And to top it off: cancellations of pending sales rose to a record rate in July.

By Wolf Richter for WOLF STREET.

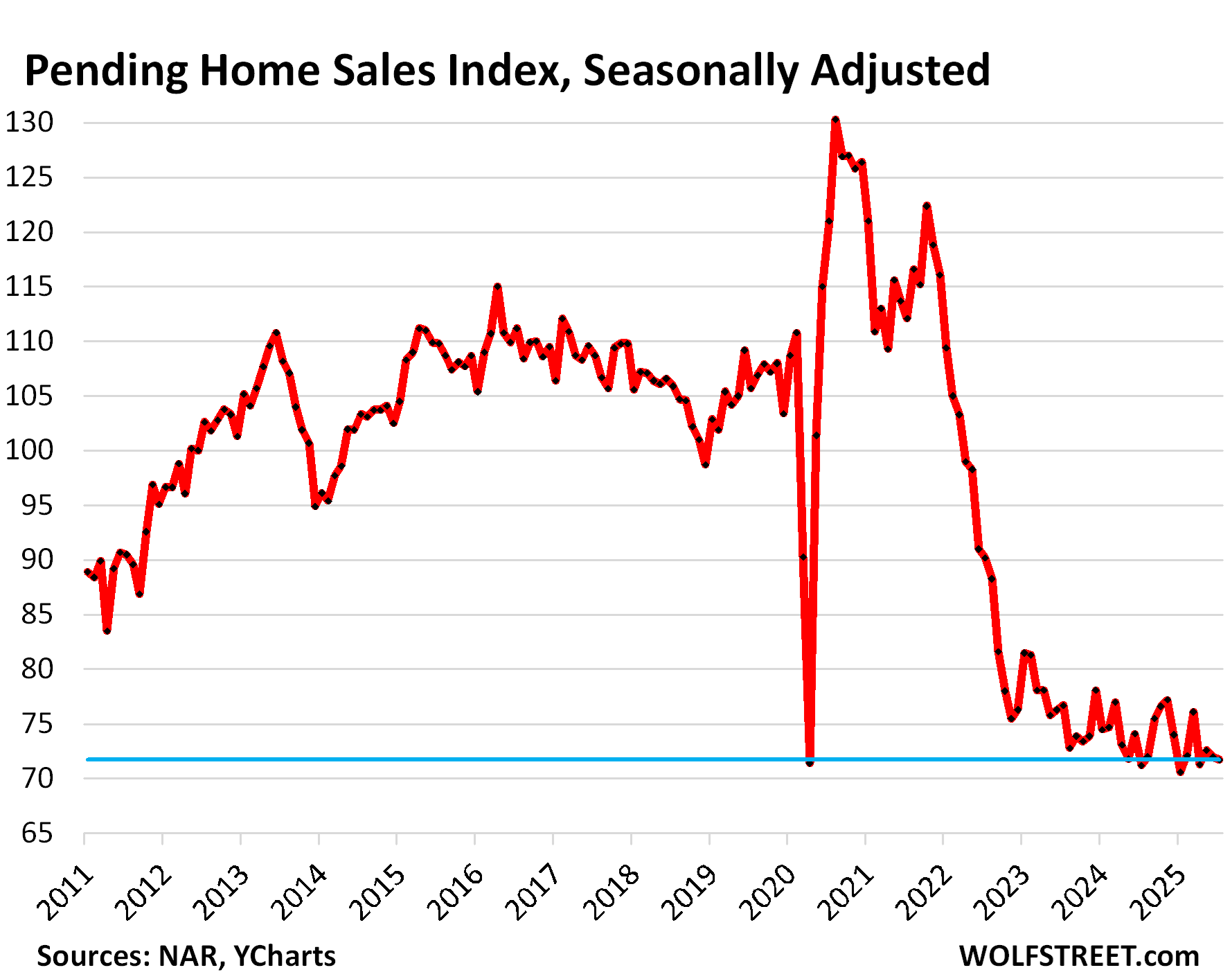

Demand in the housing market sagged further: Pending home sales dropped by 0.4% in July from June, seasonally adjusted. They have now spent nearly three years crawling along, or setting, record lows, according to data going back to 2010 from the National Association of Realtors today (historic data in the chart via YCharts):

It’s even worse: the cancellation rate. Pending sales are based on contract signings and track deals that haven’t closed yet and could still get canceled because buyers cannot afford or even get homeowner’s insurance, or for other reasons. Signed contracts that then get cancelled are included in the pending sales here, but are not included in closed sales reported later.

Alas, Redfin reported that in July, 58,000 pending sales were canceled, amounting to 15.3% of all pending sales, the highest rate for any July in Redfin’s data going back to 2017

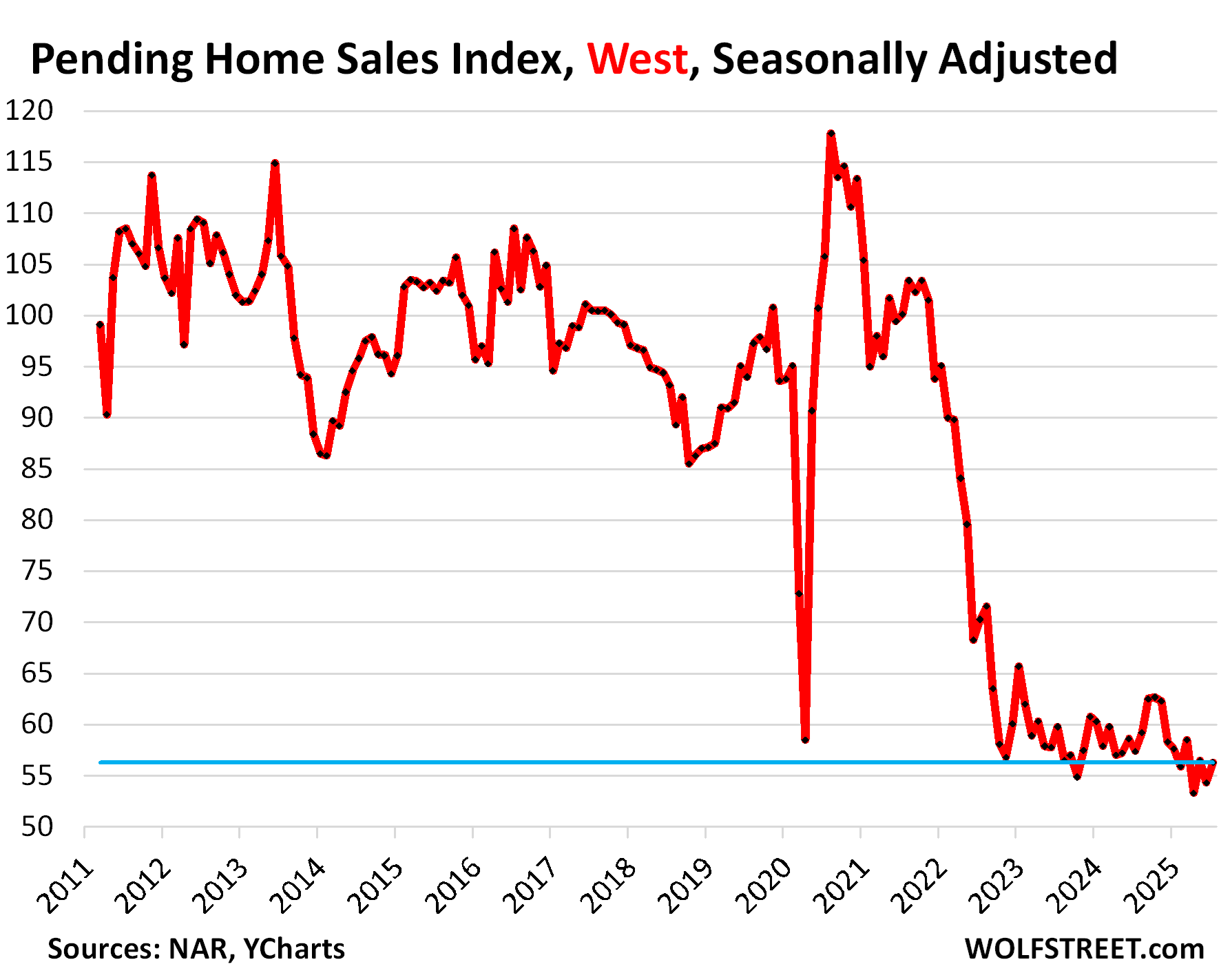

Pending sales in all regions near record lows. Pending sales fell sharply in the Midwest, but also declined in the South and Northeast. The West was the only region where pending sales rose. Pending sales remained near record lows in all four regions.

Pending sales of existing homes in the US, compared to the Julys in prior years:

- 2024: +0.7%

- 2023: -6.5%

- 2022: -21%

- 2021: -36%

- 2020: -41%

- 2019: -32%.

The Buyers’ Strike continues because prices are too high after shooting up by 50% or more within 2-3 years. Those prices no longer make economic sense.

