A bigger rise in March got more than wiped out by a drop in April. That’s how it goes with zigzagging month-to-month data.

By Wolf Richter for WOLF STREET.

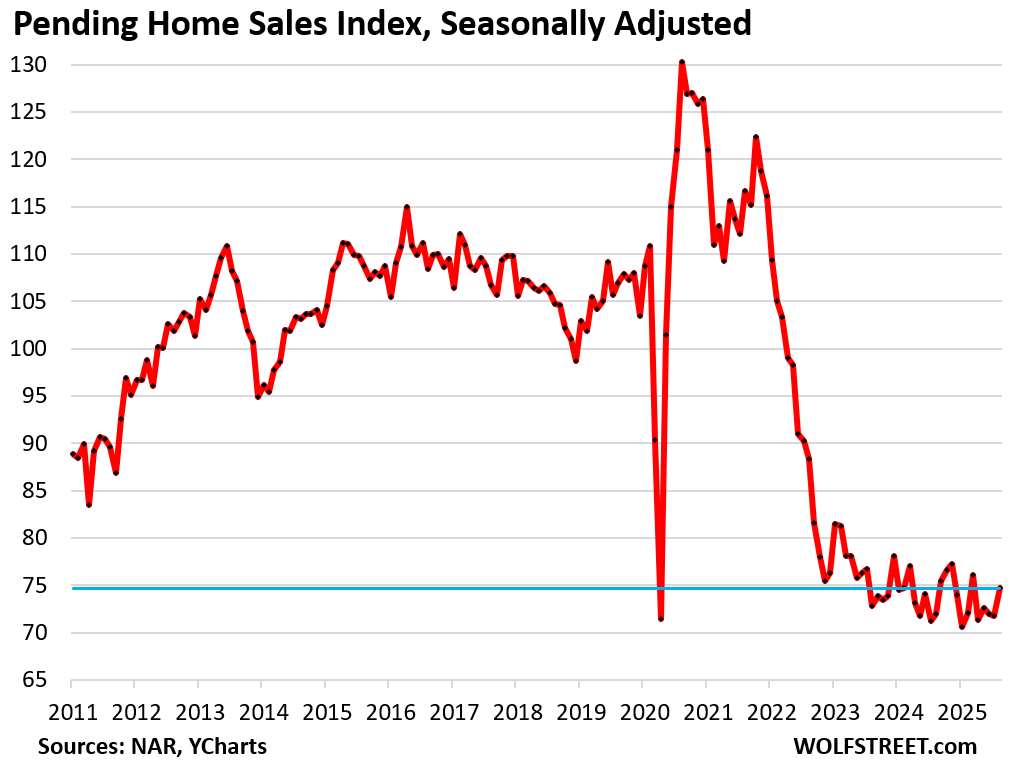

There was a lot of housing-promo hoopla in the media this morning about that 4.0% month-to-month increase in pending sales of existing homes in August, sign of a sudden burst of demand due to lower mortgage rates, or whatever, written by goofballs or AI that never look at a chart.

That 4.0% month-to-month seasonally adjusted increase in the Pending Homes Sales Index by the National Association of Realtors today was off near-record low in the prior month, and was still down by 30.1% from August 2019 and by 42.7% from August 2020.

And the index was below March 2025, when there was a bigger widely ballyhooed surge in demand, or whatever, that was then more than wiped out by the sharp decline in April. That’s how it goes with zigzagging month-to-month data (historic data via YCharts):

Pending home sales compared to the Augusts in prior years:

- 2024: +3.8%

- 2023: +2.6%

- 2022: -15.4%

- 2021: -35.9%

- 2020: -42.7%

- 2019: -30.1%.

Pending sales are based on contract signings and track deals that haven’t closed yet and could still get canceled because buyers cannot afford homeowner’s insurance, or cannot sell their own home, or for other reasons. Signed contracts that then get cancelled are included in the pending sales here, but are not included in closed sales reported later.

And cancellations of signed deals are running high. Redfin reported that in July, 15.3% of all pending sales fell through, the highest rate for any July in Redfin’s data on cancellations going back to 2017.

