After inflation, “real” yields on money-market funds are near 2%, and households kept pouring cash into them. But CDs lost ground.

By Wolf Richter for WOLF STREET.

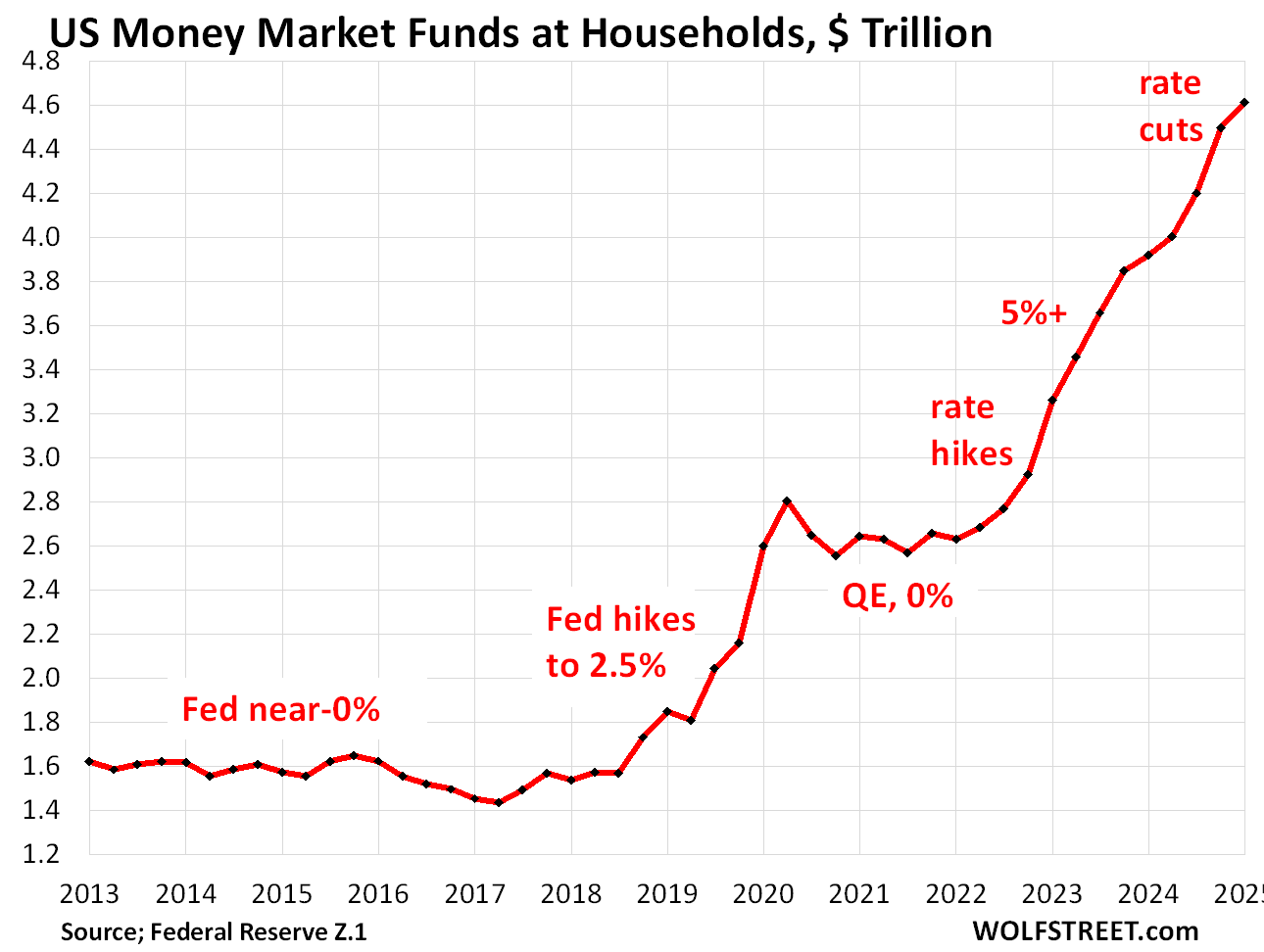

Balances in money-market funds held by households at the end of Q1 continued their massive surge and rose by another $115 billion from the prior quarter, to $4.62 trillion, and were up by $696 billion year-over-year, according to the Fed’s quarterly Z1 Financial Accounts today. Since Q1 2022, when the Fed started hiking its policy rates, balances have surged by $1.99 trillion.

