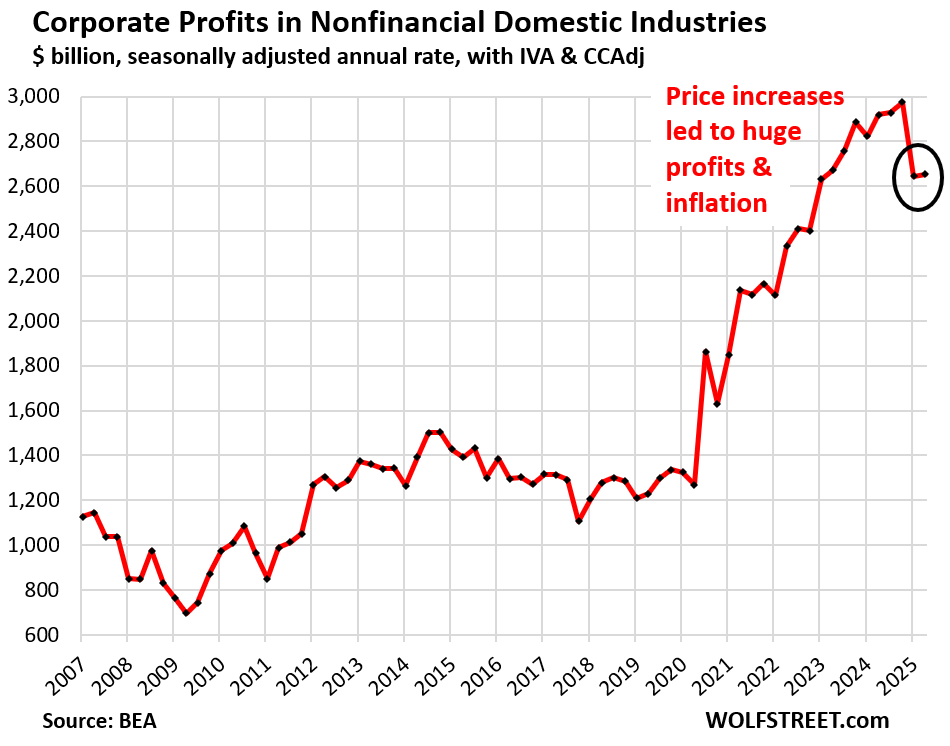

But profits are still huge after the pandemic free-money spike, except in auto manufacturing where losses pile up. Financial industry profits rose to a record.

By Wolf Richter for WOLF STREET.

The measure of corporate profits here are pre-tax profits “from current production” (more on what that means in a moment) by businesses of all sizes that have to file corporate tax returns, including LLCs and S corporations, plus some organizations that do not file corporate tax returns. The data are not based on surveys but on administrative data, such as corporate tax data from the IRS and from financial statements filed with the SEC. The by-category corporate profits for Q2 were released by the Bureau of Economic Analysis on Thursday with its third revision of Q2 GDP. All dollar figures here are seasonally adjusted annual rates (what profits would look like for an entire year at this quarterly pace).

And there were huge revisions of the Q1 data: Revised profits in Q1 of nonfinancial incorporated businesses plunged by $331 billion, or by 11.1%, from Q4. This means they were still massively profitable, with pretax profits at an annual rate of $2.64 trillion, but that was $331 billion less than in Q4.

This revision of Q1 produced the biggest quarter-to-quarter plunge in the data going back to 2001 in dollar terms. In percentage terms, it produced the third-biggest plunge behind Q4 2020 (when profits gave up some of the majestic free-money spike in Q3 2020), and in Q4 2008 during the Financial Crisis. Then in Q2, profits of nonfinancial businesses inched up by $9 billion annual rate from Q1 to an annual rate of $2.65 trillion, but that was down by $322 billion from Q4.

If profits in Q3 and Q4 remain at Q1 and Q2 levels, total profits for the whole year would be $327 billion below the Q4 pace. This is about the annual pace of the tariffs.

The plunge took place largely in manufacturing, wholesale trade, transportation and warehousing, and retail including ecommerce – the segments most exposed to tariffs.

But they had it so good for so long: From Q2 2020 through Q4 2024, profits in nonfinancial industries had spiked by 134%. Over the same period, the high-inflation years, CPI inflation surged by 22%. Corporate profits are where a big part of the inflation surge went.

So the plunge in profits this year comes off that spike during the high inflation years, and even after this plunge, pretax profits at nonfinancial firms from current production are still huge.

What are profits “from current production?” The BEA adjusts profits from IRS and SEC data in three ways to get “profits from current production”:

- “Inventory valuation adjustment” (IVA) removes profits derived from inventory cost changes, which are more like capital gains rather than profits “from current production.”

- “Capital consumption adjustment” (CCAdj) converts the tax-return measures of depreciation to measures of consumption of fixed capital, based on current cost with consistent service lives and with empirically based depreciation schedules.

- Capital gains & dividends earned are excluded to show profits “from current production,” rather than financial gains.

Corporate profits by major industry.

