The long-defaulted federal student loans come out of the shadows of government forbearance.

By Wolf Richter for WOLF STREET.

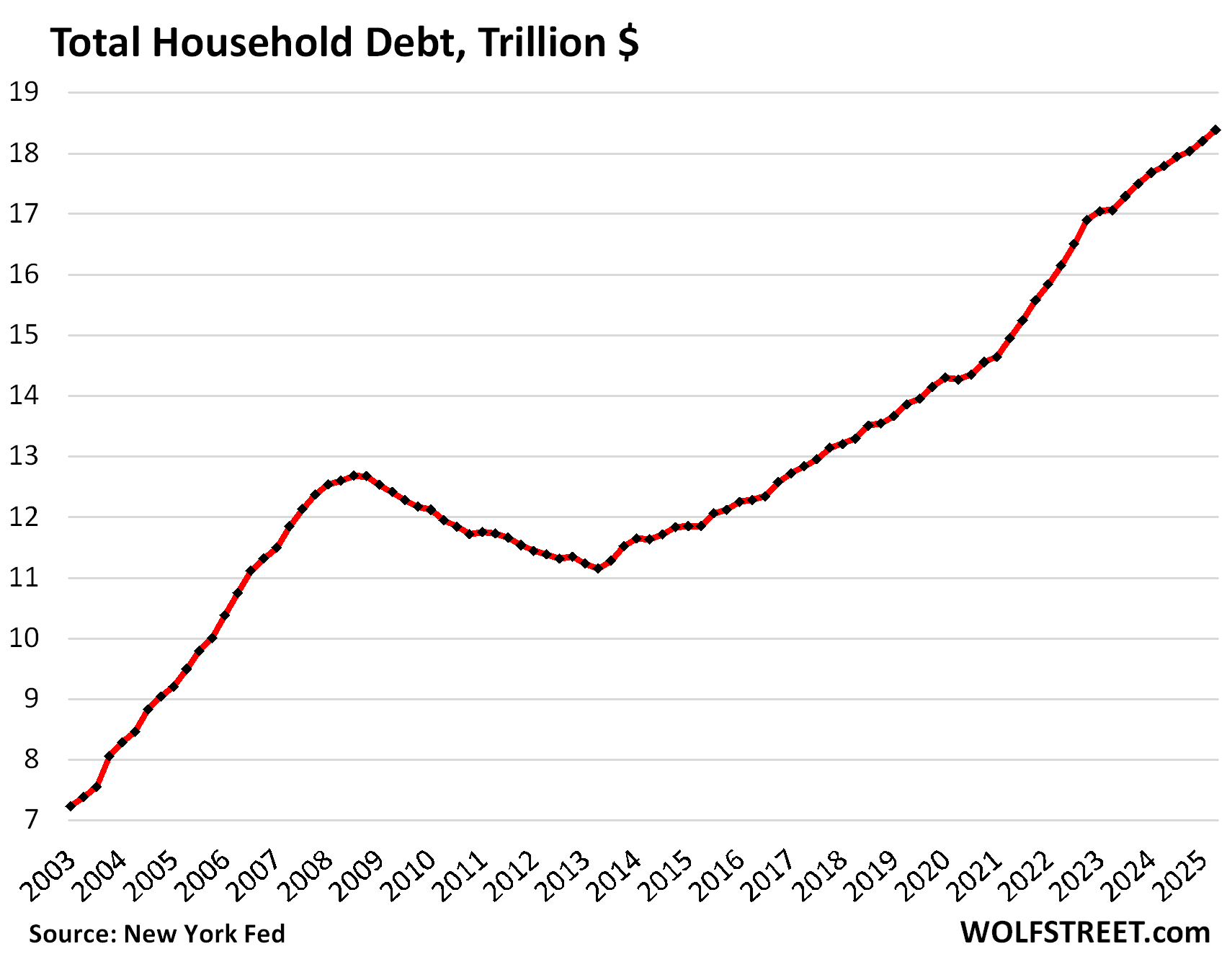

Total household debt outstanding rose by $185 billion in Q2 from Q1, or by 1.0%, to $18.4 trillion, according to the Household Debt and Credit Report from the New York Fed today.

Year-over-year, total household debt grew by $592 billion, or by 3.3%, the third-smallest growth rate since Q1 2021, behind only Q1 2025 (+2.9%) and Q4 2024 (+3.0%).

And this debt was carried by more workers earning records amount of money, and the overall burden of their debts in terms of their disposable income (the debt-to-income ratio) declined even further; more in a moment.

Balances increased quarter over quarter in the categories of auto loans, credit cards, student loans, mortgages, and HELOCs, but dipped for the second consecutive quarter in “other” revolving credit (personal loans, BNPL loans, etc.). We’ll get into the details of housing debt, auto loans, and credit cards each in a separate article over the next few days. Today, we’ll look at the overall debt, its burden, delinquencies, collections, foreclosures, and bankruptcies.

In terms of delinquencies, the standout is that student loans became loans again this year, and those loans that have been delinquent since 2020, but covered by the government’s forbearance programs, started counting as delinquent again this year, and the results are sort of funny. The move this year is so massive that it jacked up overall delinquency rates.

