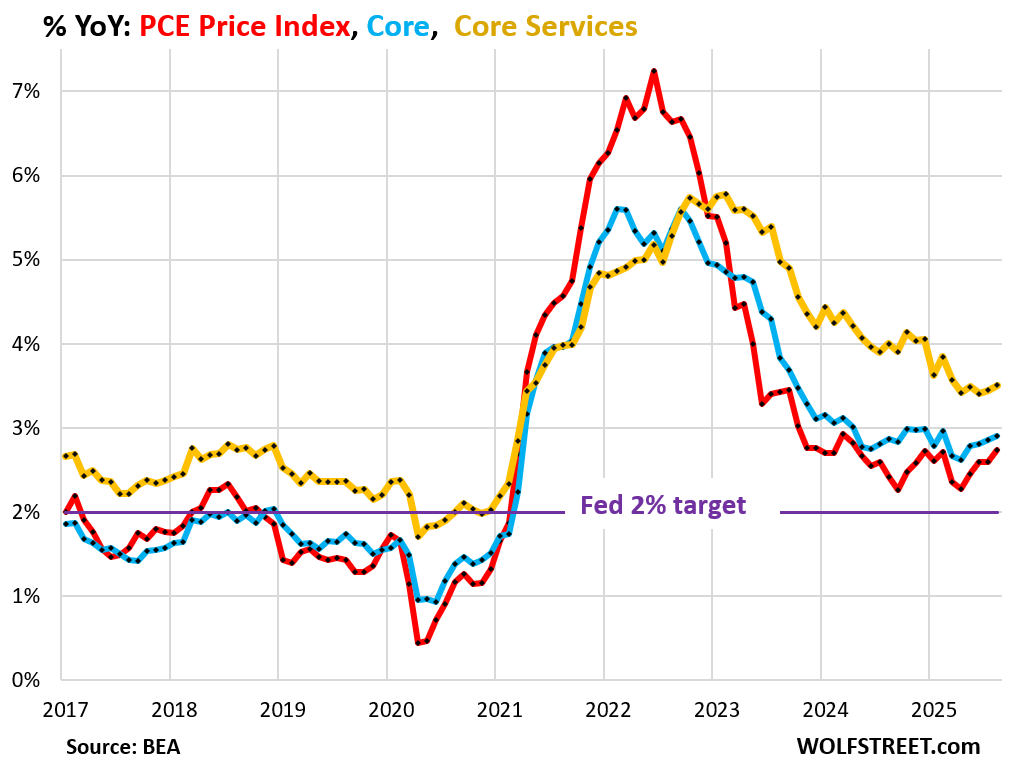

The 12-month overall PCE & core PCE price indices, which the Fed uses for its target, are worse than a year ago.

By Wolf Richter for WOLF STREET.