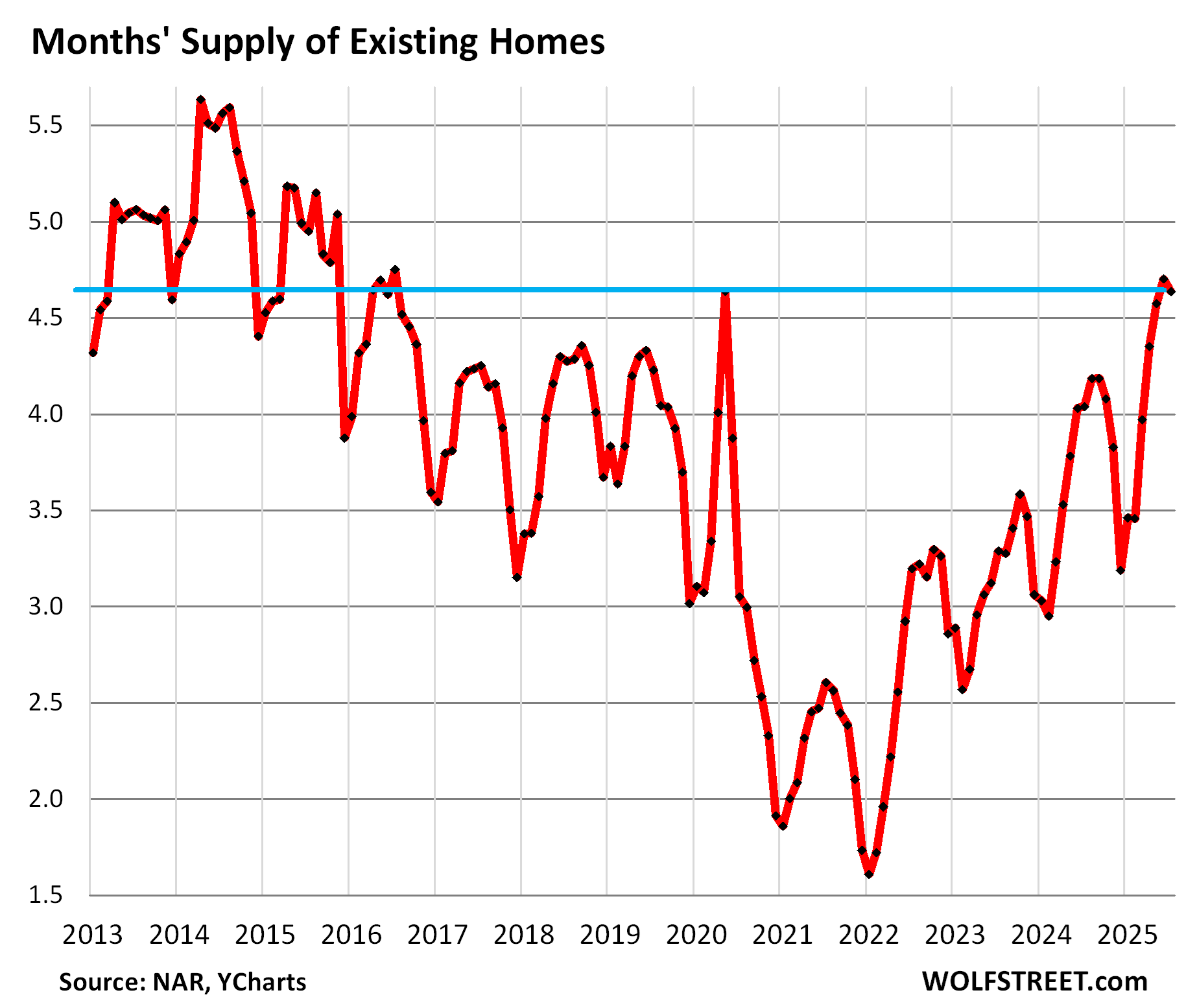

While inventory surged. This plunge in demand coincides with surging inventories of existing homes for sale – despite large waves of delistings by frustrated sellers – leading to the most supply since July 2016 over the past three months, along with May 2020.

Split out by single-family homes and condos: Supply of single family homes rose to 4.5 months while supply of condos has been over 6 months since April, the highest since 2012 at the end of the Housing Bust. Here is the combined supply:

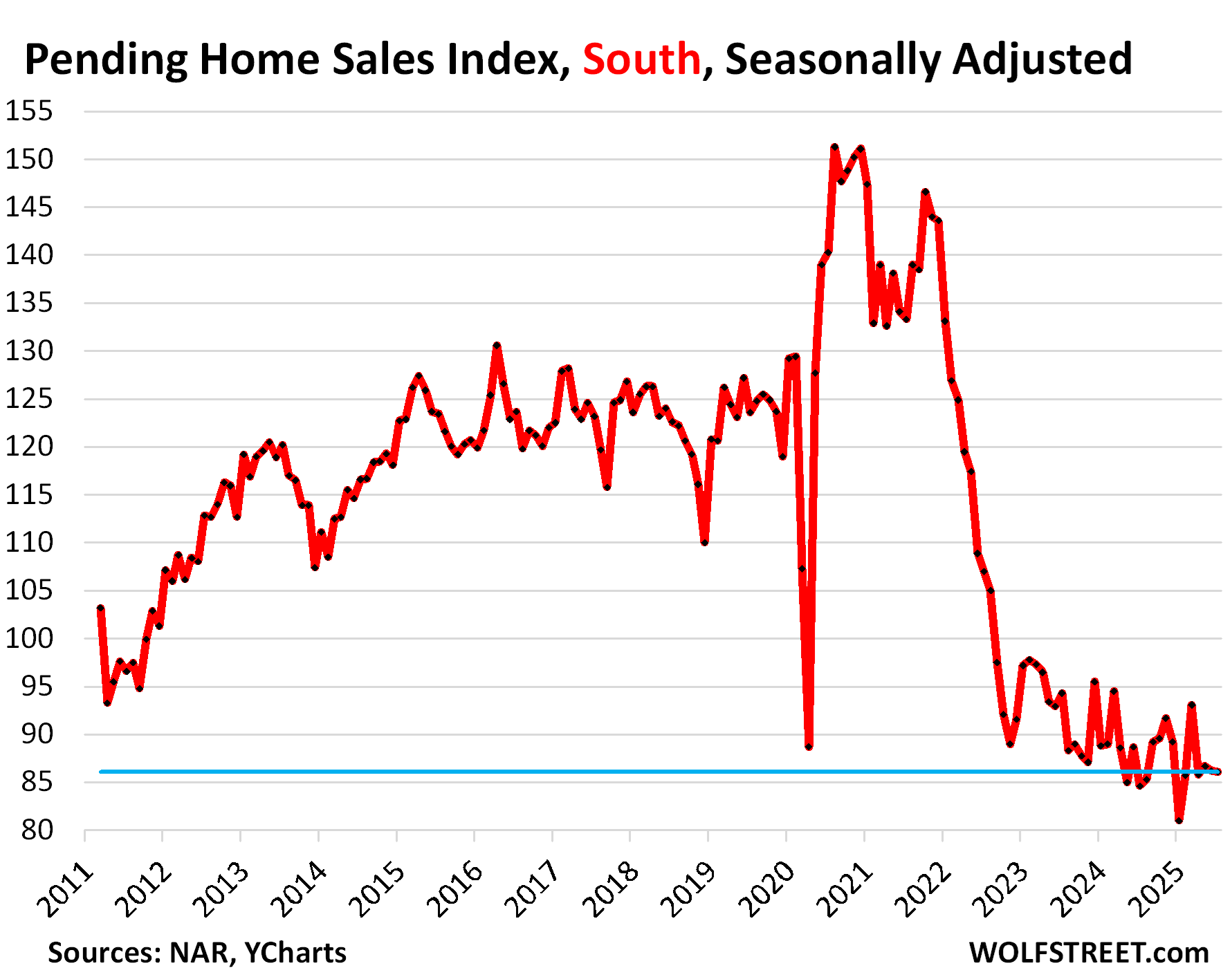

In the South, pending sales dipped 0.1% month-to-month, seasonally adjusted.

A map of the four Census Regions is posted in the comments below.

Compared to the Julys of prior years:

- 2024: +1.8%

- 2023: -9%

- 2020: -39%

- 2019: -30%

But inventories surged across the South.