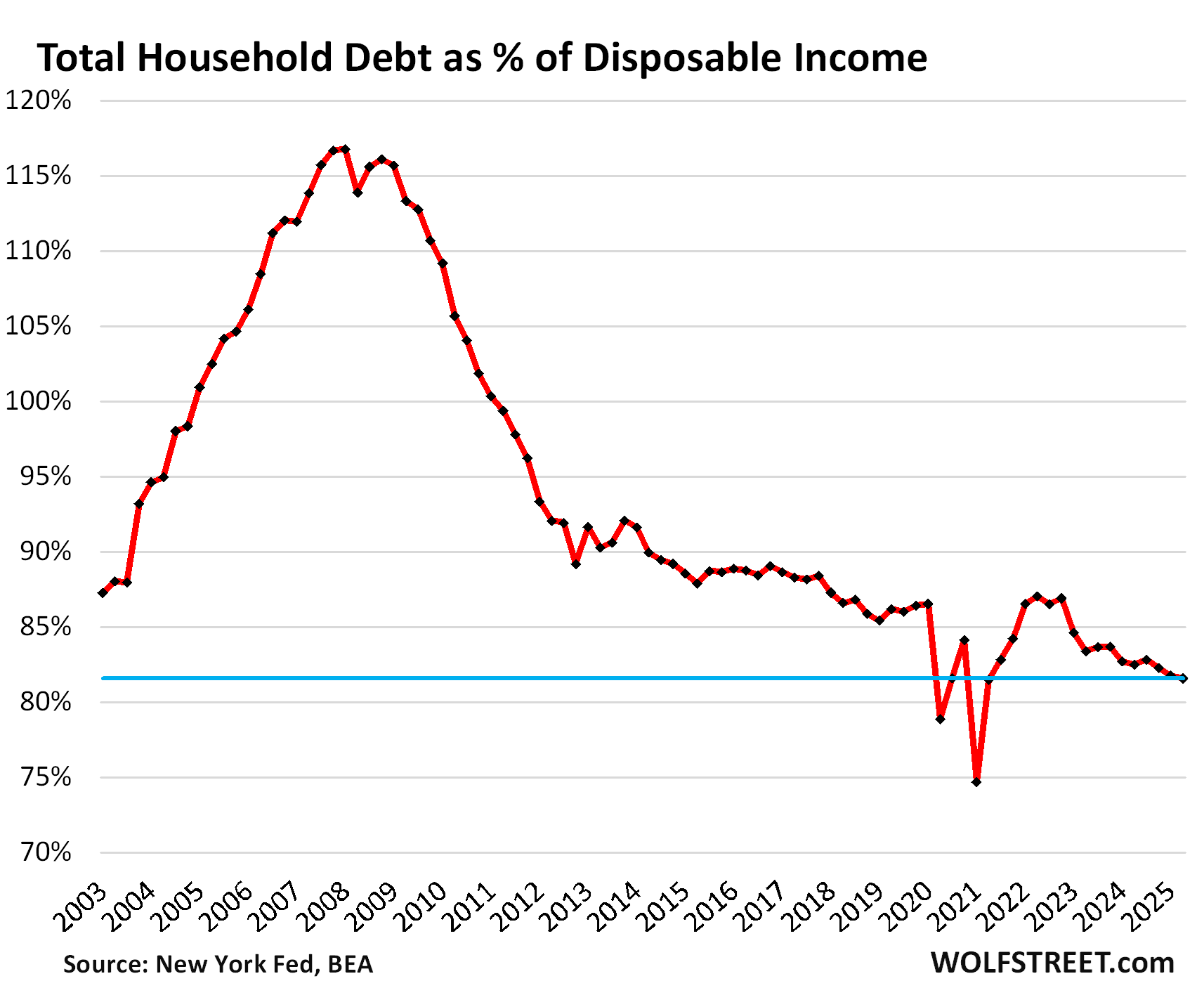

The burden of household debt: Debt-to-income ratio.

A common way of evaluating the burden of a debt is to look at the debt-to-income ratio. With household debt, we look at the ratio to disposable income, which accounts for more workers and higher incomes.

Disposable income, released by the Bureau of Economic Analysis, is household income from all sources except capital gains, minus payroll taxes: So income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc. Disposable income is essentially what consumers have available to spend and service their debts.

Disposable income rose faster than debt in Q2:

- QoQ: disposable income +1.2%, total debts +1.0%.

- YoY: disposable income +4.5%, total debts +3.3%.

The debt-to-income ratio thereby declined to 81.6% in Q2, the lowest ratio in the data going back to 2003, except for two quarters during the free-money-stimulus era (Q1 2021 and Q2 2020) that had inflated disposable income into absurdity.

So seen as a monolithic entity, the American Consumer is in good shape, the balance sheet is in good shape, 65% own their own homes, over 60% hold equities, they have $4.6 trillion in money market funds that still pay around 4% in interest, they have $1.1 trillion in small CDs, and $2.4 trillion in CDs of over $100,000 that all generate income. That’s a pile of cash they’re sitting on.

It seems our Drunken Sailors, as we lovingly and facetiously call consumers, learned a lesson and became a sober bunch, most of them. But not all of them.

Subprime-rated borrowers – a small subset of consumers – are always in trouble with high debt-to-income ratios and missed payments in their credit history, which is why this segment is called “subprime.” But it’s not a fixed part of the population; people fall into subprime credit scores and climb out of them all the time, it’s a constant flow. And subprime doesn’t mean “poor” or “low income,” it means bad credit; the young dentist that goes in over his head is a classic example. Low-income people rarely can borrow enough, if at all; it’s the higher income people that can borrow a lot that can get into deep trouble.

The heavily indebted economic entity to worry about is not the consumer but the federal government with its ballooning mountain of debt and reckless deficits. The other entities to worry about are overleveraged businesses, often funded by private equity and/or private credit.