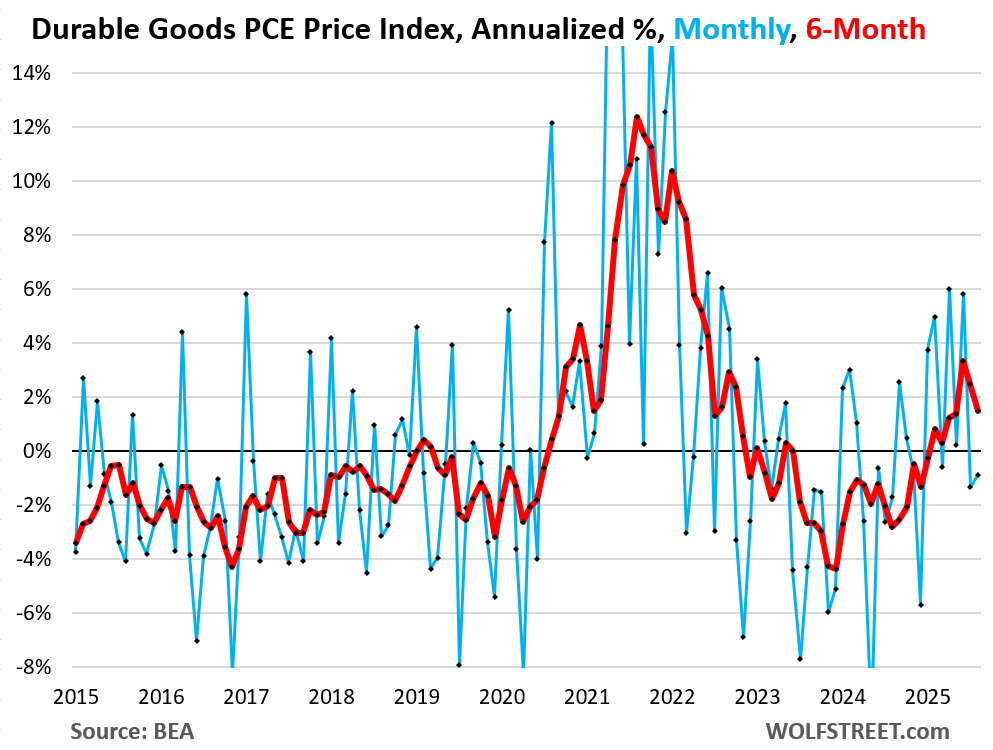

Inflation is in services, where it accelerated further, even in the inflation index that the Fed prefers, the PCE Price Index released today by the Bureau of Economic Analysis, though Powell has been denying it in recent speeches, blaming instead imported goods and tariffs for the current inflation impetus. But the PCE price index for durable goods, many of which are tariffed, fell (negative readings) in August for the second month in a row, while inflation in services, which are not tariffed, accelerated further.

Both the overall PCE price index and the core PCE price index accelerated further year-over-year, and their increases (+2.7% and +2.9%) are now worse than a year ago.

