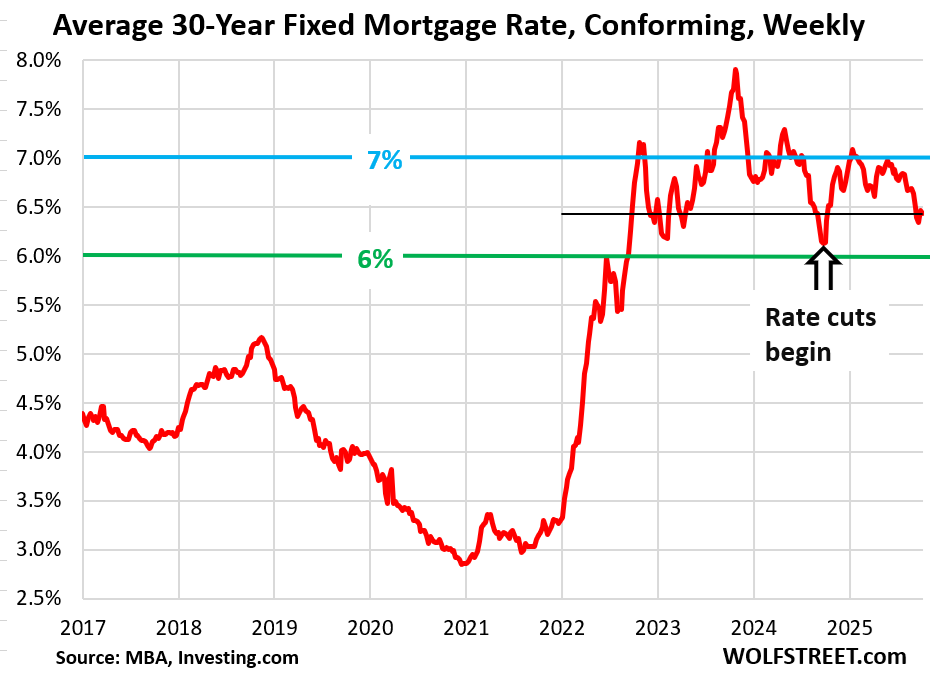

Mortgage rates are still higher than before the rate cuts started over a year ago.

By Wolf Richter for WOLF STREET.

The average weekly mortgage rate for conforming 30-year fixed mortgages edged down to 6.43%, according to the Mortgage Bankers Association today. But that was still higher than two weeks ago and three weeks ago, and quite a bit higher than in September and early October 2024 when it bottomed out at 6.13% just before the Fed started cutting interest rates.