The three-month Treasury yield is still at 4.36% currently, and has been in this range since the last rate cut in December. Yields of money-market funds (MMFs) closely track the three-month Treasury yield and remain in the 4.2% range, give or take, and are well above the current inflation rates, with CPI inflation at 2.4% in May. This puts the “real” yield on liquid ultra-low-risk cash at just under 2%, which seems to be an attractive proposition, and households keep pouring their extra cash into them.

These MMF balances include retail MMFs that households buy directly from their broker or bank, and institutional MMFs that households hold indirectly through their employers, trustees, and fiduciaries who buy those funds on behalf of their clients, employees, or owners.

MMFs invest in safe short-term instruments, such as Treasury securities with less than one year to run, much of it with less than six months to run, in high-grade commercial paper, in high-grade asset-backed commercial paper, in repos in the repo market, and in repos with the Fed.

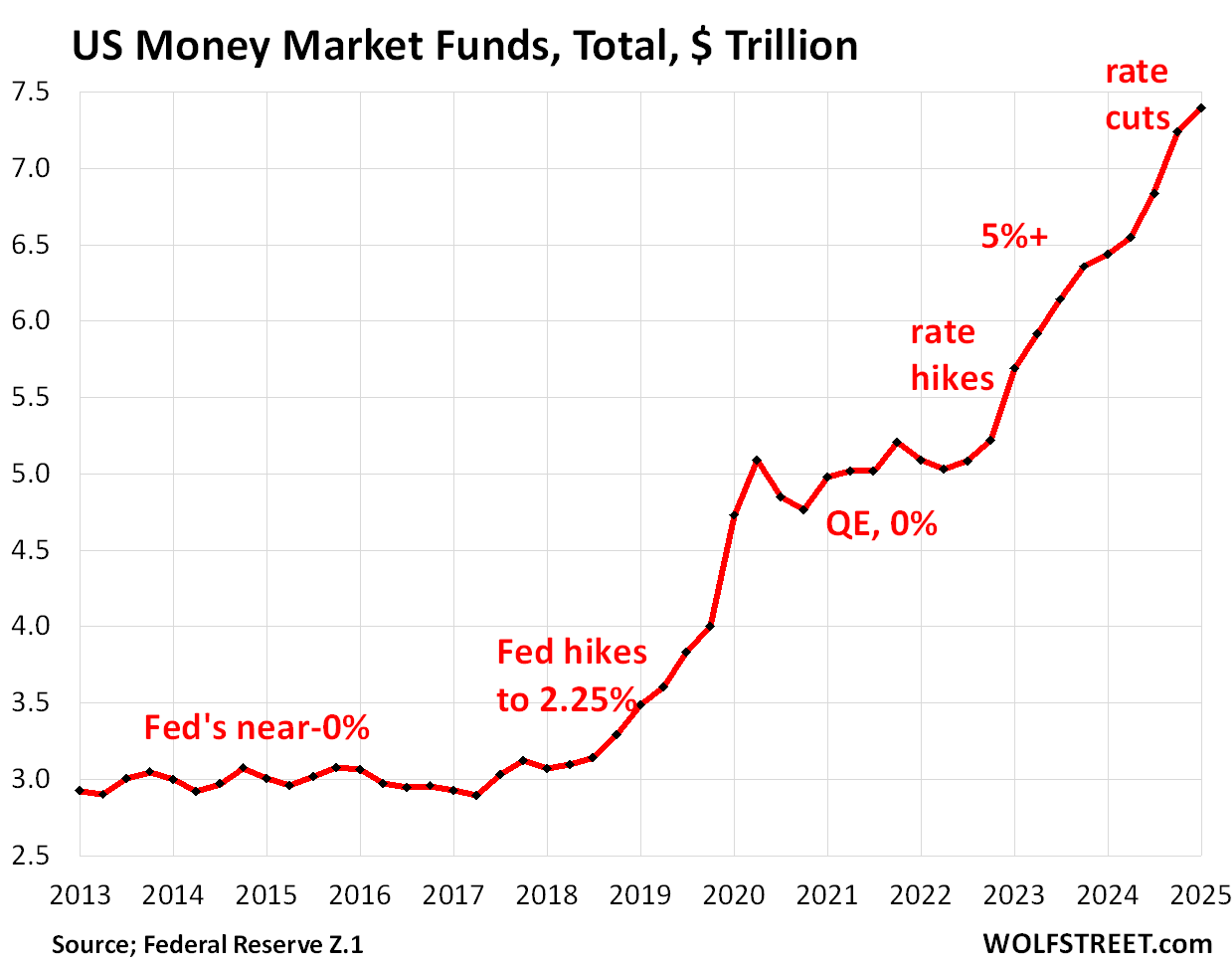

Total MMFs (those held by households and institutions) rose by $155 billion in Q1 from Q4, and by $957 billion year-over-year to $7.40 trillion. Since Q1 2022, balances have ballooned by $2.31 trillion.

MMF balances balloon with higher interest rates. When rates were near 0%, balances remained roughly stable for years at about $3 trillion. There is always some need for liquid cash even if it doesn’t yield anything. When the Fed hiked rates in 2017-2018, to ultimately 2.25%, $2 trillion of cash poured into MMFs. When yields started rising again in 2022 after the pandemic-era interest-rate repression by the Fed, MMFs ballooned by another $2.3 trillion. Higher yields bring a tsunami of cash to money-market funds.