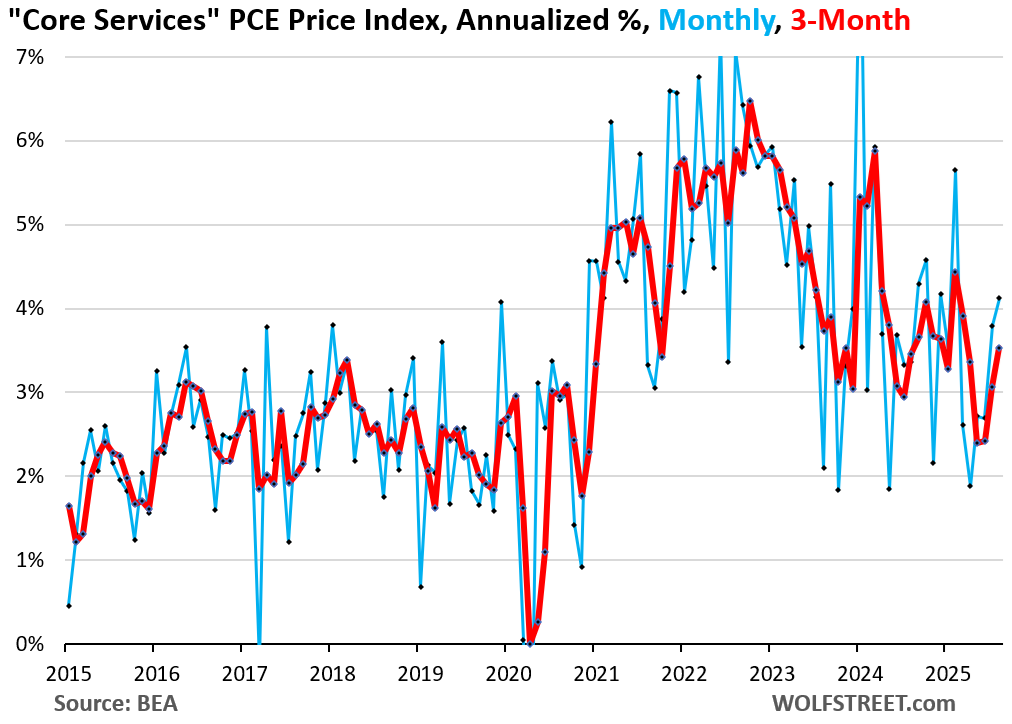

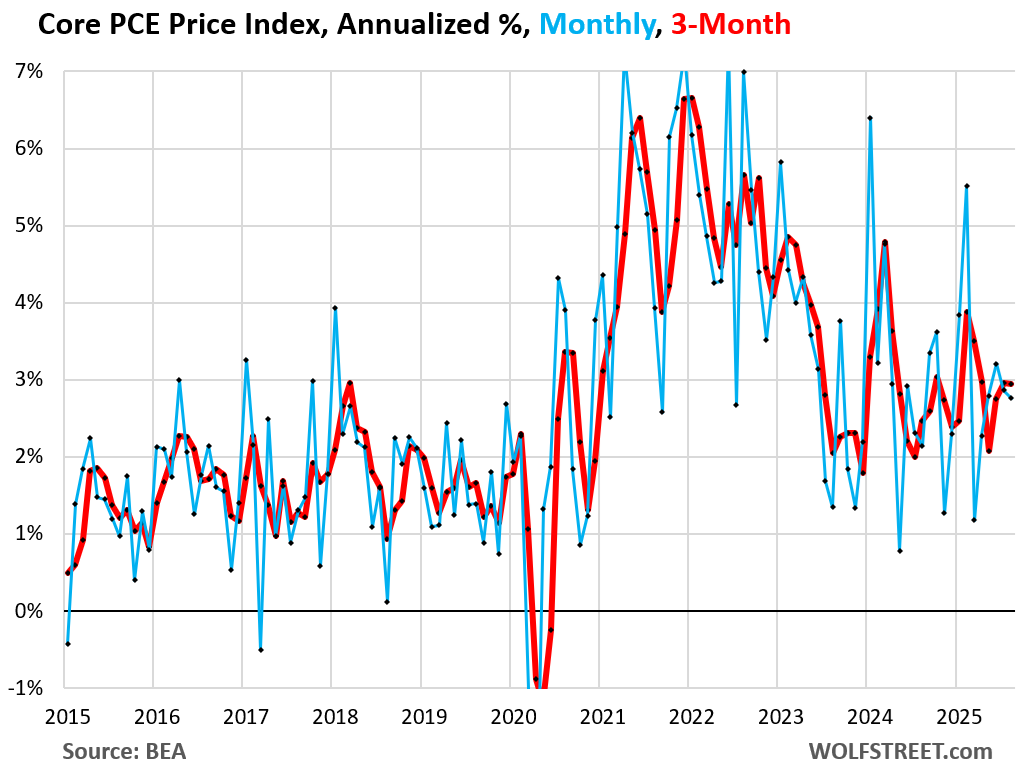

The core services PCE Price Index, which excludes energy services, accelerated to +0.34% (+4.1% annualized) in August from July, the fourth month in a row of acceleration. The increase was driven by rents (+4.4% annualized, the worst since March) and some non-housing services (blue in the chart). The 3-month index accelerated to 3.5% annualized, the worst since March (red).

This confirms what we have already seen in the primary inflation index of the US, the CPI, whose August data were released earlier in September by the Bureau of Labor Statistics: the month-to-month increase of core services was above 4% annualized for the second month in a row, the worst since January.