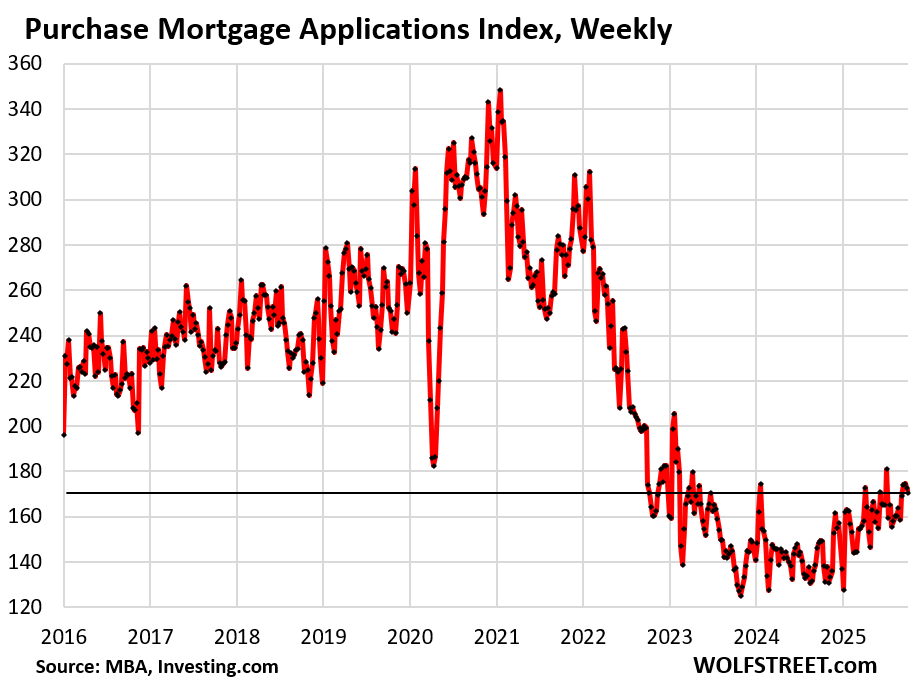

Demand for mortgages to purchase a home, with home prices still way too high, remained abysmally low.

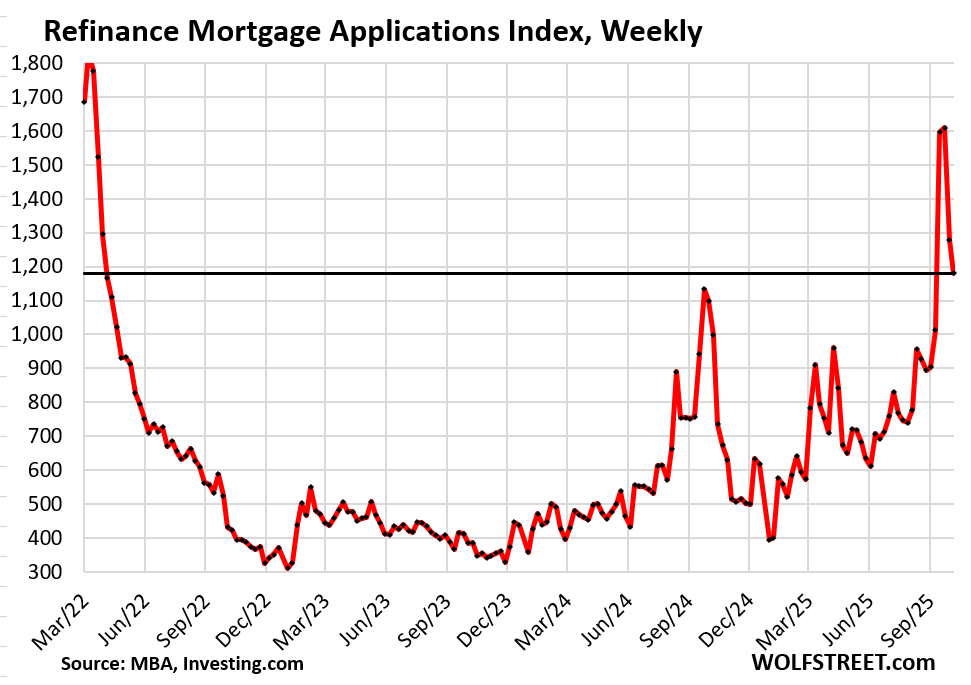

And the September spike in applications to refinance existing mortgages on this minuscule September dip in mortgage rates has unwound.

From mid-September 2024 through early January 2025, mortgage rates jumped by 100 basis points, as the Fed cut its policy rates by 100 basis points despite reaccelerating inflation. A lot of hawkish talk from the Fed since then calmed down the bond market’s inflation fears, and the mortgage market is geared on the bond market, specifically the 10-year Treasury yield, and not the Fed’s short-term policy rates. The somewhat calmer bond market has helped mortgage rates come down.

Aggressive rate cuts by the Fed this fall, as inflation has been re-accelerating, could cause those mortgage rates to jump back up as they had done last year at this time.

The spike in refis that didn’t last. There had been a sudden spike in applications for mortgages to refinance existing mortgages starting in mid-September when mortgage rates dipped just a hair. That spike lasted for two weeks. And when rates inched up again a hair, that spike in demand for refi mortgages settled back down.

