10-year and 30-year yields rose after rough auctions, despite huge issuance of T-bills to take pressure off long-term yields.

By Wolf Richter for WOLF STREET.

This week, the government sold $724 billion in Treasury securities spread over 10 auctions, held on four days. Of these sales, $505 billion were bills with maturities from 4 weeks to 52 weeks, including $100 billion of 4-week bills; and $219 billion were notes and bonds, including a somewhat rough auction of 10-year notes and what was called an “ugly” auction of 30-year bonds.

| Type | Auction date | Billion $ |

| Bills 13-week | Aug-4 | 86.6 |

| Bills 17-week | Aug-6 | 65.2 |

| Bills 26-week | Aug-4 | 77.1 |

| Bills 4-week | Aug-7 | 100.3 |

| Bills 52-week | Aug-5 | 52.8 |

| Bills 6-week | Aug-5 | 89.7 |

| Bills 8-week | Aug-7 | 85.2 |

| Bills | 556.8 | |

| Notes 3-year | Aug-5 | 77.7 |

| Notes 10-year | Aug-6 | 56.3 |

| Bonds 30-year | Aug-7 | 33.5 |

| Notes & bonds | 167.4 | |

| Total auction sales | 724.2 | |

This is the Mississippi River of debt, as we’ve come to call the massive flow of hundreds of billions of dollars sold at auctions every week that the market has to absorb.

This heavy skew toward T-bills puts a lot more T-bills out there that then mature constantly since they’re so short term (between 1 month and 12 months). All these maturing T-bills will have to be refinanced, on top of the issuance needed to fund the ongoing deficits with new T-bills. So the already huge T-bill auctions will become gigantic.

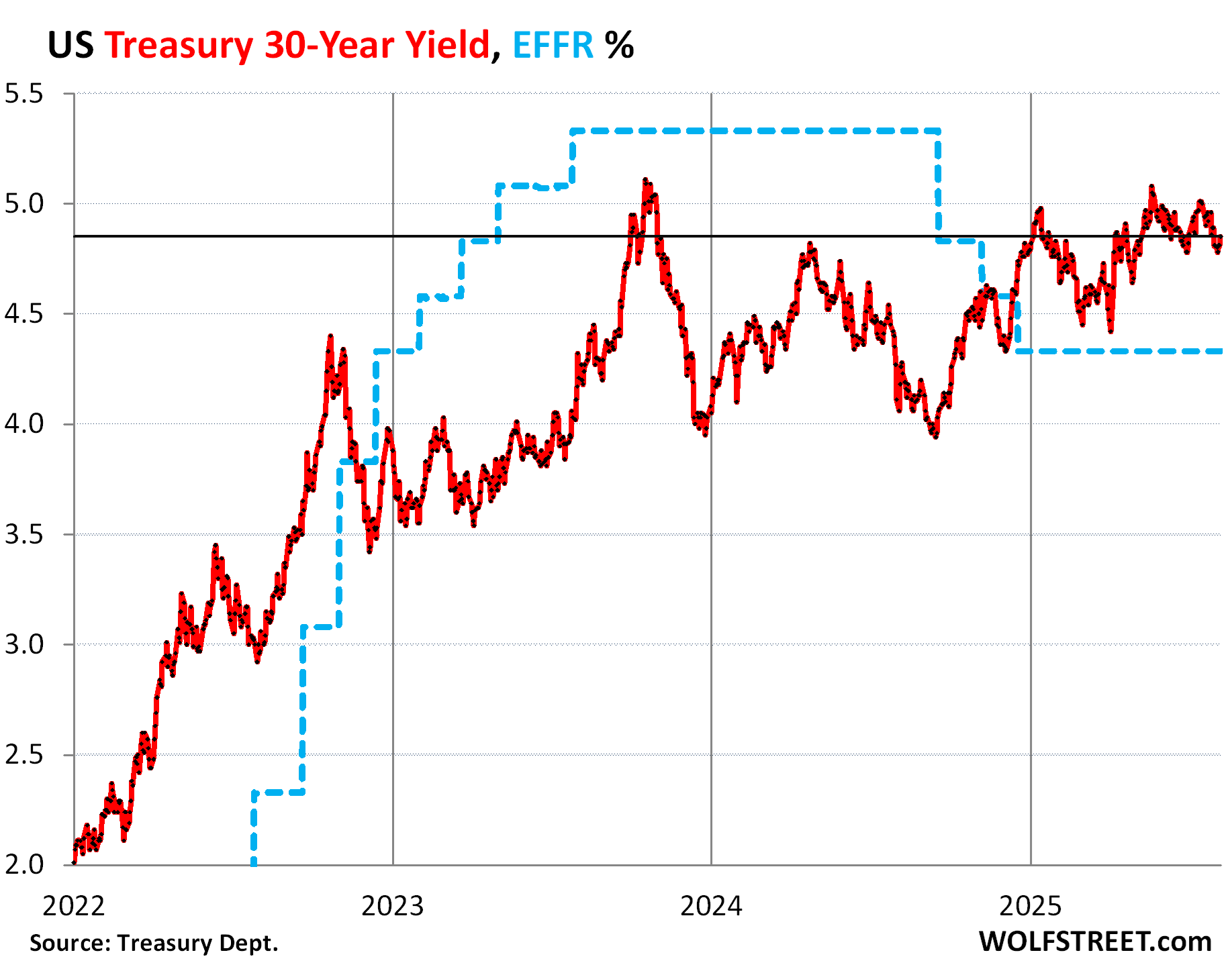

Despite the heavy skew toward T-bill issuance to take pressure off long-term yields, the 10-year yield rose by 7 basis points over the past four days to 4.29% today.

The 30-year yield rose by 9 basis points over the past four days to 4.85% today. It has been nervously clinging to the upper portion of the range of the past three years.