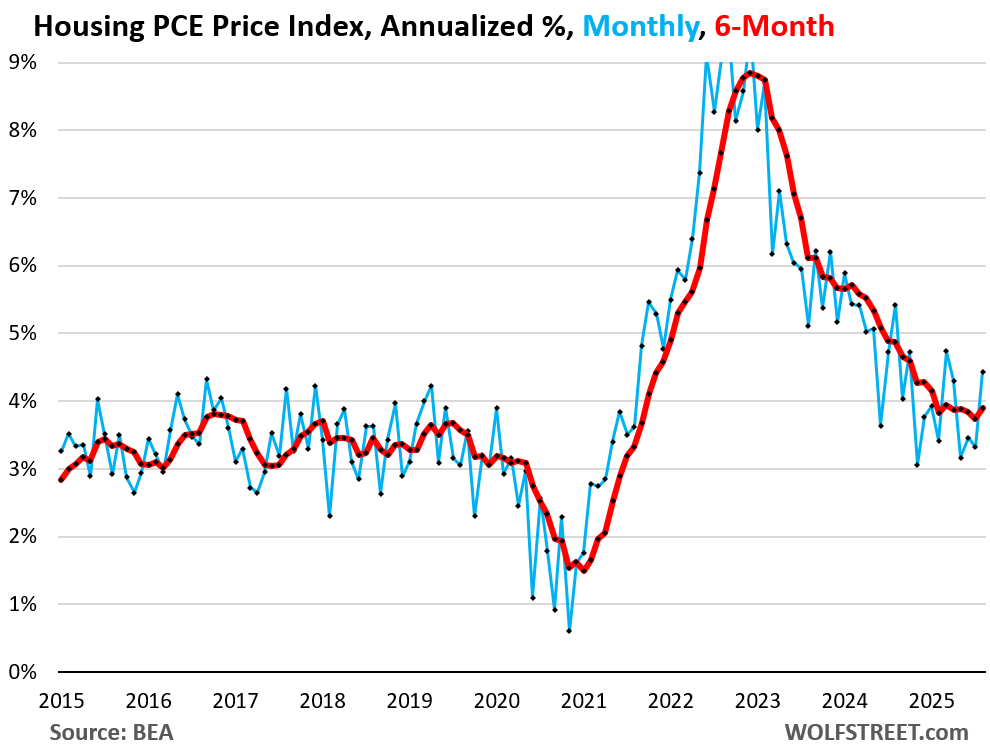

Rent inflation jumped in August, increasing by 4.4% annualized from July. The six-month index ticked up to 3.9%, the worst increase since March.

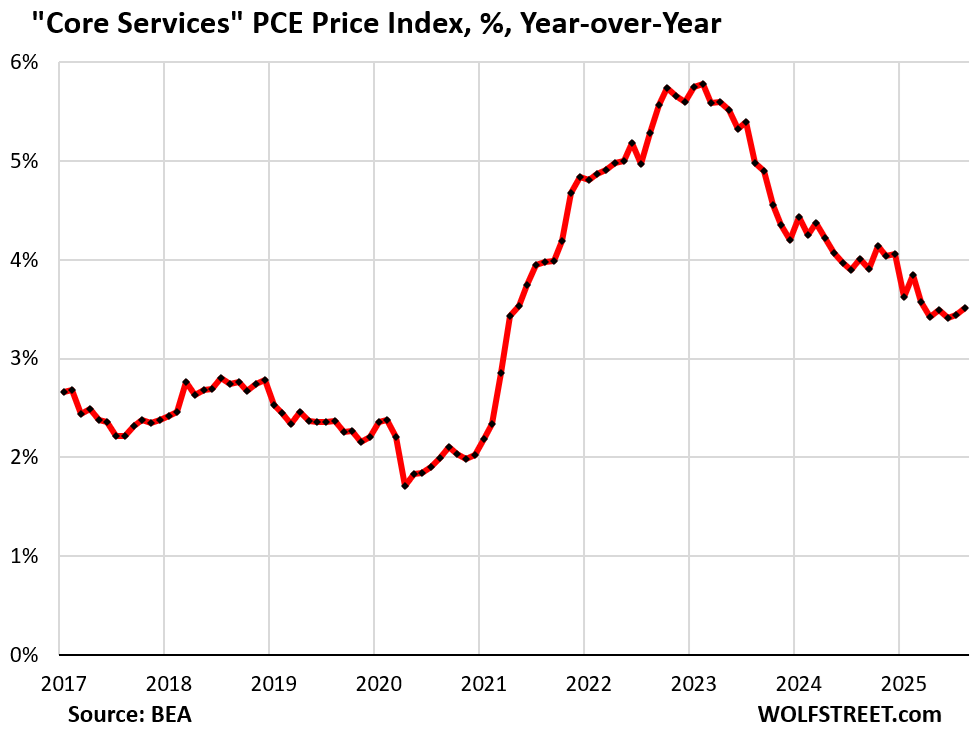

Year-over-year, the core services PCE price index accelerated to 3.51%, the second month in a row of acceleration. It is substantially above the pre-pandemic range and accelerating away from it.

Two-thirds of consumer spending is for services, and this year-over-year inflation rate of 3.5% powers the overall PCE price index and the core PCE price index.