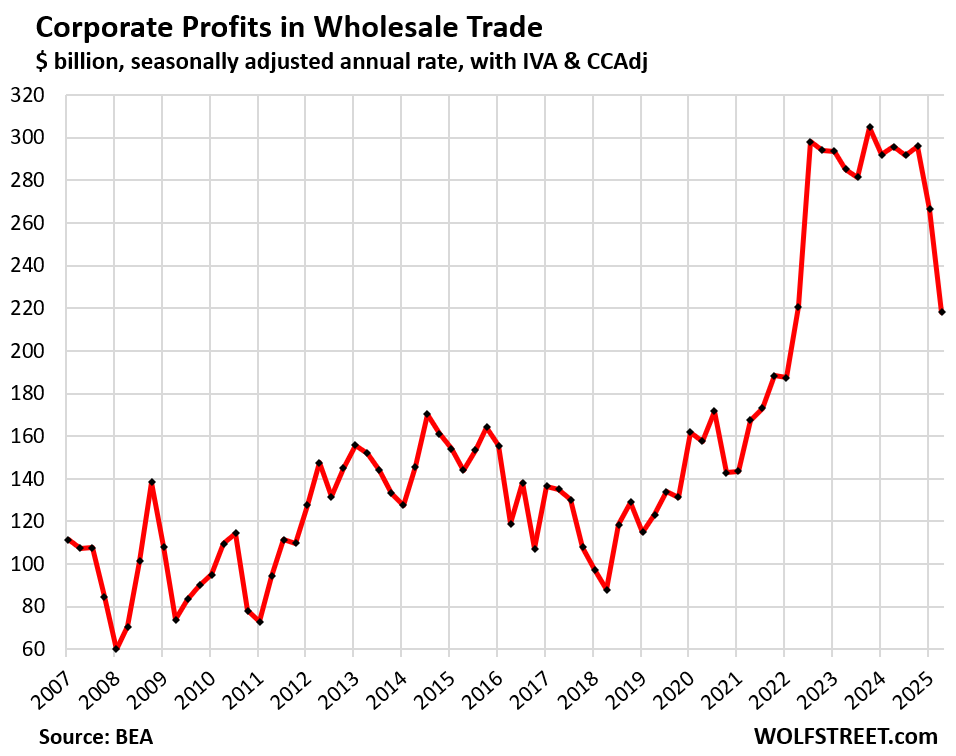

Wholesale trade: Profits plunged by 18% in Q2 from Q1, and by 26% from Q4, and also by 26% year-over-year, to a seasonally adjusted annual rate of $218 billion.

But since Q2 2020, profits are still up by 38%.

Transportation & warehousing: Profits plunged by 8.5% in Q2 from Q1, by 25% from Q4, and by 26% year-over-year, to a seasonally adjusted annual rate of $93 billion.

But since Q2 2020, profits are still up by 313%! And from the prepandemic high in Q2 2017, profits are still up by 32%.

![]()

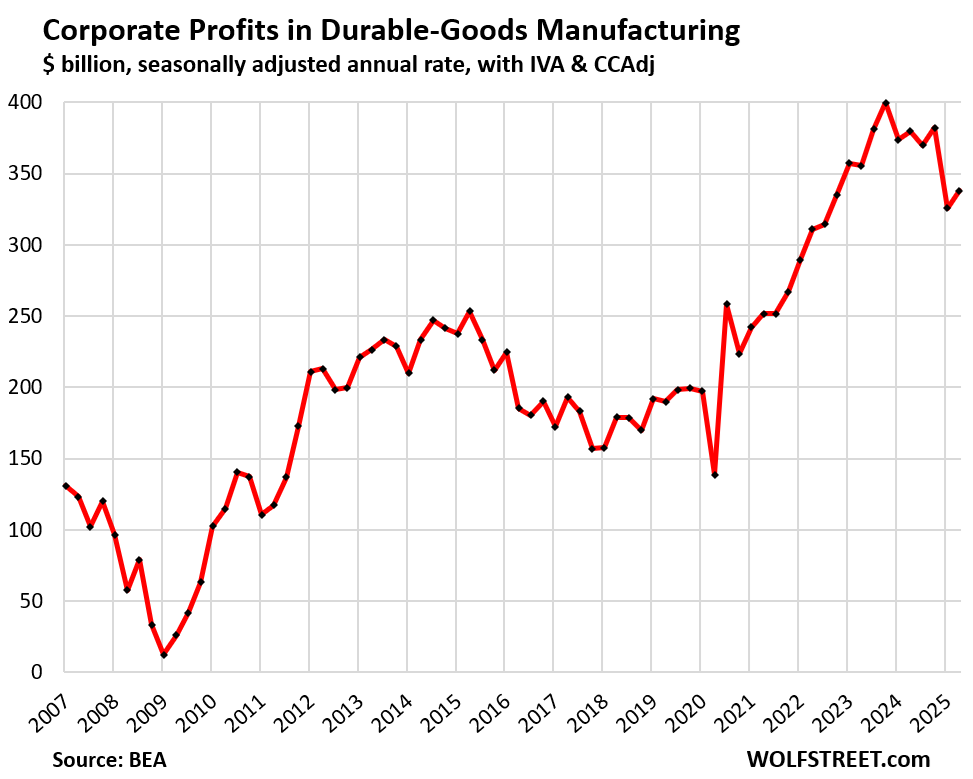

Manufacturing industries, durable goods: Profits rose by 3.8% in Q2 from Q1 after plunging in Q1. Since Q4, profits fell 12%, and year-over-year, they fell 11% to a seasonally adjusted annual rate of $338 billion.

Durable goods include motor vehicles and parts, aircraft, machinery, computers, electronic and electrical equipment, appliances, trailers, fabricated metals, components, etc.

