After the price explosion comes the hangover.

By Wolf Richter for WOLF STREET.

It boils down to this: In terms of single-family homes, sales that closed in June fell further, to approach the lows set in the prior two years, the lowest since 1995, seasonally adjusted; and supply spiked to the highest level since 2016, according to data from the National Association of Realtors today.

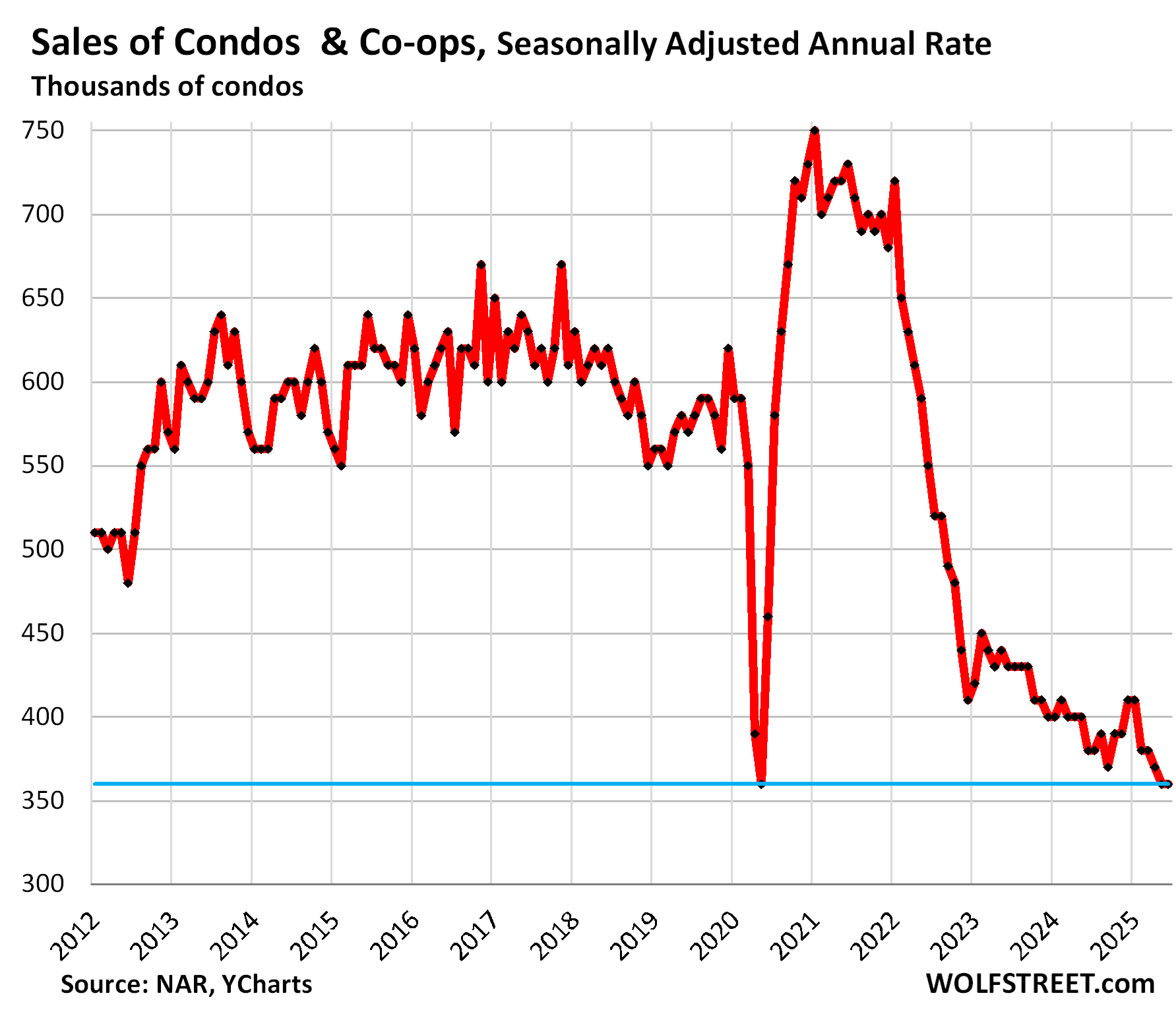

In terms of condos, sales remained at the low point in the data, along with May, and Lockdown May 2020, seasonally adjusted; supply ticked down a hair from the spike in May, but remained at the highest level since the Housing Bust.

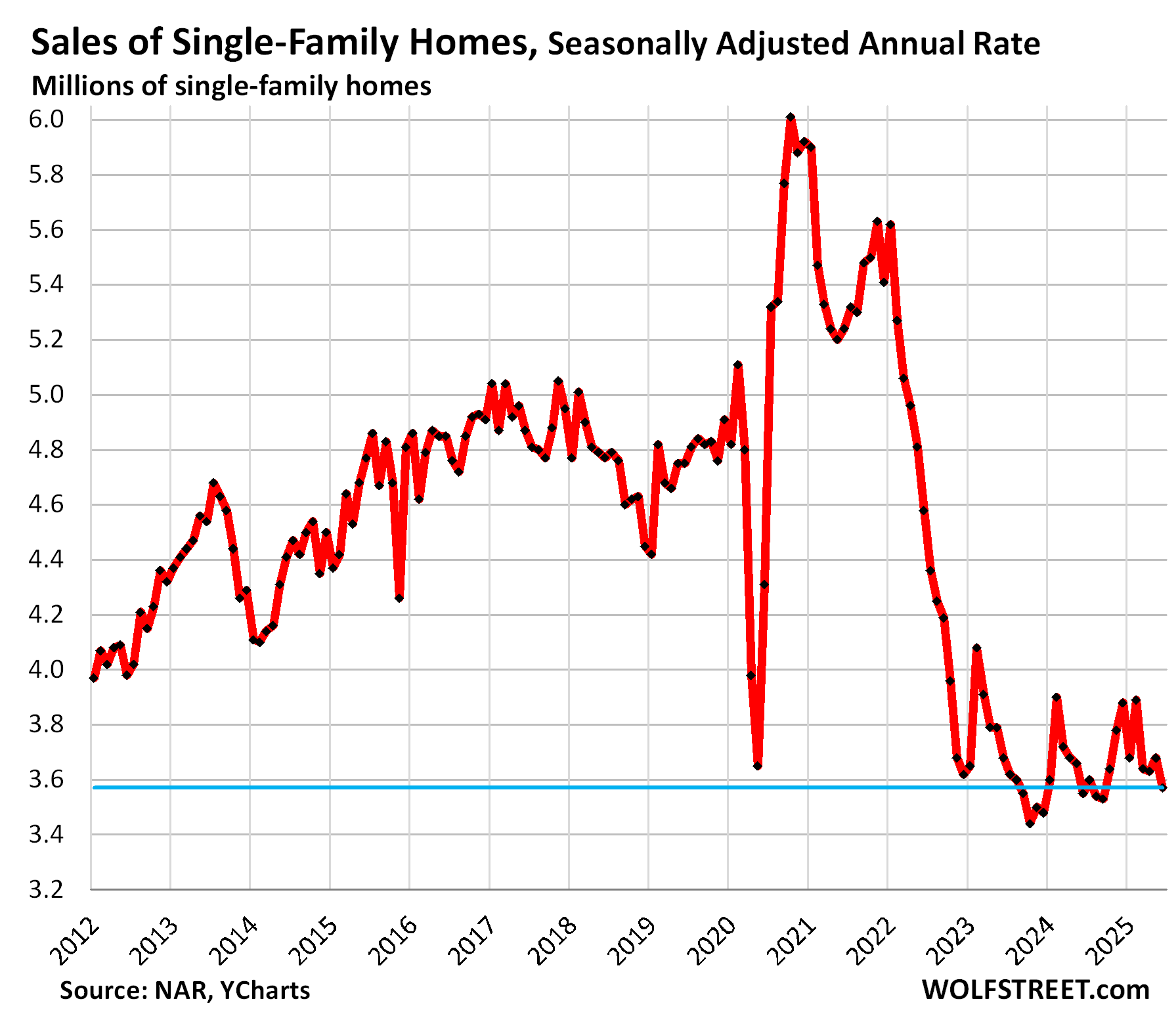

Sales of single-family homes fell further in June, to a seasonally adjusted annual rate of 3.57 million homes, hobbling along the lowest levels since 1995. They were roughly flat with June 2024 – with the year 2024 having been the worst year since 1995. Sales were down by 25% from June 2019, by 28% from June 2022, and by 32% from June 2021 (historical data from YCharts):

In terms of actual sales of single-family homes, not seasonally adjusted and not annual rate, 356,000 homes were sold in June, just below June 1995.

