Liquidity now begins to drain out of the markets for the first time since the debt ceiling.

By Wolf Richter for WOLF STREET.

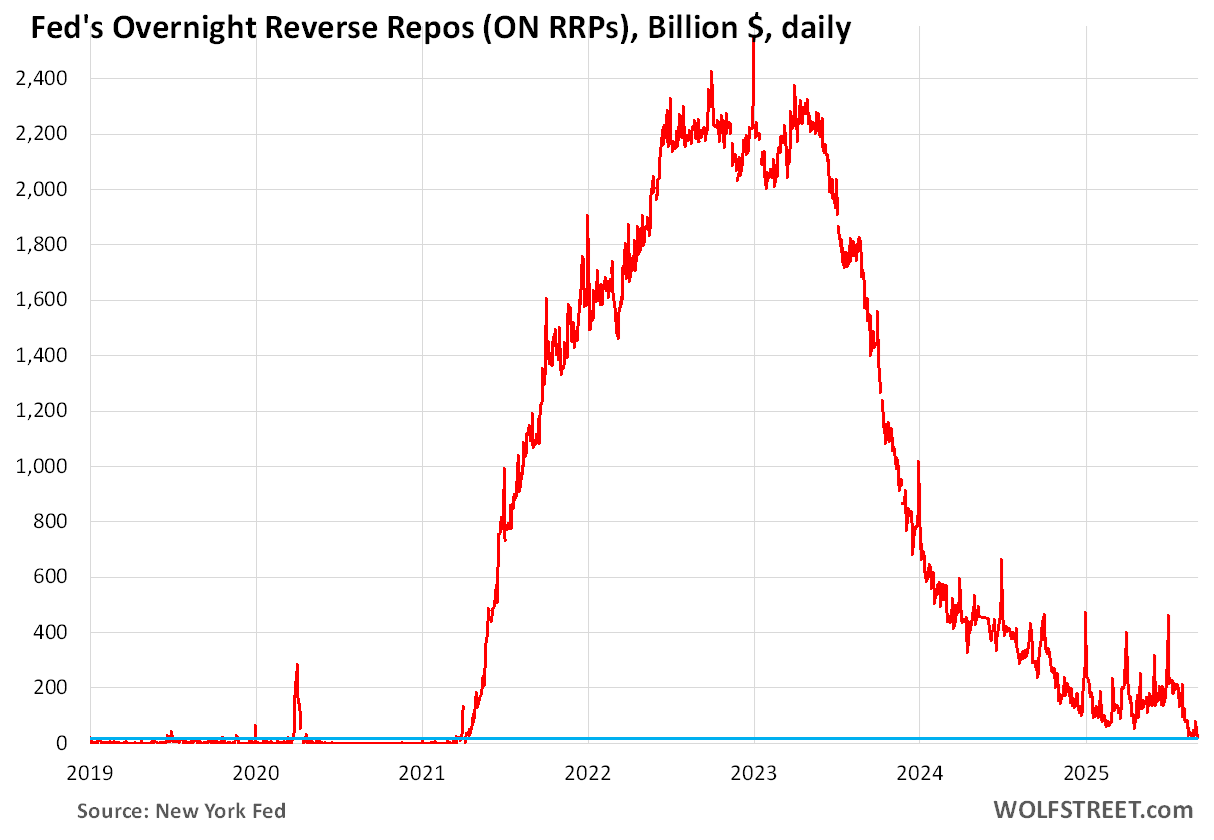

ON RRPs fell to $17.9 billion today – essentially near zero compared to the peak range of around $2.3 trillion that prevailed from May 2022 through June 2023 – and the lowest since early April 2021 when huge amounts of QE were beginning to wash into ON RRPs. In normal times, these Overnight Reverse Repurchase agreements are zero or near-zero. But QE wrecked the normal times. The blue line in the chart denotes the current near-zero level.