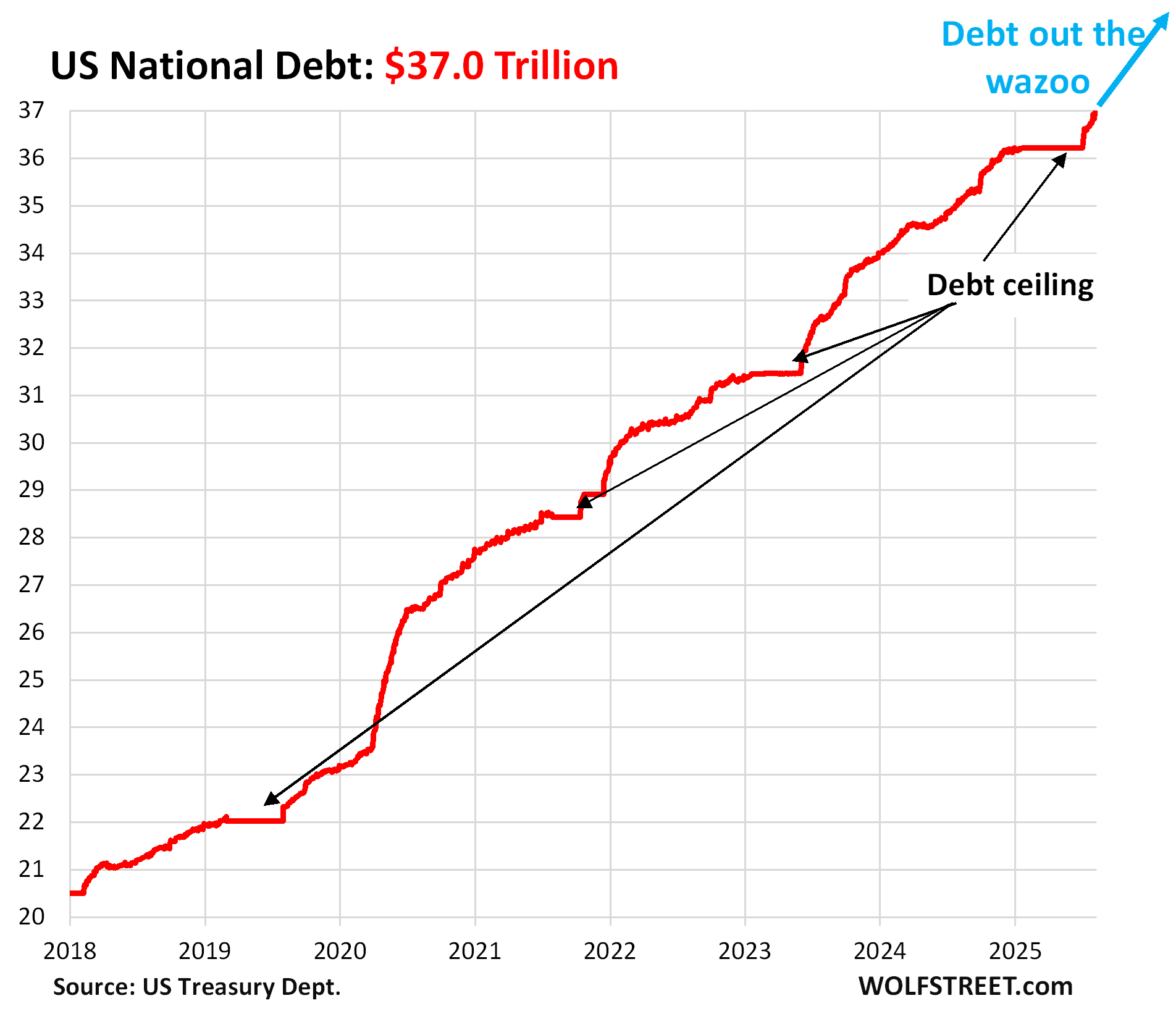

Recklessly ballooning federal debt hits $37 trillion.

Some of this new issuance replaced maturing debt and did therefore not add to the US government debt. The rest funded the new deficits and helped refill the government’s checking account, the Treasury General Account (TGA) at the New York Fed, which had been drawn down substantially during the debt ceiling period. That portion of the issuance increases the US government debt.

Some of the bills that were sold this week were then “issued” this week and became part of the overall debt. The remaining bills will be issued next week, and the notes and bonds sold this week will also be issued next week, and they will be added to the overall debt next week.

The total debt by the federal government jumped to $37.0 trillion (to be precise: $36.996 trillion), as of Thursday evening and reported Friday evening by the Treasury Department. It doesn’t yet include the portion of the securities that were sold this week but will be issued next week.

In a little over a month since the Debt Ceiling, the debt has spiked by $780 billion.

The flat parts in the chart reflect the periods of the Debt Ceiling – or, as the illustrious WOLF STREET commentariat said so poignantly, the “new debt floor.”