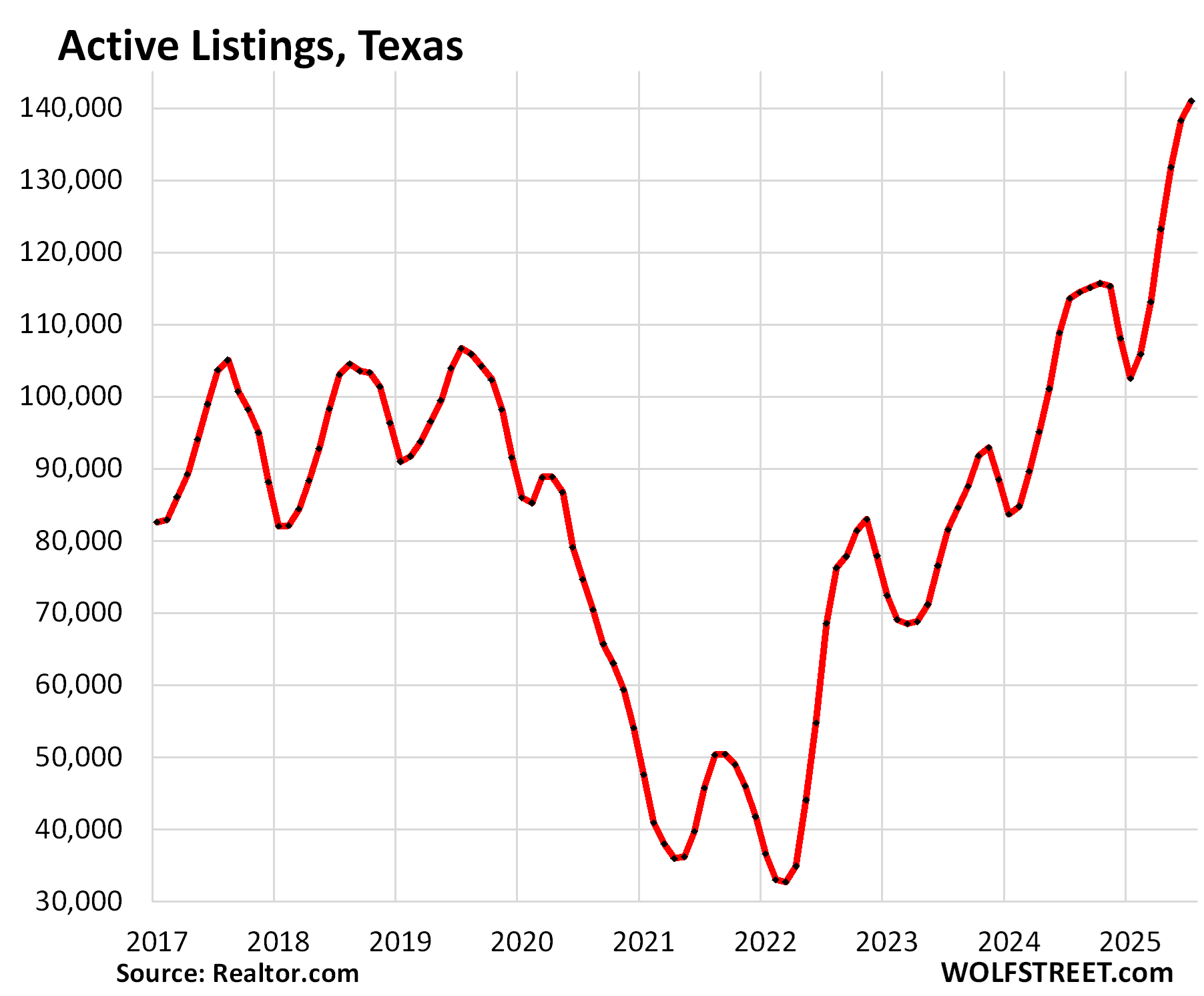

In Texas, inventory of existing homes for sale in July jumped by 24% year-over-year, and by 32% from July 2019, to the highest in at least the decade of data from Realtor.com (we discussed the inventories of the big metros in Texas here).

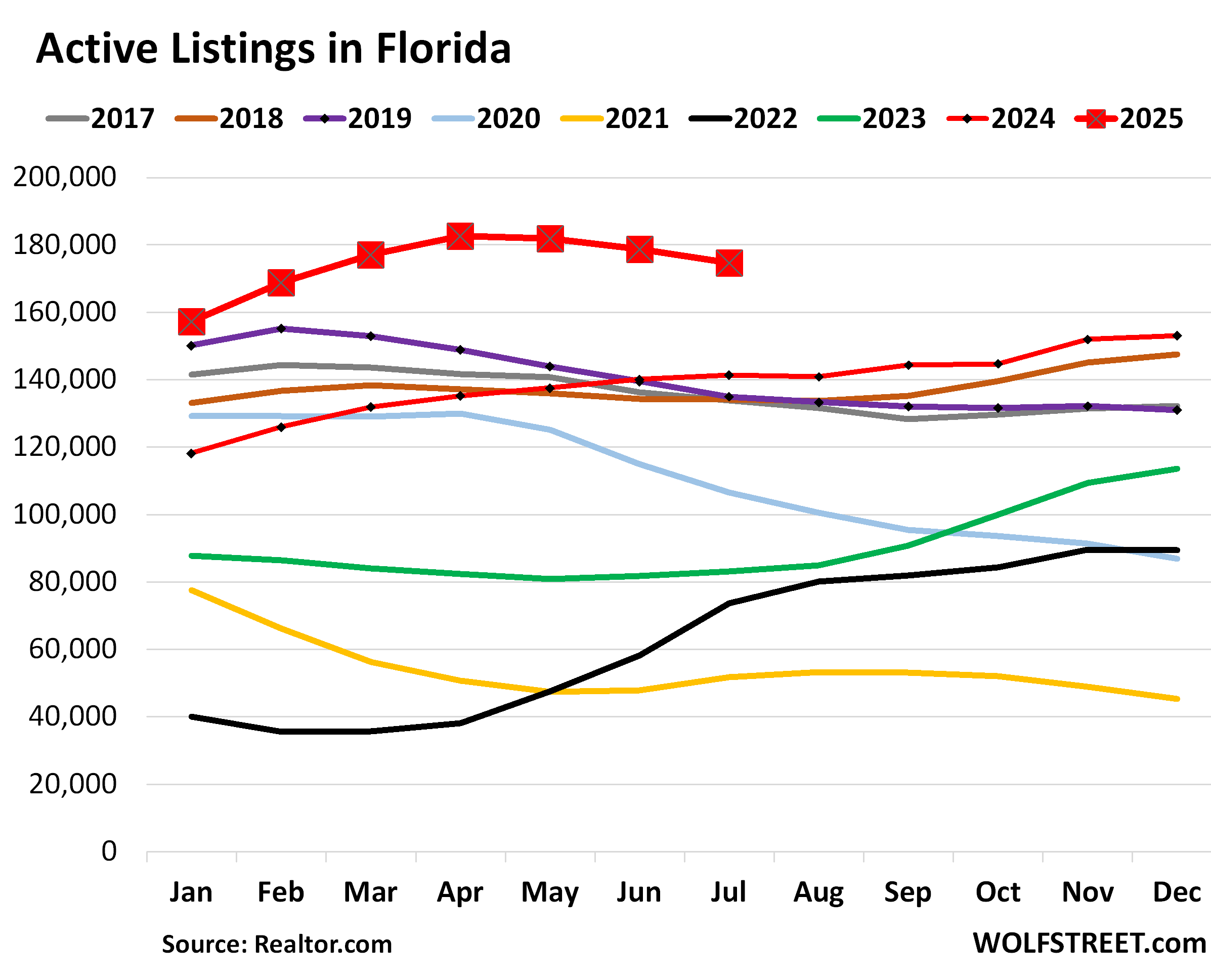

In Florida, active listings in July jumped by 23% year-over-year, and by 29% from July 2019, according to data from Realtor.com (we discussed Florida’s by-metro inventories and days on the market here):