The prior spike in demand for refi mortgages occurred a year ago in September 2024, when the MBA’s measure of the average weekly 30-year fixed mortgage rate dropped as low as 6.13%.

Any little dip in mortgage rates brings out new waves of homeowners that pounce to try to refinance a mortgage and cause refi mortgage applications to spike. And when rates rise just a little, that demand fizzles.

Despite those mortgage rates in the 6-7% range, homeowners still want to refinance mortgages for various reasons, and so some refinancings are still happening.

There are up-front fees to be paid by homeowners when they refinance a mortgage – typically 1% of the mortgage balance – and those fees are then added to the loan amount and increase the payment, which reduces the advantage of lower mortgage rates. So homeowners who want to refi a mortgage to lower their payment do a breakeven analysis with online calculators or through brokers or mortgage lenders, to see if it’s even worth it. And when that calculus tilts in their way, they might pounce, creating these brief spikes in refis.

Other homeowners have different reasons to refi, and the points are secondary. Mortgages also count as refinance mortgages when homeowners that no longer have a mortgage do a cash-out mortgage on the home they own (this could be cheaper than a HELOC).

But demand for refi mortgages, even at the top of that spike in September, was still relatively low compared to the years when much lower mortgage rates prevailed.

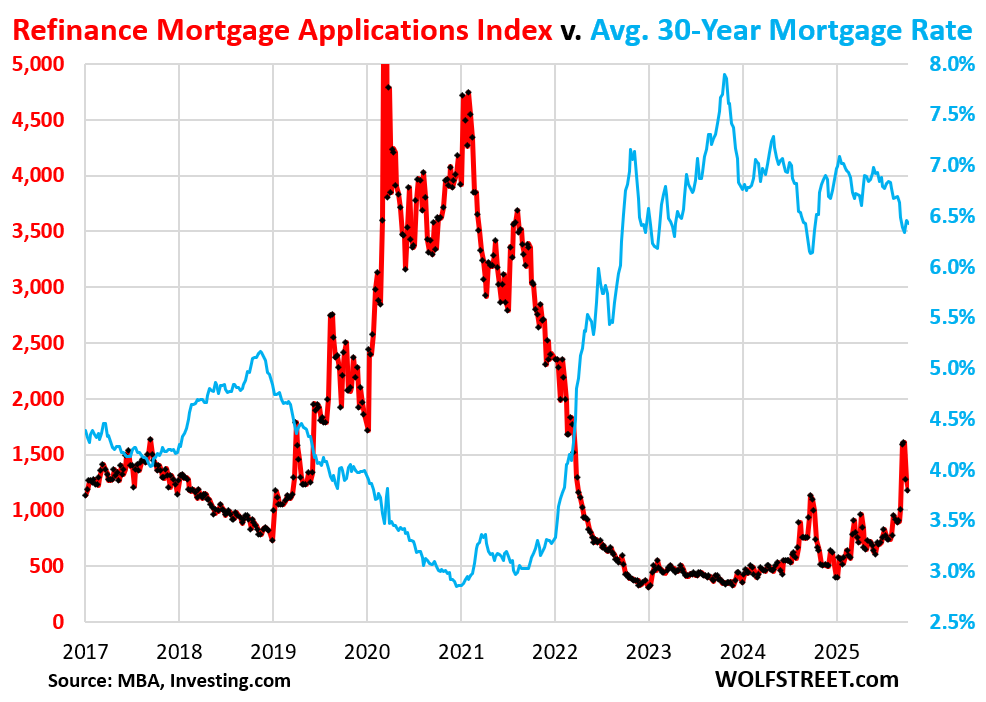

This is the decade-long view of mortgage rates (blue) and refinance mortgage applications. It shows the inverse relationship between mortgage rates and refi applications:

Mortgage applications to purchase a home dipped for the second week in a row and has been essentially unchanged for five weeks. While up from rock-bottom, they remained at dismally low levels, down by 32% from the same week in 2019.

Purchase mortgage applications are a measure of demand for homes that may become actual home sales in the future and are therefore a forward-looking indicator of home sales.

