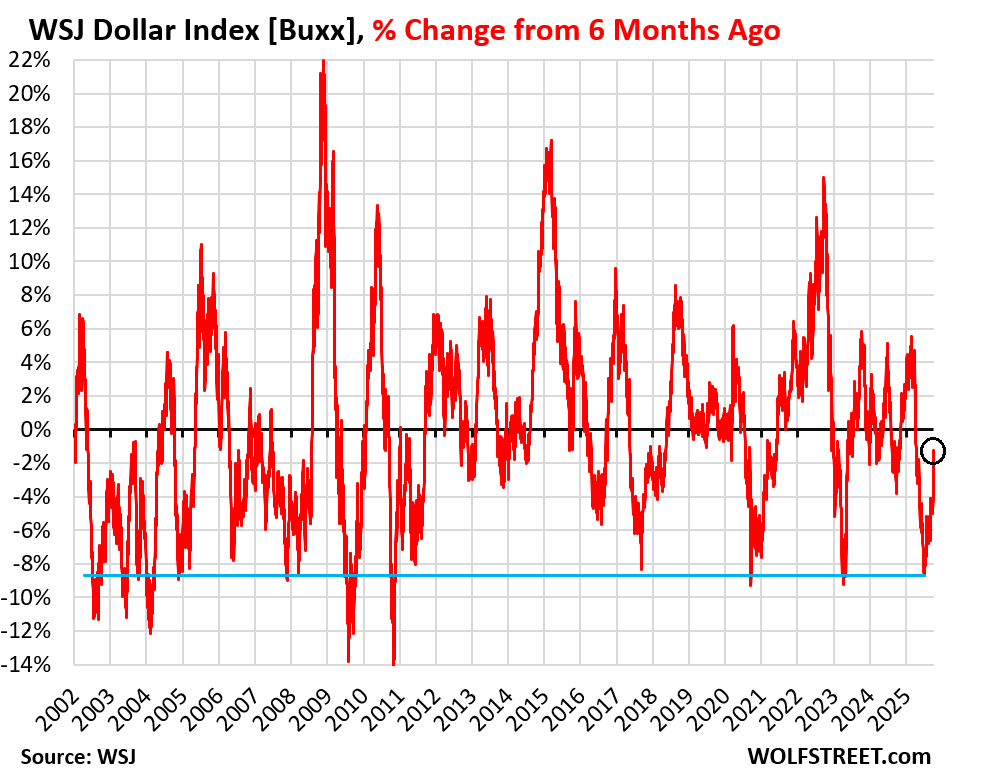

What did occur is that the dollar indices had spiked in the last four months of 2024 and topped out at the very end of December. And that four-month spike was then unwound-plus-some over the six months exactly from the beginning of January through the beginning of July, with the euro and yen dominated DXY Dollar Index dropping 11% and the broader WSJ Dollar Index [BUXX] dropping 9% over the first six months of the year.

But even bigger six-month drops were common and bottomed out in:

- April 2023

- September 2020

- November 2010

- August 2009

- April 2008

- June 2007

- Etc., all the way back to Adam and Eve.

The only thing that was unique about the 6-month drop in 2025 was that it started at the beginning of January. Only the start date was unique.

This chart shows the 6-month percentage change of the WSJ Dollar Index [BUXX], which tracks a basket of 16 major currencies.

The blue line indicates the 6-month 9% drop from the beginning of January through the beginning of July. Note all the even bigger 6-month drops that have dropped through the blue line over the past 23 years.