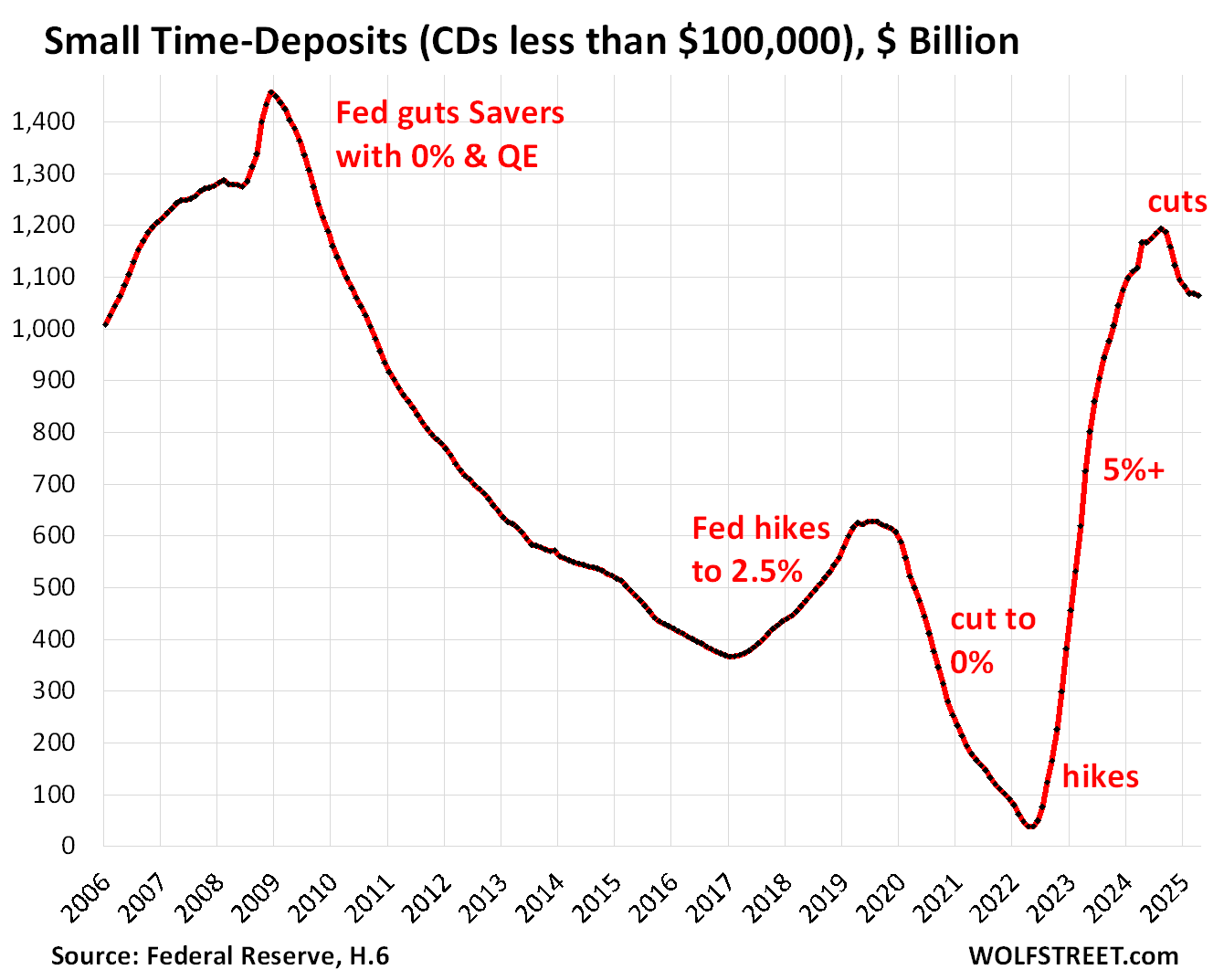

Small Time-Deposits (CDs of less than $100,000) have remained essentially unchanged at $1.06 trillion over the three months through April, after dropping from their highs in August 2024 of $1.19 trillion, according to the Fed’s latest Money Stock Measures.

But note the explosion of those balances as the Fed started hiking its policy rates: they went from near-zero in April 2022 to $1.19 trillion in August 2024.

These small CDs reflect regular savers. When the Fed gutted savers’ cash flow from savings in 2008, they began spurning CDs, and by mid-2022, small CDs had nearly vanished.

Banks only pay interest if they have to. For banks, deposits are loans from customers that form the banks’ primary funding. Paying higher interest rates on deposits increases a bank’s cost of funding, and lowers their net interest margin (net interest income minus the interest paid depositors and other sources of funding). So they offer higher rates only if they have to attract new deposits or retain deposits from existing customers. Bank accounts that provide essential services, such as transaction accounts, attract cash at near 0% because customers need those services.

Banks rely on deposits being generally “sticky,” especially in transaction accounts, and they expect when rates rise, that a big portion of deposits stays put even with near-0% rates. But as we can see in the CD charts here, CDs are not sticky, and they include brokered CDs sold through a brokerage firm; they’re like hot money that can leave at the end of the term if rates are too low.

