By the time they finally wanted to sell their home, it wasn’t easy anymore because demand had plunged, and fewer of those mortgages got paid off.

By Wolf Richter for WOLF STREET.

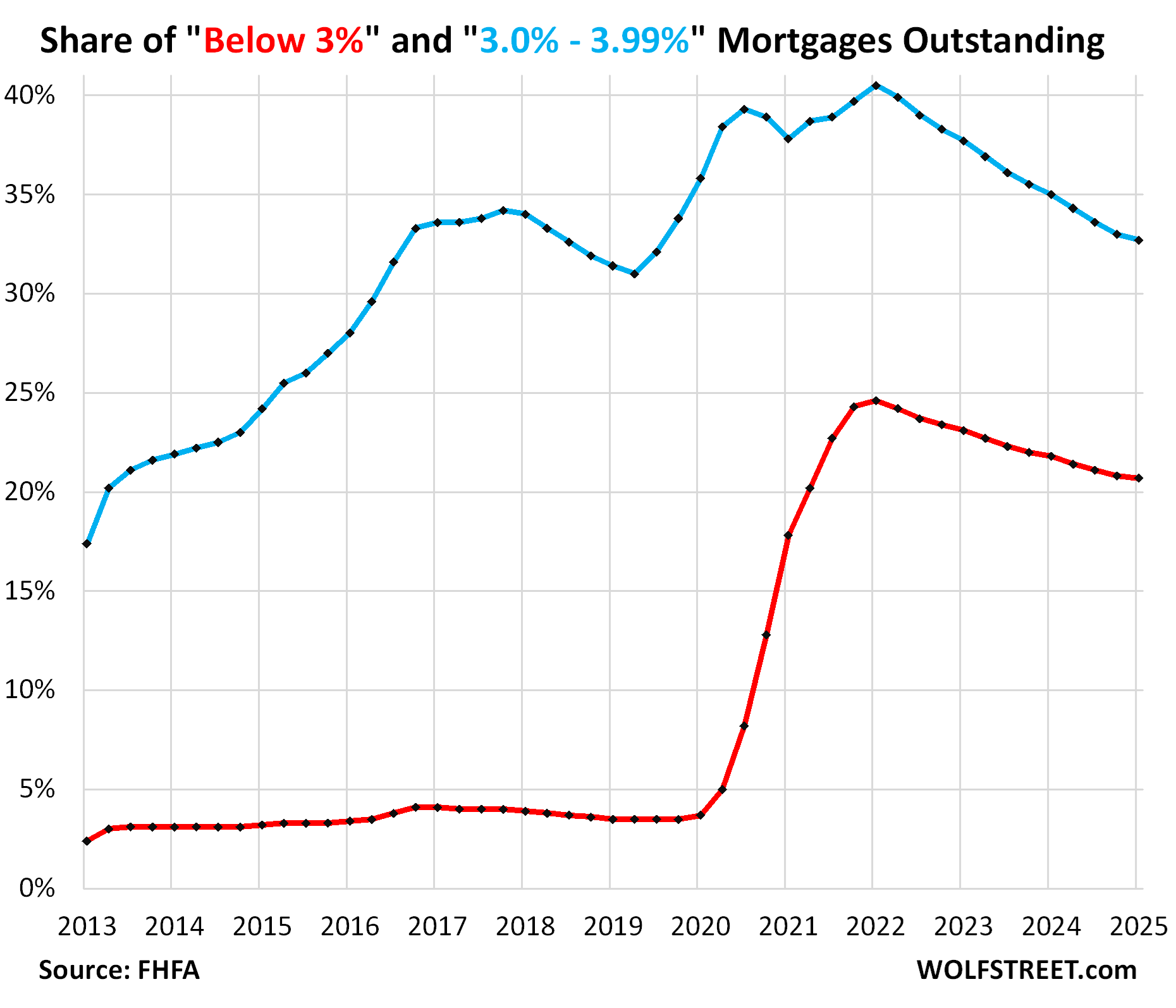

Mortgages outstanding with rates below 3% declined to a share of 20.7% of all mortgages in Q1, according to data today by the Federal Housing Finance Agency (FHFA). Their share started to decline in mid-2022. But the decline of just 10 basis points Q1 was the smallest since the declines started. Over these three years, the quarter-to-quarter declines of the share of these below-3% mortgages averaged just over 30 basis points, with a range between -20 to -50 basis points (red in the chart).

Similarly, the share of 3-4% mortgages declined by 30 basis points to a share of 32.7%. But the average quarter-to-quarter decline since mid-2022 was nearly 70 basis points, with a range from -50 to -90 basis points (blue). In the chart, the slowdown is visible in the flattening of the curves at the end.

