Its holdings of commercial paper & corporate bonds are nearly gone. The BOJ is cleaning up its balance sheet.

By Wolf Richter for WOLF STREET.

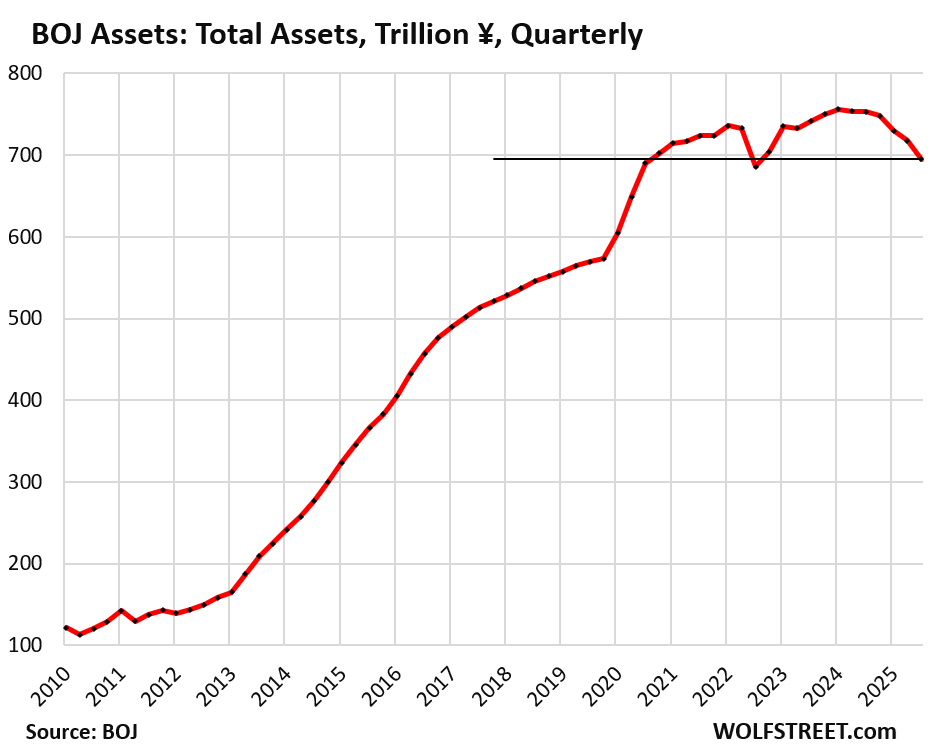

The Bank of Japan further accelerated its quantitative tightening: Total assets on its balance sheet fell by ¥22.3 trillion ($148 billion) in the quarter through September, the biggest quarter-over-quarter decline since QT started in early 2024.

Since the peak in the quarter through March 2024, total assets have fallen by ¥61.2 trillion ($407 billion), or by 8.1%, to ¥695 trillion ($4.62 trillion), back to where they’d first been at the end of 2020, according to the BOJ’s balance sheet.

The BOJ fiscal year ends March 31. For the sake of simplicity, all quarters here are expressed calendar quarters (quarter ended September 30 = Q3).

Back in the QE days, the BOJ conducted QE in several forms:

