US year-over-year home-price gain shrinks to +0.4%. Prices drop YoY in 18 of the 33 metros: San Diego, Austin, Tampa, Miami, San Francisco, San Antonio, Dallas, Phoenix, Orlando, Atlanta, Denver, Raleigh, Houston, Seattle… YoY gains nearly vanish in Los Angeles, San Jose, Charlotte, shrink in Boston, Chicago, New York, Columbus…

By Wolf Richter for WOLF STREET.

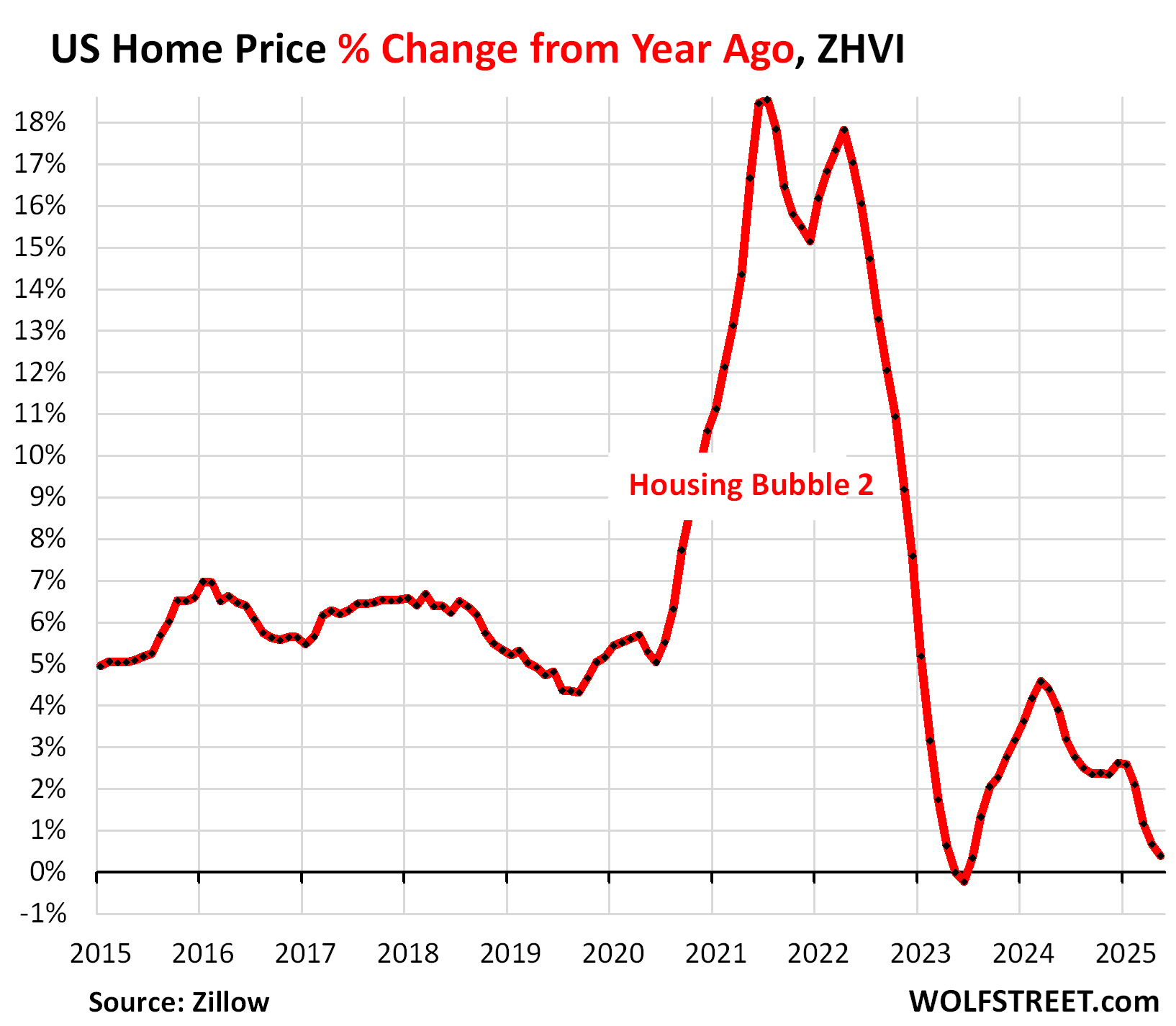

Prices of mid-tier single-family homes, condos, and co-ops in the US whittled down their year-over-year gains further, to just +0.4% in May.

The “spring selling season” is normally when not-seasonally-adjusted US home prices rise on a month-to-month basis, after the declines in the winter, and in aggregate, they did so this spring, but less than normally: In May, they ticked up just 0.6% from April, compared to +0.8% in May 2024, +1.3% in May 2023, +2.0% in May 2022, and +2.6% in May 2021. A similar pattern of below-normal price increases played out in prior months.

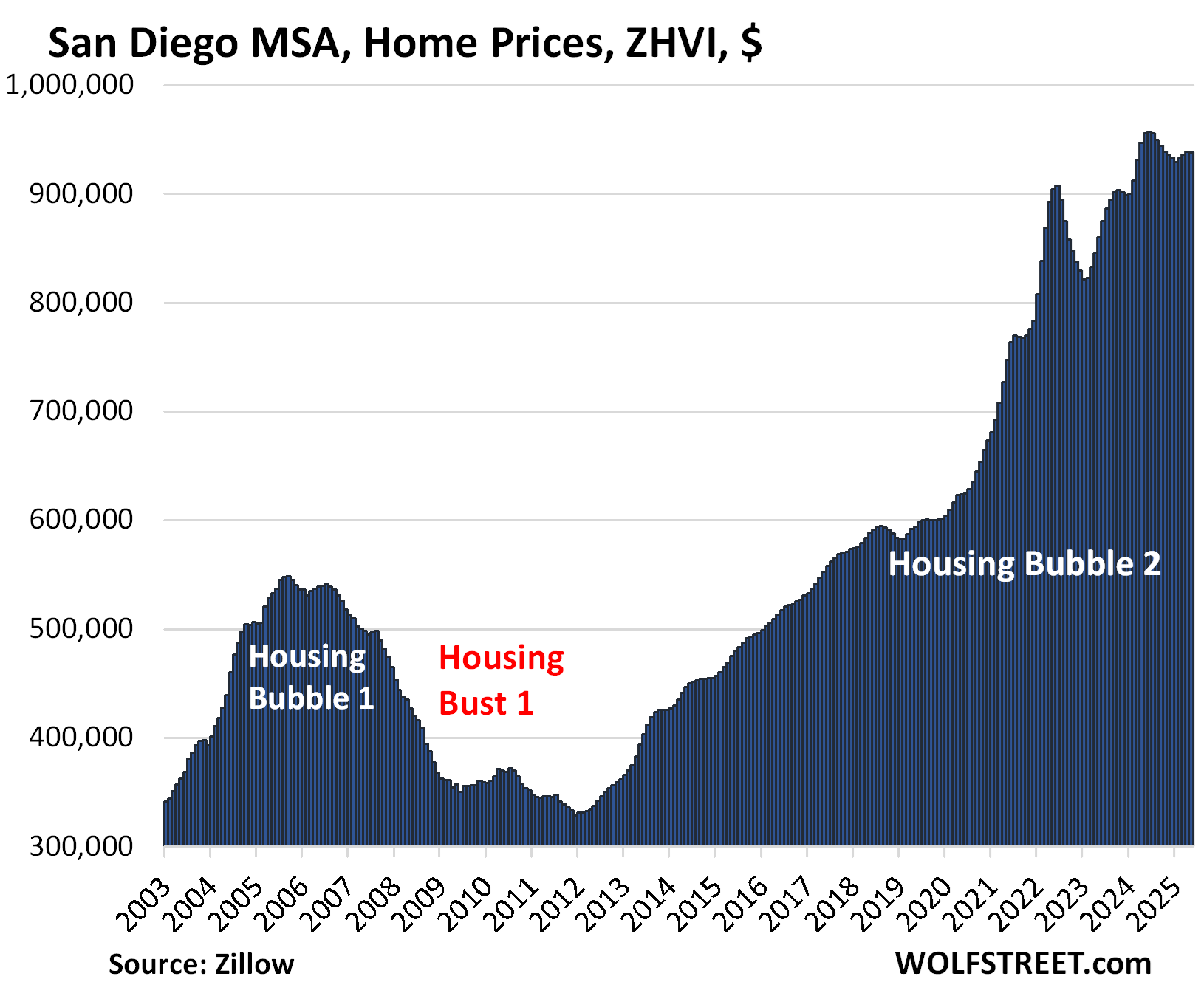

In terms of the large expensive 33 Metropolitan Statistical Areas (MSAs) that we track here, 18 showed year-over-year price declines in May, up from 6 at the end of 2024, and those year-over-year price declines worsened from prior months. Even in San Diego, the year-over-year decline worsened to -1.9% in May, from -0.9% in April, as prices dipped month-to-month while inventory ballooned because demand has withered.

All data here is from the “raw” not seasonally adjusted mid-tier Zillow Home Value Index (ZHVI), released today. The ZHVI is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals. Zillow’s Database of All Homes also has sales-pairs data.

To qualify for this list, the MSA must be one of the largest by population and must have had a ZHVI of at least $300,000 at some point.

Some metros that are large enough don’t qualify for this list because their ZHVI has never reached $300,000, despite the massive surge of home prices in recent years, such as the metros of New Orleans, Oklahoma City, Tulsa, Cincinnati, and Pittsburgh.

The growing list of year-over-year price declines.

In May, the list of year-over-year decliners got a new member, Seattle. In total, of the 33 MSAs here, 18 show year-over-year declines, up from 6 at the end of 2024. In all of those 18 metros, the year-over-year declines worsened.

Year-over-year declines in May:

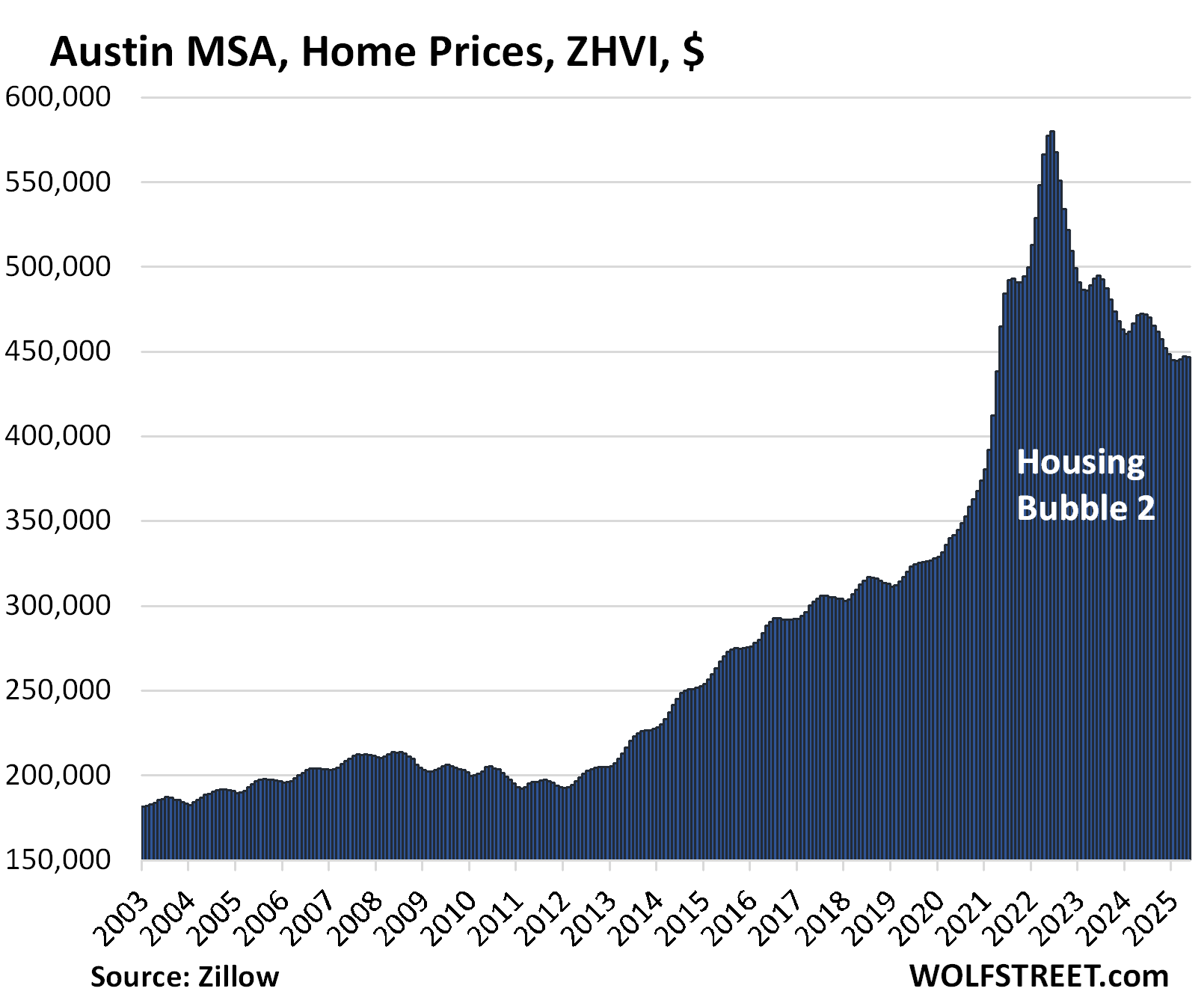

- Austin: -5.5%

- Tampa: -5.5%

- Dallas: -3.4%

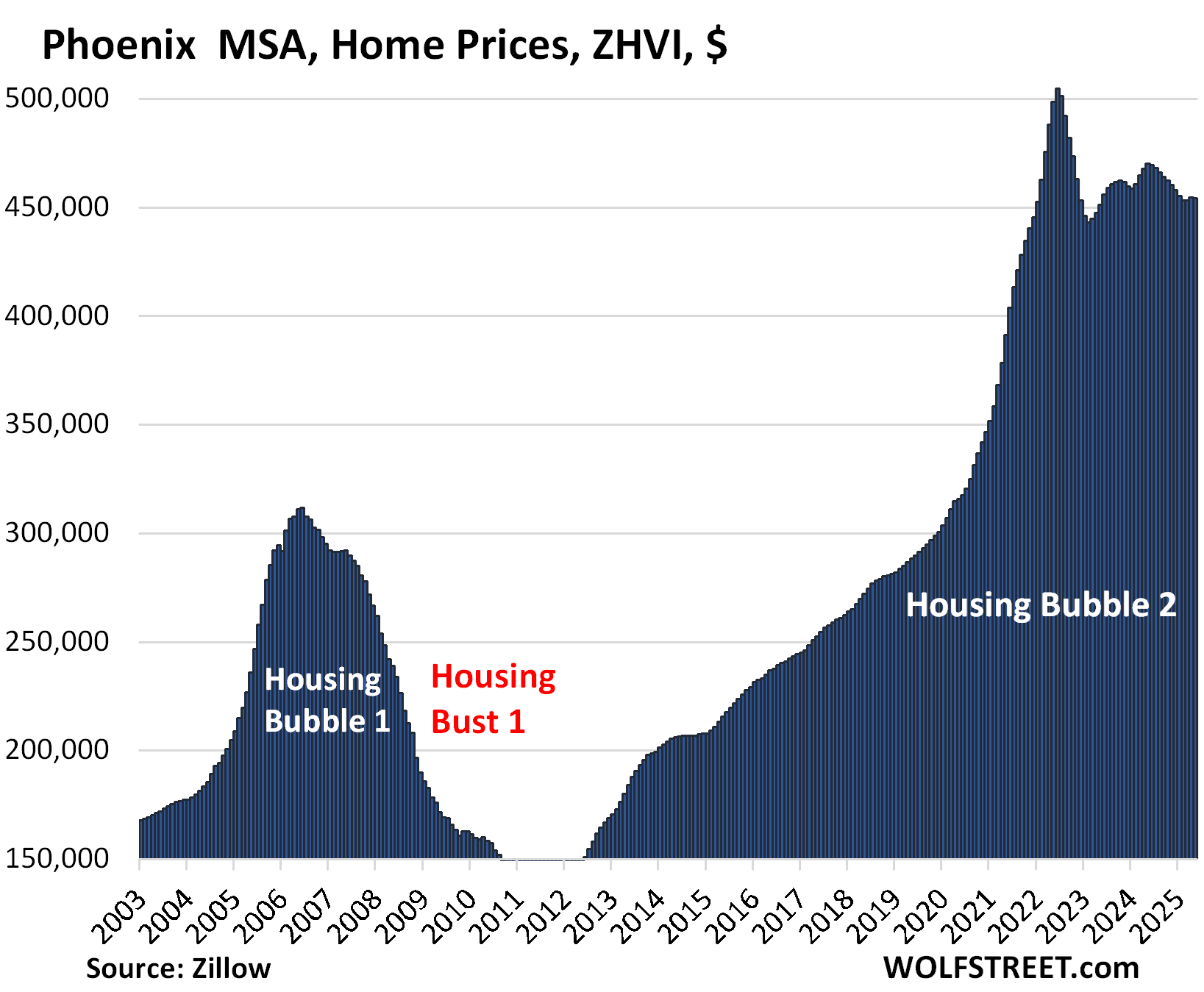

- Phoenix: -3.4%

- San Antonio: -3.3%

- Orlando: -3.2%

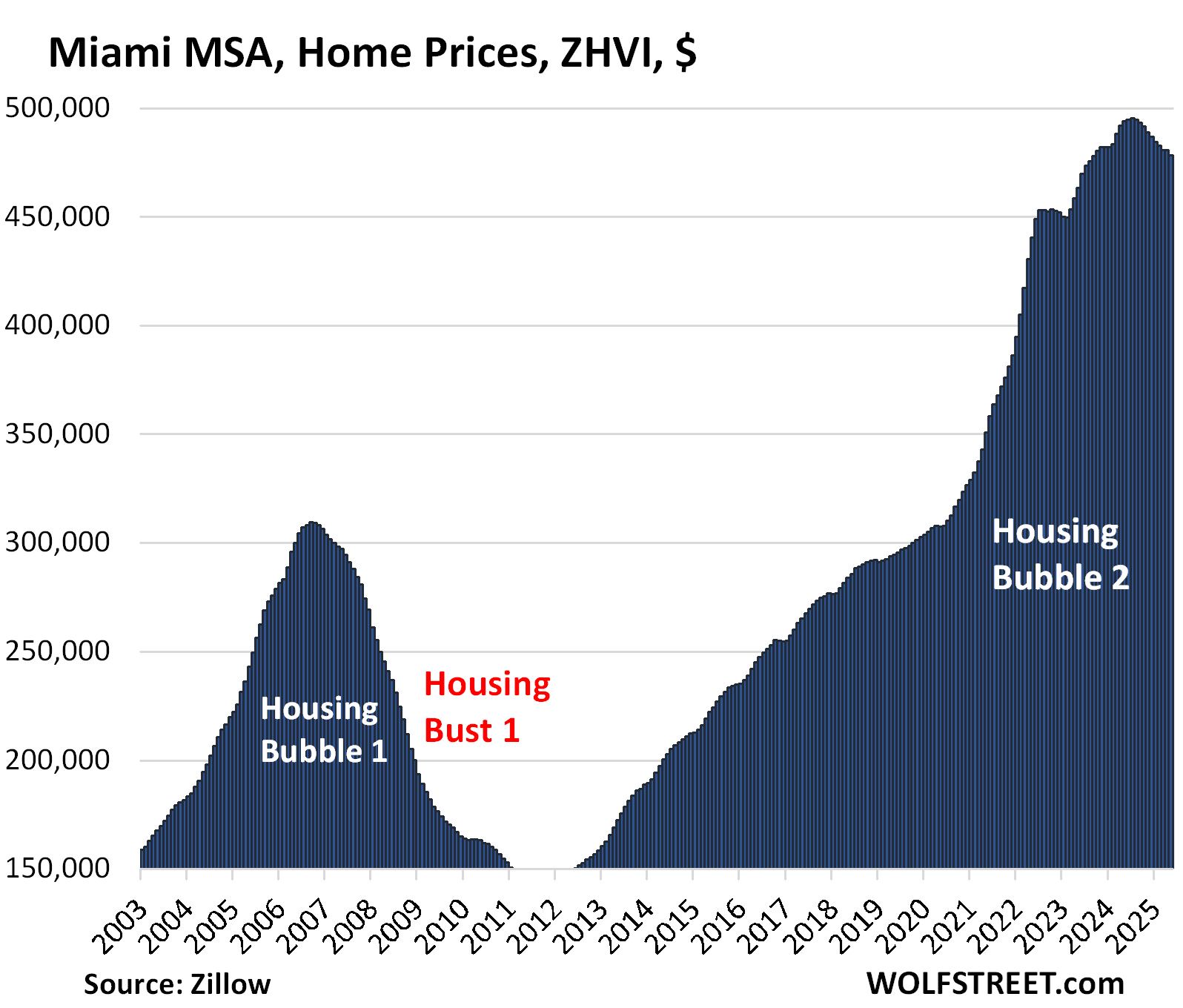

- Miami: -3.2%

- Atlanta: -2.7%

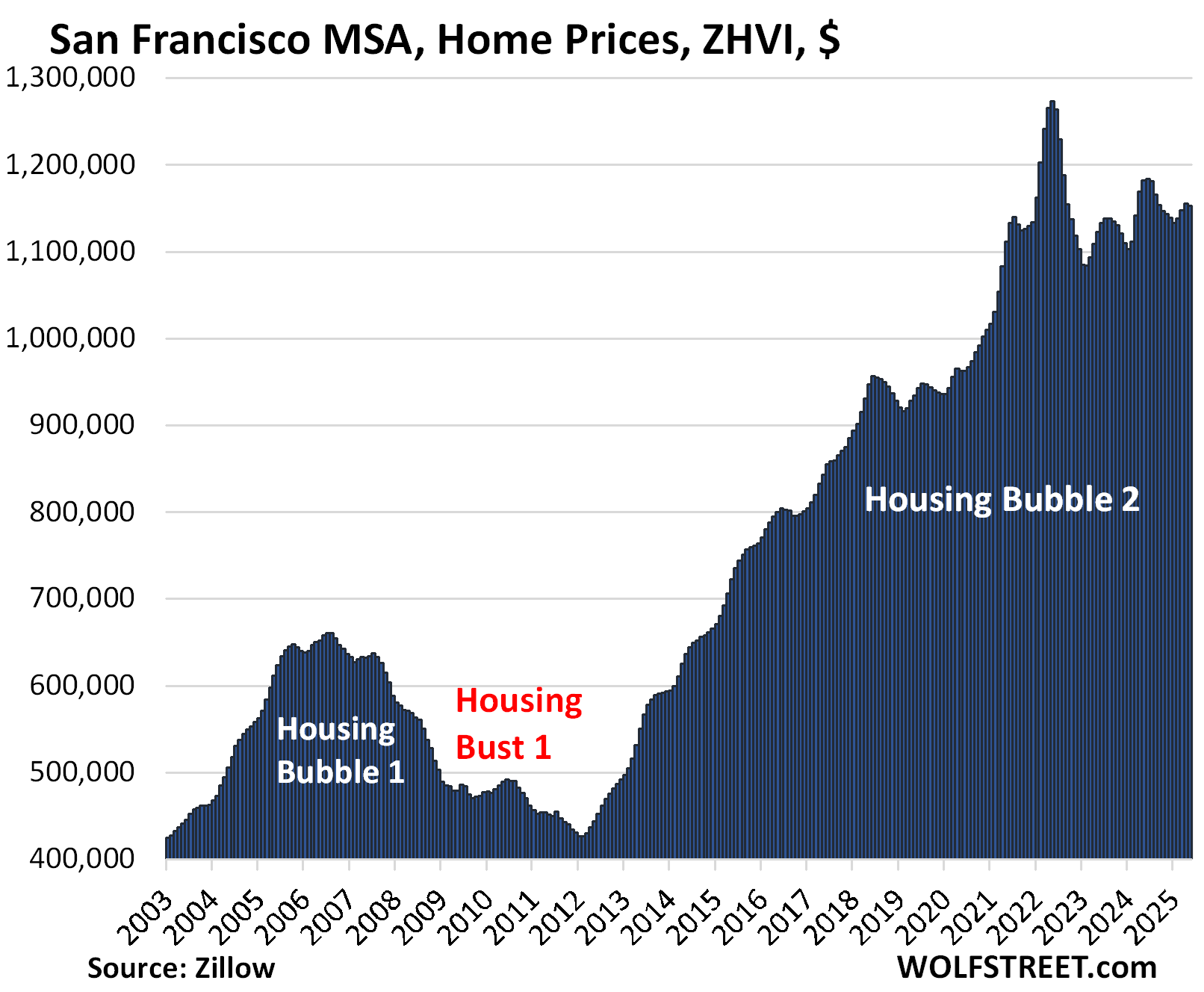

- San Francisco: -2.5%

- Denver: -2.4%

- San Diego: -1.9%

- Raleigh: -1.8%

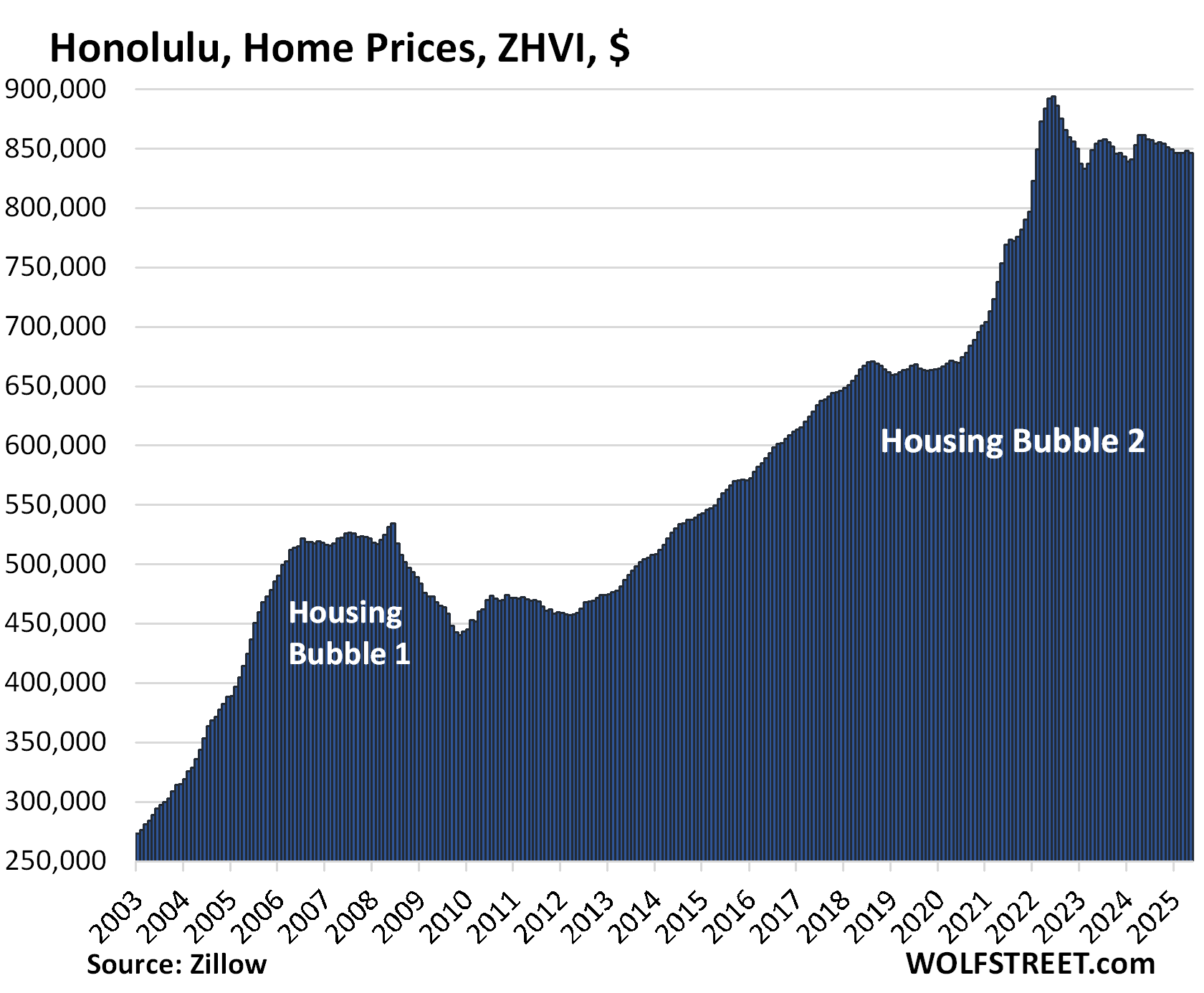

- Honolulu: -1.7%

- Houston: -1.5%

- Sacramento: -1.4%

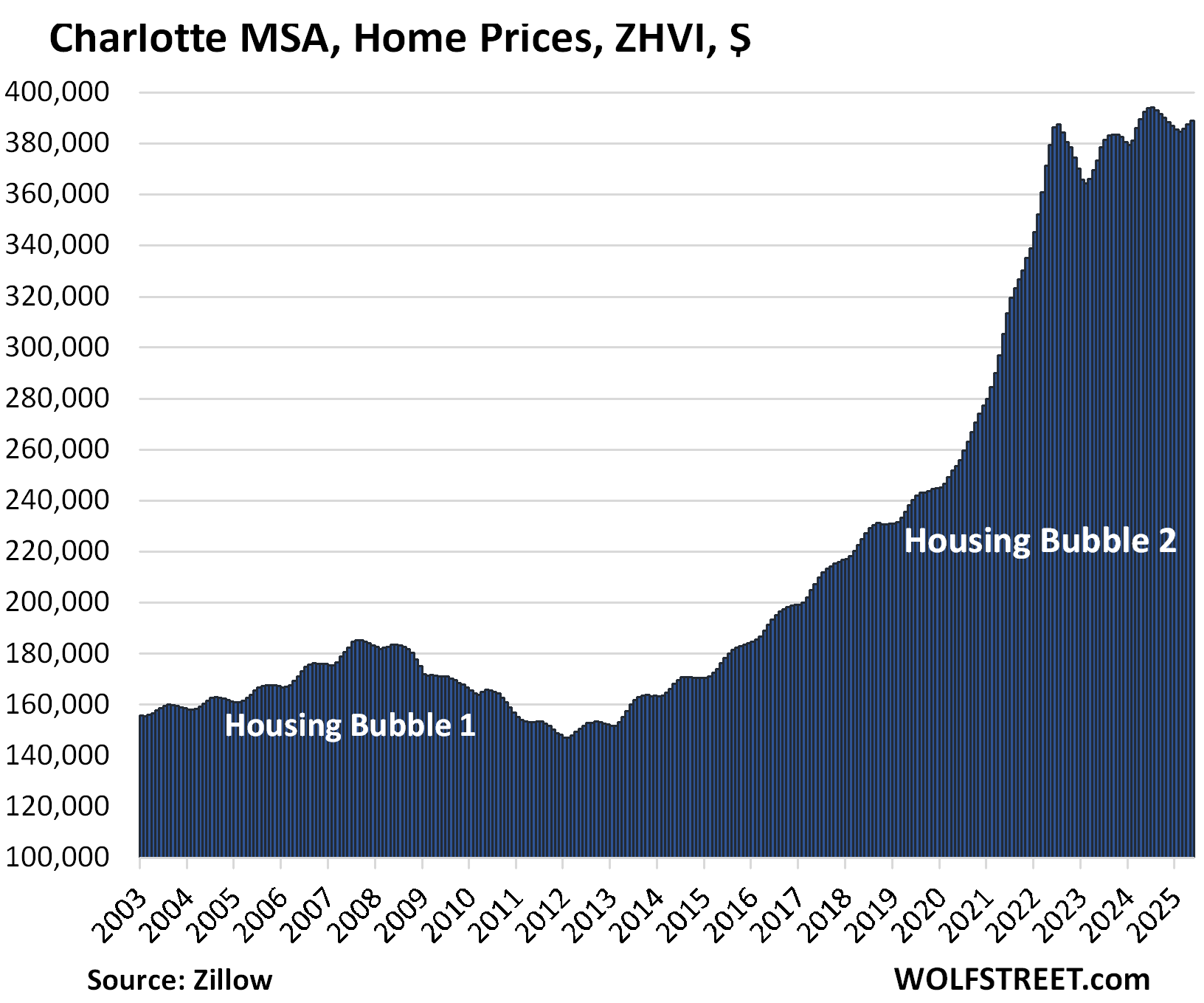

- Charlotte: -0.9%

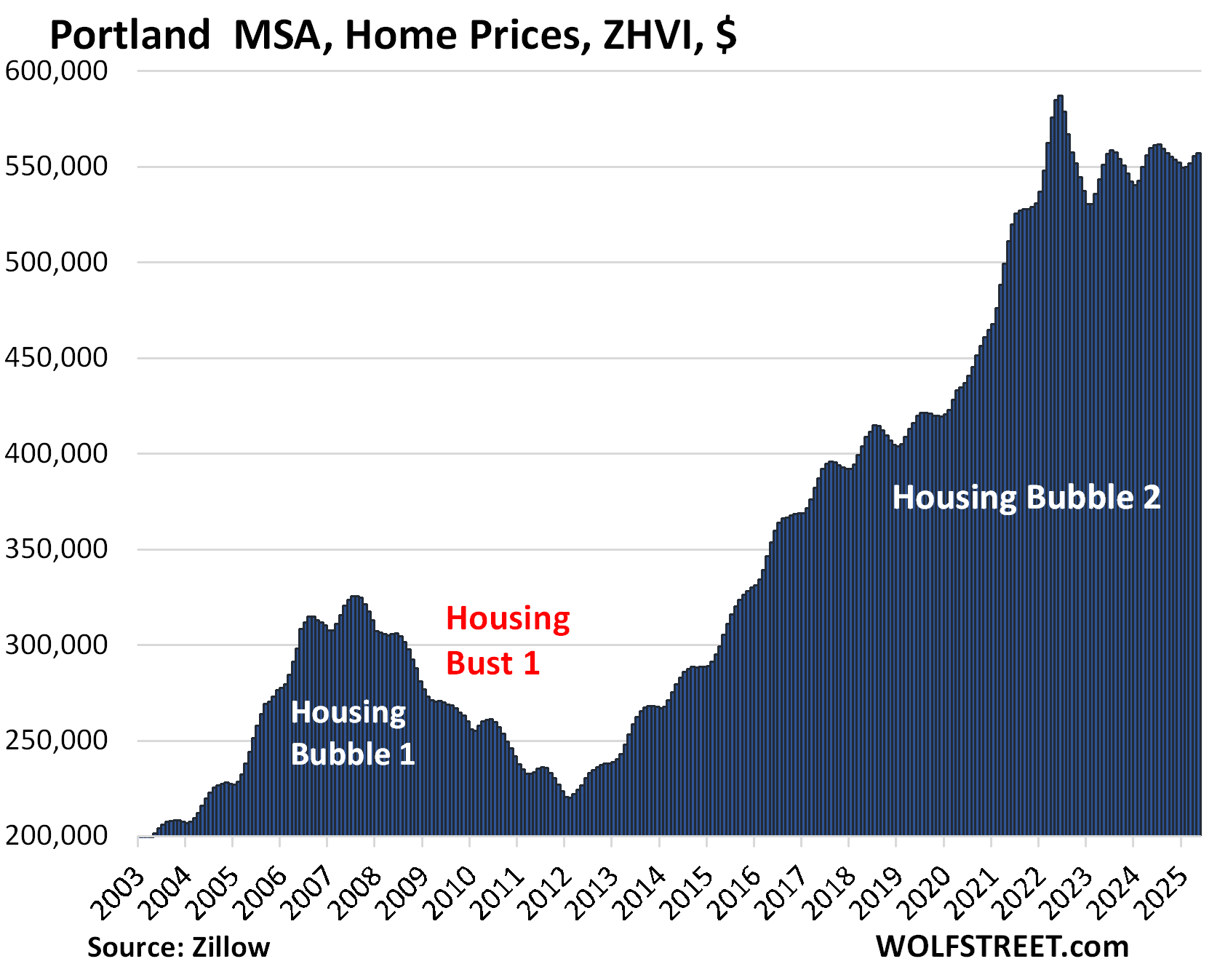

- Portland: -0.5%

- Seattle: -0.1% (newest addition)

This price action is occurring as supply of existing homes for sale in the US jumped to the highest supply for any April since 2016. Inventory is suddenly piling up in the largest markets in California, such as by 66% year-over-year in San Diego, and by 40% in the San Francisco metro where it reached the highest level in many years. In the biggest markets in Florida, inventory is piling up at astonishing rates.

The 19 metros whose prices are down from their 2022 all-time highs.

Led by the metros of:

- Austin: -23.0%

- Phoenix: -10.0%

- San Francisco: -9.5%

- San Antonio: -8.9%

- Denver: -7.4%

- Dallas: -6.7%

- Sacramento: -6.4%

- Tampa: -6.3%

So here we go:

| Austin MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -23.0% | -0.2% | -5.5% | 155% |

The YoY decline worsened from -5.1% in April. Prices are back where they’d been in April 2021.

The Austin MSA includes the counties of Travis, Williamson, Hays, Caldwell, and Bastrop.

Markets in the oil patch didn’t have much of a Housing Bubble 1 in 2002-2006, and then didn’t have much of a Housing Bust 1 afterwards. But they got into it this time around, including in Texas.

This is a completely insane chart for a housing market; home-price charts should never look like this:

| Phoenix MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -10.0% | -0.1% | -3.4% | 217% |

The year-over-year decline worsened from -2.8% in April and -1.6% in February. Prices are back where they’d first been in January 2022:

| San Francisco MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -9.5% | -0.3% | -2.5% | 295% |

The year-over-year decline worsened from -1.2% in April, after having flipped from YoY gains in March.