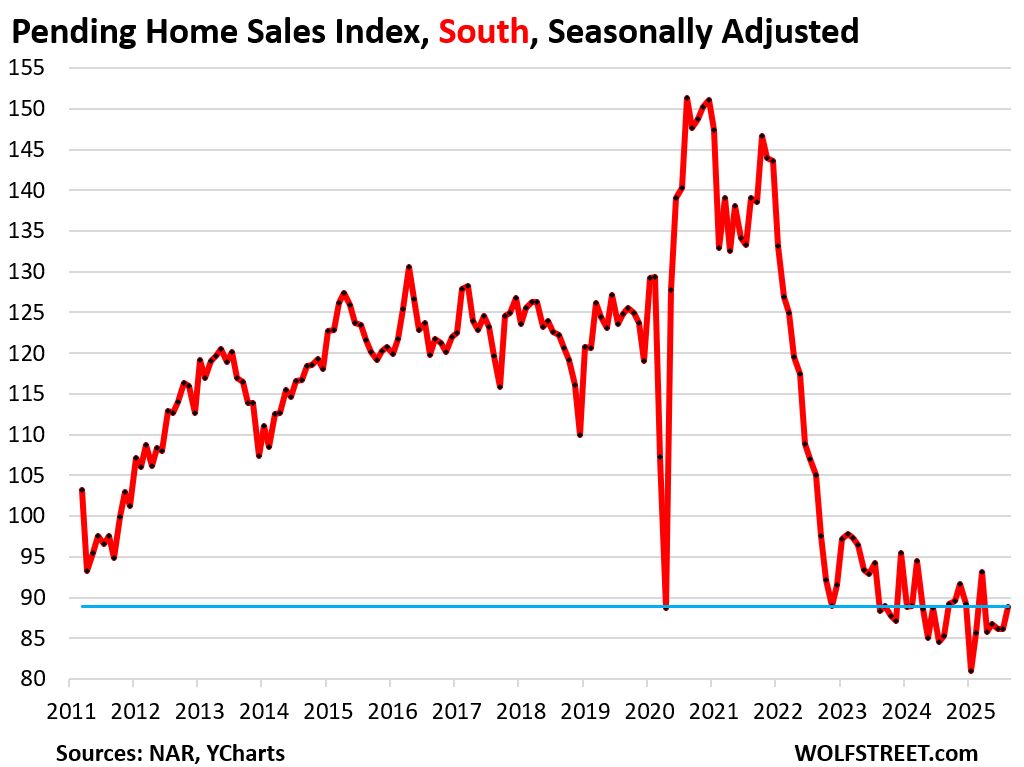

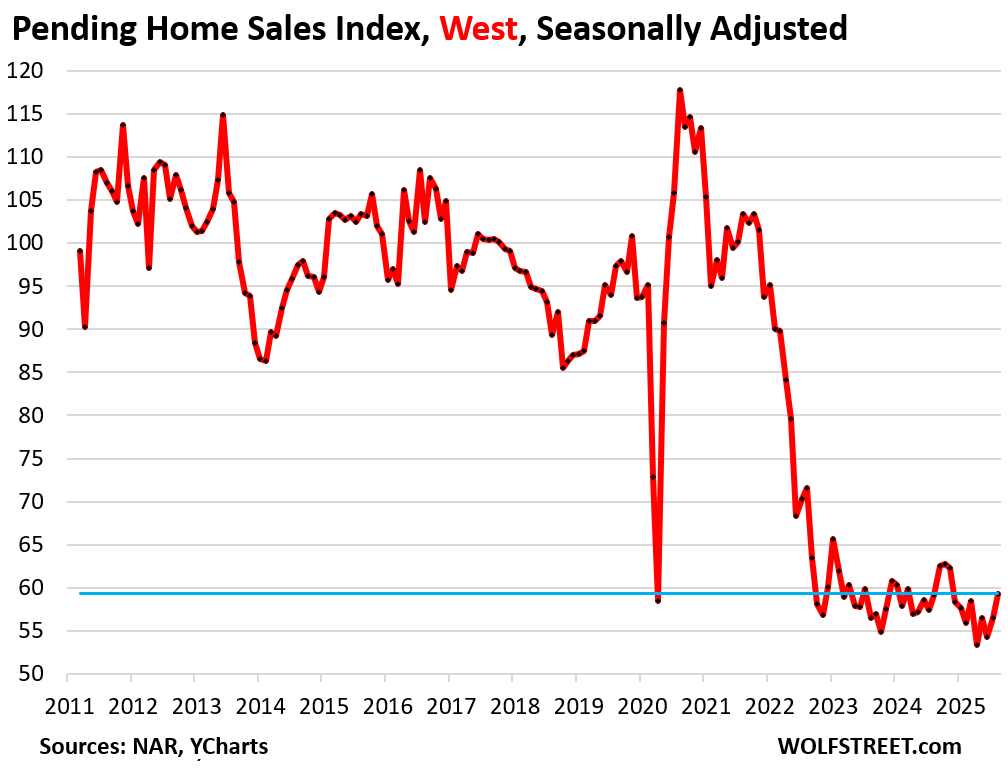

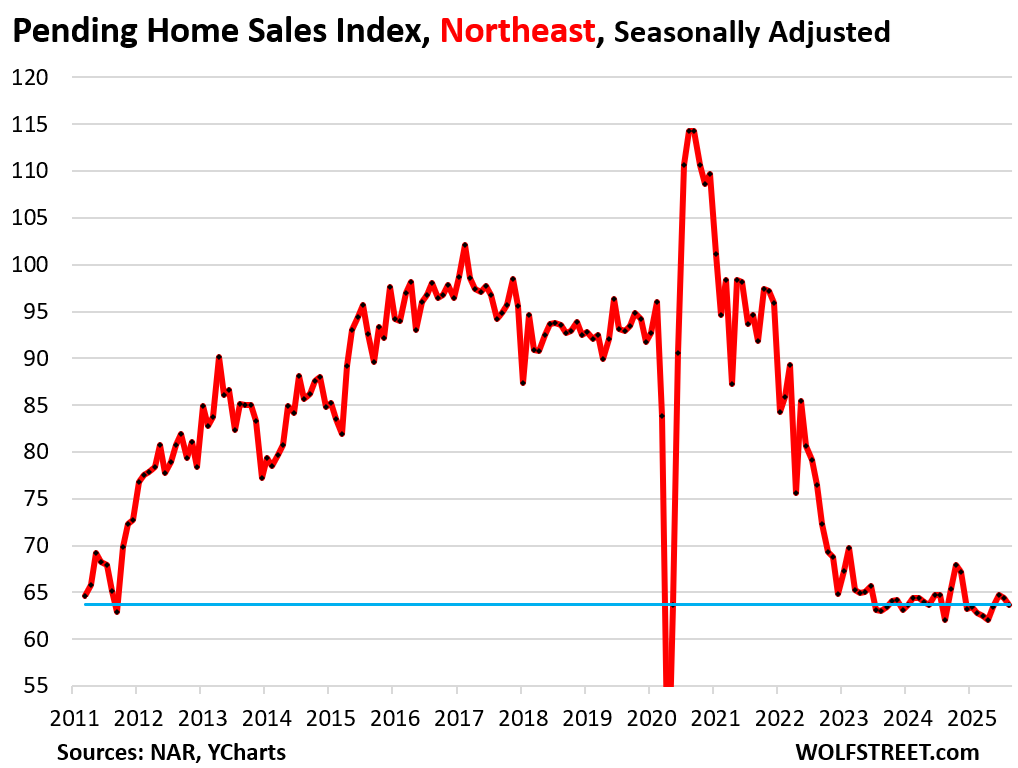

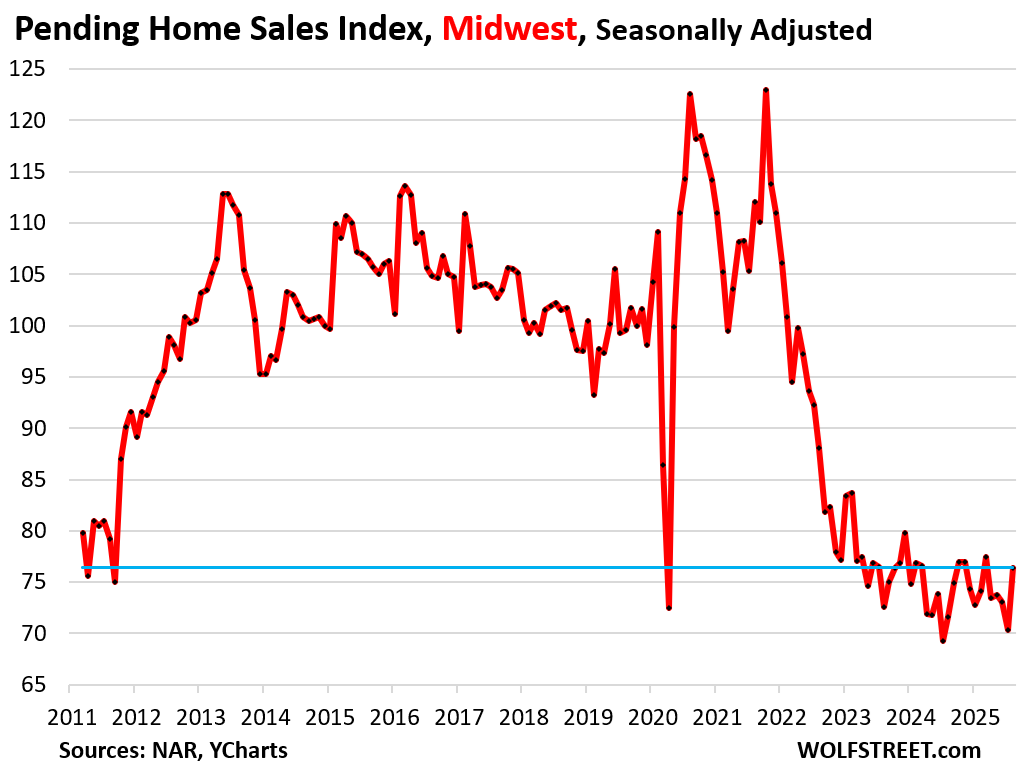

Pending sales in all four regions zigzag along near record lows.

A map of the four Census Regions is posted in the comments below.

In the South, pending sales rose 3.1% in August from July, seasonally adjusted.

Compared to the Augusts of prior years:

- 2024: +4.2%

- 2023: +0.7%

- 2021: -36.0%

- 2020: -41.2%

- 2019: -28.8%.

In the West, pending sales rose by 5.0% in August from July.

Compared to the Augusts of prior years:

- 2024: unchanged

- 2023: +5.0%

- 2021: -42.6%

- 2020: -49.7%

- 2019: –39.1%.

In the Northeast, pending sales dipped by 1.1% month-to-month, seasonally adjusted.

Compared to the Augusts of prior years:

- 2024: +2.6%

- 2023: +1.1%

- 2021: -32.7%

- 2020: -44.3%

- 2019: -31.4%.

In the Midwest, pending sales rose by 8.7% in August from July, but July was the second-lowest in the data going back to 2010.

Compared to the Augusts of prior years:

- 2024: +6.7%

- 2023: +5.2%

- 2021: -31.8%

- 2020: -37.7%