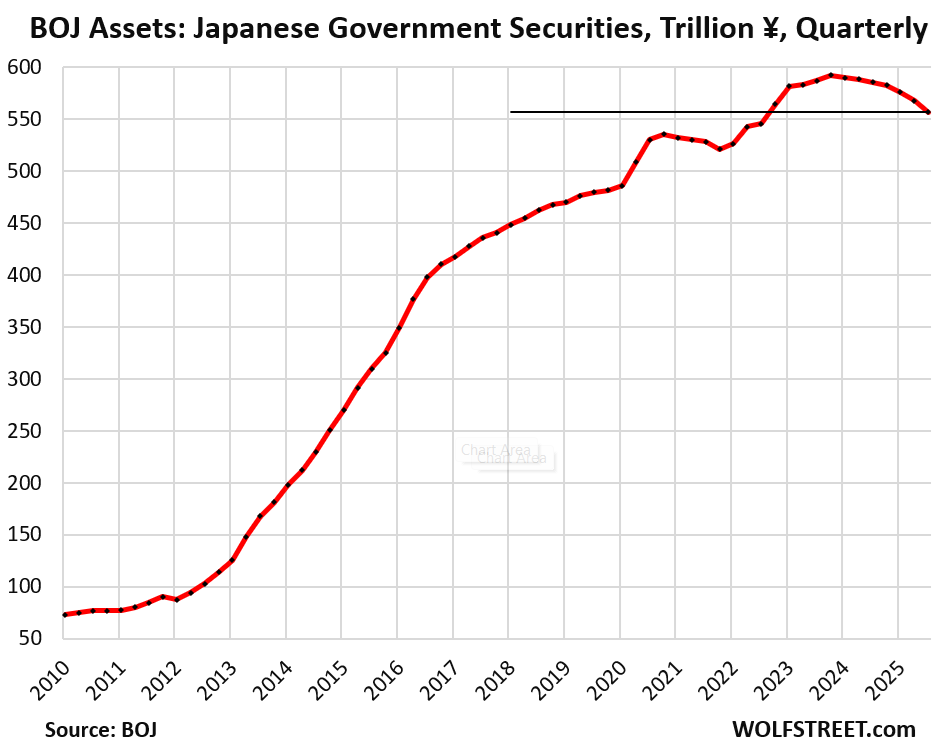

- Japanese government securities (now 80% of total assets).

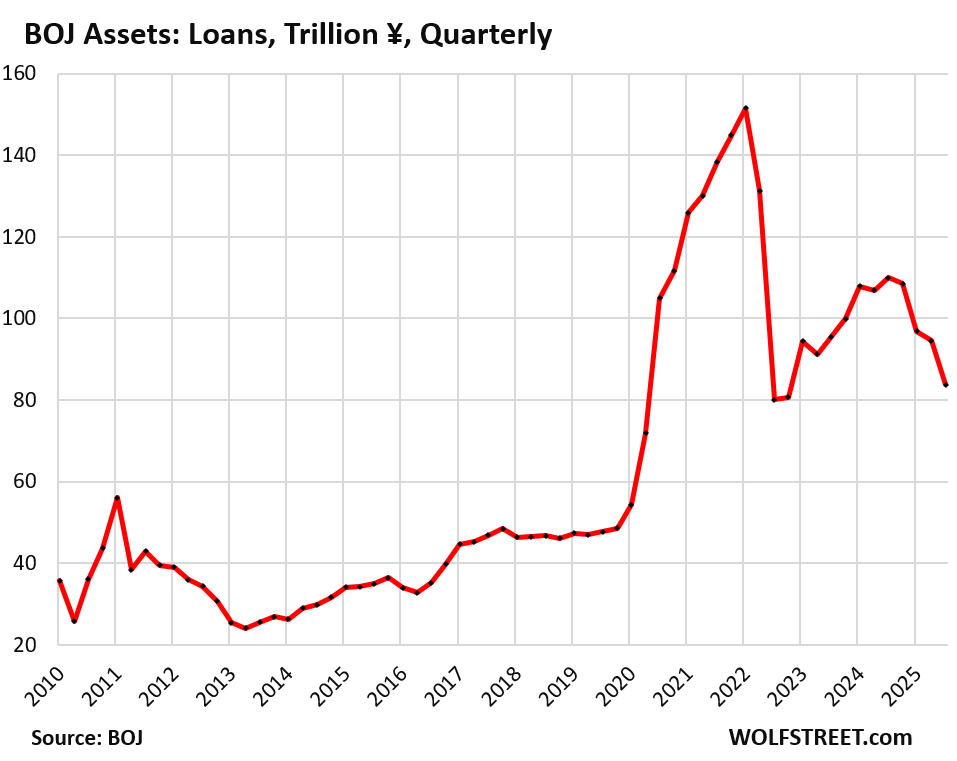

- Loans (now 11% of total assets).

