Prices of condos drop year-over-year, single-family price growth “near zero.” West & South take serious hits.

By Wolf Richter for WOLF STREET.

Demand for existing homes remains crushed, and amid highest supply in years, prices are beginning to bend.

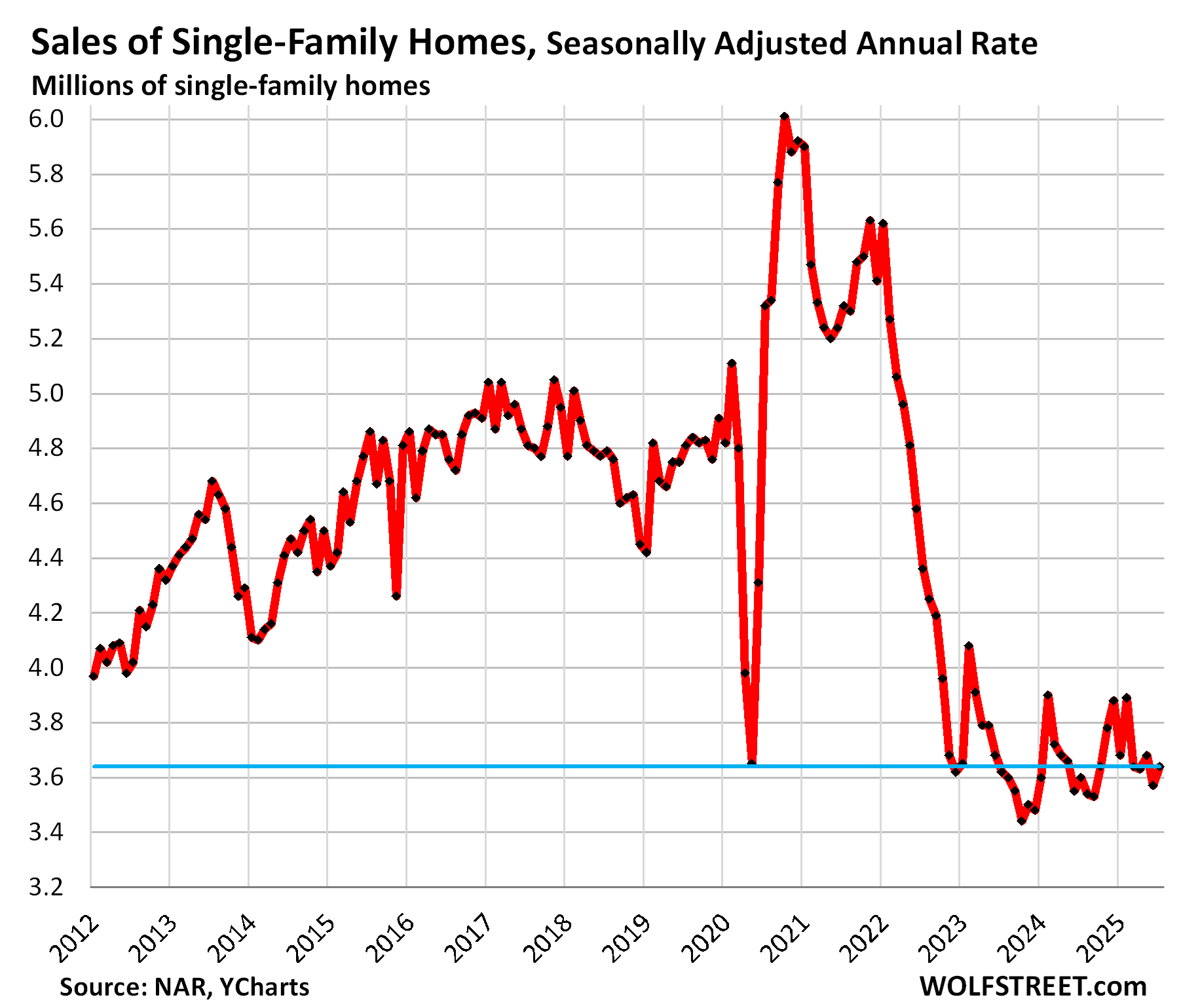

Sales of single-family homes that closed in July ticked up from ultra-low levels to still ultra-low levels, to a seasonally adjusted annual rate of 3.64 million homes, hobbling along the lowest levels since 1995, down by 24% from July 2019 and by 32% from July 2021.

Compared to July 2024 – the worst year since 1995 – sales were up by 0.8%, according to the National Association of Realtors today (historical data from YCharts):

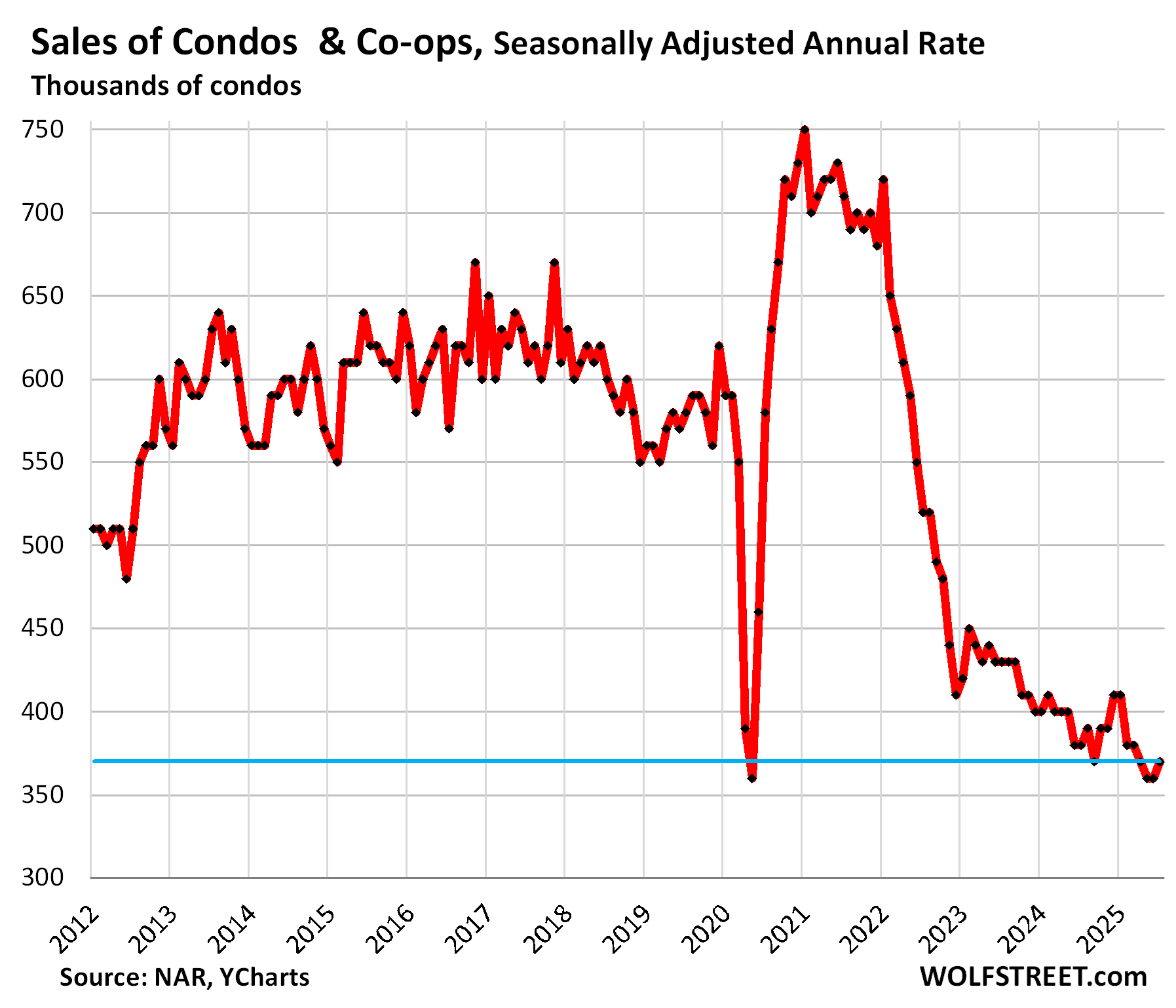

Sales of condos that closed in July ticked up from record-low levels of NAR’s data going back to 2011, to a seasonally adjusted annual rate of 370,000 condos, down by 36% from July 2019, (historical data from YCharts):