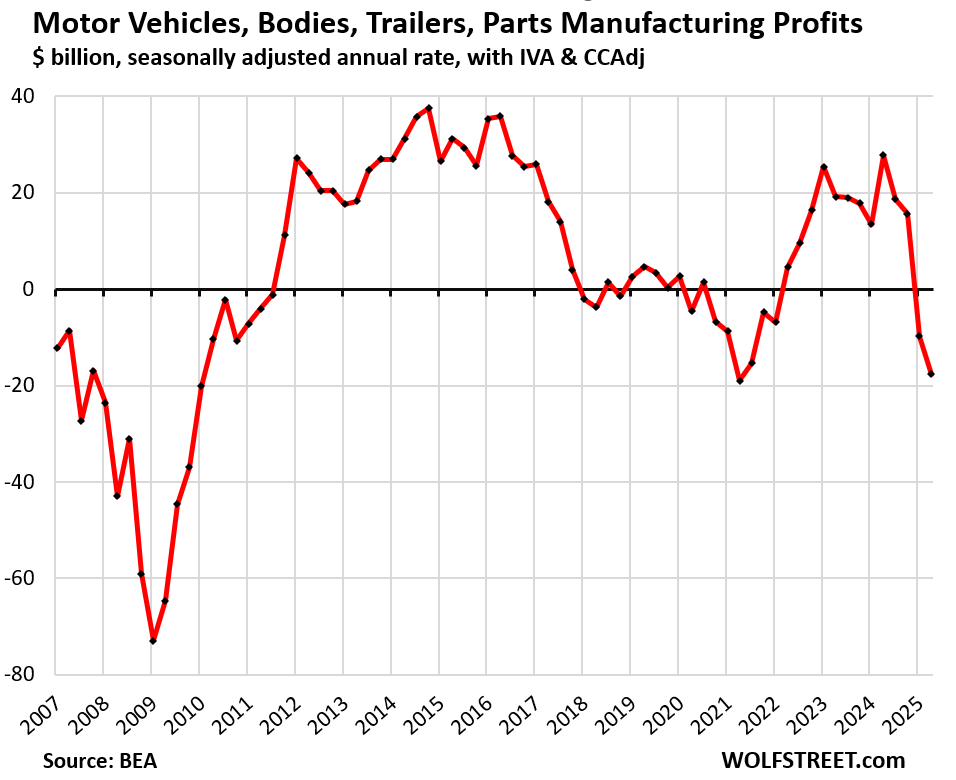

For example, manufacturing of motor vehicles and parts, which is part of durable goods manufacturing. The sector booked losses “from production” in both Q1 (-$10 billion annual rate) and Q2 (-$18 billion annual rate) as these companies could not pass on the tariffs and had to eat them, because they had to cut prices and throw incentives at the market to maintain their sales volume.

The problem is the orgy of jacking up prices from 2020 to mid-2022, until those prices hit a ceiling, when consumers came out of their pay-whatever stupor and refused to pay more. Since then, companies had to offer deals to make sales happen. Tariffs cannot be passed on under these conditions. They all know it, they’ve all said it in their earnings announcements, and they’re busy shifting more production to the US. But that’s a slow process.

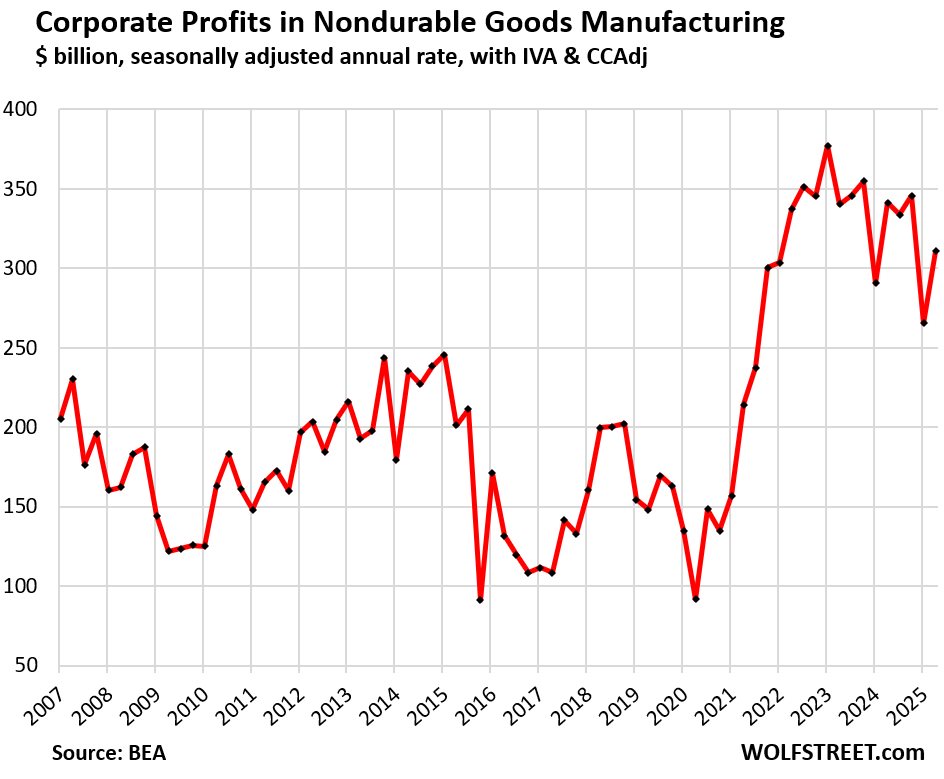

Manufacturing nondurable goods: Profits jumped by 17% in Q2 from Q1, to $311 billion annual rate, but had plunged in Q1, and are still down by 10% from Q4, and by 9% year-over-year.

The sector includes food (such as packaged food), beverages, tobacco products, supplies, petroleum products, chemical products, coal products; apparel, shoes, and accessories, etc.

Since Q2 2020, their profits are still up by 239%.