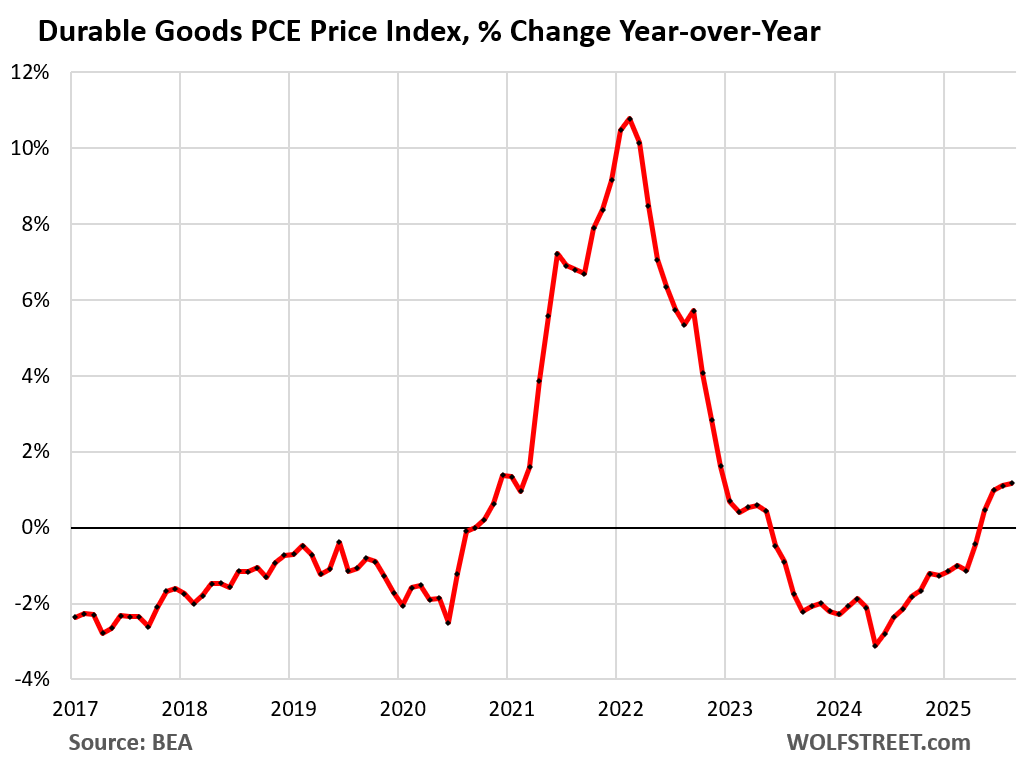

But the durable goods PCE price index fell by 0.1% (-0.8% annualized) in August from July, the second month in a row of negative readings.

Many durable goods are imported, or their components are imported, and many of them are tariffed. Durable goods include all motor vehicles, appliances, furniture, bicycles, laptops, phones, audio and video equipment, etc.

Durable goods are where a big part of the tariffs would show up. But whether or not companies can pass on these taxes depends on market conditions – whether consumers keep buying products at higher prices now that the free money is gone, or whether sales fall, and companies have to cut prices to get the sales they want.

Durable goods prices blew out from mid-2020 through mid-2022 and reached ridiculous levels, with year-over-year increases of over 10%, triggering a huge spike in corporate profits – which is where a big part of this inflation went.

But then consumers emerged from their pay-whatever stupor and began resisting higher prices by not buying these products when prices were raised further, causing sales to drop for these products, which forced companies to cut prices and offer deals in order to sell their goods.

This price cutting from ridiculously high price levels was why the month-to-month durable goods PCE price index turned negative in late 2022, and why the year-over-year durable goods index turned negative in June 2023, reached -3.1% in early 2024, and then began to get less negative every month until April 2025 when it turned positive again.

In August, the year-over-year increase in the durable goods PCE index was 1.2%, which helped pull down overall inflation rates driven higher by services. And much of that has been due to used cars, whose prices have been re-surging for 12 months, after a hard plunge (used cars are not imported).

The core PCE price index decelerated to +0.23% (+2.8% annualized) in August from July.

The deceleration was the result of the negative readings in durable goods overpowering the acceleration in services.

The 3-month index rose by 2.9%, same increase as in July.