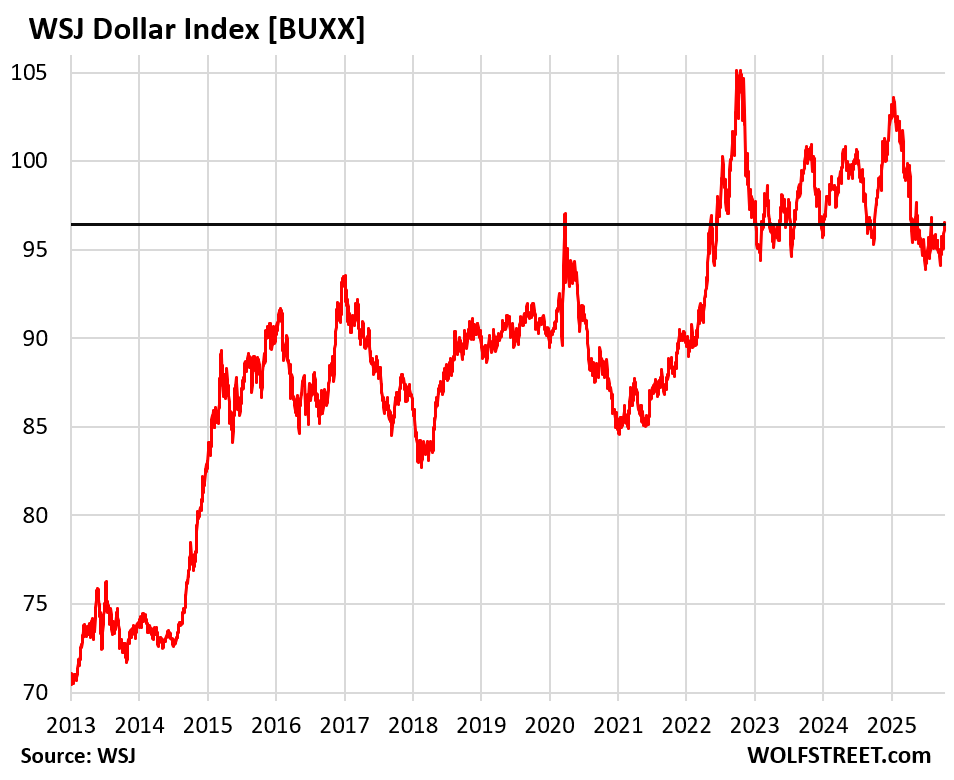

And of course, the dollar has bounced back some since the beginning of July with the WSJ Dollar Index rising today to 96.4, up by 2.6% from the low at the beginning of July.

The 16 currencies in the trade-weighted index are: Euro, Japanese Yen, Chinese Yuan, Canadian Dollar, Mexican Peso, South Korean Won, New Taiwan Dollar, Indian Rupee, Hong Kong Dollar, Singapore Dollar, British Pound, Australian Dollar, New Zealand Dollar, Norwegian Krone, Swiss Franc, and the Swedish Krona.

