They’re among the stragglers, behind other big markets whose inventories have shot up to at least decade-highs.

By Wolf Richter for WOLF STREET.

Inventories of homes for sale in the Midwest, the Northeast, and the Mid-Atlantic have also started to surge, but are behind the other markets, and their inventories are still far below where they’d been before the pandemic, and in some of those markets are still low.

These markets are the stragglers. In Texas and in Florida, and in some of the formerly hottest markets in California, inventories spiked to the highest levels in at least a decade, and in the metropolitan areas of Seattle and Denver, inventories also shot up to the highest levels in at least a decade.

The stragglers that are now coming up are the metros of Washington D.C., Boston, New York City, Philadelphia, Chicago, and Detroit, where active listings of homes for sale are still relatively low though they have begun to surge too.

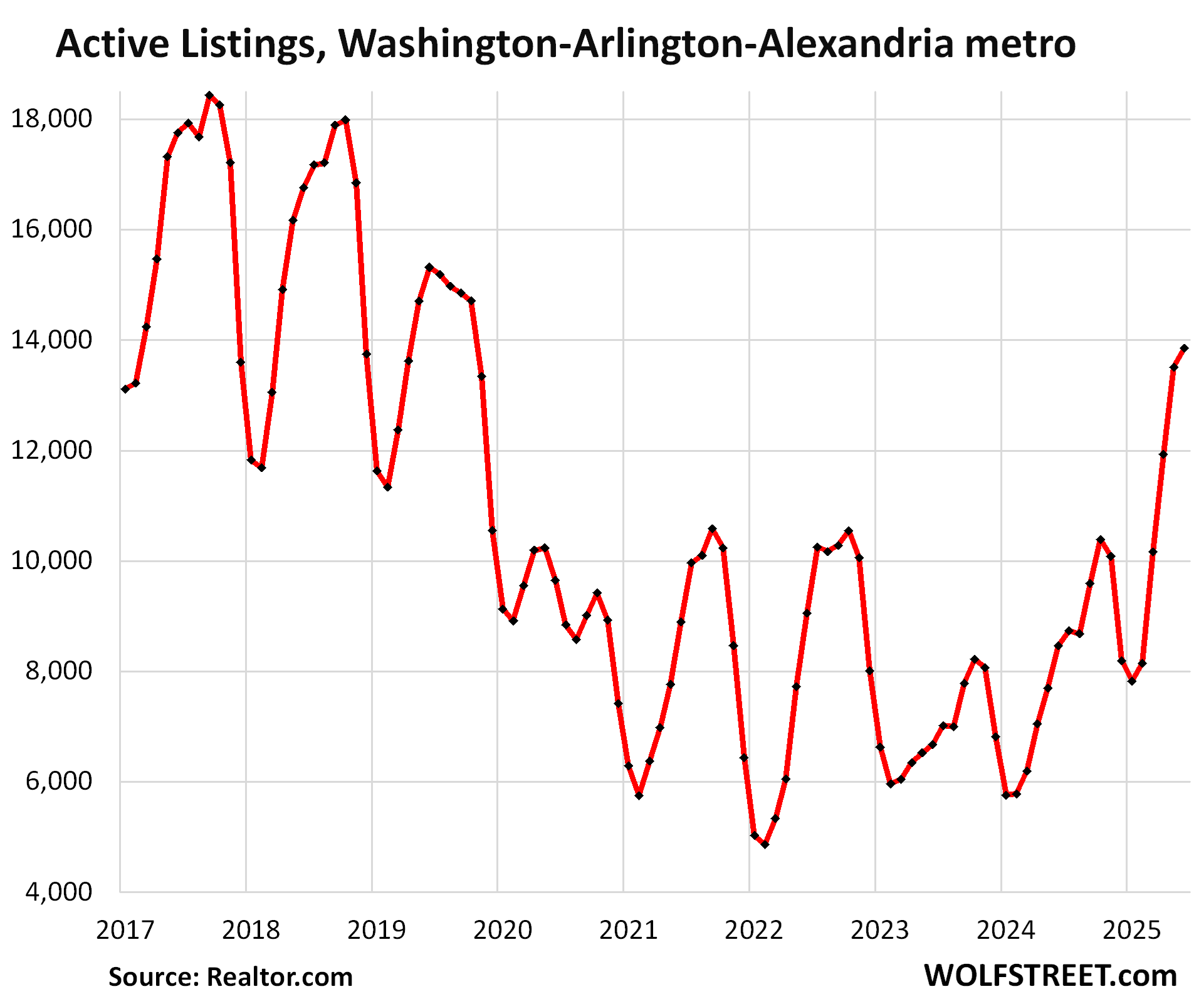

In the Washington-Arlington-Alexandria, DC-VA-MD-WV metro, active listings spiked by 64% from June 2024 and by 107% from June 2023, to 13,854 homes listed for sale, the highest for any June since 2019, according to data from realtor.com.