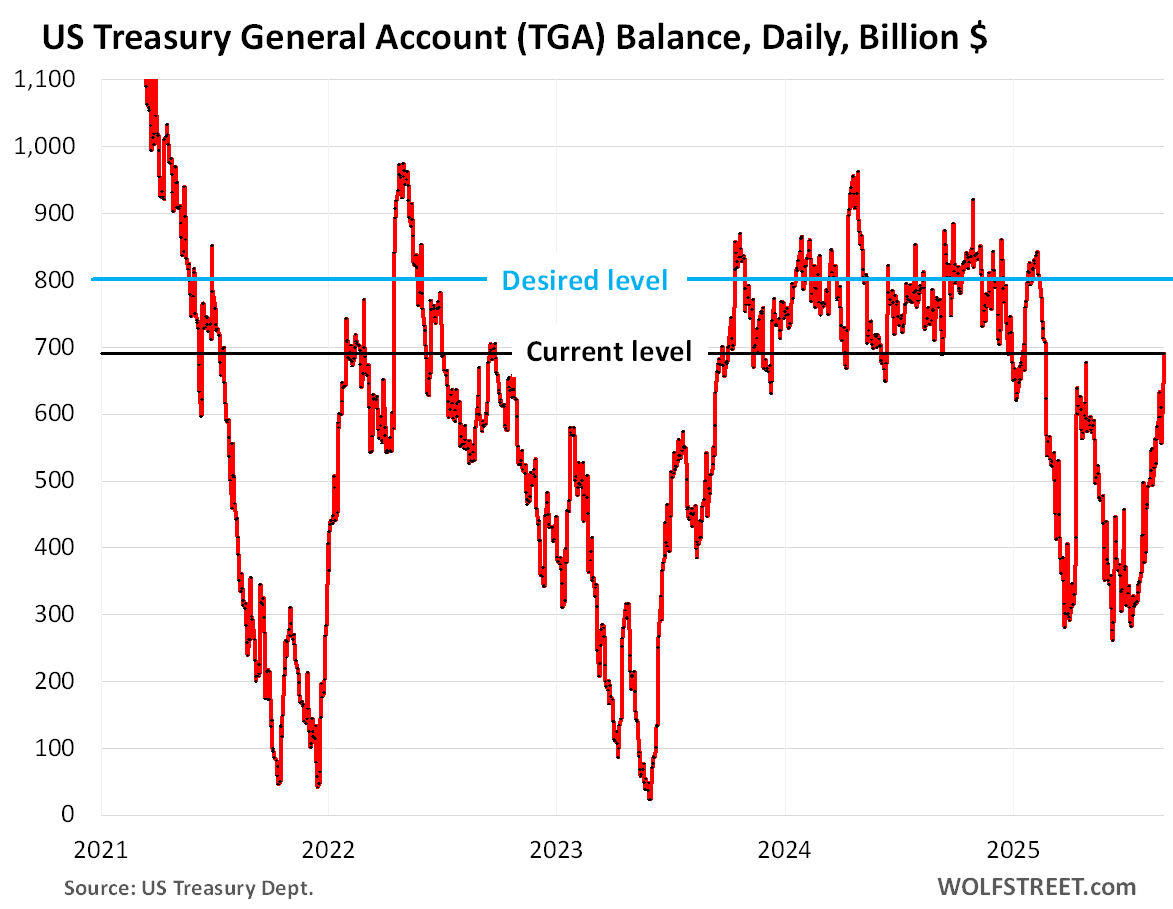

This has big implications for liquidity flows out of financial markets. ON RRPs, now being near zero, can no longer supply any noticeable amount of liquidity to the financial markets. But the government’s checking account, the Treasury General Account (TGA), is still getting refilled after the debt ceiling and is still draining liquidity out of the financial markets.

ON RRPs, refilling the TGA, and QT.

