Taxpayers and investors are mostly on the hook this time, not banks.

By Wolf Richter for WOLF STREET.

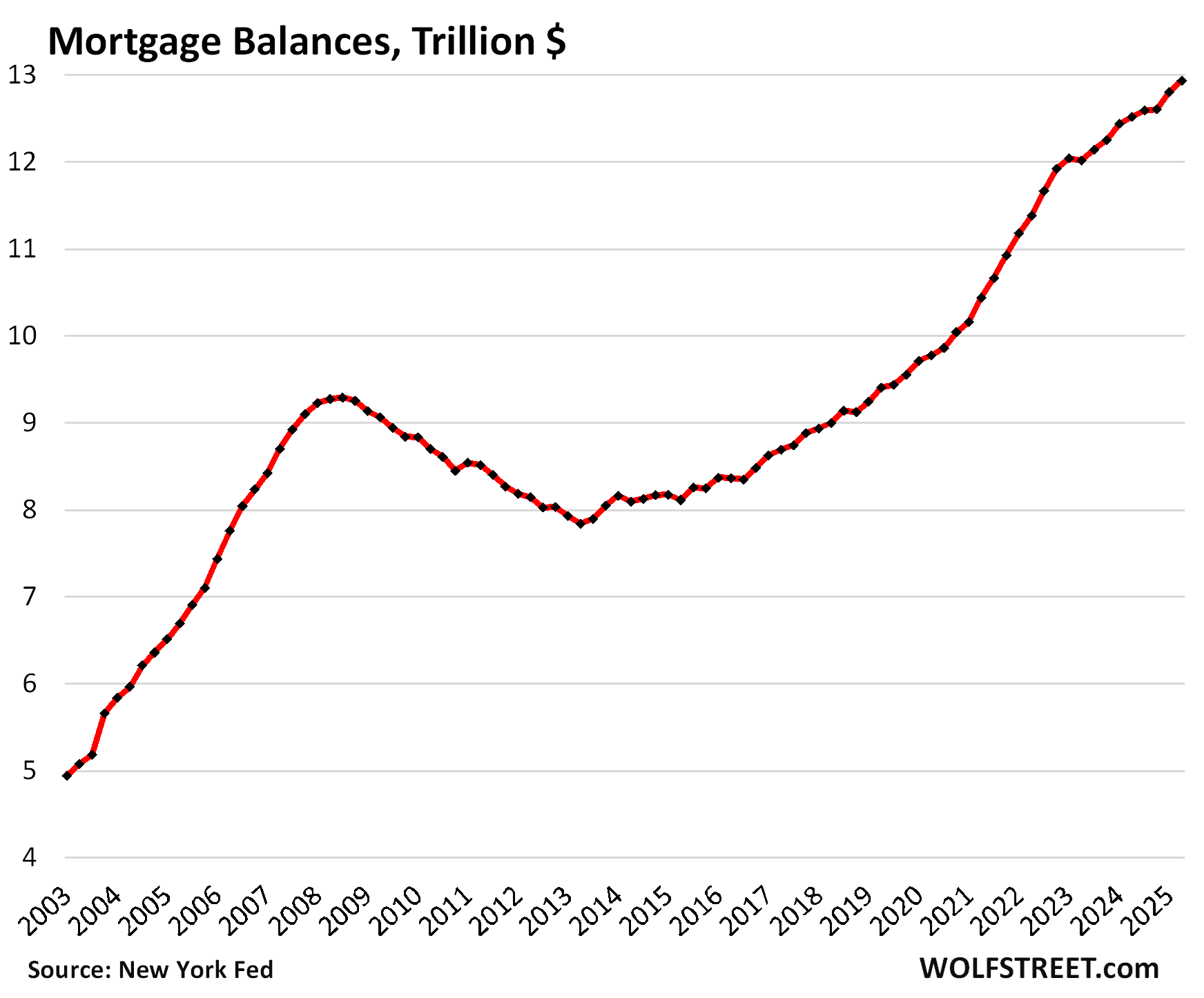

Mortgage balances rose by $131 billion (+1.0%) in Q2 from Q1, and by $416 billion (+3.3%) year-over-year, to $12.9 trillion, according to the Household Debt and Credit Report from the New York Fed, based on Equifax credit report data.

Back in 2021 and 2022, the year-over-year increases were in the 8-10% range. Since then, demand for existing homes has plunged despite spiking supply, while demand for new houses has been soft despite a supply glut.

In general, mortgage balances rise when homeowners sell their home with a partially or fully paid-off mortgage, while the buyer gets a new mortgage for most of the purchase price. Mortgage balances also rise with cash-out refinancing of existing mortgages. And they rise when homebuilders and condo developers sell a new home (population growth, employment growth = income growth and more homes), and the buyer uses a mortgage to fund the purchase. Rising home prices accelerate that process.