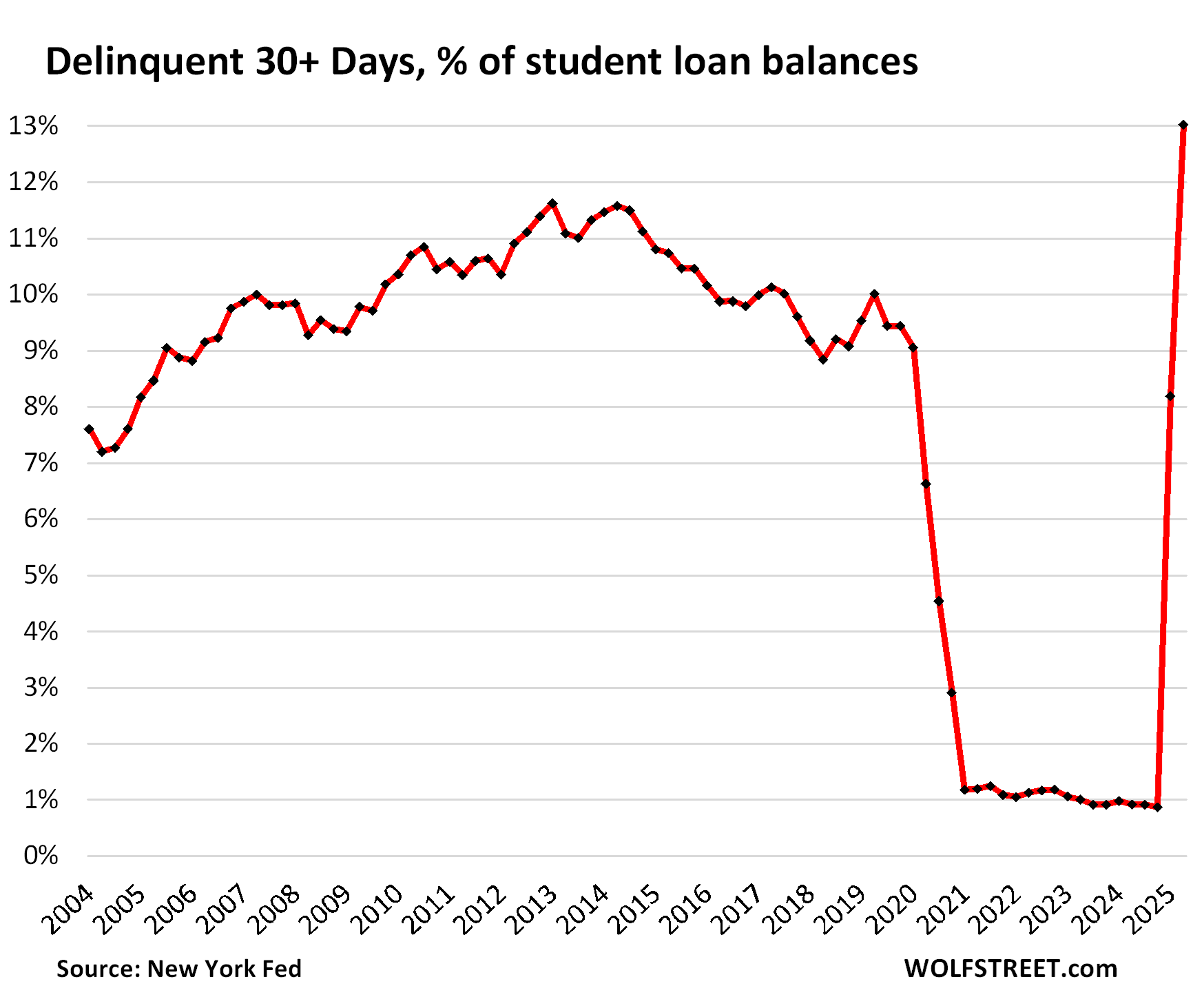

Delinquent student loans face reality again.

In 2025, federal student loans that had been covered by blanket forbearance since 2020 while waiting for forgiveness, face the reality again that a loan is a debt that needs to be serviced, and if it isn’t serviced as agreed, it becomes delinquent. And these delinquent federal student loans, after having been absent from credit reports since 2020, are back in them, and with a vengeance.

The 30-day delinquency rate spiked to 13.0% in Q2, the worst ever, up from 8.2% in Q1 and from 0.9% in Q4, according to the NY Fed’s report today, based on Equifax data.

Roughly $213 billion (13.0%) of the $1.64 trillion in student loans outstanding were 30-plus days delinquent in Q2.

The spike was driven entirely by moving these delinquent loans out of the shadows back into reality and into credit reports.

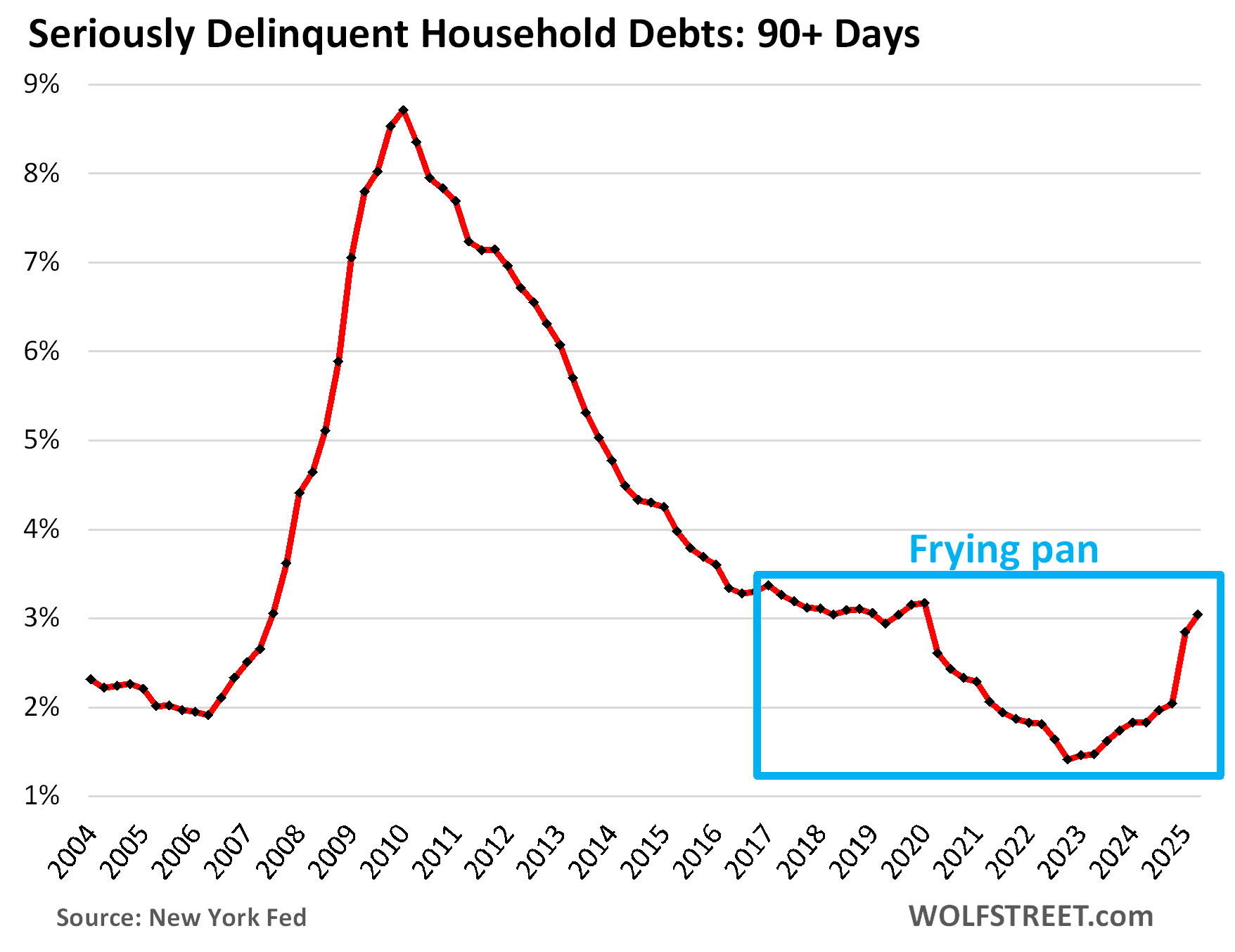

The 90-plus day delinquency rate for student loans spiked to 10.2%

There is suddenly an old reality out there: Delinquent loans mess up credit scores, limit the ability to borrow, and increase the interest rate borrowers have to pay when they do borrow. That should have been taught in college.