But that spike in listings started from ultra-low levels, and so listings in June were still down by 10% from June 2019 and by 17% from June 2018. But they’re on the right track:

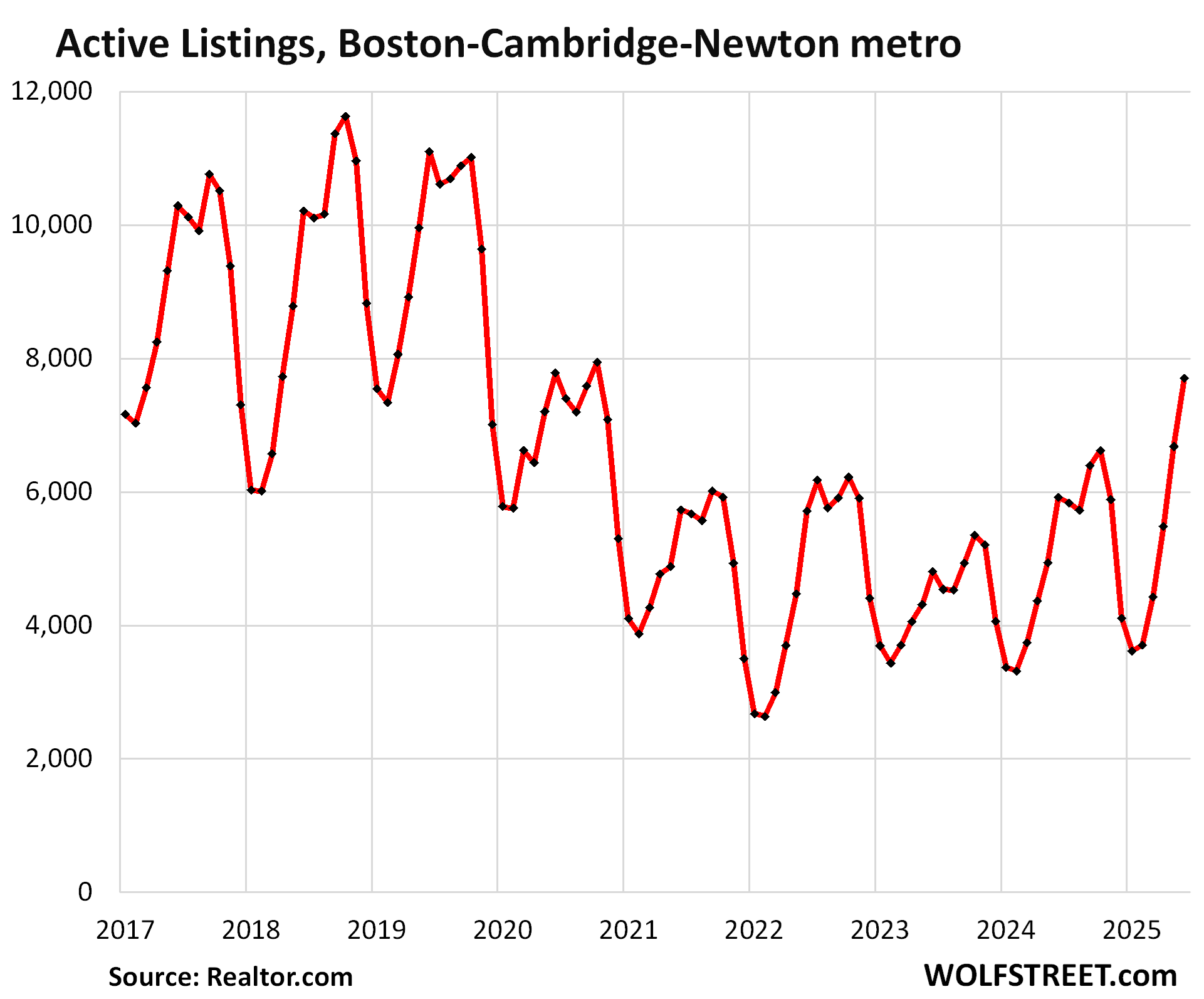

In the Boston-Cambridge-Newton, MA-NH metro, inventory jumped by 30% from June 2024 and by 60% from June 2023, to 7,705 homes, the most for any June since 2020, according to data from realtor.com

These are big increases, but off ultra-low levels. So inventory was still down by 31% from 2019 and by 24% from 2018.