The declining share of these ultra-low-rate mortgages represents the exit of homeowners from the “lock-in effect.” This slowdown in the rates of decline – the slowdown of this exit – is not what the real estate brokers and mortgage lenders were hoping for. But it’s not that locked-in homeowners didn’t want to sell – on the contrary, supply has ballooned as they put their homes on the market. It’s that demand has plunged further in Q1, even below the beaten-down levels from a year earlier, and a lot of them couldn’t sell, and so fewer of these mortgages got paid off.

When these low mortgage rates came along in early 2020, they triggered a tsunami of refinancing of higher-rate mortgages, and the number of these outstanding low-rate mortgages exploded through Q1 2022.

The lock-in effect is where homeowners refuse to move because they would have to sell their home and pay off the mortgage, and finance the next home at a much higher mortgage rate. This lock-in effect is in part responsible for the roughly 40% collapse in demand for mortgages compared to 2019, and for the plunge in sales of existing homes – by 23% from 2019 for single-family homes and by 38% for condos.

But even the closest thing to free money that Americans could borrow has slowly been getting paid off because homeowners moved to take a new job or accommodate a larger family, or got divorced, or died.

Or they’d already bought a new home a few years ago and moved into it, but kept the old home to ride up the home-price explosion all the way. And now the carrying costs of that vacant home are becoming a burden, and prices are no longer exploding; but instead in some markets, there are downdrafts in single-family home prices, and in more markets, there are serious downdrafts in condo prices. And so they put these vacant homes on the market, and pay off the mortgage if they sell the home.

The hope of brokers and mortgage lenders was that the lock-in effect would loosen up, and that more of these locked-in homeowners would return to the market as buyers and sellers and generate commissions, fees, and points coming and going.