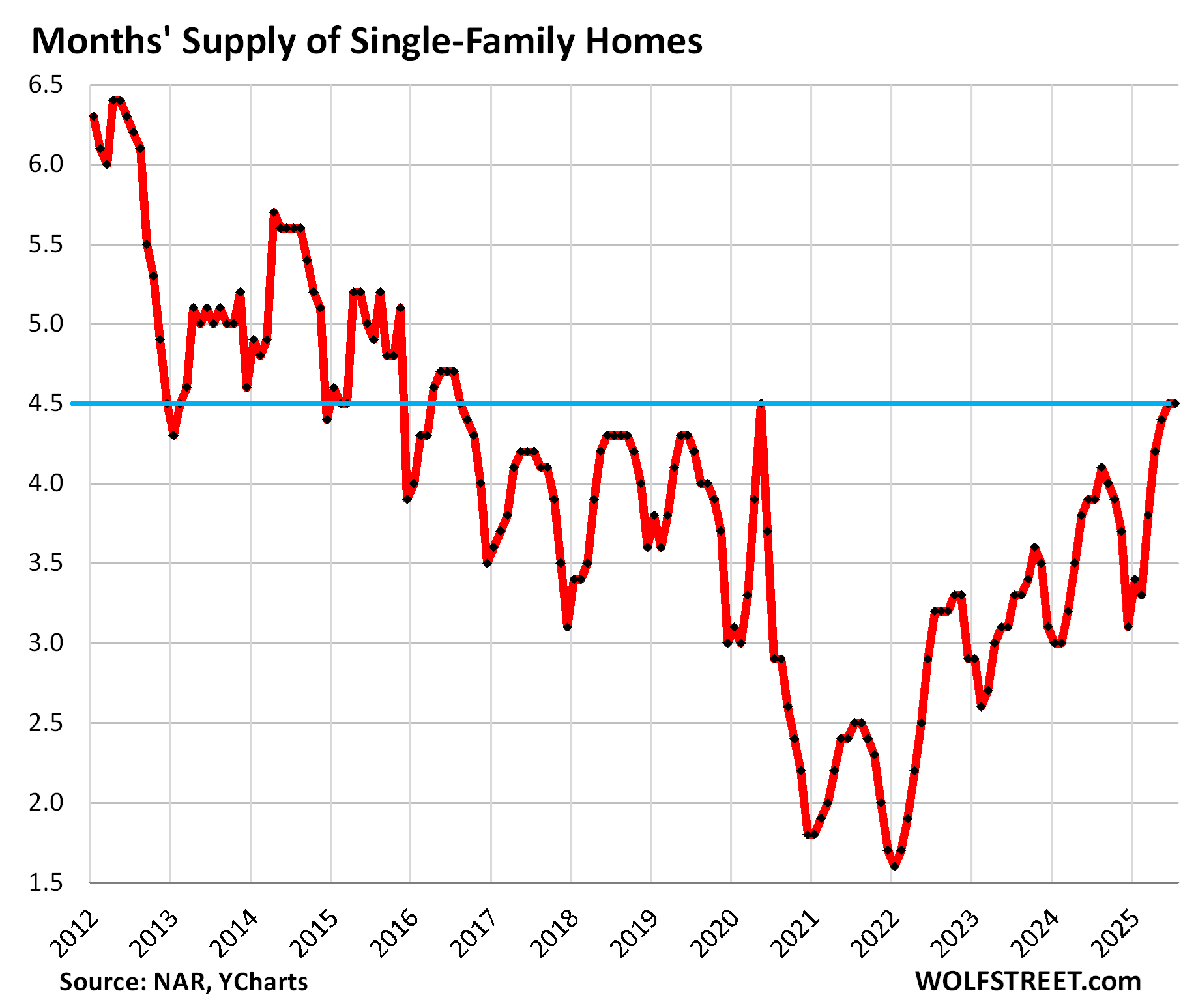

Lots of supply.

Supply of single-family homes has been shooting higher for the past two years and in July remained at 4.5 months, same as in June, and both matched the supply in Lockdown May 2020 when closed sales had collapsed, and both were the highest supply since mid-2016 (historical data from YCharts).

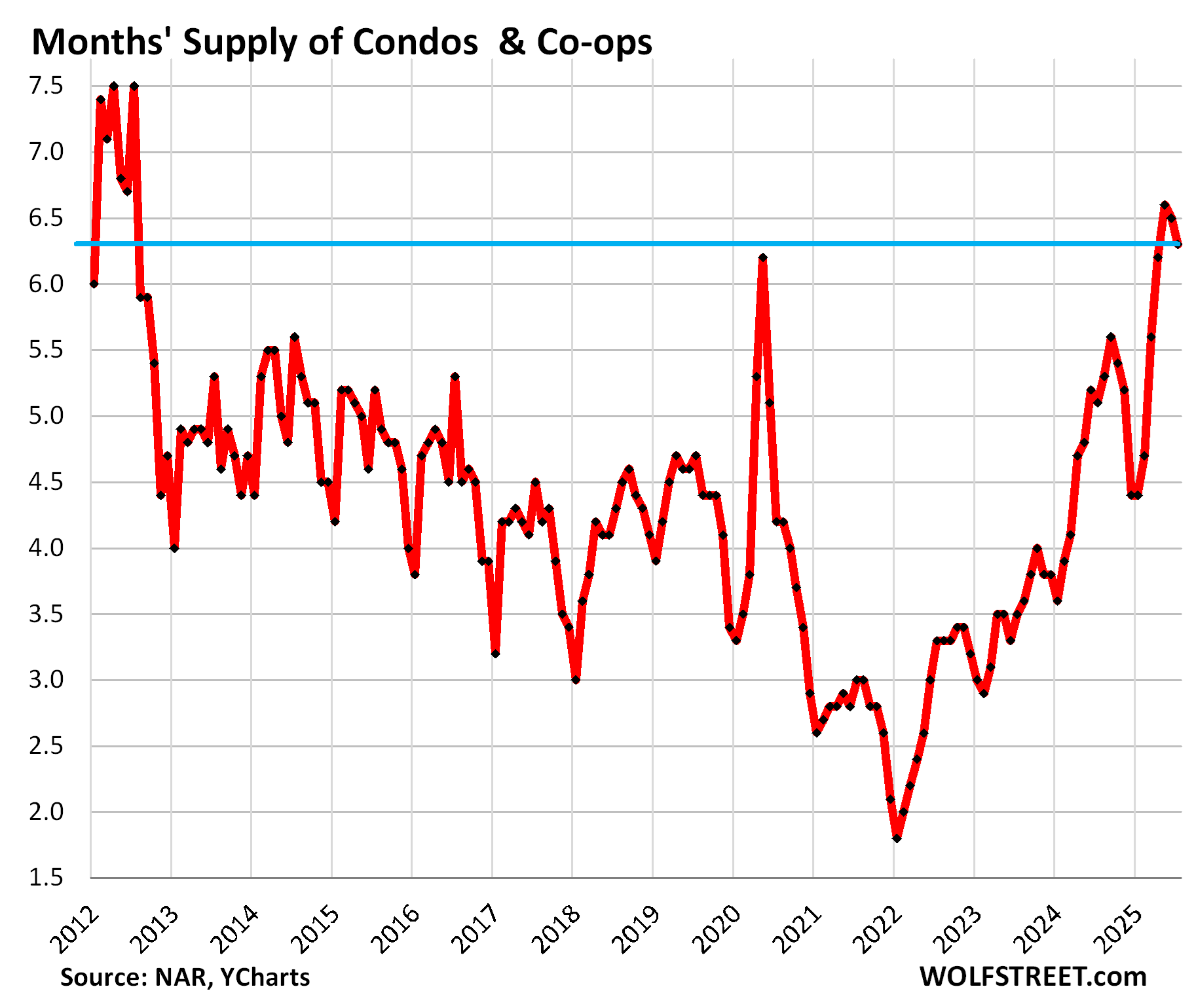

Supply of condos dipped to 6.3 months in July. Over the past three months, supply was the highest since the end of the Housing Bust in 2012 (historical data from YCharts):