Mortgage principal payments and mortgage payoffs by homeowners who don’t sell (to invest a bonus check, for example) work in the opposite direction on mortgage balances.

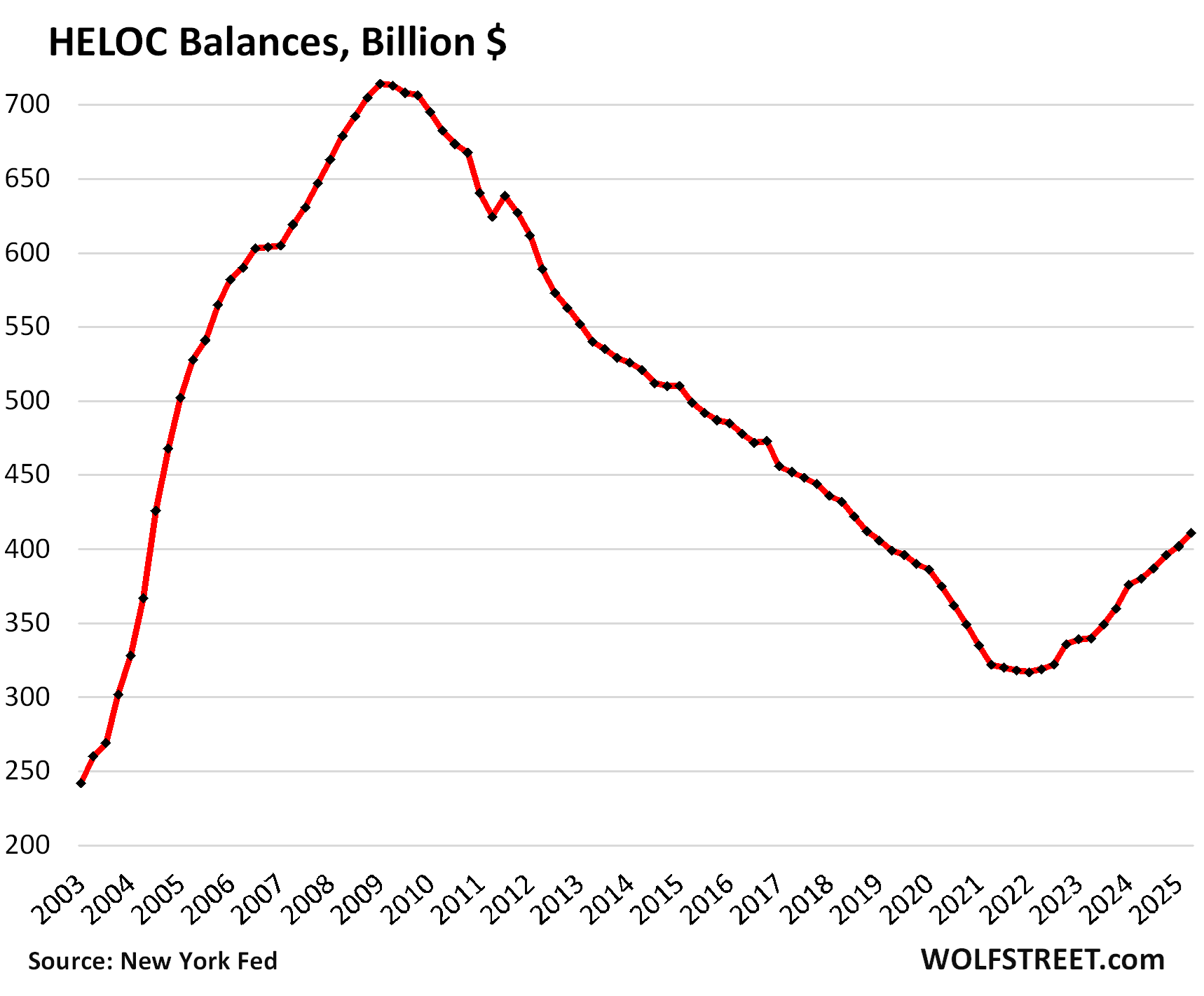

Here come the HELOCs: +30% since Q1 2021.

Balances of Home Equity Lines of Credit jumped by 2.2% quarter-to-quarter, and by 8.2% year-over-year, to $411 billion. Since the beginning of 2021, HELOC balances have surged by 30%.

During the Housing Bust, HELOCs did a lot of additional damage, and lots of lessons were learned at the time. Then mortgage rates plunged, and cash-out refinancings at lower mortgage rates took off, replacing HELOC activity. As a result, HELOC balances declined for 13 years.