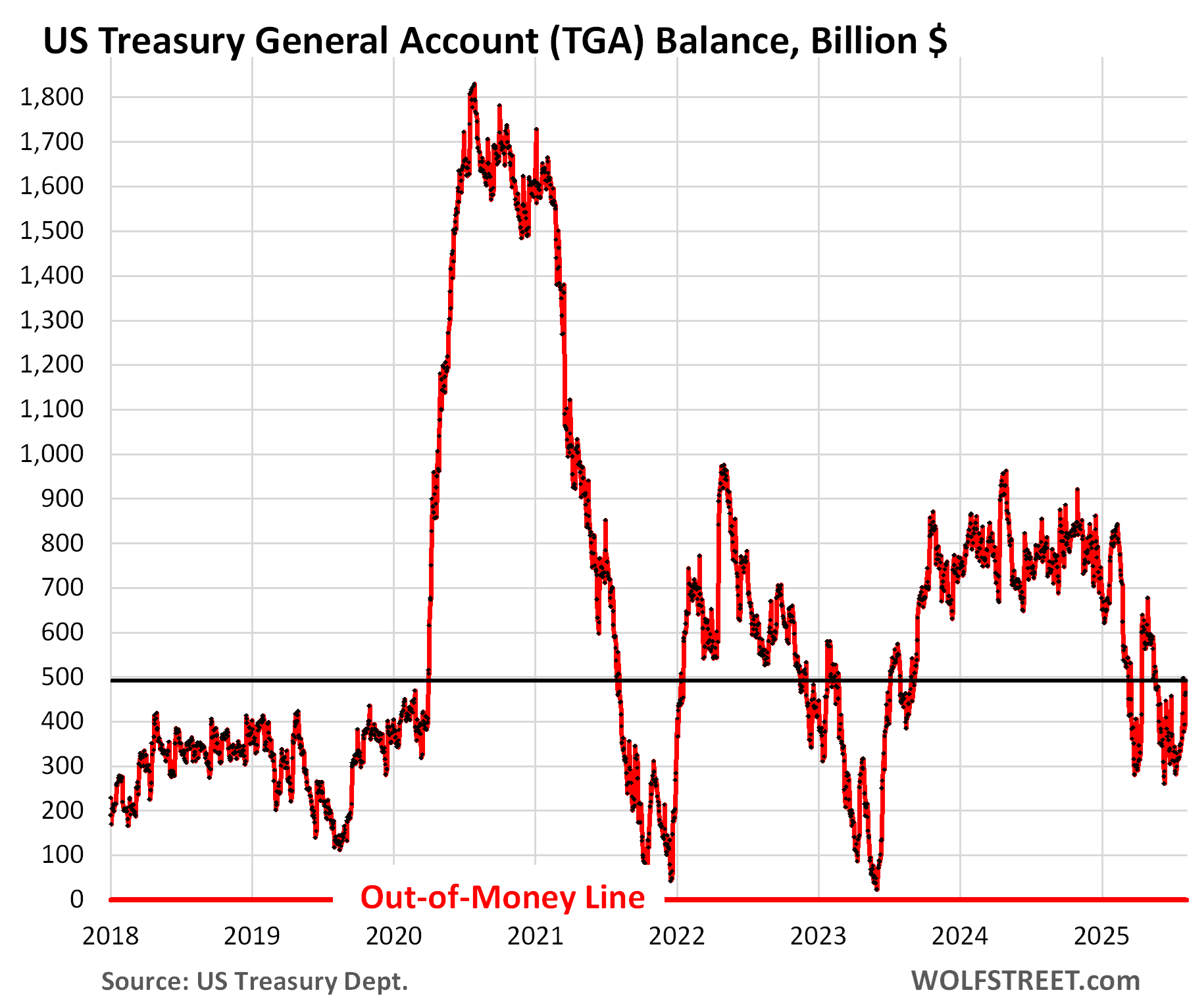

Refilling the TGA.

This additional $780 billion in new debt since the Debt Ceiling was used in part to fund the deficits, and in part to refill the government’s checking account, the Treasury General Account.

The TGA bottomed out at $260 billion on June 12. Then came a flood of quarterly estimated taxes due on June 15, plus the new tariffs that pumped an additional $20 billion a month into the TGA account.

And before the TGA had a chance to drain further, Congress lifted the debt ceiling. And since then, the TGA has risen by $178 billion and now holds $492 billion, according to the Treasury Department today.

The desired level of the TGA is $850 billion by the end of September, according to the Treasury Department. So roughly $350 billion in new issuance more to go to refill it, on top of the new issuances needed to fund the ongoing deficits, and on top of the issuance needed to refinance the maturing debt.

T-bills and the Fed.

The Fed has for a long time been discussing – including most recently Fed governor Waller who is angling for the chairman job – how it wants to shift the composition of its $6.6 trillion balance sheet toward T-bills.

It wants to get rid of its $2.1 trillion in MBS entirely, which could include the outright sale of MBS to speed up the process. And it wants to reduce in a big way its $4.2 trillion in Treasury notes, bonds, and TIPS, even as QT continues.

With this shift, the Fed would absorb over time $3-4 trillion in T-bills and in return throw $3-4 trillion of MBS and Treasury notes, bonds, and TIPS at the market that the market will have to absorb. That massive shift from long-term to short-term securities by the Fed would normally push up long-term yields and cause all kinds of problems in the bond market.

There are currently only $6 trillion in T-bills outstanding, and if the Fed needs $3-4 trillion in T-bills over time, there aren’t nearly enough T-bills outstanding for the Fed to shift into T-bills. So the Treasury department has started to issue a lot more T-bills so that the Fed can shift into them.

At the same time, as the Fed shifts its long-term securities into the market, the Treasury Department is not increasing by much the issuance of long-term securities, so that the market doesn’t get flooded with long-term securities from both directions.

The Treasury Department and the Fed – perhaps at Powell’s and Bessent’s weekly breakfasts – are clearly coordinating these massive multi-trillion-dollar shifts, and they will have to coordinate them before the Fed even starts shifting from long-term securities to T-bills, or else there are going to be some fireworks in the bond market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Nothing in the world’s more expensive than ‘free’.”

DB Cooper’s lament about the deceptive nature of “free” is apparently not that free is a ripoff like “cheap,” but rather that because free comes with conditions it is hardly a bargain at all.

I would like to add to DB that in living a greedy existence of trying to save a dollar at every corner, we are more often than not being penny-wise, pound-foolish, stressing ourselves unnecessarily, and living a broken existence where the cost of everything is known and the value of nothing is appreciated.

Is the cost of health care known?

“ a greedy existence of trying to save a dollar at every corner, “

Saving is greedy?

Work…..then preserve what you earned is greedy?

What I don’t see in the comments is the 2 primary drivers of that debt being mentioned. The first is literally spending too much, especially on Defense. And the second is obviously not taxing enough. Primarily not taxing the Rich and Corporations enough and hoping for the elusive Trickle Down. Hope is not a strategy. Continuing to put debt on the Government Credit card is a BAD strategy.

spoken as a true “warrior of the proletariat “.

49% revenue from Income tax, 35% revenue from SS, Medicare, Medicaid payments. Roughly 84% from people and corporations are paying 11%.

Rug pulls creates 1 winner 99 victims 🌞

Wolf’s recitation of the facts is a litmus test for challenging one’s pre-concieved ideals.

The 30-year yield rose by 9 basis points over the past four days to 4.85% today.

The absurd feature is that this debt is selling at a market price that discounts the risk as near zero.

For the next 30 years which previous experience is not predictable and therefore the 10 year should be over 5+ pct in a free market environment.

I’m right with you on that, Dang, as some of us would expect these yields to be higher. Yet recently, every time the long-term treasuries (20-year and 30-year) have punched above 5%, there seems to be so much demand dragging the yields right back down. Meanwhile it would seem that Bessent at Treasury and Powell at the Fed are both working in tandem as a “tag team” to balance short-term versus long-term treasury transactions in a concerted effort to keep a lid on these yields. Where are the new generation bond vigilantes?

Long end of the curve doesn’t look convinced about a cut in September 🤔

It doesn’t look convinced about inflation just going away. It looks very nervous about inflation.

This is the way the curve reverts. Short term pushed down by hopeful toadies, long term pushed up by sensible adults.

IMO the long end of the curve doesn’t know which is the likely path of short term interest rates. Falling interest rates are a harbinger of the monetary stimulus to the economy that a reduction in interest rate provides. A bowl of sugar saturated advertising.

The demand for monetary stimulus suggests that the American economy is faltering.