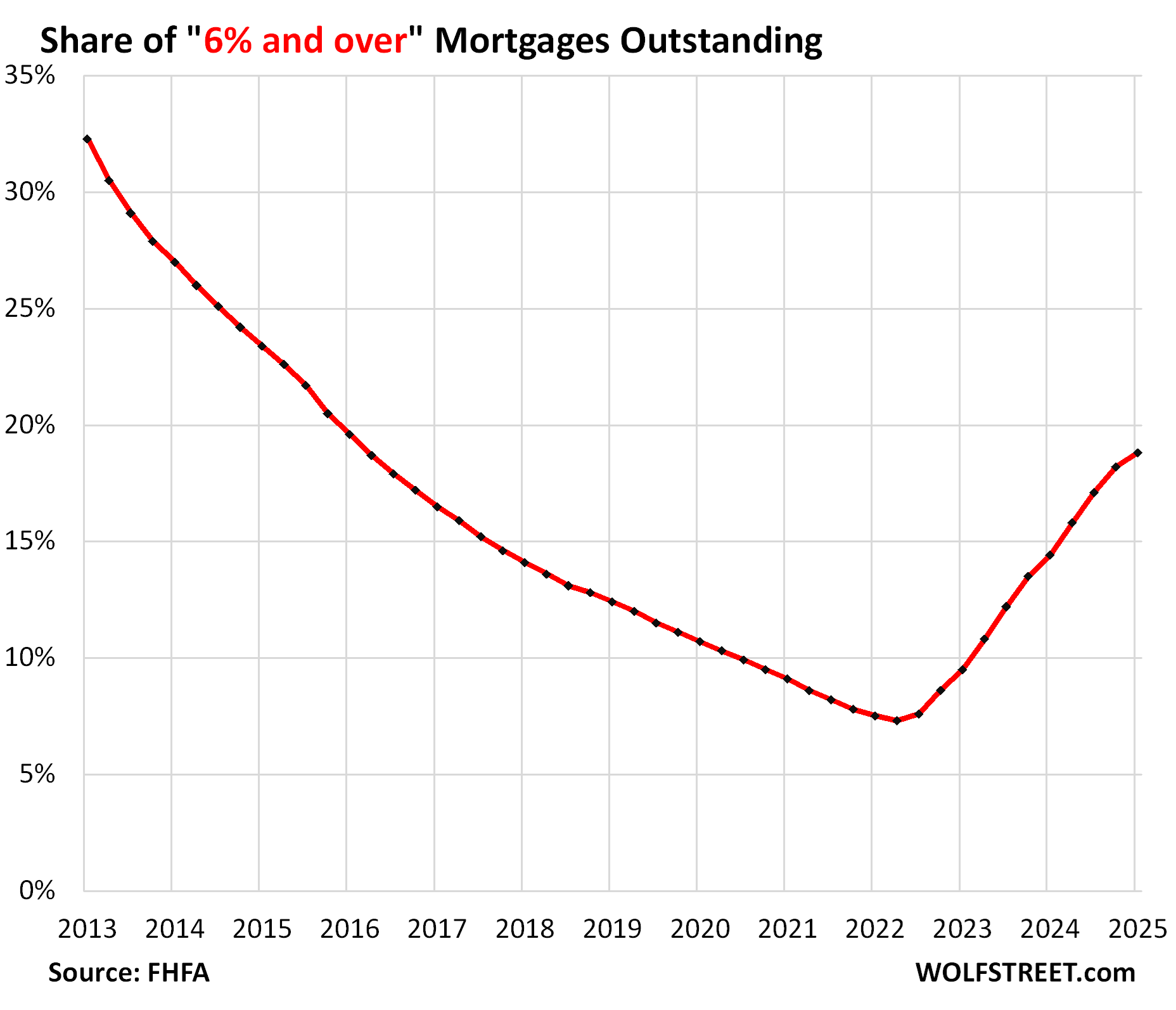

The share of 6%-plus mortgages rose by 60 basis points to a share of 18.8% in Q1, the highest since Q1 2016. Their share has multiplied by over 2.5, from 7.3% at the low point in Q2 2022.

But that 60-basis point increase in the share was the slowest increase since increases took off in mid-2022. Between Q3 2022 and Q4 2024, the increases averaged nearly 120 basis points per quarter, with a range from +90 to +140 basis points.

The ultra-low-rate mortgages were a brief phenomenon.

The below-3% mortgage rates burst on the housing scene from mid-2020 to October 2021, as a result of the Fed’s massive pandemic QE that included purchases of trillions of dollars of mortgage-backed securities.

Even the 3-4% mortgages were a relatively brief phenomenon that came and went several times since late 2011 as a result of the Fed’s Financial Crisis-era QE.

Even the 4-5% mortgages did not exist before the Fed’s Financial Crisis QE at the beginning of 2009.

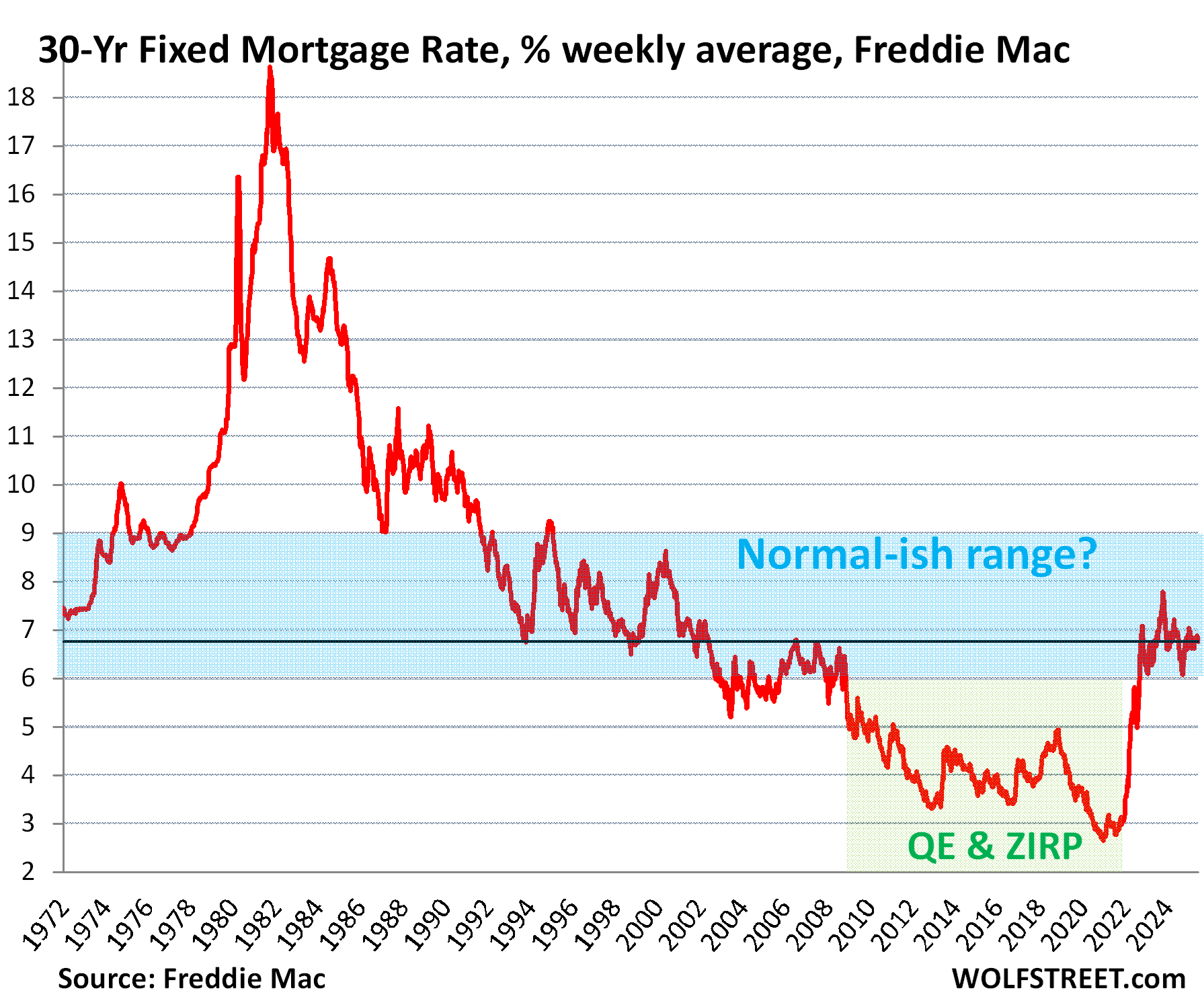

For a few years in the early 2000s, mortgage rates were in the 6% range – so low that they created the Housing Bubble that later imploded, and the resulting mortgage bust helped trigger the Financial Crisis that threatened to take down the entire US financial system.