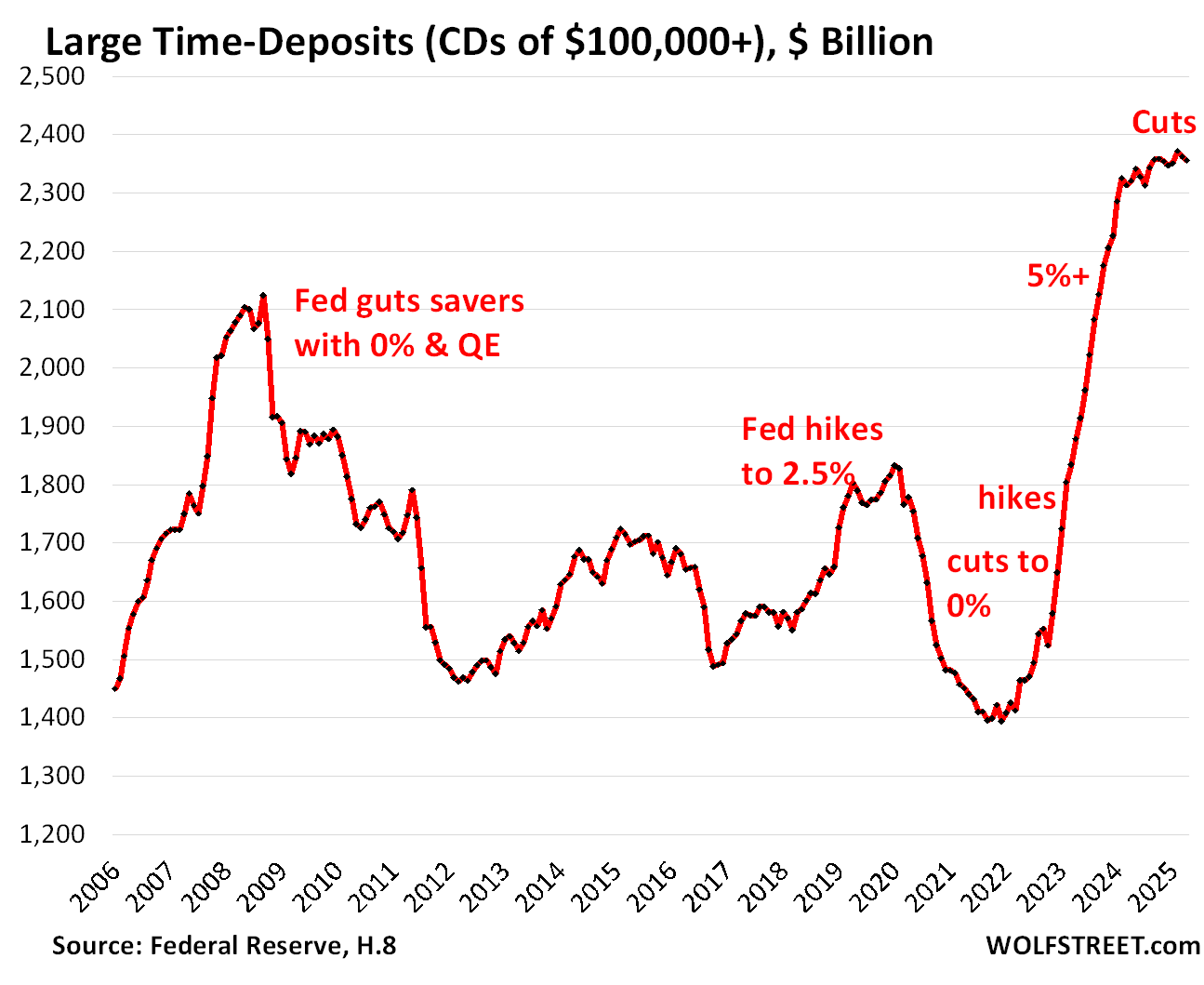

Large Time-Deposits (CDs of $100,000 or more) ticked down a hair over the past two months to $2.36 trillion in April, from the record in February, according to the Fed’s monthly banking data.

Since March 2022, when the rate hikes began, large time-deposits have surged by $943 billion.