There was a related story that I was wondering about; an op-ed on Bloomberg back in mid-July which read in part:

“…Treasury Secretary Scott Bessent has advocated a different approach [than fixing the budget]: shifting issuance of government debt toward short-term bills. Recently the average maturity of outstanding Treasury securities was about 71 months, a bit above the 64-month average since 2000. Bessent thinks the government can save money by borrowing at shorter maturities instead of locking in today’s high rates, which he expects to decline in the future.

If pursued aggressively, Bessent’s idea would signal a significant departure from the US practice of “regular and predictable” debt management. For more than 40 years, the Treasury has sought to convince investors that it won’t trade against them — that its genuine financing needs, rather than opportunism, drives the composition of its debt issuance. This has been viewed as the best way to minimize borrowing costs overall, across time and maturities.”

Several articles on this said that everyone was waiting for the July 30 “quarterly refunding plan” to see where they were going with this. How did that end up looking?

So we have A) a wager that long-term rates are going to decline, and B) a strategy which risks creating a perception that the treasury is “trading against” the market. How do we see that playing out?

None of this is my area of expertise so I’m not even going to speculate.

A very similar approach wit ARMs (Adjustable Rate Mortgages) was being used with housing back in 2005-2007 which for a short time made mortgages ‘much more affordable,’ but how’d that work out in 2008-2009? By the way, Scottie, won’t be running for the Federal Reserve in 2026.

Read the last section of this article, sub-heading: “T-bills and the Fed.”

And read it very carefully so you understand.

Does this needing to have T-bills to shift into have anything to do with program where they buy long bonds issued with a very low coupon at depreciated prices and replace it with new debt? I thought it was just a way to help make banks clear a bad “hold to maturity” portfolio

They buy some notes and bonds with low coupons at big discounts, and they buy more recent notes and bonds with big coupons at a premium. They’re buying “off-the-run” securities across the board, some at a discount, some at a premium. The discount purchases are usually bigger than the premium purchases.

But total numbers are minuscule, just a few billion a week. It’s way too small to have impact on anything except provide easier trading (liquidity). Not related to the banks. They can sell their bonds in the market, and the Fed is paying market price, same difference.

And just a reminder: the Treasury buybacks involve no money printing. The Treasury issues new securities and uses some of the cash raised to buy back older securities. It’s just a swap of older securities for newer securities at market price.

One thing I haven’t seen discussed anywhere is the expected impact on treasury rates when the Social Security Trust Fund has to exhaust its treasury holdings over the next 8 years and then that debt has to be publicly financed instead.

borrow short term for long term obligations. We all know how that works out in the fullness of time.

Re: “ (between 1 month and 12 months). All these maturing T-bills will have to be refinanced, on top of the issuance needed to fund the ongoing deficits with new T-bills”

I think that’s the magic trick that’ll bite them in the butt — this massive Mississippi flood of issuance that continually gathers momentum and speed — with more issuance, re-issuance and of course, increased interest costs.

This is totally disastrous — period!

Is this akin to the rabbit in the python’s throat scenario? In the not too distant future these plentiful T-bills will choke the supply/demand pipeline. Hopefully the U.S. Govt will be able to digest them but at what cost, i.e. unacceptably high yields, or worse yet the bills will become indigestible?

I have been thinking about the T-bill market in which many people have their savings invested because the long term is obviously fixed.

Risk has been deleted in the valuation equations used to justify the absurd prices.

Wolf, is there likely a point where the 6m or 12m rate decouples from the Fed rate? Right now they’re anchored to expectations of the next year’s worth of Fed meetings. But if the Fed rate goes below inflation, is a revolt even in the short term Treasury market theoretically possible?

They run on rate expectations, and those rate expectations could be off, and then correct, and so you get volatility.

The strategy of selling its long-term QE holdings, $4 trillion roughly is problematic since the average yield on these securities is about 2%. The fed would have to take immediate and significant losses if this done in year ahead. Their mark to mark losses on total QE portfolio is over $trillion I believe. How do they hide downside of the absurd amount of QE done during beginning of pandemic?

1. Losses don’t matter to the Fed.

2. They’re not planning to sell the Treasuries, they’ll continue to run off when they mature; they’re planning to sell the MBS ($2.1 trillion left), and losses are much smaller because the buyer gets the passthrough principal payments at face value. If they sell $40 billion a month in MBSs, it’s not a biggie.

The idea that there is some big shift with the QE holdings is obviously incorrect. it will take years for this supposed adjustment to take place, if it does at all.

Hopefully, if there is a new policy, it will be to finally stop doing QE once the vast majority of balance sheet holdings run off in 5-6 years?

The short term t-bill explosion makes perfect sense given nobody expects short term rates will go up but conversely will likely decline over the next year or two, then they can issue more long term. For now the appetite seems to be there for US debt, even at lower yields. How long that holds up is a big question though, as really seems no likely path back to fiscal sanity.

The path back to fiscal sanity will occur when the treasuries stop selling.

There is no path to fiscal sanity.

I can assure you after few years debt would be 100 trillion and we’d still be talking like this .

“…everybody knows there’s no such thing as sanity clause!”

-Chico Marx

may we all find a better day.

The FED has been offloading MBS’s for quite a while now.

All this time i speculated they see trouble in mortgages coming and don’t want to be the bag holder. According to the latest news, the housing market is not as ‘hot’ as it was. The FED must have a good crystal ball there. Or even a Palantir. hmmm

No, the Fed holds only “agency MBS” — meaning they’re issued and guaranteed by the US government (Fannie Mae, Freddie Mac, Ginnie Mae, etc.), and all the credit risks are with the government. If those mortgages blow up, it’s the taxpayer that is on the hook, not the MBS holders, such as the Fed; agency MBS have a similar credit risk as Treasury securities, which is essentially zero.

The primary reason why the Fed wants to get rid of MBS is that they’re unpredictable in terms of when they come off the balance sheet: they leak off the balance sheet on a monthly basis in unpredictable amounts as unpredictable mortgage principal payments (mortgage payoffs from the sale of a home, refis, and mortgage payments) are made and passed through to the MBS holders.

Yes, looking forward to the re-inversion of the yield curve. The space between the rock and the hard place for the Fed keeps getting smaller…

Thanks Wolf. Seems like a shortage of liquidity and higher rates because of all the money needed to absorb t-bills, mbs’s. Qt is taking it out right?

The personal savings rate is lower than pre C-19

https://fred.stlouisfed.org/series/PSAVERT

The FED has to eliminate the artificial suppression of interest rates, i.e., paying interest on bank reserves. We need high real rates of interest for saver-holders.