And these low levels of purchase mortgage applications are another sign, among many others, that going forward, demand for homes remains historically low after the price explosion between early 2020 and mid-2022.

In case you missed it: The “Lock-in Effect” and Mortgage Rates: Update on Unwinding a Phenomenon that Wrecked the Housing Market

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

LOL, just date the rate right? That date is starting to turn into a roofie fueled nightmare. Hopefully the up to date RE agents still not selling that BS to their prospective FOMO buyers…

Invest in gold.

Gold is not an investment but just a manically speculative and absurdly overpriced fungible commodity. Watch out below.

Like everyone else, don’t normally reply to your ‘shiny rock’ gospel, but have to point out in passing that if something is a ‘commodity’ it is ‘fungible’ by definition. So yes, an ounce of gold is interchangeable with any other ounce of gold.

Fungible is good.

“Speculative and absurdly overpriced” Gold and South Cal. House both grown 100x since 1950.

You’re an idiot or a banker. Your own words betray you. Yes, all commodities are fungible and any productive business, that actually makes things, knows just how valuable fungible commodities are, unlike fiat currencies. One BIG DIFFERENCE with gold however, is that is that the world, especially the world’s central banks, have also agreed that this particular commodity is also a “tier one” asset and UNIVERSALLY accept collateral. Considering how much DEBT the world governments have issued, it makes such collateral even more valuable. So thanks for confirming gold is going much higher. Unless, of course you really believe there will be a debt jubilee…

In that case, don’t be an ass, just share your “insight” with us. LOL.

Neither the Fed, not the ECB, nor the BOJ, nor the BOE have been buying any gold.

The central banks that have been buying gold are smaller central banks, and they didn’t buy gold with their own currency, but with foreign currency that they get from their trade surpluses.

“they didn’t buy gold with their own currency, but with foreign currency that they get from their trade surpluses”

EXACTLY, when they use to buy OUR treasuries. Perfect example of risk being repriced. PBoC is buying, so has the Russian central bank. Producers are opting to preserve wealth with gold over government bonds. This will make funding governments in debtor nations much harder. Not a good thing Wolf, if you are in a debtor nation.

SoCalBeach Dude –

“Watch out below.”

Pretty sure you said this around $1500 gold.

Pete,have a lot of “in hand “metals,that said,be doing for 10 years or so and the recent seemingly dramatic rises in gold have me concerned.

I guess me investments in brass/lead also good,hope I don’t need it all!

You can’t live inside gold.

Don’t have to pay yearly taxes, do yard work, get insurance and replace roof’s on my gold. And its mobile.

Exactly.

Housing is an asset that costs you money (but provides other benefits, such as a place to store your gold).

But it sure helps..

Fun fact: the ratio of the S&P500 to hold had been constant since 2015. In other words, gold and the stock market have had the same increase in price for a decade. Is that the behavior of a hedge or an asset bubble?

That “fact” is, an error (assuming hold= gold).

The GOLD:SPX ratio has been changing, since the S&P was created.

Since 2015, this ratio has ranged from about 0.375-0.7.

The importance of this ratio is to indicate the “direction” of money flow. Of course, the S&P is “not fungible,” as the index of today is different than other eras.

Gold has been considered money, and a store of value since forever. The economies of the world have risen and fallen, since then: often priced in gold.

Not sure why mortgage finance operations are still offering 30-year fixed mortgages in the US in the first place. If rates rise, the lender is locked in a below-market loan and suffers a huge loss (largely guaranteed by taxpayers). If rates fall, the borrower refinances, so there is no benefit to the lender. It’s the most lopsided game around, and unfortunately the largest private loan bucket in the economy.

Crazy. We should have learned something about the bailout risks in this area.

If you were going to purchase or refinance today would you do a 30 or 15 year loan.

Couldn’t the exact same thing be said about bonds? Yet there are robust bond markets.

” If rates rise, the lender is locked in a below-market loan and suffers a huge loss….”