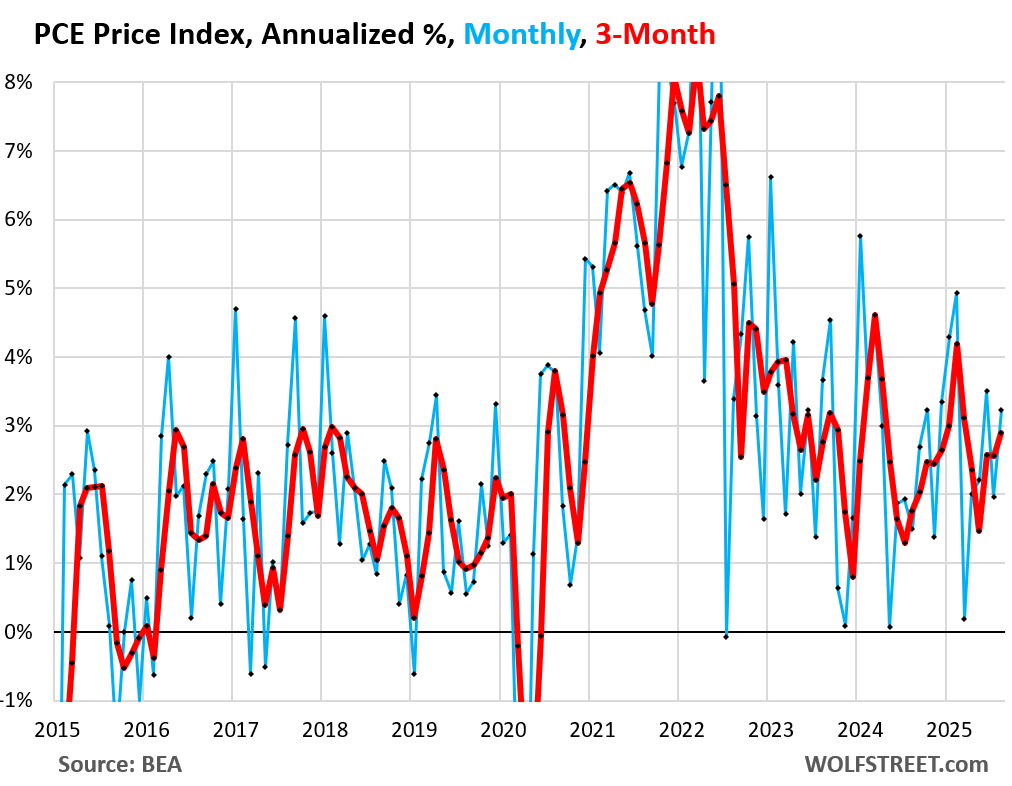

The headline PCE price index accelerated to +0.28% (+3.2% annualized) in August from July, pushed higher by month-to-month spikes in both:

- Food prices: +0.47% (+5.8% annualized)

- Energy prices: +0.79% (+9.9% annualized).

The 3-month headline index accelerated to 2.9% annualized.

Year-over-year and the Fed’s 2% target.

The year-over-year overall PCE price index and the year-over-year core PCE price index form the yard stick that the Fed uses for its 2% inflation target. Both are well above the 2% target and accelerating away from it.

Both the overall PCE and core PCE were worse in August than they had been in August last year.

Overall PCE price index accelerated to 2.74% in August, worse than a year ago (2.41%), and the fourth month of acceleration in a row (red in the chart below).

Core PCE price index accelerated to 2.91%, worse than a year ago (2.87%), and the fourth month of acceleration in a row (blue in the chart).

Core services PCE index accelerated to 3.51%, the second month in a row of acceleration (yellow).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Not out of the woods yet on potential tariff inflation.

Yesterday: 50% Tariff on all Kitchen Cabinets, Bathroom Vanities, and associated products, starting October 1st, 2025. Additionally, we will be charging a 30% Tariff on Upholstered Furniture.” Additionally, drugs and big trucks new tariffs.

Yes, lots of tariffs for companies to eat. All of the products you mentioned can be manufactured in the USA, and there are no tariffs on products manufactured in the US, so they can buy USA-made products, which is the primary point of tariffs, the secondary point being the additional tax receipts that companies are now paying to the Treasury at a rate of over $30 billion a month.

Those tariffs are coming out of corporate profits. But those profits spiked out the wazoo during the high inflation period when companies jacked up their prices and profit margins, while consumer paid out of their nose. So now they’re giving up some of those big-fat profit margins to tariffs. It’s not the end of the world. I’ll show you some charts on that later today or over the weekend. Make sure you read that article on “corporate profits” in Q2.