- 2019: -23.3%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The four Census Regions of the US:

North South East or West… certainly looks like the same pattern to me. Encouraging ?? Not yet.

Think the only good news about the housing sales slow down the last 2 years is that the consumer economy is still somewhat holding up. People have been on the sidelines with housing for a while now the stand off between buyers and sellers and prices have not moved too much (unless over heated market). Think we will see healthy increase in 2026 in sales if Trumps Fed Chair pick can take another 1% off fed rate it will be even healthier.

” Think we will see healthy increase in 2026 in sales if Trumps Fed Chair pick can take another 1% off fed rate it will be even healthier.”

The problem is FED does not control Mortgage rates. Infact, recently, mortgage rates are going up despite FED cutting rates.

The problem is not mortgage rates but High prices!

We can thank the high end customer for holding the economy together.

And, maybe youve not noticed the correlation between fed rate and mortgage, but not so linear lately.

We’re on a debt/inflation train to hell.

Trump’s Fed pick and mortgage rates have little correlation….I don’t understand why people refuse to understand.

A bump in activity though would be reasonable from people full on hopium but doubtful it would be sustainable until a washout on prices

The 12 member FOMC at the Federal Reserve, not the Chairman of the Federal Reserve, sets the Federal Reserve’s short term overnight interest rates. As to mortgages rates, the Federal Funds Rate and related rates have nothing at all to do with mortgage rates except that the lower the Federal Funds Rate goes the higher mortgage rates rise exactly as we saw in the Fall of 2024.

yeah. Until the ultra low mortgages are paid off, there will be low sales volume. I still wonder who is holding these mortgage loans. It must feel lousy to lose money like this.

No money is lost when MBS instruments are held until maturity. Nearly all mortgages are now securitized into MBS instruments and not held by banks as used to be the case.

Ah……finally, some normalization is starting to creep into the market.