What has happened is that prices exploded through mid-2022 beyond what the market can bear, and this price explosion has crushed demand, and as sales plunged while inventories ballooned, months’ supply at the current rate of sales has been shooting higher since 2022.

The spike in supply of homes for sale this year has destroyed the real-estate industry hype that there’s a “housing shortage,” which they deployed liberally – and still in the media these days – to incite homebuyers to pay these too-high prices.

Prices begin to bend.

The national median price of single-family homes, townhouses, condos, and co-ops combined dropped sharply in July from June, reducing the year-over-year gain to just 0.2%, as Condo prices fell year-over-year (-1.2%), while single-family home prices whittled down their gain to just 0.3%.

“Near-zero [year-over-year] growth in home prices suggests that roughly half the country is experiencing price reductions,” the NAR said in the report.

Yes maybe, for single-family homes, where the median price growth was “near-zero.”

But the median condo price growth was negative, it fell year-over-year, as condos in much of the US are getting hammered.

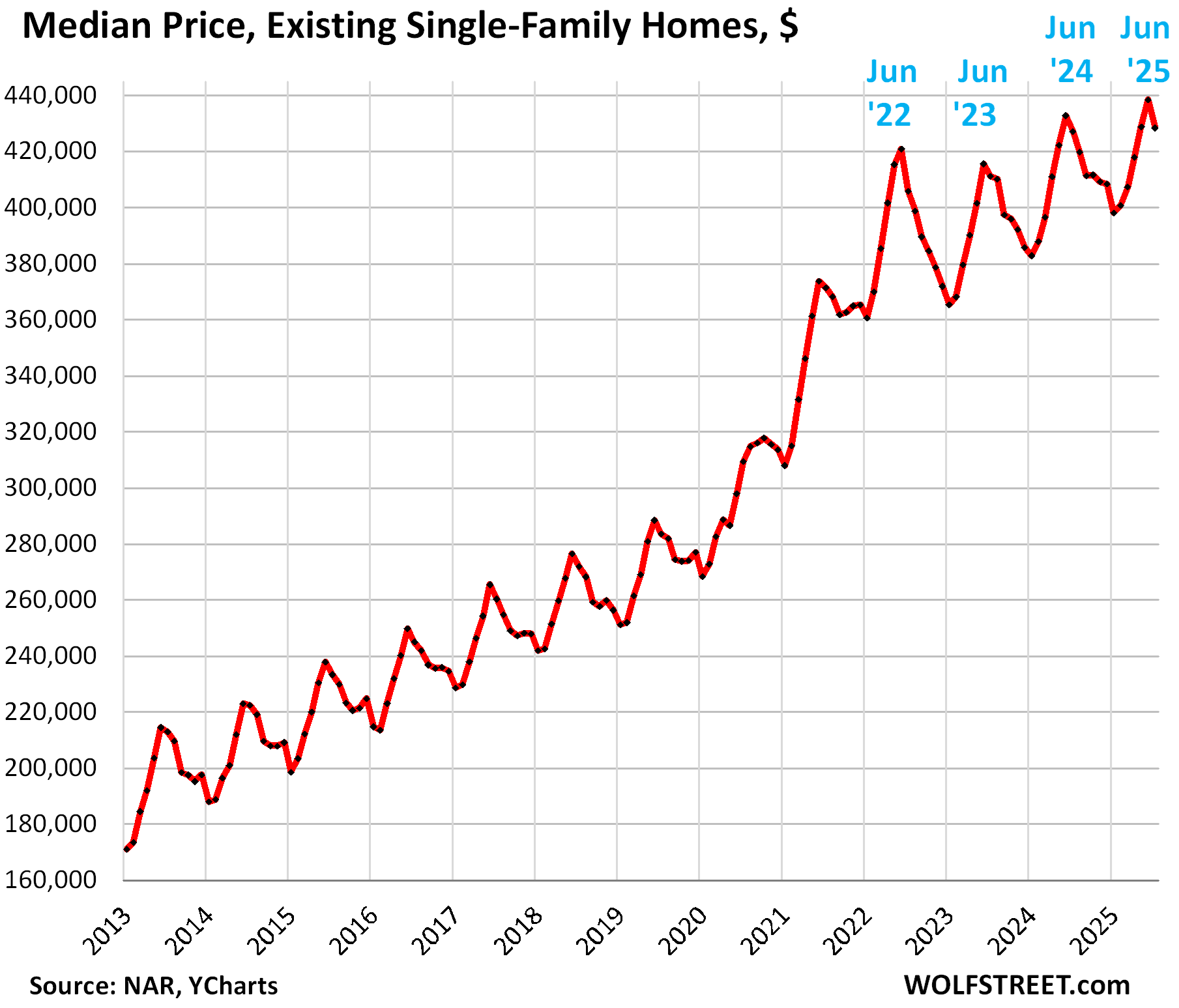

The median price of single-family homes fell 2.3% in July from June, a larger than typical decline, to $428,500, cutting the year-over-year gain to just 0.3%.

But prices fell year-over-year in the West and in the South. Single-family home prices by region, month-over-month (MoM) and year-over-year (YoY):

- West: -1.2% MoM, -1.2% YoY

- South: -1.7% MoM, -0.3% YoY

- Midwest: -6.5% MoM, +3.9% YoY

- Northeast: -1.1% MoM, +0.8% YoY

Home prices are beginning to respond to the mix of desperately low demand, high levels of supply, and prices that had exploded.

Demand has plunged since 2022 because prices had exploded by 45% in the three years from June 2019 through June 2022, according to the NAR’s national median price. This price explosion was a phenomenon of the Free-Money era, but those prices don’t make economic sense, and demand has wilted. Prices eventually fix demand problems – that’s what markets are for. But housing is a slow-moving market.