ON RRPs represent excess liquidity in the financial markets. They’re used mostly by money market funds to deposit extra cash at the Fed. They’re a liability on the Fed’s balance sheet, and the Fed currently pays 4.25% interest on ON RRPs. Money market funds have many other options, including Treasury securities with less than one year to run, commercial paper, and lending to the repo market. They will shift funds to where they can earn a little more and still satisfy their liquidity needs.

Other approved ON RRP counterparties are banks, government-sponsored enterprises (Fannie Mae, Freddie Mac, etc.), the Federal Home Loan Banks, etc.

The spikes in the chart above occurred at quarter-end and at year-end for window-dressing purposes.

When ON RRPs rise, they have the effect of draining liquidity from financial markets; and when they fall, they have the effect of adding liquidity to the financial markets.

ON RRPs have been falling since the end of the debt ceiling, thereby adding liquidity to the markets, just as the refilling of the TGA drained liquidity from the markets.

But ON RRPs are now near zero – where they are in normal times – and cannot fall much further, and cannot add much more liquidity to the market, so this influx of liquidity from ON RRPs into the markets has run its course. But the draining of liquidity via the refilling of the TGA continues.

The TGA is being refilled after the debt ceiling drained it down to $260 billion. Refilling the TGA back to the desired level of $800 billion requires that the Treasury Department sells even more Treasury securities at auctions than is needed to just cover the deficits and refinance maturing securities. Financial markets have to come up with this extra cash to absorb those Treasury securities needed to refill the TGA.

Refilling the TGA thereby drains liquidity from the markets. But the ON RRPs provided much of that liquidity. With ON RRPs now down to near-zero, the rest of the cash to refill the TGA back to $800 billion will come from the markets.

The TGA balance, at $690 billion at close of business on September 2, is still over $100 billion shy of the desired level, and as the TGA gets refilled to around $800 billion, those amounts get drained from the financial markets.

The massive surge of ON RRPs starting in 2021 was the result of the Fed’s QE that created so much liquidity that markets didn’t know what to do with it, and when it was even a little more profitable to deposit this liquidity at the Fed, they did, and ON RRPs ballooned to a range of $2.3 trillion back in 2022 through June 2023.

The subsequent plunge in ON RRPs is largely a result of the Fed’s QT, which has shed $2.3 trillion in assets from the balance sheet. Most of the QT has come out of ON RRPs so far – meaning that QT has so far only drained excess liquidity.

But ON RRPs are now near-zero, the additional liquidity needed to refill the TGA plus the additional QT will come out of reserves, which represent liquidity that banks have deposited at the Fed. Reserve balances were still at $3.22 trillion as of Thursday’s balance sheet. And they should now begin to decline under QT and the refilling of the TGA.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

good technical piece. thanks wolf

Ok, call me a moron…we all know what QT is.

You tell what TGA is in your SECOND paragraph:

So, what the heck is ON RRP’s??

I kinda-sorta figured it out in the first paragraph. Still not 100% sure.

How would you like it if I walked into the room and started speaking Russian with you?

1. Read the text below the first chart. Paragraphs 3-9 explain exactly what ON RRPs are, including their position on the Fed’s balance sheet, and what they do, and who uses them (if you need a more basic explanation, look it up).

2. Since many WOLF STREET readers know what ON RRPs are — there are countless articles on this site about them going back many years — I cannot clog up the first 2 paragraphs with a detailed explanation about ON RRPs for the readers who don’t know what they are. But I give that explanation in paragraphs 3-7 or so.

I also admit to zero knowledge of rrp’s(among many financial instruments),though read article and though will again feel the need to find a few rabbit holes to learn more.

I also a lot of times when still unsure let comments build for awhile and gain some insight there.

This is probably the most important dynamic now facing the economy. The S&P directly mirrored Fed liquidity from 2008 forward with QE. The rolling off of assets via QT is liquidity tightening that will ultimately break the everything bubble, especially as fiscal deficits become harder to fund. That’s why they’re backing BTC stable coins, to create another source of sterilized funding for the huge deficits. The casino remains open.