Some banks discovered this about Treasuries a couple of years ago. They aren’t banks anymore. The kerfuffle was covered in detail on this forum.

“If rates fall, the borrower refinances, so there is no benefit to the lender.”

Just like a callable bond. I bumbled into this while dabbling in agencies through a brokerage account. The stakes were much lower than for the above-mentioned banks.

A long time ago thought the average house ownership time was 7 years.

So one thing I have to correct you on is that most mortgage originators are not holding the mortgages they originate on their own balance sheets, but selling them to the GSEs (Freddie, Fannie, etc.). They get paid a spread to originate loans, and it’s a volume game for them.

Once the GSEs buy them, they pool them into securitizations.

What you are asking is why investors are willing to buy bonds backed by those 30-year mortgages.

The answer is simple. They get paid a spread over the 10 year treasury, so they’re getting even more than they would with a 30 year treasury. So by buying them, they’re banking on rates not dropping THAT much.

I’m not saying it’s smart, but that’s probably what they’re thinking.

I mean, people are loaning to Uncle Sam for 10 years at 4.1%. I think that’s a terrible deal but clearly others disagree.

Yes, investors willing to loan money long-term to the U.S. when we’ve clearly shown ourselves to be irresponsible is enabling that irresponsibility.

If the loan is held to term, the lender receives what was contractually agreed to in terms of principle and interest. There is no loss (except in the case of inflation).

However, there can be an opportunity cost as you note.

Lenders also have the option of selling loans. We have seen where than lead as well.

Looking down the road just a couple of years: If AI (formerly called “computer or machine learning”) does actually cause “millions of jobs” to be lost AND if mortgage rates stay high and the housing market sinks or maybe collapses, then we have a catastropie on hand. Not enough people working and earning money; more government meddling in the welfare market and assistance and the dollar spinning out of control. Plus, what if AI is a bust and the ROI does not work for those funding these outrageously high amounts of money that the robber-barons are raising for their AI schemes? Another whammy! What does work historically in times like these when potentially there is runaway inflation is investments in those items that monetize; real estate, stocks of companies that actually earn money, and to some degree precious metals that can be bartered. Silver for everyday purchases; not gold. Gold for buying a home would work or for a car however; not for the small stuff. I could go on and on and half the people in this country with disagree with my take. Get debt free; have reserves; and foodstuffs; and water. Fill up your pool. We are in for an interesting ride.

“Looking down the road just a couple of years: If AI (formerly called “computer or machine learning”) does actually cause “millions of jobs”

Anything is possible and there’s also some probability there but wouldn’t put that as a high if what they consider as AI is still based on LLM. There’s already been documented case of companies jumping on AI to replace their workforce and now have to backtrack or scale back.

and I truly hope we don’t need to rely on AI to take over in order for price to have major crash or correction..

AI is only as good as the person writing the prompt and the person making the judgement call as to whether and where the output is useful.

Which is to say, that it’s a tool that will help high cognitive ability people rapidly accelerate. It will also help accelerate fools and lazy people out the door because they will just create slop.

Anyone banking on massive job replacement with AI has been drinking the Sam Altman hallucinogenic.

Correct. In my “real” job I have used machine learning a lot. If you put very specific guard rails on it, such as telling it specifically what math or algorithm you want it to apply AND you restrict the database it is using to a scientific one, where the data is actually real observations (photon absorption data, molecular structures etc.), then it becomes a very powerful tool. However, AI does indeed have a built in need to please the user, it will lie. Moreover, if you simply allow AI to access ALL digital data on the internet (99.9% of which is complete bullshit) then you get complete bullshit on steroids.

Sometimes a big change is kicked off by an unexpected event. WFH became more prevalent due to COVID. There is a lot of white collar jobs that can be done by software. AI increases programmer efficiency so they can write that software.

American bussiness have too much overhead. AI will get the blame for job losses but it has been a long time coming.

I don’t know where AI will ultimately lead.

I do know that the standard technical innovation curve follows a pattern of early adopters and failures until a technology eventually becomes a so called commodity – both on the supplier and consumer sides.