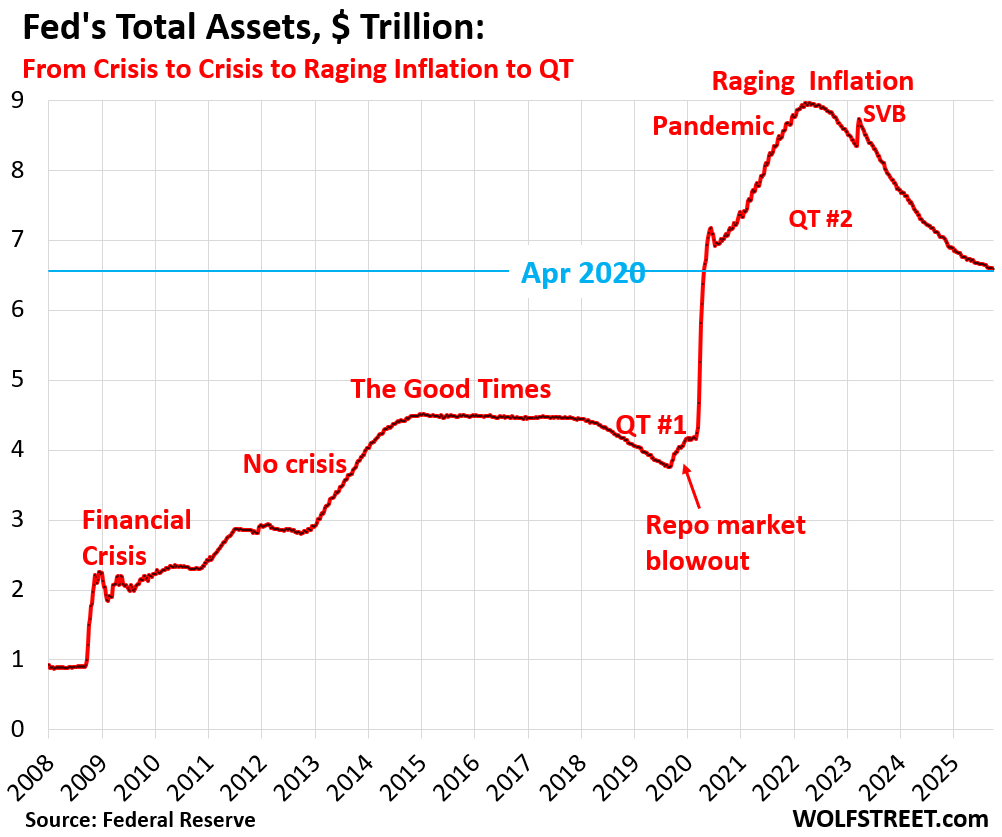

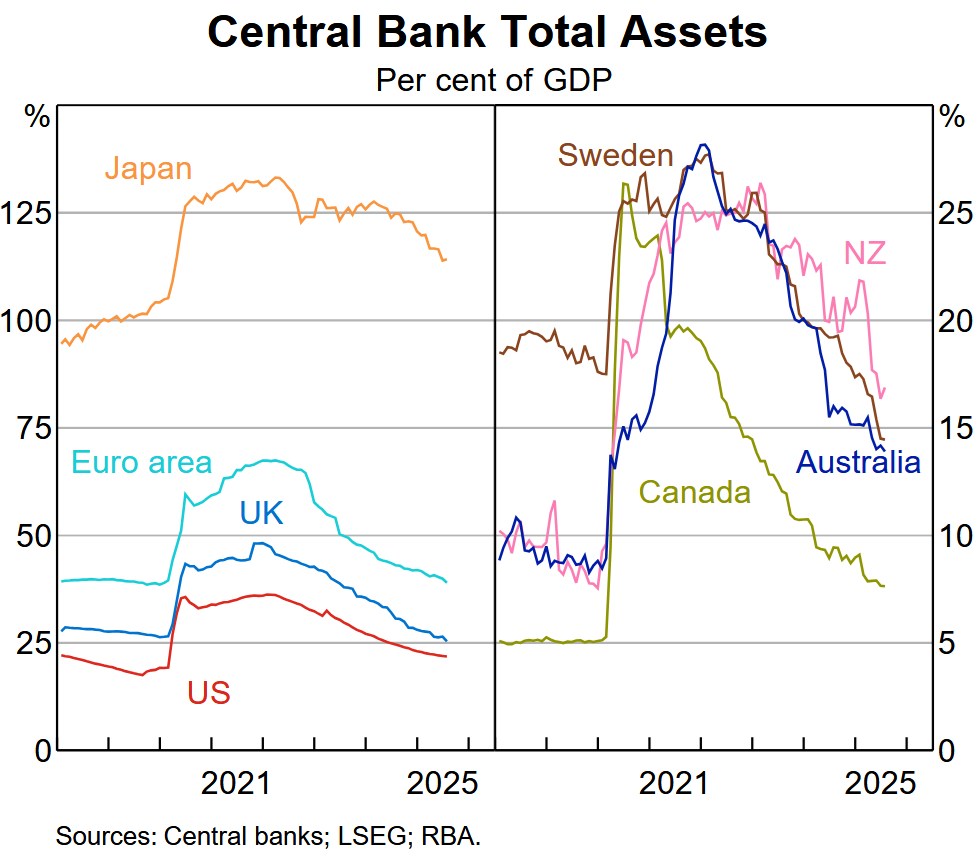

The Fed has been doing the opposite of “money printing” for over three years, having shed $2.4 trillion in assets by now – “money unprinting?” – and it continues to shed assets under its Quantitative Tightening program, and folks promoting the debasement trade need to take a look at this:

Other central banks too have been shedding assets under their QT programs, most notably the ECB and the Bank of Japan. Here are the balance sheets of some of the major central banks in relationship to the size of their economies, another eye-opener of what the debasement trade faces: Amazing How the Money-Printing World Has Reversed.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Too many moving parts at the moment to understand bond yields. There is a huge amount of manipulative accounting and regulation to push bond yields lower. For example, if the GSEs didn’t exist and the Fed didn’t own any mortgages, what would that do to mortgage rates, bleeding over to all the other bond instrument yields?

Mortgage rates would surely be higher without the taxpayer on the hook.

TYPO:

What did occur is that the dollar indices had spiked in the last four months of 2025

Should be 2024.

Thanks for all you do!

Not so much a debasement trade, but an effort to not be in anything $ denominated-such as stocks, bonds, cryptos, myrrh, etc.

At the start of the pandemic I bought a pound of gold, 16 one oz bars. This week I bough a gold miner ETF – GDX, and a Silver ETF – AGQ. Just before the last fed meeting where they lowered rates by .25 I started to go short with SDOW & SQQQ. All of these investments are up except SQQQ and if the dollar goes up just a bit more I plan to add a dollar short.

I’m hopeful the fear and panic will continue coming from the gold and silver sales folks and doomsday people or that our President keeps opening up his crazy mouth threatening tariffs… also I hope not too many people discover Wolf.