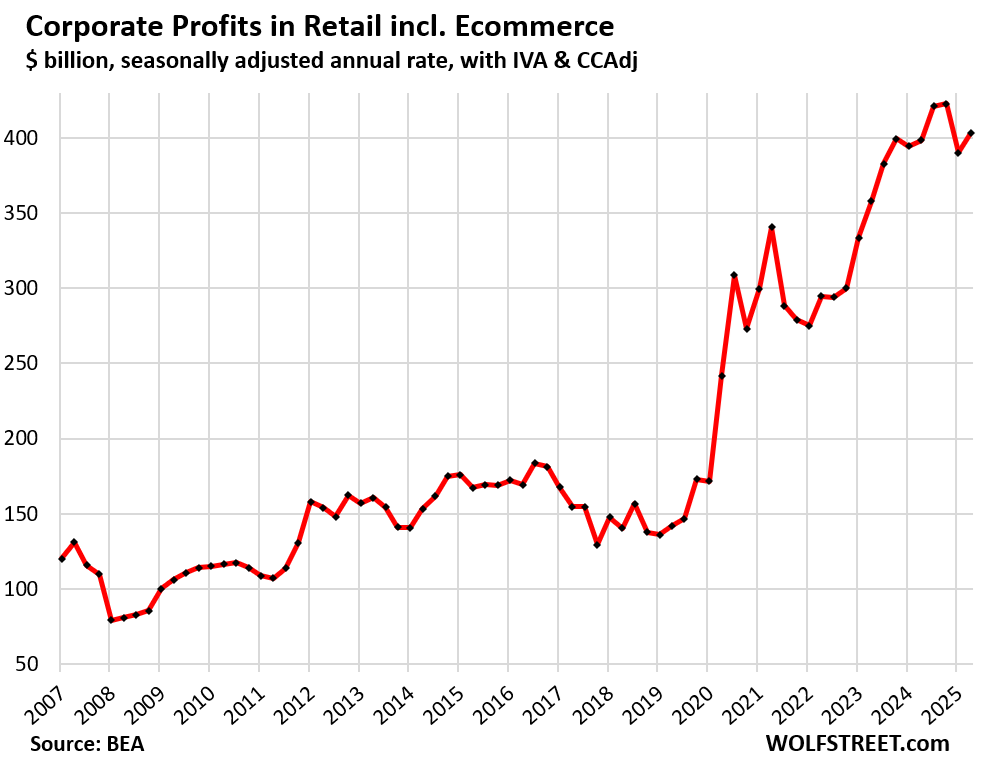

Retail trade, including Ecommerce: Profits rose by 3% in Q2 to $403 billion annual rate, but profits had declined in Q1, and are still down by 5% from Q4

Since Q2 2020, their profits have surged by 67%. And since Q1 2020, profits have spiked by 135%. That’s where part of the inflation in products that consumers buy at stores came from.

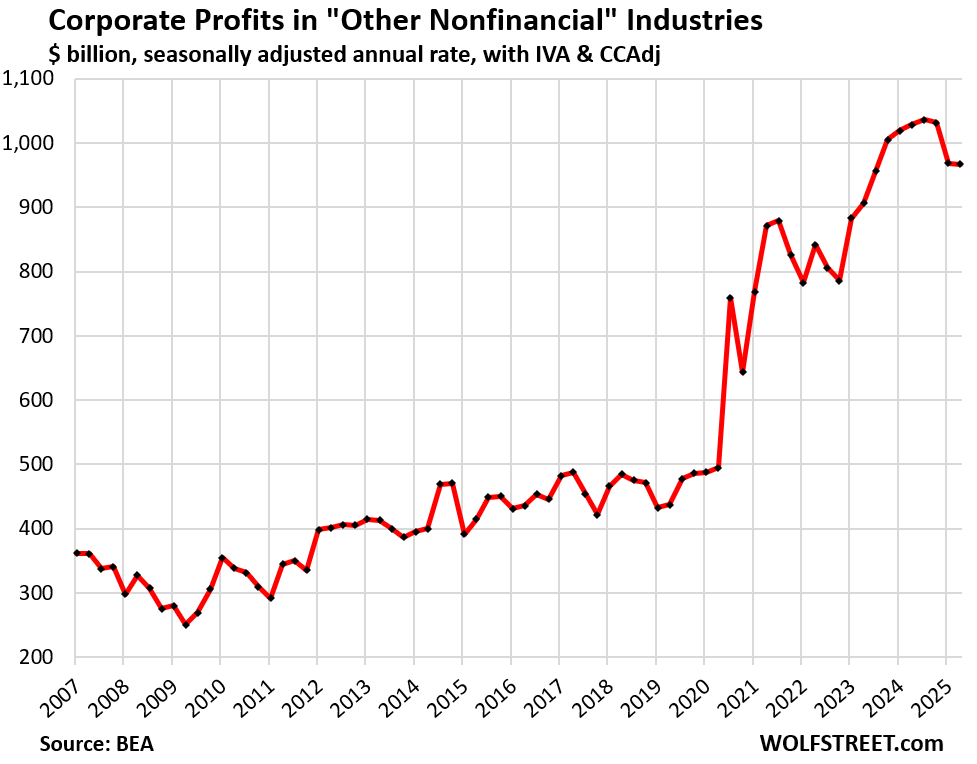

“Other nonfinancial” industries: This is the biggest nonfinancial category, with huge industries, mostly centered on services that are not heavily impacted by tariffs: professional, scientific, and technical services (includes some tech and social media companies); healthcare and social assistance; real estate and rental and leasing; accommodation and food services; construction; mining and oil-and-gas drilling; administrative and waste management services; educational services; arts, entertainment, and recreation; agriculture, forestry, fishing, and hunting.