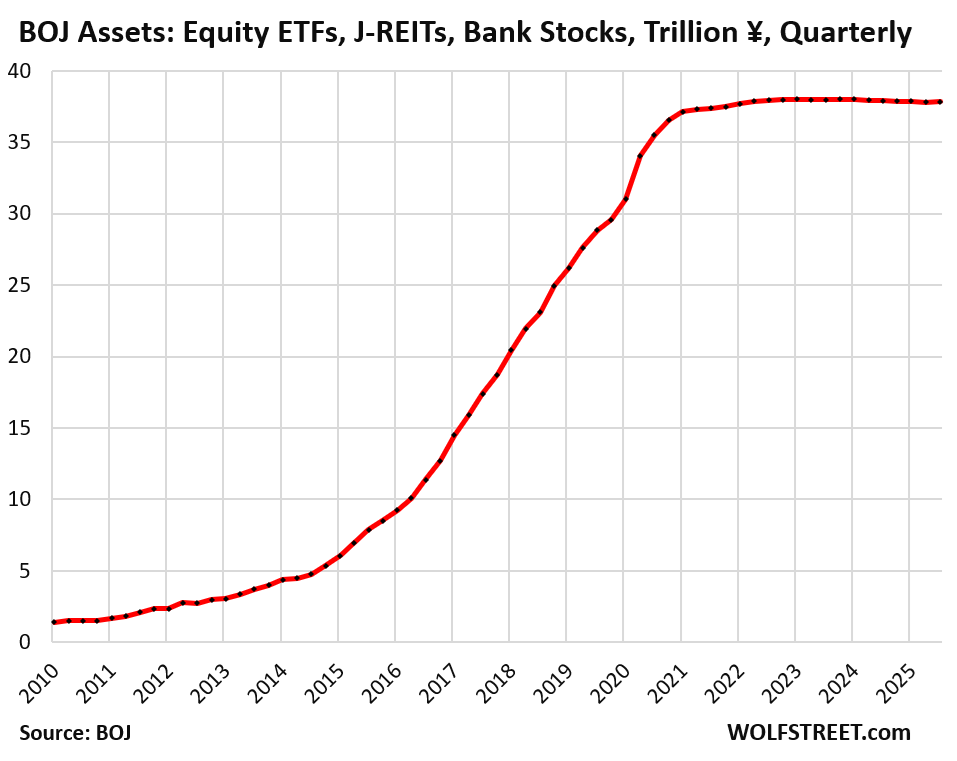

- Stock-market traded equity ETFs and Japanese REITS (now 5% of total assets)

- Commercial paper and corporate bonds (down to 0.6% of total assets).

- Bank stocks purchased in 2000 and 2009 (sold the last ones in Q3).

Japanese government securities declined by ¥10.8 trillion (-$71.5 billion) in Q3, to ¥567 trillion ($3.66 trillion), the lowest since Q4 2022, down by ¥35.5 trillion (-6.0%) from the peak in Q4 2023.

Nearly all of them are longer-term Japanese Government Bonds (JGBs); its holdings of short-term Japanese Government Treasury Bills were unchanged at just ¥1.7 trillion ($12 billion).

The acceleration of QT, in terms of the quarter-over-quarter declines of its holdings of Japanese government securities:

- Q3 2025: -¥10.8 trillion

- Q2 2025: -¥8.4 trillion

- Q1 2025: -¥6.4 trillion

- Q4 2024: -¥3.1 trillion

- Q3 2024: -¥3.0 trillion

- Q2 2024: -¥1.2 trillion

- Q1 2024: -¥2.6 trillion

- Q4 2023: end of QE

The BOJ’s holdings of Japanese government securities move in three-month cycles due to the timing of when long-term bonds mature and when they’re replaced with newly issued bonds of the same type. The BOJ also makes quarterly data available and refers to quarterly data in its balance sheet discussions, which iron out the three-month cycles.

Loans declined by ¥10.8 trillion in Q3 from Q2, and by ¥26.1 trillion year-over-year, to ¥83.8 trillion ($555 billion).

Since the peak in Q1 2022, the outstanding balance has fallen by ¥67.7 trillion, or by 45%.

These loans now account for 11% of the BOJ’s total assets. The BOJ provided loans to banks and other entities under several programs, including the pandemic-era loans that caused the total amount of loans outstanding to more than triple in two years:

BOJ’s equity ETFs, Japanese J-REITs, and bank stocks.

Equity ETFs, Japanese REITs, and bank stocks don’t mature, and therefore the BOJ can’t get rid of them by letting them mature without replacement, unlike Japanese government securities, commercial paper, and corporate bonds. To get rid of its equity ETFs, Japanese REITs, and bank stocks, the BOJ has to sell them outright.

The BOJ is preparing to sell its ETFs and Japanese REITs, it said at its September meeting. It will start selling them at an initial pace that is very slow: equity ETFs at a pace of ¥330 billion per year ($2.2 billion) and Japanese REITs at a pace of ¥5 billion per year ($33 million).

It said that it could review the pace of those sales at future policy meetings. It said the sales would start when the operational preparations are completed.

The BOJ carries them at acquisition cost and didn’t write them up as market values rose since it started buying them in 2012. It stopped buying in Q4 2023 when they’d reached ¥37.8 trillion ($250 billion) at acquisition cost.

Equity ETFs and J-REITs only account for 5.0% of the BOJ’s total assets. They were always only a small part of the BOJ’s QE operations, but the hype around those purchases in the US QE-promoting financial media was enormous.