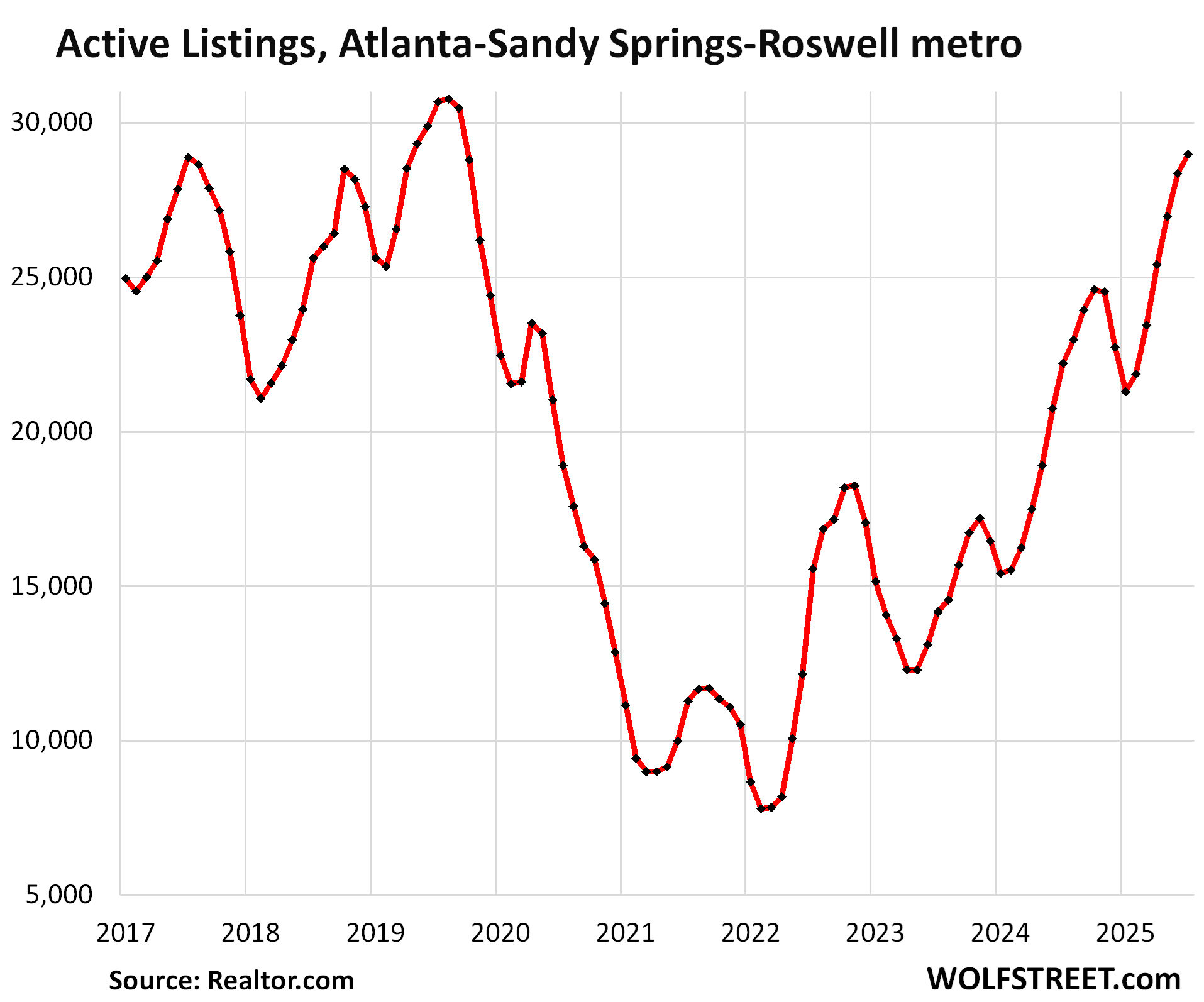

And for example, in the Atlanta metropolitan area, active listings spiked by 31% year-over-year in July:

In the West, pending sales rose by 3.7% in July from June, which had been the second-lowest on record.

Compared to the Julys of prior years:

- 2024: -1.9%

- 2023: -6%

- 2020: -47%

- 2019: -40%

Active listings in the West have also been surging.

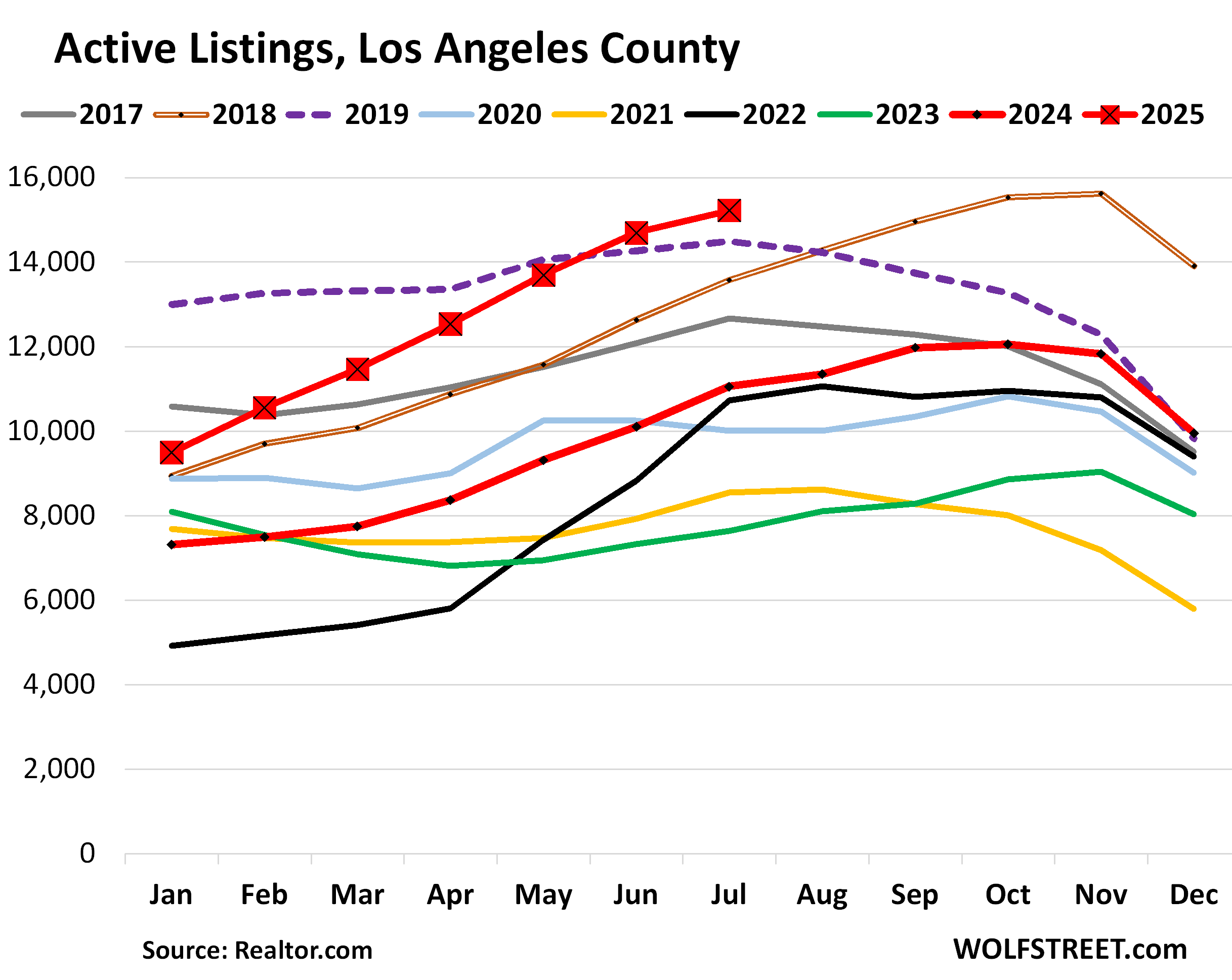

In Los Angeles County and in the San Francisco metropolitan area, active listings reached the highest level for any July in the decade of data from Realtor.com (discussion of inventories of in biggest markets of California is here).

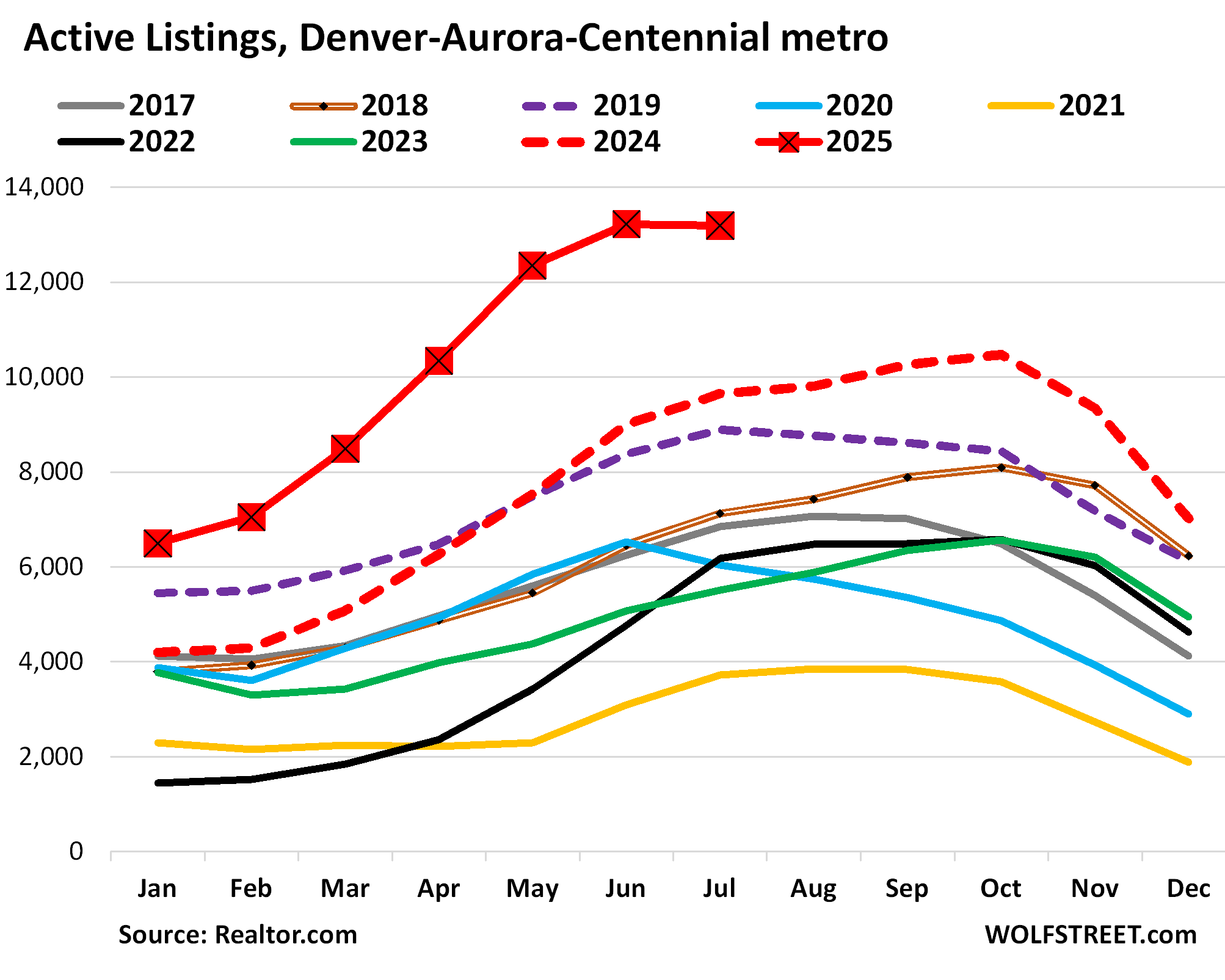

In other markets in the West, inventories have also surged, reaching the highest for any July in the decade of data in the metros of Denver, Seattle, Salt Lake City, Phoenix, Tucson, Portland, and Las Vegas (discussion by metro here).