This is distorting the savings->investment allocations away from the bond market. It skews asset distributions, stoking alternative asset price inflation, as Bernanke foretold. MMT has been denigrated.

“Neither borrower nor lender be

For loan oft loses both itself and friend

And borrowing dulls the edge of husbandry.”

I don’t pretend to understand half of this stuff so this question might be foolish. Who would be willing to purchase the Mortgage Backed Securities if the general indicators point to a devaluation in the housing market?

“Who would be willing to purchase the Mortgage Backed Securities if the…”

The Fed holds only “agency MBS” — meaning they’re issued and guaranteed by the US government (Fannie Mae, Freddie Mac, Ginnie Mae, etc.), and all the credit risks are with the government. If those mortgages blow up, it’s the taxpayer that is on the hook, not the MBS holders, such as the Fed; agency MBS have a similar credit risk as Treasury securities, which is essentially zero.

The primary reason why the Fed wants to get rid of MBS is that they’re unpredictable in terms of when they come off the balance sheet: they leak off the balance sheet on a monthly basis in unpredictable amounts as unpredictable mortgage principal payments (mortgage payoffs from the sale of a home, refis, and mortgage payments) are made and passed through to the MBS holders.

Re: “ It wants to get rid of its $2.1 trillion in MBS entirely, which could include the outright sale of MBS to speed up the process”

That topic goes way back to post GFC and the belief and hope, that the Fed would never sell their MBS at a loss — because that would send a very bad message about their ability to manage money — selling at a loss would send multiple shockwaves and destroy confidence. I guess that’s one way to end the Fed.

We’re already seeing the Fed not making a profit, so what better way to dig their hole deeper — while Treasury is simultaneously flooding the market with compounding issuance, and paying higher and higher interest on the deficit.

We’re also seeing foreign debt traders becoming more skeptical about our banana republic debt policies — if we continue down this path, fewer people will invest here.

Re: “ With this shift, the Fed would absorb over time $3-4 trillion in T-bills and in return throw $3-4 trillion of MBS and Treasury notes, bonds, and TIPS at the market that the market will have to absorb”

Correct me if I’m wrong, but if Fed sells these MBS at a loss, won’t that require Treasury to issue even more bills (than currently forecasted) — that loss has to be coordinated between with Treasury or Fed????

1. Losses are irrelevant to the Fed. The Fed has been making losses since Sep 2022.

2. The capital loss from selling the old MBS will be over time balanced out by higher yields from T-bills and by lower interest expenses (paid on reserves) as reserves would shrink. Yield works that way. If a life insurer sells a 30-year Treasury bond bought in 2020 at a 40% loss, it then reinvests the funds in higher yielding 5% bonds, and over the next 25 years it balances out, and offers advantages to the life insurer. Yield works that way.

3. If the Fed sells $40 billion in MBS a month, the monthly losses would be fairly small. The losses on MBS are much smaller than regular bonds because MBS make constant passthrough principal payments at face value that the buyer of the MBS will get, on top of the interest paid on the remaining balance.

4. “Fed would never sell their MBS at a loss — because that would send a very bad message about…” is Wall Street BS, in the same category as back then, “the Fed will never do QT,” or “the Fed will never hike rates again,” and “the Fed will cut rates into the negative.”

I think the point is the treasury doesn’t want to issue longer-term debt when they know in 1-2 years overnight rates will be 1% as trump dictates to whomever becomes next head of fed. Maybe all members don’t go along with that, but the fact is it costs fed government roughly $300 bill at least by having rates at 4% versus 1% in future. So bond investors will be stuck once again with negative real rates in shorter maturities.

Hopefully, those holding longer debt demand more yield for a government that seems help bent on borrowing more every year 6-7% of gdp, when nominal growth only in 4-5% range. As someone else here already said – Banana Republic type policies.

1. Trump dictates a low tax rate

2. Inflation goes up

3. Market loses confidence on the dollar

4. Rates go up

Right, here’s what I think they think.

They’ll load up progressively more on the front end of the curve via bills as rates come down. That seems dumb to us, because we think long rates will rise as the Fed lower o/n rates. But the admin doesn’t think that will happen. They believe that inflation will get squashed from Trump’s love for increased energy production, browbeating pharma and other CEOs, etc. And if that fails, they’ll just keep saying inflation is a one-time hit from tariffs, or there’s no inflation or that CPI or whatever is rigged. With the long end suitably lower, they’ll borrow more long term.

But really, this is not an administration that’s going to lose sleep over a kicked can. If they can’t finance at lower long rates, they’ll tilt more and more toward bills.

The point for whom? Delusional dreamers?

Markets have already lost confidence in the dollar, which is why people are willing to trade their dollars for overpriced tech stonks.

Well said, Gattopardo. Do they actually think DOGE cuts/tariff increases will reduce inflation, alongside tax cuts and insane levels of spending? My guess is they sure hope so but they know otherwise and just don’t care- or are spineless to stand up against it. So they’ll double down on the short end over the next few years, blame inflation on literally anything (which will get lapped up), and watch with amusement as we get closer and closer to the tipping point. And honestly we deserve it.

Most of those MBS are government guaranteed. So they will be made whole in terms of dollars. Risk has left the building. As for housing, it is mostly the burn rate in current dollars that is the problem. Houses require an endless flow of money to keep afloat, taxes, insurance, upkeep, etc. And if they are empty, they devalue fast- especially if you get squatters.

Stock and flow questions. As for finance, well, it becomes a wasting asset, one that has to flow to make it work. Stagnant pools, and untended gardens.

Someday this war’s gonna end…

The fed will lose $40 bill financing just this mortgage piece of QE balance sheet given yield of portfolio is 2% and financing cost 4%, do not exactly risk free.

There seem to be no answers to your big questions, but it is possible to do small things that are likely in the right direction. One you mention is keeping gold in a Swiss vault (not a bank). Anyone can buy a few Eagles and take a short trip to Zurich to open a safe deposit box. It may seem far fetched, but really not, and it’s quite doable.

Concentration on the front-end of the yield curve will suck money out of the commercial banking system, increasing the supply of loanable funds.

The banking system is drowning in a vast amount of excess funds now and that has been the case for many years.

Scott ordered Jagermeister🦌,but he’ll get served Hamms 🐻.

Wolf:

Re “Government sold $274…”

Based on your analysis, what is your best estimate of the level of short, medium, and long term US Treasury rates over the next few years? I am asking as a retired income investor.