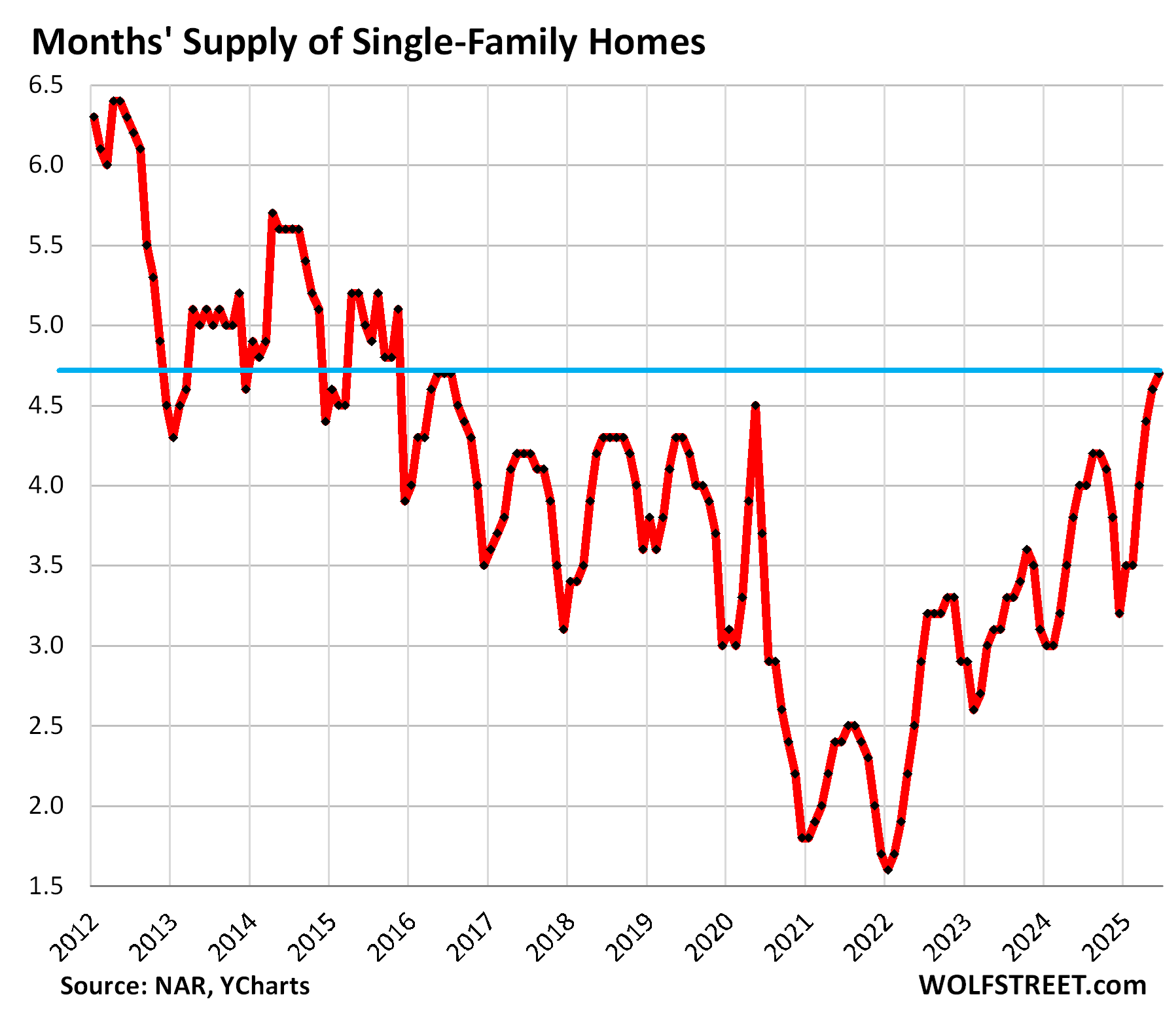

Supply of single-family homes has been spiking all year and in June reached 4.7 months, the highest supply since mid-2016, also 4.7 months. All of them were the highest since 2015 (historical data from YCharts).

Condo sales in June remained at the low point carved out in May, of a seasonally adjusted annual rate of 360,000 condos, same as May 2025 and Lockdown May 2020, and all of them the lowest in the data going back to 2011. Sales were down by 37% from June 2019. This is the effect of prices having exploded in recent years far beyond what the market can bear, and demand destruction on an epic scale has set in (historical data from YCharts):

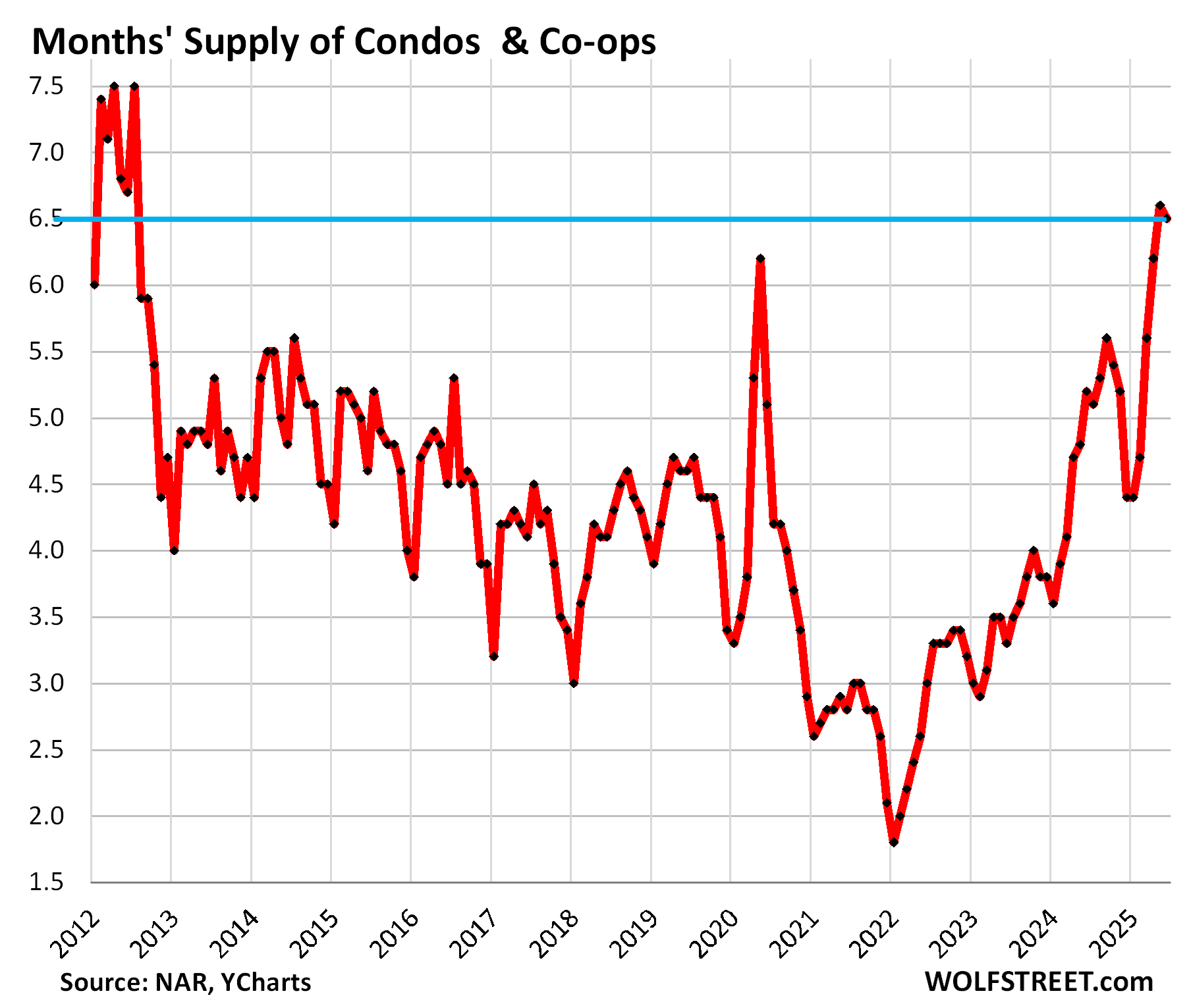

Supply of condos, at 6.6 months in June, is at the highest level since the Housing Bust in 2012 (historical data from YCharts):

End of the “housing shortage.” Supply spiking like this destroys the real-estate industry hype, deployed to drive up prices, about there being a “housing shortage.”

But what is real is that prices have exploded beyond what the market can bear, and so demand has plunged because prices are way too high. When sales began plunging in 2022, the theory by the real estate promoters was that sales were plunging because there was nothing to sell. But sales continued to plunge even as inventories soared, and now it’s a buyers’ market with plenty of supply, but there are few buyers.

Prices for condos and single-family homes.