For example, active listings in the Denver-Aurora-Centennial metro are up by 48% from July 2019 (dotted purple), and along with June the most in the decade of data from Realtor.com.

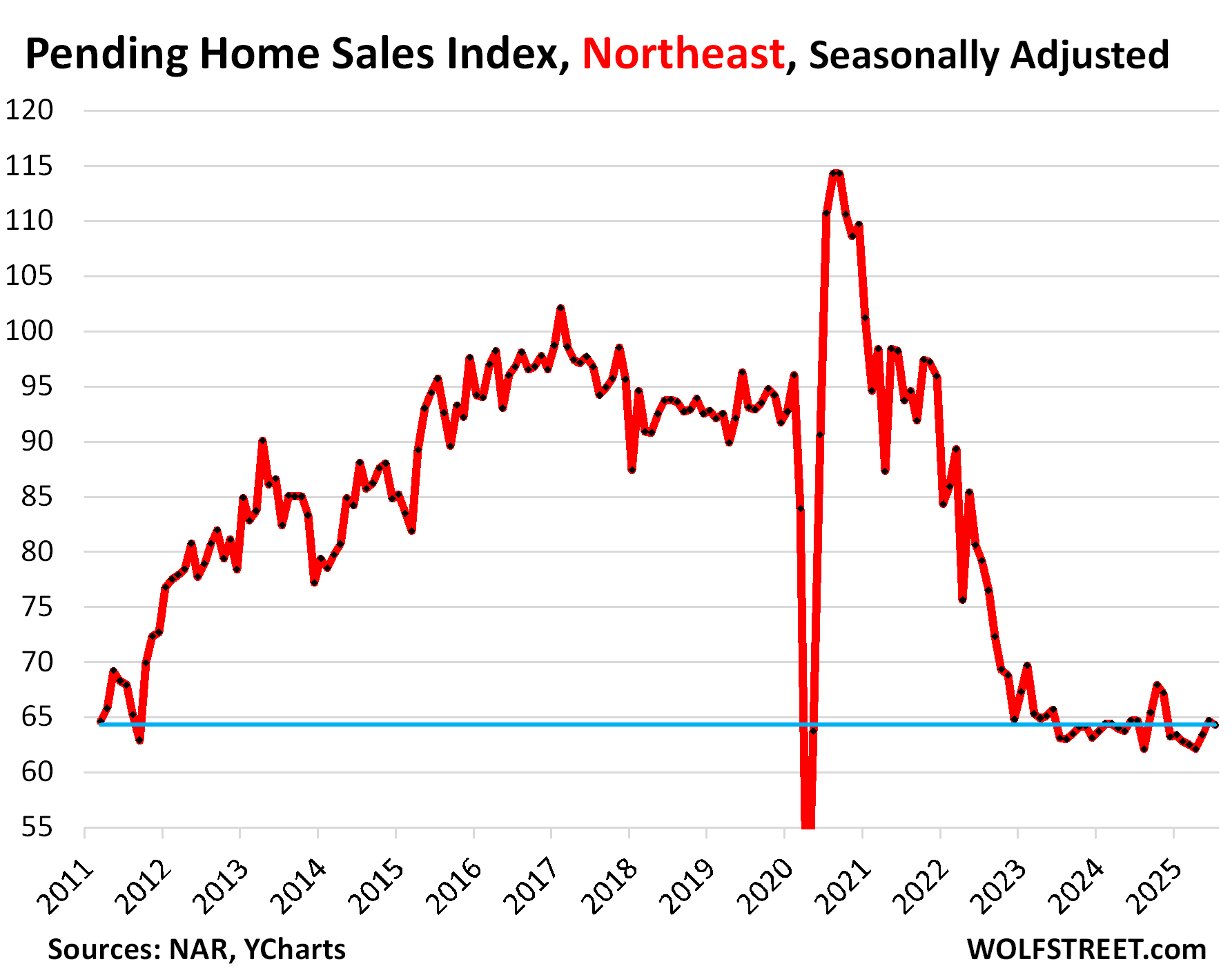

In the Northeast, pending sales dipped by 0.6% month-to-month, seasonally adjusted.

Compared to the Julys of prior years:

- 2024: -0.6%

- 2023: -2%

- 2020: -42%

- 2019: -31%

In the Northeast, inventories have also grown, but remain tighter than in other parts of the US.

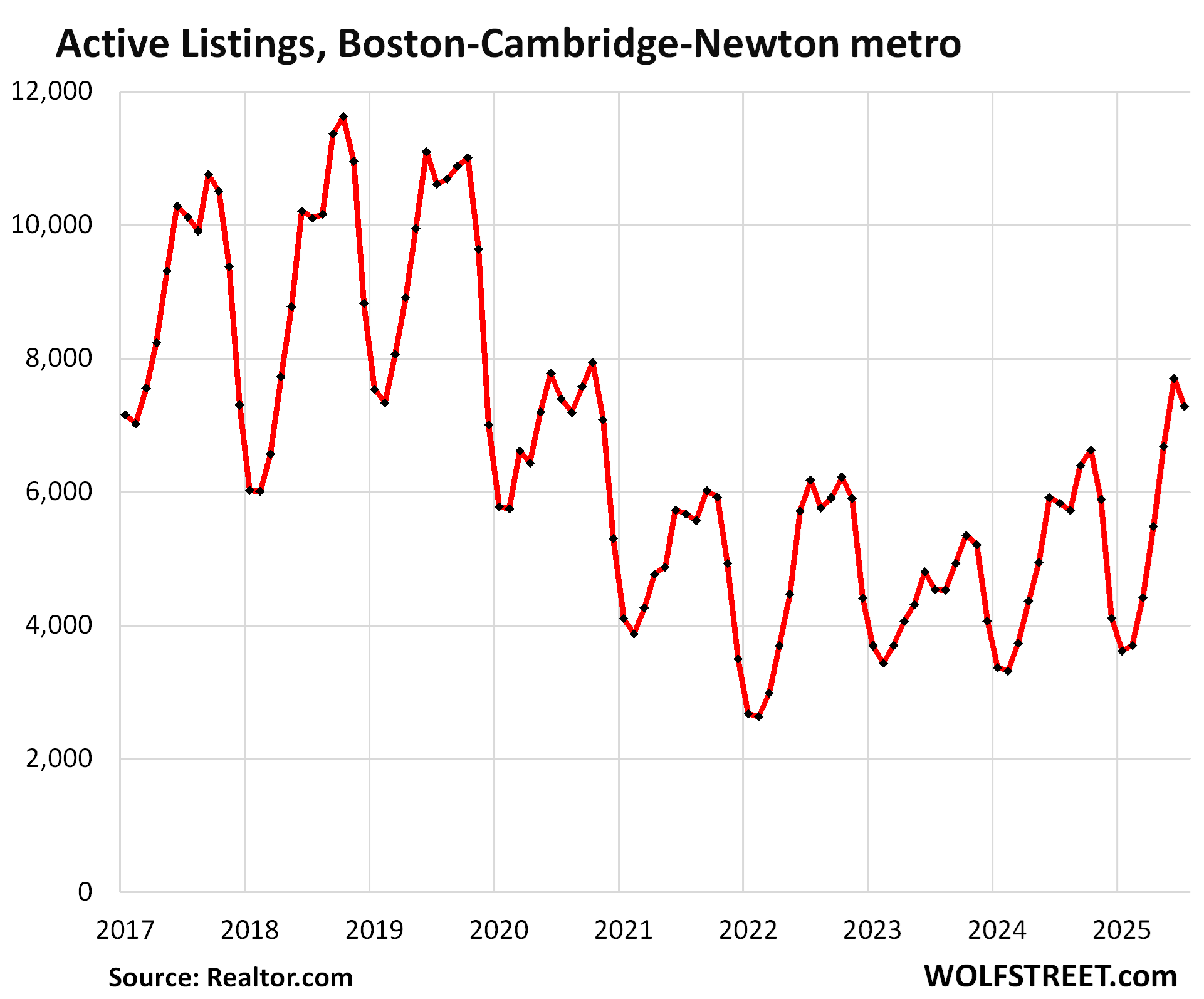

For example, in the Boston-Cambridge-Newton metro, inventory jumped by 25% year-over-year and by 61% from July 2023, to be roughly level with July 2020, but well below the prepandemic years.