Even if the Fed drops overnight rates, might short rates otherwise remain stable or even rise due to the elevated supply? Re long rates, could the relative decrease in supply be sufficient to counter concerns about inflation? My feeling is that rates over all maturities could remain relatively stable, or increase.

I’m not expert in bonds at all, but if I’m reading this right, the Treasury and the Fed are colluding to expand US debt by adding and then buying $Ts of T-bills while unloading long term debt, thereby hoping to prevent a meltdown in the long term bond market. If that’s right, what’s the plan when they’ve soaked up all the T-bills? Doesn’t that just weaken the US even further and open up further vulnerability to the debt markets?

Thanks wolf

What would happen if say the Fed cuts rates 75 basis points but the 10 year bond doesn’t respond much?? The debt market is so huge now it seems possible the government/banks can start losing control and if we keep getting weak jobs #’s rates will need to go much lower to get the housing market going again……..

I think a loan shark would recognize this tactic

OK, I think I have a blind spot on this and I have forgotten most of the more technical finance stuff that I used to know, so maybe this is a stupid question…

Taken to an extreme, what would happen to long term mortgage rates if the government started to sell only the short term securities?

Let’s say they didn’t offer any more 10 year or 30 year, whatever, securities.

There are certain types of funds who are obligated to hold long-term securities in their portfolios, would they be obligated to buy a limited amount of mortgage backed securities’s and drive the rates way down?

This administration doesn’t care much about historical precedent or norms, isn’t it possible they could do this to lower long-term rates, juice the housing market again, and benefit real estate holders?

I’m pretty negative on the real estate market in general, but I’m not sure why this couldn’t happen if somebody was trying to put their finger on the scale…

These crazy extreme hypotheticals fall apart before they hit the ground. The sun will rise tomorrow. It’s a waste of time to speculate on what would happen if the sun doesn’t rise tomorrow.

I believe, the world saw enough paradigm shift in the last 10 or 20+ years (internet, GWOT, great recession, QT, Millennials, Crypto, Trump, COVID, BRICS, GenZ, AI and so on). The shift means, 30 years become the new T-bills, and T-bills become the new 30 years. This is the new, new thing…No body know what happens but accept and move on…

Black Rock is short US debt.

‘The rising supply of US government bonds will increasingly need to be financed by price-sensitive domestic buyers since global investors currently lack a yield incentive to increase allocations to increasingly risky US debt.

Across portfolios, like the BlackRock Tactical Opportunities Fund, we remain short 30-year US Treasury bonds outright and short US fixed income versus more austere and attractively priced markets like the UK, Eurozone, and Sweden.’

Elsewhere BR adds: ‘The US Treasury is issuing about 500 hundred billion a week in new debt, as foreign buyers begin to pull back’

RE: the last about the ‘500 billion per week of new debt’

I checked back in case they had said 500 million, because 500 billion a week would be two trillion a month, which seems too high to be true. But that is what they printed.

Also, they say ‘new debt’ but if it’s replacing long bonds is it new ?

So BlackRock is a fund manager, it’s not their own position but their clients’ positions. What they’re saying is that on net, their clients are short longer-term Treasury yields, meaning that on net, BlackRock clients expect longer-term yields to rise. I think that’s a valid expectation.

As you point out, they’re talking about replacing maturing T-bills mostly, and the much smaller amounts of maturing notes and bonds, that’s over $500 billion a week. Replacing maturing securities with new securities adds no additional debt, it just rolls over every week a portion of the existing $6 trillion in T-bills, plus some notes and bonds. If that $6 trillion grows to $12 trillion over the next few years, as the government adds to the supply of T-bills, they will have to refinance about $1 trillion in T-bills every week. I would expect that to go smoothly, but if there is any kind of accident, such as a debt ceiling fight gone awry, it would quickly throw huge amounts of T-bill redemptions into doubt. And that would be a mess – even if temporary.

Nearly all of the US Treasuries (borrowing) by the US government should be done on a long-term 10-year to 30-year basis as the debt is simply increasing and not diminishing. It is pointless to issue it for short terms and as bright as taking out a 1-year ARM on a residence.

The borrowers decide what they will buy and how much return they want to lend their money. The long bonds are falling out of favour with the buyers. The US govt can’t force them to buy at a rate the US govt likes.

The US Treasury certain can stop issuing such a large quantity of short term bonds (below 10 year) and those buyers will have no place to put new funds but for long term bonds of 10 to 30 year duration.

Or as Blackrock advises, move to the bonds of more ‘austere’ economies, and it’s not hard to find some more austere than the US.

Not if you rely on solar off the grid!

There seems to be no mention of the obvious financial move to make when the debt becomes too much. The United States can just declare bankruptcy; typically countries have quietly traded old money for new money with a cap on the amount that can be converted.

The serfs keep their cash with no rabble in the streets. Since foreigners hold the Treasury securities, then just do them like tariffs and take their cash; what are they going to do? Not buy anymore? Anyways, don’t need to borrow to pay interest anymore; going to get there eventually no matter what.

Unless the Fed’s, in a genius move, are setting up foreigners for an enormous one time “score” of the dollar’s goodwill. Just send foreigners crates of old money dollars from the warehouse and bags of the turned in old money, paid in full.

The Argentine Solution to govt debt has not played out well for Argentina.

It also didn’t turn out well for one of the ‘Big Six’ Canadian Banks, Bank of Nova Scotia. BNS for some reason had a big presence there. The favourite way to save there was a US$ account, to avoid the Argentine peso.

BNS had lots of them. Then one day the govt swooped in, took the US $, and replaced them with pesos. Women were outside BNS shuttered doors for months banging on pots and pans. BNS bailed, its stock took a big hit, now years later recovering.

There are no provisions whatsoever in the US bankruptcy laws for either states or the federal government to be able to file for bankruptcy. The Federal Reserve has been tightening money for years. 100% of the federal debt has been run up by CONGRESS and not the Federal Reserve and is due in full with interest by its citizens to its array of creditors.

The US declared BK when Nixon screwed gold redemptions for dollars.

LOL, gold bug stuff

Is that why China, Russia and India are hoarding gold? They’re bugs?

You’re descending into gold buggery BSdom.

Your phrase “The US declared BK when…” is a braindead bullshit lie. So maybe you meant it as a dumb joke, and then hahahaha, but sounds like you were serious? In that case, it’s gold buggery BSdom.

Look, gold is a valid long-term investment, but don’t lie about history to support your stance.