Student loans whack the overall delinquency rate. That $213 billion in delinquent student loans in Q2 caused the overall delinquency rate of 30-plus days in Q2 to shoot to 5.3%.

In Q4 2024, before these delinquent student loans were counted, the overall delinquency rate was 4.1%, well below any period before the pandemic.

The 90-plus day delinquency rate – the rate of “serious” delinquencies – rose to 3.0%, pushed up by the 90-day student loan delinquency rate of 10.2%.

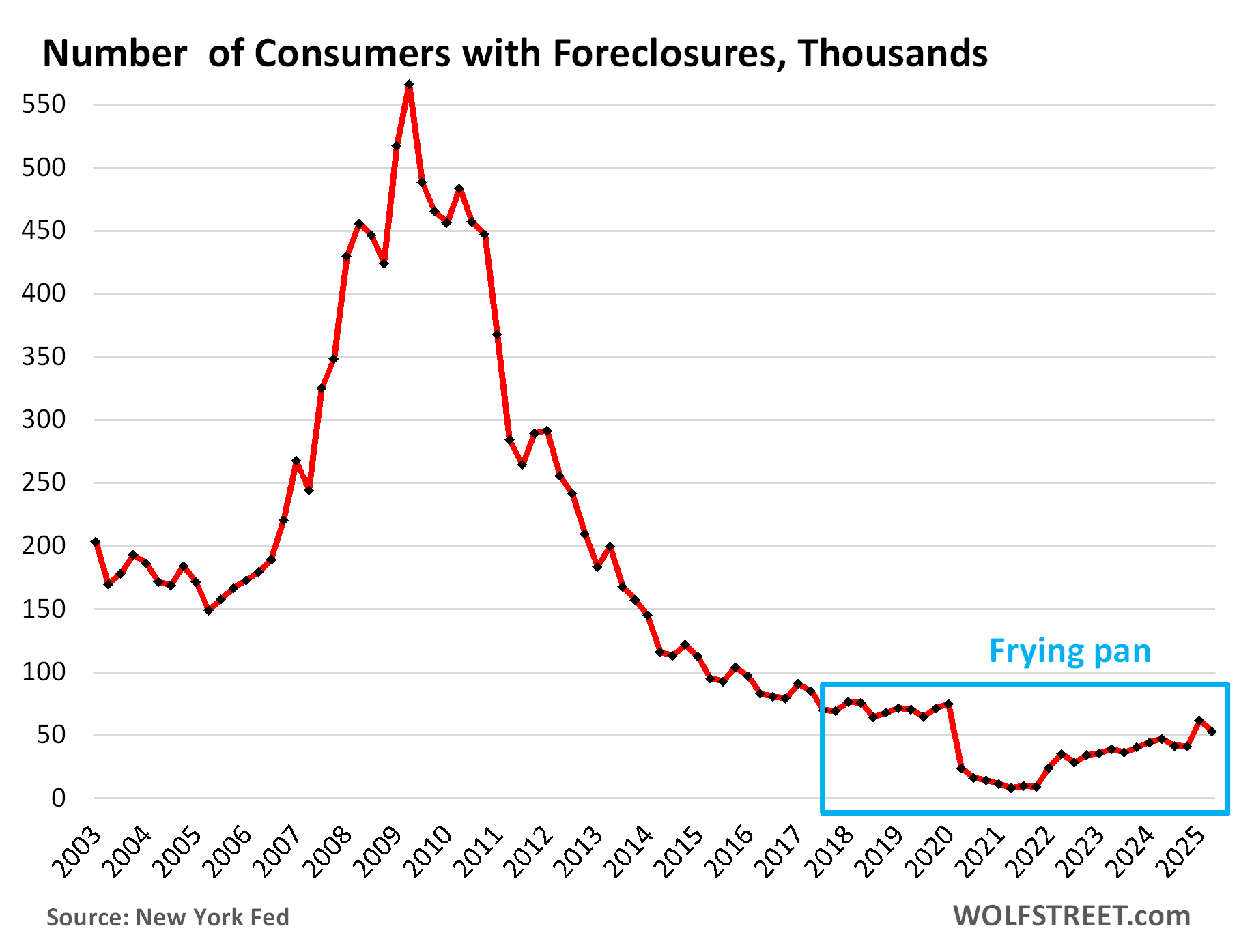

The infamous “frying pan pattern” – a WOLF STREET technical term – has formed, where the panhandle represents the prepandemic level, the pan represents the free-money level, and the other edge of the pan represents the post-free-money return to prepandemic levels:

Foreclosures declined and are low. The number of consumers with foreclosures in Q2 dipped to 52,800, and remained below the range of the Good Times in 2018-2019 between 65,000 and 90,000.

During the Free-Money and mortgage-forbearance era, during which foreclosures were essentially impossible, the number of foreclosures fell to near zero.

What is keeping foreclosures low is that home prices exploded during the Free-Money era, so most struggling homeowners can sell their home for more than they owe on it, pay off the mortgage with the proceeds from the sale, and walk away with some cash, and their credit intact.

But in markets where home prices have dropped more significantly, this option is starting to slip away from buyers who’d bought near the peak.