So now, even after the 30% surge from those very low levels, HELOC balances are still relatively low. These are the actual balances drawn on HELOCs:

HELOCs come with a second lien on the home, and if homeowners default on the HELOC while keeping the first-lien mortgage current, they can still end up in foreclosure.

In addition, after a foreclosure, when the first-lien lender takes the home, lenders of the HELOC can pursue homeowners with deficiency judgements for the unpaid HELOC balances even in the 12 “nonrecourse” states, including California, that don’t allow deficiency judgements on first-lien mortgages.

So HELOCs come with some extra risks for borrowers and lenders – which is also why lenders charge a higher rate for HELOCs than for first-lien mortgages.

But HELOC interest rates are a lot lower than interest rates on credit cards, which are unsecured debts and can come with 20% or 30%-plus interest rates.

So homeowners can use HELOCs as stand-by lines of credit with no balance and no interest cost (though same fees may apply), to have the cash for big projects at a lower cost than borrowing on their credit cards. Or they can use it to pay off their credit cards and save some money on interest.

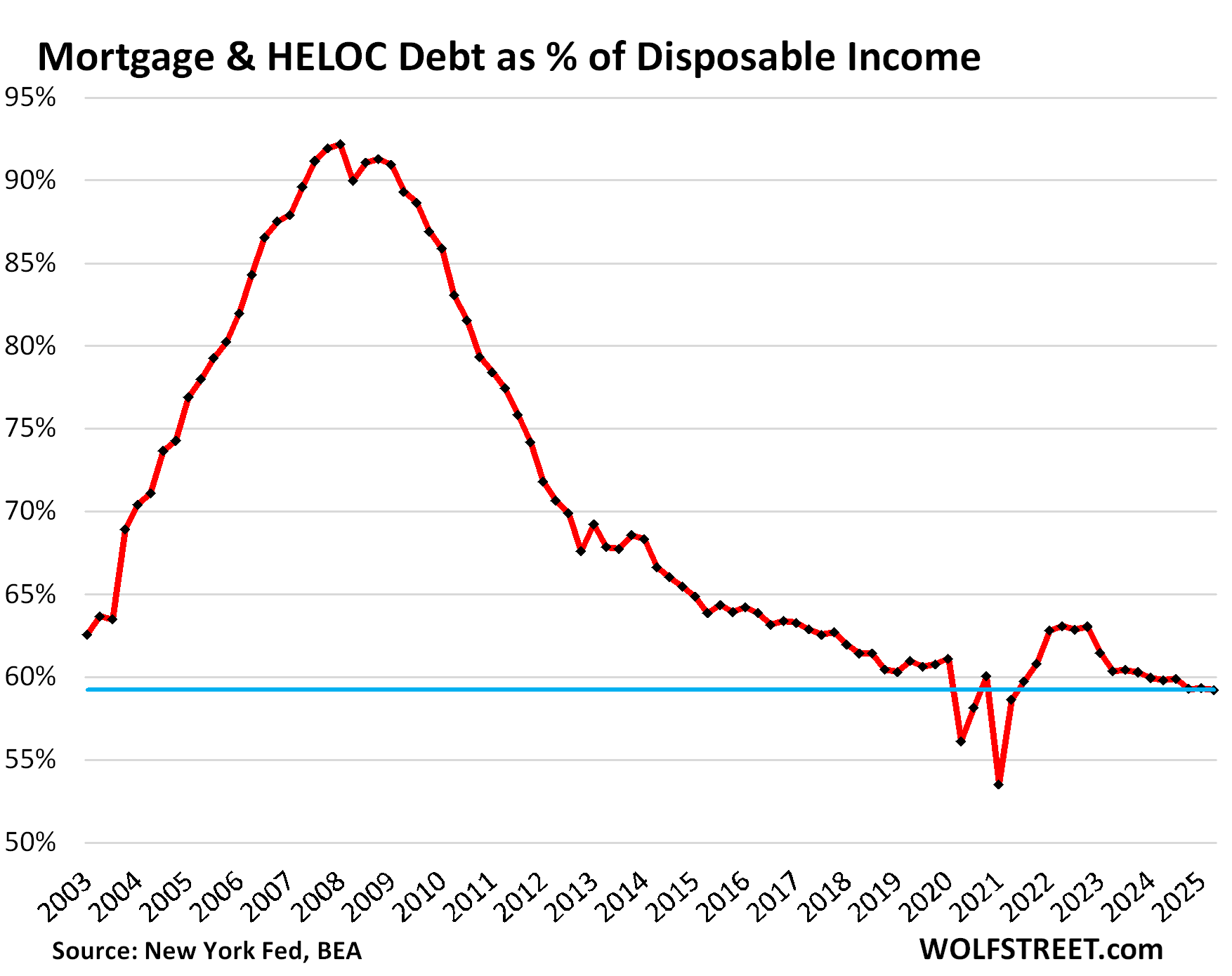

The burden of housing debt: Housing-debt-to-Income Ratio.