I hear you, however, BK is typically a reorganization of debt. If the gov’t decides (and did) to trash the gold backed dollar with controlled inflation then a reorganization did take place. The end result has not been kind to the vast majority of Americans(massive shift of real assets to a tiny fraction of the populace), much less many parts of the world. Some day your “debt out the Wazoo” will face its day of reckoning. I hold no physical gold simply because owning it brings its own problems…I’d rather grow food! Food can be shared. Gold can easily be taken by some clown with a gun!

What will these massive bills do to banks in terms of reserves and deposits? Will deposits and bank reserves disappear as fed monetises the bills?

The Federal Reserve is not ‘monetizing’ anything.

Credit-card debt declines for second straight month in June

Gas dropped to under $3/gallon here in the Swamp. I just topped off my underpowered 1.2 leter engine Mitzibushi Mirage for $15. Meanwhile Wolf is still pumping his gas guzzler hybrid and getting gouged at his “Gas Station From Hell” at $6.99/gallon. Notice no pictures from that station in months if not years.

Our gas station from hell is still over $5.

California’s gasoline tax is composed of several elements, resulting in one of the highest per-gallon costs in the United States.

Here’s a breakdown as of July 1, 2025:

State Excise Tax: This is the largest component, currently at 61.2 cents per gallon, adjusted annually for inflation and dedicated to state highway maintenance, rehabilitation, and improvements, as well as local streets and roads.

Federal Excise Tax: This tax adds an additional 18.4 cents per gallon, dedicated primarily to federal highway and transit programs.

State and Local Sales Taxes: A statewide sales tax of 2.25% applies, along with potential local district taxes, which can vary.

Low Carbon Fuel Standard Program: This program, overseen by the California Air Resources Board, aims to reduce the carbon intensity of transportation fuels and adds an estimated 5-8 cents per gallon to gas prices.

Cap-and-Trade Program: This program, designed to lower greenhouse gas emissions, adds an estimated 23 cents per gallon to gasoline prices.

Underground Storage Tank Fee: A 2-cent per gallon fee is levied on owners of underground storage tanks containing petroleum.

Drivers in California pay roughly 90 cents per gallon in total taxes, fees, and climate program surcharges, according to the U.S. Energy Information Administration. The state excise tax alone is the highest in the nation.

Wolf,

With FED shifting its balance sheet to short term/Bills, will they suppress short term rates?

With Operation Twist, they brought down long-term rates, then in TIPs market they brought down Market based expectations for inflation.

Now operation in other direction. Right now 4-weeks rate is very close to Fed funds Rate. If FED starts buying all or most of Bills, why Treasury will pay FED Funds Rates to non-FED buyers? It will be best auction for Treasury.

I understand FED wants to come out of MBS. So they need something to buy with those proceeds in order to maintain gradual balance sheet reduction. But first they have to start selling MBS.

Shouldn’t FED stay away from all those manipulations? Haven’t they learnt any lesson from excessive QE and ZIRP?

You can’t have the “boom” without the “bust” and vice versa; that is the central hallmark of a capitalist economy. Therefore, constant money manipulation is required.

Short-term financing, what leaps to mind? Bear Stearns.

Are the new revenue streams being tried by the Trump admin (tariffs, IPO’ing Freddie/Fannie, etc.) anywhere close to the new spending?

This feels like the government is taking a few freelance jobs on Fiverr while maxing out all its credit cards.

Somebody please help me understand this…

All this talk about getting rid of the existing MBSs, the whole $2.1T of it. My best guess is that most of it has a low return rate, in the 3…4% range from the free money era. Why would anybody want to buy that when they could purchase fresh ones at 7%? Or buy 30y at 4.85%? It just doesn’t make sense to me.

There is a vibrant market for these older MBS, institutional investors buy and sell them all the time. Those MBS that have low interest payments are sold at a discount to face value to get the current market yield, just like all bonds. Yield works that way.

So the Fed would sell them at a loss. But the losses on MBS are much smaller than losses on long bonds because the buyer gets the stream of passthrough principal payments at face value, not at discounted value. If they sell $40 billion a month in MBSs, the loss for the Fed would not be a biggie.

I think there’s a pool of unknowns about the MBS losses — if they actually sell the toxic legacy waste from GFC, a lot of these type govt losses have impacts and consequences, imho.

The reason I’m curious about this, is my belief that money mkt rates are heading lower — and my confidence in the integrity of investing in anything, is shaken.

Nonetheless, Yellen obviously decided against that MBS loss strategy (while goosing the economy).

Prior Fed losses are seemingly hidden in a deferred asset account which will delay remittances to the Treasury until at least 2029 — so, along with inflation slowly drifting higher, along with the Mississippi flood of Treasury issuance — both the Fed and Treasury are borrowing cash at a higher real rate — as the deficit explodes.

In that light, maybe nobody does care about Fed losses, or a banana republic Treasury (except the ancient sleeping bond vigilantes).

In theory, yields should rise if investors continually lose confidence in this casino bankruptcy — who can say?

“I think there’s a pool of unknowns about the MBS losses — if they actually sell the toxic legacy waste from GFC, a lot of these type govt losses have impacts and consequences, imho.”

Ignorant bullshit. The Fed sold ALL of the MBS it had purchased during the GFC by September 2018 and made a $2.5 billion profit on them. There was nothing hidden about it, they were kept in entities called “Maiden Lane,” they were reported on its balance sheet, and the New York Fed, which does the securities trading, reported the details on them. This was widely reported in the financial media at the time.

I’ve had it with your ignorant bullshit that you then use as foundation for your conspiracy bullshit. Start your own blog, a Substack for example, and you can post all your ignorant conspiracy bullshit there, I told you this many times already, and adios here.

https://www.newyorkfed.org/markets/maidenlane

Why buy short if there is a possibility of recession with lower revenue and higher costs, more debt, Trumps hammer on rates to 1% and sticky higher inflation.?

After reading this article my Q is what is holding 30yr bond under 5%, it should be between 5.5-6% yields already, if it’s due to Fed then we could have a problem when they do QE

The Federal Reserve is doing QT, and is not intending to do any QE.

Such Drama! All that matters is the value of the dollar (prices) and the next election!

Far right here and I will vote far left until this Trump Disease is over.

As though the far left never played a critical role in overall gov’t spending/debt aggregation? That the far left wasn’t pushing MMT?

This is a whole of gov’t problem that started to accelerate with the 2008 election. It arrives from both sides of the aisle.