In the decades before then, mortgage rates were at around 7% and higher, which is roughly where they’ve also been over the past three years.

Unfortunately, the data from the FHFA on the share of mortgages by mortgage rates goes back to only 2013, and therefore only reflects the era when QE had already repressed mortgage rates.

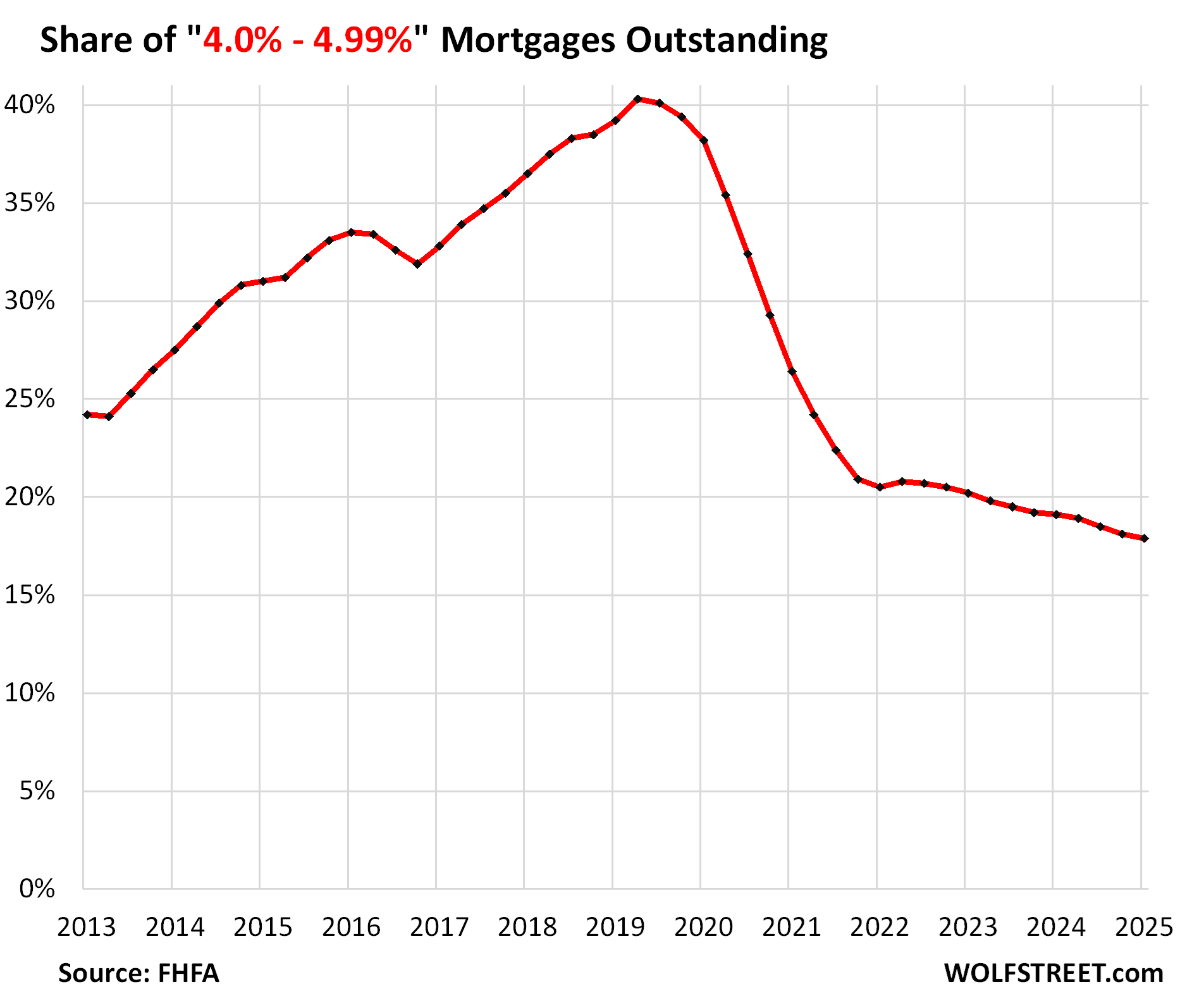

The share of 4-5% mortgages dipped by 20 basis points to 17.9% in Q1. That share is the lowest in the FHFA’s data going back to 2013.