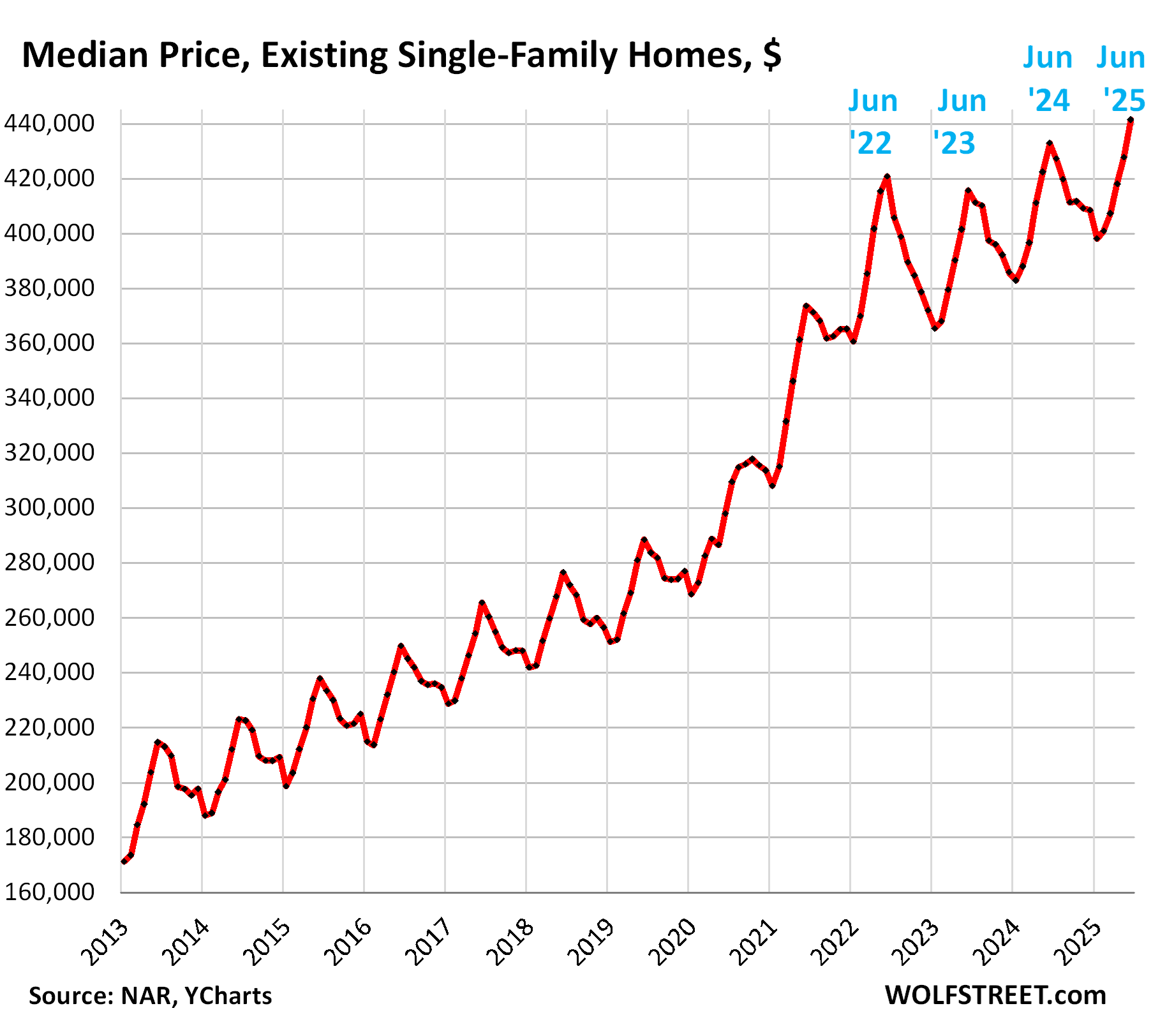

The median price is heavily skewed by changes in the mix of homes that sold (my explanation and chart of how changes in the mix skew the median price). In the spring, nationally, a larger number of higher-end homes come on the market and sell, which changes the mix of what sold and shifts the national median price higher. It does the reverse in the fall and winter. June is generally the seasonal high point of the median price, which then declines through January or February the exception was 2020).

In addition, when demand collapses, as it has now, it might collapse more at the lower half of the sales price spectrum than at the higher end, to where sales at the low end fall more than sales at the higher end, which also shifts up the median price.

The median price of single-family homes rose to $441,500 in June, up by 2.0% year-over-year.

This measure of the national median price had exploded by 50% in the three years between June 2019 and June 2022, on top of the large price gains in the prior 10 years, driven by the Fed’s interest-rate repression and FOMO.

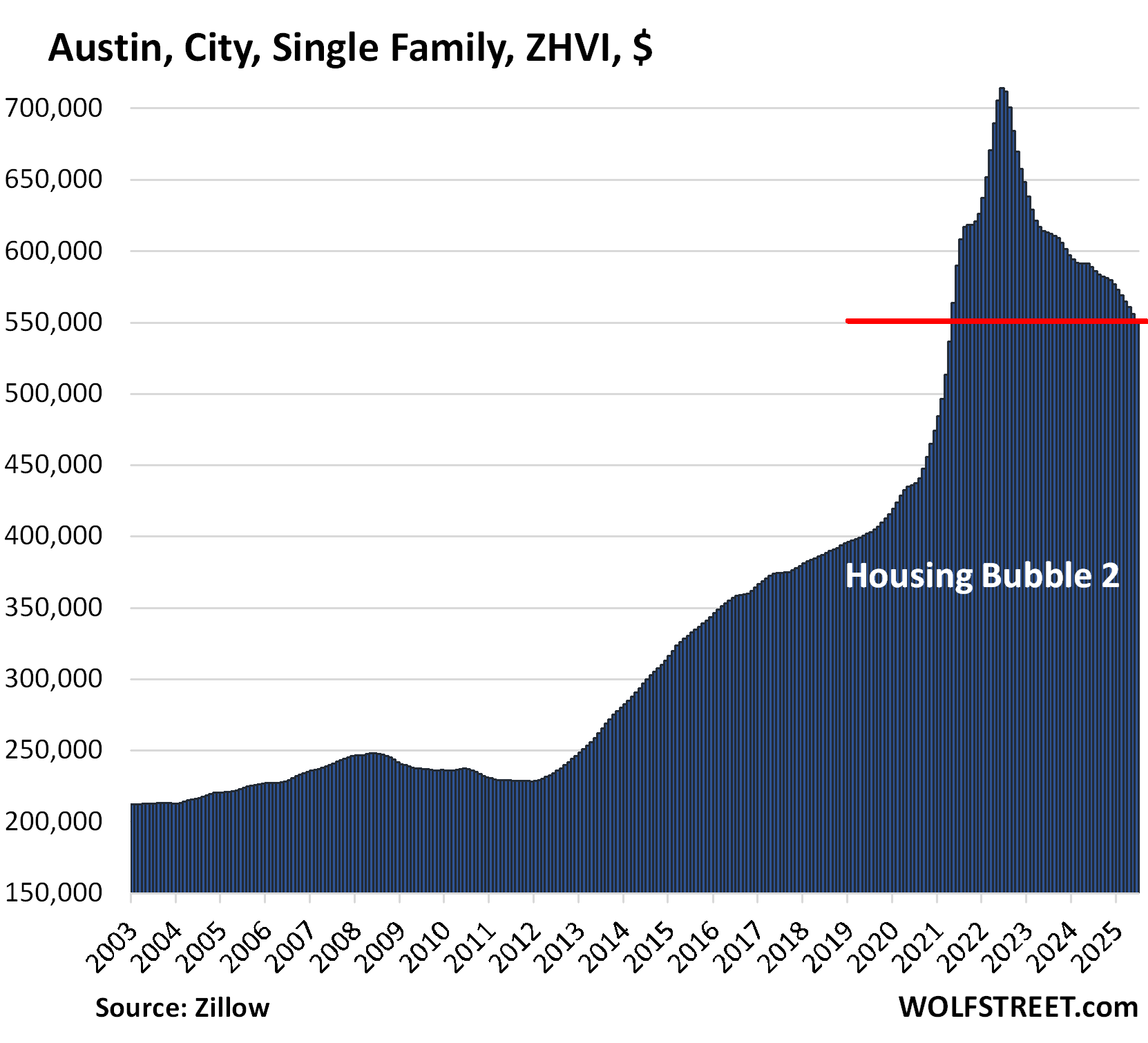

But lots of markets have turned. In 10 bigger cities, prices of single-family homes have declined by 9% to 23% from their peaks. And these are not median prices that are skewed by shifts in what sells. These are prices of mid-tier single family homes. The discussion and charts of the 10 are here.

Austin (-23% from peak) and Oakland (-22% from peak) are the top examples of the 10. Home buyers are not buying the national median home, they’re buying a home in a local market:

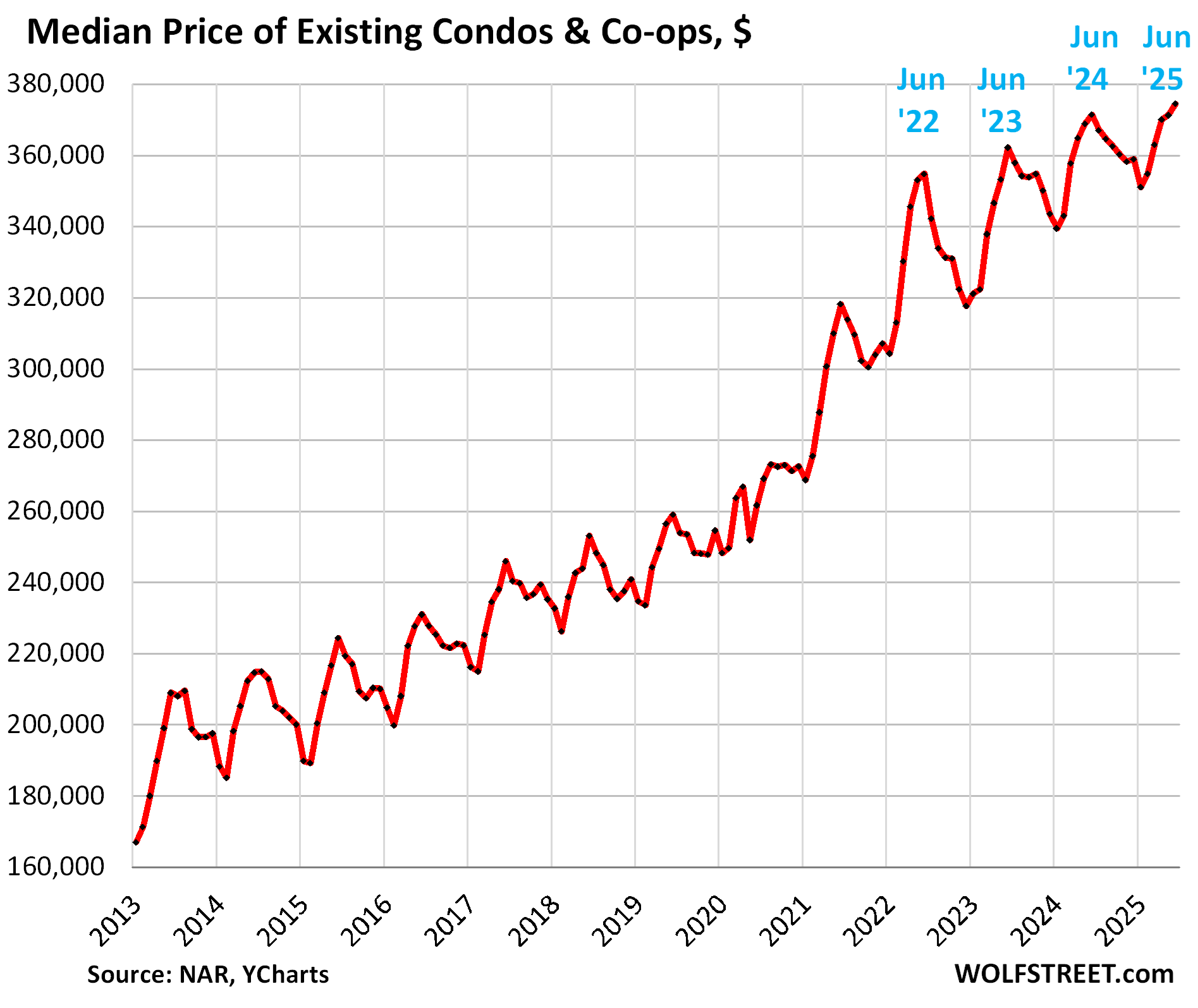

The median price of condos rose to $374,500 in June, up by 0.8% year-over-year.