The MSA includes San Francisco, much of the East Bay (such as Oakland), much of the North Bay, and goes south on the Peninsula into Silicon Valley through San Mateo County. It does not include the San Jose metro, which covers the southern portion of the Bay Area (see below).

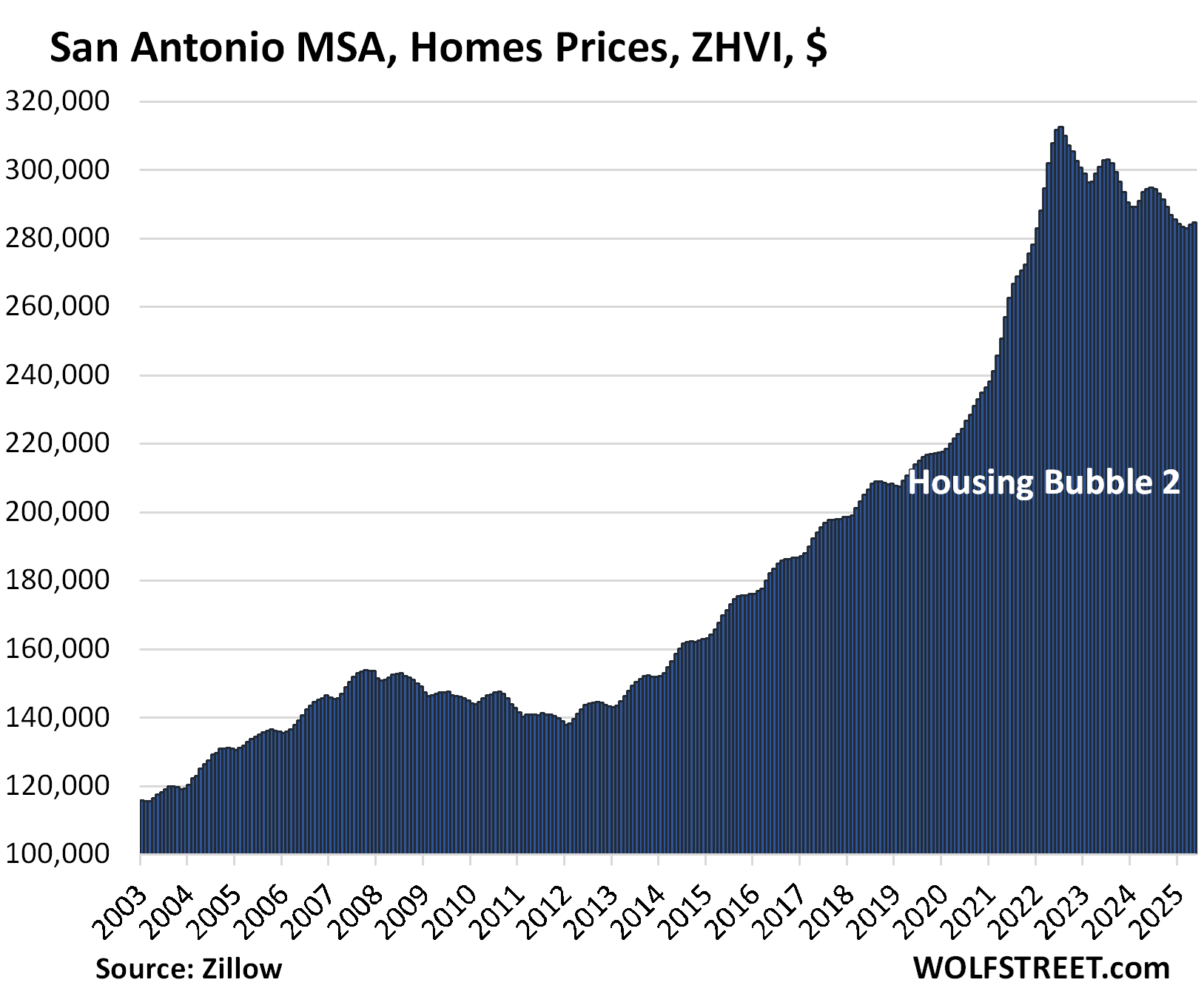

| San Antonio MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -8.9% | 0.2% | -3.3% | 147% |

The YoY decline worsened from -3.2% in April. Prices are back where they’d been in January 2022.

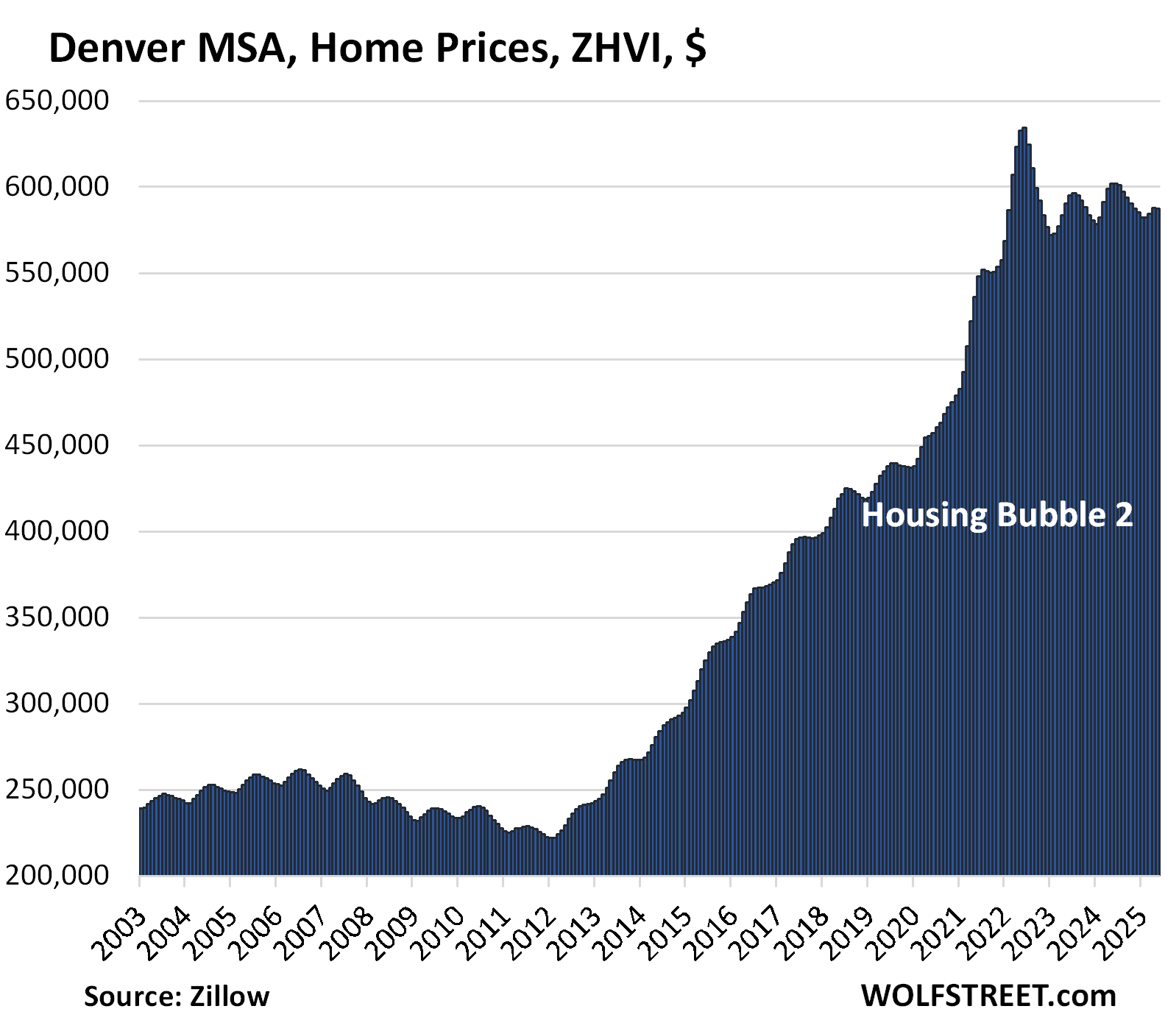

| Denver MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -7.4% | -0.1% | -2.4% | 212% |

The YoY decline worsened from -1.8% in April. Prices are back where they’d first been in early 2022.

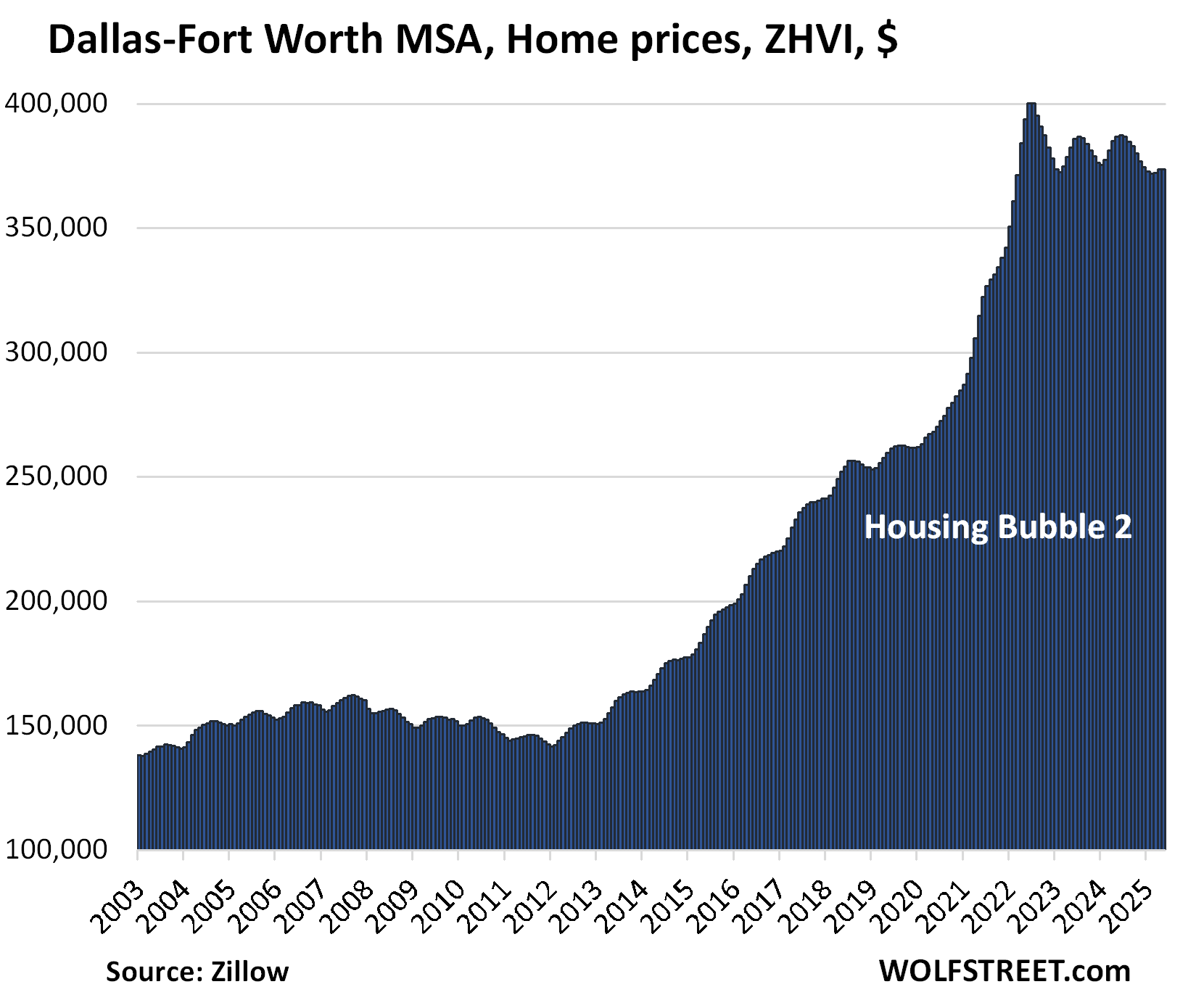

| Dallas-Fort Worth MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -6.7% | 0.0% | -3.4% | 191% |

The YoY drop worsened from -3.0% in April.

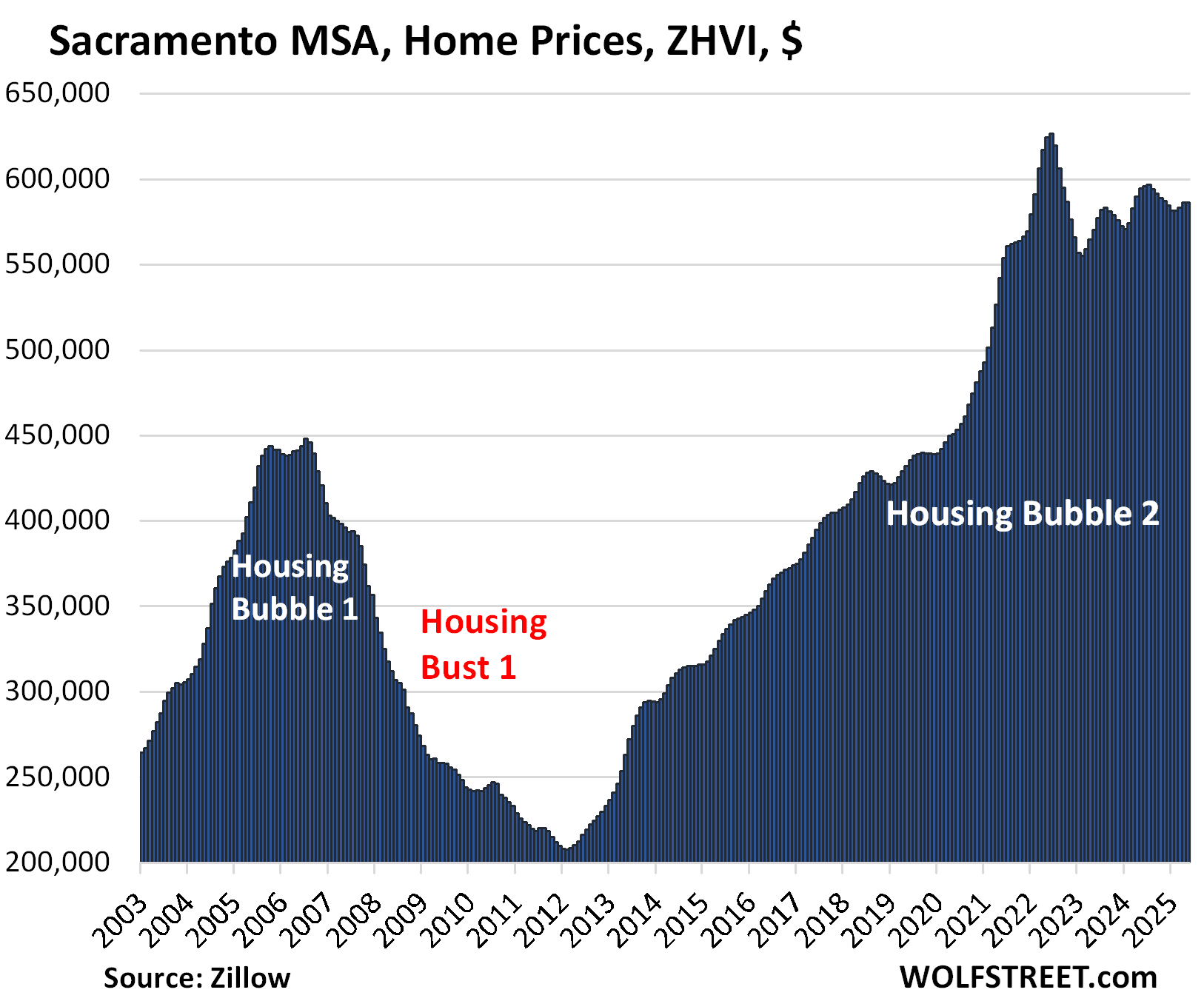

| Sacramento MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -6.4% | 0.0% | -1.4% | 245.8% |

The year-over-year decline worsened from -0.6% in April, when it had flipped to negative, from +0.1% in March, and +1.3% in February.

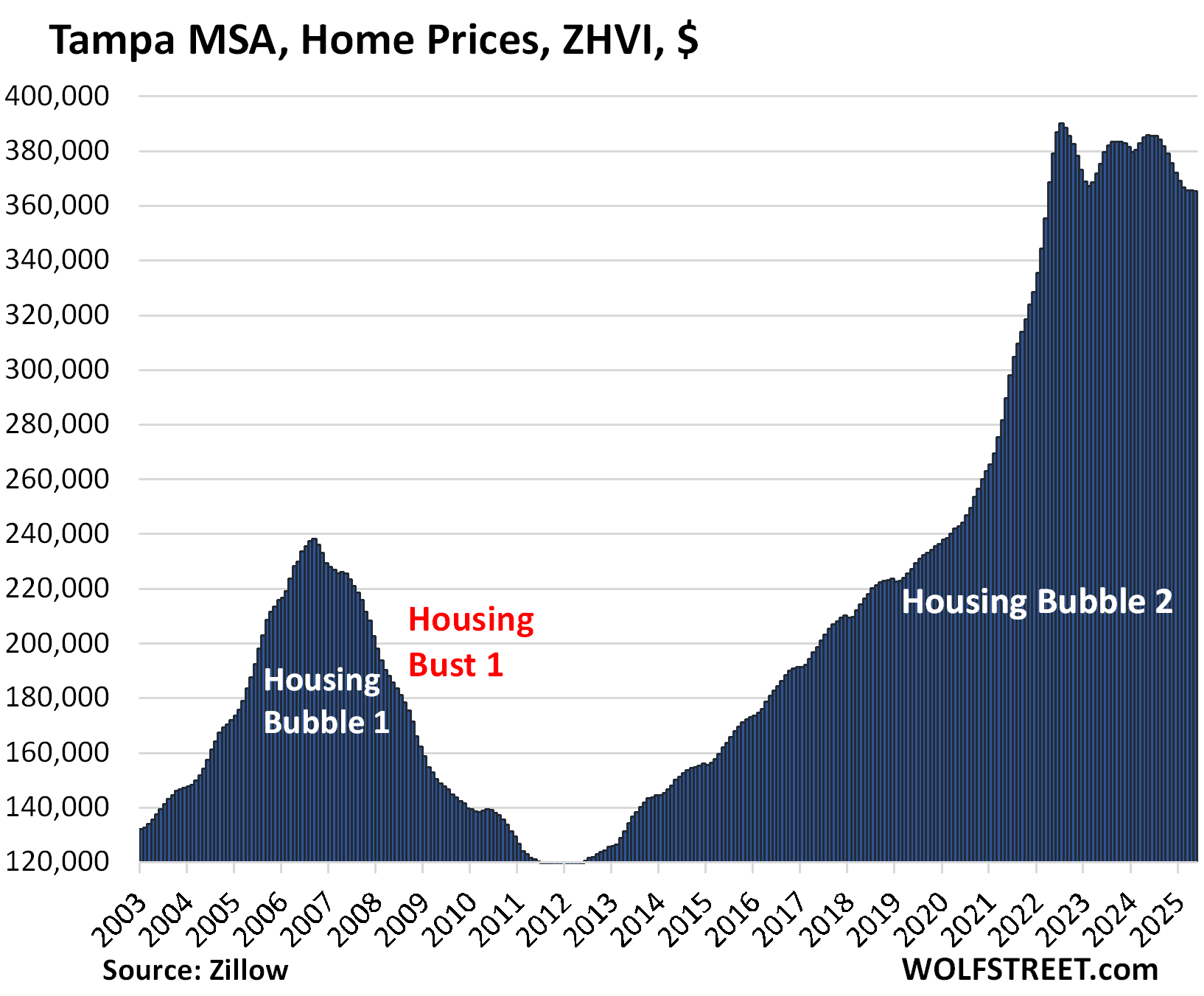

| Tampa MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -6.3% | -0.1% | -5.4% | 261% |

The YoY drop worsened from -5.0% in April.

| Honolulu, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -5.3% | -0.2% | -1.7% | 278% |

The YoY decline worsened from -1.6% in April. In March, the YoY gains had flipped to negative from positive.

| Portland MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -5.1% | 0.3% | -0.5% | 220% |

The YoY decline worsened from -0.1% in April, when the index had flipped from YoY price gains.