Some of these mortgages were refinanced into lower-rate mortgages when mortgage rates began to drop in 2019. Then in Q2 2020 through Q1 2022, the tsunami of refinancing caused their share to get cut in half, and their share has since then declined further.

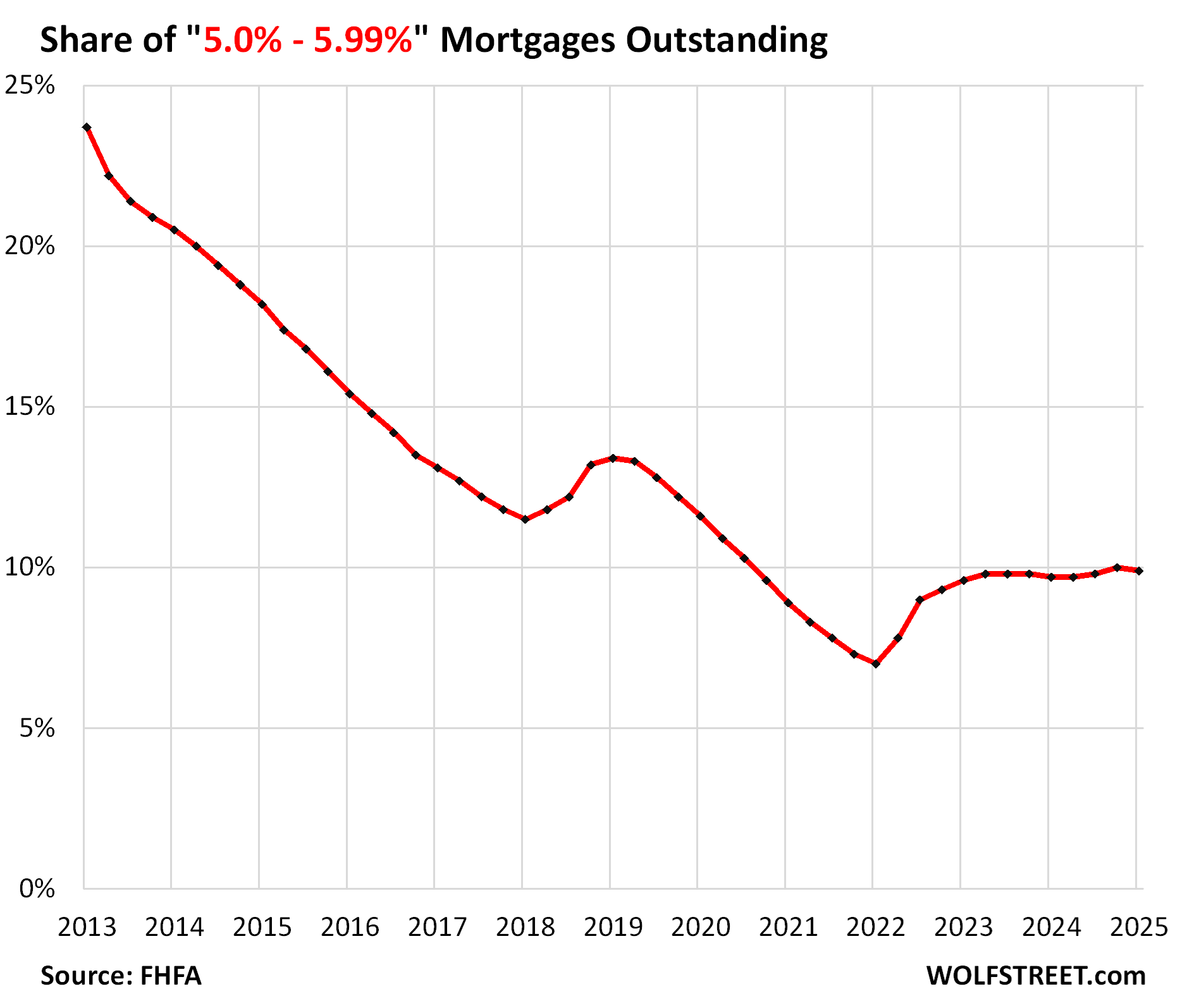

The share of 5-6% mortgages has remained roughly stable over the past two years, mostly just under the 10%-line. In Q1, the share dipped to 9.9% of mortgages outstanding.

There are fixed-rate mortgages offered in this range. For example, the interest rate of the average conforming 15-year mortgage fell below 6% in February and has largely remained below 6%.

The long decline of the share of these 5-6% mortgages during the QE era to bottom out in Q1 2022 at 7.0% was interrupted only by the Fed’s QT and rate hikes in 2018, when mortgage rates rose, and the average 30-year fixed mortgage rate briefly hit 5% in November 2018. But in 2019, mortgage rates declined again amid the Fed’s rate cuts and end of QT.