I trust you figured out the acronym ON RRP = Overnight Reverse Repurchase agreements. This is basically “parking” money for a few hours.

There is nothing to “figure out” about the acronym. The acronym is explained in the 1st paragraph. “Overnight Reverse Repurchase agreements” is exactly what the 1st paragraph says. You just have to read it.

What does this mean practically for the bond market? Sounds like more pressure towards higher yields because the market has to absorb the balance? Could the fed decide to reverse course on QT later this month? Sorry. I’m stupid.

Draining liquidity from the markets would take fuel away from the stock market.

“Could the fed decide to reverse course on QT later this month?”

No.

But several of the Fed chair candidates, including current Board member Christopher Waller and former Board member Kevin Warsh, have spoken out for increasing QT or against decreasing QT (Waller dissented when the pace of QT was reduced in June) and want to shift the Fed’s holdings from MBS and long-term notes and bonds to short-term T-bills. Even the rate cutters want to continue reducing the balance sheet.

1.) Goto Google

2.) In your search bar make sure “AI Mode” is enabled

3.) Enter this into the search bar “what are overnight reverse repurchase agreements”

You should see something like this:

An overnight reverse repurchase agreement (ON RRP) is a monetary policy tool used by the Federal Reserve (Fed) to set a floor on short-term interest rates. In this transaction, the Fed sells Treasury securities to eligible financial institutions, such as money market funds and banks, with an agreement to repurchase them the next day at a slightly higher price. This process absorbs excess short-term liquidity from the market, preventing short-term rates from falling below the Fed’s target range by providing these institutions a safe, short-term investment option.

Back to normal ON RRPs = good

Continuing to refill the TGA = bad, at least in the short term

What are the possible consequences? Is this just filling the coffers before the inevitable raising of the debt ceiling? Won’t it put upward pressure on interest rates? How does this impact Fed policy? I’m so confused.

Why?

TGA (Treasury General Account) is just the cash the federal government has at hand for day-to-day operations (absorbing tax incomes, expenditure of federal services). We need a substantial buffer to ensure unforeseen events do not immediately lead to shutdown of government services.

The TGA fluctuates by tens of billions of dollars at all times due to fluctuations in expenses and tax incomes. These days, every year it drops significantly as it covers the weeks or months congress takes to sign a new debt floor/ceiling. The months after sees a spike in debt issuing as simultaneously the expenses start getting paid by issuing new debt and the TGA starts to be refilled. This is spread out over the year to soften the blow to the banking system. This is less impactful than it might seem, as excess cash is build up in the period where the debt ceiling prevents issuing of new federal debt.

So no, thare are no unforseen or unexpected consequences of refilling the TGA. But yes, issuing new debt will affect interest rates as it would do in any environment where money has value. However, blaming TGA for this is like blaming your creditcard for charging you when you’re in the red. The problem is that we’re spending more money than we receive, not the vehicle through which we do that.

I think Mr. Naive is viewing the perpetually growing TGA size as a proxy for the perpetual US fiscal deficits and perpetually growing US fiscal debt.

Agreed that the TGA is just an interim funding/iquidity tool for the USG – but it exists and grows because the US G is a perpetual and growing debtor.

Does it push up long yields or only short yields?

$2.3 Trillion has been drained during QT, yet we’re just back to the starting point? That’s insane to reflect on. More QT is likely required to offset the years of excess before anything resembling a balanced market can occur too. Crazy.

The market cap of the S&P500 is over $50T. The total US housing market is valued around $50T.

Nvidia’s market capitalization has reached $4 trillion, making it larger than the GDP of many countries, including the United Kingdom and France, and it represents about 3.6% of the global GDP. If Nvidia were a country, it would rank as the fifth largest in terms of GDP, following the U.S., China, Germany, and Japan.