A classic way of evaluating any borrowers’ ability to manage the burden of debt is the debt-to-income ratio, or a debt-to-cash-flow ratio. In terms of households, “disposable income” roughly represents cash flow after payroll taxes that is available to spend on the costs of living, such as housing, food, fuel, healthcare, etc., and debt payments.

Disposable income is household income from all sources except capital gains, minus payroll taxes: So income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

The housing-debt-to-disposable-income ratio accounts for the growth in the population and income (more households and higher incomes per household) in relationship to the mortgage debt.

Disposable income rose faster than mortgage and HELOC balances in Q2:

- QoQ: disposable income +1.25%, mortgage & HELOCs +1.06%.

- YoY: disposable income +4.5%, mortgage & HELOCs +3.5%.

So the housing-debt-to-income ratio declined to 59.2% in Q2, the lowest ratio in the data going back to 2003, except for four quarters during the free-money-stimulus era that had inflated disposable income into absurdity.

From the chart below, it is obvious where the problem was in the run-up to the mortgage crisis that nearly blew up the financial system in 2008: households overindebted with housing debt, with the housing-debt-to-income ratio exceeding 90%. Now it’s below 60%.

Taxpayers and investors are mostly on the hook, not banks.

One of the most consequential changes coming out of the Financial Crisis was the transfer of mortgage risk to taxpayers. There won’t be another mortgage crisis, as far as banks is concerned. And taxpayers don’t care as long as their taxes don’t go up.

Commercial banks only held $2.65 trillion, or 19.9%, of the $13.35 trillion in total mortgage debt, HELOC debt, and second-lien mortgage debt outstanding, according to Federal Reserve data on bank balance sheets.

Government entities held, guaranteed, and securitized $9.2 trillion in single-family residential mortgages at the end of Q2, according to Ginnie Mae data. The resulting MBS, which have essentially zero credit risk because taxpayers took that on for a fee, were sold to investors such as bond funds, pension funds, the Federal Reserve, banks, etc. If borrowers default, the taxpayer has to eat the loss.

The share of government-guaranteed mortgages by total unpaid principal outstanding:

- Fannie Mae: 38.8%

- Freddie Mac: 33.2%

- Ginnie Mae: 28.0%

The remaining $1.5 trillion in mortgages that banks didn’t keep on their books and that the government didn’t guarantee, such as jumbo mortgages, have been packaged into “private label” MBS and sold to institutional investors around the globe, such as pension funds and bond funds, and it’s these investors that carry the credit risk for those mortgages, and not banks.