The lock-in effect has depressed demand for homes, and real estate brokers, mortgage lenders, and mortgage brokers have gotten hit hard by this plunge in demand and shed a large portion of their employment to deal with it (I discussed the effects here: Housing Bubble & Bust #1 and #2 as Seen through Employment at Mortgage Lenders: They Shed Jobs Again, 38% Gone).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

They always miss their exit. I love it. Better luck next bubble.

The way and speed we blow up the last bust to current bubble, wouldn’t doubt it the next one if this one EVER pop will re-accelerate even faster and bigger, maybe down to 1-2 year just like the Covid peak from bottom to top.

Unless there’s a generational narrative and mindset shift for the general public that housing is not a fool proof great return investment, people will buy into it another bubble again and again, especially if government have an incentive and benefit from high housing price such as tax revenue, wealth affect…etc

Oh no….seems like another one of RE and some of the house humpers talking point is slowly getting chip away. First it’s the generational lack of supply so price will stay high forever or the rate is temporarily high now but wait for that rate cut back to 2% so price will only go up, add the never ending “lock in” effect narrative so no one will ever reduce price to sell their place therefore price and market will never go through a painful correction and RE can go only up. Many cracks are forming now, what other talking points do they have left to justify that this is not a bubble…I am sure we can find something on /REbubblejerk

If anything there is a vast oversupply of real estate in the US as opposed to the opposite. Current owners are simply not at all interested in dropping their asking prices to sell their property prices which makes more real estate supply available every day.

Realtors and most economists deny it, but this housing downturn will make the last one look like a day at Disneyland. It’s going to be absolutely devastating.

What if you consider a day at Disneyland devastating?

The Fed is a serial asset blower…central banks have been doing this for 300 years…the trump, Powell theater is like people think we have a 2 party system… housing is now unaffordable for young people across the board, student loans like old mortgages…it’s a plutocracy of thieves and grifters… with a printing press…

I will occasionally post this housing documentary unless Wolf asks me to stop. Two parties, one giant wall st. grift.

It is a lesson in how homes were turned into financial instruments.

TheCon dot TV

Since 1725??

hold my powdered wig sir!

Yup.

It was all intentional and robbed an entire generation of a normal life. Most 30 and under live with the expectation that they will never own a home.

We might as well all live in a 3rd world country if only the rich can buy a house.

Right this minute, I can purchase a fixer upper near the ocean in Florida in a popular city for 120K. You might not get the house you want, as we didn’t. But not getting any house is a failure if imagination.

Correction. It’s 115K.

And there’s another fixer upper on the water in MA for 129, 30 min from a popular city. And another one not a fixer upper in a decent part of Colorado for 199. Several that aren’t fixer uppers in a popular beachside city in Florida for 200-250K. I mean WTH. So looking at houses that are not starter homes and maybe you’ll get somewhere. Heck, you can buy a used travel trailer and park it on the land of a major fixer upper, which is exactly what we did with plenty of money in the bank for our NY cabin in the woods a couple of years ago. WTH. It’s not that hard. This mindset is actually a function of being spoiled by the best things in life including the best houses. They are not the only option.

Are you trying to say good deals can be found on housing and prices haven’t been inflated to unreasonable levels, or what exactly? Yes there is a tent for sale and a camper for sale and a box for sale somewhere, for cheap, but the reality is on average….. an average home in an average place is way more unaffordable than before, for an average person. Hence the supply buildup.

@Gazillion In 1980 when I started college the minimim wage at McDonalds in CA was $3.10/hr (I was making $3.10 + tips valet parking) and my rent was $385/monrh (124x min wage) for a 2br (I paid half). Today the mimimium wage in CA at McDonalds is $20/hr and rent for a similar 2br apartment in Sacramento is $2K/100x minimum wage. I do not want to complain about the thieves and grifters that get kids to borrow over $100K for worthless degrees at fancy private schools but in the early 80’s tuition per semester at a CA State College was 124x minumum wage and today it is just up to 176x mimum wage (so the cost of college and housing combined is just about the same compared to minimum wage as it was 40 years ago – back when every college student didn’t have a cell phone, cable tv or order food to be delivered ecept for a pizza using coupons).

What do you think the upcoming SLR changes will have on mortgage rates? From what I understand it will create 7 trillion dollars in demand for treasuries to hold long-term rates down which would essentially keep real estate inflated?

Yes it creates $7T OF ROOM ON BANK BALANCE SHEETS, but banks have no business owning long treasury securities.

“create 7 trillion dollars in demand for treasuries”

🤣❤️ you had way too much 🍺🍺🍺🍺🍺

it might not create much of any demand for Treasuries. Banks can make more money with zero risk by keeping their cash in their reserve accounts at the Fed, which is risk-free and instantly liquid and currently pays 4.40%.

But as Countrybanker said, it will create some room on bank balance sheets so that they can make more loans, such as C&I loans, which would be a good thing. And banks would make a lot more money on those.