This measure of the national median price of condos spiked by nearly 50% in five years, but in many cities, condo prices spiked by 60%, 70%, even 80% over those five years. Now those prices are way too high and don’t make economic sense anymore, demand has collapsed, and prices of mid-tier condos have begun to plunge in many of those cities.

By city and not using the median price: Here are the 19 cities were condo prices have dropped between 12% and 24%. The top two examples are Oakland (-24%) and Austin (-24%). Six of the cities have had price drops of 16% and more, including San Francisco.

Oakland condo prices are back to where they’d been in 2016:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I just saw the new excuse is high mortgage rates, I am surprised realtors are not pushing sellers to lower their prices, since they make $0 on no sale. I am not sure how the mortgage brokers and the realtors are making it with this little inventory turning over.

Listing agents fear getting fired if they push their clients too hard to lower asking prices. It’s a very careful dance. They want to tell prospective clients, list with me, I can get you the maximum for your property, but they also want to actually sell the property, which they can’t if the price is too high. They make zero commissions if their client drops them or doesn’t hire them in the first place, or if there is no sale because the price is too high. This is a very tough market for Realtors. Many have exited. It’s only fun in a booming market.

And to see a realtors face when you have the audacity to say..

“How about we both take a cut and get this sold? I’ll lower the price 10%, you lower your commission appropriately, say .5 or 1%. ”

The BS replies I’ve received have been priceless.

I ended up selling on my own both times and just smiled running into the agents months later.

Fsbo is making a comeback. As a buyer and seller I never met a realtor who brought any knowledge to the table. It’s comical how people are so lazy that they can’t put a listing on Zillow and hire a real estate attorney to handle the financials.

I absolutely don’t see any value in using realtor services especially when all the information is readily available.

I am OK with paying couple of grand to realtor for their services but we are talking big money if the home price is couple of millions.

@Danno every time I have sold a property (both personal residential and apartments) I have paid an extra 1% above market to the “selling” broker. When the property hits the market almost EVERY broker with a buyer will push them to buy it (whether it is a good fit or not) since the selling broker will make $10-$50K more than they would if their buyer buys another similar priced property. I have got the same look Danno has has from “listing” brokers but I have never had a realtor walk away since 1% less is better than nothing and they know that when I want to sell I am going to sell (I’m not a test the market guy who will waste their time).

@Danno,

Ha! Love that idea. I can only imagine those BS realtor replies. A colorful group of hot air balloons.

Here in Ohio, the “sucker fishing” competition continues. That is, some listings are originally placed with 2022 prices in the hope of landing a P.T. Barnum type of buyer. That buyer profile is still out there, but as Wolf pointed out, the supply has decreased.

The smart play on an agent’s part would be to wait for the seller to bring up the idea of a price decrease. After all, many of those agents initially received the listing because of their promise to “get the best price.”

So, 1) get the listing by promising a high selling price (despite the agent being fully aware that initial listing price will not be realized in today’s market), 2) wait for the buyer to bring up the idea of dropping the price when the home does not sell even after multiple showings, 3) blame the price decrease on “changing market conditions”, and then 4) repeat until the home sells. Lather, rinse, repeat.

That scenario is often playing out here in flyover land. More listings are showing price decreases – sometimes multiple decreases. Also, more listings continue to sit on the market despite those price drops.

It brings to mind the old joke about lawyers. How can you tell when they are lying? Their lips are moving. To which other group could that joke apply?

Sales joke…and to who else, Cold?…..well…..

Everyone loves affirmation. I think it’s one of the most basic sales tools, never having sold ANYTHING (or tried very hard…..although I could be a natural and not know it…doubtful) except maybe myself to get a job and guy toys/tools, and my off grid “house”. It IS sometimes hard to avoid “selling” in day to day living and in language, though……women, etc, etc. But let’s just say NEVER for a living, and/or for over an hour.

So read the Aesop fable about the Fox and the crow and the cheese and get it burnt into your brain. If the Fox feet fit, then WEAR them.

To me I’m an overeducated redneck (CA coastal logger species) that will never quit learning…….to others?….I have no FN idea.

Meaning others HERE…..My ONLY social media……I have some idea in the face to face talk world.

DC is getting rid of Realtors period. There have been so many complaints with the Realtor’s commission for unethical behavior that they’ve decide to require a brokers license to list property. A major class action suit was filed against Realtors by consumers which involved commissions for buyer’s agents who were ripping off buyers. The suit went against the Real Estate buyer’s Agents. Realtors are history in DC. Good riddance.

How can they be banned? What agency can make this happen? Are all the licenses of agents revoked? Please add more detail

Good luck with that!!!

The Prez is/was a realtor

Chinese will buy. 😓 On Chinese social media WeChat, Chinese realtors who are in Orange County, LA County & San Diego County now are pushing these inventories to Chinese who have made housing market unaffordable in Australia, New Zealand & who think housing price is cheap in 🇺🇸🤯 two European countries are on their favorites now – Greece & Hungary. Now let’s see what housing price will look like in these two countries in 12 months. What really disturbing is that all they talk about Re these homes are (1) how much $$ they can make through rents or capital gain & (2) how cities like Irvine not cheap (after they destroyed the pricing in those cities & turned everything into wealthy people game 🙄) . Greed @ steroids

What you describe peaked in 2017 and 2018. I even wrote about it at the time. This article is from June 2018. It has some screen shots of ads run in China about US homes. This is how the article starts:

https://wolfstreet.com/2018/06/07/how-chinese-investors-inflate-housing-markets-in-the-us-canada-and-australia-as-governments-try-to-stem-the-tide/

“Top residential real estate brokerages in the US have been promoting US homes to investors in China for years. Brokerage firms in Canada, Australia, New Zealand, and other countries have done the same. Commissions are at stake! They have set up units in China and are partnering with Chinese real estate portals, such as Juwai.com.

“Warren Buffett’s Berkshire Hathaway HomeServices, a subsidiary of HomeServices – the second largest residential brokerage in the US – entered the fray belatedly a year ago with a marketing agreement with Juwai.com “to syndicate all of its franchisees’ residential listings.”

But that mania peaked in 2017 and 2018, and then came the big flop. Since that peak, purchases by buyers from China have plunged by over 70%:

I remember this article and , hate to see that I had to compete with those in 2012-2014 when was just graduate with little rooky income.

Yeah, I remember that. Have a relative in the Irvine area who said they we “Fung Swaying” (or whatevering) entire developments and each house in them.

I scanned that whole link…..lot of forgotten names (unless people change them a lot) and was easier to get links in…some were really good, I think, like a USArmy link about China’s Capital flight. (just a guess)

Wolf’s work was load lighter then, I guess.

Depends on the market.

NY metro market is still extremely hot.

How do prices explode beyond what the market can bear, if the prices are set based on recent previous market transactions?

Somebody was willing to pay those prices, with the incentive of low interest rates, etc, at one point, and people are still paying those prices now, although not in the same numbers as in 2021-22.

Eloquently explained in the article: “…driven by the Fed’s interest-rate repression and FOMO.”

Now those buyers have their homes, the remaining market can no longer bear those prices, which is why sales have collapsed.

It seem likely that the market will bounce along horizontially (probably helped by the fed if (iff) needed) until prices intersect the prepandemic climb cycle in ’28 or ’29

Prices of assets (stocks or RE) can’t come down numericalically so just have to wait for inflation to bring pricea into a reasonable ratio with other prices (like bread, iron ore, bonds, milk, wages, etc)

“…the market will bounce along horizontally…”

That kind of horizontally?

https://wolfstreet.com/2025/07/22/the-10-bigger-cities-with-the-biggest-price-declines-of-single-family-homes-9-to-23-from-peak-through-june/

Or that kind of horizontally?

https://wolfstreet.com/2025/07/19/the-19-bigger-cities-with-the-biggest-price-declines-of-condos-12-to-24-from-peak-through-june/

Inflation, yes. You do not really make a profit selling your home. Given moving cost, commissions, gains taxes, state taxes, and inflation; you just like to think you do. This is especially true when moving from one to another home, which is possibly higher priced because of inflation. You can not win so you do not move.

“Prices of assets (stocks or RE) can’t come down numericalically ”

Brother, do I have some news for you.

SFH markets didn’t bounce around horizontally after the first SFH bubble – prices collapsed (after the Fed allowed semi-normal rates in 2006-2007, following the 2003-2005 Seeds of ZIRP).