So $2.3 trillion is pocket change… a rounding error to all those 400+ Economic PhD’s at the Fed who gave us ZIRP, ZIRP, and more ZIRP.

But we need a rate cute?

That’s not how that works. The $2.3 trillion was newly created money and then newly destroyed money. That’s very different than the inflated price of an asset. During QE, newly created liquidity chases after assets in an endless loop, driving asset prices higher for a long time: when one of the Fed’s primary dealers sells the Fed $10 billion in Treasuries, they get $10 billion in newly created cash that they have to do something with. So they buy other assets, say more Treasury securities, so now the sellers of those Treasuries get the $10 billion in newly created cash and buy other assets with it, such as stocks, and the sellers of those stocks get the $10 billion an buy other others with it…. and it goes round and round, driving up asset prices as it goes. That’s how QE works. So now do that with $2.3 trillion. Or with the pandemic QE total, which was $4.8 trillion. And only part of that has been drained by now.

Market cap is not a good metric to compare with GDP. If you compare Nvidia revenue (165B trailing 12 month) against GDP those comparisons against other countries look a lot less impressive.

You are so right. I wish the commentary would stop comparing NVDIA’s market cap to GDP or other measures of revenue. If you want to compare market cap, do it to total wealth.

Air pockets and distortion aka bullish sentiment from bid ask spreads drove the total Us stock market valuation to 64.5 T as close of yesterday. I explain to my kids that debt is a fixed liabilities, except cash most assets float in value(mark to market) I understand cash changes value compared to other currencies. If bullish sentiment changes to bearish sentiment, emini change overnight valuation change in a blink of eye when cash markets open. Limit down mornings happen! Just on news.

” I explain to my kids that debt is a fixed liabilities, except cash – most assets float in value(mark to market).”

This.

Very much

This.

Enormous “goodwill” “assets” are a prime example of this.

1) Sociopathic CEO overpays for acquisition by $10 billion.

2) Suborned accountants *paid* by sociopathic CEO can’t (despite hair-pulling, life-threatening) attach that $10 billion to anything remotely resembling a real, hard asset that could be liquidated for anywhere near $10 billion.

3) But for accounting rules to “balance” that excess $10 billion has to be tied to an “asset”.

4) Behold…”goodwill”

5) Which more or less can evaporate (including to zero) in very short order once revenue/income results become bad enough…and new CEO decides to “reset”.

6) Instant multi-billion dollar write-down of “assets”.

7) Meanwhile, on the liability side…

8) Lenders – “Too bad your vapor-asset evaporated…pay me 100% of my money (loan liabilities).”

(Picture the restaurant arson in Goodfellas…)

Finally!

So, after reading this piece and all the comments, I still don’t have a clear sense of what effect this will have on rates, if any.

This ON RRP liquidity was pouring into the stock market and other places. That begins to end as of now. And it’s now beginning to drain out of the stock market and other places, taking some fuel away from the stock market.

Jim Hansen,

Very broadly speaking, as artifically supplied funds/liquidity (the Fed) are drained out of any market…the related interest rate faces upward pressure.

Because the Fed – that supplier of (artificial) buying interest/power is no longer there – so *new* lenders (liquidity suppliers) have to be induced into stepping into those shoes.

More or less by definition, they will only do so at a higher rate (otherwise, the Fed would not have needed to get involved in the first place trying to keep interest rates *down*).

Markets are dynamic and always in flux…so weird things can happen in the short term…but longer term, the interest rate pressure is upward.

Telegraph: Bond markets show world flirting with disaster…

LOL, these idiots at the Telegraph! Since when are 5% long-term yields a “disaster”?

Global investors are becoming increasingly skittish about public finances across the advanced world. Long-term bond yields are marching higher again.

At the time of writing, UK 30-year bond yields are at a 27-year high of 5.7pc. The UK faces the highest benchmark borrowing costs in the G7, at around 70 basis points above equivalent US rates.