The BOJ sold off its last bank stocks in Q3. It had purchased them in the early 2000s and then again in 2009. The purchases of bank stocks ceased in 2010. In 2016, the BOJ started selling them and said at the time that sales would be completed by March 2026. As of the end of September, the last of the bank stocks were gone. This process can be a guideline for how the BOJ will sell its ETFs and J-REITs.

The BOJ’s total stock-market-traded assets combined – bank stocks, equity ETFs, and J-REITs – have declined since the peak in Q4 2023 at a microscopic pace, totaling 0.9%, due to the sales of the bank stocks. The decline is so small it gets lost in rounding.

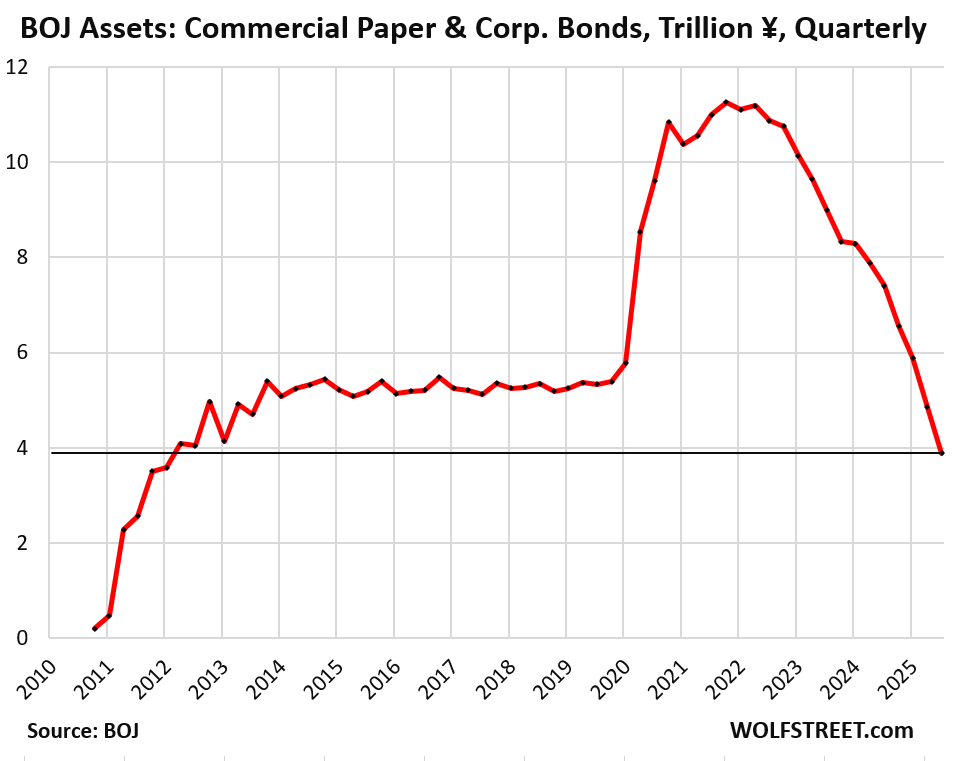

Commercial paper and corporate bonds fell by ¥1.0 trillion in Q3 to just ¥3.9 trillion ($26 billion), the lowest since 2012.

Since the peak in Q4 2021, they have plunged by 57%. The BOJ stopped buying commercial paper and corporate bonds in early 2022, and its holdings have been running off the balance sheet as they mature.

They were never a significant part of the BOJ’s QE operations. At their peak in Q4 2021, they accounted for only 2.2% of the BOJ’s total assets, and their share is now down to just 0.6%.

In case you missed it: Fed Balance Sheet QT: -$15 Billion in September, -$2.38 Trillion from Peak, to $6.59 Trillion.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What have they done with the BoJ’s Gold reserves??? (if any)

Why would such a trivial little asset class like gold matter at all?

The BOJ lists ¥441 billion of gold at cost on its balance sheet (about $2.9 billion). It has been unchanged since 2000.

According to World Gold Council, the BOJ has 846 tonnes of gold. So that’s about $109 billion at today’s price.

But now a female PM? There goes the country!

To be serious, both the UK and Germany have had good female leaders: Thatcher and Merkel.

I know a lot of lefty Brits didn’t like Thatcher but they forget the basket case she took over. Example: incredibly, the press unions had negotiated a ban on the intro of modern tech into printing newspapers. They were still melting hot metal being cast into letters on Linotype machines. After a page had been assembled in a box, a proof was taken. One man would roll ink over the letters, another would place a sheet of paper, a third would press the sheet. None could do another’s job: that would cause a strike.