As for money printing, sure they’re tightening by shedding balance sheet assets, but the national debt, personal debt, and funny crypto money and all manner of assets at nosebleed levels, combined with what it takes to bring home a bag of groceries makes it pretty easy to be fooled into thinking they’re printing money, or that fiat money is being debased.

Great comment. The POTUS seems to get most of what he wants lately and he VERY much wants to run the economy hot. He VERY much wants the fed to abandon that imaginary 2 percent inflation target. He VERY much wants to rev up the crypto world too. It is going to be VERY fun to see if that giant bond industry is right about this or the POTUS gets to “grow our debt away”. I’ve got popcorn and a great view of the battlefield!

Cryptos are being debased each and every day by definition via mining of new cryptos. And there are now tens of thousands of cryptos. But it doesn’t really matter because they’re just gambling tokens anyway.

I agree that they’re purely speculative and not “investments” but a Bitcoin doesn’t get debased by a Memecoin any more than a Rembrandt gets debased by a painting my daughter does in school.

My understanding is that ultimately any crypto coin is a string of numbers stored on a computer network, basically a secret code that describes each individual “coin”. Unique and special and apparently valuable.

So with Bitcoin being the Rembrandt of crypto, what stops anyone from creating “Bitcoin 2” where all 21 million magical numbers just have a “2” added to the end and then there’s a second Rembrandt level coin that can be traded and hoarded and make everyone rich? Now there’d be 42 million “gold standard” cryptos out there..

I suppose someday there could be a “3” and a “4” and a “5” but let’s all try to get rich first before anyone figures it out. Who’s with me?

bitcoin gets debased by bitcoin mining (first sentence in my comment above).

The whole crypto space gets debased by thousands of new cryptos and coins arriving every year (second sentence in my comment above).

I’d guess no one is trying to buy your daughter’s painting (no offense).

But plenty of people are buying fartcoin.

Ironically your daughter’s painting may turn out to be the better investment long-term.

You no doubt bought 16 troy ounces of gold, right? These ounces are heavier than avoirdopois (spelling?) ounces by nearly 11%; there are 14.583333…. troy ounces in an avoiropois pound.

Also, one Troy pound is 12 Troy ounces, not 16.

Which is why a pound of feathers weighs more than a pound of gold. (A favorite puzzle from when I was a kid.)

I’m just having a hard time figuring out to do right now with new investments. I feel like I have enough bitcoin exposure, which I know this community generally frowns upon. I also feel like plowing even more money into stocks right now at these insane valuations is also risky, and I certainly have enough stock market exposure in my other accounts.

I have never been a big gold guy, but I have added a minimal amount just for some exposure over the last six months. If you have $550,000 of liquidity to work with, which I currently do, do you just keep rolling over 3-month CDs? That is what I have been doing, but now we have a dovish Fed.

I don’t need AI-like gains, but something better than 3.75% to 4% sure would be helpful. I know this is a first world problem, but any thoughts are appreciated (if this is even allowed). I am just frustrated with the CD returns and am wary of this market where one Truth Social post craters the market.

How much risk are you willing to take with that investment? Are you willing to lose 20% or 50% of that investment? 100% (all of it)? That’s the first question you need to answer to yourself.

Wolf, we must differentiate between losing “liquidity” for a time vs. losing “capital”. SPY, QQQ, DIA “cannot”

go to zero, but can certainly stay down 50% for a while.

Cryptos can go and many did go to zero. Many thousands of stocks went to zero, including formerly very big stocks. Many thousands of bonds went to zero. Lots of real estate investments went to zero for the owners when the lenders took possession of them. Even some real estate debt investments went to zero for lenders. Options go to zero routinely all the time. Those things are NOT coming back. They’re gone, vanished. Zeroed out from your portfolio forever. The list of what instruments went to zero is very very long.

ETFs can go to zero, or almost zero, such as the ProShares UltraPro Short QQQ that since inception has lost about 100% of its value, though it’s still out there getting traded.

Others went down a lot, including index funds that track the Nasdaq, which went down by 78% from March 2000 – Sep 2002, and stayed below its 2000 high for 15 years. S&P 500 tracking funds went down by 50% twice in the last 25 years.

Treasury Direct is mich easier then rolling CDs every 3 months. You can set any timeline (up to 2 years with T-Bills), build a ladder, so some money returns to your bank account automatocally. You will get approx 4.2% on 1m T-Bill now and it can be reinvested automatically ( up to 2 years). You avoid state tax on interest I think.