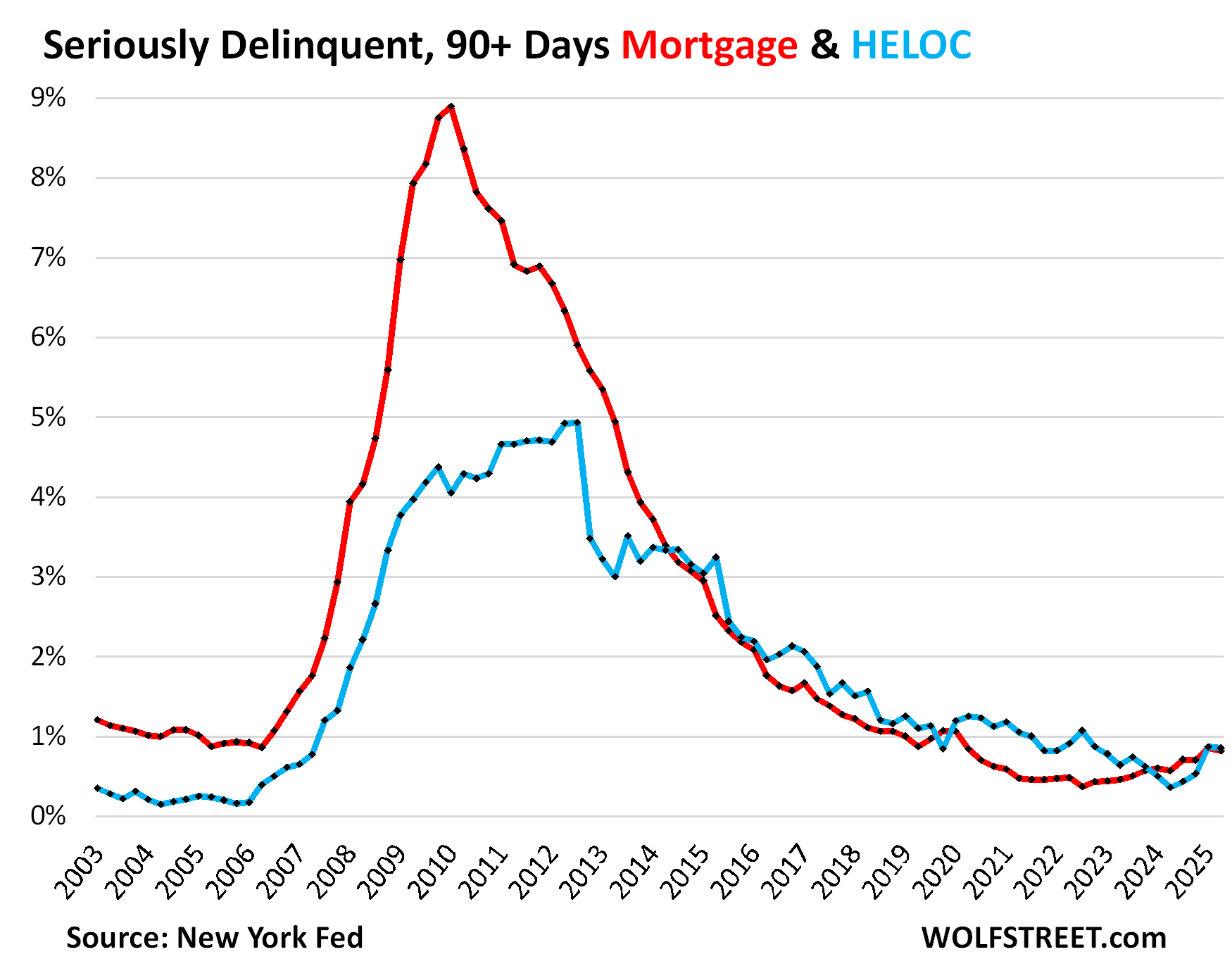

So far, so good: delinquencies and foreclosures dipped and are low.

Serious delinquencies ticked down in Q2 and are low for both, mortgages and HELOCs.

Mortgage balances that were 90 days or more delinquent dipped to 0.82% of mortgage balances outstanding, which is below the historic lows before the Free-Money era (red in the chart below).

HELOC balances that were 90 days or more delinquent dipped to 0.85% in Q2, below the prepandemic range and a little higher than in the pre-2006 years (blue).