Anecdotal from here in the Great Lakes (Cleveland) region from someone who is house hunting in the $450-$650 range: homes still seem to be moving briskly, and concessions/price cuts are minimal.

From a colleague who is looking at the $1mm and up market, it seems that there are some relatively significant price cuts going on at the upper end of the market.

In my current neighborhood, 1700-2000 sq. ft. 1920s-1950s colonials and bungalows (inner ring suburbs) are moving pretty quickly in the $165-$250 range.

It is surprising prices have not fallen a lot more than they have with pending sales near 2012 levels. It’s like a tree branch that is weakening under pressure, but hasn’t snapped yet. When it does snap, look out below.

Hard to say, however in my area, there are a lot of people that are sitting out for lower rates. Reality would be the dollar lost a ton of value in 5ish years due to inflation and debasement of currency units. Places that intentionally restricted building are seeing the price cuts.

When this branch snaps, there will be another branch a little further down, and another branch after that. It’s not 2008. Long, slow, boring slog sideways for years to come.

People are definitely still buying and in some hot markets like SoCal, even though there’s drop, some of the transaction is simply bonker, makes you wonder if the people buying now are the last one in the crowd theatre before the fire or this is the new FOMO norm…

Case in point, saw a house in LB listed for 1.26M, sold for $1.3M on Refin and no the house is not under price to begine with. Surprise to still see selling over listing in this day and age without it being a bargain. Needless to say this will be a long drag out fight in some markets unfortunately, some like Austin…not so much.

But there maybe a push pull on prices in front us — if mortgage rates drop a ton (like 200bps) that will quickly cause buyers to jump back in and may start causing prices to rise. Just a thought. Also, I’m still not sure how the price of housing filters into the CPI

Mortgages rates won’t drop 200 bps unless the Fed starts QE again or we enter a brutal recession.

It just ain’t happening.

I anything, mortgage interest rates will rise from where they are now.

Thank you for the 30k ft. view and good perspective on the “huge” 4% MoM / 3.8% YoY increase in Aug., ’25 PHS. A picture – or chart in this case – is indeed worth 1k words. In my view, and the take-away from this post is that sales are still bouncing along the bottom of the 30 yr. low.

My view on prices: Used/Existing/Resale homeowners are still holding out for pandemic era prices, when mortgage rate were sub 3%, but now rates are super 6% (6.38% today for 30 yr., fixed-rate). NEW home sellers (i.e. builders) are cutting prices so that they’re now BELOW USED home prices, which is just another indication that the U.S. RRE housing market is massively distorted and FUBAR. Let’s not forget about the other dumpster fire in CRE. I probably don’t need to mention the AI bubble in stonks, but I will.

Here are the options, absent any additional interventions, by .gov and/or the Fed:

Door #1: Incomes need to rise by more than 60% – Capital tells labor that’s not happening (family friendly version).

Door #2: Mortgage rates need to fall to 2.35% – Bond vigilantes tell long bonds that’s not happening with $37T in debt and spending continuing at recessionary levels. I think someone said “out the wazoo.” The Fed raised the FFR in Sept. ’24 and again just now in Sept. ’25. 10 yr. (mortgage tied to this) and 30 yr. long bond rates rose soon after.

Door #3: Prices (Used) need to fall by 38% – Only option left, and is what history says happens to asset bubbles. They (eventually) burst. An inconvenient truth.

These numbers are “according to Fannie Mae calculations,” but I’ve also run the numbers and they’re close to what I have, based on mortgage P+I monthly mortgage payment only. Let’s not forget that in addition to P+I, T+I are very high also, as are HOA, maintenance, and repairs. Oh dear!

Summary: PHS – a leading EHS indicator – are still stuck in the mud. Prices are sticky to the downside. Just like in HB 1.0.

House prices are still unaffordable to the avg. shelter buyer. That’s the real problem that – in my view – only lower prices will fix.

Have you ever hear of the ol’ ‘rug pull’?

I think it will be a rug pull with the housing market. We are chugging along, albeit at a very slow, sluggish pace but some could say that all appears normal. And it does! Chief word being ‘APPEARS’.

But when the rug pull trick is performed, it will be like a Jenga tower falling down. Game over. Millions underwater. Prices crashing. Sales almost nonexistent. The good ol’ rug pull. 🤔 Coming soon to a neighborhood near you.

Is it like one of those saying “”Slowly at first, then all at once”?