I do not believe there is better or easier “risk free” option right now. Paying off one’s mortgage is an option for some.

And SGOV is even easier for a small fee.

I asked AI about this. It says –

Quickly! Sell you car, buy triple-short ETF!!

It actually pointed me to some Farmers credit union 5.75% CD from July-September 2024. AI is pretty stupid.

AIs have date cutoffs for the data. Tell the LLM the current date and tell it to search for information it needs to fill in the blanks.

Do not attempt to use a tool that statistically predicts the next word or pixel for reasoning tasks.

As wolf said: “ These bond investors bet that inflation will cool further over the longer horizon, and that the relatively low yields they get on their securities will therefore adequately remunerate them for inflation and for the risks they’re taking, and that the cooling of inflation will cause yields to decline further in the future, thereby pushing up prices of bonds that had been issued earlier at higher yields.”

Sell the crypto and gold and lock in longer rates.

My opinion the USA is a deflationary bent economy. Somebody said the inflation is transitory.

Why exactly is the US a deflationary-bent economy? I’d argue that the way it’s structured right now, it’s quite the opposite.

To have a deflationary-bent economy you need an economy that favors savings and investments over consumption. This is emphatically not the United States and it hasn’t been since the 1930s. We’re quite the opposite, and if you want proof, look at the trade deficit.

This isn’t to say that can’t change – I think one of the long-term effects of Trump is that this change will happen, away from consumption and towards investments/savings – but that’s not how America is at present.

I went to AI to help explain what I think.

Force

Effect

Example

Technological innovation

Deflationary

Cheaper electronics, logistics

Competition

Deflationary

Margin compression

Credit expansion

Inflationary

Rising housing prices

Central bank policy

Inflationary

Money supply growth

Globalization

Deflationary (mostly)

Cheap imports

Capitalism by itself is structurally deflationary — because it relentlessly drives down costs through innovation and efficiency —

but modern capitalist systems are managed to produce mild inflation through monetary and fiscal policy to keep economies “growing” and debts manageable.

What about the Treasury debasing the $USD with an impending debt refinance bubble and continued COVID era deficit spending? Couldn’t gold be seen and a forward looking hedge to this and wouldn’t bond yields begin to spike as the market is flooded with new and refinanced notes? Or are you saying the market has already been flooded with these notes and they are still being gobbled up at depressed yields?

No. Gold is just a maniacally speculative laughable bubble commodity.

If gold was more than a speculative pretty rock it should be worth $280 sextillion today. per AI

The debasement trade is just the latest rationalization for line go up FOMO idiots. There’s always a new reason that valuations don’t matter.

I think we are the only ones that want to know the truth!

The Chinese along with every other central bank in the world has been adding to their gold reserves. Apparently these people are chumps and the place to be is low yield US bonds.

The article doesn’t say anything like that. You need to read what the text actually says before posting BS.

No, they have not and China only has 3,300 metric tonnes of gold and all central banks have NOT added to gold reserves by much at all and have around 35,000 metric tonnes which is about the same as they had 10 years ago with the US having the largest gold holdings of around, 8,133 metric tonnes owned by the US Treasury valued at $42.22 per metric ounce.

If everyone is worried about the stock market being a bubble because it’s at an all-time high, and because valuations like price/earnings are also relatively high, why doesn’t the same logic apply to gold?

S&P 500 has doubled in the last 5 years and is at all-time highs!

Gold has doubled in the 2 years and is at all-time highs!!

S&P 500 has a P/E ratio of almost 40!

Gold has a P/E ratio of infinity!!

Even if you believe gold is a hedge for inflation, shouldn’t that mean that its price after adjusting for inflation doesn’t change. And yet, the inflation-adjusted gold price is also at all-time highs.

In fact, the ratio of the S&P500 to gold price has been roughly constant for over a decade. It’s almost like the price of everything you can possibly is all rising at the same time! So how do you know which one will be the winner in the end?

From 1980-2000, the inflation-adjusted gold price went from 2500 to 500. Not much of a store of value.

The main indices (eg Dow) are down like 60 to 70 percent in the last 25 years when priced in gold. Check out Northstar on X he has some great long term ratio charts that eliminate the confusion caused by pricing with a rubber ruler.

Um, only because you picked a very specific and important date: 2000. This was the very top of the Internet stock bubble.

As I accurately said, the S&P500 to Gold ratio has not changed significantly in 10 years, and is about where it was just before the 2008 recession.