The only thing that salvaged SFH (2011-2019) and ignited idiot bubble 2.0 (2020-2021) was ZIRP 2 (The Revenge).

The last 25 years of politically driven Fed interest rate policy has turned the US housing market into a highly volatile speculators market, fuelled by Government supplied leverage (artificially low interest rates achieved by money printing and Fed-Treasury fiscal incest).

exactly, the number of people willing to pay super high prices is very small but they are still out there

But not nearly enough of them.

Cmon don’t be disingenuous. If prices run up 200% and then fall 50% in a span of 5 years, that’s still insane growth.

Prices literally can’t keep on climbing forever.

Whoopti

“If prices run up 200% and then fall 50% in a span of 5 years, that’s still insane growth.”

True. A still insane growth of 50% total or about 8% growth a year:

$100 + 200% = $300;

$300 – 50% = $150.

from $100 to $150 in five years = 50% growth, which would be about 8% per year, still insane.

BTW, I didn’t say anything about price growth in my comment that you replied to with “Cmon don’t be disingenuous.” Maybe your comment got into the wrong place?

And the prices are going down slowly but surely almost everywhere.

If some location is left out of prices not going down, they’d catch up or down!

I’ve asked people who have paid peak 2022 pricing in the past 6 months, “Why? Why did you pay double for this house what it was worth in 2019?” Most of them have just done something like shrug and say “Ehh, that’s what they cost now.”

The thing is, they wouldn’t cost that if buyers would stop overpaying. Most have, as the article points out, but enough are still doing it that it gives the remaining sellers hope that their gravy train will come in too.

I bet @TSonder is a popular guy at parties asking people “why did you overpay for your home”….

Popular guy….,perhaps not but feel I would have fun having a few drinks/chatting with him!

Believe it or not, I have had people tell me that they paid over list or entered a bidding war, and even acknowledged that they overpaid. When someone tells you they overpaid, it’s not reasonable to ask why.

I overpaid in 2023. Life situations dictated that I needed to buy. I don’t plan to ever leave. It’s very affordable for me, but yes, I overpaid. I got impatient and I’m fine with it.

Sorry, that should have been “not unreasonable to ask why.”

I bet Sonder would be much more popular than some people here.

This capitulation by buyers is vexing. Even with the excess inventories, sellers seem to expect these huge gains and they’ve so far been rewarded for holding out.

Prices aren’t resetting in many markets (price are down a bit, but not that much) and I’m not sure we will see a 2008 style reset.

A lot of hot Locations have already seen big price drops and are still dropping .

Other Locations would catch up.

Prices have gone down and are going down .

Dont belive me .. Just read WRs other articles .

He has been meticulously documenting these price drops.

“they’ve so far been rewarded for holding out.”

Actually, you can only *really* be rewarded by *actually selling* – “holding out” only generates theoretical paper gains and very real carrying costs.

I get what you are saying (there is psychic satisfaction in paper gains) but there are no actual *financial* gains until you actually sell.

Cas127, what I believe GotRocks meant is that those who have held out, and actually sold, have been rewarded. In other words, if in 2021 in Florida or Texas 1,000 houses in a particular area sold, now only 400 have sold in that same period, because volume has collapsed. But those who have held out for 6 months and eventually sold have gotten close to the bubble price. The rest are just holding their overpriced house out there, waiting for a dumb buyer.

His point was that if all buyers collectively refused to pay peak 2022 pricing, nobody would be rewarded.

You also have to consider the interest rate.

From 2020 to 2024 paying People to stay home and receiving more money than could ever imagine jacked the economy/real estate up to unrealistic highs.

Those days are long gone, Time to come back down to reality.

Howdy 209er. Don t forget , ZIRP, No money down , No income verification , just sign your name and you can walk out of a closing with a check in your pocket. Only in AmeriKa baby…..

Ironically, the only mortgage product that does that is a VA loan.

albeit at a steep premium to FHA 3% vs. 1.7% in lieu of PMI

NINJA loans are long gone.

ARMs are making a comeback;

this time in a bullet proof vest.

Howdy MotorCity. You underestimate Govern ment.

I was renting a room at a vet friend’s around 1980-1, and I remember he and a couple other vets on the street all had a shit-fit when their loans went to 6% or higher…forgot. Maybe Cal-Vet loans?

I really don’t know, but I DO know the country and therefore the government OWED them MORE than that bit of help, Bubba.

1300 sq ft 3 bed 1 ba tract homes…..too much to ask for a year in hell, and a good chance of coming home in a box, or living in a VA home the rest of your life?

They were government…….did you underestimate anything?

“No income verification…”

Bubble 1 – Mortgage qualified if you could fog a mirror.

Bubble 2 – Absolutely everyone mortgage qualified because 1 million killed in pandemic and couldn’t fog a mirror.

The US has really rendered itself into a financially insane country.

Now is the time the Real Estate hype machine starts telling sellers that it is a buyer’s market and to price accordingly. They don’t make money unless things sell and they’ve squeezed all they can out of the bull market.

The next propaganda will be to price competitively to attract buyers.

Nah, they’re still at the rate buy-down and seller concessions phase.

Give it another year a or so…

Follow the Wolf.

The data point of median price is flawed, as mentioned in the article. In my mind, a better data point is price/foot on closed sales for homes in various strata (e.g., 2000 ft and lower, 2000-4000 ft, and >4000 ft) and in a specific locality, with the extremes on both ends disregarded. But this takes a lot of time to put together.

Which is what the data I used for my local home prices does: it’s “mid-tier” (the middle third, so that reduced the impact of shifts in the mix), “city” or “MSA” (so local markets), and it’s not median price, but based on millions of data points, from public records to Realtor associations, and includes sales pairs data.

And between 1995 and today the US population increased by ~21%. Or does “seasonally adjusted annual rate” factors that in already?

Seasonal adjustments don’t include population increases.

Actually it’s the complete opposite in south FL where I live.

The “~21%” is an about-sign (about 21%), not a minus-sign. Does that clarify the situation? It’s hard to see that it’s a squiggle line not a straight line.

Howdy Folks. Rut Row, is the hissing getting louder?????

Oh Boy, isn t this great???? Bubba maybe coming out of RE Retirement earlier than I thought.

Bubba. Quit being an a* s and know it all. It is ugly.

Howdy Countrybanker. Bubba loves RE.

Prospective buyers smell blood in the water. They can bide their time now. Can’t see how these trends turn around without a significant price correction.

This is me. I’m sitting on the money to buy a place pretty much outright. However, I refuse to pay double what things were only 4 to 5 years ago. The one thing keeping this going is the inflated stock and cryptomarket. The economy would be slowly heading into a recession if retail investors weren’t driving an asset bubble in crypto and stocks. I’ll keep riding the lows and selling the highs as long as people want to play chicken, but this seems insane at this point.

Everyone is absolutely convinced that the government will do everything it can to prop up the stock market, no matter how bad for the dollar.

Until something happens to challenge that deeply-held belief, the meltup in all assets will continue.

You mean like leading up to every other crash in history when investors were convinced that they couldn’t lose any money in stocks? Like when the Federal reserve was desperately cutting interest rates during the com crash and 2008 but stocks continued to crater? beliefs don’t mean spit against reality.

SuperHans, perception is a powerful drug. If people believe it and scoop up any dip, it becomes a reality until that belief is shattered.

Massive tax reductions over decades has put a lot of money into the hands of investors. And the tax code is designed to keep them investing.

Kent, how much money they have has very little to do with it.

People will act very differently if they actually think they’re going to lose.

75 percent of outstanding mortgages are under 5 percent, 30 percent of existing inventory has no mortgage, those folks make up the majority, they aren’t looking to sell…not every asset class should be a speculative bubble..zombie buyers, fomo and fools theory need not apply…

“30 percent of existing inventory has no mortgage, those folks make up the majority, they aren’t looking to sell”

If they don’t want to sell then why take so much pains to list!!!

Many interesting points here. One that I’m not seeing: pent up demand.

People have all kinds of good reasons to move (better job, family needs, lifestyle desires, etc). But sitting on a 3% mortgage is a good reason not to move. That has created a tension between moving, and not moving. In the long run however, that 3% mortgage is just a financial reason, and “life reasons” eventually win out. Those folks who overpayed in 22? Life reasons won out.

They will again, for many people, fairly soon.

Don’t forget, every buyer (other than first time buyers) is also a seller.

When the dam breaks, and all that pent up demand to move for “life reasons” starts to spill out, those seller/buyers will price reasonably (home prices fall) which will spur other seller/buyers, and sales volume will spike. No matter what the interest rates are (which will then be characterized as the “new normal of mortgage rates finally being accepted”).

The question we all wish we knew the answer to (but don’t), is WHEN will this happen?

I predict it will be a fast move when it comes, and that it will be in the next few years, but I don’t have a crystal ball as to exactly when. (I wish I did, my business relies on home sales volume)

“One that I’m not seeing: pent up demand.”

What we knew would happen has stared to happen: “pent-up supply” has started to become un-pent. Which is where the surge in inventory of existing homes is coming from.

Similar to my thoughts. Regardless of the size of bubble #1, the % drop of #2 is pretty small.

Could it be that enough people have the money to hold on to these homes indefinitely…empty or as NOT full cash flow positive rentals, be it especially PE, and also Corps, AI types, or even some just owning a few?

The wealth inequality is severe in this country, and I realize the subject is not popular here. And I apologize for my inability to talk house buying, owning, and selling talk.

If you look at inventory levels clearly there are in fact a lot of people who want to sell.

Their insurance, maintenance, and HOA increases make up the difference and also more reason nobody wants to buy at these prices.

Don’t forget property taxes.