But that is not to say the US is doing much better. With the exception of the short-lived “Treasury tantrum” in 2023, US 30-year rates have not been at their current level of 5.0pc in 18 years.

Similar problems abound elsewhere in the developed world. Japan, which only began issuing 30-year paper in 1999, is now paying record-high yields at this maturity, at 3.2pc. German 30-year debt costs are up too, at a 14-year high of 4.4pc.

Yields are just normalizing after 15 years of ZRIP.

But yes, 15 years of ZIRP have induced governments to engage in reckless fiscal policies — when money is free, why not borrow endlessly to deficit-spend? Those policies are now coming home to roost. ZIRP should have never been allowed to happen.

I like that Wolf, ZRIP as in Z-Rest In Peace.

When they all have 30 year bonds at 2%?

Bad planning, I say…

It’s not just them. I saw CNN describe current rates as “painfully high.”

Tell it to the 10 year. Effectively bounded between 4 and 4.5 for 3 years now. It didn’t feel painfully high in ’22 and it sure doesn’t now

Dear Wolf,

if 5 % isn’t a problem, what number could be a problem? (7 %, 10 %, ?)

Thank you

A 30-year government bond yield should be about 3 percentage points above the expected inflation rate over the longer term.

If I expect CPI inflation to be 3.5% longer term on average, then the 30-year bond yield begins to look endurable at 6%-plus, given the risks involved in holding 30-year debt.

The risk is that inflation under a dovish central bank is allowed to spiral up to 10% for a while, and holders of 30-year bonds take a huge licking.

The way to get long-term yields down is to have a hawkish central bank that keeps short-term rates high and keeps trimming its balance sheet, and a government that reduces the deficit to manageable levels.

It’s moronic to expect low long-term interest rates while the government blows out the deficit, while inflation accelerates, and while the central bank cuts rates into accelerating inflation. In this scenario, long-term bond investors should demand an arm and a leg before buying 30-year bonds. I don’t understand why they don’t.

Wolf, what is the basis for the 3% above inflation? Is this a historical trend? Respectfully, I am very skeptical of that spread even as a “rule of thumb” because the spread is based on a number of factors that indicate in your comment.

Separately, how much of the 30-yr bond purchases are from 401k retirement target funds like those by Vanguard et al that are just on autopilot?

last year Gen-X married to Boomer here.

reason I’m buying 30 year at 5% and TVAs slightly higher is these bonds will maintain our purchasing power over decades if inflation averages 4-5%.

You address it later but, semi-jokingly…

“Since when are 5% long-term yields a “disaster”?

Since the Federal debt is double what it was the *last time* long term yields were allowed to be 5% and the country survived.

As I said, you address it later – but the initial quote was too Establishment to let pass.

https://wolfstreet.com/2025/08/28/us-governments-fiscal-mess-interest-payments-on-the-treasury-debt-interest-rates-tax-receipts-and-debt-to-gdp-ratio-q2-2025/

Wolf,

It is exciting to see ONRPP finally getting to these levels (I really thought/hoped you might be writing this article a year ago!). Do we have any sense of what banks will want to part with their reserve balances? I imagine the answer is higher rates, but have been surprised how tightly they have clung their $3T(ish) throughout QT. Is there something I am missing in terms of why this is the reserves banks feel comfortable with? Do we have any sense of much (additional) interest they will want as they are now called upon to start reducing these balance?

-b

**Summary (25 words):**

ON RRPs hit near-zero, ending liquidity inflow; TGA refilling continues draining markets. Fed QT now taps bank reserves, tightening financial conditions further.

**Implication for U.S. Stock Market:**

This signals a shift from excess liquidity to tightening. With ON RRPs depleted and TGA refilling ongoing, markets lose a key liquidity buffer. As the Fed’s quantitative tightening (QT) begins drawing from bank reserves, risk assets like equities may face headwinds—especially growth stocks sensitive to funding conditions. Expect increased volatility, reduced momentum, and heightened sensitivity to macro data and Fed signals.