Prices are back where they’d first been in early 2022

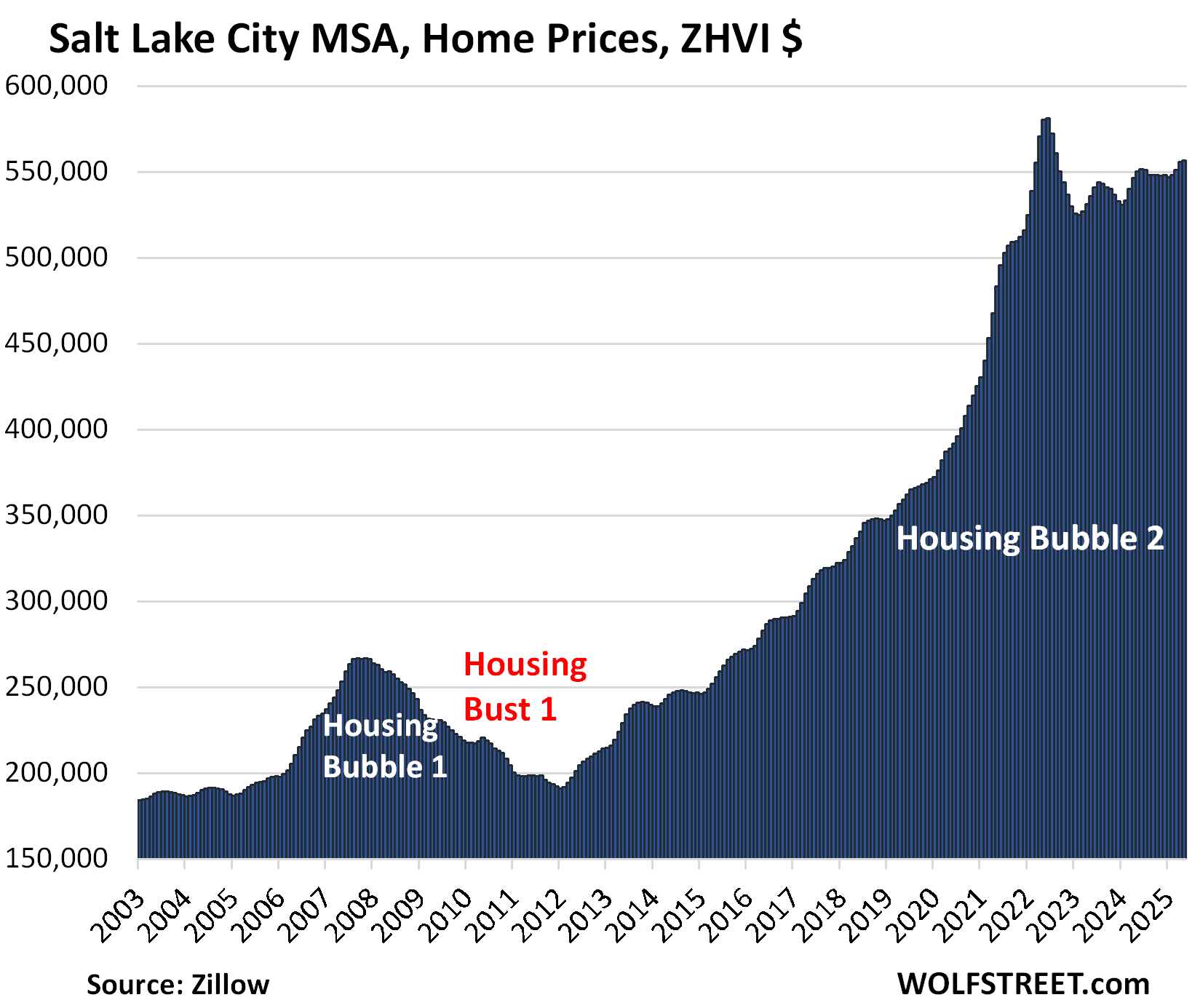

| Salt Lake City MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -4.2% | 0.2% | 1.2% | 219% |

The year-over-year gain declined from +1.7% in April and +2.0% in March.

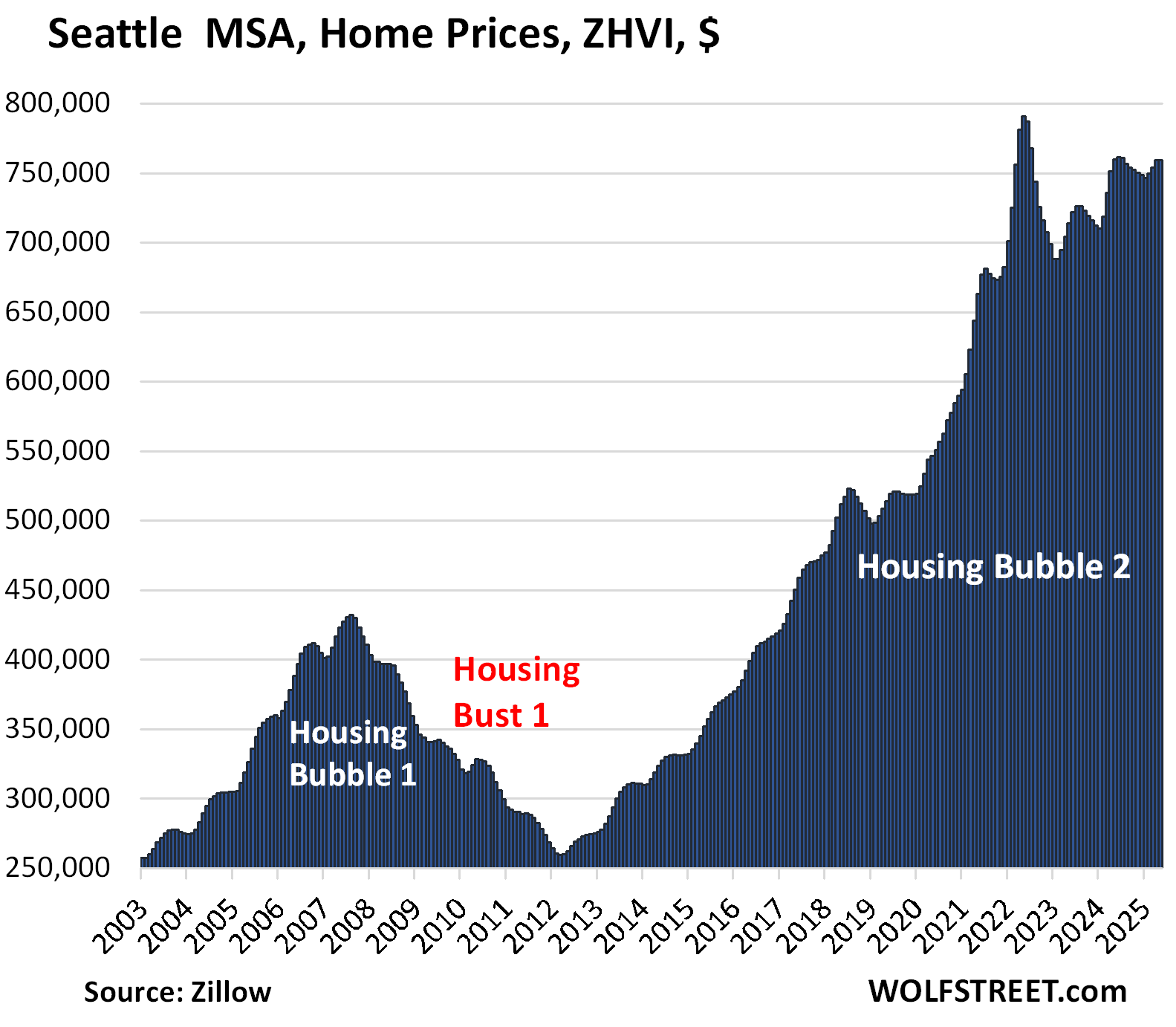

| Seattle MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -4.0% | 0.0% | -0.1% | 242% |

The YoY price change flipped to negative (-0.1%) in May from positive (+1.1%) in April, and from +4.3% in February.

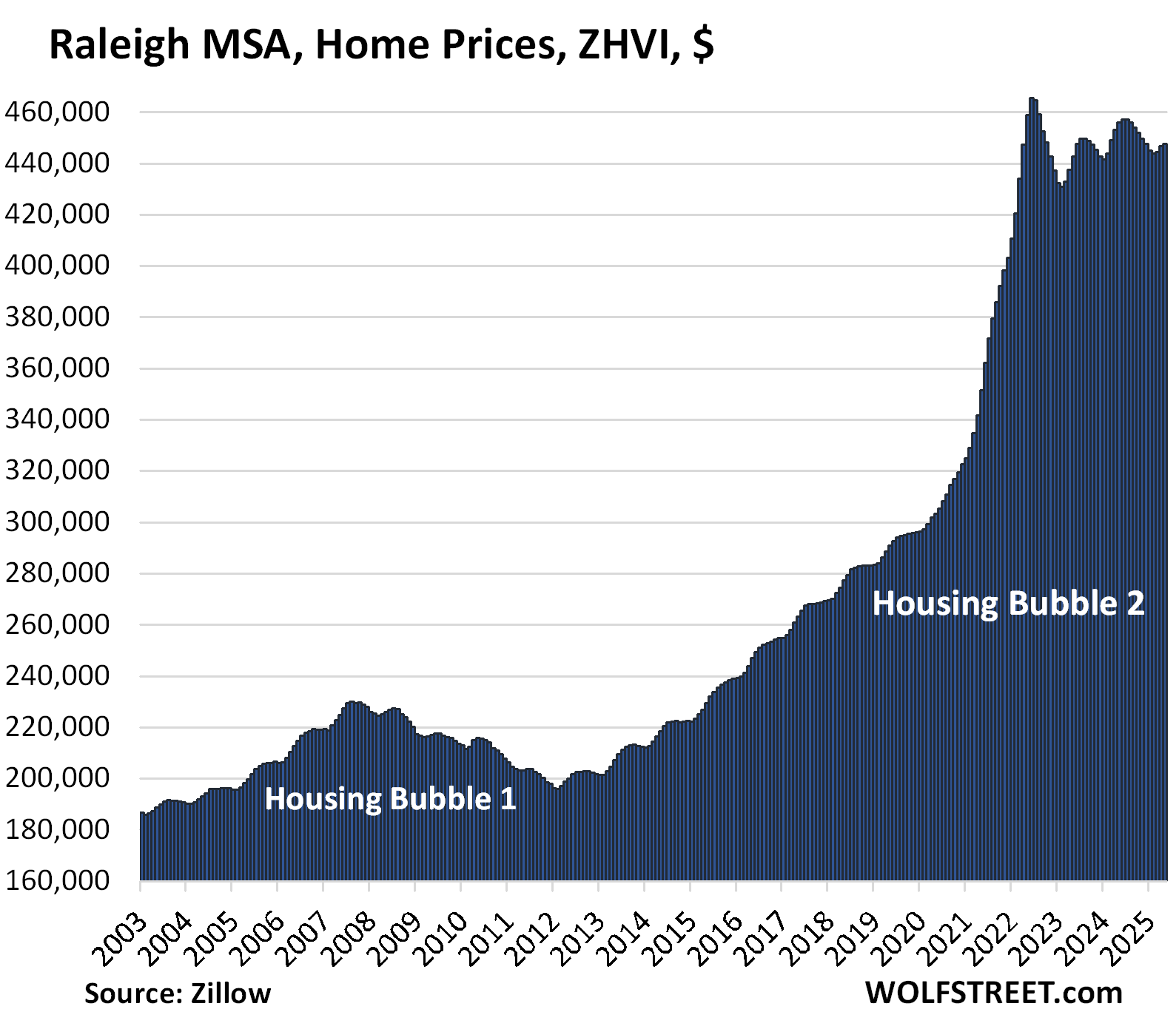

| Raleigh MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -3.8% | 0.2% | -1.8% | 157% |

The YOY decline worsened from 1.4% in April.

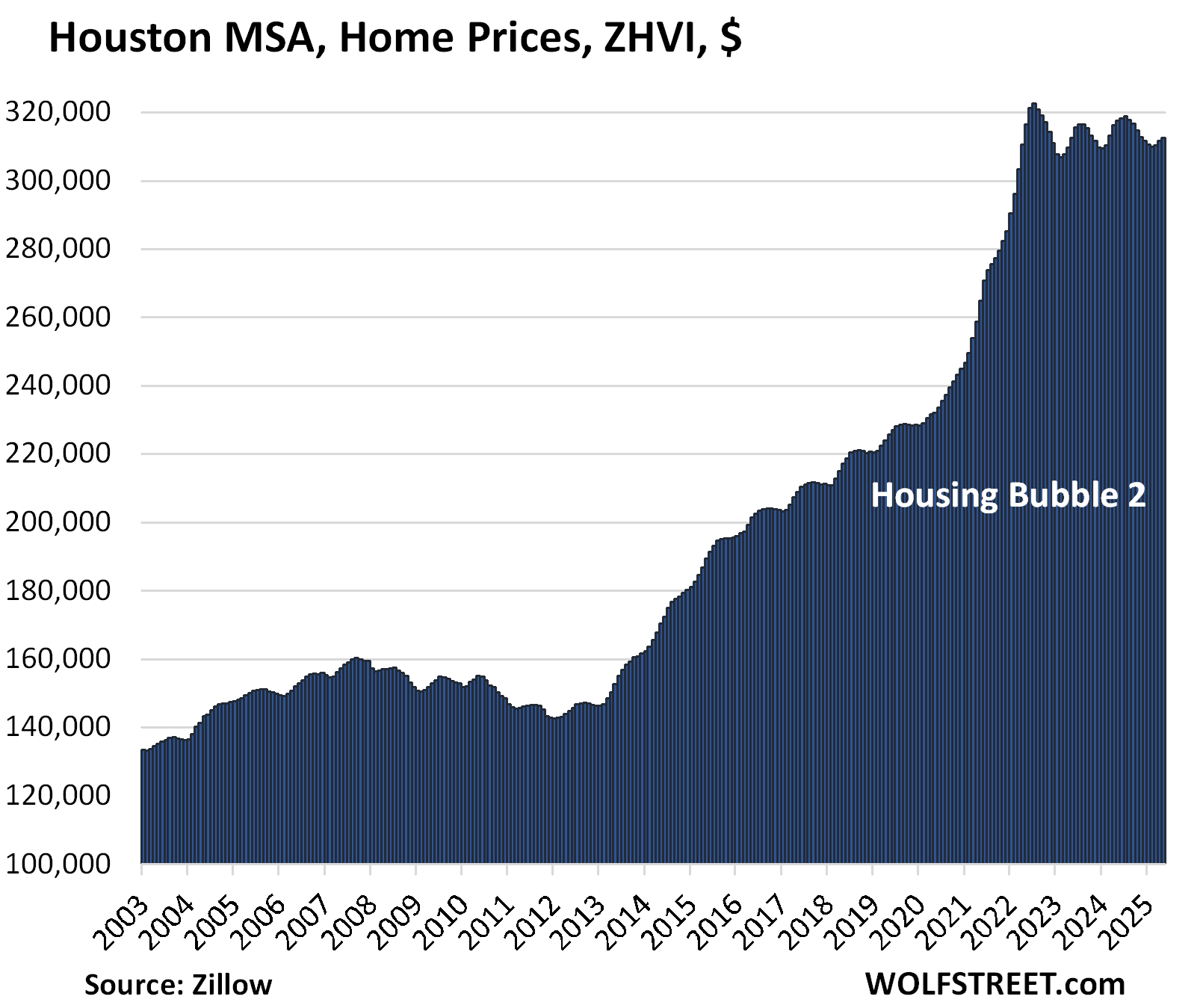

| Houston MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -3.1% | 0.3% | -1.5% | 151% |

The YoY decline worsened from -1.4% in April. The index is where it had first been in April 2022.

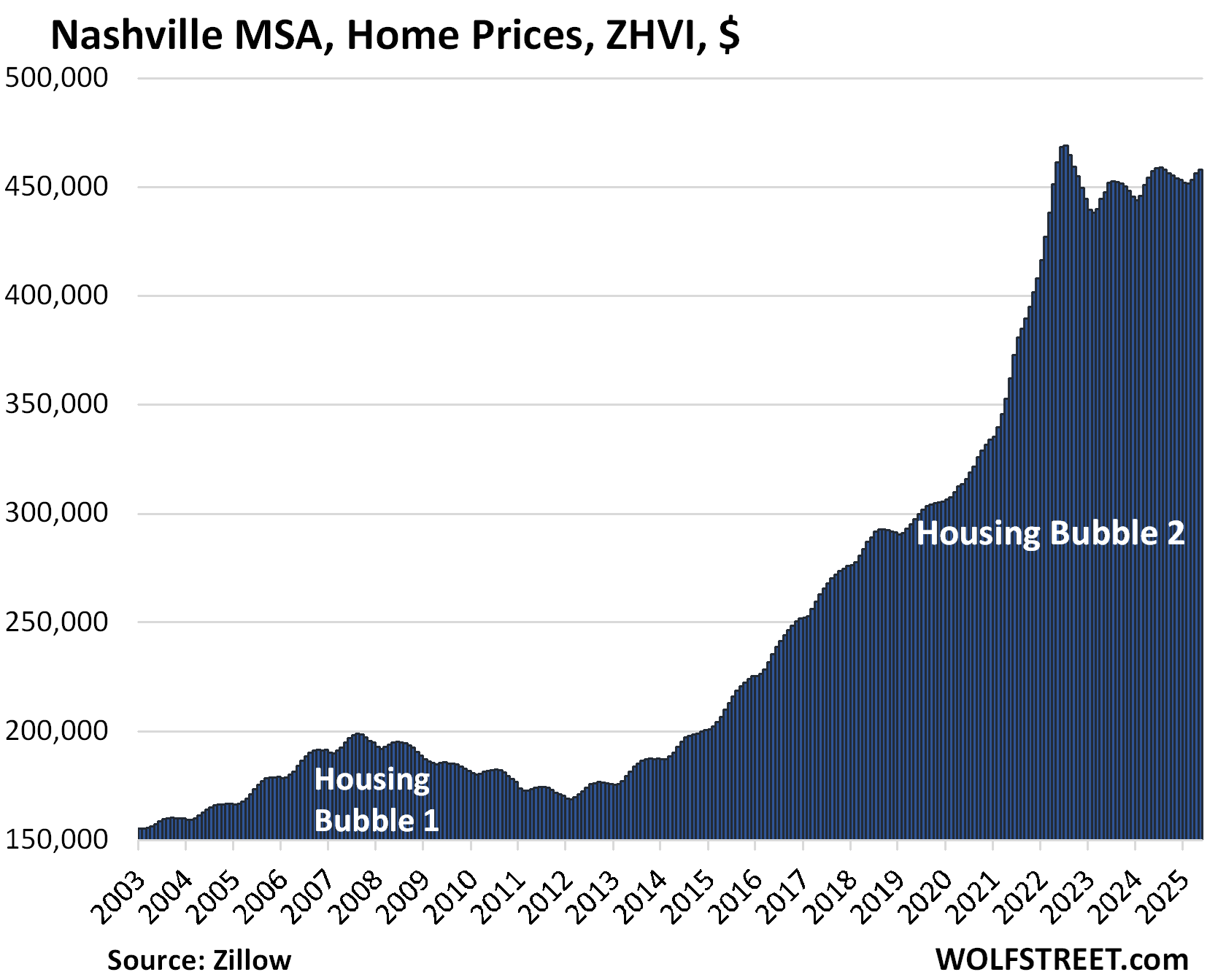

| Nashville MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -2.3% | 0.3% | 0.1% | 220% |

The YoY gain shrank further, to just +0.1%, from +0.4% in April. The index is where it had been in April 2022.