And local governments directly profit (essentially costlessly) from inflated home valuations (the base of property taxes) – so local governments have a *massive* conflict of interest when it comes to allowing new housing to be built locally (baloney restrictions under “zoning”, “safety”, or “quality of life” rubrics).

Locals G’s would also profit (over a longer horizon – essentially inconceivable concept for fatback politicians) if *new* housing were allowed – but *new* housing supply comes with costs (roads, public service response, etc.).

Idiot home overvaluations are mostly free money to local governments (despite destructive influence on long term local economy).

How screwed up can local governments make things?

So screwed up *THE STATE OF CALIFORNIA* had to force freer market(!!) principles upon their local G’s (so ugly was the impact on the broader Cal economy from restrictive SFH zoning).

When the State of California is telling you your government is too interventionist…

The interest- rate induced lockdown of the Bubble Machines has only been applied to one industry this far.

Stocks, Cryptos, metals are at or near ATH or at least multi year highs. Total CryptoCrap has just bumped up against $4T. Total stock capitalization worldwide is probably $125-$130T. Only food and energy are staying tamed… for now.

Can the US debt keep up?

Home affordability is something which is directly impacted by treasury yields/mortgage rates. Stocks, other assets are impacted but not directly.

I see home prices going down over time, if the rates remain high.

I don’t see rates going down anytime soon, keeping in mind the debt level and deficit not going down.

Stocks and crypto don’t have carrying costs, so people can afford to FOMO.

They have carrying costs if they were bought on margin.

Even if they weren’t bought on margin, they do have opportunity costs. Right now, anyone can get 4% or a bit more on USD cash or t-bills. If the holder also has debt, then the payout has to be more than the interest cost of the debt that could be paid off, AND the tax rate on that income needed to pay the interest.

Sure, but 4% is nothing if you get 20% per year in stocks. Investors believe that will continue indefinitely, which is why the broader market has P/E ratios that are basically records.

Why are new home builder stocks rebounding? I thought it would be the opposite.

I can only speak for my little slice of flyover.

I would have to go back to pre GFC, since I have had a year were the job requests on new construction has been over 80% of our work.

Typical year 60-40. GFC 20-80.

Hi Tom,

Sorry I’m a little dense. Could you elaborate on your stmt “job requests on new construction”? I don’t understand the what this or the ratios below represent. Thank you, –Geezer

Live in rural flyover. No central treatment. All homes are on septic systems. Thats what we do. We are on site before permits are obtained for new builds.

You can still sell houses quite easily if you price them right and can offer financing incentives – which the builders can do.

It was an earnings beat on lowered expectations by DRHorton.

3.36 vs. 2.94 expected; less than 4.10 the previous qtr

Home builders are all low float stock and volatile;

also trade at very low forward multiples <10 pe

Existing home sellers are high as heck and refuse to cut their prices. New-home buyers only have to cut their margins some (and there was plenty of space to do so) and get to undercut existing home sellers.

That dynamic means that home builders can essentially build whatever volume they want, without fear of saturating the market, because the group that loses are existing home sellers. Combine that with still-respectable margins, and you have a good stock buy.

Losses also accrue to buyers of the new homes as the builder decreases prices and margins to sell homes.

The only real winners as prices fall might be renters.

Yes, that is exactly right.

Still not the home builders problem, though. And that still won’t happen much or quickly until existing-home sellers realize that to sell, they have to cut their prices and not just a little bit.

It also helps that those losses are only recognized if someone needs to sell the home, which usually doesn’t need to happen quickly if one doesn’t lose their job.

Wolf, you used “housing shortage” in scare quotes. It is taken as an article of faith in most quarters that there is a massive housing shortage in America. It’s never made much sense to me. Here you imply it is a fiction of the industry. In broader context it’s usually framed as an equity issue. I think I can agree that in some areas, housing is expensive, even insanely so (San Francisco) has come to mind, and even if it’s easing now, it’s still crazy expensive for middle class folks compared to their salaries). But I’m not convinced the answer is to just build a zillion more homes (and in SF, it’s probably not even doable). Do you have a take on this?

Yes, if you will, there is a shortage of realistically priced homes after the Fed and the RE industry have conspired for many years to drive prices out the wazoo. But there are plenty of homes. It’s just people cannot afford them. If you have enough money, you can buy multiple homes anywhere, and people do. If you don’t have enough money, you cannot buy anything anywhere. That’s the definition of a pricing problem, not a shortage.

Wolf: Would a bust be good for the country. I know there will be winners and losers, but overall wouldn’t it be net, net good for the industry and the economy? Thx.

A sudden huge bottom-falls-out bust would probably not be good for the economy in the short term. But if it’s a slow decline stretching out over the years, and is combined with income growth so that they can meet somewhere in the future, there would be big benefits.

High home prices (relative to incomes) are a big leech on the economy. So over the long run (we’re all dead), lower home prices would be:

1. good for consumer spending because consumers would have more money left to spend on goods and services. And that’s 2/3 of the economy, so it would be good for businesses that can sell more, and for the economy. Interest and principal payments and purchases of existing homes don’t go into GDP, but consumer spending does go into GDP.

2. good for employment because consumer spending drives business revenues and the economy, and a growing economy creates jobs

3. good for businesses (employers) in now-high-cost markets because compensation costs are much higher in places with high home prices, and lower housing costs would allow for lower compensation costs, and companies would have more money left over to invest in expansion projects

4. good for homeowners because the monthly carrying costs would be lower, esp. property taxes and homeowners’ insurance => which translates into having more cash left over to spend on other things in the economy, and so it would be good for the economy.

People can probably come up with other benefits to the economy.

The main drawback of long-term lower home prices:

1. Lower property tax revenues, which is why state and local governments pump up real estate prices at every chance they get. All they think about is extracting property tax revenues from homeowners.

2. Lower incomes for the mortgage lending industry that get paid fees based on the loan values; and for RE brokers because they get paid on the transaction prices.

So pros and cons, but the pros far outweigh the cons.

Let me tell you what is not good for the economy. The stock market being held up by AI providers and advertisers. Until you posted it a few days ago, I had no idea that Google and Facebook were taking most of the advertising revenue of the world. Now I know why every newspaper seems to be behind a paywall now.

Just about anything that posts an interesting article to read is behind a paywall, not just newspapers.

Back when I subscribed to (ie paid for) printed newspaper, they had adverts. So, now why should I expect to read free online? Someone has to pay for content, and of course mgt, hosting fees, etc.

I think the early internet trained folks to think content was free.

Dougzero, you completely missed my point. They have to go behind paywalls today, because they can’t make money on the digital advertisements, because Google has used its monopoly power to steal it all.

Read Wolf’s article last week on it.

If there’s more transactions though because things become affordable would that eliminate con #2?

“Lower property tax revenues, which is why state and local governments pump up real estate prices at every chance they get. All they think about is extracting property tax revenues from homeowners.”

Say it louder for the folks in the back!

“4. good for homeowners because the monthly carrying costs would be lower, esp. property taxes and homeowners’ insurance”

check it out….the insurance companies devastated by the global warming catastrophes still managed to record all time high record blow out profits the past 3 years. Buffett be lovin’ his Geico. The rules are set up whereby you must have insurance if you have a mortgage. “It’s Big Club and you ain’t in it.” – Mr. George Carlin

I don’t see the logic in your drawback #1: In CA, where I live, ptax is driven by what you paid to buy the house, and doesn’t go up relative to current market value. LG only benefits from turnover of houses that have appreciated in value over time, and the new buyers pay PT at the new value. Have you ever heard of a LG actually reducing PT???

Buyers of homes will pay property taxes on the price they paid. And if that price is 3x of what you paid 10 years ago, they’ll pay 3x as much in property taxes. That’s hugely important for California. There are a lot of transactions every year — in a good year, not now — that reset the property tax payments on that property. In the last good year, 2021, there were 444,000 transactions in the state.

If the stock market keeps at ATH and consumer spending stay buoyant I expect home prices to dip/level off before a move higher

A decline in tax revenue assumes that local governments actively accept the loss by giving out lower assessments, and passively accept it by not adjusting the tax rate.

Some locations that are allergic to taxation will fall prey to a property value decline. But others will just adapt. Property value declines don’t necessarily decrease income so there’s little inherent reason that total taxation must decrease.

I don’t think local governments will be able to get away with such tricks forever.

Raising rates in many areas is impossible without a referendum that I have little doubt would fail since the government wouldn’t be able to justify the tax raise with extra services.

As for your valuation idea, not only do I think courts would take a dim view of a practice like that, so would the public. Furthermore, some localities are already locked to transaction prices, like those in California with Proposition 13. If revenues in a place like Los Angeles go down at all for any reason, they will have to default.

Everyone takes a dim view of tax assessment practices. But it happens anyway. You have legal recourse but it’s slow, unreliable, only saves you a few hundred dollars, and then crushes your Zestimate. So only retirees who plan to die in their current house go through with it.

My operating assumption is that these housing prices are going to fall by 80% when this bubble is all said and done.

No way that assessed value continues at 2022 amounts when the actual home is not worth even a quarter of that. What you’re essentially describing would be arbitrary taxation and even if it’s legal now, it wouldn’t be for long when the bubble collapses. And of course, after the bubble collapses, why should anyone care about some estimate that may or may not be indicative of the actual market?

You are correct that local governments have some leeway on the matter, but not so much that they can assess the value of your home at 5x the value it really is. If they did, why shouldn’t they be doing that now, when they’re already running into fiscal trouble? Why shouldn’t some ghetto crap shack in Chicago be valued at $5 million for tax purposes?