“Refilling the TGA back to the desired level of $800 billion requires that the Treasury Department sells even more Treasury securities at auctions than is needed to just cover the deficits and refinance maturing securities. Financial markets have to come up with this extra cash to absorb those Treasury securities needed to refill the TGA.

…

the additional liquidity needed to refill the TGA plus the additional QT will come out of reserves, which represent liquidity that banks have deposited at the Fed.”

Is it just the banks moving from easy overnight money into buying government bonds, or will various cash holders (money market funds and insurance cos.) demand higher interest rates from the government bonds before they will sell equites and buy bonds?

Definition on web: “Commercial paper (CP) is an unsecured, short-term debt instrument issued by large, creditworthy corporations to meet their immediate and short-term financial needs.”

This is what Mr. Wolf writes is something money market funds are buying. Sounds like corporations are running out of cash.

“Sounds like corporations are running out of cash.”

No. And commercial paper has been around forever and money market funds have always been the primary buyers. Only Treasury money market funds don’t buy it; they only buy Treasuries. Prime money market funds hold a substantial portion of their assets in commercial paper.

A couple of questions about the mechanics…

If the Fed is paying 4.25 on ONRRP now, what is the Fed currently paying on reserves held at the Fed?

When the Fed alters the rates to encourage a drop in ON RRPs, do the banks and other eligible parties make a move or is there an automatic procedure?

Do the banks say “we will take those securities back” ? Do they have a choice? Is that decision made each day on the over nights by the parties?

If the Fed is making ON RRPs unattractive at 4.25, they must be paying out more to the parties involved to unwrap the ON RRPs? Right?

Thanks

1. 4.40%

2. The rate that the Fed pays on ON RRPs and the rate that the Fed pays on reserves are among the 5 policy rates that the FOMC decides on at every meeting. Currently, these 5 rates are between 4.25% and 4.50%. The FOMC generally changes those rates at the same time by the same amount. If it cuts by 25 basis point in September, all five of those rates will be cut by 25 basis points.

I always itemize those five rates in my FOMC rate-decision articles. Here is the last one, scroll down a little:

https://wolfstreet.com/2025/07/30/the-fed-torn-by-two-governor-dissents-sticks-to-wait-and-see-keeps-rates-at-4-25-4-50-frets-about-uncertainty/

So banks could but don’t use ON RRPs (4.25%) because they make more money on their reserves (4.40%).

3. “Do the banks say “we will take those securities back”” In terms of reserves, there are no securities involved. Reserves are just like a high-yield savings account at the Fed.

4. The Fed is not making ON RRPs “unattractive.” But market instruments are paying slightly more, and there isn’t enough excess liquidity out there to plow into a slightly inferior product.

Thanks so much for the explanations…

you say..

““Do the banks say “we will take those securities back”” In terms of reserves, there are no securities involved. Reserves are just like a high-yield savings account at the Fed.”

But there are securities involved in ON RRPs, correct?

Correct. They’re overnight contracts (repurchase agreements), where cash is exchanged against collateral. The contracts expire the next business day, and in this case, the money market fund gets the cash back plus interest and the Fed gets the security back. They can do this every day. If they don’t the balances fall.

Wolf-

How do the decreases in ON RRP’s, and the decreases in interest-bearing bank reserve deposits with the Fed that you mention, impact on the Fed’s annual cash remittance to the US Treasury, if at all? It seems that the Fed’s interest payed would go down, but I assume that interest earned will drop too…

Is this a step toward returning to annual remittances to Treasury?

Thank you.