I have to laugh. There are no adults left in the room, watching the economic decisions made with lamentable consequences.

20% increase in the price of gold in just less than six months. This is ugly. So, your house is now worth 20% less than it was on January 20- LoL, and everyone is now complaining about houses? Didja miss the rest of the disaster?

And we just took vacation properties out to be shot, just imagine how many people are going to come to LA for the Olympics. And everyone keeps thinking it is just going to be business as usual.

Nope. This is the new new. And it sure isn’t what we have been used to. It isn’t panic, if you go first and are right.

So many pieces are breaking, and we are not fixing anything, instead our government is intent on breaking everything.

But patience, we still have more to break. As Wolf keeps talking about, at least the Fed is still functioning. For now.

I am starting to become very pessimistic, and we still have a lot of trade stuff to solve.

Wait for Trump’s sycophant fed chief to lower rates to zero and then watch the fireworks start!

Jerome Powell is Chairman of the FOMC (Federal Open Market Committee) which makes all Federal Reserve interest rate policy decisions. The Federal Reserve FOMC is not a one-man show but rather a committee comprised of the 7 Federal Reserve Board of Governors members and 5 of the 12 Federal Reserve regional banks. Trump apparently does not comprehend any of this at all.

…semantics and self-view. Someone sees their office as ‘ruling’ in place of its former status as ‘administrating’. Many of the now-‘ruled’ are having great difficulty in adapting their own semantic views of the separation of powers to this major fork in the road…

may we all find a better day.

Well said.

See how it works is…

The stock market fell, so people pulled money out of there and made a ‘flight to safety’, ala went to gold or Bitcoin (lunacy).

now that the stock market is hot again (minus the 10% drop in dollar value thanks to the new policies), people may jump back in.

Then some bad news may melt the stock market again.

Then back to gold!

What pushes up the price is more investors in the finite amount of investment. Meanwhile Bitcoin is like 1000 people trapped in a miserable room, 5 begging to get out and promising you “it’s great in here! Give me $5k and I’ll give you my seat” nevermind the room is on the titanic

Bitcoiner here. Even if you give me 250k now, you won’t get my coin!

I guess elections have consequences. Unfortunately we elected a vengeful nitwit and he surrounded himself with a merry band of thieving scumbags.

Yeah most recently I’ve been watching the Hispanic leaders down in Miami saying “we were deceived and used.” Used, yes. Deceived, hell no. Trump and the GOP were very clear about all of their intentions. Anyone not happy who voted for him has only themselves to blame. For the rest of us, it’s a damn shame.

Easy fix Wolfman as far as +7% mortgage rate, just adjust lending standards to allow up to 53% of household income to pay for the mortgage.

That will loosen up the market and help to spur more sales.

Realtors should think about changing careers. Nothing is going to change. The only thing that will bring down interest rates, make homes more affordable, and create more churn in the market to boost their commissions is a major depression or repeat of the GFC of 2008/2009. That’s not going to happen any time soon.

How would falling prices boost any realtor’s commission?

Because sales would start happening.

Plenty of realtors made money selling for closures in 10,11,12, etc. because stuff was selling.

There are untold forces at play in the housing market, a few very significant (e.g., mortgage rates), but others less so but still impactful.

Take building costs (materials and labor): A steep rise from the recent inflationary impulse. Sure, starter houses will still get built (even more cheaply) as well as super high end stuff where money is no object.

But where I live, building lots bought in anticipation of building that $1M++ dream house are sitting dead in the water, and will probably never be built on unless sold to someone with very deep pockets or the lot/land discounted significantly.

How does this affect existing house values? It is a subtle force that helps hold up existing house prices in some markets.

Again, just one of many forces out there on real estate prices.

There are plenty of homes available at very low prices, 20k. They are called tiny houses. Granted, if you want to keep up with the Jones 2000 + SQ ft home you will have to pay up.

Not with land at that price. And a house without land is pretty useless.

Lots of them: RV’s, mobile homes!

And there are lots of RV/mobile home parks where people live full time. There’s one about 5 miles from me and it has hundreds of units.

Powell came out saying that they likely would have lowered rates if not for Trump’s tariffs. What a degenerate. They didn’t lower rates because they don’t want the long-term bond market to blow out as a result of entrenched services inflation.

Why is this guy lying?

What is in any way wrong about Jerome Powell, Chairman of the Federal Reserve, in saying that the 12 member FOMC sees inflationary issues present and at work in the US economy?

Just about EVERYONE, outside of us here and a few other hardy souls, thought that tariffs would massively jack up inflation. Remember the clickbait BS in the media and social media and in the comments here about prices of cars gonna jump 20% in three days, etc. That was the doctrine spread far and wide, and this site got attacked like never before by this tsunami of BS. To get control over it, I ended up having to close the comments on one article entirely.

So that predicted explosion of prices didn’t happen.