Profits were roughly unchanged in Q2 at $967 billion annual rate, and were down by 6% from Q4. Year-over-year, they were also down by 6%.

Since Q2 2020, profits have nearly doubled.

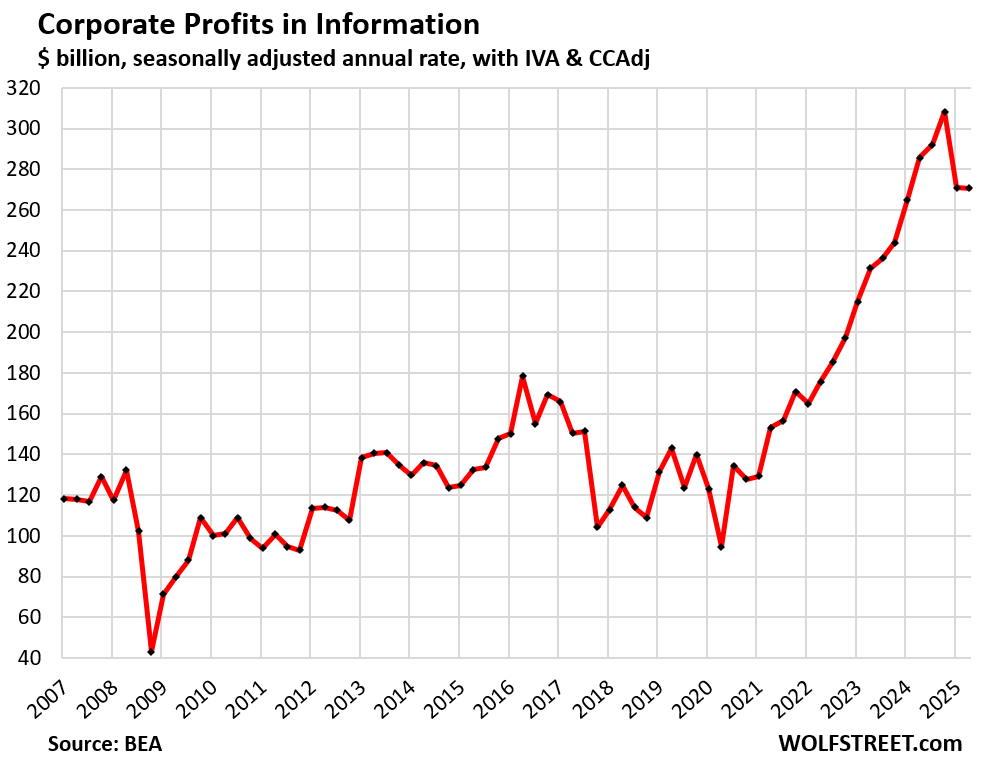

Information: Profits were unchanged in Q2, at $271 billion annual rate, and down 12% from Q4. Since Q2 2020, profits have spiked by 186%! From the prepandemic high in Q2 2016, profits have surged by 51%.

The category includes businesses engaged in web search portals, data processing, data transmission, information services, software publishing, motion picture and sound recording, broadcasting including over the Internet, and telecommunications.

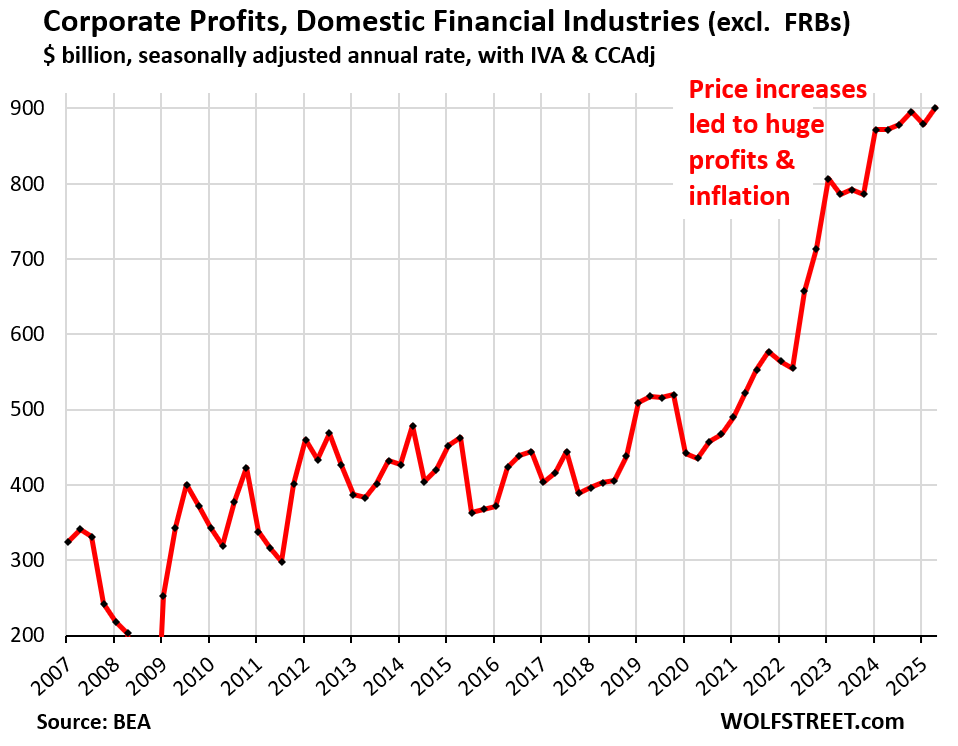

But in the financial industry, profits rose by 2% to a record $901 billion seasonally adjusted annual rate in Q2, up by 1% from Q4 and up by 3% year-over-year.