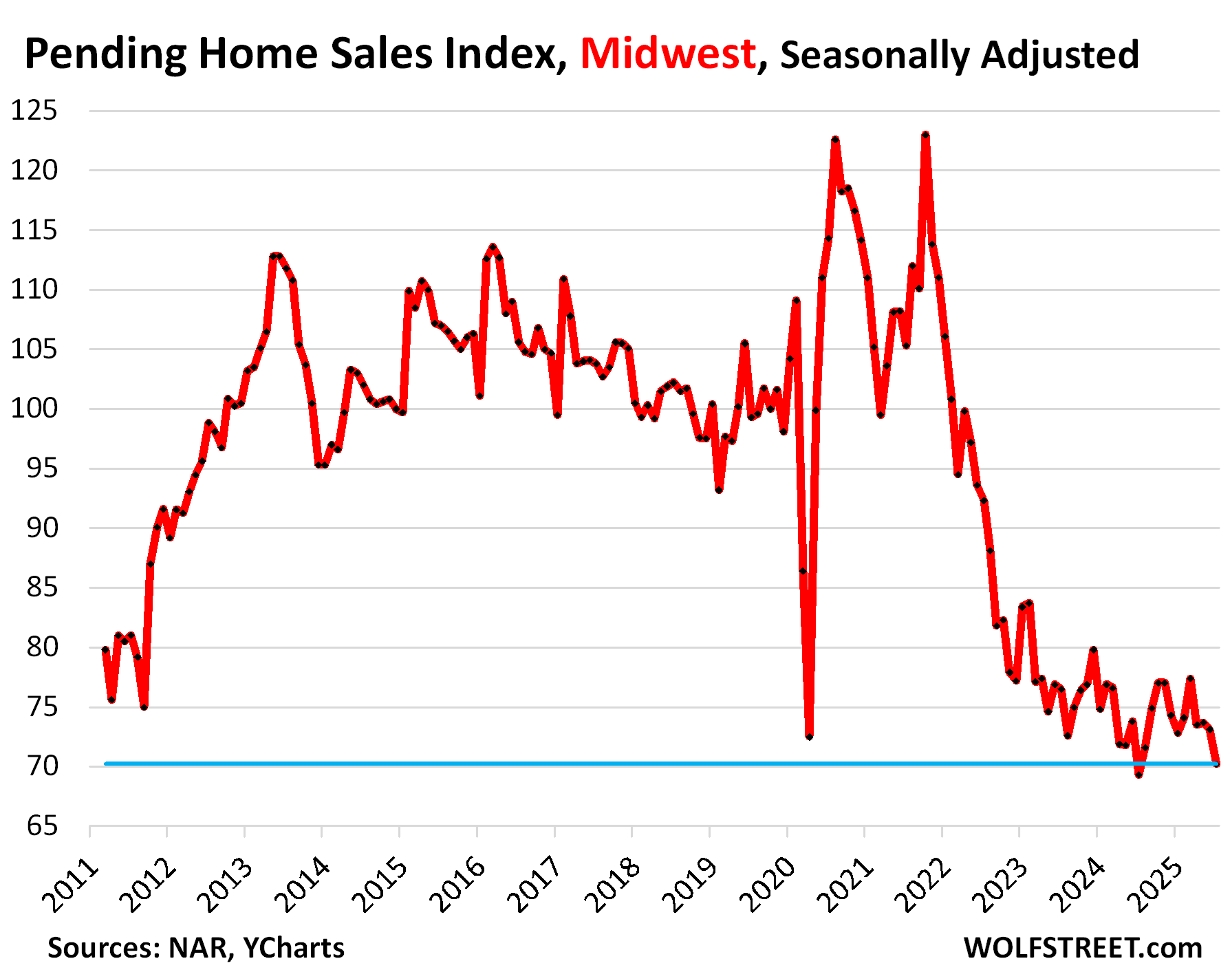

In the Midwest, pending sales dropped by 4.0% in July from June, seasonally adjusted, to the second-lowest sales in the data going back to 2010.

The record low had been July 2024, and compared to this record low, sales were 1.3% higher.

Compared to the Julys of prior years:

- 2024: +1.3%

- 2023: -8%

- 2020: -39%

- 2019: -29%

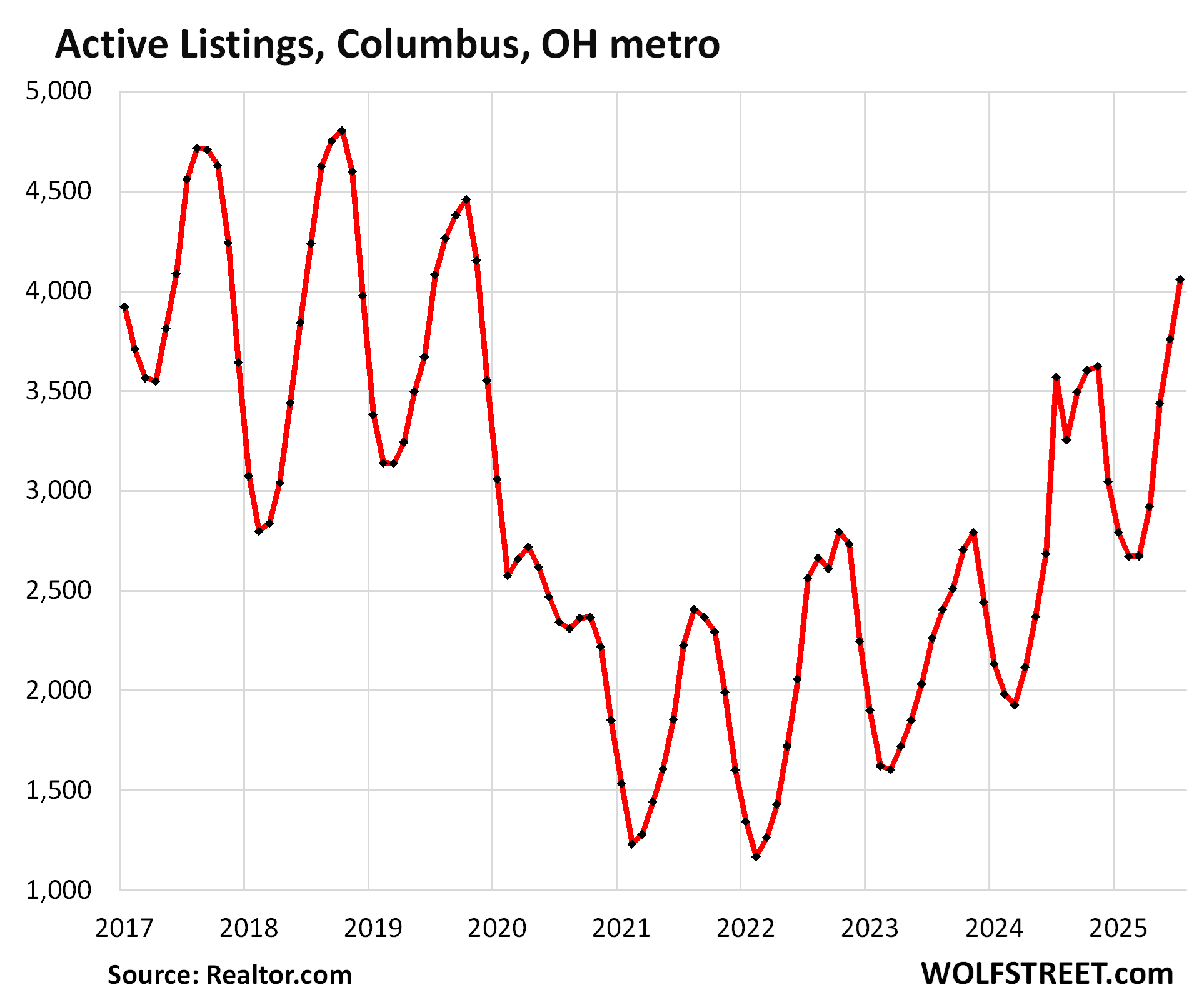

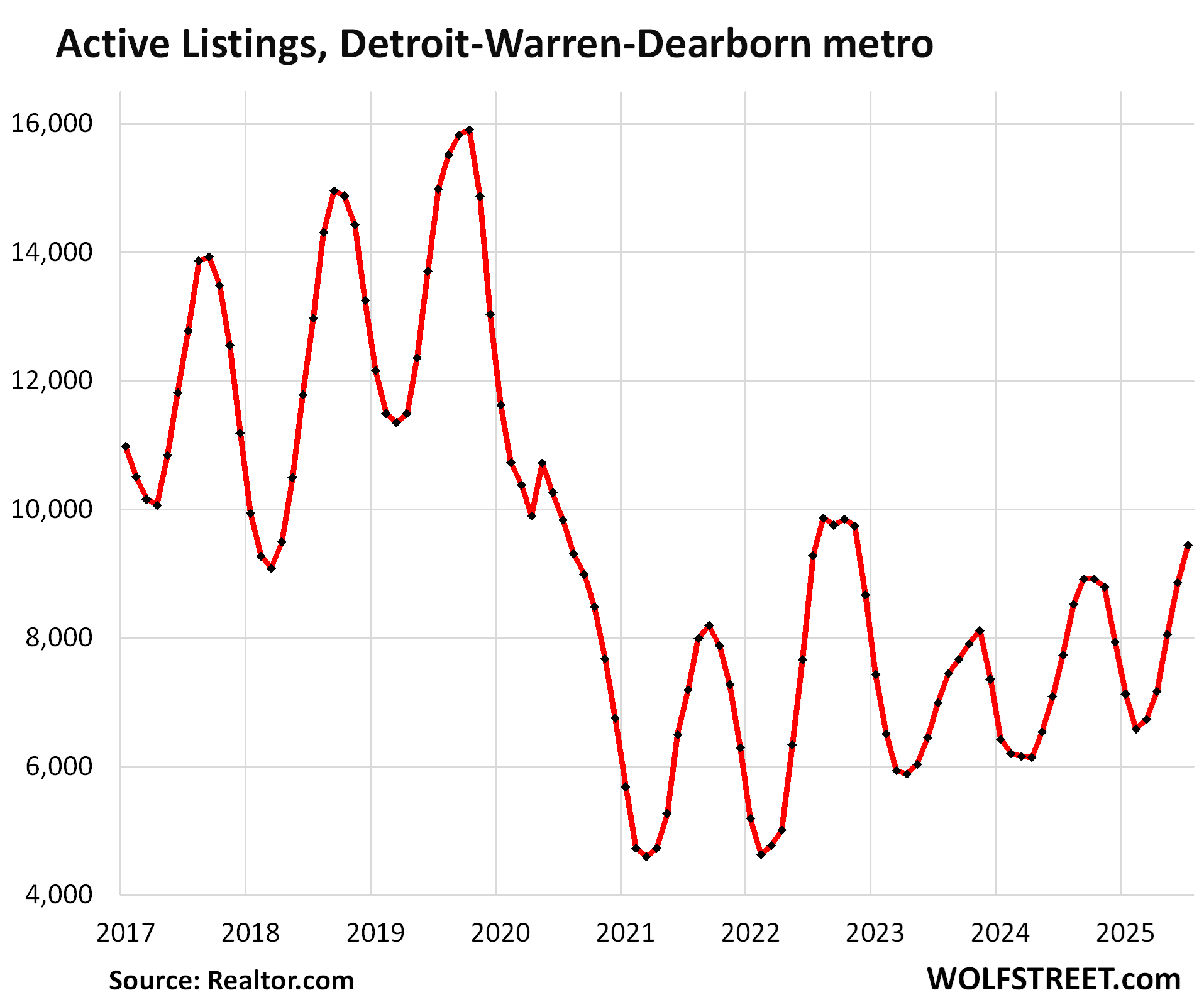

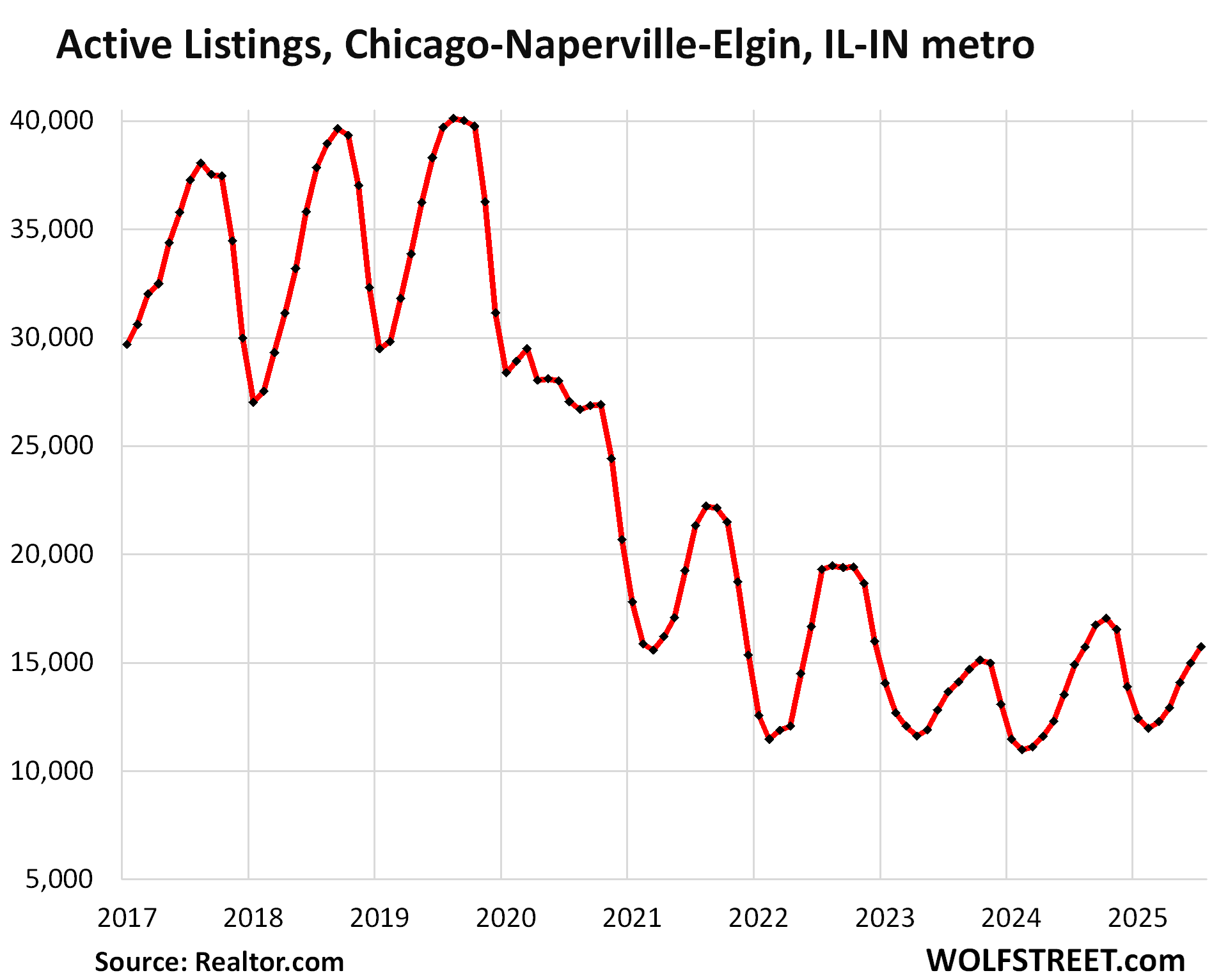

Inventories in some of the big metros in the Midwest diverge, rising sharply in some, such as in the metro of Columbus, OH, but less so in the metros of Detroit and Chicago:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The four Census Regions of the US:

Thank You for the report W.R. 🍻

Realtors must be dining on rat kabobs at this point.

Depth Charge,

Sold a house FSBO a few months ago and the buyer brought a realtor into the equation… what a sleazy, lying, crook. Got the deal done in spite of his incompetence. I enjoy the idea of him eating rat kabobs, which would be a form of cannibalism.

Tom

Perfect comment!!;!;

I like to think of them rocking back and forth on the floor, chanting “date the rate….date the rate…. date the rate”

In previous housing bubbles, many owners were forced to sell, which started a snowball effect of further lowering prices, more forced sales and foreclosures etc. This appears to be a unique situation where most sellers just pull their homes from the market. So apparently they can afford the carrying cost of an empty home or losing rental. The number of forced sellers appears to be insignificant. Buyer want a bees are seeing lower rents and smell a bubble so they are chilling until prices drop. Sellers saying I’ll just keep the place. We’ll see who blinks first, but this can apparently go on a long time since neither side is in a forced to act position.

“We’ll see who blinks first, but this can apparently go on a long time since neither side is in a forced to act position.”

Deaths, divorce, job relocation, kids. Life happens, albeit slowly.

The interest rate is what determines the market in real estate handstone there is no other common denominator more important than that yet The Fed continues to hold the rate up For no reason other than political this is regional ridiculous the rate should be at 5% for the average mortgage right now not 7 1/2

I’d love to hear the analysis behind the comment.

Lol, inflation is still raging and I wouldn’t expect to see 5% rates anytime soon. If Trump manages to force down short term rates there will be a rebellion in long term lending and he will eventually wish he hadn’t.

Buyers are never forced to buy – renting is always an option.

Sellers can be forced by changing life circumstances.

Wolf’s data show that sellers are already blinking first.

If my memory serves me correctly, you have to live in a house for 2 of the last 5 years prior to the sale, otherwise you lose you capital gains exclusion. That may be a motivating factor.

I do agree though something probably needs to kick it off to start the snowball effect. Once the downward trend is confirmed/people will want to get out before it drops further (like every other bubble).

I had a friend suggest the media narrative will change once all the big players are cashed out or deleveraged since most of our media is not truly independent and once the media reports what wolf has been saying but in their usual panicked generating of clicks way the downturn will speed up. No idea if it’s true – but kind of makes sense. Typically the media jumps on any alarmist topic they can for clicks – but they’ve been eerily positive about real estate.

MW: Trump’s push for lower interest rates is on a collision course with government bonds

@SoCalBeachDude

You are correct, Dude.

Not related, but today CNBC ran a headline saying “Nvidia’s results prove AI boom” or something like that. It shows that the other Mag7 are buying these chips and data center services, but it doesn’t show that AI actually generates returns.

Is it ignorance or cognitive dissonance?

AI generates returns… for the people who supply AI data centers. Kinda like how the people who made the most money during the California Gold Rush were the people who sold the shovels.

And those data centers gobble power and water like nobody’s business. Here in Tucson, there’s quite the uproar over a proposal to build something called Project Blue.

The backers of said project came in here with all sorts of slogans — including Water Positivity — and let’s just say that the people of Tucson aren’t buying it. And did I mention that we’re in a drought?