CACTI,

Previous metals will be interesting as BRICS is exploring a precious metals exchange. Obviously not a new concept but a significant new player.

There seems to be a persistent group of people actively rooting for the collapse of civilization in the belief that they and their big pile of stuff can survive on their own. I wonder if they ever consider if the downfall ever comes, their big pile of stuff would make them a big fat target for all the have-nots. How large a wave of desperate marauders are you prepared to repel? My philosophy is the more you believe you can survive a downfall, the less you will work to prevent it. And vice versa.

Ross,

I already know come a zombie apocalypse I am one of the first to go. I have seen the last of us and not a time I want to live through.

Ross,feel most folks like meself who are “paranoid preppers”hope to a large degree our preps were a waste/that said,will still use our goods/skills/ect. packed away.

I have a mixed bag investment wise including finances and also a lot of dommsday investments,,that said,hope they are never desperately needed but will be used even in hopefully peaceful/tranquil times.

What are considered doomsday investments – are these guns and ammunition?

I appreciate your comment, thanks.

Once the home becomes the atm machine….Its over.

Have a fantastic day all !

You mean a speculative asset.

I kinda agree with you when taken to extremes – as happened in the lat decades.

Fair to say mortgage refinance activity is back to a more “normal” level, judging by the index before the pandemic?

And we’re now waiting for the purchase mortgage index to climb back to pre-pandemic levels?

6-7% mortgages becoming more mentally normal by the day, like $15 burritos.

Explains while my online bank is still offering 4.2% savings accounts. Treasuries are still a better play until difference is .4% as that is the appropriate state tax implications for me and nice to Newsom have more budget problems. California legislature were drunken soldiers at one point too. One banner year with capital gains revenue doesn’t mean you should tons of long term spending bills.

I love longterm inverse relationships and cyclical ratio stuff, helps me spot regime trend shifts. Seems like we’re in an upside down chaotic phase.

The stampede for the exits will be historical when the illusions fade, propaganda no longer works, people question the state farm, and they are and the kleptocrats take the stolen loot to Switzerland and the desert mirages…50 years of tv brainwave spoon fed nonsense…the sleepers are awakening…go create another 9 trillion funny Moon eye…global sell outs…money is loyal to money, not country….

The sleepers are awakening. I have to laugh. No, they are not awakening. Clueless as they ever were.

It’s does seem most never question how the system works, obviously folks like wolf are real educators but fraud, propaganda and big lie theory is so obvious, but it’s their programmed brains and ignorance doesn’t allow them to wake up…

A little incoherent, and I don’t think anyone has had an intelligent “awakening”. Look around, the average person is an idiot, and half of them are dumber than that.

I think we can all simply agree that capital and talent go where they are respected and RISK is being repriced on a global scale.

Hedge accordingly.

1:04 PM 10/8/2025

Dow 46,601.78 -1.20 -0.00%

S&P 500 6,753.72 +39.13 0.58%

Nasdaq 23,043.38 +255.02 1.12%

VIX 16.30 -0.94 -5.45%

Gold 4,063.80 +59.40 1.48%

Oil 62.38 +0.65 1.05%

Please include silver in your list.

We just bought our first house after 12 years of renting and were frankly happy with our rate and price. Houses are finally somewhat affordable for lower-middle-class folks like us, even in the sizzling North Texas market.

Poor ,congrats and hope the family/home do well,nice to hear positive news!

Wolf, i feel like it’s been a while since you checked in on our Drunken Sailors. How are they doing?

Consumer spending has been growing at about 2.5% adjusted for inflation. Savings rate over 4%. Doing fine.

Last data on our drunken sailors was in the GDP revision on Sep 25: consumer spending +2.5% adjusted for inflation in Q2. July and August have been similar, per preliminary consumer spending data.

https://wolfstreet.com/2025/09/25/what-slowdown-q2-gdp-growth-revised-up-to-the-hot-zone-of-3-8-on-stronger-consumer-spending-private-fixed-investment/

Would be interesting to see how delayed home buying for folks under 40 influences this (and other equity bubbles).