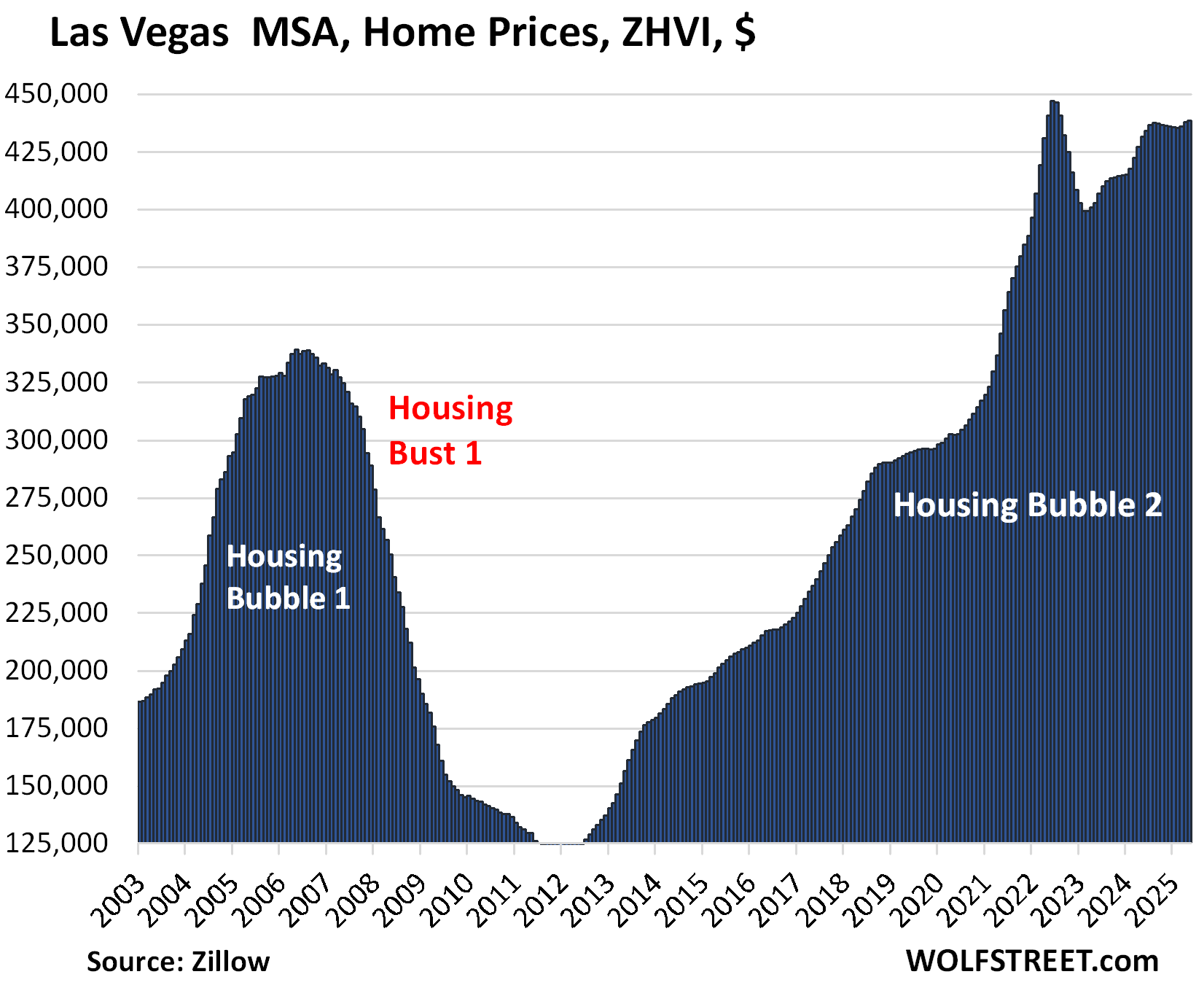

| Las Vegas MSA, Home Prices | |||

| From June 2022 peak | MoM | YoY | Since 2000 |

| -2.0% | 0.1% | 1.6% | 180% |

The YoY gain shrank from +2.5% in April and +4.25% in February.

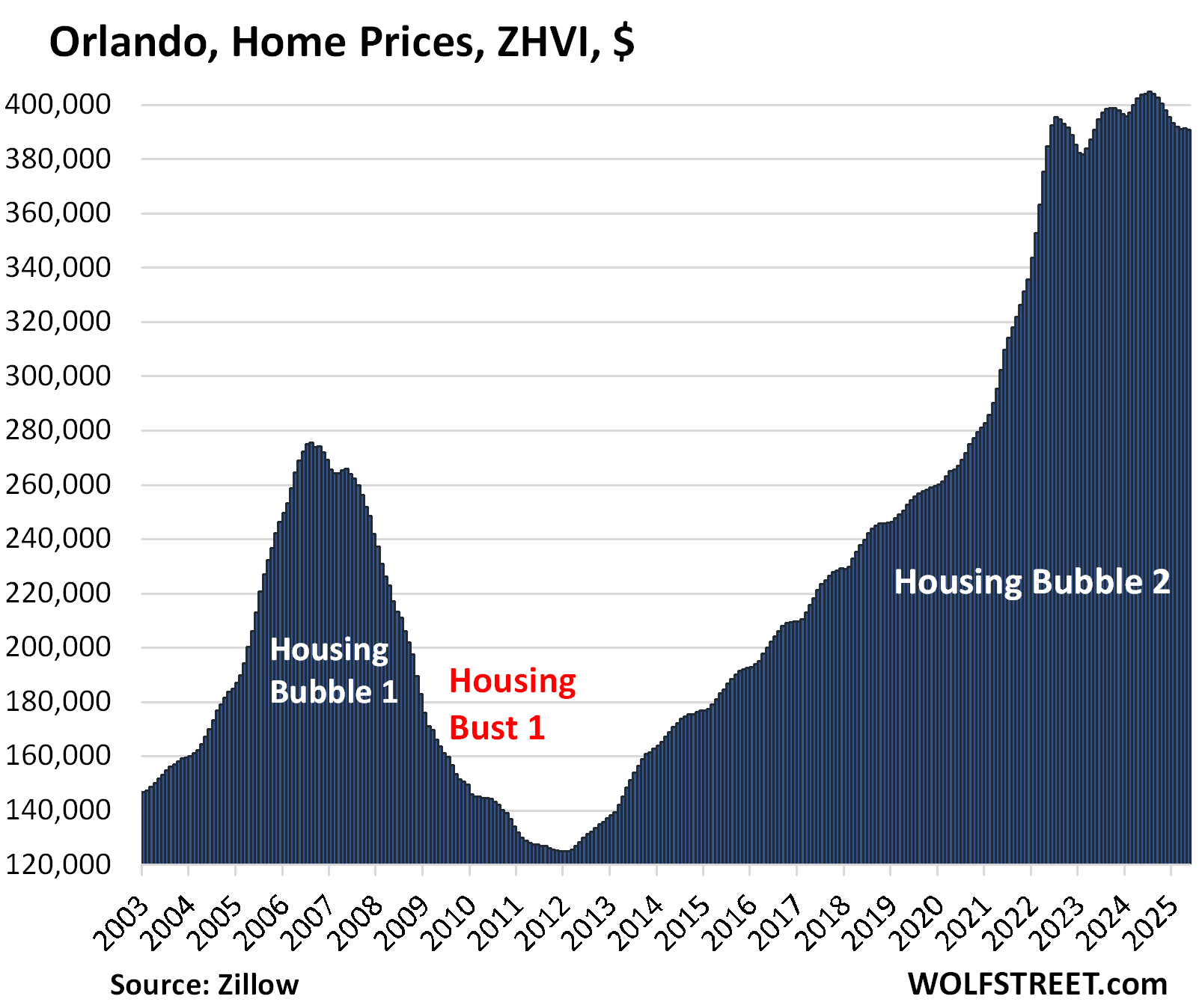

| Orlando MSA, Home Prices | |||

| From June 2022 | MoM | YoY | Since 2000 |

| -1.2% | -0.1% | -3.2% | 231% |

YoY decline worsened from -2.7% in April and -1.4% in February.

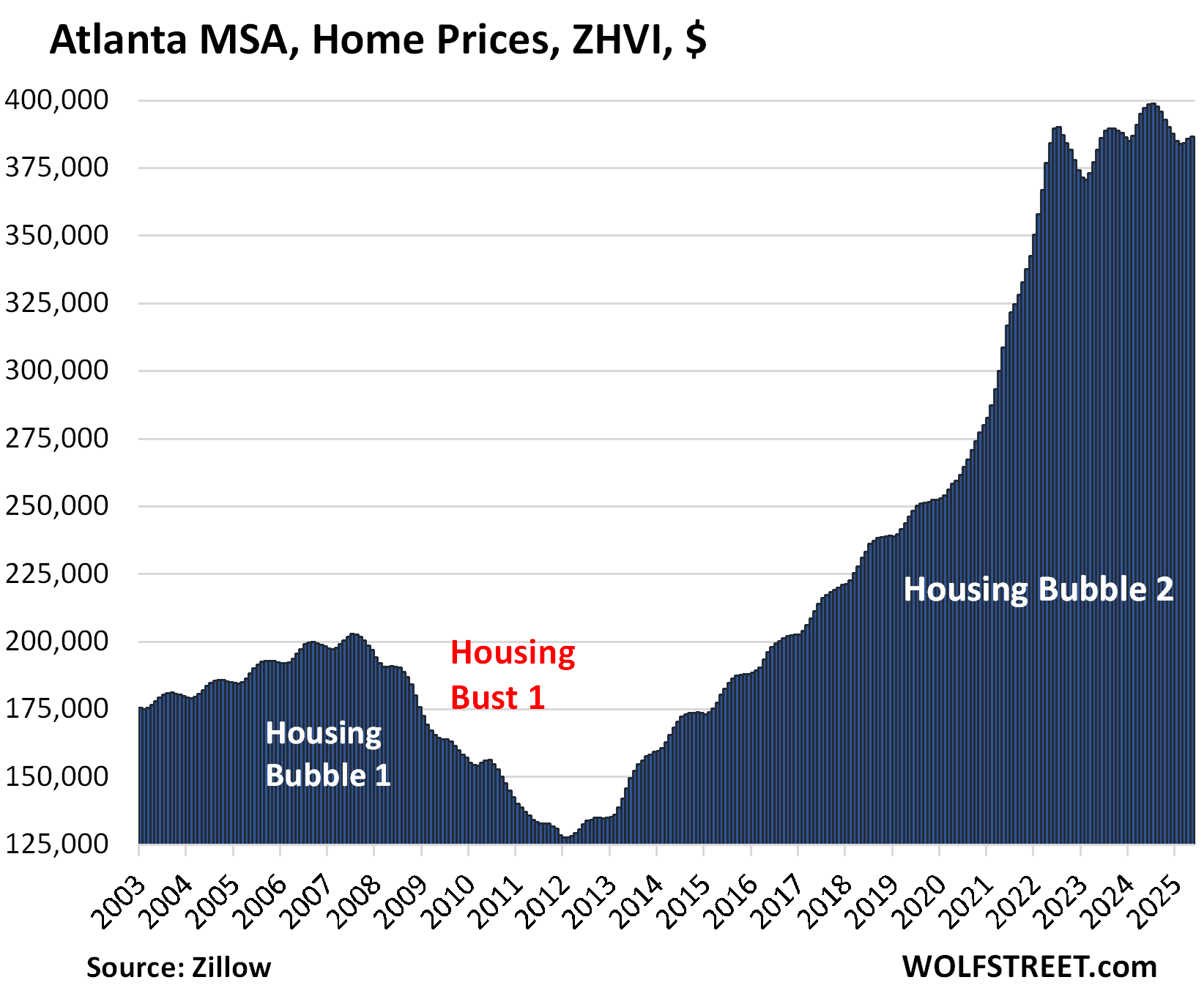

| Atlanta MSA, Home Prices | |||

| From July 2022 | MoM | YoY | Since 2000 |

| -0.9% | 0.2% | -2.7% | 159% |

The YoY decline worsened from -2.3% in April and -0.7% in February.

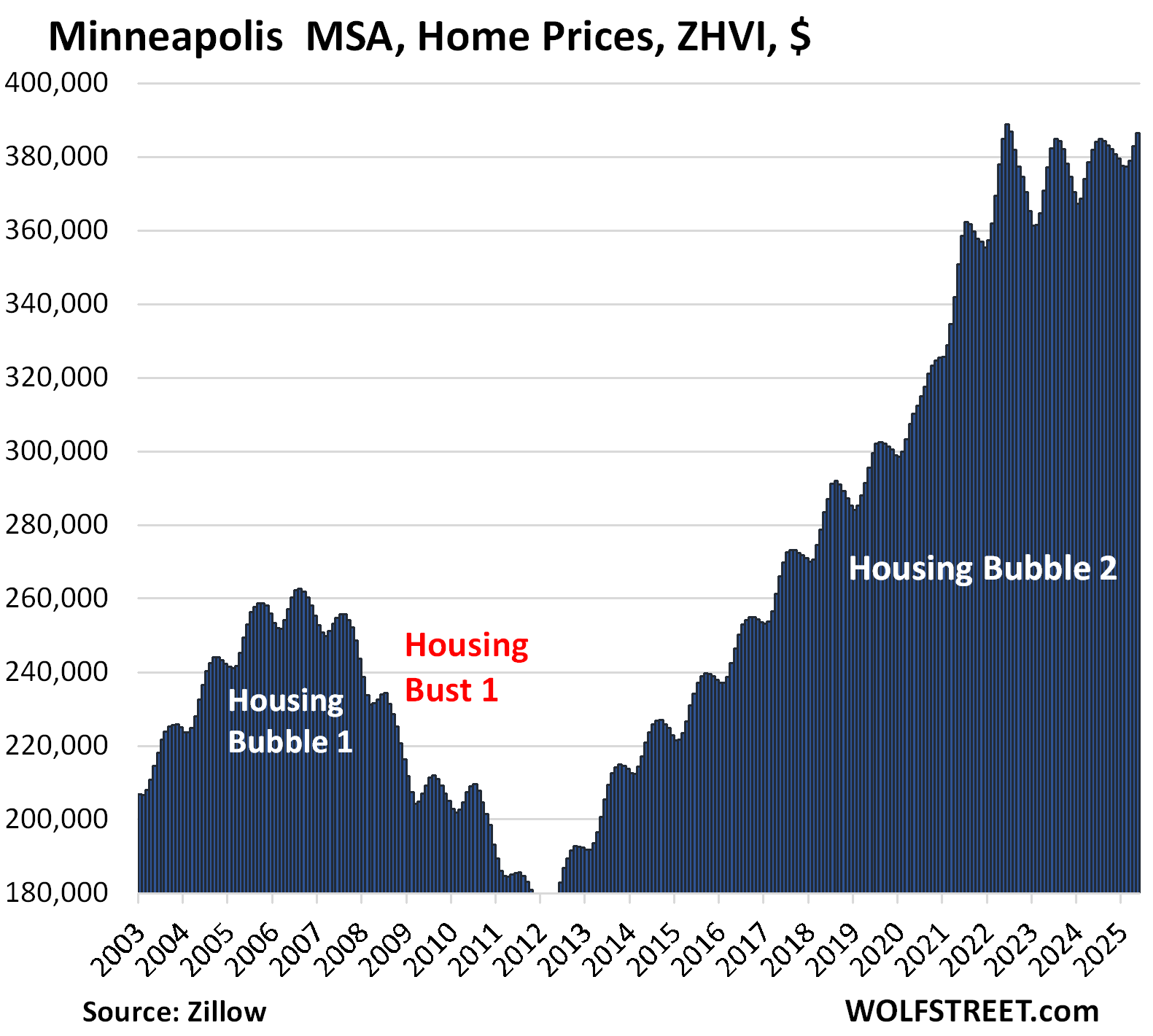

| Minneapolis MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -0.6% | 1.0% | 1.2% | 161% |

The YoY gain was unchanged from April.

The 3 metros that are still higher than in mid-2022, if barely, but down YoY:

| Miami MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.4% | -3.2% | 322% |

The YoY decline worsened from -2.3% in April and -0.2% in February. Since the high in July 2024, the index has dropped by 3.4%.

| San Diego MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.1% | -1.9% | 335% |

The YoY decline worsened to -1.9% in May after having flipped to negative (-0.9%) in April from positive (+0.5%) in March.

| Charlotte MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.4% | -0.9% | 171% |

The YoY decline worsened from -0.6% in April after having flipped to negative in March.

The index is now just a hair above where it had been in mid-2022:

The 11 metros still up YoY and higher than in mid-2022.