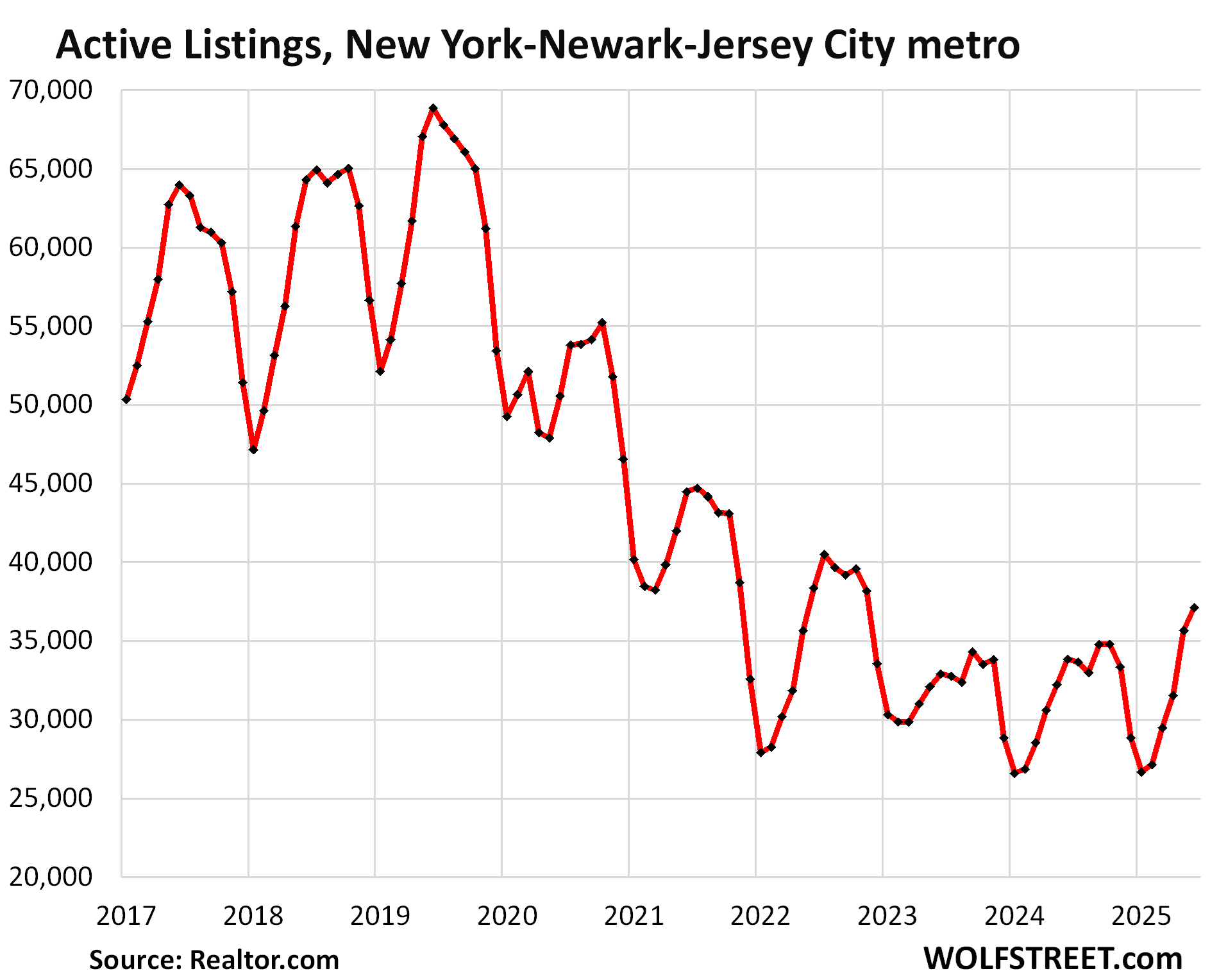

In the New York-Newark-Jersey City, NY-NJ metro, active listings rose by 9% from June 2024 and by 13% from June 2023 to 37,131 homes, the highest for June since 2022, according to data from realtor.com.