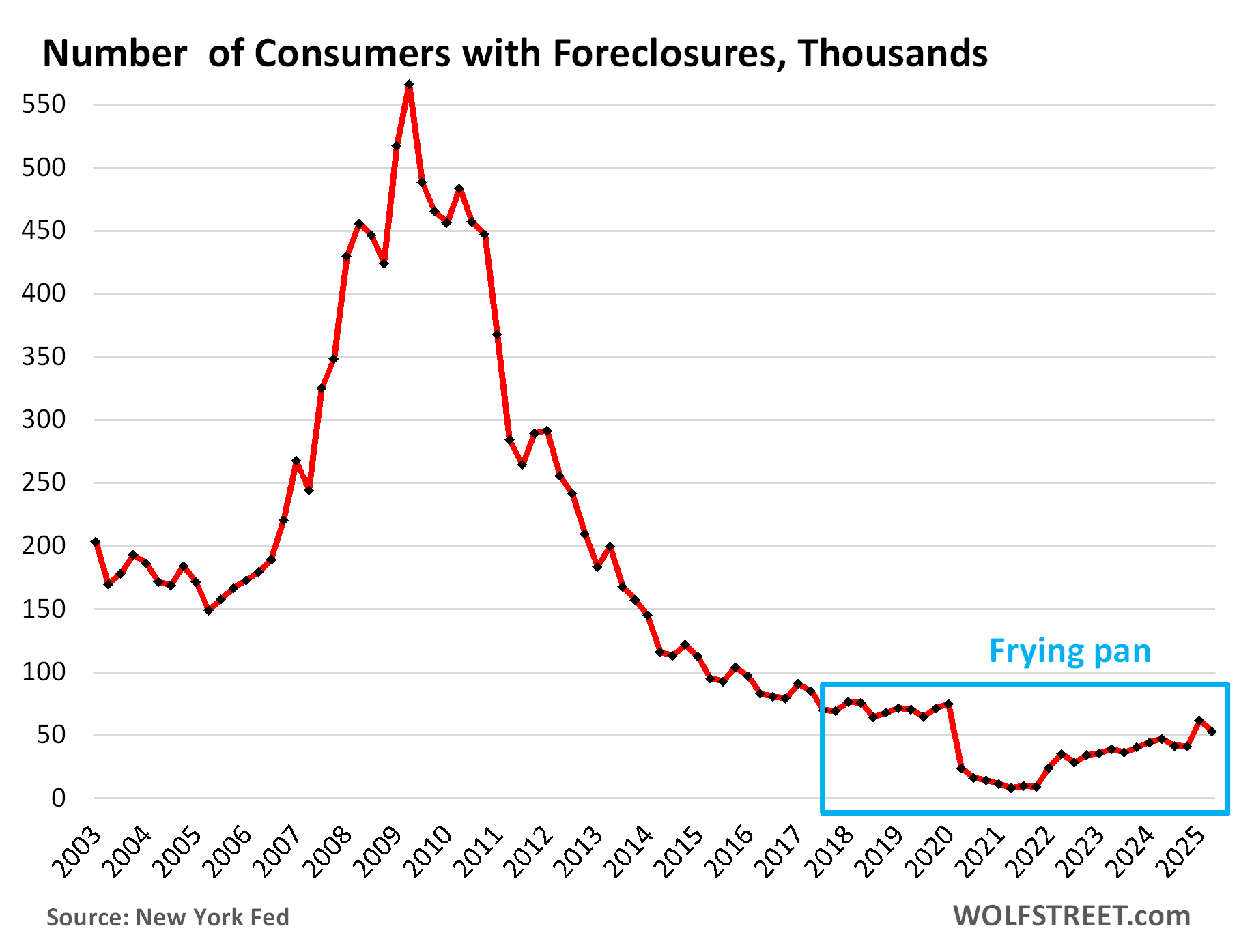

Foreclosures declined and are low. The number of consumers with foreclosures in Q2 dipped to 52,800, and remained below the range of the Good Times in 2018-2019 of 65,000 to 90,000.

The mortgage forbearance programs and foreclosure bans during the pandemic, and other government programs for government mortgages, made foreclosures essentially impossible, and the number of foreclosures fell to near zero.

Most of these programs have ended, and foreclosures have risen from the near-zero levels of the Free-Money era, which is forming the “frying-pan pattern,” that has been cropping up in a lot of data.

What is keeping foreclosures still low currently is that home prices exploded during the Free-Money era – see: The Most Splendid Housing Bubbles in America, June 2025: The Price Drops & Gains in 33 Large Expensive Metros. As a result, most struggling homeowners can sell their home for more than they owe on it, pay off the mortgage, and exit with some cash.

But in markets where home prices have already dropped significantly, this option is slipping away from the relatively small number of buyers who’d bought near the peak.

And in case you missed it yesterday: Household Debts, Debt-to-Income Ratio, Serious Delinquencies, Collections, Foreclosures, Bankruptcies: Our Drunken Sailors’ Debts in Q2 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’d be interesting to see age groups that take out HELOCS. I’d be suprised if 20 or 30 year olds are taking these out.

“HELOCs come with a second lien on the home, and if homeowners default on the HELOC while keeping the first-lien mortgage current, they can still end up in foreclosure.”

Doubling down on disaster….Why ?

I’m guessing credit card debt which has far greater interest rates. I suppose it could also be more home expenses like a new roof and so on. I’m sure people don’t for the wrong reasons too.

Yeah, even with a very high salary if your lifestyle creep has you with 50k in credit card debt. It’s very hard to make the minimum payment + the added interest + a payment to principle.

Some generations go thru a lot of job losses and looking for a new job. During this time one may have to bridge the gap with credit cards. Then the cycle repeats and you are just looking to hang on.

A HELOC can break that cycle for good. But you have to change your lifestyle finally and be frugal.

Anecdotally, not wanting to touch the base mortgage that was refinanced to sub 3.5%, with greater flexibility than a second mortgage.

Because HELOCs are interest only initially and have a lower interest rate than HELs. These loans are being pushed onto consumers left and right and what consumers don’t understand is they’re just putting off their problems for another day as HELOCs have variable rates in an unstable market and will amortize eventually, essentially doubling their payment, now at a rate close to the credit cards they used it to pay off. The other issue consumers don’t understand is that they’ll be paying interest on this debt far longer by using a HELOC. The HEL has a higher payment and interest rate but, it consolidates debt and removes compounding interest, making it a better choice as long as the monthly spend is lower and you’re able to apply more to principal, paying off your debts faster than you would have in the current situation.