There’s one major time in recent history where you made more money on gold than on stocks: 2000-2008. If you stayed in gold, you then missed out on the stock recovery from 2012-2015.

Before that, from 1980-2000 the S&P500 to gold ratio increased almost 20x.

If the inflation-adjusted dollar is a rubber ruler, then gold is a random rock you picked up.

I was curious, so I backtested a few scenarios.

The critical factor is whether you rebalance, and that depends on whether you can buy and sell your gold annually.

If you do not rebalance, gold and bonds serve the same role; they both reduce overall yield but also reduce volatility and drawdown.

If you can rebalance both bonds and gold annually, gold is a better hedge than bonds. But if you can only rebalance your bonds, then bonds are better than gold.

So if someone wanted to put 5-20% in gold, and could be sure they could buy and sell it every year, that would be a decent investment choice.

Of course, since gold has had such a large recent return, is it a good idea after it has doubled in price? How much farther could it go?

Gold is a purely speculative unproductive asset, everything else is just a BS narrative. These people are becoming as annoying as “buy at any price” index investors. Clearly it’s the same mentality.

Thanks wolf

“If the bond market were fearing a rapid and substantial debasement of the US dollar – the theme being hyped by the debasement trade promoters – it would demand much higher yields. But that hasn’t been the case.”

Are there sectors, such as pension funds and insurers, who are required to invest in AAA-rated paper and thus can’t always demand higher yields in the absence of a clearly better alternative? I think that some large, institutional purchasers have limited options, especially insofar as foreign government bonds present a similar currency debasement risk.

“who are required to invest in AAA-rated paper”

no, not in the US

No exactly. No “mandate” per se, but banking (Basel III), insurance, pension regulations require “high quality liquid assets”, of which Treasuries get highest status. All other assets, including AAA corporate bonds, ECB, SCB bonds, do not.

that “who are required to invest in AAA-rated paper” was the question to which I replied with NO. You’re replying to a question no one asked.

In addition, since you brought up Basel III, banks only hold a small portion (6.2%) of marketable Treasury securities, or $1.8 trillion of $29 trillion:

https://wolfstreet.com/2025/03/18/who-holds-the-ballooning-us-government-debt-even-as-the-fed-and-foreign-holders-unloaded-treasury-securities-in-q4/

Insurance companies do I believe.

Insurance companies buy all kinds of credits, including some junk bonds, leveraged loans, CMBS and CLOs, of various ratings, etc.

Every political podcast now seems to have an ad selling gold. Dalio is on cnbc hyping it. There are swarms of substackers, Fintwit, podcasters that are absolute gold bull zealots. Reminds me a lot of 2011 when back then it was every AM radio talk show that was selling gold.

But we do have the $38T in nat debt projected to be $50T in 4 years by the CBO. And deficits aren’t getting smaller.

I was wondering that in 10 yrs probably what at least 25% of the older boomers will pass on? That means lots of people going OFF social security, medicare, medicaid, VA benefits due to dealth. And the Gen-Xers now starting to hit 60 are a much small generation. Will this do anything to the nat debt? Since most of the deficit is due to medicare, medicaid, ss, VA benefits?

And yet my IAU calls keep printing.

USD is easily the best currency. EUR will always have crises as the monetary uniion isn’t supported by a fiscal union. Now it’s France’s turn to exceed the debt limit. GBP is a problem because of UK budget defecit. CNY is restricted. AUD and CAD are cyclical currencies that are leveraged to growth and commodity prices.

Gold is in a bubble and crypto has no intrinsic value. Plus the big probelm with gold and crypto is their yield is 0. With equities you get dividends and bonds you get coupon payments. Not a big issue when bonds where yielding next to nothing but you can now get decent returns, particularly on long duration treasuries. And US equties are priced to perfection with, I believe, more downside than upside. Plus credit spreads are unusually low making junk bonds unattractive. In my view, this leaves T-Bonds as the most attracive investment opportunity.

That boring 4% return may end up looking amazing compared to 40% losses everywhere else.

USD does not preserve value over time. So it is a currency but not money. This causes the never-ending search for yield, have to keep ahead of dollar debasement. Which is built in to the Fed system and in particular the banking system. Gold is a great form of money, houses now are about the same price as in 1890 when priced in gold. There can be serious volatility in the shorter term but the longer term is the domain of money.

Oil, priced in gold, has also been roughly the same for the last 40+ years.

But wait – comodities themselves are inherently deflationary.