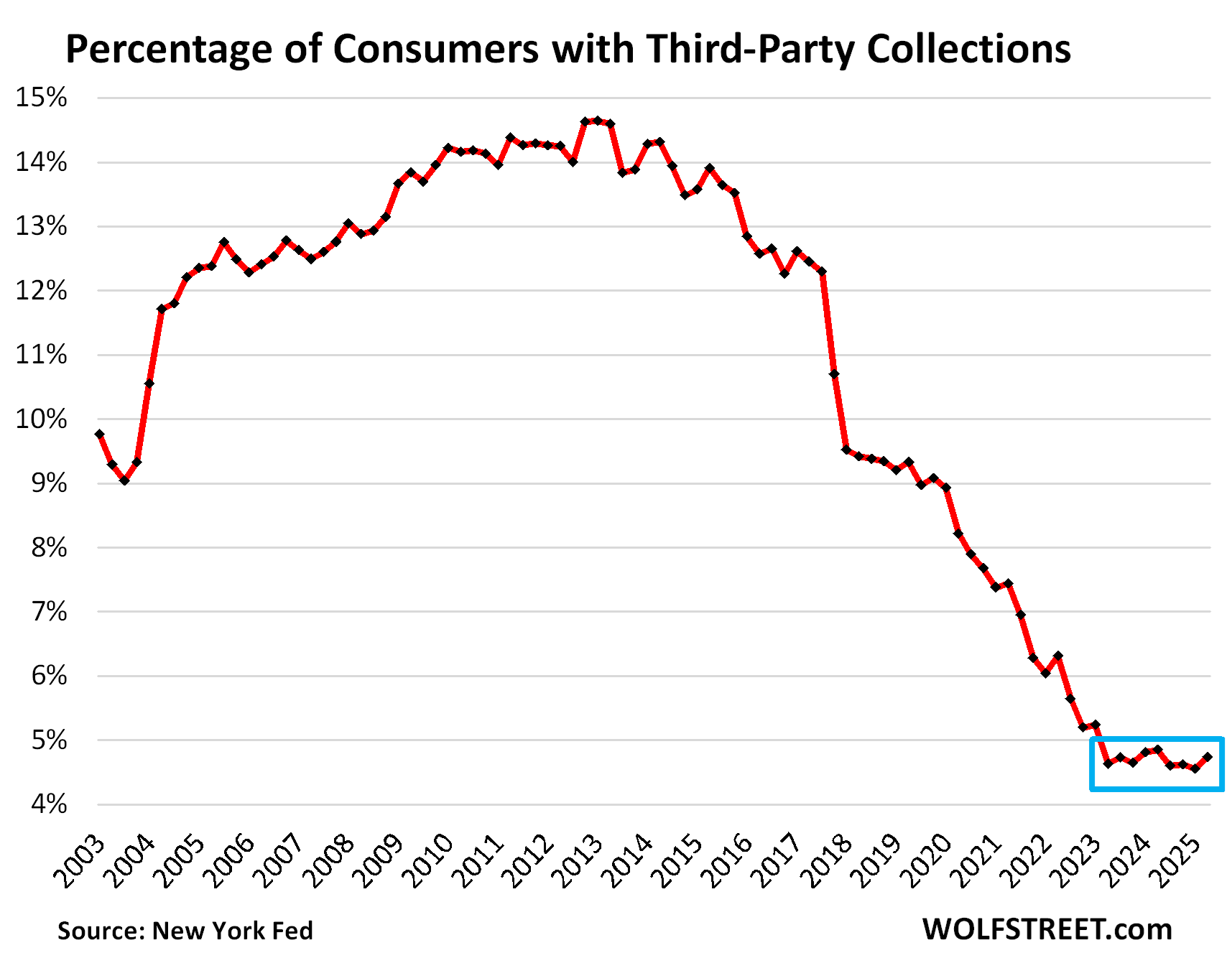

Third-party collections at rock bottom. A third-party collection entry is made into a consumer’s credit history when the lender reports to the credit bureaus, such as Equifax, that it sold the delinquent loan, such as credit card debt, to a collection agency for cents on the dollar. The New York Fed obtained this data on third-party collections in anonymized form through its partnership with Equifax.

The percentage of consumers with third-party collections skidded from record low to record low during the Free Money era and has hobbled along near those record lows even after the free money vanished, and in Q2 was 4.7%.

But, but, but… there is some discussion to turn defaulted federal student loans over to collection agencies – and if that ever happens, it will cause the percentage of consumers with collection entries in their credit records to spike.

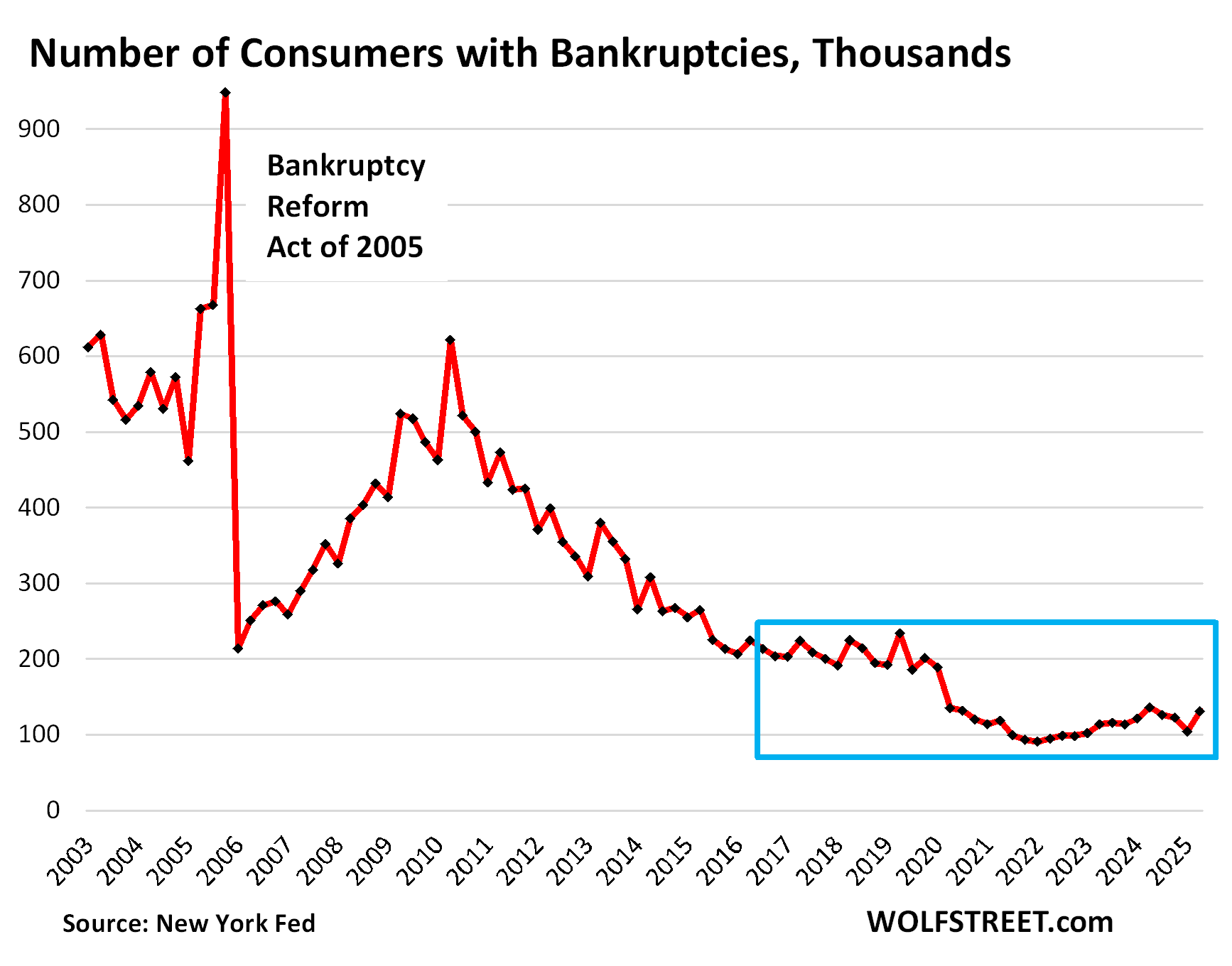

Bankruptcies remain low. The number of consumers with bankruptcy filings rose from a near-record low to 131,320 in Q2.