I work as a refinance banker and see so much credit card debt but, clients are scared of the mortgage industry and the reputation we have so, they don’t often educate themselves on the different products and only chase the lowest interest rates, often making a new financial hurdle to overcome down the road.

I refinance my main mortgage to a heloc so i could build a house in South America. The heloc gave me the ability to “pay cash” for the South America house. What is do now is send all of my income into the heloc every month and use the heloc to pay my bills.

I have bought down the balance from 600k to 400k in only 3 years by doing this.

Now I moved to Colombia, still working my job remotely, rented the house in the US and I am able to send about 20k per month into the heloc.

If used property Helocs are a wealth builder.

Do mortgage balances also rise by accruing interest? I’d assume so if principal paydowns reduce balances.

If that’s the case, how much of the increase in mortgage balances comes from interest accrual on existing mortgages vs new mortgage origination?

That would be a negative amortization mortgage. Is that still a thing after 2008?

Interest that is paid monthly with the mortgage payments doesn’t accrue after it’s paid. The only interest that accrues is interest that is due but not paid. This is the case with forbearance when the borrower made a deal with the bank and the unpaid portion of the interest is tacked on to the mortgage balances, and it is the case with delinquent mortgages where the borrower has stopped making payments. But as you can see, the amounts of interest added would be minuscule.

Ahh now I understand – thanks Wolf and blahblahbloo.

Lower the ridiculously over proceed houses and I’ll buy

That HELOC increase is interesting, the trajectory now when we’re still in decent employment numbers likely will steepen if there’s any shock to the economy. Will it steepen as much as 2008 and beyond? That’s the $64k question…

Btw, Wolf, looks like you have build quite a bit of a fanbase over at /Rebubble with all these housing related articles, I find below posts responding to your housing inventory in Denver article especially interesting and you might get a kick out of it…

”

acqua_di_hoomertears

•

2d ago

Luxury Vinyl Flooring Enthusiast

whenever i read something from Wolf Richter i picture a jacked, 60-something sitting in his den with all the blinds closed, surrounded by WWII books, a TV in the distance with CNBC on 24/7, with a huge fucking glass of iced tea, he’s got a printed-out manuscript sitting next to him a screenplay that he’s written about how the world financial systems collapse, there’s a bunch of Desert Storm memoribilia on the walls although he never served, etc

acqua_di_hoomertears

•

2d ago

Luxury Vinyl Flooring Enthusiast

i picture there’s a ‘gun room’ in the house. just like a room chock full of guns for some reason. he drives a Toyota Avalon from the 2000s that’s in showroom quality. he seems a little on the spectrum to me, so you know his house has at least one wild card like a bookshelf devoted to Stargate SG1 shit. kitchen is straight out of the 70s with needlepoint art framed on the walls, bathrooms have toilets that are pink with wood toilet seats and high-pile carpet lid covers. etc”

lol.

My mind’s eye picture of Wolf’s room is a wall of bookcases filled with books and Japanese prints on the wall, with a big fat old fashion microphone for podcast interviews on his desk, and a view of San Francisco Bay out his window.

Maybe Wolf will post a picture and disabuse us of our phantasies.

They break my💔🤣

What I see when I sit in my chair right now. The red circle is around your comment. Note the closed shades (it’s sunny outside), the Japanese, German, and French books, along with a bunch of books in English, translated from other languages. The big old-fashioned mic is off to the side, not visible. Also not visible is my double-barrel 10-gauge goose gun with which I shoot down high-flying comments.

What you see when you stand on the other side. Books are all in English. I don’t think any are translations. The empty chair shows my AI replacement taking over my life, but you cannot see it.

haha…thanks for the effort in giving us a glimpse in Wolf’s den and also goes to show plenty of nutty commeters on Reddit with some wild imagination, especially when it comes to someone pointing out facts they don’t want to accept…

Still awaiting the shag seat cover pic on the pink toilet.

I hear those 10 gauger’s pack quite a punch.

This beats the Swamp’s office area which consists of a computer on a table next to my un-made bed with some dirty socks laying on it for good measure. A total embarrasment for video zoom meetings.

Wolf – You are my life goal. I am envious of those bookcases. Just a friendly reminder that AI will not replace the human touch. You are one the best.

Are you sure Wolf, that you don’t really live in an underground bunker in the middle of say, Iowa, or Oklahoma, off-grid, just waiting for doomsday – the future point in time when homes can’t be GIVEN AWAY? When the SHTF? Maybe the shade is just a decoy. Doesn’t look like the city by the bay.

Is your bunker tsunami resistant? 🤣

Wolf has the blinds closed so we can’t see the red-light district outside with all the junkies and homeless. Home, sweet home – San Francisco.