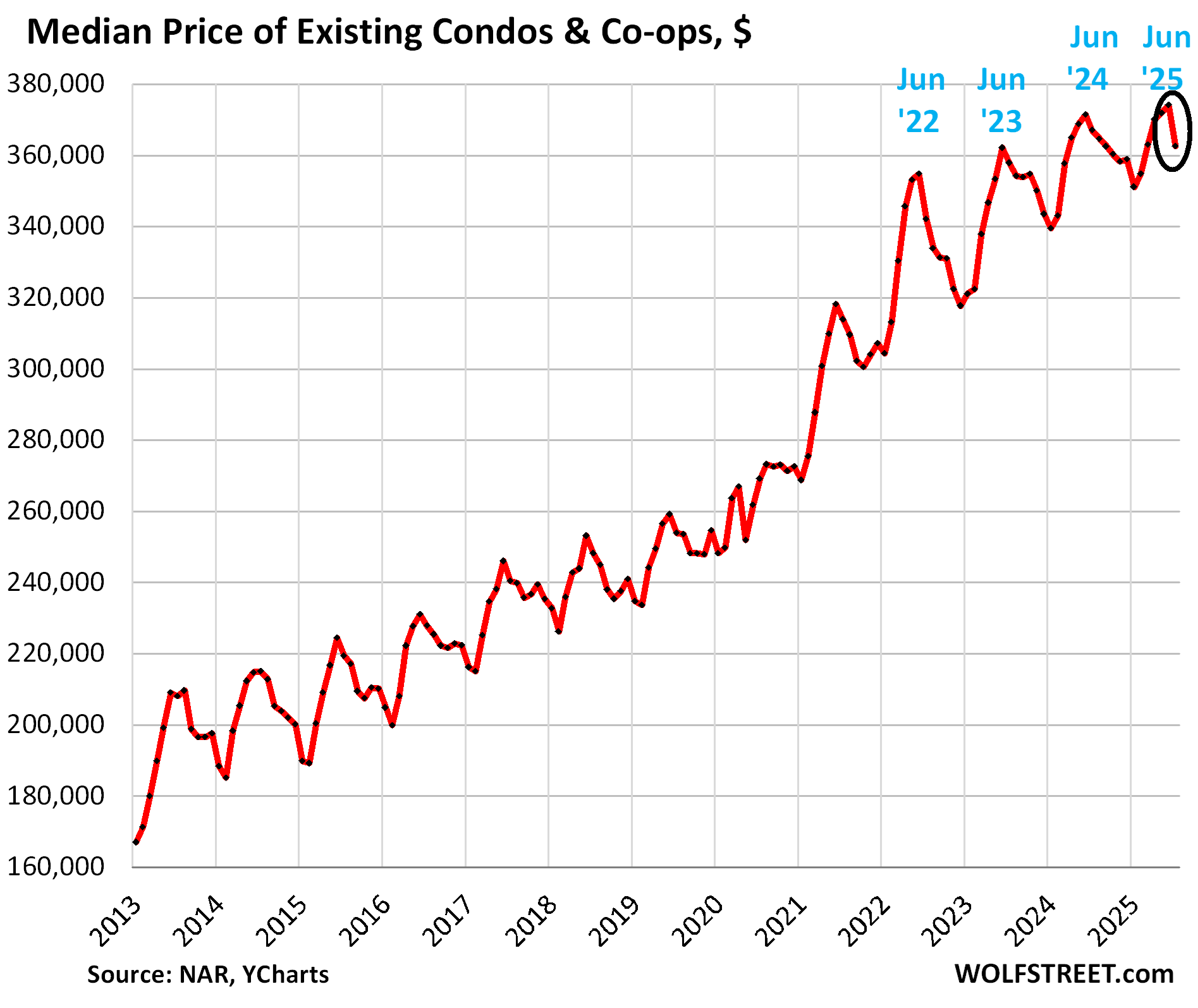

The median price of condos and co-ops plunged by 3.1% in July from June, to $362,600, which caused the year-over-year comparison to flip to a drop of -1.2%.

Condo prices are getting crushed in the West (-6.6% YoY) and in the South (-5.3% YoY). By region, month-over-month (MoM) and year-over-year (YoY):

- West: -4.9% MoM, -6.6% YoY

- South: -1.7% MoM, -5.3% YoY

- Northeast: -3.7% MoM, +0.9% YoY

- Midwest: -0.9% MoM, +3.2% YoY

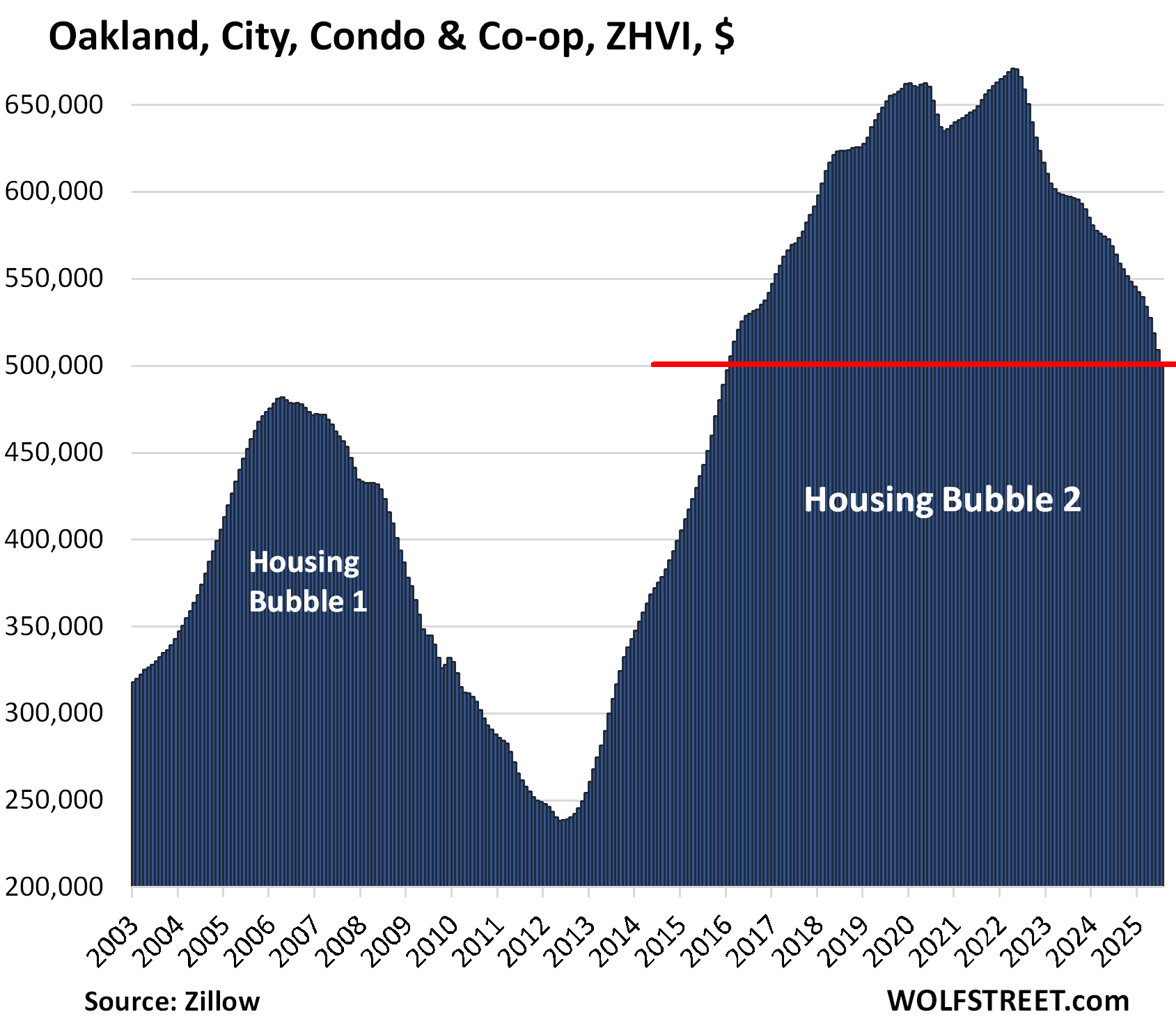

In many cities, a condo bust is already in process: condo prices have dropped by 12% to 26% in these 21 bigger cities: Oakland, Austin, San Francisco, Denver, Tampa, Seattle, New York City, Saint Petersburg, Fort Myers, Sarasota, Boise, Jacksonville, Detroit, New Orleans, Portland, Arlington, Naples, Mesa, Aurora, Reno, and Scottsdale.

In some other markets, prices were still near their highs, or edged higher still. But the price declines in many markets overpowered the price increases in others, which caused the big drop in July and the flip into the negative year over year.