During the Good Times before the pandemic, the number of consumers with bankruptcy filings ranged from 186,000 to 234,000, which had also been historically low.

We’re going to wade into housing debt, credit card debt, and auto debt in separate articles over the next few days. Next one up is housing debt.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Looks like there is absolutely no reason for the Fed to cut.

But they WILL cut.

Next meeting. Apparently 90% chance atm.

The jobs side called in sick

(Also we’ll see how well this ages 🥛)

The curve is going to get steep at this rate. Jobs vs inflation is going to be an unwinnable battle.

How accurate have prediction markets been at predicting the Fed’s actions over the past few years?

Bubble economy is rocking! Wait till stock, crypto, and real estate reality hit.

Ahh peep show.

What a good one

📺

How could you forget the ham? On Christmas Jeremy!

The fact that it is celebrated when the debt to income ratio is ‘only’ 81.6%, is certainly not reason for joy.

It is utterly absurd to have that high of debt ratio, even if measured against net after tax income. That leaves only 18.4% left over to pay recurring bills, rents and food.

Secondly, as to some homeowner supposedly being able to sell their house for more than they owe on it, is patently ridiculous right now. Irrespective if they bought at the peak or not.

The housing inventory sale to closed transaction ratios are dismal. It’s in the data clearly, and as inventory for sale rises yet further with layoffs, we will see those delinquency and default rates rising as well.

Assuming the banks actually report the data on loans honestly in a mark to market environment.

1. You misunderstood in your first paragraph. The ratio here is “debt” to income, so the “total amount you owe” to income. It is NOT “debt service” (monthly principal and interest payments) to income.

2. “Assuming the banks actually report the data on loans honestly in a mark to market environment.”

Most of those mortgages are government guaranteed and held by investors via agency MBS; most of the remaining mortgages that are not government guaranteed are also held by investors via private label MBS. Banks only hold a small portion of the mortgages. That’s one of the hugest changes out of the financial crisis.

It is total debt as a percentage of household income. Mr. Wolf clarified it nicely.

Zero debt is the new American dream.

Thank You for the post W.R.

It looks like the big Dipper actually. If you don’t pay the annual property taxes, you don’t own your home…perpuality is a given like paying for a bridge or road toll, forever after the asset has been paid off numerous times…60 percent of households own stocks… didn’t know this, thought it was much smaller.

Taxes pay for the system that creates and maintains property rights. No taxes, no property rights, no ownership.

*angry libertarian noises

Water, sewer. streets, cops, schools, libraries, fire…etc.

A more chilling stat is that the top 10% of households on 93% of the stocks held by households. It is extremely lopsided.

Had an argument with a coworker that ‘so what if amazon barely pays taxes (despite benefitting from the taxes we all pay) the stock has gone up a ton!”

That’s why they’re the top 10% and why they became the top 10%, LOL. If the bottom 10% owned 93% of the stocks, they wouldn’t be the bottom 10%, they’d be the top 10%!

The distribution of stock ownership is important. The top 10% of households by wealth own around 93% of stocks. The remaining households own around 7%.

I’m not sure I understand your point about “perpuality is a given like paying for a bridge or road toll, forever after the asset has been paid off numerous times.” A bridge or toll road needs to be paid for in perpetuity because those assets need to be maintained in perpetuity or will decay beyond the point of usefulness. Paying for most assets is only the first step in an ongoing process of keeping those assets functional. Likewise, property taxes pay for schools, roads, police, and other services whose costs run in perpetuity, or at least until the community becomes a ghost town.

Nothing goes to heck in a straight line except that 2-month jump from 1% to 13% for delinquent 30+ days of student loan balances. What the actual F?!

Anecdotally, I have a close friend who I suspect is delinquent on his 50k+ student loan debt, or may be soon based on hearing he’s now living paycheck to paycheck with a 100k+ salary. Brother never wants to talk about finances or ask for input/advice. Hedonic adjustment through and through. Ugh.

So the taxpayer is on the hook for the $200B+ delinquent student loan balances right? More ugh.

Makes me wonder how consumer spending for 24-40 year olds are going to shift, if at all, in the short and medium term based on return to paying student loan balances and the delinquencies.

A lot to unpack. Interest payments on student loans was supposed to pay for ACA. Before the pandemic, there was a lot of mismanagement of money. Today it’s worse due to a long pause of student loans. BNPL will show up on credit reports soon. Terrible policy created today’s financial distress. Repayment rate of student loans low before pandemic and now worse than before. I was one of the 450k people that made payments of a 40 million populous of loans. Wish there was something good to say about this, but people need to be more responsible.

I agree, but there’s been a whole generation of kids that were raised with the idea that all you have to do is go to college and everything else will take care of itself.

Still on board with the personal responsibility thing, but feel kind of bad for the people that were making major long-term decisions at only 17 and 18 years old based on lousy advice.

Going to college can work out very well if you pick the right subject. Plenty of bad advice was flying around about that by the looks of it.

I was fortunate that my advice of ‘better get a second degree you can get a job in to supplement the one you love that the college encouraged you to get’ worked out well. Got a bit more debt to income ratio than was necessary for the advisee but that’s life.

We call that bad parenting.

Every action must have a reaction. Colleges committed fraud and became an entire industry over employing and over paying. Just like healthcare. If you bailout student loans, the job market will still suck, but the colleges will get off scott free. Isn’t it odd that in the last 20 yeas, the only industries that have grown and grown and the costs have become unreachable for many is healthcare and higher education? If you polled how those people vote, how do you think it would look? They are literally that quote from some guy back in the 18 century about democracy only lasting as long as people realize they can vote themselves money.

The benefits of a college education are obvious. Trouble is many students and many parents are foolish.

My fourth child just graduated and will soon be working in NYC in the banking industry. Computer Science degree and 4 year varsity athlete. She had a plan, worked hard, and developed marketable skills.

I went to college to get into medical school.

You’ve got to set goals and then execute your plan to achieve them.

So personal responsibility, nobody is arguing with you Chris.

In fact, i’d say when you boil it down, every problem our society faces is do to a rejection of personal responsibility. Seriously think about it. Name a problem and i’ll tell you how its due to a rejection of personal responsibility. And this is why the left will lose in the long run. They reject nature, fine if they want to do that, just don’t make me pay for it.