Bahahaha these posts are epic

LVF enthusist sounds like a mid level reject fbi profiler who got Doge’d when his fetish for vinyl, albeit floooring, got exposed.

Howdy Youngins. Some of US older folk built wealth using HELOCs. Just have to know what you are doing and can add and subtract properly.

Foreclosures are good for business. We appraisers are salivating over the prospect of more foreclosures. Fees are higher and the work you have to do is less. No home inspection, repairs, realtors. It’s a non-stop gravy train. Bring it on!

Geez,

More like we need to keep people in their homes and teach them proper techniques to manage their money.

Ebeneezer over here sending people to the debtor prisons… lol /s

The “taxpayer on the hook” cuts out the middleman banks this time; everything is all set for the American workers to “hold the bag.”

“Privatize the profits, socialize the losses”, implemented. Nearly total risk transmission onto another party. It’s brilliant, in its way.

A famous economist said, “Economics is not a morality play.” While there is a lot of unfairness in the economy, enhancing and encouraging it doesn’t strike me as good social policy.

the data in general may look good but it will likely all change fast.

I’m trying to find a better job and despite a PhD and many years experience and licenses in STEM it isn’t happening.

HOA past due notices are exploding at my HOA and tenants seem to be paying behind schedule. Though I know some that are still saying the rent is being paid. I think the best part of this cycle is over

Long-end rates being fueled by uncertainty, which implies mortgage rates remaining sticky at higher levels — especially HELOCs, that have been sensitive to elevated Prime Rate.

“The fact that primary dealers had to absorb such a large portion of the recent auction suggests a potential disconnect between the offered yield and investor appetite for the specific duration and risk profile of the 10-year notes at that time”

Like I’ve been posting. The debt to income shows there will be no repeat of 2007-2012, you’re welcome. The breaking point of not making your mortgage payment is simply not there. There will be “deals” in real estate, but they will be few and far between until a few years from now when, like in the ‘90s, after zero ish nominal appreciation, people wake up and realize that houses are 30+% cheaper on an inflation-adjusted basis than they were in 2022.

You funny! You very funny. This time make 2007-2012 look like walk in park. You comedian!

The charts make me think this will be long slow grind down barring any major black swan. Consumers still look to be in good shape for the most part.

What if the black swan already happened and you didn’t recognize it? Just a thought

everyone missed the black swan, and it floated by and disappeared into the distance and nothing happened 🤣

If you say so Wolf. Time will tell

That’s what you said. There was a black swan that went by and we didn’t see it…

I’m of the opinion you refuse to see it, but just my opinion so like i said, time will tell!

I don’t think anyone would miss it unless they lived in an uninhabited corner of the world.

Idont – there’s a Master Berra-ism in there, somewhere (…or mebbe the late, great Firesign Theatre’s: ‘How can you be two places at once, when you’re not anywhere at all?”…)!

may we all find a better day.

DEFINITELY IS a Yogi-ism in there dustoff……but I certainly lack his clarity of mind to yank it out…….

Still EXCELLENT recon, and useable enough report….a heads up…even with unknown unknowns…..forgot what I was doing whenever Firesign was on, though…..few memories of it…. Take care.

Later.

Americans with mortgages receiving severance/UI Benefits will find it difficult to land comparable positions in this tight job market.

Always make payments on the car before your house, unless of course you commute in an RV.

Remember when UI paid 50k a year in 2020? And you didn’t have to pay your housing note, didn’t have to pay rent, and didn’t have to pay school loans for five years?

When I see charts with nominal data, I try to imagine what they look like on a real basis. For example, the nominal 20% increase in total mortgage balances in the 2021-2023 timeframe is actually almost 0% in real terms.

You’re not going to adjust home-price inflation to consumer price inflation which is dominated by services, are you? People do it, but it’s intellectual goofballism. Might as well adjust home price inflation to grade inflation or whatever.

If anything, to check changes in “affordability,” you can adjust home price inflation to wage inflation. If wage inflation outruns home price inflation, homes become more affordable. You have to do that by local market, not nationally. You can figure other expenses into it, such as local property taxes, local homeowners’ insurance rates, and mortgage rates. The Atlanta Fed has an affordability tracker like that. It only tells you something about “affordability,” though.

And houses are rapidly becoming more affordable on a wage basis.

Higher for longer HELOCs

recent weak Treasury auctions highlight a growing concern about the ability of the US government to easily finance its increasing debt. This situation is further complicated by shifting investor dynamics, including the declining participation of foreign buyers, and the need for higher yields to attract sufficient demand

Hi Wolf,

I see you mentioned the frying pan pattern in a few articles. Can you explain what it correlates to? Is it predictive of something?

The pattern it shows: normal, plunge, return to normal.