Nice that you exclude GWB’s term. He took Clinton’s budget *surplus* (the only one in recent history) and turned it into massive deficits. He also was president during the GFC which was in in 2007 and at which time the whole government was writing trillion dollar blank checks to wall at to bail them out.

Or maybe you include him by saying it started to accelerate in 2008? After all, Obama didn’t take office until Jan 2009…

‘wall at’ should be Wall St. Sorry about the autocorrect :)

TDS on display

The dollar will lose roughly 50% of its value in the next decade.

Plan accordingly.

It’s called crowding out – “when government spending fails to increase overall aggregate demand because higher government spending causes an equivalent fall in private sector spending and investment.”

Pushing the Federal debt into the front-end will spark a flight from safety, a run on the US dollar. Hence the decline in the exchange value of the dollar, the rise in gold, bitcoin, etc.

Gresham’s law “bad money drives out good”

Wow, that a lot of eggs in one basket, be a shame if somebody was to accidentally knock it over.

Sellout Fed has to accelerate QT and Lower Rates

So if the Fed issues more T-bills, prices should go down and yields should go up ceteris paribus. But the Fed decides what interest rate to pay on T-bills. Hmmm.

If the FED lowers the rates,this will save the bond market and boost wall street.It will probanly inflate the real estate market.

Inflation will rise,so this will put real rates negative,which is what you need when you have such a pile of debt.

Treasuries will be more difficult to sell,but they will find a way to monetize and buy them.

Last year, when the Fed cut 100 basis points, mortgage short shot up 100 basis points. Careful what you wish for. That was a huge topic here at the time, seems you missed it.

If i understand well,you say the 10 year yield will rise sharply.

But the government will be able to borrow more short term to buy long term bonds…..You know there is no more limit to the debt level anymore….

“you say the 10 year yield will rise sharply”

No, that’s not what I’m saying. What I’m saying is that “Last year, when the Fed cut 100 basis points, mortgage rates shot up 100 basis points” which means that there is no direct connection between the Fed’s short-term rates and the bond-market’s long-term rates. If the bond market gets spooked about inflation, such as through a dovish Fed amid rising inflation, then long-term rates and mortgage rates go higher.

Your second part is BS. You need to read my articles, including about the buybacks and the Fed, including this article here. The government is buying back minuscule amounts of long-term securities, and is STILL issuing MORE long-term securities than before. So the amounts of notes and bonds outstanding is still increasing. It’s just not funding the entire new deficit with notes and bonds, and so the amounts of notes and bonds outstanding are growing. In addition, the Fed will shift its holdings to T-bills from note, bonds, and MBS. That will throw trillions of dollars of long-term securities on the market that the market has to absorb. So RTGDFA, including the last part.

before 2008 60% of the fed securities matured in less than a 1 year, afterwards it declined all the way to about 0%, today it’s 25%. I understand this is different from buying short-term securities outright but I think it’s useful to know, so I made a custom graph on FRED to show it: https://fred.stlouisfed.org/graph/?g=1LeO2

“today it’s 25%.” That much matures in 1 year? 25% of $4.2 trillion in Treasuries = $1.05 trillion that mature over the next 12 months? That’s a huge number.

On the Fed’s actual maturity schedule, I see $741 billion maturing from August through July 2026: $475 billion notes and bonds, $195 billions bills, $3.5 billion FRNs, and $68 billion TIPS.

But even $741 billion in 12 months is a huge amount. If the Fed let all of them run off without replacement, that would be a lot of QT.

Here are the notes and bonds that will mature every month through Jan 2028. The Fed buys securities to replace the maturing securities over $5 billion, and the shorter-term securities it buys are then added to the maturity schedule as shown, so it changes over time:

I WAS WRONG! sorry about that, I double counted one data series, now it shows $688 billion maturing in less than a year (as of Aug. 6) which is only %16.4. Fixed graph

The govt needs to stop issuing debt. There is no need for debt. Our government can and should move beyond that to a better method of funding. They don’t even need to bother the Fed.

Fortune reported that Musk’s DOGE team identified 14 ““magic money computers” at the Department of Treasury and other government agencies” . Just use those magic money computers to pay for anything Congress says to pay for. We could even use these to pay down the debt! Think of the benefits! We could also use these to pay for homes for all the people who want to live here, and food for all the hungry people.

Money doesn’t work that way at all.

SoCalBeachDude,

read Absur Ditty’s screen name as one word out loud. This is a sarc account.

OK, but better with a /s!

E.J. Antoni, longtime critic of Bureau of Labor Statistics, was nominated to replace Erika McEnfarter, who Trump fired. Antoni could hardly do a worse job. If the monthly jobs numbers are structurally of a preliminary nature, they should be followed by a capital Pee. In the future, I will ignore the initial jobs numbers and focus on the revisions, hoping they reflect something close to reality.

That’s why the big fat red line in all my employment charts is the three-month average, which includes the revisions. The thin blue line or blue columns are the month-to-month. I have done this for years for that reason, and I don’t pay that much attention to the month-to-month changes, though I mention them. The revisions also affect the three-month average, but to a smaller extent. Here is an example:

Trump is in the process of changing senior leadership at BLS and the Fed. Pretty soon important and critical financial data will be nothing more than propaganda. It will be interesting to see how the bond market reacts.

I will reserve my judgement on that. The BLS started to modernize its data collection years ago. In terms of CPI data, it has been using a lot of private sector data, web scraping, etc., but has been way too slow in shifting to modern tech across its data sets, and to private sector data, corporate data, etc.

I have blasted the BLS for its failed method of figuring the health insurance CPI, for example, which blew up a few years ago, but nothing changed.

This is typical of government agencies with bureaucrats that resist change. Sometimes it takes a kick in the butt to get the job done – or get it done more quickly.

So we’ll see if they try to modernize the BLS quickly, or if they try to manipulate the published data for the sake of pleasing Trump. Trump has been right about some stuff — and kicking the BLS in the butt to get it to modernize may be one of those things.

The other option is that results will be faked going forward, and that would be catastrophic. But I think the adults in the Trump administration know that.

Wolff, your views on a new FED chair kick starting a Yield Curve control on the long end just like japan did.

ZH Bullshit. They’ve been promising QE and YCC in a month or two ever since QT started in July 2022.

I dont think we see any change of the Fed balance sheet composition until a new governor is appointed. The other thing is, why should the Fed reduce their bond portfolio? My view is the Fed will start active selling of MBS, and reinvest this amount in T-Bills. And whether they restart a “Operation Twist” in the opposite direction, is a different question.