This is what the condo bust in Oakland looks like: Condo prices fell month-to-month by 1.8% for the third month in a row in July, are down by 11.4% year-over-year, and by 26% from the peak in May 2022. They are back where they’d been nearly 10 years ago:

And in case you missed it: The Most Splendid Housing Bubbles in America, July 2025: The Price Drops & Gains in 33 Large Expensive Metros

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Buying a condo is a total disaster now. Its not even the price or mortgage rate, its the HOA and property taxes terrors that come with it. Easily can be higher than the principal and interest payment and no regulations (with few exceptions) how high they can be.

I think HOAs have their uses, but need to be reigned in. There’s no reason that an HOA payment should be approaching towards a X percentage value of the value of the property itself.

The 2024/2025 Minnesota Legislature began with bipartisan support for an HOA Reform Act. It passed in the Senate on 6 May; then went to the House.

82% of all the State’s new homes have HOA membership requirements for new owners. 82 percent!

Three of the Senate’s provisions were to:

1) Require HOA boards or property managers to get three written bids for all repair jobs costing $50,000 or more.

2) It would block cities from requiring that there must be an HOA as a condition for approving any housing development within the municipality.

3) It would provide a path for dissolving some of Minnesota’s HOAs; particularly those within single-family detached communities that have no shared property, like a community center or a pool.

To me, #3 should be a slam-dunk.

But as the Legislative session neared its closing date and the House took up the Bill, the HOA Associations went into overdrive to defeat it. One after another, HOA managers and administrators testified about all the horrors that this would create for their power structures.

Nope, the House shut it down at the last minute. Nothing changed. HOAs have arbitrary power that is unchecked.

So, as I commented a few days ago about Minneapolis having nice starter homes for around $300k, I should have added that the 100 year old homes, such as my Sears Craftsman 2 br bungalow kit-built house, have no F ing HOA to pay for or deal with!

Thank you for this report, Wolf. From what I read in it, perhaps it would be wise to wait it out a little while longer before buying, eh?

Good luck everybody . .

People need to stand up and be very vocal about HOA overreach.

During the COVID insanity, my HOA, despite their own bylaws saying the could not discriminate against anyone for anything, and against HPPA laws, was going to require all residents who used HOA facilities to be “vaccinated”. By that time I was already a 2x “survivor” without any jabs.

I had personally told the president he had two choices: pass this insanity & give me back my dues for the year, or I would sue the Board and the members individually for overstepping their rights and violating mine.

I went to a public meeting, conveniently held at s time most residents would not be there, and they made it the last item on the agenda after a discussion of … dog poop. Three hours wait to promote my position.

A week later they had a Zoom board meeting where residents could listen in, but not participate vocally. However you could text in. Every time one of these power hungry ninnies advocated for this illegal position, I texted in “You are coming dangerously close to getting sued. Think long and hard about violating your own bylaws.”

In the end it failed by one vote.

And yes, I was 100% prepared to sue them all. Plenty of free cash flow to do it as well.

If you don’t stand up for what’s right, the know-it-all control freaks will make your life a living hell.

Just say NO.

I was on an HOA board for a few years – our community’s big expense was a pool – and the big problem is lack of owner participation. I was on the board because there was an opening and I was the only sucker there willing to sign up. The other big problem is that the rules are written in such a way to make it extremely difficult to change anything. Coupled with the lack of participation, the board could do almost whatever it wanted until they were voted out or left. Even a hot-topic issue couldn’t get the 2/3rds (or whatever) of all owners’ vote, especially when an increasing share of owners were landlords that didn’t care (unless the vote was to limit the number of rentals).

Thank *you* for the detailed insight into how specifically HOAs can abuse their power (frequently in cahoots with local governments).

The bidding process is borderline meaningless. The guy who gives the HOA president the biggest kickback will oftentimes come in as a low bidder. Then there will be a change order, and no one wants to switch contractors halfway through a project, so the homeowners pay up.

Win-win-lose for the president, contractor, and homeowners, respectively. HOAs are well-intentioned systems, but tend to be super corrupt and regulations won’t change that.

HOAs, even in condos where they are pretty much necessary, have gotten out of control. In major cities, fees of $1/sf/month are quite common. So your typical 1BR is going to run $500-1000 in HOA fees (on top of mortgage, and whatever utilities aren’t covered).

The HOA numbers *have* gotten fairly insane.

And another really bad aspect is that those fees tend to be buried/hidden when looking at surface level housing “prices” as reported by major comparison sites.

Hopefully few get through the entire SFH sales process without finding about the HOA specifics but…this “hiding the salami” still creates an overall atmosphere of misleading prices (like Vegas hotel rooms with phoney-baloney “Resort Fees” that go undisclosed until the very last minute).

Do the builders profit from this? UK builders have been boosting profits for years with outrageous service charges and selling units leasehold instead of freehold with egregious long term ground rent increases.

Are there any safeguards in the US preventing similar shenanigans? For example, is the builder able to manipulate an HOA into uncompetitive and very long term maintenance contracts?

>Are there any safeguards in the US preventing similar shenanigans?

I don’t think there are any. What I learned the hard way is that HOA can be under builder control for a very long time. Ours had a clause that ALL houses must be completed AND sold, but they also had a loophole that allowed the builder to buy an adjacent lot in the middle of development of the initial parcel, add it to the existing HOA and essentially extend builder control for almost 2 extra years.

Even once they hand the control over to homeowners, it is extremely hard to fire an inefficient management company that keeps inflating dues every year while entering into some shady service contracts.

The only thing I know right now is that I will do my absolutely best to avoid having HOA of any sort in my next house.

There are buildings where you get a lot for that money, and others where you don’t. My aunt and uncle live in one where he pays $650 a month. But that covers the pool, tennis court, gym, maintenance of the common areas, insurance for the building itself (so their individual insurance is low), included cable/internet, and so forth.

If you don’t get anything, or don’t use it, then it’s not a good deal.

Fair, and this is all in the eye of the beholder, but you can get all of the pool, tennis, gym, etc for much less than $650/month. At the question is how much is it worth to you to have those things in your condo building?

Everyday there’s a conflicting report about housing. I don’t think any of these idiots know what’s actually up or down.

I wonder if this is the same for co-ops? NYC has a lot of co-ops, some in expensive locations in Manhattan. How “at risk” are these higher end properties?

The data here includes co-ops, but doesn’t split out co-ops from condos.

NYC coops are exclusionary by choice.

They have extremely large capitalization deposits required at time of purchase and high maintenance fees. They were always expensive but in the 1980’s, all the Wall St. money made them millionaires only properties, now even millionaires can’t afford them.

Co-ops are just like condos, just structured differently to avoid mortgage recording taxes.

No. There is more involved. Legally speaking what is owned by a coop owner and Condo owner are very different. Also most. Oops especially on Long Island have no amenities. Just 4 walls like an apartment, are yours.

The ownership structure is very different.

With a condo, you own the inside walls of your unit plus your percentage of the common area. So if the square footage of your unit amounts to 1% of the total square footage of all units, you also own 1% of the common area (land, pool, building, etc.). You pay the property taxes. HOA pays the homeowners insurance. You pay a monthly HOA fee. You can sell your unit to anyone, and the HOA cannot get in the way as to who you sell it to.

A co-op is a corporation, and you own shares in that corporation, based on the size of your unit. The corporation pays the property taxes and homeowners insurance. You pay monthly maintenance fee. Co-op boards have a say as to who you can sell your shares to. If they don’t like the buyer, they nix your sale. This makes co-ops harder to sell.

Nice summary on this topic! Condo Schmondo.

Permeating all of this, as player972 mentioned “property tax terror” is a real issue, not to mention homeowner insurance which has also escalated a significant amount in recent years (Wolf, where does homeowner insurance stack in your “services” inflation data, or is it in a separate data stack?) Will leave the HOA fiasco to others to comment.