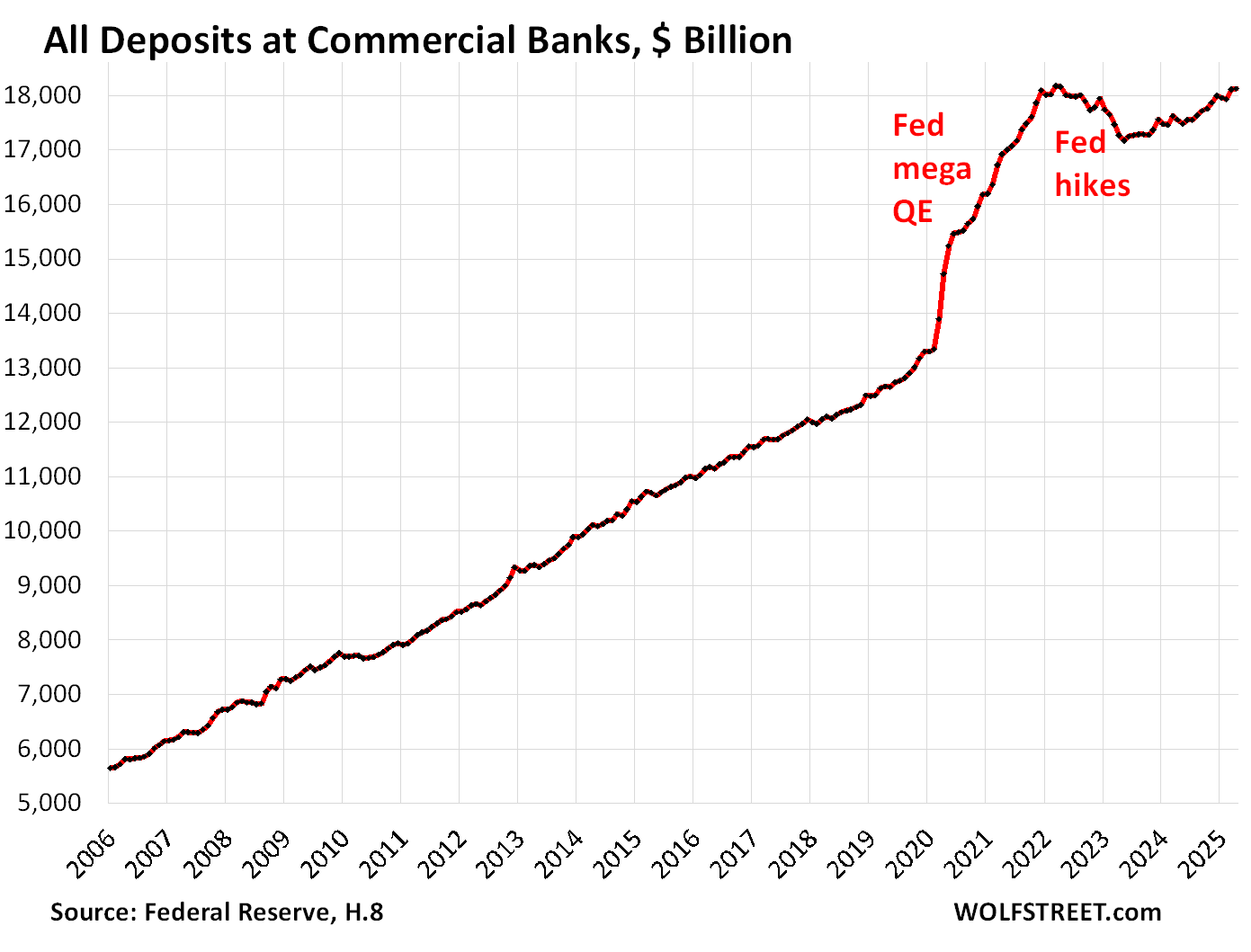

But CDs are only a small part of bank deposits. Total deposits at commercial banks are currently at $18.1 trillion, back where they’d been before the rate hikes. But they did drop by about $1 trillion from early 2022 through early 2023 as competing interest rates rose, and customers yanked their cash out. Higher deposits rates by banks then stopped the outflow and brough the cash back in.

As total deposits dropped by $1 trillion between early 2022 and early 2023, CD balances soared by $2 trillion during that time. What this means is that banks lost about $3 trillion in deposits in saving accounts and transaction accounts during that time.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Current situations make it really difficult to figure out where to diversify and out fixed income part of portfolio and how much. Are tariff policies stabilized enough, will the One BBB pass as defined, is inflation coming under control, how much will international events create instability, will the Fed cut rates later this year and next? I suppose it has always been like this but as I move closer to retirement the decisions seem more important. Pretty sure if the 10 year got to 5% again I might go for it with a decent chunk.

…broughT the cash back in.