Since Q2 2020, profits have more than doubled.

Includes: Insurance companies of all kinds, banks and bank holding companies, firms engaged in other credit intermediation and related activities; firms engaged in securities, commodity contracts, and other financial investments and related activities; funds, trusts, etc. But it does not include the 12 regional Federal Reserve Banks (FRBs).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So profits have declined (even if still above 2020 levels) but valuations of publicly traded companies seem to be near all time highs?

This market is completely oblivious to everything.

Absolutely. In the last 4 or 5 months Tesla stock has doubled while sales of their cars have cratered in Europe, China and even America. It’s a car company, and should be trading at 8 times earnings like GM and Toyota, companies that also make EVs. Tesls based on real earnings should be priced at 15% a share but it’s a cult stock and lots of empty promises by its dear leader have kept the company’s stock aloft. We won’t have humanoid robots for a very long time because human movement doesn’t run on gears. As for autonomous EVs….TSLA owners need to look at the lawsuits.

I was reading a finance thread on a UK forum talking about USA markets, and someone said how inflation was good for corporate profits and valuations, and no one else disagreed except me.

And I disagreed because it’s not what I’ve been reading here for over a decade.

The world has gone mad, and far too many people seemingly now believe the post-GFC QE/suppressed rate paradigm only, and all the distorted trends and market behaviours that went with it.

Interestingly also in the UK, JLR have had a shutdown due to a ‘hack’ and now apparently bailout from government for JLR and their suppliers.

I wonder how many other car manufacturers will be hacked now JLR have been bailed out.

Market valuations are not based on inflation hedges, as inflation ultimately hurts companies too, as they can’t pass everything on.

They’re based on the belief (not totally unfounded) that the Fed and Congress will bail everyone out and make sure there is no pain.

As I’ve said before, this will persist until there is a protracted market and economic downturn and the government stays mostly hands off.

Kenny,

Jaguar Land Rover is owned by Tata Motors of India. (As I’m sure you know.) 33,000 people in the UK work directly for JLR. It is the biggest auto manufacturer in the UK

From SKY News 23 September:

“Industry body the Society of Motor Manufacturers and Traders said while government support should be the last resort, it should not be off the table.”

Interesting to me, was to check out my neighbor’s new 2025 Triumph Speed 400 motorbike. A great beginning road motorbike to learn on!

Triumph is an icon British company, yes. But this bike is made by Bajaj Auto in India. The fit and finish of small details are very well done. The robotic MIG welds on the steel framed chassis are also very nice and clean. MSRP on the bike in the USA is $5.4k.

Wolf,

Recent data from federal reserve says that wealthiest 10% of Americans hold 93% of stock value.

Do you have a chart of last 25 years how we came to this point? What is an impact of such a one sided game?

1. I’m not fact-checking your data or what it means, or how it might have been misquoted. For now I’ll just take it “as is,” with no warranty, expressed or implied, whatsoever.

2. I assume this includes shares of privately held companies, such as me holding all 5 million shares of the Wolf Street Corp media mogul empire. Some very large companies have all their shares are in private hands. In addition, there are quite a few companies where the founders or founding families hold a very large part of the shares, such as Musk with Tesla, and Dell with Dell Computer.

3. Over 50% of all households hold at least some stocks, such as in their 401ks, or in their trading accounts, an all-time record.

We are long long away from recession. Companies still making lot of money.

I’m not suggesting we are anywhere near a recession but I wouldn’t use corporate profits as the gauge. Better to look at unemployment, hiring and other indicators as to whether it is approaching. Decreases in immigration and related probably helping the unemployment low although not sure how significant.

Here’s your GREEDFLATION, right here.

So in all of these graphs, every industry appears to have doubled their profits. Geez, I wonder how that happened?

I love the association between Nonfinancial Domestic Industries & the annual cost of tariffs.

This all comes down to massive price gouging by corporations and the US Anti-Trust Laws not being enforced.

When is enough enough to put a stop to all of this massive price gouging?

It will happen when people change their behavior and refuse to be gouged. We seem to be seeing it in the auto and housing industries. But those are most folks two highest ticket items and it needs to move to more down-priced items. I changed my behavior almost immediately, but I don’t watch the “news” and blame big gubmint for individual corporate decisions.

The US government is 2 days away from shut down and this is barely even being discussed in the media and the Democrats and Republicans aren’t even seriously debating the issue but rather trying to figure out who gets blamed for the US government spending nearly $2 trillion more than the bloated budget and having to borrow that each year just to keep kicking the can down the road.

Solid vacation for those that don’t get paid, don’t have to work, and get back pay when they return. I’d take a piece of that action. And yes, I do understand implications are well beyond that and it will cause pain for many. My money is on democrats folding.

Tariffs are bringing in roughly 300B annual so we just have to find another 1700B in savings to get that 2T deficit down right? I would presume that USA production brings in more tax revenue that having production offshore. Any reason tariffs plus more tax revenue from increased onshore couldn’t close the gap to 1T in a couple years once the onshore factories start running?

No one says that you have to close the budget gap. But get the deficit down to 3% of nominal GDP, and over time, with 2.5% economic growth (adjusted for inflation) and 3% inflation, the burden of the debt would shrink. So the first step is to get the deficit to 3% of nominal GDP. Right now that means get the deficit to down below $1 trillion. That’s what the goofballs in Congress should be working on. Tariffs are a step in the right direction; shifting production to the US is a big step in the right direction. But it’s going to take a little more than that.

So right.

And achievable.

Come on politicians!!

Can we relate that to the required return necessary for someone to maintain the value of their savings?