PITI + HOA + PMI (for some) has increasingly become burdensome.

Homeowner insurance, HOA fees, and other expenses of homeownership in CPI are supposed to be reflected indirectly in the CPI for Owners Equivalent of Rent (OER), which accounts for about 25% of total CPI, but it’s not a very good approximation:

More detail here, scroll down to OER:

https://wolfstreet.com/2025/08/12/feds-nightmare-cpi-inflation-in-core-services-worst-in-6-months-pushing-core-cpi-to-worst-in-6-months-some-goods-prices-fell-others-rose/

Clarification helpful based on how it’s defined by the data source. Agree as a component of OER it may not provide needed isolation for these costs to be effectively reported/tracked. Thank you, Sir!

I think no matter how you calculate it residential home ownership is a PITA.

Agree, similar to children.

@Bob B you are correct that the ownership of real estate (like the ownership of a car) is a PITA but it is less of a PITA than sleeping in the park or renting a home (or taking the bus or riding your bike)…

“renting a home”

eh…no.

Renting

(even at its *worst*, where coked up complex speculators who have (over)paid some ZIRP-era Insanity Price and then try to squeeze blood from tenants)

provides…

Flexibility, in an era of insanity.

1) Apartments usually offer a *range* of price options (because complex owners usually have used a range of financing to acquire ownership…from *none* to ZIRP crack cocaine)

2) Apartments offer a *range* of size options – directly affecting price.

3) Apartments offer a range of time/exit options that allow tenants to get the hell out of complex/neighborhood/city/MSA/friggin Country if pricing insanity persists.

That “exit optionality” is extremely valuable in contrast to the frequently low liquidity/high immobility world of traditional housing/back-breaking mortgages/ravening property tax authorities/mad insurers/etc.

That old “paying your landlord’s mortgage” line (used by SFH broker-hucksters) is only true if renters behave like utter potted plants.

@cas127 You are correct that moving from a rental home is less of a PITA than selling a home, but “you” get to decide when to sell the home and don’t always get to decided when to move from a rental home (and you can’t argue that looking for a new rental when you are told the landlord is not going to renew your lease is not a PITA).

In decades of renting apartments, I’ve never had a landlord end a lease on me.

Try and jack up the rent – sure.

Tell me there was no price I could rent at? Never.

I can only imagine this occurring in some sort of apt-to-condos conversion which I think is fairly rare (especially before ZIRP madness grossly distorted RE asset prices).

Throw it open to Wolf’s audience…has anybody ever been absolutely booted from an apartment, being told there is no (or even no remotely reasonable) price for future rent?

I can see obscene rip-off *attempts* circa 2021-23 (thanks, Fed) but even if obscene and utterly unexpected, at worst you pay the hostage price for a 6 month new lease…and then get the hell out (who wants to transact with such landlords?)

That’s the whole point of renting – flexibility and optionality.

*Buying* means locking in to an asset with,

1) Large valuation fluctuations over the last 25 years,

2) A definite minimum buy-in size (very, very large)

3) Inescapable tax, insurance, and maintenance costs

4) Relatively speaking, pretty darn illiquid sales markets relative to many other asset markets.

cas127

“has anybody ever been absolutely booted from an apartment, being told there is no (or even no remotely reasonable) price for future rent?”

So maybe not the way you phrased it, but…

A Landlord trying to get rid of paying good long-term tenants by hook or crook is a common problem in rent-controlled buildings in San Francisco. After they successfully by hook or crook get rid of the tenant, they can remodel the apartment and put it back on the market at much higher rents.

Veritas, a scandal-plagued huge former landlord in SF, was accused of doing that because that was its intended business model from get-go, to buy old apartment properties, force out the tenants one by one, remodel the units, and put them back on the market at much higher rents. But that’s legally hard to do, and so the “by hook or crook.” Its scandals were constantly in the local media. Over the past few years, it ended up defaulting on loans backed by hundreds of buildings and thousands of apartments in SF. The lenders ended up selling those loans (and thereby the properties) to several other investors.

What a strange comment. Residential home ownership is NOT a PITA for people who do their research and buy a well-built house, not in a natural disaster area, and not in an HOA. If I want a swimming pool I can build one… or pay for a health club membership that has one. Don’t fool yourself to think that “renting” is a better option. Costs are costs – pay them as an owner, or pay them as a renter.

Good comment Greg,

Lots of folx do NOT real eyes that if you rent, you still pay the LL costs, taxes, etc., plus.

While I totally agree that SFR ownership is definitely at PITA and costly, after 75+ years of going between renting and owning, IMO owning is better.

Keep in mind that most states continue in the very clearly punitive for owners of increasing ”property taxes” for SFR that really should stop increasing after at most 10 years, but certainly at some age/duration of ownership.

Otherwise, as many have commented ”one” is only renting RE from the local taxation authority and will likely LOSE said RE sooner or later…

Certainly one reason SO many folx have been moving from high tax states to FL.

Exactly. Some people just have an issue with commitment. Couple that with a poor credit score, poor job history, low or inconsistent income.. housing is not their first priority…Renting forever is not a business plan. But some will cut out housing expense over their vices. Live in their cars etc. By the time they are middle aged or senior, unless someone rescues them, not having housing as a priority catches up with them. Shelter, food clothing. Should be the order if priority. But t g ere,are people iut here with $1000/mo car payments.

Are there any credible price forecasts? The scenarios i’d love to see simulated would be with 0, 150, 300 basis point drop in 2026.

( Assuming this is not wolf’s jam given none of us have a crystal ball and the messy political climate )

It’s completely by city, but in the bigger picture the ultra-rich will start buying up every available asset again if the Fed cuts short term rates in a month. The big boys are no longer going to be comfortable parking their boatloads of money in MM’s and other short-term investments if they are returning 3% when inflation is hovering around that number.

As an extra bonus, the Fed will blow out long-term rates when they cut prematurely and mortgage rates will go up, not down.

The fed cutting rates without inflation getting down to the target will be an absolute disaster for regular folks trying to buy a house to actually, you know, live in.

How this all intersects with the upcoming AI crash debacle will be interesting.

That’s been the real tragedy of the past 20 years. Retirement assets and housing is now unaffordable to many people.

There is no reasonable entry point for assets any more. You can either buy at today’s prices and hope the mania continues or you can park it in t-bills. If you buy stocks and we end up with a 30 year stagnation like Japan, then you won’t have anything extra when you go to retire.

If you are talking about basis point drops in the Federal Funds Rate, you can keep guessing, because I’m not sure how closely the funds rate and 30 year mortgages are aligned any longer – particularly with the ginormous Federal deficit, and the Treasury playing games with securities to finance the debt. How will a 300 basis point drop in the funds rate be reflected in the market for 10 year TBills? If it is caused by politics and not economics – perhaps not at all. Perhaps evens the reverse – if the markets get spooked.

Fed funds rate and mortgages have never had the correlation that mortgages do with the 10 year treasury. a 300 basis point cut in the fed funds rate will blow mortgage rates out at least 250 basis points, to the upside.

That very last graph (Oakland) showing Housing Bubble 1 and Housing Bubble 2 looks like a humpback whale beside a dolphin. ‘ They’ created a veritable monster this time around! 🐋

“Sales of Existing Single-Family Homes Crushed..”

Crushed, squashed, decimated, annihilated, obliterated, wiped out, eviscerated. Help me out here….

I wouldn’t want to be a real estate agent at this point in time. Bottom line: Housing market is BROKEN. Yes, BROKEN.

Fed policies from 2002 to date, to “save” the US economy (translation – obscure the existential crisis presented by rising Chinese international competitiveness) turned the US housing market into a casino.

How could the US survive without its centrally (mis)managed economy?