Similar conditions in auto plants: one important plant only had two weeks of uninterrupted production in a year. Meanwhile, in 1974, W Germany, VW had its first strike. It lasted for one day.

Both women were scientists, Thatcher worked with X ray diffraction and did research for 3M, before becoming a lawyer, before becoming a politician. Merkel did nuclear physics as applied in reactors.

Let’s hope a female PM helps other women to breakthrough Japan’s very thick ‘Glass Ceiling’ in its business world.

Looks like the equity sales could continue for as long as the market keeps going up. If the sales aren’t big enough they are just selling the annual profits

“If the sales aren’t big enough they are just selling the annual profits”

No, by definition, because the amounts are at their acquisition costs at which they carry the ETFs on their balance sheet. They never write them up to market.

So selling ¥330 billion per year means ¥330 billion at their acquisition costs. The actual sales proceeds could be far higher, depending on when they bought those particular ETFs that they sell; for the early purchases, the sales proceeds can be four times their acquisition costs. So actual sales would be far higher. But their balance sheet would drop by the amount of the acquisition cost.

Also note how they started out slowly with their JGB reductions and then sped up. There is a table in this article with quarterly JGB roll-off amounts so you can see the acceleration.

Start out slowly, then speed up. That’s how they do it. But even after accelerating the pace, they will still take decades to sell those ETFs, just like they took 10 years to sell their much smaller position in bank stocks (which was tricker because those were the stocks of individual banks).

Wolf -really appreciate your periodic scrutiny of Japan, knowing that you’ve indicated in the past that it’s not one of your more-popular arenas…

may we all find a better day.

thanks. Yes, I’d be out of business if I did a lot of it. I’ll post a quarterly ECB article on Wednesday, same thing there. This stuff about the big central banks is really important, yet few people read them. However, my monthly Fed balance sheet articles are big. It’s like there’s an army of people out there just waiting for it, and if I skip it one month, my inbox blows up with people asking where it is.

Initially I was very interested when the BOJ said it would sell its index ETF and REIT holdings. Then I read the fine print: it will likely take more than 100 years! Maybe they don’t want to scrare investors and the actually rate of selling will be higher than they indicated.

Like I said in the article, this is the initial pace. Look at the initial pace of the JGB roll-off in the table in the article. It started out in Q1 2024 at ¥2.6 trillion. And then it accelerated from there every quarter. In Q3 2025, it accelerated to ¥10.8 trillion. That’s how the BOJ works. People like you also laughed at the JGB roll-off in Q1 2024. And after 7 quarters of acceleration later, the BOJ’s QT is faster than the Fed’s.

Are there any other countries accelerating QT?

Good question. Yes. The ECB has further accelerated its bond QT this year. During QE, it had purchased all kinds of bonds, including the sovereign bonds of its member states, corporate bonds, asset backed securities, mortgage bonds, etc. a huge pile of bonds. When QT started, it put a cap on the amount of the roll-off, at first at a fairly low level on one of its portfolios and no roll-off at its other portfolio, and then it raised the cap on the first and started the roll-off on the second, and this year it removed the last cap from the bond roll-off. So whatever matures in both portfolios comes off its balance sheet. The amounts of the bond-roll-off are now quite substantial.

Article coming with the latest figures, including the mark-to-market of its gold holdings, in less than 24 hours.

Merkel was a terrible leader, particularlyduringthe last half of her yearsin power. Her immigration and energy policies are why Germany has the economic problems it is currently facing. Plus, she relied on Russian gas while claiming Russia was a threat, and kept defense spending at about 1.2% of GDP during most of her years in power. The chickens are coming home to roost, and as is often the case, it takes years, sometimes a decade or more, to see just how bad policies really were.

AI Overview

Before the Ukraine war, numerous countries bought Russian oil and gas, including all EU member states, which imported significant amounts of Russian oil and pipeline gas.

So she had company in the EU,,,everyone.

Yes, cheap Russian natural gas has been a huge factor in Germany and other countries, and all German politicians had to pray at the altar of cheap natural gas from Russia.

When I was a kid, living in Germany in the 1950s and 1960s, we had coal gas, produced at the local gasworks from coal. It was toxic and expensive. We used it in the kitchen stove and oven. We also had a big coal-fired boiler in the kitchen that heated the hot water that heated the entire apartment. We had a coal gas fired tankless water heater in the bathroom. Then during the Cold War, Germany helped fund the first natural gas pipeline from the USSR to Germany, and it brought about huge changes, adios household coal and coal gas. It gave Germany access to cheap clean fuel. Cheap clean fuel is addictive.