It’s amazing how virtually no other news outlet views tariffs this way–a tax on corporations that simultaneously makes American goods more competitive.

Also interesting that liberals who favor raising corporate taxes can’t figure this concept out either. Somehow all tariffs are passed directly to consumers but an increase in the corporate tax rate would never be passed on to consumers.

Yes, this stuff is endlessly amazing.

I love it. It sort of functions like a general higher corporate income tax rate, with credits if you manufacture here.

I would much rather have real incentives to give jobs to Americans. I don’t care where the companies are headquartered, what I care about is whom they are hiring to build this stuff.

Its not the “stuff” that JQ Public buys at Walmart, Amazon etc, its the companies selling you insurance, new gutters, lawncare, dental work, dishwasher installation, remodeled bathrooms, roofing etc etc, is it “tariff affected ” services? probably not, or is it the now cliche “its just Greed! the Democrats cry from a town square somwhere?

The bond vigilantes are sharpening their knives

The bond vigilantes died a long time ago. Taking their place are idiotic fools who like handing over their money for a measly rate of return that barely covers inflation.

“Inflation Is in Services despite Powell’s Denials”

Powell the liar. And you wonder why I don’t trust the FED?

I appreciate your focus on year on year actual changes and not current vs expectations. All the market seems to care about is the latter, but it’s the former which matters.

The evidence of inflation, contrary to the conventional wisdom, cannot be conclusively deduced from the monthly changes in the price indices.

And calculating inflation on a year-to-year basis minimizes, over time, the rate of inflation since the rate is being calculated from higher and higher price levels and higher bases.

This makes no sense. It’s a percentage increase. If you’re saying that compounding annual changes leads to larger changes in the long run, well, yes, of course. But why does that matter?

The 2.5% average annual inflation since 2000 does in fact add up to 87% total, and not 25*2.5=68%. That doesn’t mean that prices weren’t 2.5% higher each year.

Typo, that should read 25*2.5=63

This looks like it’s stuck at a little below 3% for about 2 years now.

The target is 2% and the average over the last 30 years is 2.5%.

A little worse than you’d like, but relatively stable. Most definitely not a reason to cut rates or to lose vigilance, but also not a reason to panic.

Inflation averaging 25% above target each and every year since 1995 is really bad, one might even say incompetent if 2% is actually the Fed’s target.

It’s not clear there’s much evidence that 2.5% is noticably worse than 2% (plus there’s a long and complex history of the 2% target, which was only implemented secretly in the late 1990s and openly in 2012).

Does it matter if prices double in 36 years instead of 29 years? Would anyone really notice?

The main thing people (economists and ordinary citizens alike) care about is: is inflation high (above 5%) or not? The obsession over snap movements isn’t about the movements themselves, but whether this is a sign of a big increase that can’t be controlled (or can only be controlled by creating a recession).

2.5% annual inflation yields a USD half life of 27 years. The original scheme of 1913 assigned a nominal half life of 21 years, or 1 human generation.

I think this is a pretty sensible way to look at it. Generation length has increased in the intervening time too, from about 23 years in the 70s to about 30 years today.

I don’t necessarily disagree with this, but inflation expectations also matter a lot. And I fear they are becoming unanchored with a lax central bank too focused on unemployment numbers.

Stagflation-lite seems like a very real outcome at this point.

It looks like the Fed will have to raise interest rates soon as a matter of urgency

It has been clearly stated that the Fed will ‘look through’ the numbers.

same as the denial you suffer when you ‘look though’ your cheating spouse lies.

They have been looking at numbers above their target for 6 months so I assume they are very forgiving of the facts before their eyes.

Not Powell’s fault on denial. He probably learned it is a river in Africa and never looked back.

Did you trust the Fed before Powell? I sure didn’t. But, yes he is either carrying an agenda or willfully ignorant. Probably a combination of the two.

The thing is: inflation due to tariffs would not be the Fed’s faults. Inflation due to services IS the Fed’s fault. So…

They also willfully ignored services inflation spiking in 2021 for nine months, before they finally acknowledged it and began the planning the process of tightening.