Prices are still too high relative to incomes. The sellers are not motivated enough yet, and they can hold out until inflation reduces the actual price they receive in real terms, which is happening to some extent already. Of course, by the time the properties sell, the owner will have paid additional overhead in taxes, maintenance, HOA etc. So the price paid in real terms will be less and the costs associated with holding the property will accrue.

I have tried using “AI” to help me decide if it would be a good time to buy a house and what price I should pay, but so far it hasn’t been very helpful. Something about “Insufficient data to train the model on today’s current housing market, pricing, and interest rates to make a highly probable recommendation. Considering buying bitcoin. “

On the other hand my Magic 8 Ball is knocking it out of the park..

“Should I buy a new home?”

Response “It is Decidely So”

;)

Can’t tell if this meant to be facious or not, but AI isn’t AI. These LLMs are just good at writing and it’s technically machine learning. They cannot think or problem solve. What they can do it write and summarize data far better than an Google search for any content that already exists.

You could build a model and train it to try to forecast real estate price movements, would still also be machine learning and not AI, but that’s not available to the public via chat gpt or Gemini.

What used to be called machine learning is called AI. What used to be called AI is now AGI. We’re still very far from something that can actually think. What we have is something that is really good at repetitive tasks and consolidating/summarizing pre-existing information

Exactly. You can’t get any new knowledge. Only refined existing knowledge that was used to train the model.

Technically, AI is a field of study. Machine learning is a mechanism for training different kinds of models in LLMs or even robots.

I think, like all Real Estate, it’s about location, location, location.

In 2023 we sold our Chicago West Suburban SFR and bought an even further Chicago West Suburban condo.

So far … so good.

But as an attorney buddy of mine, who has now met his maker, would joke …

Q: What’s the difference between an STD and a Condo?

A: You can get rid of an STD.

With any luck we’ll be so out of it … the kids will have to worry about it.

The warning signs the AI bubble is about to burst

Shock sell-off after study warns most investments in artificial intelligence get zero returns

We may be facing the dotcom bubble 2.0

As US tech stocks lose $1 trillion, we must remember that overhyped tech can cause catastrophe

Yeah it will be interesting to see which pops first. I think we can have a housing market decline without a stock market decline, i.e. minimal impact from a housing bubble. However, I think a stock market decline could cause a significant increase in housing prices declines.

If the Fed cuts rates in Sept the long term bond market will crash like it did just before the last election. Mortgage rate will go up. You can say goodby to the Real Estate market. It will go from a recession to a depression.

Our Great Leader has commanded that interest rates be lowered. So it shall be done in accordance with his wisdom about everything.

What politicians dont want lower rates?

And if it all crashes anytime soon, who has been set up as the “fall guy”? Powell

Frankly it’s smart marketing.

Perhaps so the bond market freaks out and his companies can buy things for cheap.

Or he secretly doesn’t want rate cuts, he just wants someone to blame if there’s negative press re: housing market or economy.

I haven’t figured out which yet. But I in no way believe that he actually wants to cut rates to reduce real estate costs. He’s a sales man, he’s trying to sell a concept to America – the question is why? What’s his angle?

“What’s his angle?”

Near term profits.

Median prices for SFH:

Midwest: -6.5% MoM, +0.8% YoY

—————————————

Is there a typo mistake here?

I hope not…

No, it’s not a typo. This -6.5% is month-over-month, and there is always a big drop in July from June, so there is a lot of seasonality in it. But this was a bigger MoM drop than normal, and it did shave down the YoY gain to just 0.8%.

The asking price exceeds the offering price by a substantial amount. The logical conclusion is that the current human population seems to be confused by the concept of delusion.

The buyers are going to win this one.

MW: Homes are taking longer to sell, with more on the market than at any time since the pandemic

In my neighborhood (Bay Area city), Overall houses are sitting for longer time. But still owners are NOT reducing prices. Few may be reducing less than 5%. Few owners have hold off selling. Now they are trying to rent it.

I just hope, FED sticks to inflation mandate. Even if they drop rates, they expedite MBS Sale. So Mortgage rates are driven by Markets and not manipulated by FED.

I want Home prices to go Pre-pandemic levels. That’s AT LEAST for me to even start looking to buy.

Stock Market ATH has given A boost to Owners and those who are buying now. Those ATH iN STOCKES making many tech employees very rich. For them, it wont matter as long as Stocks are high.

Pre pandemic prices I doubt we will ever see again

That would mean cutting the price of housing in at least half

Not going to happen , commodities would need to drastically decrease as well as Labor

At this point in time, I think owning a place to live is the best way to preserve assets regardless of taxation

Commodities are inherently deflationary.

I would love to see my house assessed *below* what I paid at the start of 2021.

“That would mean cutting the price of housing in at least half”

Let’s assume that in your market, prices rose by 50% since the beginning of the pandemic. They would have to drop by only 33% to get back to the last price before the pandemic.

If prices rose 100% (doubled), they would have to drop by 50% to wipe out that 100% gain.

If you go to my condo price article, you will see that in several markets prices already dropped well below pre-pandemic levels.

https://wolfstreet.com/2025/08/20/condo-prices-already-dropped-by-12-26-in-21-bigger-cities-through-july-condo-bust-takes-shape/

If incomes keep growing and rates drift back to ~5.5%, affordability normalizes by 2028 even if prices rise modestly.

What are you talking about?

Per the Fed’s affordability monitor:

Median priced home is $401k. Median HH income is $79,500. Currently it takes 48% of your gross income to make the monthly payment – extremely unaffordable!

If incomes continue to grow at 3.9% then in 2028 HHI would be $89,100. Even if all housing costs stay the same & rates drop to 5.5%, it would still require 42% of your gross income to make the payment. Affordable is considered 30% or lower.

Please Let your grade school math teacher know she was an abject failure.

The median price charts look like the heartbeat of stupidity, LoL. Never buy a condo! If there is an insurance claim, you will have never ending litigation and most likely end up paying for someone else’s stupidity! But hey, you were dumb enough to buy a condo in the first place.

People waking up to the fact that interest rates are NOT the problem, it’s the inflated PRICE.

Seeing a lots of single family and town homes on the market, prices dropping. Holding the line, more deal will be coming for folks with cash. History may not repeat exactly, but it sure as hell rhythms.

People might be waking up, but they are still encountering MASSIVE amounts of NRA spin everywhere to the effect of “Woe! The interest rates are killing the housing market. Somebody DO something (uncontrollable sobbing of sellers in the background).”

Those articles are everywhere, even in reputable sources. NAR money talks….

If anybody ever wants to dispute the power that (frequently distorted) interest rates have the power to artificially distort transactional volumes (and therefore asset prices), I suggest they take a look at SFH sales volume explosions (2020) and collapses (2022).

But the true madness lies in thinking the prices set during these periods of profound volatility are necessarily sustainable over the long term.

And today Powell opens his trap with some mealy-mouthed nonsense like “Inflation is still above target, and there is uncertainty regarding pricing because of tariffs and immigration, but the balance of risks warrants rethinking our rate strategy.”

It’s hard to conclude at this point that he wants anything other than to maintain and continue to inflate this insane asset bubble, making housing and retirement unaffordable to large swaths of America. And he can say all he wants that his decisions have nothing to do with Trump’s bullying, but no one believes it.

He’ll go down in history as a squish who can be easily manipulated.

I have full faith in Powell to cut rates in September .

He may be forced to do a token rate cut of 25 bps to save himself from the trouble.

How would long term rates behave is another matter

He has to balance unemployment vs inflation. Unemployment will take precedence over inflating asset prices.

There are cracks in the employment sector. Unemployment for current college graduates is at 5.8% which is highest since 2012.

Gen Z men with college degrees now have the same unemployment rate as non-grads—which is around 7%.

There also was increase claims and increasing continued claims

Wolf, sorry if I missed it, but do you ever get specific about who’s holding the bag this time if it isn’t the big banks?