The reason why is because they would get shot down, and furthermore attempts to do so will mean, at the least, that they will lose the leeway they’re given now, or perhaps they’ll lose the ability to tax property altogether. Certainly your valuation idea would violate several Constitutional amendments, most notably the 5th Amendment.

In my state, one can appeal their town’s assessment to the state; there is an entire division (board of land appeals) that adjudicates disputes between property owners and municipalities.

Earlier this year, I submitted an appeal for my 2024 assessment. It is currently expected to be heard sometime in 2026, and due to case volume the court has recently encouraged me to mediate with my town.

Seems like a lot of folks don’t think they should be assessed based on peak BS bubble prices.

I wonder if the big banks and mortgage companies are looking at how many mortgages in their portfolio are at those peaks in 2022-2023 and are making contingency plans for the eight year point (average life of mortgage). Some of these people (sellers and/or mortgage holders) are going to take a pretty good haircut when it comes time to sell/move.

I keep thinking of the line in “Margin Call” when the Jeremy Irons character John Tuld says:

” I’m here for one reason and one reason alone. I’m here to guess what the music might do a week, a month, a year from now. That’s it. Nothing more. And standing here tonight, I’m afraid that I don’t hear – a – thing. Just… silence.”

Banks are not too worried. They washed their hands off most of the mortgages.

The government now guarantees a big majority of the mortgages and packaged them into MBS and sold these to investors. Not even the investors carry credit risk; only the taxpayer does.

Many of the remaining mortgages were packaged into private-label MBS and sold to investors, but these investors do carry the credit risk. Still banks are off the hook.

There are only $2.3 trillion in residential mortgages on bank balance sheets, and that includes 2-4-unit multifamily loans. That’s only 18% of the total household mortgage debt. But the percentage is even smaller since the $2.3 trillion includes 2-4-unit multifamily buildings that are not part of the household mortgage debt.

This is one of the big changes coming out of the financial crisis: the banks will walk away from the next housing crash with a bruise, but the taxpayer will get mauled. But no one cares about the taxpayer.

Flat prices until 2035 will cure everything about this housing bubble. Nobody makes stupid money, nobody loses everything they own, “saving up for a down payment” actually means something again. And by then the Fed should finally be out of the MBS business.

It’s only the land under the house that actually gains in value – the rest of it rots away and costs you plenty. So basically these bubbles have just been land speculation crazes over and over.

You’re dreaming. Learn about normal economic cycles and corrections.

Simply having flat prices until then is wishing dreaming at best.

Median housing prices need to come down to no more than 150k nationally so that younger generations can work up the demand to clear the market in the face of Baby Boomers housing investments being sold off.

Unless you’re proposing that over that timeframe younger workers get a quadrupling of income, you’re practicing wishful thinking at least as bad as the real estate industry hype. And even if you are, you’re still practicing wishing thinking at least as bad as the real estate industry hype.

No, this will only end one way – a long-term crash where prices go down and stay down for a long time.

If we have a lot of inflation over the next 10 years, and home prices trade sideways, they will be affordable again relative to income.

Inflation alone will not cut it. In fact, inflation in non-home pricing will actually make things worse for the home market since it will make less income available for home buying.

Even if you assume only wage inflation happens, and that all other inflation doesn’t happen at all, you need the income of that 25-34 age group to quadruple if you want current home prices to make sense for them. It’s not quite that bad for older ages, but it’s not all that much better either.

To have this happen on a 10-year time scale would require wage growth faster than any time in history, in any country – ever, particularly concentrated on the lower income brackets and the young.

So – either fantastical wage growth better than anything that has ever been seen anywhere, or housing bubble pops and prices fall by 60-80% (most likely the higher end of that). I know which one I’m betting on. This is why I said that if you think home prices will be sideways for a long time, you are guilty of delusional thinking just as much as the idiots who think housing prices can go up forever and ever without end. This will end only one way – a crash, panic, and enormous losses to those who were stupid enough to buy into any other narrative.

The thing about inflation is it’s like the tide, all boats rise when the tide comes in. So with higher inflation, housing prices could easily rise again, but maybe not nearly like what happened during the free money period.

Inflation-adjusted house prices are about double what they were in 1987, amounting to approximately a 2% annual increase over that time.

Inflation-adjusted mortgage payments are about 20% higher than they were in 1987.

House price to median income has increased about 50% since 1987.

The housing affordability index (i.e. mortgage payments as a percent of median income) is about where it was in 1990.

None of these really points to a crash, but taken together, they hint at what Short TLT says: about 5 more years of no price increases (or slight decreases) coupled with 3% inflation and continued household income growth. This would be a roughly 15-30% drop in real prices (after inflation adjustment)

One way of explaining the bubble is that ZIRP made housing the most affordable it’s been in US history (or at least as long as anyone alive can remember).

Even the land price goes down and is going down.

No flat prices for years as prices are already going down as documented by WR.

America’s biggest car makers left furious as Trump’s tariff deal backfires and hands massive win to their biggest foreign rival

President Donald Trump just signed what he calls the ‘largest trade deal in history.’ But America’s carmakers hate it.

America just reached a trade deal with Japan — US automakers are furious.

Tuesday night, President Donald Trump announced a deal to slash tariffs on Japanese imports to 15 percent, including vehicles and auto parts.

Under the deal, Japanese-built cars will face lower tariffs than the parts US automakers import to build their own.

The kicker is that US manufacturers pay 25% when importing cars and part they build in Mexico or Canada.

Another walk into the abyss for US manufacturers is the insane cost of steel, aluminum and copper. The insane tariffs are causing major dislocation of manufacturing in the US. GM’s profits are down 35% and the crushing of margins is just starting.

Who does Trump work for?

“GM’s profits are down 35% and the crushing of margins is just starting.”

Good. GM is among the worst in having offshored its production. It’s importing vehicles from China, South Korea, Mexico, and Canada. All Acuras, all Teslas, most Hondas, many Toyotas, etc. are assembled in the USA and have 65%-plus US content. There isn’t a single GM model in that group of 65%-plus US content. GM was bailed out of bankruptcy by the US taxpayer, and in return, it offshored production to other countries, in a big F.U. to the US taxpayer. Now they have reason to undo this massively stupid gamble and bring production back to the US, and they’re doing it thanks to the tariffs. I don’t give one iota about their profits as long as the incinerate billions of dollars in cash with share buybacks.

Here is GM discussing this situation in its earnings call (Click here).

@wolf two quick questions

1. Does the impact change if Fannie and Freddie get spun off like the administration has been discussing?

2. We’re seeing these declines with a stock market at record highs and unemployment at all times low – so people are in a good financial situation. What happens if that changes? What do these graphs look like if there’s a prolonged 20-30% stock market decline? Crypto drops 50%? Or unemployment spikes to 5-6%?

Good questions. Answers will be pure speculation. In terms of the spinoff, if it takes place, the devil is in the details. A big stock market decline and/or a recession would put a lot more pressure on the housing market as it might create highly motivated and forced sellers while taking even more potential buyers out of the market.

State Farm sparks backlash in blue state of Illinois with record rate jump

State Farm has sparked fierce backlash by hiking home insurance rates in Illinois by 27.2 percent, adding $746 to the average bill.

The insurer insists the hike is unavoidable, claiming it’s paying out far more in claims than it collects in premiums in the state.

For every $1 collected in the state in 2024, the company says it paid out $1.26. The year before, the sum it paid out was even higher, at $1.30.

Hail damage is the main culprit, the company said, with Illinois trailing only Texas for the number of hail-related claims last year.

Rising labor and material costs have also driven up repair expenses.

But lawmakers have blasted the price hikes, which could hit policyholders as soon as August 15.

Illinois Governor JB Pritzker called the increases ‘unfair and arbitrary’, promising to work to deliver more protections for homeowners in the face of soaring costs.

Illinois is one of the few states where insurers can raise rates without approval from regulators.

I’ve had a bearish outlook in housing for a decade, but I was bullish, selling my house in June 2022 — no regrets!

I’m now turning super bullish and have daily pangs of FOMO, and look at these recent volcano charts @ Wolf World, as hysterical — clearly seeing gargantuan tsunamis of opportunity, versus a ridiculous unfolding crisis — why the change of heart? Easy, it’s Crypto Stupid…

It’s as simple as two wrongs making a right – pure math — it’s integers,

I saw this story on the internet, and I was immediately, magnetically sucked into a totally new orbit, that gave me a super tight perspective:

“ Turn your home into a Bitcoin acquisition engine,’’ one of the start-up firms called Horizon, said in a post on X.

Here is how it typically works: Some of the firms loan the homeowner cash to buy Bitcoin based on the value of the equity in their homes. The firms typically make money by sharing in the appreciation in the value of a house when an owner sells it.“

Duh — it’s pretty friggn simple to see, all this exploding inventory is going to be vacuumed up by bitcoin exploding higher. No need to expand narrative.

All those mummified baby boomers that are locked in to cheap rates, will unlock their mortgages, when Gen-Z crypto wizards dangle digital diamonds in front of these ancient fools — like shooting flash frozen fish in a trawler fridge.

What we need, is moar inventory!

R

Respectfully, you are either insane or a moron. Perhaps both ?

I suggest a third possibility: he’s being sarcastic!

Phil

Possibly……in that case the correct notation is /s

As long as we the rational buyers who stand together & hold on the strike, let those speculators especially Chinese who cheat on their system & now want to screw our market like how they did to 🇨🇳 market get burned.

One home in San Clemente sold on 06/07/2024 for $1,618,888 listed $1,869,000 for sale on 06/11/2025. Just dropped the price $370k.

I wonder whether the $$ to purchase this house is tied to a criminal investigation now against Wells Fargo executive Ms Mao who just got deterred in Shanghai. Mao allegedly helped somehow moved $264B last year.