For someone with a 33% tax rate, I see 4.5%. This allow tax to be paid and still provides 3% nominal growth of principal.

Then the question is how to achieve that. Neither the 10 year nor short term treasury bills pay that much (4.5%), and the 10 year has duration risk (uncompensated I think).

All other investments are out on the risk curve and a roll of the dice.

“…and 3% inflation, the burden of the debt would shrink.”

That kinda sorta looks like an argument for the Fed to modify it’s inflation target. Now you just have to get them to say the words. That’ll be a fun day. Let the bond market repricing begin!

Given the egregious nature of these corporate profit charts, it would seem that it may not have been wage inflation that caused all the post pandemic consumer prices price inflation, but corporate price gouging.

So much for the long standing media narrative of blaming all consumer price inflation on rising employment wages.

So, Retail Trade hardly suffered a decline in profits in Q1 and Q2. Since retailers import a lot of stuff for the coming festive season, presumably their profits will also be hit by tariffs in Q3 and Q4. I can’t see retailers being able to pass on tariffs given the foul public mood at present. It’s interesting how no blame from people doing it tough has yet attached to the big ‘corporations’ – they won’t hear about those obscene profits from the mainstream media. Thank you, Wolf.

Yet another glaring sign of how the Fed and everyone else in government lied straight to our faces on inflation. All signs point to 2x-3x what they claimed.

Thanks Wolf. Your articles are very well written and are delightful to read.

Q1 2025 plunge can’t really be due to tariffs, as they kicked in partly in Q2 and partly in Q3.

Assuming tariffs are bringing in 300b annually, should we expect to see another 200-300b downtick in Q3 numbers, as and when they are reported?

Well no. The first tariffs came in January. And more were added in quick succession. Then the 25% tariffs on Mexico and Canada and additional 10% tariffs on China started on Feb 1. Companies are required to account on an “accrual” basis, so when they know they have to pay for something (such as by invoice), they account for it as an expense before they actually pay it. That is required by accrual accounting rules. But the tariff figures that the government releases are on a cash basis, when the cash was actually received by the government. So the tariffs received in March and April were likely from January and February. May tariff receipts may have largely been expensed by companies in March. So those would all fall into Q1.

Interesting article on CNN this morning, titled “Americans have more money in stocks than ever before. Economists say that’s a bright red flag.”

It’s actually more balanced than I expected. I don’t agree that “Record-high stocks are generally good – that lets more people benefit from Corporate America’s gains” when it’s based on P/E expansion, and not sustainable earnings.

They rightly point out that so much riding on the stock market means that the economy as a whole is more impacted by a downturn. They also rightly point out that a huge percentage is based on the Mag7 and AI.

Most importantly, there is a large segment about how the rich get a disproportionate share of any benefits. I don’t think I’ve ever seen the mainstream media admit that before. Here’s that part:

“That’s in part because the job market, where most Americans make the bulk of their money, is stagnating, while the stock market, which is how wealthy people tend to make their money, is surging.

“Those who have a high degree of wealth in the stock market feel like they’re doing extraordinarily well,” said Michael Green, chief strategist at Simplify Asset Management. “Those who don’t, who are largely tied to employment as their primary asset, feel much more constrained in today’s society.”

That is creating distortions in economic data, too, helping to paint a rosier overall picture than the one many Americans are feeling in their lives. The buoyant stock market is propping up the net worth of the wealthy, fueling their own spending, which in turn has helped propel economic growth, Roach at LPL Financial said.”

You know what’s cool about having all these rich people so intimately tied to something that defies all logic?? They are going to be the ones that suffer when all this normalizes.

To a certain extent we were told that the foreign companies would pay the tariffs, however this article seems to say the tariffs are being paid by domestic companies. That’s a big difference, with big implications.

If “we were told” that foreign companies would pay the tariffs, whomever was talking was outright lying.

No one ever made the claim that the headquarters or place of incorporation would dictate whether a company would pay tariffs. It’s purely based on whether the GOODS are being made in the United States or imported. If Toyota, headquartered in Japan, makes Rav4s here in Kentucky, no tariffs are paid on that car (ignoring the materials and parts for the purposes of this example).

If Ford, headquartered in Michigan, makes F150s outside of the U.S., it would pay tariffs.

Of course they are going to get paid by domestic companies who import their stuff. Which is a lot of domestic companies

Isn’t is a moot point? The tariff tax is paid domestically and the increased cost is passed on to the consumer. If a tax was instead placed on foreign sellers, they would want to maintain profit and raise their prices accordingly, similarly resulting in an increased price to the consumer.

You and I must have read different articles. The one I read makes a compelling case that the tariffs are mostly being eaten out of profits, implying they’re not passed on to the consumer. For the moment, of course. Businesses could try to change that if the stock market wakes up to this arrangement.

From the article:

“If profits in Q3 and Q4 remain at Q1 and Q2 levels, total profits for the whole year would be $327 billion below the Q4 pace. This is about the annual pace of the tariffs.”

Corporate profits may have declined somewhat, but profit margins are still sky high at 17.8%, up from about 12% in the 2010s and from 2% in the 1950s and 1960s.

https://fred.stlouisfed.org/series/A466RD3Q052SBEA

No reason to be concerned about the oligarchs…

1. That measure you linked is NOT “profit margins.” It is called “profit per unit of real gross value added.” Among other things, it is adjusted for price changes in those products or services (inflation/deflation).

2. Don’t cite figures that you don’t understand and then misrepresent them and turn them into a fake theory.

3. Even this measure (which is adjusted for price changes, dropped by a full percentage point, from 18.8% to 17.8%.

4. Yes, it’s still a lot higher than it was before the pandemic. It was 11.2% in Q2 2019, v. 17.8% in Q2 2025, so 59% higher. The dollar figures I cited are 104% higher over the same period.