But those increases were on top of very low levels, and so listings in June were still down by 46% from June 2019 and 42% from June 2018.

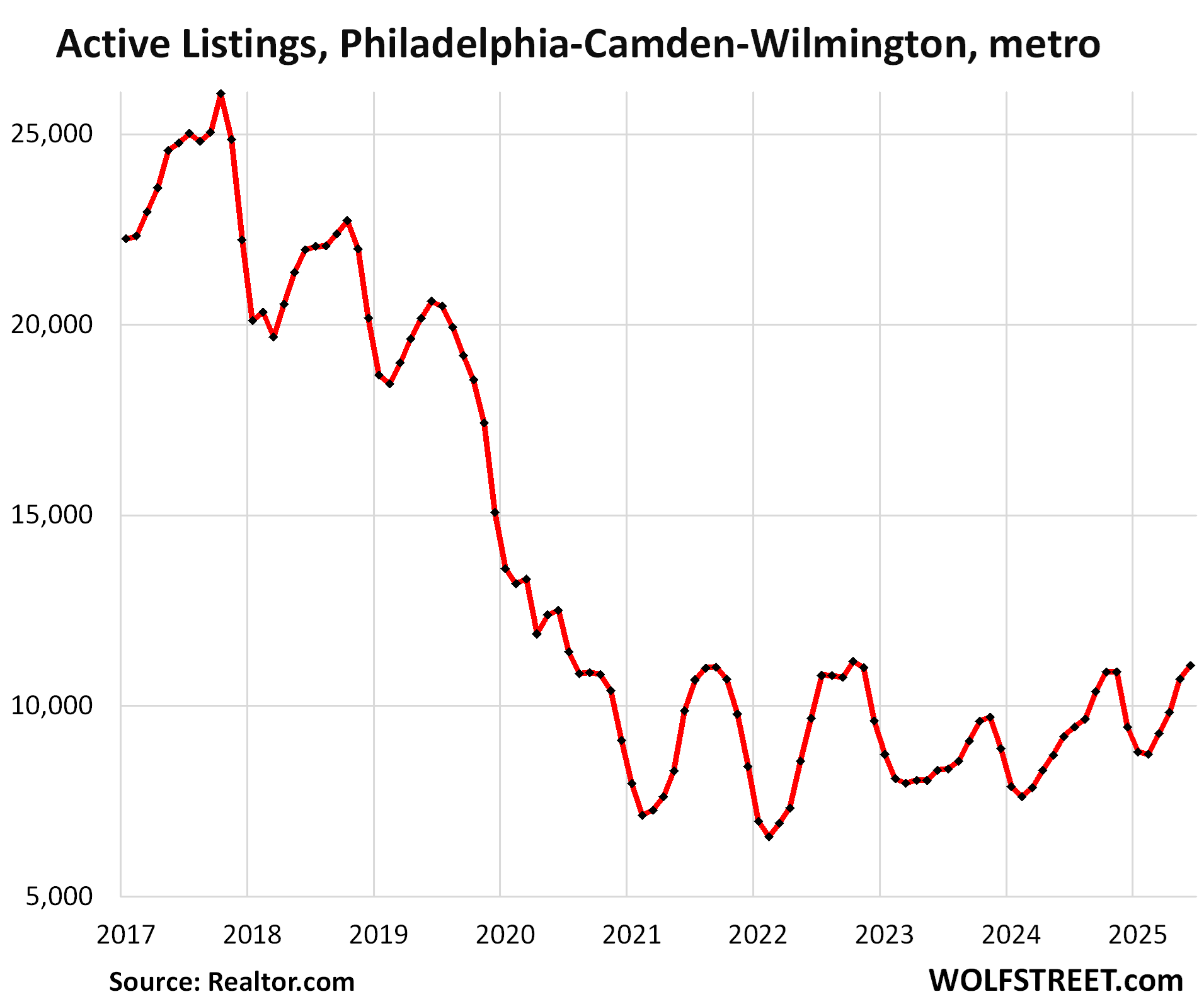

In the Philadelphia-Camden-Wilmington, PA-NJ-DE-MD metro, active listings jumped by 20% from June 2024 and by 33% from June 2023 to 11,057 homes, the most for any June since 2020.