any mm investor who depends on the current EFFR could drop one place in on the class ladder if said rate were halved, for instance. dont want to bore you with the numbers, a million earns 45000 a year, if thats all you have you go from middle to lower class. if you have a bloated pension its a slightly different story, those will take longer to deflate. but one really big rate cut changes the earnings power of a lot of average Americans. and thats TAXABLE income, so government has to make adjustments too.

“It compounds as well”

Benjamin Franklin

You have absolutely no idea what “lower class” is like in America if you think someone with a million dollars would be lower class because of interest income.

…If that’s all you have to live on, $45k (not inflation adjusted over time) is lower class. It’s minimum wage at McDonald’s in California. Yeah, at some point in your retirement you can amortize it and boost your payout, but $45k is lower class, which I believe the post was saying.

Depends where you are. In some places in the US, $45k lets you live quite nicely. But in expensive places, it’s well below the poverty level.

I think he’s saying you’d still have $1m. Not just the $45k in interest.

Like Wolf said, 45K/year in some parts of this great country, you could live nicely. Honestly, I wouldn’t want to go there…..

However, if you are 65 with 1M, you could pull 40k from the principle each year and live off 80K per year nicely most anywhere with a paid off house.

That would get you to 90. Honestly, I’ve seen many 90 yo being fed jello. I’d be ready to go. OK, I realize some are still climbing hills and quite sharp so this is a tough question.