5. The idea of the dollar data here was to show the impact of changes in selling prices by these companies over the high inflation years. If you adjust the changes in selling prices away as inflation, then that part becomes a flat line, and what’s left is other factors that caused profits to rise, such as on the cost side, where price increases were much lower than their selling price changes. This is what your cited data shows.

Wolf. Can you provide the analysis as to why business profits grew so fast from 2020 to now. Biggest factors?

Countrybanker,

Profits grew because customers were willing to pay the increased prices. Nothing more complicated than that. People were willing to pay because of all the money that the US govt and the Fed were busy showering.

I agree that your last point about the influx of government money or fiscal stimulus ; that said money from the government was borrowed, instead of the government taxing it’s citizens, and finally the FED monetizing that debt with huge growth in its balance sheets buying all kinds of debt including government debt.

I do not think it is simple as that, thus my question is

I think that implies that savers paid through the diminished purchasing power of those dollars that were saved prior to the inflation.

Countrybanker

“…why business profits grew so fast from 2020 to now. Biggest factors?”

Jacking up prices. I said that may times, including in this article.

And I explained many times, including in this article why they could jack up prices: free money and consumers/companies willing to pay whatever under the influence of free money.

And I explained many times, including in this article, why they cannot jack up prices now: the free money is gone and consumers/businesses are no longer willing to pay whatever.

Root Farmer,

Think that is an oversimplification. That would be true if it was something purchased that was truly not a need. Even something like a new car can be a need or travel for example. Not suggesting printing money wasn’t a big part of it but at the same time, what does one expect companies to do? They operate to maximize profit regardless of industry and there are few controls to keep profit to the traditional sense of the word. Doesn’t matter if it is health care or alcohol or anything else and they have little concern for consumer debt as long as customer keep coming. Americans, by and large, just accept this as a healthy economic system.

I don’t see the numbers for tariff dollars going to the government so am curious as to the difference in corporate tax cost after tariff cost is deducted from income tax. Would probably be a good article from Wolf.

Personal info, but I’ve been retired since 2000 and am now beginning to feel the cost of inflation. Yes my small share of the market has been growing but my fixed income as stagnated. Company has stopped all inflation raises and bought an annuity for my payment. Think this means no increase from now on. Which also means my consumption will decrease. Thanks to the larger tax deduction I will gain a bit this year. Problem is the next admin will simply reduce that deduction. It being a low hanging fruit for them.

“I don’t see the numbers for tariff dollars going to the government…”

Good lordy! These are the receipts in cash by the government from the tariffs, reported here monthly. Next one coming up early next week.

The chart “motor vehicles, bodies, trailers, parts manufacturing” squares well with our experience in the truck equipment world.

Everyone on the outside thinks we are making a mint, but the reality is a story of booms and busts that gradually cancel each other out and make running the business pretty lame.

Since February of this year, volume has absolutely fallen off a cliff. Depending on the reference point, unit orders were down -65% to -89% from “normal” this September, the worst month so far this year. The magnitude of this 2025 downturn is now exceeding the downturn of 2008/2009.

The first half of the year was modestly profitable but that will be wiped out by year end because of low volume as we strive to hold on to the best of our workforce despite very little product going out the door.

I can’t help but think that the profits should be divided by revenue to check if the margins changed.

excellent point.

Margins are down too. We’ve discussed some nonfinancial industries here where margins have plunged, including automakers and homebuilders.

Note my comment in reply to JohnH above about “profit per unit of real gross value added.”

Very interesting analysis Wolf, love this page. While leading indicators have been pointing to a recession and none has come, I have had four pillars in my mind that were important on keeping a lid on it and having the economy tick along: Corporate profit margins being very high, expansion of the public sector under Biden (government and health care jobs), student loan forgiveness under Biden, and AI infrastructure capital spend. Two of those pillars are completely gone, corporate profits are starting to weaken (as you show), and for now AI capital spend is still going strong. The problem will come when the AI capital spend slows, doesn’t even have to stop, just needs to slow from parabolic. The stock market will read that in advance and sell the names that have lead this bull market. That will have a reinforcing effect on an economy that is so dependent on the stock market doing well. When is a fools game, but how interesting is it to see this pattern yet again in the “roaring 20s”

“The problem will come when the AI capital spend slows, doesn’t even have to stop,..”

Yes, I’ve said for a quite a while here that when the AI investment bubble stops (slows a lot), the recession begins.

AI is taking a lot of jobs away, including taxi-type drivers. This is already happening. The Waymos are doing very well in more and more cities. Other companies are also rolling out this technology. Waymos are still just an experimental tech, but when it’s ready, Waymo may either get massively into taxi operations and/or license it to automakers, Uber, taxi enterprises, etc. This is going to take some years, but it has already started. And those driver jobs are going away. There are many other jobs that have started to disappear: call center jobs (in Bangladesh?), tech support jobs, lots of jobs in tech and other areas.

AI is also creating a lot of new jobs, often highly paid jobs, from tech to construction and equipment manufacturing. But when the AI investment bubble stops, the AI job creating will slow, while the AI job destruction will continue. There will be lots of other factors. But that’s the recession. But we’re not close yet.

Tariffs protect essential industries. Wages in favorite industries will rise.

Wages in unfavorite sectors will not rise. Workers in those sectors will not

be able to afford higher prices. They will cut consumption. Thus tariffs, without increasing M-2, don’t cause inflation. Some prices will rise. Other prices will fall.