But compared to June 2019, listings were still down by 46%, and compared to June 2018, by 50%.

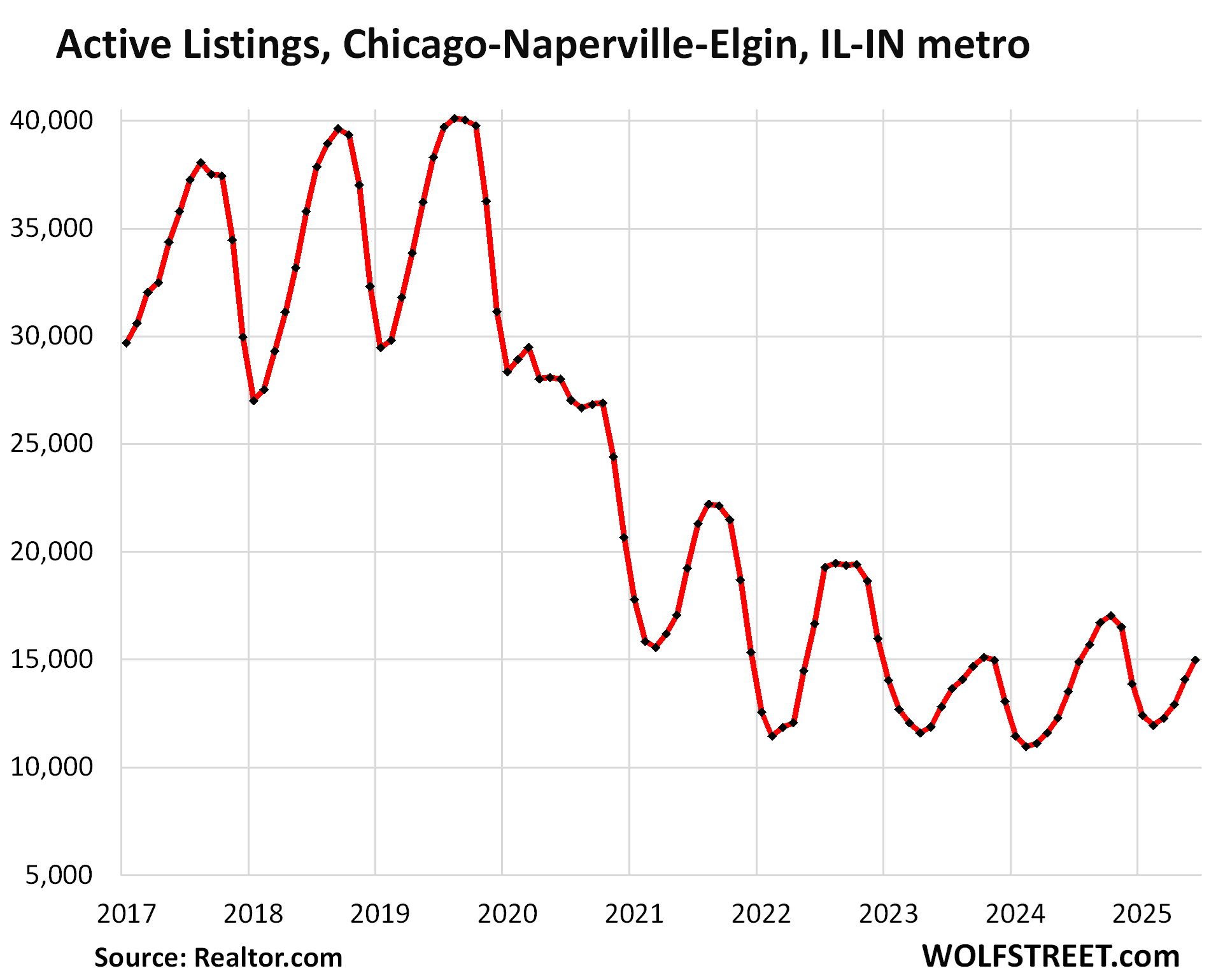

In the Chicago-Naperville-Elgin, IL-IN metro, active listings in June rose by 11% from a year ago and by 17% from two years ago, to 14,975 homes, the highest inventory for June since 2022, according to data from realtor.com.

But those increases came off ultra-low levels, and inventories are still very low, down by 61% from June 2019 and by 58% from June 2018.