Yes, I’ve gotten “specific” a million times:

The biggest bag-holders will be taxpayers, because the government guarantees/insures the mortgages that back the MBS it issues, so that holders of MBS have essentially a government-guaranteed investment. This is one of the biggest changes coming out of the financial crisis.

The second biggest bag-holders are investors that buy “private label” MBS where lenders securitize non-qualifying mortgages and sell these MBS to investors such as bond funds.

Banks are mostly off the hook. Their still hold some mortgages, but the total is only a small portion of all mortgages.

And this specific Henry Paulson testimony is what officially announced that going forward taxpayers would be on the hook, no longer the banks:

https://m.youtube.com/watch?v=OX_BIV0oAdc

8:30 mark

So the Fed is likely to cut in September which means long rates and mortgage rates could very likely go up again. The front end of the curve probably will respond though, 4-week back under 4%. Seems like the whole thing is balanced on the edge of a razor now anyway. Do they save jobs, housing, CRE or stocks – seems like it can only be one.

“according to Rosenberg Research, which foresees a major drop in home prices that could drag the pace of inflation close to 1% — well below the Fed’s 2% price growth target.”

For that to happen to home prices, Powell can’t cut rates anytime soon.

It’s deja vu all over again. A while ago, Powell dropped rates 50 bp based on jobs data that turned out to be wrong. Now he appears to be leaning toward dropping rates again based on data that has shown itself to be clearly unreliable, the BLS jobs numbers. This in the face of rising inflation. Doing the same thing over and over again and expecting different results is the definition of insanity. Fool me once, shame on you. Fool me twice, shame on me.

He does have to please the King at some point, if he doesn’t who knows, might get a FBI raid at his place…

Seems like it’s almost a certain thing now rates will drop again, the ONLY thing we can hope for is long term yield will rise again and all these knuckle draggers promoting cut short term rates = lower mortgage rates get humiliated again and again…small consolation price for those that have been staying on the sideline buying Tbills, guess they are really anxious to push them into overpriced stock markets, housing, Crypto….can’t get there without slowly (or rapidly) into TINA environment again.

My concern is that as they drop short term rates, large investors will roll some of the money from t-bills into 10 years instead, causing yields to drop. That would vindicate these people.

It simply doesn’t work that way when there are major inflation expectations. If overnight short term rates fall then axiomatically long term yields and interest rates will rise proportionately just like the last time around when the Fed cut interest rates.

TSonder305

“large investors will roll some of the money from t-bills into 10 years instead”

That cannot be done by definition. If large investors roll billions or trillions of dollars from T-bills into something else, some other large investors have to buy those exact amounts of T-bills, because T-bills don’t just dissolve into air, and on net, investors cannot walk away from T-bills.

Same with all securities.

Hi Wolf, that is true but what I meant is not selling them to other investors, but waiting unto they mature (2 months, 6 months etc.) and THEN rolling the money it gets back from treasury into long term bonds.

Am I missing something obvious?

Curious…you obviously don’t like Trump. Do you think Trump and Pulte should ignore Fed Gov. Cooks mortgage fraud? Because “everybody” does it?

Personally, I love to see fat cat crooks go down. White collar crime is a major problem with society.

Waiono, I don’t think anybody actually likes Trump. We may like some of the stuff he does, or the fact that he doesn’t back down, but does anyone actually like him on a personal level?

Waiono,

“should ignore Fed Gov. Cook’s mortgage fraud? Because everybody” does it?”

What is not getting much attention seems to be that “everybody does it.” How is it possible that these GSEs (Fannie Mae, Freddie Mac) have allowed once again for fraud on government-guaranteed mortgages to spread like this? How much are mortgages infested with other frauds?

How come these GSEs were so lax again in checking the mortgage documents, and so aggressive in buying these mortgages without further checking.

They have all the data on prior mortgages for example. No one should be able to claim a second primary residence within a year.

All this stuff can be found out with a little bit of automated checking before buying the mortgage from the banks.

But it seems the government was more interested in whipping the housing market into a frenzy than in policing the mortgages it bought, insured, and guaranteed.

The agency that Pulte now runs is at fault here because it was willfully negligent.

I indeed. I agree 100%. Claiming multiple primary dwellings is rampant…still; tho less so now because of fewer sales but to my knowledge there is no check system in place. You’d think in a society in which insurance companies now “pool” data for customers just like the HMO’s do, that the feds could figure something out. Desktop approvals are a big thing. An Investor checks the “primary residence box” on multiple houses. How hard is that to audit?

Cook only got caught because finding a vulnerable Fed cheater is probably not that hard to do and she is easy pickings for Trump, who is now playing revenge hardball…He’s trying to stack the fed like he did the USSC.

VW, World’s No 2 automaker risks Trump fury with $4,100 per car hike as tariffs kick in

The announcement highlights a growing trend: automakers, already struggling to keep prices low, are passing tariff costs onto buyers.

Audi is raising prices on many of its 2026 models to cover President Donald Trump’s new tariffs.

The luxury arm of Volkswagen — the world’s second-largest carmaker — quietly released its new price list Thursday night without including last year’s figures.

Research shows increases ranging from $800 to $4,100 across about half of its lineup, with the sharpest hikes hitting gas-powered models.

Americans can and will just quit buying these vehicles for a couple of months, and buy USA-made Hondas or Teslas or Kias, and then VW will have to cut prices via huge incentives and discounts. That’s always how it happens. Sticker prices don’t matter in the car business.

Automakers have been offering deals over the past few months because demand isn’t very strong, and if they raise prices, sales plunge. Simple as that.

People still don’t understand cpi is based off transactional prices… not asking prices.

Wolf, on a not so unrelated issue. I am anxiously awaiting your article on Powells speech today.

https://wolfstreet.com/2025/08/22/powell-makes-room-for-rate-cut-fed-kills-average-inflation-targeting-that-caused-so-much-damage-when-inflation-raged/

@StPeteDave almost all first time home buyers buying a “median priced home” make well above the “median household income”. I agree that almost all homes in America are overpriced and prices should continue to decline but just like few people making the “median income” were buying new Porsche 911s when they were still under $100K few people making the “median income” were buying median priced homes even when they were under $300K.

People still don’t understand cpi is based off transactional prices… not asking prices.

So what. It’s not how the fed calculates home affordability. We are in objectively one of the worst affordability crisis of all time and it’s due to the prices.

Don’t believe me – check out Atlanta fed affordability monitor for yourself

This is a good article on the current problems in selling a home in todays environment.

from Business Insider: “The Mortgage Buydown Backfire”

You have already predicted many of these things: home sellers competing against new home builders, negative equity, etc.

Some interesting quotes from the article:

“I’m hearing more and more stories of buyer’s remorse,” says Jess Uphoff, a mortgage lender who previously worked for a homebuilder. Not long ago, a temporary buydown seemed like a win-win: Builders could keep list prices higher while still passing along savings to buyers in the form of lower monthly payments. But if one of those buyers is trying to sell now, they’ll likely be competing against the same builder who sold them their home — “only the builder has been steadily lowering prices or layering on new incentives.” Uphoff says. “That means homeowners often can’t resell for what they originally paid.”

and from another broker:

“Where I’m running into challenges right now is with the people who bought a couple of years ago that want to sell,” Dempsey tells me. “I’m bringing estimated net proceeds that have negative numbers attached to them, so the seller has to bring cash to the closing. And I know I’m not alone in that right now.”

One guy in the article sold two homes. He made six figures on the first and lost it all on the second. He is now living in an apartment and a little wiser.

If you can’t afford it, don’t buy it.

Take a few years, save money, then buy it.

If it doesn’t work out, you will survive.

If you think you ever own your home, you are a moron.

Try not paying property taxes to the bureaucrats.

Then you will find out who owns your home.

Simple