But the effects of tariffs on inflation are unpredictable. We can look back at the 2018/2019 inflation data (Trump 1 tariffs), and there wasn’t any kind of major increase of inflation of durable goods. And I pointed that out. But that was then, and this is now, and the tariffs could still push up inflation.

But the big “known unknown” is this: if companies see they have pricing power again, they will jack up prices on services, which are un-tariffed and dominate consumer spending and inflation. Companies discovering they once again have pricing power is VERY inflationary because they will use it, as we have seen.

And that’s what Powell and the others are worried about. And they have said so. And they have said they didn’t expect this to happen very quickly because the discovery of pricing power is a process that takes time. Companies are careful with it because if they think they have pricing power and jack up their prices, and then they lose sales and market share and get crushed because they raised prices, well that’s a very costly gamble. All this stuff is very uncertain.

And if the bond market sees that inflation is blowing out again, and that the Fed is lackadaisical about it, long-term yields would just go WOOOSH.

…seems ‘charging what the market will bear’ is an eternal verity (…and game of ‘Blind Man’s Bluff’? Thanks, as always Wolf, for your tireless(?) efforts to lift the veil as much as possible…)…

may we all find a better day.

I sold my place three years ago — and had a beautiful mortgage payment of $360!

It was hard walking away from that, but have no regrets. I hate the rent I pay —- but, would hate to be in a position today, to sell or buy.

I’m sure somewhere out there, honest, qualified realtors exist, but as the inventory glut explodes further, the dynamic of market transitions will increasingly be stressful — especially with more unqualified AI-themed experts and absolutely stupid situation.

These locked-in positions are like timebombs, perhaps somewhat similar to SVB — what once seemed like a good thing, is a huge liquidity disaster going forward.

I’m sure tons of well healed baby boomers can sit around waiting for the mkts to go up, but, as in my case, my gain on selling my house far outweighs a cheap mortgage. It’s crystal clear, that my cash is growing faster than the value of my old house.

This lock-in dynamic will eventually be an important part of the Great Flood of 2026. Get in the ark while there’s time!

“I’m sure tons of well healed baby boomers can sit around waiting for the mkts to go up, but, as in my case, my gain on selling my house far outweighs a cheap mortgage. It’s crystal clear, that my cash is growing faster than the value of my old house”

You might be right..out of pure stubbornness and entitlement they might just hang on to it until they expire as long as they have enough money to survive day to day. Seen couple of examples of friends parents ended up being put into retirement home and still refuse to sell and left it to the kids to deal with the aftermath after they passed. Even though they could’ve sold years before sunset and set themselves up with a nice nestegg .. All because they think their house is worth even more down the road.

Red – no doubt true for many well-‘healed’ Boomers, but in this one’s case, several of a lifetime’s inevitable wounds have yet to scab over and scar.

e pluribus unum?/”Eight Million Stories in the Naked City”

may we all find a better day.

@Wolf when you wrote: “Or they’d already bought a new home a few years ago and moved into it, but kept the old home to ride up the home-price explosion all the way. And now the carrying costs of that vacant home are becoming a burden” it reminded me to ask if you have ever seen anything that estimates the percantage of empty homes owned by people who want to “ride up the home-price explosion”? I know it happens, but I would guess it is a tiny percentage since most (almost all) the people who are hoping to get more money selling a home in the future at a higher price will also want to get more money by renting the home (rather than have negative cash flow every month).

Let us do the maths, which is considered haaard. There are 59 million people who are over 65 today. Most of them are between 65 and 75 years old- with an estimated 40 million today. 19 million are older than 75. Of these, 75% are homeowners. So these people own at least 45 million homes. Given mortality tables, after 75 years old, the annual decrease in population is just under 5% per year. So, the leading edge of boomer has entered the permanent downsizing period. That means, after 75, the shrinkage of the population is roughly 5% per year, so this means nearly one million persons older than 75 are going to be passing per year, plus two percent of the 65-75 cohort, roughly another million per year- so, that will yield about 1.5 million houses per year coming on the market or being held by heirs.

Now, given some will be retained by surviving spouses or held by heirs, one can reasonably see 1 million homes coming on market. By the way, this is nearly double the year 2000 numbers in terms of elderly and homes. And totally ignores second homes, etc. Now, this is the truth boomers currently comprise 33 million households, but will shrink by 10 million households by 2035.

These numbers are pretty much set in stone, and we all will live with this backdrop for decades. There are more old folks in America than anytime in our past history, and they will be far more influential than the silent generation on aging in America.

We have no history for this, so in we go. The boomers have always been special, so their exit will be the same.

Now, the biggest transfer of real estate in history is going to start, and everyone thinks it will just be business as usual? How? There are literally not enough younger workers to buy all these houses at these prices, so either price or wages will adjust to make a market.

I would also suggest anything else the boomers have is going to suffer the same fate.

Someday this war’s gonna end…demographic edition.