The seasonal highs are roughly in September and October.

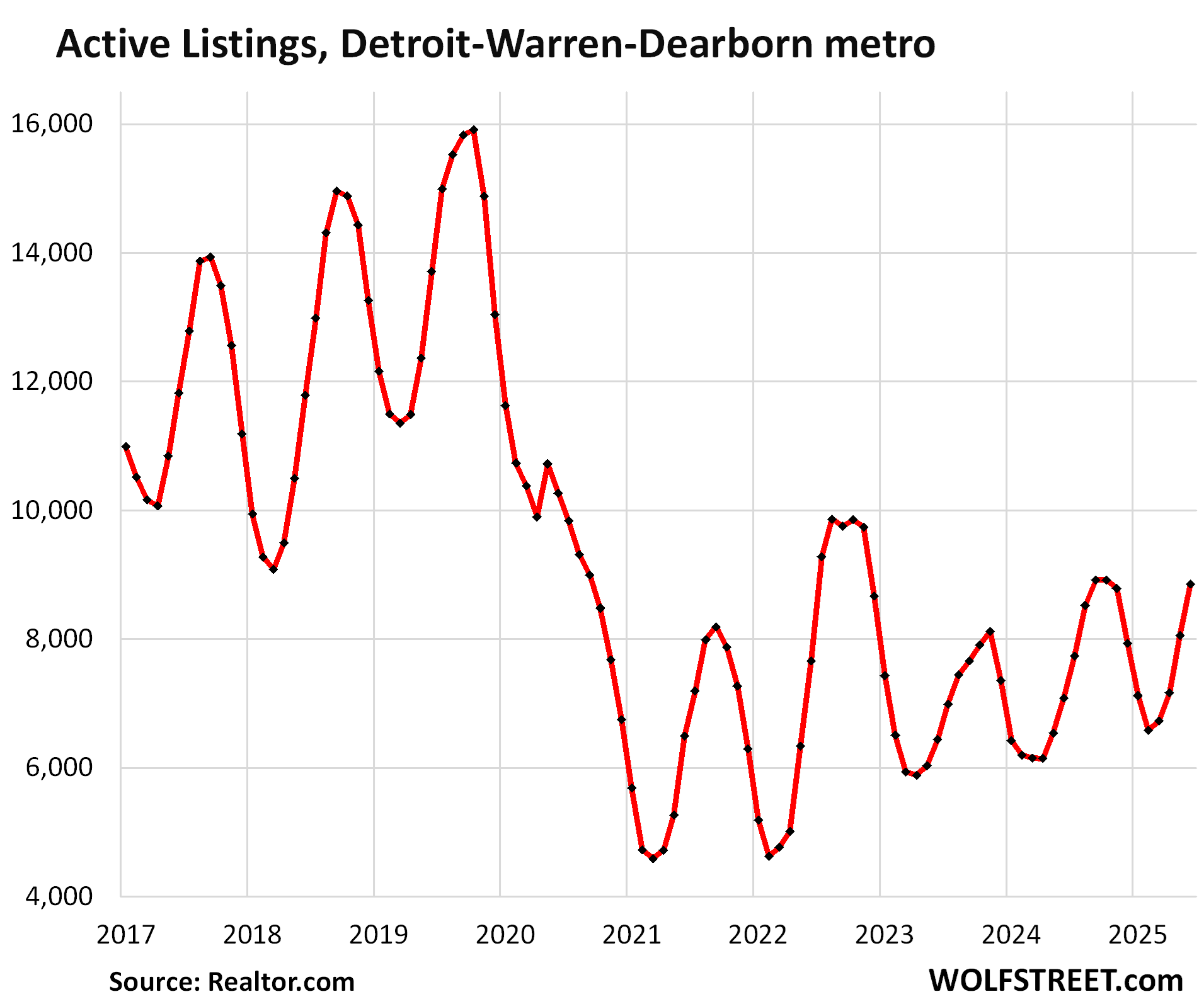

In the Detroit-Warren-Dearborn, MI metro, active listings in June jumped by 25% from June 2024, and by 37% from June 2023 to 8,859 homes, the highest for any June since 2020, according to data from realtor.com.

Compared to June 2019, inventories were still down by 35% and compared to June 2018 by 25%. The seasonal peaks are largely in September.