In what way does gold preserve value when its price in dollars dropped 50% from 1980-1985? And after adjusting for inflation it lost 2/3rds of its value in that time period and 4/5th from 1980-2000?

There is literally nothing on earth that can preserve value, because value is a constantly changing concept. Value only comes from what people want it for, and that can (and does) change at any moment.

Gold YTD +56%.

I agree USD is easily the best currency for now, but I don’t think that’s guaranteed to be for hundreds of years in the future, as many people think.

You are correct that with equities you get dividends. That said, the dividend yield for the S&P sucks right now. You can still get some good dividend stocks, but the Mag7 holding up the indices don’t really pay dividends worth speaking of. They either buyback their own shares or they burn the money on AI.

So anyone buying the S&P is not doing it for dividends, but for future capital appreciation (which is not a sure thing given how high the prices are).

I don’t see investing in gold today as any different than investing in TSLA or NVDA today. In all cases, you’re buying them because you think a greater fool will pay you more later. Period.

Currently, you can get an annual yield of about 3% with Ether by “staking” it (i.e making it illiquid to run the network). The actual number varies because it is a fixed amount split among all those staking.

Still a purely speculative thing, though, not an “investment”.

With Wolf showing persistent services inflation that isn’t showing signs of getting down to 2% in any hurry, I don’t know who is buying a 10y at 4% yield. Equity prices are insane, so maybe 1% real gain doesn’t look that bad to the big boys?

Personally I’ve shifted to paying down my 4.1% mortgage as fast as I can. Not seeing yield on bonds/bills/notes, and not really looking to increase my US stock exposure (I’m probably 70%+ today). Might as well get some tax efficiency.

Would love somewhere reasonable to throw money in a 3% inflation environment with even more US govn’t debt to be financed in the next 5 years.

Yes this is exactly where I am regarding where to put new funds to work. It is tough to find anything that isn’t already overpriced or at risk for another mini- or major correction. I guess I will just keep parking in ST CDs, etc.

I think people have an easier time with debasement when as consumers, things trend overall higher every year. At this rate, if inflation were to fall to 2 percent next month, debasement has already occurred in one form. Since the inflation from years past has already pushed up prices permanently. Theres no going back to 2019 prices.

Having said that isn’t this the same “bond market” that had the sell-off in April due to the liberation day tariffs? Should we really give them that much credit?

When certain asset prices shoot up by 50% or 100% in a year, it’s not 3-4% annual inflation that is doing that. Asset prices shooting up by that much… that’s a result of people piling into the debasement trade.

Wolf – you should hire me.

I would be in charge of the ‘More Interesting than Watching Paint Dry Department.’

I like your site. Variety is sometimes a desirable feature.

I’m not sure I understand this comment. Just to be clear, CNBC has a dedicated person assigned to each of: transportation, real estate, the Fed, etc. Wolf, alone, covers almost every area that CNBC covers, and some additional areas that CNBC doesn’t cover (imploding stocks, for instance).

Excellent article

But this time it’s different….

Yes, is is vastly worse this time by orders of magnitude.

Everyone is in the same place. In a stock bubble world with too much cash floating around, even bonds are unreasonably depressed. I don’t want to payoff my 2.75% mortgage. And since I am 70 years old, I don’t see any reason to take too much risk. Precious metals have now joined the bubble.

All that I see as cheap is energy and healthcare. But today I sold my healthcare stocks and harvested the meager tax losses. I have too much energy related holdings as it stands already, but some natural gas etf and stocks are still attractive. But they are risky in a recession if and when that comes to pass.

I purchased some preferred stocks paying 6% or so dividends in my IRA and 401K, but they continue to bleed small losses. I really like some preferred cumulative closed end fund stocks, but the market does not seem to agree with me.

I purchased a basket of highly leveraged mortgage REITs paying 9% or so, but they continue to lose money.

Beats me— but 3.8% to 4% federal government money market rates and very short term treasuries look like the best alternative given my 10% state tax bracket.

Vegan dream in tatters as $8 bn fake meat darling now worthless after brutal Wall Street selloff

The meatless burger company is struggling to pay $800 million in debt. It’s a wild fall for a company that used to be worth $7.8 billion.

Why hasn’t it shut down yet? Why does it keep getting funds to burn?

I know a fair number of vegetarians. The problem is that most of them don’t even like the taste of meat anymore, so they don’t want soy/vegetable based burgers that attempt to taste like meat. They’d rather have an actual veggie burger.

For people who do like the taste of meat and who are not vegetarians, there is no reason to eat these. They’re expensive and unhealthy relative to actual beef/turkey burgers, and people have realized that.