My bank was paying decent (ish) rates and then they fell quite a bit over the last year, so as they came out for renewal, I asked them what they could do. Nothing of course “these are our rates”

fine, took it all out, it’s now in treasury bills doing better than their rates before taxes. It wasn’t millions, but it wasn’t trivial. (and it’s a small local/regional bank). So be it, they get nothing.

The banks hate this 1 trick!

Yeah, in zero days I didn’t care and just kept my spending money in the checking account. Now I take 3 months out of my retirement account, put it in monthly T-bills and spend 1/3 each month as they mature, rinse and repeat. It’s not a huge deal but it’s an extra, “free” dinner with my girlfriend.

That’s the difference between a bank and the system. From the standpoint of the system saver-holders never transfer their funds outside the system unless they hoard currency or convert to other national currencies.

The pressure is on to lower rates – renew “financial repression”. Weather its the data or TDS, the FED resists or perhaps is not certain they can get away with it again, but it seems inevitable that they will try again at some point. But, perhaps Powell will hang tough and surprise everyone.

Whats the best index to judging USD strength ?

Lets see to what degree USD is still the safe haven refuge in time of war ?

No, our 10-month rate-of-change in our “means-of-payment” money supply is still positive. We’d have to have a “Black Swan” for things to change.

I would like to know who holds the MM funds. How much is NOT the top 1% or 10%.

Seems like extra spending income if you are retired living on interest. How much of a boost to spending is this.

I just received my beautiful “Wolfstreet” mug.

It will proudly be displayed in my curio!

Thank you for all that you do for us!!

🍺 Cheers!!

Banks are not your friend. I keep only enough money to pay my monthly bills in my banks. Bank CD’s all have draconian early withdrawal penalties, the least draconian is you lose three month interest on CD’s less than one year. They tend to hide these early withdrawal penalties, usually not even mentioning them on their web sites.

I am not sure why people bother with banks (other than to have cash to pay bills) when 1, 2, and 3 month T-bills pay around 4.3%. They are completely liquid, no commissions to buy or sell with most brokers, no early withdrawal penalties, and no state income tax on interest.

I agree 👍

Because banks are FDIC insured is a huge reason. Yes, even thought T-Bills are safer, pay more, are liquid and more tax efficient if you live in a state that has income taxes. People rather get an FDIC account. There will be people that will read these comments. Maybe do their own research after reading this that confirms what we are saying, to then proceed and renew their CD instead of bothering with T-Bills. I work in the industry.

I think the hassle of buying t-bills and other instruments through Treasury Direct, and the perceived risk of not being able to access that money should the government decide to flag your account for some reason, also cannot be ignored.

Having $100k in the bank is one thing, but having $100k in a government account that is accessed through a user-unfriendly website is another. Treasury Direct crashed a couple of times when the i-bond variable interest rate shot through the roof a while back, and people had a rough time getting through.

When Treasury Direct has an issue, its a major hassle getting support. I feel this is a non-trivial barrier to some retail investors.

Do not use Treasury Direct. Treasury Direct sucks. Use a broker like Schwab or Fidelity (no commission for T-bills, buy and sell whenever you want). I use Schwab and can easily contact a representative by phone day or night. I only use Treasury Direct for buying I-bonds, because I have no other choice.

Treasury Direct works fine. Brokers work fine. They serve different purposes. You cannot trade in Treasury Direct. You trade in your brokerage account.

I find TD reasonable to use. Never had an issue over 4 years now. It is not a ‘new and shiny’ interface, but works fine for me. Just have to read and follow the instructions, which are hard for some.

What is the difference in yield [after management expense] for a short-term treasury ETF (Schwab) vs buying a similar-duration treasury from Treasury Direct?

Correct. That’s why many of us diversify the “low risk” side of our portfolios by increasing both MMF and T-bills during uncertain times…

In fact, just took some of that gain in RTX and will buy more T-bills…

I use Lending Club bank savings account but only as an in and out to treasuries plus ensuring have a little extra liquidity. Currently 4.4% which is pretty solid rate. Still hang with treasuries to avoid giving California a cut of the action.

I think they are liquid because the fed demands they are.

If you sell you do prob lose any interest.

It’s not like if a treasury matures in a year and you sell 1 day after buying, that you will gain. And perhaps if rates just increased they may be worth even less than on the day you bought them.