In case you missed it: The inventory situation in the big metros in Texas [Inventory of Homes for Sale Blows Out in Texas, Price Cuts Spike], the big metros in Florida [Homes for Sale in Florida’s Biggest Markets Rise to Highest in Many Years and Languish as Demand Fizzled], and the big metros in California [Inventories of Homes for Sale in Big California Markets Jump to Highest in Years, Days on the Market Soar, Demand Withered].

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m hoping that soon you will put out articles tracking the ZHVI for smaller metros such as Pittsburgh! Good info as always

I wonder what the SALT deduction increase will do? In my market (Boston), that plus the mortgage interest deduction give a pretty chunky reduction to the effective cost of a mortgage at the typical household incomes here. It’s still cheaper to rent, but the gap has narrowed a lot, particularly with rents continuing to increase.

Anecdotally, I don’t think it’ll do much. I haven’t heard anyone take the SALT deduction into account one way or another when making decisions like this.

The stragglers just need more time, to catch up to other places. There’s far more pessimism and uncertainty hovering on the horizon, and as that continues to grind away — more inventory will bubble to the surface, and prices will need to adjust downward (to thaw out frozen sales).

From Redfin a month ago, supporting that notion:

“16.4% of sellers who bought their homes after the pandemic are at risk of selling at a loss in today’s market, compared to 9% of those who bought during the pandemic and 1.8% of those who bought before the pandemic.”

MW: Housing market is sending a stark warning to the U.S. economy, Moody’s economist says

LOL! I think the great financial fraud of 2008/2009 showed us just how useful those eCONomists are.

It’s sad, many of the homes in my area end up being flips that look really nice but are very poor quality once you take a closer look (flooring that is not flat, gouges on the window glass, poor caulking, the cheapest materials, lowest quality appliances). Purchased a few months ago, then relisted for an extra 200-500k. I have also visited a few houses that were “remodeled” by the same person, because it had the exact same style!

@xilex flipping houses like buying and selling used cars is a LOT of work so there is always a tempation to hide flaws (eg drywall mud over rot or bondo over rust). Over the last 50 years I’ve seen honest people but they leave since it is a lot of work for a little profit. The people that stay in the business are mostly (but not all) the kind of people that can sell a home in the summer after stain killing and painting over water damage from roof leaks or sell a car to a single mom with 20 year old tires (and a 20% loan)..

With your post last week on rates climbing back to Jan level and the potential for higher rates should the Fed lower the prospect for housing prices and sales without large discounts indicates that the current new listings could be the smartest of the bunch. As you frequently remind us people sell and buy homes for a variety of reasons . Buyers will emerge with lower prices . A home has large carrying costs and many homes are not what I call rent friendly (too big or too expensive) in many markets .

New listings aren’t smart if they are listing as aspirational peak 2022 pricing. If they’re actually pricing them to sell, then they are.

Lay off over 100,000 Federal employees, and houses are gonna start popping up for sale in the greater DC area.

Wonder what was going in Philly to cause listing decline beginning in 2018, rather than pandemic?

For the first time in history, Federal workers are being fired left and right. Everyone knows someone who’s been fired. This place could suffer a real estate meltdown in the very near future, as the Supreme Court has given the go ahead to continue on with the purge. The chart above shows that the meltdown is just beginning. The firings are based on functions that are no longer needed, not employee performance. People are being fired without warning by e-mail. This has Musk’s fingerprints all over it. Musk did this over at Twitter. Even though he’s gone, his legacy lives on.

Oh no. Happens all the time in the private sector

I see this argument frequently, but I don’t understand the point. What is the point?

There were numerous RIFs (Reductions In Force) during the first years of the Reagan Administration, and plenty of buyouts during Al Gore’s government efficiency commission in the 90s. Mostly these are accomplished with attrition and sometimes early retirements. There are some controversial firings like with the Agency for International Development (AID), but it’s a longstanding joke on the taxpayers because people who get riffed or take buyouts come back and work as consultants, often at much higher rates.

Meanwhile, government spending from all sources… federal, state, and local, exceeds 50% of total GDP. I don’t know if that means we’ve crossed the line into socialism.

People are trapped in their houses for the most part with low interest rate mortgages. Yes some areas have too many houses for sale but it’s not true where I live in New Hampshire. Prices are high and are staying high. They’re not dropping. Washington DC is a special case with so many government jobs disappearing with thousands losing their positions. Some of those homes will go on the market.