I wonder how much is $137B home purchase $$ is with her help.

🇨🇳 govt imposed more restrictive regulations prevent Chinese from buying properties overseas especially not in 🇺🇸.

Things are getting interesting.

I’ve seen homes in the Seattle burbs (the Eastside) that were bought 6 months ago or so, got maybe a $50-80k remodel (I can only guess as I did not see them the first time around), and now relisted for $300k+ more. It just blows my mind. I’ve done complete cosmetic remodels so I have some idea of costs.

At the same time I see “paint” remodels where obviously no one ever remodeled a kitchen or bath, and sellers think their $1M time warp w/new paint actually competes with houses within a mile of the same size that at least got new kitchens & baths in the 90’s or 00’s.

These are (were) your middle class hoods where in the early 90’s that home was $2-250k. Now $1.35M. I know as I owned one of those homes.

I’d love to see one of these $1M “middle class” 2200 sq ft homes finally come down to the 800’s. Finally help my son get into one.

“…and now relisted for $300k+ more”

They’re going to have a lot of competition and not a lot of buyers:

IMO you are likely to see continued home price reductions due to tech layoffs on the Eastside. Microsoft recently eliminated about 3,000 high paying positions locally. I think that means a lot of contractors got laid off too. Plus, tons of new apartments are coming on market for the many workers who cannot or will not purchase housing.

Frankly, I don’t know why anybody would want to buy one of the old drastically overpriced homes in the area. Most of the mechanicals, plumbing, carpets, windows, insulation, and roofing usually need replacement soon, and who knows what lurks under the home and inside the walls with all the darkness and water. My advice to anybody considering the area is to rent a nice new place near your job or near a rail line. Forget about buying anything unless prices crash.

If you buy a decent place now, you wind up paying an additional $1M compared to other cities/states. That extra million tied up in housing can earn you $50k to $100k a year in investment income.

“After the price explosion comes the hangover.”

I say “After the tsunami comes the devastation!”

Maybe even TEOTWAWKI in the real estate realm.

On another website, there is a headline “ June home sales drop as prices hit a record high.”

It’s TOTALLY the Twilight Zone. Maybe they should change the headline to say “Every home sells for OVER $1 Million, but there are NO buyers.” 🫤

This market defies gravity, defies all reason.

The market doesn’t defy gravity, the headlines do. Also helps to read the section where I discussed prices that you mention, rather than just regurgitating braindead headlines here. So go back upstairs and ACTUALLY READ the entire section about these prices; don’t skip anything.

There are many markets with big price declines. Here is are bunch of them. Click on the two links and look at the pictures:

https://wolfstreet.com/2025/07/22/the-10-bigger-cities-with-the-biggest-price-declines-of-single-family-homes-9-to-23-from-peak-through-june/

https://wolfstreet.com/2025/07/19/the-19-bigger-cities-with-the-biggest-price-declines-of-condos-12-to-24-from-peak-through-june/

Where you will find charts like this:

Austin, My dear Austin: At one time, one of the hottest housing markets in USA. I have friends who bought homes there to rent out. Now prices are crashing there and almost all over USA.

The ride down just started, buckle up guys!!

A lot of Americans purchase $1 million homes and $100k cars, but even more can’t afford $100k homes or $10k beaters.

The Fed’s “Wealth Effects” for some, “resulted in poverty” for most.

Who needs personal responsibility when you can easily blame the Fed!

When you have an official policy of inflating assets in order to encourage people to spend more, you don’t get to play dumb when the few percent who own a disproportionate share of the assets benefit from that way more.

Housing rising much faster than incomes. Economy is being run in reverse. In the US Golden Age in Capitalism, velocity financed 2/3 of the economy. Today money finances virtually all of the economy.

Stocks are being pushed up by an expansion of the money stock. This will reverse.

What expansion of the money stock? That ended over 3 years ago.

I’m in the Boston metro area. Still renting and investing what’s leftover in the hopes of a first time purchase eventually. The math don’t match to afford a 3BR 1Bath anywhere around here (the burbs)

I have hope the market will correct, but trends are less dramatic up here, and idk why, but somebody is still buying the inventory.

My plan is to allow the math to math…logic says there’s room for prices to decrease but the narrative is “Boston never loses value’

I wonder what effect companies like Blackstone have on this market. They have a vested interest in keeping the rents high in the properties they own. Or are they more likely to just be selling the single family homes they bought cheaply at the last bottom and redeploy the cash elsewhere.

The biggest single-family landlords — Blackstone is not among them, they spun theirs off via an IPO — have said for over a year in their earnings calls that they’re SELLING homes that they’d bought in 2012. They’re building entire new for-rent developments. Some have their own builder divisions, others work with D.R. Horton and other homebuilders. This build-to-rent is the hottest thing in the housing market. For landlords, it makes total sense. Instead of having 400 older rental houses with lots of maintenance problems scattered all over a market, they build a development of 400 houses with its own leasing and maintenance office, common amenities, such as a pool, etc. These are nice houses, for renters of choice with above median incomes who want to rent, instead of buying. Part of the supply on the for-sale market is from these home builders that are dumping homes they’d bought in 2012 at huge profits.

Kinda like selling Capital Equipment to people or groups who want to start businesses?

Or are my terms/concepts wrong?

I consider these to be rotten evil businesses, but you already knew that.

No answer means “sorta”, as I have obviously made up my socialist mind…..making the question a statement, and know you are busy.

In my market, Long Beach, CA. I experience house flippers that are buying high and selling really high with below average materials, but good marketing. I call them the Temu Flippers. I’ve tracked a distressed house in my area that purchased for 850k by a realtor, then sold to the Temu flipper for 1m. Temu flipper replaced everything down to the studs and sold 5 mos later for 1.3m Young couple that bought it said, everyone they know is buying houses at 1.1 to 1.3 and that’s reality to buy a house today. They just have to pay the higher price.

Are consumer opinions about a house shifting from an Elastic Product to an Inelastic Product? I need housing, so I have to pay the higher price.

Long Beach, CA market prices are remaining stable at the price right now and not decreasing as inventory as increased a bit….maybe because?

1) Prop 13 purchase keeps owners property tax at the lower purchase price before 2021 and to get a better property the price is too high for the salary. Prop 13 discourages housing movement as opposed to Texas where property taxes assessments encourage new development for cities to expand housing options increasing supply and lower prices.

2) Movement from LA market work from home employees to cheaper Long Beach market added more homeowners. The diff between avg LA and Long Beach house is smaller now than in 2020.

3) Less decerning buyers hoping for government future rate decreases to make housing more affordable. I believe we have a generation of people that say we need housing and it’s a human right and not a privilege. Government Bailouts and market adjustments have given this perception.

4) Airbnb – This is a small percentage, but I see inventory being snatched up for profitable short-term rental investments. People willing to pay $600/night in a single-family home instead of hotel for 6 people removes available inventory of single-family homes.

5) The Temu Flipper is willing to forgo the average flipper commission and buy houses for higher prices and then sell at even higher. The avg margin for flippers in this area was 5-8% and I’m seeing Temu flipper with 1%-3% margin. They could be laundering money for their investors or making it up in loan arrangements and payback for design services, realtor listing commissions. idk how they make this little and stay afloat.

Long Beach has some of the worst houses in Southern California and has only two nice areas for houses – VCC (Virginia Country Club) and Naples. Most of the junk in Long Beach used to sell well below $100,000 and is now more run down and junky than ever.

Agree, but these junk 50s houses are the only thing in my price range at these rates. But my rent is about 2k less per month than me putting a big down payment in and getting a 6% if I’m lucky rate for 30 yrs right now. 5 miles from the beach, meh I think I’ll just keep renting.

Genuine question,

Are we seeing a deflation or even slowing of inflation in the housing component of CPI?

Would it be due to a lag or how it’s computed for CPI?

I feel like if housing values are going down it will crater inflation with how much it affects CPI.

*Disclaimer I’m far from an expert so I’d appreciate people correcting or informing me or evening telling me what Google to learn more

Housing inflation measures in CPI are based on rents, not home prices.

CPI tracks “consumer price” inflation. Homes are considered assets like stocks, and not goods that consumers “consume,” and therefore don’t go into consumer price inflation measures – they go into asset price inflation measures, such as the home price charts depicted on this site. “Home price inflation” is a thing.

But if CPI housing measures were based on home prices, we would have seen massive deflation (big negative overall CPI readings) for two years during the housing bust and Financial Crisis in 2007-2009, but obviously, inflation was alive and well at the time, except for a brief period when the price of oil collapsed from $150 a barrel.

Thanks for the informative answer. I appreciate it. That certainly cleared some things up.

Hello everyone,

This is the first time I have stumbled upon this writer. Great writing and wonderful followers with comments.

I’m in the Raleigh, NC area and the home prices here are dropping. The most over hyped areas, Sanford, NC and Cary, NC are finally seeing price decreases as well.

Housing is always about supply and demand. Focusing on national data for housing is a fool’s game–even the metro by metro data shows that almost all of the price declines are in the far west and deep south–and the states with the most construction are (drum roll please) Texas, Florida, Cali, etc. Go figure, national, massive builders went all-in in those markets and are now scratching their heads on what to do with the excess inventory. That isn’t a tale of national collapse, it’s market-specific supply and demand imbalance. Not to mention the talk of 50% declines–the financial crisis led to 35% or so declines, 50% declines in the overall housing market means more than financial catastrophe that none of us can really imagine.

Investor sentiment remains complacent about the real estate market, as judged by the Housing Fear & Greed Index.

Apparently, this is just a short-term setback to the next new highs, in their opinion. Only more steep declines might change this greedy mindset.