The Fed pays interest on both of them. So declining short-term rates and declining balances of reserves and ON RRPs dramatically reduce the Fed’s expenses and losses. The worst year was 2023 when the Fed lost $114 billion. In 2024, the loss declined to $78 billion. For 2025, the loss may be less than $35 billion. In 2026, with a few rate cuts and continued QT, the Fed might break even or make a small profit.

https://wolfstreet.com/2025/03/21/feds-operating-losses-declined-to-78-billion-in-2024-unrealized-losses-rose-to-1-06-trillion/

Mr. Richter,

“The worst year was 2023 when the Fed lost $114 billion. In 2024, the loss declined to $78 billion. For 2025, the loss may be less than $35 billion. In 2026, with a few rate cuts and continued QT, the Fed might break even or make a small profit.”

Three questions:

Any thoughts on a potential resurgence of inflation, a reversal of rate cuts/expectations and a potential resurgence (and acceleration?) in the Fed’s Operating losses? I know Fed Operating losses are just an accounting entry, but these Operating losses must be an indication (a cancer) of something?

Second, as the Fed’s Operating losses are somewhat treated as a nothing burger, what’s the impetus for the Fed to hold down their operating costs and spending?

Finally, apparently there’s a manual out there for central bank accounting and you even looked at it (but it gave you a headache)……………..ok, I’m curious, who wrote the manual?

Thanks much and have a great day!

here is the “Financial Accounting Manual for Federal Reserve Banks” updated in May. It covers the 12 regional FRBs. The 12 FRBs are consolidated to form the total balance sheet of the Fed.

https://www.federalreserve.gov/aboutthefed/files/bstfinaccountingmanual.pdf

Is the ~$100 billion difference between where the TGA is now and where it needs to be a large enough number to meaningfully impact markets?

Is that a “large” number, especially if the refilling is paced over a few months?

O yeah~ Liquidity creates bullish sentiment and lack of liquidity creates bearish sentiment.

Thanks Wolf! The article was great and educational :)

@wolf

Is refilling the TGA really draining liquidity from the market or changing the viscosity of flows (or some such, I don’t dare say velocity). Likely, in net terms there is a reduction.

In a gods eye, there is no difference between a treasury note and an equivalent value pile of dollars. To you and me there absolutely is, but for large entities in the “market”, I am sure they can do all sorts of interesting things with the treasuries they have that allows them to earn more than what .fed pays.

Great to finally read the article where this hits ~0!

When the money market funds pull their money from the overnight repo’s and the banks pull out money from their FED accounts ( reserves) , does the FED sell an asset on their balance sheet to fund the cash transfers above. Or what mechanically happens to make assets = liabilities + capital and be in balance.

So the cause and effect is kind of the other way around. When the Fed sheds assets, that reduces liquidity which reduces either reserves or ON RRPs. Now that ON RRPs are near-zero, it will come out of reserves. Reserves are bank cash. Banks get this cash from their customers (deposits). So when the customers in the banking system buy bonds that the Fed sheds, they reduce the cash in their bank/brokerage accounts, which reduces the cash that banks have on deposit at the Fed.

The Fed does not have a cash account. Instead, they create cash when they buy something and destroy cash when they get paid for something. So regular accounting rules don’t work because in normal accounting, sooner or later, every transaction goes through the cash account. There is a manual out there for central bank accounting, and I even looked at it, LOL. It gave me a headache.

Wolf,

Is bank reserves at on the balance sheet entirely correlated with when “the customers in the banking system buy bonds that the Fed sheds” reducing the cash in their accounts? I thought (perhaps wrongly) that the reserve levels were to some extent a decision made by the banks as to how much money the wanted super liquid (vs loaning out, buying notes, giving back to shareholders, etc). If so, and if banks have strong opinions about their reserve levels, wouldn’t the banks come up with this money being withdrawn other ways rather than reducing their reserve balances?

If the ON RRP’s are being drained & liquidity is being siphoned from the financial markets how long will it take to affect these markets? I read that the total market cap of the US equities is $67 trillion. This liquidity drain seems small by comparison?