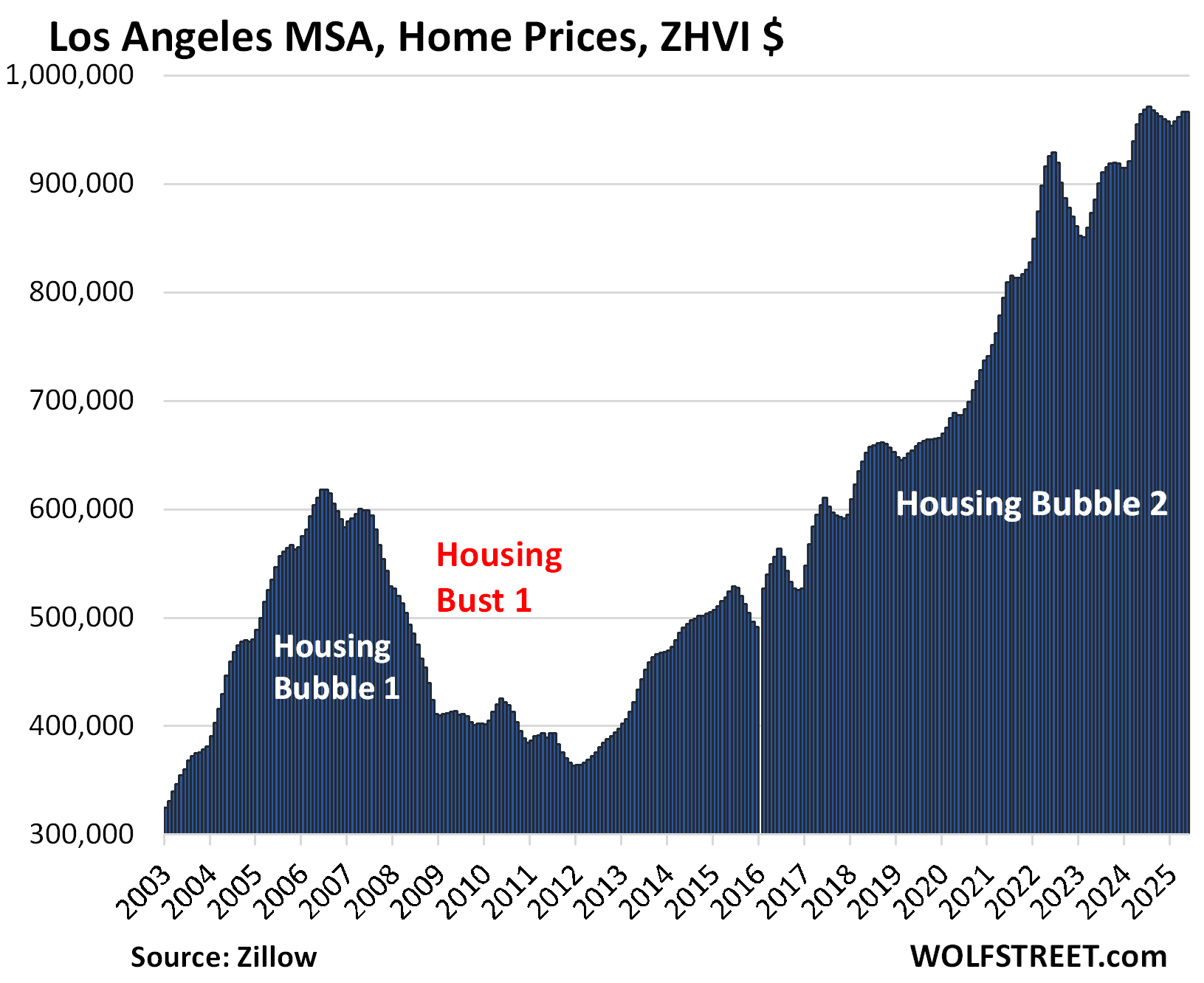

| Los Angeles MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.0% | 0.2% | 333% |

The YoY gain nearly vanished, from +1.2% in April and +3.9% in February.

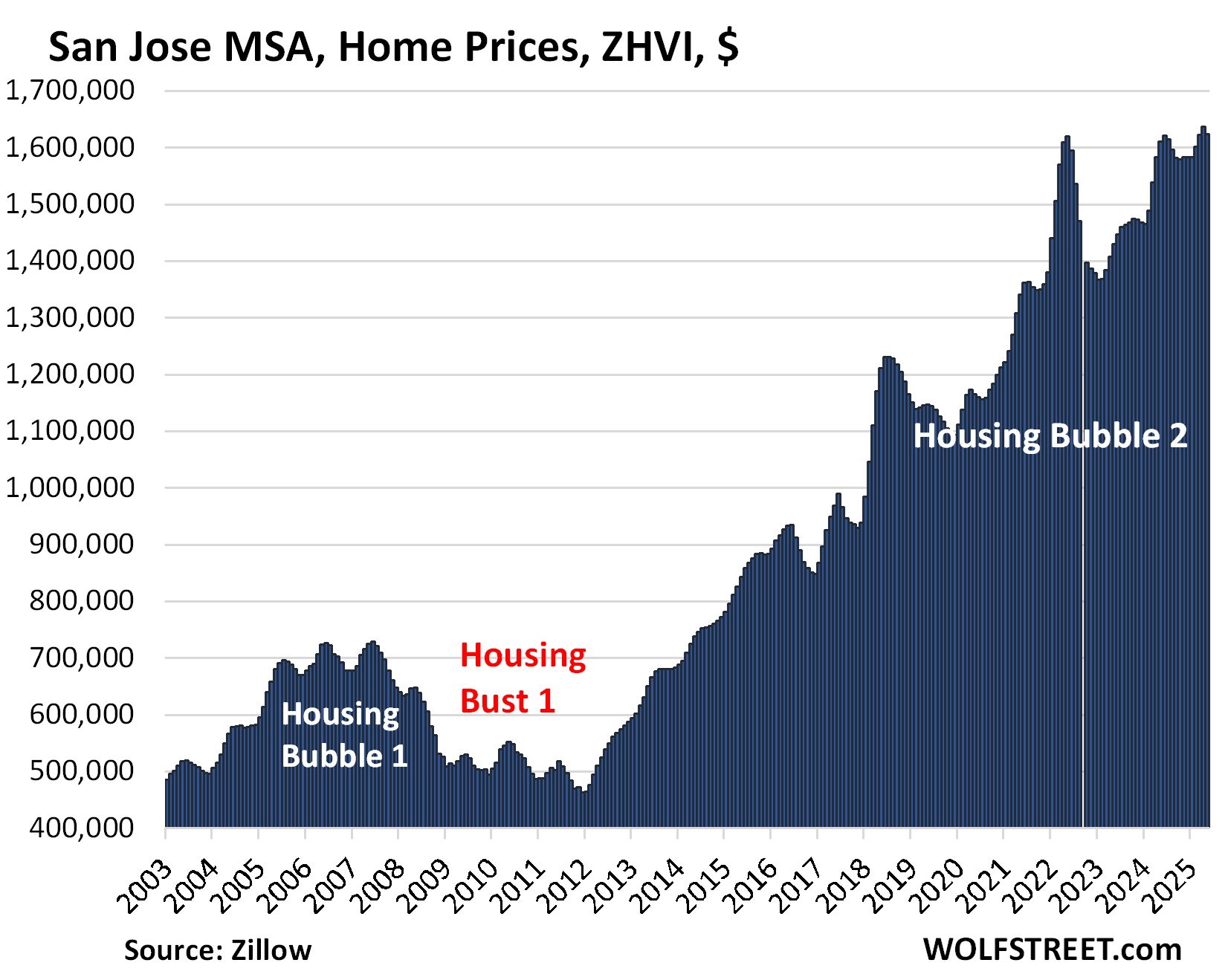

| San Jose MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.8% | 0.8% | 348% |

The big drop in May whittled down the YoY gain to just 0.8% from +3.4% in April, +5.5% in March, and +7.6% in February.

And the index is essentially back where it had first been three years ago, in May 2022.

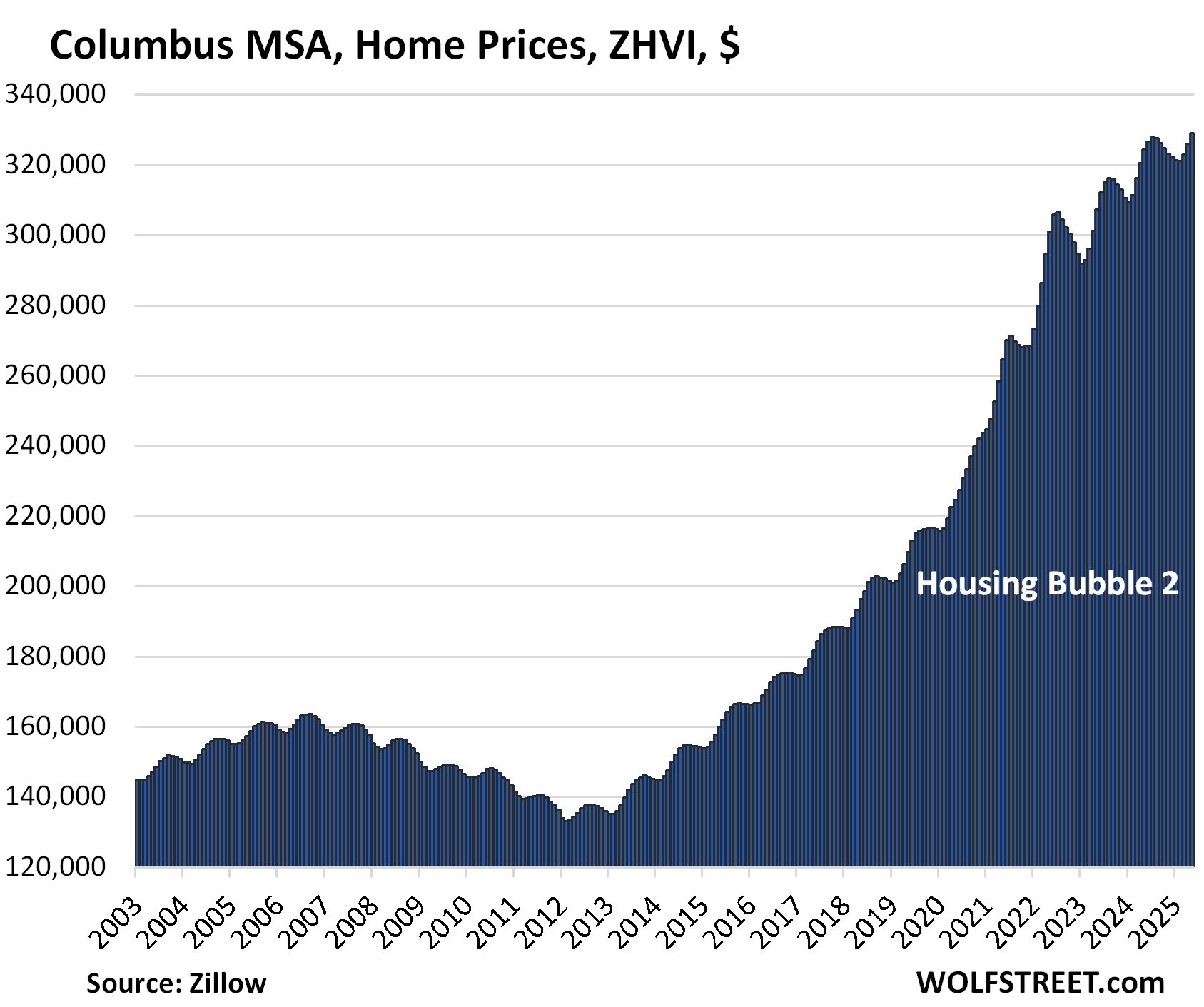

| Columbus MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.9% | 1.5% | 158% |

The YoY increase shrank further, from +1.7% in April and from +3.1% in February.

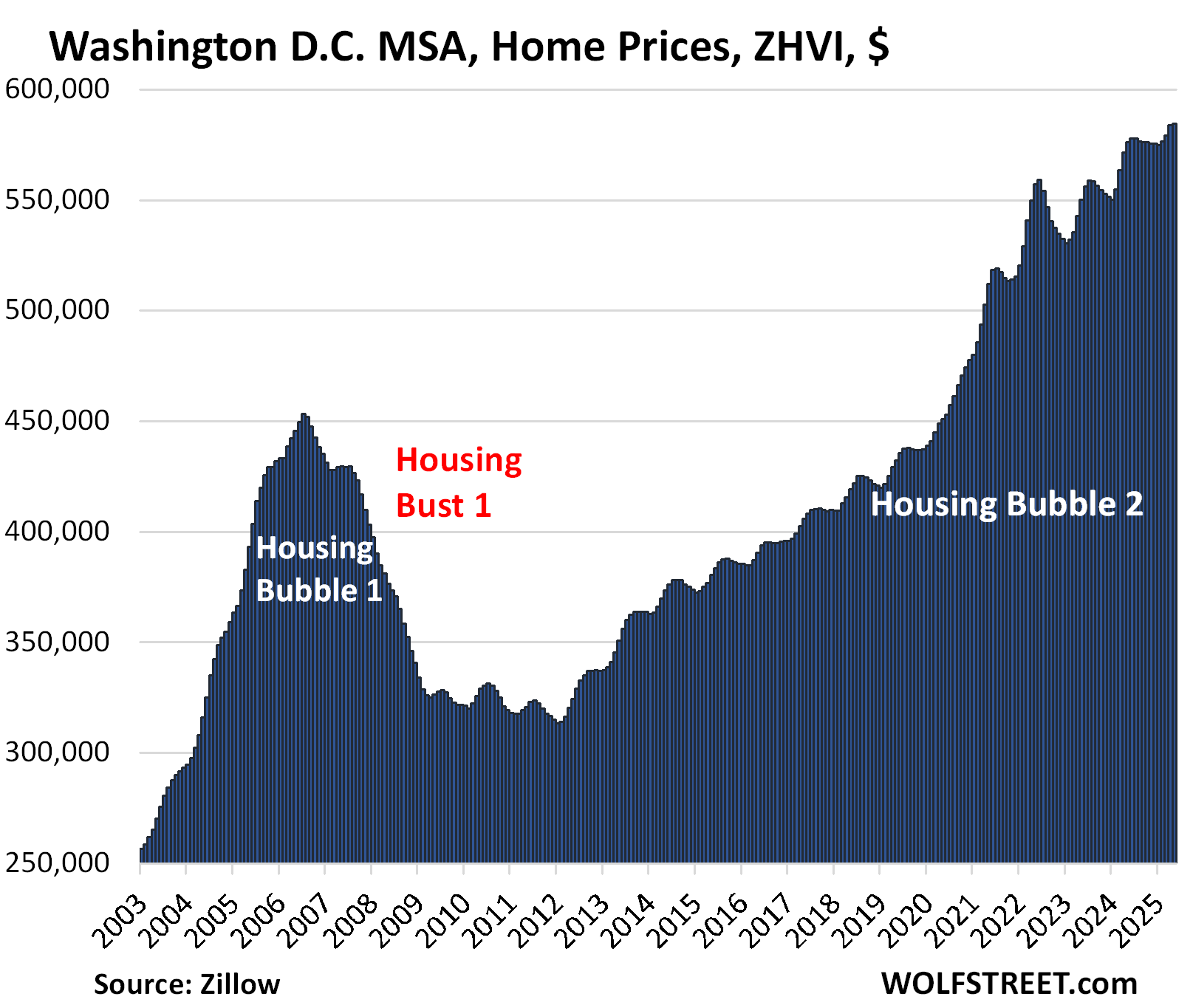

| Washington D.C. MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.2% | 1.5% | 220% |

The YoY gain got whittled down further from +2.1% in April and +4.0% in February.

The metro includes Washington D.C. and parts of Maryland, Virginia, and West Virginia.

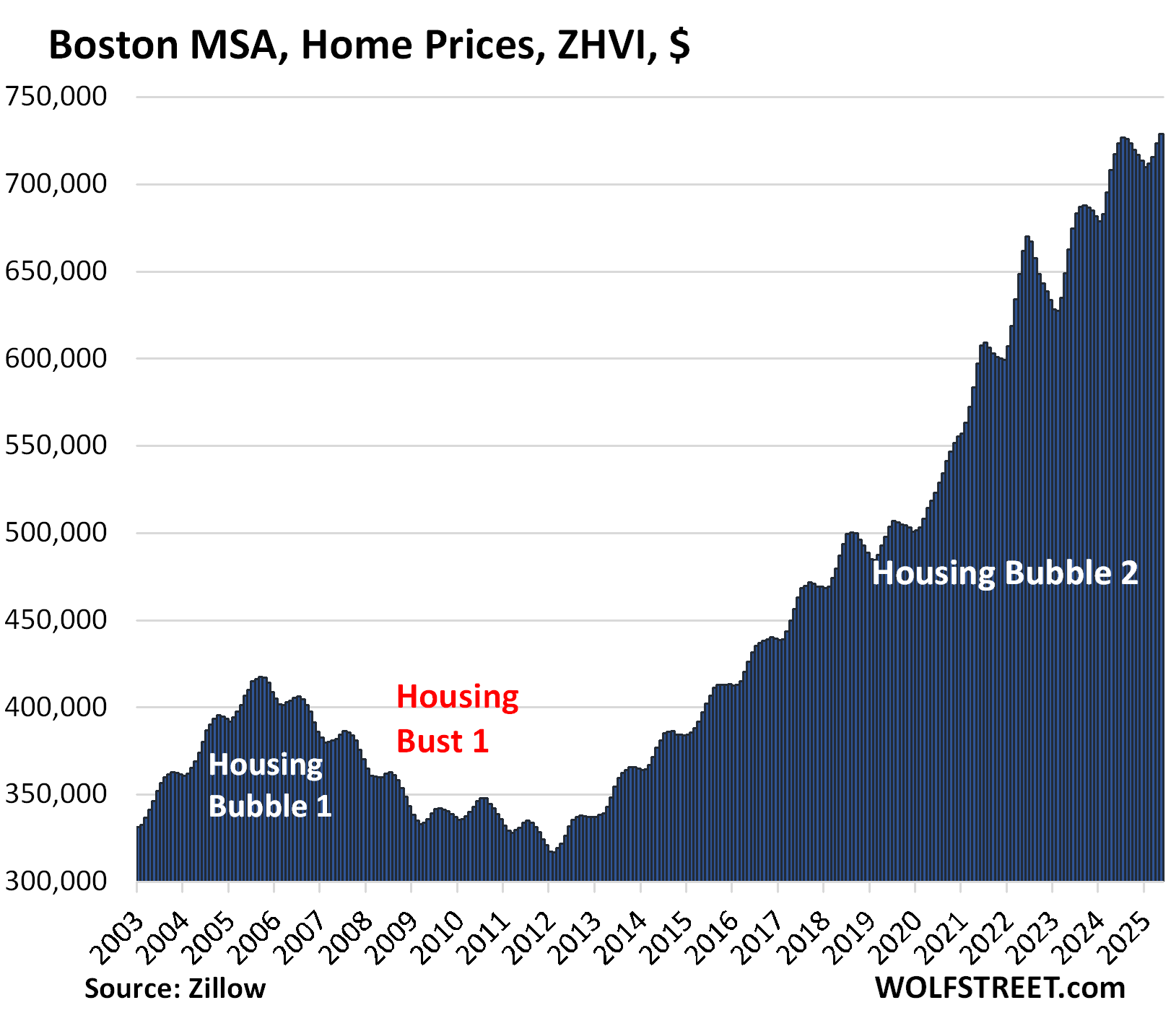

| Boston MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.7% | 1.6% | 231% |

The YoY gain declined from +2.2% in April and +4.2% in February.