So far, Tucsonans have defeated Project Blue. And locals vow to keep on fighting.

Agree the results don’t validate AI, they just mean Nvidia sold the believers a bunch of chips. Selling equipment to gold miners doesn’t mean they will strike gold. Here is a comment from a guy who should know a bit about AI:

‘Are we in a phase where investors as a whole are overexcited about AI?

My opinion is yes’: Sam Altman founder ChatGPT, quoted in THE VERGE.

Amazing analogy, you and Greg P. That’s exactly how I feel about it.

I view AI investment as an additional cost of maintaining market share for Big Tech companies. If they don’t invest, they risk losing multi-trillion dollar businesses.

I just don’t see much additional profit concentrating in technology from this point forward, at these already lofty levels, but there will be winners and losers of market share, particularly in search, advertising, and enterprise.

AI investment is do or die for Nvidia, Google, Microsoft.

There will come an inflection point when AI is useful enough and increases productivity enough to make business investment worthwhile, kind of like needing an internet connection and software. Microsoft is banking on CoPilot being useful enough to justify subscriptions from every Office suite buyer. I think Meta is banking on eliminating the need for browsers in general and their platform provides it all. Open AI seems like it wants to power everyone else’s niche product. Musk just wants something that gives the right answers according to him.

Meanwhile, businesses are doing their best Miranda Priestly “Not wonderful yet”.

What you are saying here is speculation. So far there’s no indication it will be wildly profitable. And it carries enormous costs. A bit more skepticism is warranted than you want to admit.

I’m getting a little worried about AI. A small majority of the results I get when searching topics I know about contain information that is misleading, and often flat out the opposite of the truth. I also see journalists are leaning on it very heavily.

Of course, people disseminating false information is nothing new, but previously you could use credentials and quality of writing as filters.

Journalism has been badly in decline since long before AI. Credentials didn’t ensure quality, that’s for sure. Clickbait and propaganda has been the norm for well over a decade.

Maybe it’s a form of advertising.

Hey Wolf,

Appreciate the work you do and all the fantastic articles.

I’m curious if you’d ever be interested in covering land prices, especially agricultural land?

Thank you,

Tom

Not really. I’ve looked at it over the years. And I’ve looked at the issues, such as hedge-fund ownership of vast areas of farm land (growers then lease it), ag lending, etc. Now hedge funds are trying to get utilities to commit running big transmission lines to farmland in the middle of nowhere so that hedge fund can sell it as data-center land for a gazillion bucks per acre, but utilities are digging in their heels, unwilling to commit to this fly-by-night-mania kind of stuff…. Everything is going nuts these days, even farmland.

But it’s not really my cup of tea.

thanks wolf

Sometimes when I look at these charts, I think 2019 was bubbly. It felt like we were headed for a recession back then. Then covid happened and changed everything.

So I looked at the Fed’s balance sheet release. $15 billion of mortgage-backed securities dropped off their balance sheet in the past week. In the last 3 months, $67 billion have dropped off. So much for “No one will ever sell and give up their 3% mortgages.”

How much of that amount is from monthly payments of principal?

How do you know what the rates were?

I don’t. But I’d imagine that any mortgage originated prior to March of 2022 or so would be under 3.5%, and anyone who bought after that isn’t likely to be moving that soon.

On the SOMA web page, the MBS are broken out by coupon rate…

Every quarter, I discuss the extent to which homeowners are paying off their 3% and below mortgages. This was the most recent one:

https://wolfstreet.com/2025/06/30/exit-from-the-lock-in-effect-slowed-in-q1-as-home-sales-deteriorated-further-and-supply-spiked/

It sure would be nice if commenters also read my articles about this stuff. It’s all right here. All you have to do is read it.

Every month, I tell you and show you in a chart by how much the Fed’s MBS holdings decline. I don’t understand why people here don’t know this or have to look it up. Here’s the most recent one:

https://wolfstreet.com/2025/08/07/fed-balance-sheet-qt-19-billion-in-july-2-32-trillion-from-peak-to-6-64-trillion/

Wolf

I do keep up with the above chart but how do we know what mbs the Fed is holding? Does it mirror the payoffs you chart from FHFA?

TSonder305

those balance reductions is mostly could be pass through payments too. There is no known mechanism to know how much came from sale or just regular mortgage payment where FED gets paid every month.

Sure, they could be, but think about it. If $70 billion ran off out of $2 trillion in 3 months, that’s nearly 3.5%. The last 3 months does not represent 3.5% of the remaining payments on these loans (assume they were originated in 2020, there are 25 years or 300 payments left.

This is my napkin math, but my point is that we’re seeing some real paydowns of 3% mortgages, as Wolf’s article points out.

Indianapolis is still insane.

single-family home prices: flat for the the past six months, up 1.6% YoY. However, it WAS insane over the prior three years.

Makes sense. I’m still seeing flippers here on the BI make out like bandits(JMHO).

Saw one today, very poor construction, 20 years old, bought in March at 680k, quick Lowes/HD makeover and closed today $1.4m! I doubt he had more than 150k tops in materials and I’m being generous. Sold FSBO through an agent.

If there is a reason why an agent would encourage a buyer in that purchase, it had better be a good one. I can’t rationalize it.

“If there is a reason why an agent would encourage a buyer in that purchase, it had better be a good one. I can’t rationalize it.”

The commission.

“If there is a reason why an agent would encourage a buyer in that purchase, it had better be a good one. I can’t rationalize it.”

I assume that was a implied rhetorical question with a one character answer (“$”) in spite of the lack of “?” at the end.

As far as can tell from the past, RE agents mostly represent themselves first and their client second. Some are worried about their reputation when they work in a niche market (either in geographically small area or in a somewhat rarefied market strata).

Yes 3% of 1.4=$42,000

When you see something wildly mispriced like that, there’s a hidden story.

Could be a market-manipulation scheme of the sort Liz mentioned a couple of posts ago. (Company buys up large chunks of a development on the cheap, then cooks up a few hinky trades to raise the comps, then uses the high appraisal values to refinance, give themselves bonuses, sell the company to rubes, whatever. Then reality returns…)

In this case, if it’s a market with large corporate or hedge fund involvement, they might prefer to buy a few places up here and there at high valuations to keep the rest of their portfolio from being marked down to reality.

The same sort of scheme is outlined in Reminiscences of a Stock Operator… it was used by stock “pools” in the 1910 and 1920s. Groups of investors would keep the prices high in the companies whose trading they dominated, in order to avoid having loans recalled or other financial trouble. The unwinding of a lot of those schemes was a big part of why 1929-1933 was so bad.

Market shenanigans don’t change.

For context, it would be helpful of readers when charting, to zoom out to include the last big bull run and collapse (2004-2010).

As one who has developed a fair amount of residential property over the last 42 years in the business, and living through four housing market purges, this one coming is going to make 2008 look like a day at the spa.

A market simply cannot absorb this level of credit impulse without the subsequent correction that WILL wipe out at least 50-70% of current pricing structures. This is precisely why I sold out literally everything that was attached to dirt in 2023. I mean everything and went to cash in the 28 day treasury market as well as metals.

Not in any hurry at all to redeploy a single dime of it until at least 2029 at the earliest once the bottom settles in and the last of the capitulation occurs.

Fourth time enjoying this ride and the event cycle is always exactly the same.

I am hoping for another crash like 2008 and interest rates drop to reasonable again. Our last house 3400sqft near Phoenix was 211k at 3.25% in 2013. The current house 1900 sqft Midwest townhome in SD (we liked best) we were forced to buy in 2023 was 265k at 6%. going from $1200 Mortgage payment to $2000 for smaller (still nice) home. Living paycheck to paycheck with higher income.

Just curious who forced you? How did they do it?

Monsieur Wolf,

What do you think the government would do, if anything, if and when the housing market turns into a disaster, which IMHO is a very likely scenario. It’s like when an avalanche starts – it is slow and almost unrecognizable in the beginning, but after picking up momentum, it breaks loose and becomes an overwhelming force which wreaks havoc.

You have to admit, we have NEVER had a housing bubble to this extent ever, which also means that the implications of a housing bust could bring consequences greater than we have ever seen/experienced before.

If the housing market corrects 25% to 30% and continues to move downward, millions could be underwater, and panic could set it. Bank loans would disintegrate. Wealth in the form of home equity could evaporate on a massive scale.

Respectfully, what do you think the g-ment would do? I really think that a Housing Bubble 3 is out of the question – not a possibility.

p.s.: The U.S. can’t have a functioning economy with millions of overpriced homes, and homes not selling. It’s like a freight train with the engine broken.

The government won’t be able to do much more. They’re already guaranteeing a majority of the mortgages. The entity that could do something would be the Fed, but since the banks are largely off the hook, the Fed doesn’t really worry about it anymore. The Fed worries about the banking system, and last time, the banking system was collapsing, due to, among other things, the mortgage crisis. So the Fed bailed out the mortgages by inflating home prices (collateral values). Now banks have only minuscule exposure to mortgages, one of the biggest changes coming out of the Financial Crisis, and the Fed can let the housing market reset to a level that makes economic sense, and the banks don’t care.

Dear Mr. Richter,

I’ve been following you for years from where I am, Kuwait.

Thank you for the brilliant reporting and outlook. It has been very helpful for me in many areas.

Keep it up!