So all you’re left with is the small group of vegetarians who like the taste of meat still. That just isn’t enough of that group to keep this company alive.

I always understand that the target market was meat lovers who would like to eat “a little more healthy”.

Yes, that was the marketing philosophy. The problem is the facts don’t bear it out. They’re loaded in chemicals and saturated fat. I try to eat healthy, but I’d rather eat a grass-fed burger on occasion anyday.

I’m a steak and potatoes guy, but can seriously vouch for black bean burgers. They are extremely good and my go-to when I’m not feeling a fattier burger at Bad Daddy’s. Fake meat is a solution in search of a problem, and doesn’t solve the real reason we produce so much beef at sustainable price – utilization of unfarmable but grazeable land for calories.

The problem is that the USD is massively overvalued because of foreign currency manipulation – something that also causes the trade deficit, and part of why Americans don’t save much.

If other countries stop manipulating USD to promote exports then USD falls 60-80% relative to other currencies.

That is absolutely something you do not want to be involved in! That’s why I own gold.

That being said, what’s happening now is eerily similar to late 1970s and gold trade could reverse. But that’s how investing works. You take risk, and you could lose it all.

Some have a managed float (eg CNY) but they’re the exception. Most major currencies are free floating. Their rate is determined by market forces. Occassionally there is government intervention but it’s relatively rate. There isn’t any scenario where USD falls 60% to 80%. I don’t know why anyone could believe this is a possibility.

The USD is a currency that, eventually, will fall to near zero as all fiat currencies historically do. It may happen in 5 years, 25 years, or 100 years. So, how old are you? When I say near zero, I mean purchasing power, of course. This is why it is worth considering a millennially hard asset like gold and watching its correspondence to currencies; or even to another hard asset like a barrel of oil, essential for modern development for over 150 years (but maybe not as much in the future?). Again, what is your time frame and your age?

The dollar is a currency, and you cannot invest in a currency. Gold is an investment, among many. So your choices are: gold, stocks, bonds, real estate, silver, futures, options, lending to banks via CDs and savings accounts, lending short-term via money market funds, etc. Those are your choices. The “dollar” is not one of them.

Wolf,

It is utterly astonishing to me seeing people claim that ETFs cannot go to 0, and pseudo ones like QQQ cannot drop 50% etc etc. “What are they…on dope?” Did they even go through the financial crisis. Oh wait, right, it can’t happen because the Fed will bail out the markets or whatever they’re called now. Got it😆

It’s all relative, but Wolf is correct regarding the latest dollar trend (Fed’s QT). However, regarding bond “markets” and commodities, I see two things influencing “price”. First, RISK is being repriced globally, second, if America is really going to become a manufacturing powerhouse again, then we will require a lot of commodities and energy (which also requires more commodities, copper, iron, coal, natural gas, uranium, etc. etc.). There are now over 8 billion of us on this rock. Maintaining a decent standard of living requires a lot of energy and commodities. This isn’t opinion or hyperbole, this is math and physics.

You all trade too much. I have been in gold and cash, no interest, dollars for 50 years. Paid 50 dollars and more for 345 dollars for the gold. The no interest Dollars let me buy land suddenly if it is low in price. Are any of these investments going to zero. I do not think so. That is the secret, buy things you believe in and hold forever. Do not buy them to trade them. Do not buy them if they can go to zero. All governments spend too much money and go broke. So mostly every asset you buy will go up if priced in a broke government’s money. The problems start when the broke government knocks on your door and wants you assets. I would not live in NYC today, Florida sound better.

Gold’s risen for some fundamental reasons. 1) a rise in inflation, 2) declining real-rates of interest, 3) a fall in the dollar’s exchange rate…

The CPI for Sept., Oct., and Nov. could still be high, but it’s likely to decelerate afterwards. Thus, we could be at a minor inflection point.

Cleveland FED’s nowcast seems to spike in Sept. with the CPI now coming in @ .38 while short-term money flows, the volume and velocity of money, the proxy for R-gDp, are receding.

I have some gold in my safe. Bought it back in 2021 when it was <$1800/oz. I also have silver purchased at <$22/oz.

It does absolutely nothing for me – zilch, nada. It sits there and collects dust. Occasionally I take it out and look at it, and then put it back to resume collecting dust.

All my other assets have a use: my house is a roof over my head, my car and motorcycle can both transport me places… my gold does absolutely nothing for me.

Sure I could sell it for a big profit… and then I wouldn't have any gold.