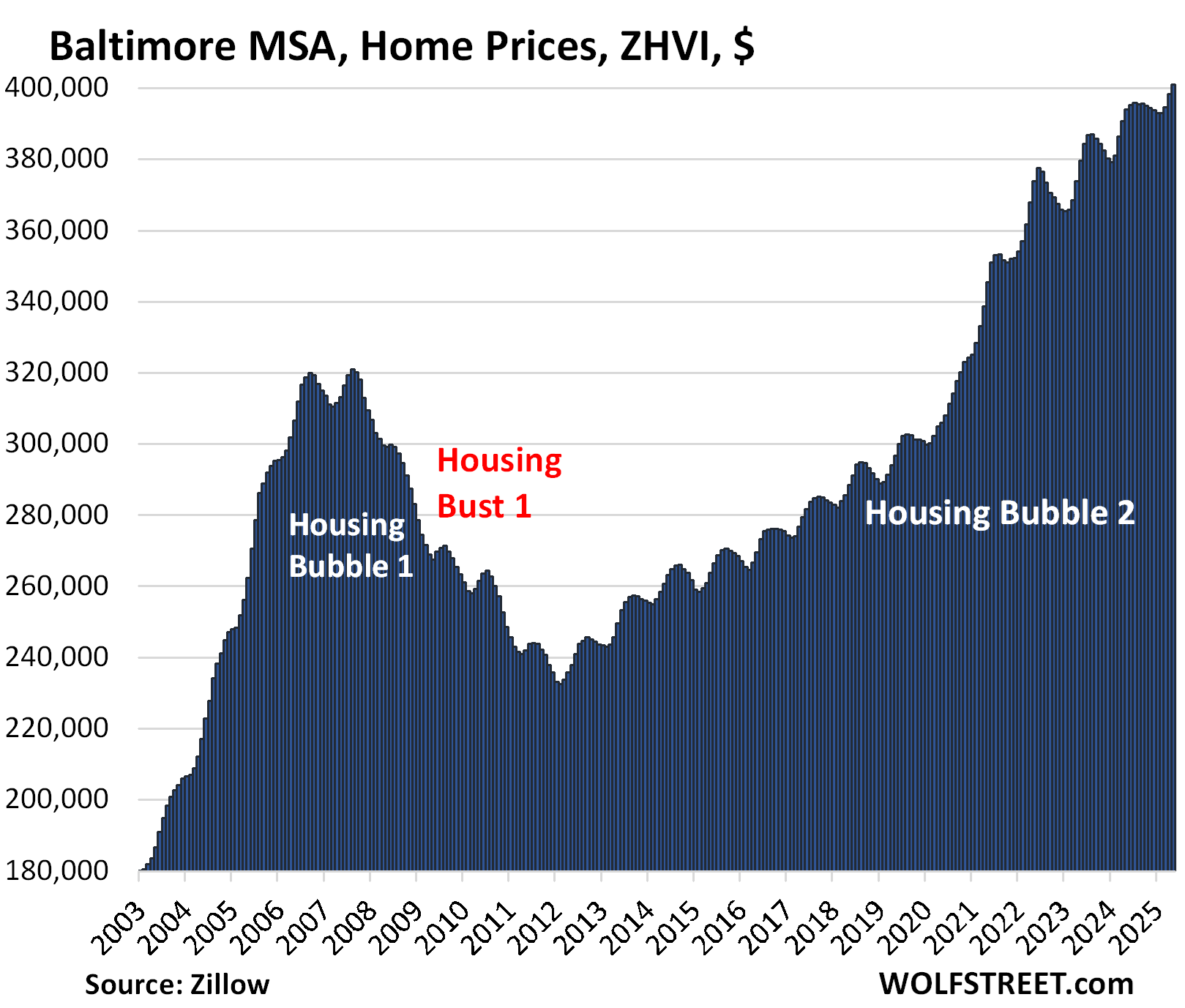

| Baltimore MSA, Home Prices | |||

| MoM | YoY | Since 2000 | |

| 0.7% | 1.8% | 178% | |

The YoY gain shrank from +1.9 in April and from +3.1% in February.

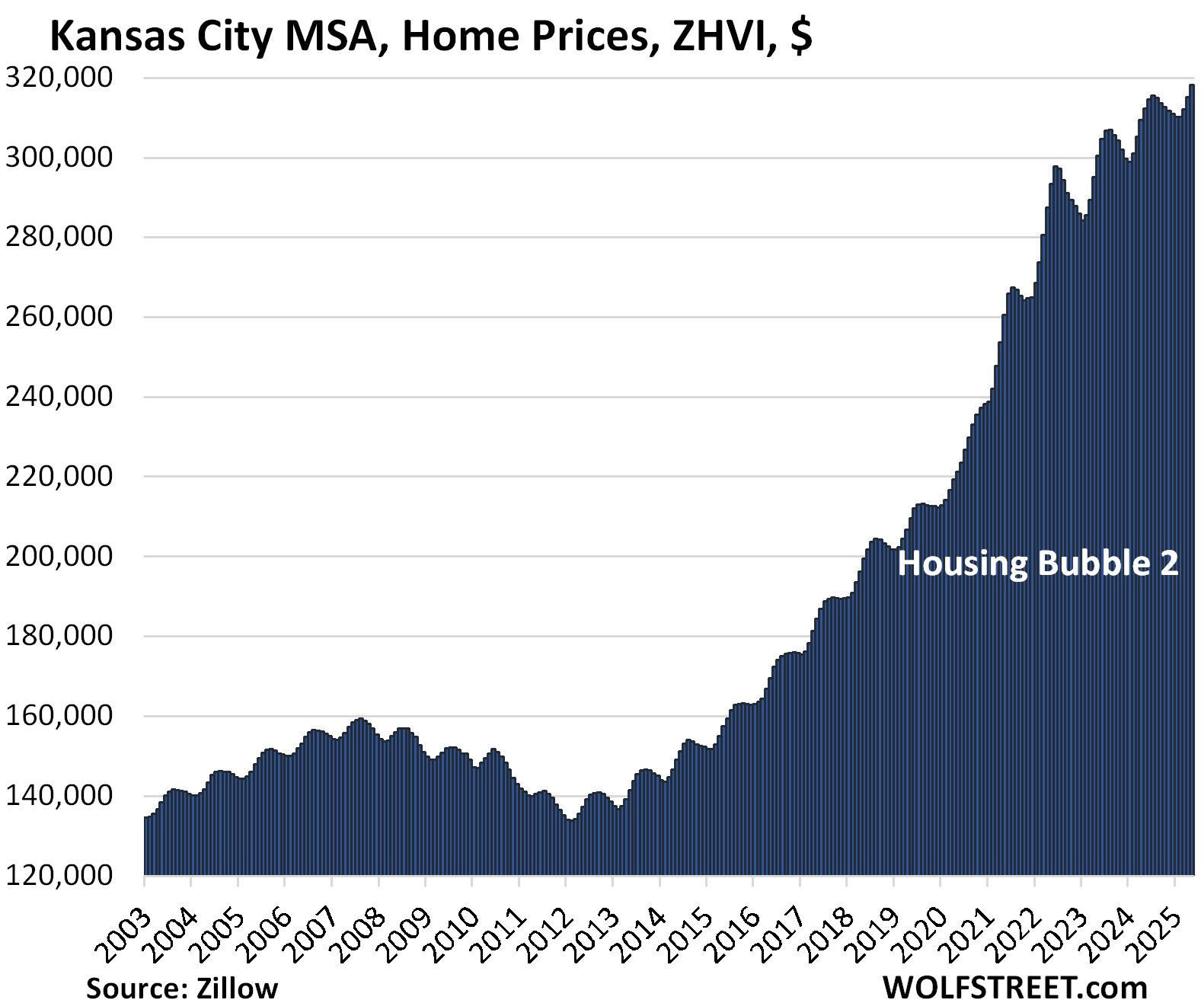

| Kansas City MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 1.0% | 1.9% | 182% |

The YoY increase was unchanged from April and down from +3.1% in February.

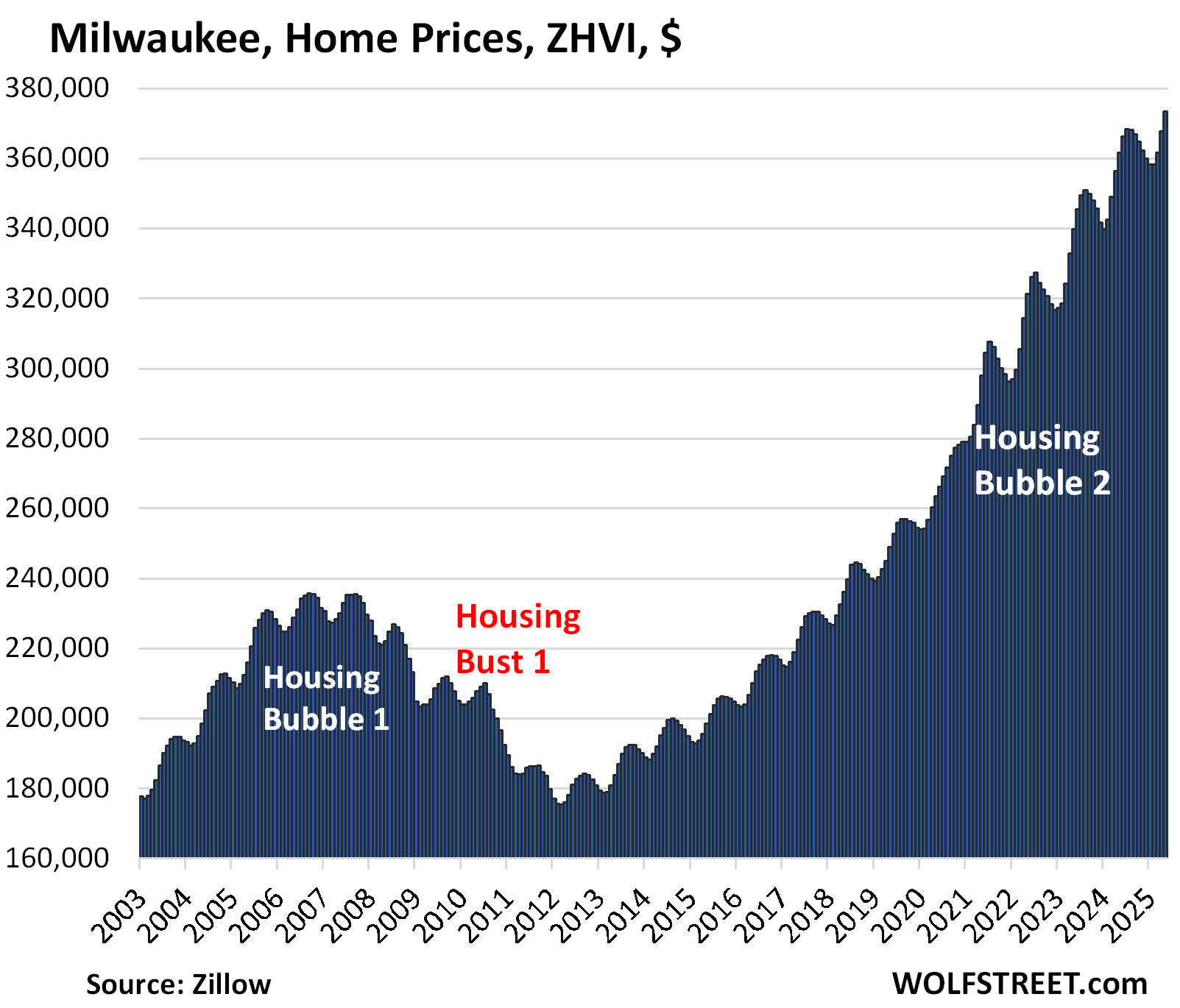

| Milwaukee MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 1.5% | 3.2% | 151.3% |

The YoY gain was unchanged from April and declined from +4.7% in February.

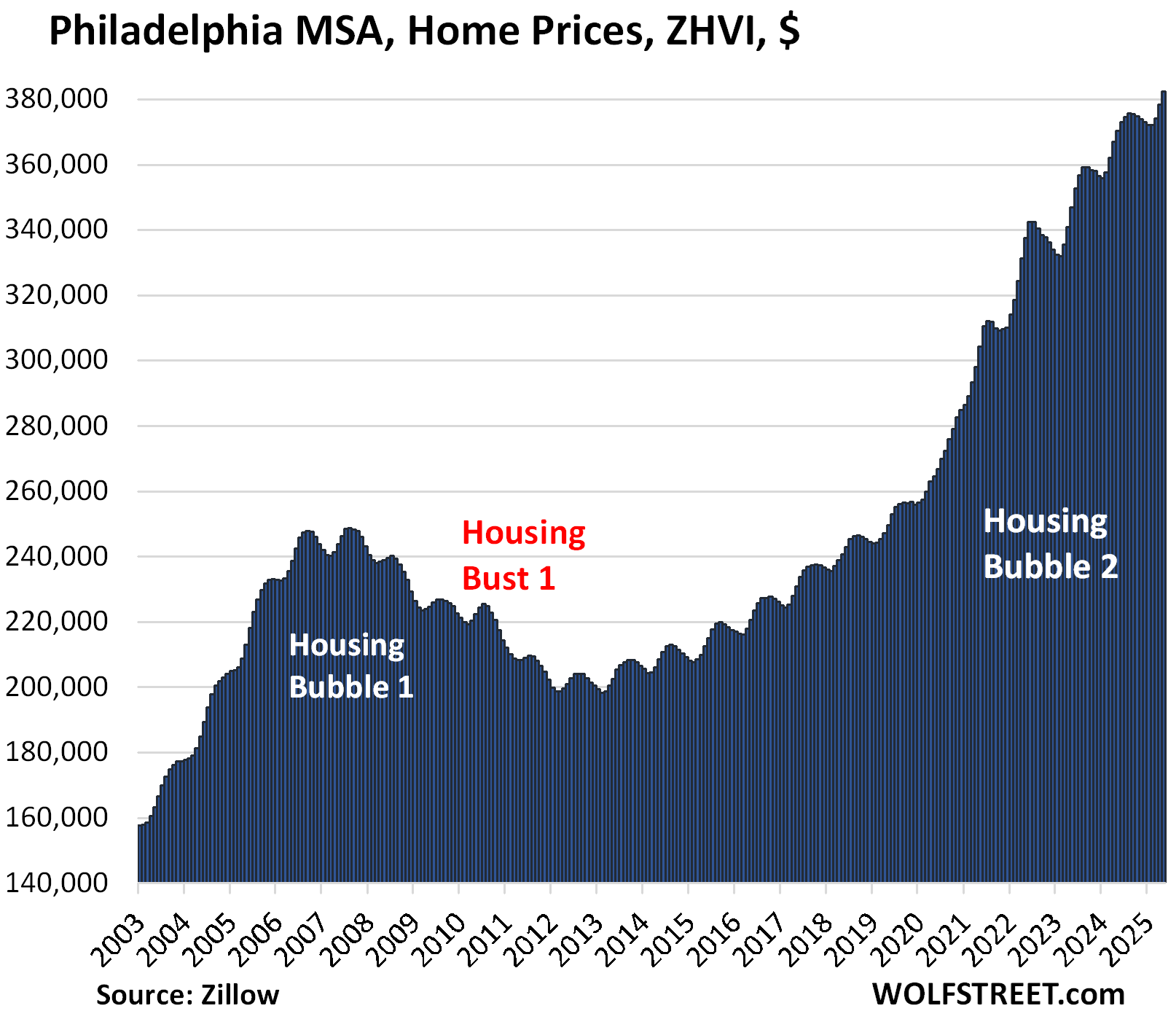

| Philadelphia MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 1.0% | 3.3% | 207% |

The YoY gain increased a hair from 3.1% in April but declined from +4.1% in February.

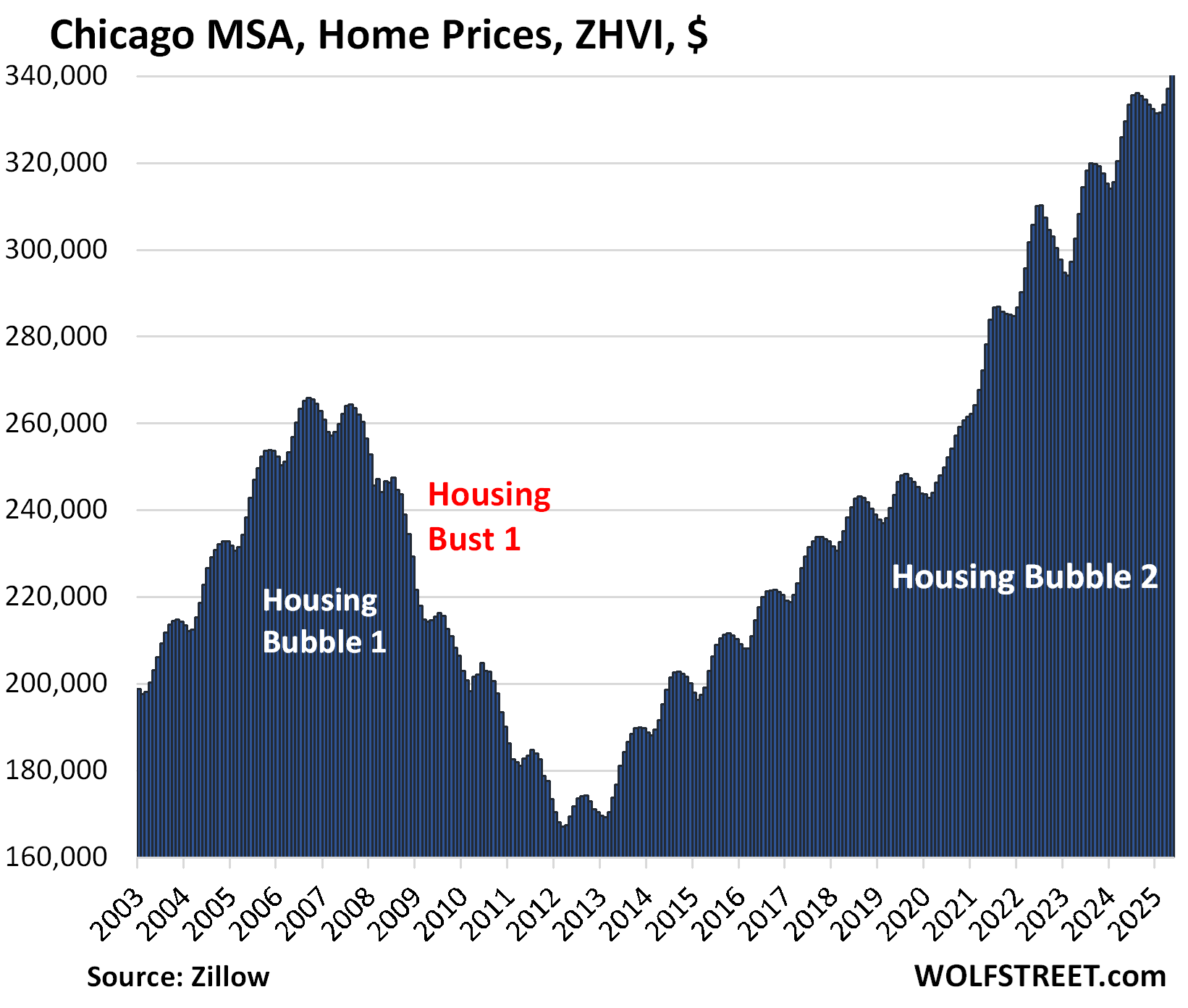

| Chicago MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 1.1% | 3.3% | 117% |

The YoY gain declined from +3.4% in April and +5.1% in February.