What about a bailout for students, Americans who supported higher education only to get eliminated by AI with limited entry level jobs? It’s interesting that the money changers got bailed out, autos, etc…but not the little people…well, they got 5 years, that’s something…isn’t fraud a business model for the fortune 500? Pay fine, move on.

How about we make the colleges and universities that sold these BS degrees cover the cost rather than the taxpayer.

I almost spit out my coffee. I love the idea!

But but but we need to renovate the gym for a 3rd time and add granite to the freshman 1400 sqft dorms!

The only way to end the student loan “crisis” is to completely stop any and all taxpayer backed Federal student loans. Cold turkey. The existing $1.8T or whatever it is can be financed at 2% fixed and paid off – or be delinquent on credit reports like any other debt.

Without that plentiful taxpayer money that “might not have to be paid back if you vote right wink wink” colleges and universities will have to either dramatically lower tuition or maybe self-fund the loans and collect the payments themselves.

MOODY’S economist says USA ‘on precipice of recession’…

According to these recession mongers, the US has been on the precipice of a recession or already in a recession ever since the Fed raised its rates to 0.25-0.5% in March 2022. There are thousands of comments here to document this.

I feel your comment on student debts: ” Delinquent loans mess up credit scores, limit the ability to borrow, and increase the interest rate borrowers have to pay when they do borrow. ” doesn’t go far enough in describing the hole into which delinquent borrowers are sunk.

Those bad credit ratings make it difficult to rent, difficult to get a good job, and cost them higher rates on insurance, and may make it difficult to get a bank account. The inability to borrow money affordably makes even transportation needed for a job difficult.

Many, if not most, will ever dig themselves out of this hole. We are creating an entire lost generation of people.

If you get current on ALL your obligations and stay current, pretty soon your credit rating starts to improve. It doesn’t improve if you don’t get current.

Wolf wrote: “So seen as a monolithic entity, the American Consumer is in good shape, the balance sheet is in good shape, 65% own their own homes, over 60% hold equities, they have $4.6 trillion in money market funds that still pay around 4% in interest”.

I’m in the 60% that owns a home, with money in the stock market and tons of cash in money market funds that is doing pretty well, but I rent to people in the 35% that don’t own a home, have much in the market and most spend more than they make most months (even when they make over $120K/year) with mulriple 18-20% credit cards with big balances that make me cry. It seems like saying “a monolithic entity, the American Consumer is in good shape” is like saying “looking at San Francisco and Phoenix as one entity the weather is a mild 89 degrees” when it is a 64 in SF and 113 in Phoenix today.

Lots of renters are “renters of choice” that pay $4,000 in rent or $10,000 in rent and are doing fine. Nearly everything that was built for rent over the past 15 years has been higher end for renters of choice — because that’s where the money is, LOL. You’re renting to the lower end of the market, it seems. But kudos. That is an essential part of the rental market.”

” with mulriple 18-20% credit cards with big balances that make me cry.”

That is a relatively small number of people — including the classic young dentist I mentioned that got into it over his head. And the total amount the owe all combined is only about $500 billion. These people will pay off their credit cards and be fine and other people rotate into their spot, and then rotate out of it, that’s how it goes, part of the learning curve. I went through that too when I was young.

Wolf is correct that I rent mostly on the “lower end of the market” (for those in other parts of the country on that SF Peninsula that is apartments worth ~$500K/unit that rent for ~$4K/month). The one property I rent that I don’t own is my brother’s first home in Burlingame that is worth ~$3mm and rents for $9K/month and the people looking to rent that home “West of El Camino”over the years have had better looking credit reports than anyone looking to rent my apartments “East of El Camino”. I would be interested if Wolf has ever seen something that calculated that percentage of “renters by choice” that could actually “buy” a home or condo similar to the one they are renting (aka had liquid assets that would allow them to make a down payment big enought to qualify for a loan to cover the rest).

So people rent in the center at a higher-end tower with lots of amenities at for example $5,000 a month, instead of buying out in suburbia for $5,000 a month… that’s a big part of the “choice” that people make: They WANT to live in a central location or within walking distance of the BART or whatever, and nearly all multifamily construction over the past 15 years has catered to them.

Then there are the other renters of choice that the big single-family landlords now go after with their purpose-built SF rental developments. These are nice houses in the suburbs or further out that now rent for less than the monthly costs of buying an equivalent house in a similar area. There may be 300-500 rental houses in that kind of development, with common amenities, such as a leasing-maintenance office, a pool, etc. They choose to rent because it saves them money, and because they don’t have to hassle with ownership issues, and if they want to move a year or two later, as many younger families do to change jobs, they can do so without losing their shirt trying to sell the home they’d bought a year or two earlier.

This is all widely discussed in the earnings calls of those landlords. They tell you the median household income of their tenants, which are above the local medians. They tell you all kinds of interesting stuff, including rent increases on renewals v rent increases on lease signings. As landlord, you’d find their earnings calls and financial statements interesting. You can get the transcripts of those calls from Seeking Alpha. I have discussed a few of them over the years here, just like I discuss the homebuilders occasionally.

If someone had told me when I graduated with over $50K in student loans back in 1992 that’d I’d have 5 years of NO interest payments and could focus on paying down the principal I’d have been overjoyed! I hope some of the people with student loan debt took advantage of the “moratorium” to either pay down their debt or save enough that they can now pay down a large percentage of that debt.

Is it possible they just forgot they had loans?

No.

I think they figured that these loans would be forgiven, and it would be stupid to make payments. Someone actually told me that. Had the temerity to tell me that.

I’ve heard this as well – it was the rationale for not paying down principal during the moratorium.

I had the exact same conversation with two young dudes at the Denver airport back in 2023. Advised them to begin paying now, because the loans wouldn’t be forgiven, for the simple reason it gives the government leverage over them. Here we are, and i’m shocked, shocked i tell you, that gambling is going on at this establishment.

Many such cases, I knew a guy who bought a house back in 2021 because he could now “afford” the mortgage with the money he no longer was putting to his loans. I wonder how he’s doing these days.

(Meanwhile, I refinanced my student loans to private in 2019 and made full payments the entire pandemic. At least my interest rate is only about 3.2%.)

I had a number of friends that weren’t aware that the payments were restarting. All with different loans from different lenders, none claimed to have gotten a notice that payments were restarting. They all took some hefty hits to their credit scores.

Thanks Wolf. I’m curious where you got the BNPL numbers. I was under the impression that they were not that transparent. Keep up the good work!

Patience. That will be part of the credit card article.