The FED is accountable to nobody. So, they can sit there and just lie their asses and blame everybody and everything else, never taking accountability – which is what they do. The FED is a cancer upon society.

The Federal Reserve was created by CONGRESS and is accountable to Congress and that has always been the case. It is one of the best run central banks anywhere in the world.

The media in all forms is compromised like our current and past regimes, at just 4 percent of the worlds population and only 15 percent of the worlds factory, you are right, you better start making stuff because the rest of the world might be moving on from 2 trillion annual deficits, propaganda, fake news, etc ..

Wolf, good analysis., I just don’t get this clear eyed approach elsewhere and I’ve been doing this for a very long time. You won’t always be right but you’ve been spot on for awhile now.

This helps me formulate how I manage my portfolio and I pledge to increase my donation going forward.

Odd to me that Powell rejects the Inflation in services and focuses on tariffs ( which have been explained away as a one off thing)

Almost like he wants an excuse to lower rates. Or at least not fight against the “prevailing winds” toward lowering rates.

But why?

I thought he wanted his legacy to be more like Volcker and less like Burns?

I mean he’s filthy rich, and leaving the Fed soon anyway

Maybe he’s just calculated to himself that this is the path of least resistance

Seems like a decent enough guy, albeit with egregious mistakes on his resume

Wolf man – i keep looking for those durable goods prices that have fallen. Do I have to go look under some rocks? 🪨. I haven’t been able to find any, and I’ve been lookin’ real hard.

electronics such as laptops, used cars (a lot), sporting goods, lots of them. You don’t see them because you don’t WANT to see them because it might blow up your narrative.

I just bought a new 34″ inch LG monitor for $200. Prices for stuff like that have plummeted.

To be fair, some of the “decrease” in durable goods prices is actually quality improvements. So list prices for big ticket durables often don’t actually drop, you just get much bigger and better things for the same price (e.g. TVs).

I standby what I have said for years. The FED was wayyyy too late to raise rates (shouldn’t have lowered in the first place) and then way too quick to lower rates.

IMO, they made one big mistake in not noticing that the stable low inflation regime of 2009-2020 suddenly ended in mid 2021. They were about one year too late in raising the Fed funds rate, possibly because they were still worried about the pandemic.

It’s funny, because the Taylor rule that was developed in 1992 had been working pretty well, but when inflation started up on 2021 and the rule said to increase the rate, they decided to ignore it for the first time since 1992.

As of right now, the rule recommends a rate of around 4 percent, and hopefully the Fed will listen this time and keep it right around there.

Wolf, would you be interested in writing an article on the AI data center investment lately? Hundreds of billions if not trillions of dollars announced – that’s probably a big factor driving the gdp growth. Large companies going into a lot of debt (are they so confident it will pay off, or are they somehow off the hook in case their investments flop?), others lending these sums (who are the lenders, why are they so eager to risk such huge funds?), electricity supply side of that (is there corresponding buildout of gigawatts of power plants? Why don’t we see the renewables in this context, supposedly they should be cheaper?). So much juicy aspects to all of this IMO.

In terms of GDP growth, the actual investments being made are in “private fixed investments.”

https://wolfstreet.com/2025/09/25/what-slowdown-q2-gdp-growth-revised-up-to-the-hot-zone-of-3-8-on-stronger-consumer-spending-private-fixed-investment/

But also, these huge figures that you read about are just announcements of future investments, whether they may take place or not; and a lot of them are circular, where Nvidia for example “promises” to invest in a company which then “promises” to buy chips from Nvidia, or invest in another company that then buys chips from Nvidia, and so in this fantasy announcement world, we don’t fully understand how many times the same dollars are being recirculated as investments in these announcements. But the moneys involved, when they actually get spent, are still huge.

In terms of the data centers, I cover that in my construction spending reports. But that’s just the buildings, not the costs of the equipment that goes into the buildings, which can dwarf the building costs.

AI will stick around. It’s already everywhere, whether people want it or not. So far, the only people that are making money with it are cost cutters that replace humans with AI, and the companies that make the equipment and build the infrastructure. Consumers will not pay or not pay much for AI. So it’s going to be tough to make money with AI itself.

I expect huge amounts of corporate cash to just get burned off over time.

What federal policies can be implemented to reduce service inflation.