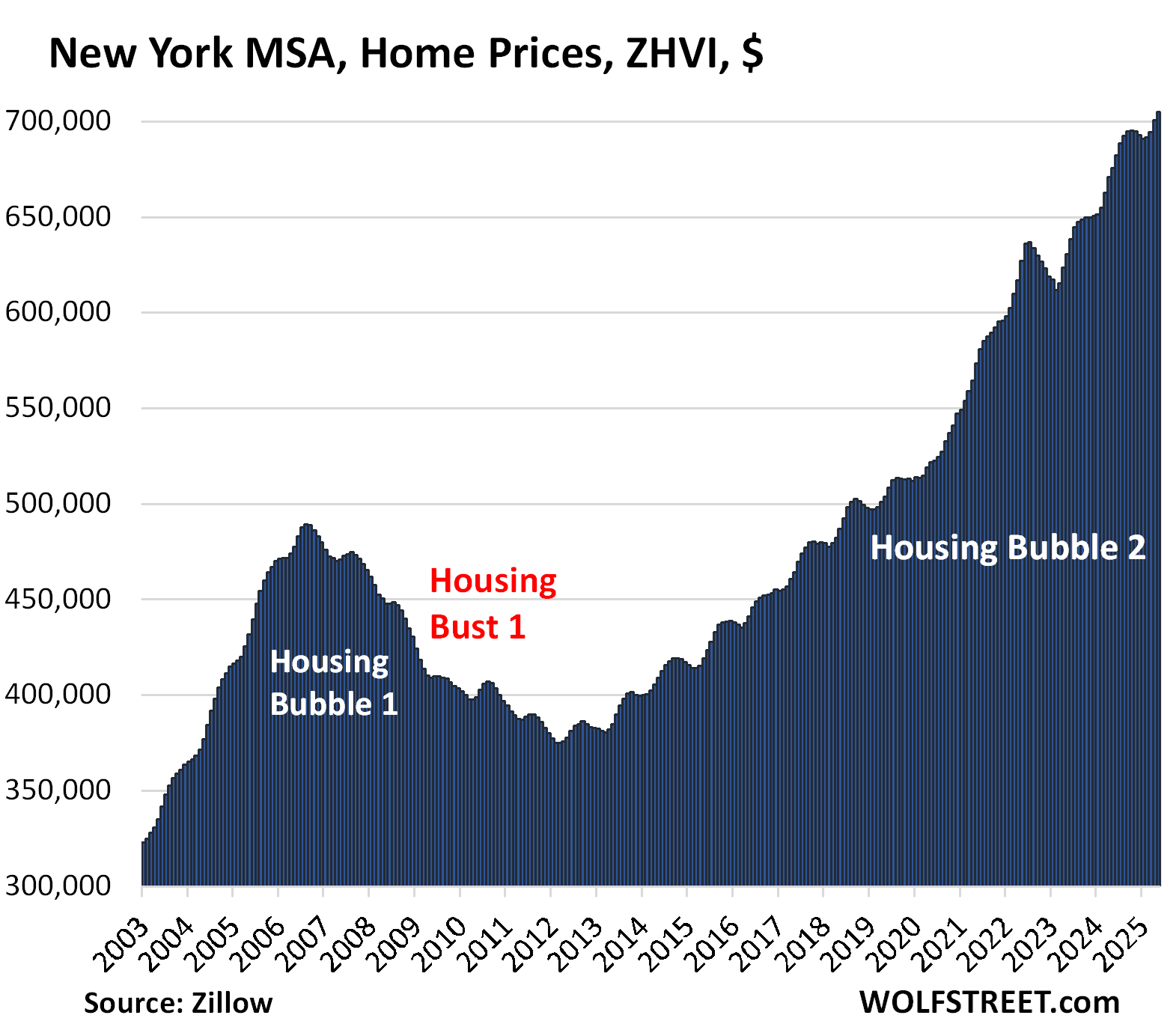

| New York MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.6% | 4.3% | 216% |

The YoY gain declined from +4.4% in March and +5.6% in February.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Everytime I see Austin’s chart and the resemblance to a ever growing middle finger is quite hilarious and fitting for all the sellers that are still asking and dreaming of 2022. Also a big F up to all the buyers that bought at the FOMO top.

On the other hand, at least the direction is looking good but the chart of LA is still painfully like looking at paint dry…in due time, can only hope for “It occurs first very slowly, then all at once” or give me something that resemble Austin’s chart please

From these charts, it looks like a bubble with some staying power to me.

“Bubble” yes, by definition. “Staying power” has already vanished in a bunch of markets. That’s what the charts are for, so you can see it market by market.

Housing Bubble 1 peaked in late 2006 early 2007, depending on locale, and bottomed out in 2012, roughly 6 years later. We are still in the early rounds of price declines. Though I do not anticipate as drastic a decline in prices, I also do not own a crystal ball.

“bottomed out in 2012, roughly 6 years later”

And perhaps did not return to 2005-2006 sales price numbers (at much lower transaction volumes) until perhaps 2017-2018.

The ZIRP-drunk, high-leverage residential real estate game can be a particularly harsh mistress if you time things wrong – or if you need liquidity in something less than 10-12 years…

How do we know we are not looking at just a relatively small drop in an essentially “CORNERED MARKET”?

By the top 1-5% (or less, including those with a lot of equity in PE and Corps)?

My richest relatives are all invested in PE, mostly work in DC or an agency/consulting outfit based there or close by, but the majority are rust belt poor and in a wide belt from Eastern Ohio to that area that was so flood damaged south of Sparta NC……but with plenty roads and towns named after their/our ancestors.

I’m sure they got some kind of BBQ set-ups working by now. For extended (yeah, and inbred, first cousins and 14 year olds are are both fair game) family gatherings. Did I say I saw duplex mobile homes in Sparta in the late 80s? Granpa worked at the shoe factory there in early 60s.

Po folk.

So, I bet I’m really closely related to VP Vance if his spiel is true (raised in exact same brand of religion, for sure).

Sure glad the old man road the rails out at 15, picked up a taste for CA, and dragged us out when I was 7 after he got out of the Army.

And yet nearly every other market is providing a middle finger to renters with prices ether stabilizing or continuing an upward trend when measuring the slop of the trend line over 5 years. Rates exploding from 3% to 7% in a year have only slowed the trend. At what point in this 15 year trend do we finally throw in the towel and just admit this is the norm?

Perhaps now, maybe insanity is the new norm unfortunately

@ Homless and free you should be happy that rent is going up by “just” 3% to 5% (fyl 3% to 5% is not “exploding’) since your landlord’s expenses are probably going up more than that. Wolf’s charts showing the price of buying a home today is getting a little lower but that has nothing to do with the operating expenses for current landlords. P.S. It is not just a 15 year “trend” most things have been getting more expensive for over 150 years. You might be able to move around to parts of the country where plants are closing to find sole low rents, but it is a good idea to admit that rent (and gas, cars, electricity and food) will keep going up in price.

My property taxes have gone up >20% in the last four years.

Great time to rent instead of own.

The lanlord’s fixed expenses are just a fraction of the rent costs, especially when amortized over all units owned. The five percent increase in fixed expenses is a much lower dollar figure than the 5% increase in rent. This comment seems disingenuous.

Based upon the near record low affordability index, there is plenty of room to roam to the downside.

Regarding the Housing Affordability Index (HAI) for single-family homes, there are reports that it has recently been near or at record lows, though the specific timeframe and exact numbers may vary depending on the data source:

Near Historic Lows: Some reports from early 2024 indicate that housing affordability remains near its lowest level in over a decade.

National Association of Realtors® (NAR) Perspective: The NAR reported that the Housing Affordability Index in July 2023 was at its lowest level in data going back to 1989.

California Specifics: While affordability remains low in California, the first quarter of 2025 saw a slight increase from late 2024.

@Desert Dweller you are correct that “Housing Affordability Index (HAI)” for homes has been high but so is the Car and Truck Affordability index (I just saw a $100K+ new truck at th TOYOTA dealer – $97K MSRP + ADM). The “average household” does not buy an “average home” or “average car or truck”. Wealthy people by $1mm+ homes and $100K+ cars abd trucks and poor people buy $100K homes and $10K cars and trucks. The trend I am seeing as a CA landlord is that more and more people don’t want do deal with “owning” a home (renters by choice) or “car” (rideshare by choice). With less and less people getting married and having kids less people “need” a classic suburban 3×2 ranch home with an an attached 2 car garage and a big back yard (that they need to take care of or pay a gardener $250/month to take care of).

Why buy a house when squatters can effectively steal it by changing the locks while you are away on a week long vacation? And I say “effectively” because the cops won’t remove them until you get a court date and “prove” that the counterfeit lease they hold using your signature that they forged from publicly available electronic county documents is fake.

Yep, more reason to have a monitored security system or at least internet surveillance cameras. As well as ask your neighbors to keep an eye on the house.

I know Florida and Colorado have tough laws against squatters and I suspect that is because of a lot of multi million dollar second homes and vacation homes in Aspen, Miami Beach, etc.

It’s a good thing most people don’t believe everything they read on the Internet. 65% of the people ignore those stories and buy a house anyway.

Watch the Youtube video by John Stossel, “Trespassers Welcome: How the Law Protects Squatters”. There are many, many news stories on this problem, including from local NBC, ABC, and CBS stattions.

1911 is the problem solver in that scenario…..,just saying.

Ummm put a house alarm with cell phone backup then call the popo immediately?

Evidence that this has happened, or is this some white male American anxiety? No one believes this actually happened.

Try googling “‘Squatter’ forged lease and sued homeowner: Queens DA” or “Squatters’ fraudulent lease schemes raise legal questions and criminal liability.” I don’t think it’s common, but it has happened.

So one case of identify theft and fraud and now the anxiety of homeowners has to be ramped up? This was a house that was going to be rented, and the squatter stayed for 3 months and will be on the hook for civil damages? This is having an effect on the housing market?? Please.

That’s funny. Your original comment demonstrated ignorance (“No one believes this actually happened”), laziness (“Evidence that this has happened”), and an animus towards white male Americans (“or is this some white male American anxiety”) and you choose to double down rather than admit an obvious error. Interesting choice. Do you think the squatter is good for civil damages? Please. There is also more than one case, I gave you searches for articles in both CA and NY.

@rojogrande

You did educate me on the dangers of squatters, and how they are coming for everyone’s homes. Thank you.

So how can we prevent and solve this issue? Maybe fund housing courts better?

@Kurtismayfield,

Give preferential rights to property owners, and in the event they evict someone unlawfully, the evicted party to initiate a lawsuit against the owner. The courts are there to resolve such issues, but the rights of property owners should supercede the rights of tenants, by default.

Kurtismayfield,

I think state and local authorities need to be more proactive in helping owners reclaim their property. Maybe unlawful detainer laws need to be changed. I don’t think squatting is a huge problem, but I remember seeing it reported in many parts of the country particularly during the lockdowns because it was so hard to get courts involved and kick squatters out.

From a rental property ownership perspective, I think the bigger issue is possible rent moratoriums. Owners can probably figure out which states to avoid if they fear that issue for the future. I think you’re right squatters are not a big enough issue to move the housing market, but it’s unfortunate if you’re the unlucky property owner stuck with one.

Testifying that it happened to a friend in 2011: He called sheriff and was told they wouldn’t do anything without a warrant, so he let it go to foreclosure.

He wanted to go there with his 1911, but the sheriff also told him HE would go to jail if he shot anyone.

Guys who bought it out of foreclosure paid the friend to relinquish ALL rights a couple years later.

Southern state where he still lives, so not naming names.

Happened with a house we were working

On. Squatters were arrested for trespassing. At least in my little slice of flyover common sense still prevails.

You would not be so lucky in California, although there *is* a loophole in California to treat these squatters as trespassers. You can pre-register a “Trespass arrest authorization” with your local California police department, which has to be renewed every 12 months. This allows police to remove anyone on the spot. Getting this authorization after the fact won’t help you, since without this authorization, police in California will usually err on the side of doing nothing.

If you don’t lock it you don’t own it.

@Wolf – Does your Seattle chart include other nearby areas too like Seattle Eastside i.e. Bellevue, Redmond, Kirkland and Issaquah ?

Btw, Seattle is well known, but has a lot of drugggs, homelesssnes, an overly sensitive culture and a tendency to increasingly tax companies. People with families seem to prefer the eastside (and parts north or south of it). So, it would be nice to consider all these regions in seattl or list them separately as seattle eastside in your charts.

The dichotomy is just like san francisco vs the peninsula or eastside (fremont etc).

Thanks !

LOL, caught another one that didn’t read the article and just wants to use this opportunity to spread BS about big cities.

What does it say in the article a gazillion times??? These are all MSAs. And the article explains what that acronym means.

The Seattle MSA is called officially the Seattle–Tacoma–Bellevue, WA MSA and consists of the three counties King, Pierce, and Snohomish, which shoots your silly theory right out of the water.

That peak in 2022 is an outlier. Ignoring the outlier it appears that most of the cities housing prices over the past five years are flat or edging up slowly. Why is this? Sellers are still pricing for gains, there is no anxiety to rush for the exits. However, the buyers are on strike, hence the low turnover. The churn is people selling because they have to, death, divorce etc. etc. etc. This state of affairs may continue for a long time until some outside force causes a change of direction.

In June 2008, a certain Sea Captain came around and said the same thing about Phoenix for example, “look, 2005 and 2006 were just outliers, and if you look at 2004, prices are flat or edging up slowly. Why is this? Sellers are still pricing for gains, there is no anxiety to rush for the exits.”

And then look what happened between 2008 and 2012 (third chart from the top). Prices fell into a bottomless pit.

Wolf was your site around back in 2008? Did this captain commented on here or just generalization of the housing cheerleaders sentiment?

I’d say: Buckle up. The flight has just started and it has long way to go OR this time is different.

The housing un affordability is historically low because of ZIRP and FED’s policies.

I may be wrong, but I see big down turn coming.

Some once hot markets like Austin and SFO are down more than 20% from their peaks and still going down.

Although, real estate is local but all of USA markets benefitted from cheap money and now cheap money is gone.

The question is when does, or will, “Housing Bust 2” make an appearance?

During Housing Bust 1 not only did “total checkable deposits” (reservable liabilities) not increase for 4 consecutive years, but the “demand for money” (cash balances) skyrocketed causing velocity to plummet (or a flight to safety).

During the GFC Bernanke caused 1/2 of the homebuilders to go bankrupt creating a “new residential construction” shortage for years.

These unusual events are likely to limit any Housing Bust #2.

If you are a reader of WR articles, he has been documenting the Housing Bust 2 in his articles.

Some once hot markets like Austin and SFO are down more than 20% from their peaks and still going down.

Although, real estate is local but all of USA markets benefitted from cheap money and now cheap money is gone.

People with vested interests are saying the impact would be limited. Then I dare ask them what happened to these once super hot markets.

This downturn is despite the strong job market.

These charts should be plotted with the idiocy of QE and ZIRP by the Fed starting in 2007. They are the real reason behind the insane asset price increases. But of course the financial media will never focus on the real culprit. They did the same thing in the seventies. Have lived thru both debacles and they will never change. Powell needs to put on some Volcker big boy pants and stay the course.

Well said Alan!

Volcker’s reign was a myth. Paul Volcker was quoted in the WSJ in 1983 that the Fed: “as a matter of principle favors payment of interest on all reserve balances” … “on rounds of equity”. [sic]

Wolf has repeatedly remarked on “interest rate suppression”.

Bernanke’s “wealth effect” doesn’t work. Link: “Changes in Wealth and the Velocity of Money”.

Changes in Wealth and the Velocity of Money (stlouisfed.org)

Bernanke’s “wealth effect” creating the highest GINI coefficient in decades.

Yes, QE was a terrible idea and I’m very glad those days are now gone. Hopefully they learned from that era and are not stupid enough to bring it back.

Bernanke, pg. 287, “Lower long-term rates also tend to raise asset prices, including house and stock prices, which, by making people feel wealthier, tends to stimulate consumer spending-the “wealth effect”.

Seems like the most likely path to get housing market moving again in the next year or perhaps two is mortgage rate declines, which would be influenced by perhaps 150-200 point cut in Fed rate. That of course is possible but not desired by most and could easily see assets increase again and perhaps a significant increase in things like gold. Seems likely some sort of mini victory will be declared with inflation that is true by most charts but hardly in the eyes of the consumer.

Getting more involved in an already escalating Middle East conflict is hardly going to help anything other than defense stocks. Certainly not going to favor the deficit and perhaps those who buy treasuries will have a conscious with what they purchase but unlikely.

The last 100 bps rate cuts didn’t help lower mortgage rates. I am not sure the next 100-150bps will either?

If mortgage rates fall by 100-200 bps, the question is why?

If the answer is economically driven, why would people (unsure about that economic driver) suddenly come out of the woodwork to drastically overpay for shelter?

I see a continual uptrend in van life. Permanent renters and only lower prices, or substantial time lapsing to thaw this housing market.

In May 2025, Carson City had 44 sales of existing single-family homes, a 10.2% decrease from the previous month and from last year.

The median sales price for existing single-family homes was $585,000, an increase of 12.9% from the previous month and an increase of 6.8% from the previous year.

The active inventory in May 2025 was 98, an increase of 42% from last month and a decrease of 3% from last year.

In May 2025, Douglas County had 50 sales of existing single-family homes, an decrease of 35.1% from the previous month and a decrease of 12.3% from last year.

The median sales price for an existing single-family residence was $714,294, an increase of 4% from the previous month and an increase of 2% from last year.

In May 2025, Storey County had 4 sales of existing single-family homes, a decrease of 33.3% from the previous month and from last year.

The median sales price for existing single-family homes was $622,000, an increase of 27% from the previous month and an increase of 13.1% from last year.

Please note that sales numbers in Carson City, Churchill, Douglas, Storey and Washoe (excluding Incline Village) are for existing stick-built, single-family dwellings, and do not include manufactured, modular or newly constructed homes unless otherwise stated.

Californians still moving to Nevada. This article was posted today by Sierra Nevada Realtors.

“This article was posted today by Sierra Nevada Realtors.” :-)

This should be the first line in your comment to save me reading the whole comments.

LOL That is a good point. A few times leaving Costco four or five cars in front of me all have Cali plates. Maybe Wolf will let me post it upside down.

@NV Raider The Carson City Costco is the closest Costco to South Lake Tahoe so that is where everyone goes to get Paper Towels and TP for STRs (and they fill up with gas since gas in NV is often half as much as gas in the Tahoe Basin). I just looked at Gas Buddy and with CA prices down from ski season regular is $5.69 at the SLT Chevron and $3.54 at the Carson City Costco…

@Apartmentinvestor This is the Costco in Sparks. Most of my new neighbors from the last several years are all from California. One from Texas.