Regarding student debt, sorry but when the previous admin suggested pardoning that debt I was major PO’d. Lot’s of parents put them through college, and lots of their kids (one being me) worked and went to school. That free ride thing was crazy, sorry to say it.

Government loans for student education should never have happened. The universities should have been the lenders to students. Many universities have rich endowments. The universities are the ones who ultimately profited from student loans, and we see this in the massive increases in professor and administrator salaries, benefits, and pensions.

The money went from taxpayers to the government to the students to the universities to the professors and administrators. I got through university by working and the occasional scholarship. Back then tuition costs were lower. Colleges actually provided an education. Loans were not generally needed and professor and administrator salaries were reasonable. Universities nowadays are cesspools of corruption and graft.

Colleges and universities are the ones who jacked tuition up through the roof over the past few decades. When I went to UCLA in the 1970s tuition was $250 per quarter for an annual in-state tuition of $750 per year for 3 quarters. Tuition – especially at public universities – needs to drop back down to these levels or become free.

Yes, who system is broken. I admire the countries that public education doesn’t stop at high school but fund valuable education that benefits society whether it be college or the trades. Fortunately at least where I am at junior colleges are almost free for 2 years. It is almost like the system was purposely setup to get people into debt early on. State universities weren’t all that expensive in the early 90s and with 2 years of JC you either had no debt or paid it off quickly.

100%

If you want to finance a new Honda, you talk to Honda Financial Services.

If you want to finance a Harvard degree, you should talk to Harvard Financial Services, not Uncle Sam.

Does own a home mean outright. mortgage free or just they are the owner?

About 40% of the homeowners have no debt on their house. The remaining 60% of the homeowners have some to a lot of debt on their home. But they’re all on the title and own the home.

“This should have been taught in college.”

Nice.

I’m just curious if this data includes people like my wife and I, who sold our house in 2022, moved multiple states away, and are renter’s of choice due to current simple math.

Yes, our income has technically increased every year, and we also carry ZERO debt; however, due to inflation and frankly, corporate greed, for the things we spend our money on, we’re pretty much a wash. The only corpo revenue garnished from us is purely inflationary/demand (if we chose to outlay).

We’re not actively increasing GDP with our spend — just maintaining the status quo. Not exactly a recipe for growth (especially at these inflated P/E ratios). Just makes me wonder how many are in the same boat, let alone those who are underwater?

The point is: not exactly a gangbusters growth scenario, regardless of debt servicing.

I feel the same way. I think I was better off in 2019, and I’ve switched jobs since then.

“There is suddenly an old reality out there: Delinquent loans mess up credit scores, limit the ability to borrow, and increase the interest rate borrowers have to pay when they do borrow. That should have been taught in college.”

Can we please add one more important (maybe THE most important) financial lesson to be taught to, what seems like everyone involved with college and college finance, from students to school faculty to administration to reporters and politicians clamoring for “affordable student loans”

Student loan interest is SIMPLE but College Costs COMPOUND and compounding always wins in the end.

If costs continue to increase at rates above a reasonable amount (inflation, income growth), at some point even a zero percent loan will be un-affordable.

Then what?

Wow. A whole lotta people here are bent out of shape over student debts. Wolf wrote: “Roughly $213 billion (13.0%) of the $1.64 trillion in student loans outstanding were 30-plus days delinquent in Q2.”

My Libertarian buddies are always telling me: “A debt that can’t be paid, won’t be paid.” If the debt can’t be paid, why carry on with all this extend and pretend ? Just write the debt off. Then either get the government out of the student loan business, or limit involvement to something small, like maybe $3,000 total.

Even that $1.6 Trillion number does not seem as big as it once was. Since the topic here started out talking about “spending like drunken sailors”, lets look at the Billionaire who spent $500 million for his yacht ( a half trillion $ right there).

A google search found: “using his vast wealth, primarily accumulated from his ownership stake in Amazon. He also likely utilized loans, potentially secured by his Amazon stock, to manage the purchase and ongoing costs, as borrowing can be more tax-efficient than liquidating stock.” Yeah baby, what could possibly go wrong here? ? (sarcastic rhetorical question). And Bezos is just one debtor.

Full disclosure here. My first semester of college back in the 1960’s was $159 (for 18 credits). A big number for the time, but manageable. Unfortunately, I had an expensive girl friend in college, and graduated with $350 in debt, which was paid off over 3 years time.

OK. Rant over.

500 million is half a billion, not half a trillion.

You are right. My mistake.

“Just write the debt off”

One person’s liability is another person’s asset.

@old ghost If EVERY household in America paid an extra $1,000 a MONTH for a YEAR we would still not pay off $1.6 Trillion.

I pay in-state tuition at a large public university in Florida. Graduate school program. $990 for 3 credits. 30 required to graduate. Thankfully employer reimburses me tuition and textbook costs, but not a couple approximately $40 in fees.

Much more cost competitive than the >$70,000 program I was eyeing at Columbia in NY.

Write off debt that “won’t be repaid?” No, the government has a big stick. It demands taxes, or else. It can demand repayment, or else. Folks may be unhappy with that, but that’s why you don’t take loans from Uncle Sam in the first place. The government should get out of the loan business anyways. Puts government in this awful position.

Wolf Street.com, the only reliable financial news provider. I will hold off another quarter before I purchase my doomsday bunker.

@SoCalBeachDude UCLA was close to $1K/year for 3 quarters in the early 80’s when my sister went there (the state school I went to was a little less for 3 semesters).

If anything I think that schools like UCLA should “raise” not lower the price of tuition. I also think that they should make the classes harder and let kids transfer in to fill the spots of the kids that can’t cut it (vs. lowering the bar and inflating grades to get a “diverse” graduating class like they are doing now).

Before the 60’s less than 10% of American adults were college grads and I feel that the main reason they were more suscessful than average had to do that they were smarter than most Americans and “most” college students were already from the social and economic “top 10%” (aka they started on third base).

Today most (almost all) high schools try and get EVERY kid to go to (borrow money) and go to college (even the kids that have a hard time reading and doing basic math). It is no surprise that most 18 year old kids will take “free” money to go party at a “college” (and we now have half the men under 30 living with parents and I have a hard time finding anyone who speaks english to fix anything).

I remember when I sent my youngest off to college. Only 10 years ago or so. They did everything possible to exclude the parents from seeing what was going on or having access to any of her records. To give me access, even to pay online both she and I had to jump through all sorts of hoops.

I sat with her one year as she went through the registration process and the screen with the final bill came up. They offered student loan financing as an option and the checkbox for that option was pre-checked. To opt out of borrowing we had to go through 2 more screens and press several buttons. They made it so easy and painless to spend and borrow…a lot like congress I guess.