If you’re not locking liquidity in a down payment, what else are you doing with it?

Rents, while increasing, still have a gap vs buying in many markets.

It’s interesting to see how even a small dip in mortgage rates can lead to a spike in refinances. However, the ongoing demand for home purchases still seems to be struggling. I wonder what factors are contributing to this deep freeze in the market?

I think Wolf has already presented some good analysis vis your question – tailored to specific geographic/metro markets.

Yes it is interesting, looks like a lot of people are on the sidelines waiting for a dip in the interest rate in order to move forward with a refinance. But until the most recent drop in refinance activity, it had been creeping up this year along with the purchase index. We shall see if we are truly past the bottom for both of these indices.

If this government shutdown continues for another two weeks, many here in the Swamp will be going without a paycheck for the first time in their lives. They are already getting desperate. They haven’t the foggiest idea what it’s like to work in the private sector where you have to actually work to earn the money you are being paid. Already, you hear these whining dogs resorting to calling in sick in mass to shut down essential services like Air Traffic Comptrollers. Look for major disruptions in basic essential services sooner rather than later. Look for the administration to order these workers back to work or face mass firings, just like Reagan did back in 1981 with the Air Traffic Comptrollers.

The 81 situation was completely different. The controllers chose to walk out. It was a strike over wages and conditions. They were being paid but wanted more. In the present situation they aren’t being paid. Blame which ever party you like for the halt to their pay, but not them.

Nick..1981 was a strike, A walkout. Yes they were being paid BUT they were fired by Reagan if they did not return to work. Today, they are not striking, there is a halt to pay, but they will receive back pay for the period of the shutdown. Getting paid changes the narrative.

Very True. But what does their contract stipulate?

One factor in the current FOMO stock bubble is that a very large fraction of contributions to 401ks is on autopilot into the Mag7 via ETFs.

As long as the inflow exceeds the outflow due to retirees and unemployed needing cash to pay essential living expenses the market must rise.

If and when the outflows exceed the inflows, it must fall, and the lower share prices go, the more shares must be sold to get the same amount of cash, starting a vicious spiral down.

With “AI” throwing some well paid people out on the street, and the government shutdown and firings on top of that, might the inflow/outflow balance reverse?

At least 50-75% of my coworkers in the private sector provide no value, or are so bad at their jobs they provide negative value.

Attacking public workers is mouth breather behavior.

A teacher at least has to show up and provide a service to 30 people. A DMV desk attendants butt is in that chair the vast majority of the day.

My HR team is off at yoga class and the coffee shop half the day.

President Garfield and President Tyler both fired 50% of the Federal workforce when they took office. Same with Andrew Jackson. So what Trump is doing is nothing new.

It adds up if you look at the big view! Over forty and you need a mortgage or go nuts if you will miss a paycheck or two! Nothing more tman wage slaves. Very sad for them.

And gold and silver are so useless, as it just sits there gaining in value, unless you know what you are doing and buy and sell.

FDR outlawed private holding of gold.

All it takes is one executive order to do it again, if the prez feels it’s getting in the way of his policies.

Au is a human right, the same as Cu (Bronze) and oxygen etc.

You forgot to mention, it did not work very well. The proof is the vast numbers of pre 33 gold coins on the market today, that sell for little more than spot.

How many today have gold and respect the goverment enough to follow such a rule.

Gold is a put option against the US dollar with no explicit strike price or expiration.

If your contract “expires worthless” hopefully the rest of your portfolio has done well.

If you need to exercise your contract… you’ll sure be glad you had it.

“Demand for Mortgages to Purchase Homes Still in Deepfreeze.”

So, the wooly mammoth is dead, frozen in the arctic ice, and some people want it revived. Sorry – Woolly is gone…no reviving to be had…may as well fire up the BBQ grill and have some

WM Burgers! 🍔 We’ll remember you fondly, Woolly, just as we will with the housing market.