Curious how it works when say a large company like Berkshire ever needed to sell billions of them to purchase a large stake in a Corp. or do they just do a trade? Treasuries for stock.

You don’t lose any interest if you sell. T-bills do not suffer the volatility of longer term bonds. Many consider them to be almost cash, cash which earns 4.3% free of state income tax.

Well I just opened a 100k CD 4.5 percent after selling MIL estate house at my bank. Why? the process took 2 min at a grocery store kiosk local bank I use. Monthly deposits into my checking there . The number of seniors that are internet impaired is very high . If one did not work (my wife) while we moved 20 times in my working career the internet passwords resets registering 2 levels of security constant reboots and lack of financial knowledge all play a part. Having a local bank is very valuable in my opinion. Even if the bank is a Major bank the local branches have to take care of the elderly. I consider myself to be pretty decent on old technology but my skills are deteriorating rapidly with age. Dementia Parkinson’s cancer diabetes physically impaired taking care of a spouse etc all play a part . I have had grandchildren for the last week with no time to myself . As I type this my 3 year old granddaughter is complaining lots of reasons to not be perfect on rates. Go MMFs and Wolf thanks

Bs ini,

Of course, if you lack the capability to use the internet, and like waiting in lines, then you should use a nearby bank branch.

A narrative floating on the info highway, is that the longterm impact of high deficits, tariffs and general inflation, with a lower dollar, will greatly erode the future value of cash sitting in these money mkt funds (as well as standard US index funds).

That narrative, of course, is linked to the concept of diversifying into foreign mkt index funds, which “they” claim will benefit from the outflow of funds that are sloshing back to their homelands.

I’m in a money mkt and have been looking into Real future returns — and wondering about how a devalued dollar might erode my future cash flow — and this isn’t easy to figure out!

If your mm is chugging along around 3% and dollar falls 20% that’s not a good outcome — but, how safe are future returns elsewhere???

The goal of yield investments, such as MMFs or bonds, is to be compensated with yield for the erosion of the purchasing power = positive real yield. So if for instance, the short-term risk-free yield is 4.2% and current inflation is 2.5%, your real yield is positive, and you are currently compensated for the erosion of purchasing power.

MMFs are short-term. If inflation surges (increased pace of erosion of the dollar’s purchasing power), and yields surge, as they usually do when inflation takes off, you can decide whether you want to get out of your MMFs (you don’t lose your principal when you sell amid surging yields, unlike long-term bonds), or hang on to them if you believe that yields will stay ahead of inflation (but the may not).

The erosion of the purchasing power of the dollar affects all dollar-assets equally. So you try to buy assets that either compensate you with yield for the erosion, or compensate you with capital gains for the erosion. There is no guarantee that asset prices rise with inflation. You can have – and we did have during the housing bust and during the dotcom bust and during the gold bust – falling asset prices AND inflation, which compounded the loss during those years.

All I can say is, it’s about time. Savers should be rewarded. Real money has been transferred from savers to borrowers for way too long. A dollar earned through labor today should have the same value 10 years from now or 100 years from now.

Bingo!

I’d argue that since 1971, the financial system and associated laws have been changing to reward bad behavior. For example, Glass-Steagall was put in place after the Great Depression to separate the banking side of the house from the investing/gambling side of the house. That was undone by a republican congress and Clinton, etc. Looks like we are being set up for war to hide the monetary and fiscal failures/theft.

Same as it ever was.

There should be high enough real rates of interest for saver-holders so as to thwart asset bubbles.

It is much more desirable to promote prosperity by inducing a smoother and continuous flow of monetary savings into real investment outlets than to rely, as we have done since 1965 on a vast expansion of commercial and Reserve bank credit to stimulate production.

In my world, the yield that matters is the after-tax, after inflation yield on my savings.

4.2% on a T-Bill or MMF only looks ok if I forget about the taxes.

Sadky, my after-tax savings are not gaining on my after-inflation cost of living.

Everyone wants lower rates, but hoping and wishing will not bring them down. Given our ever expanding debt that is now becoming hard to afford, rates are more likely in my opinion to go up for a couple of reasons.

First the president is ticking off a lot of our allies, and it’s no secret that some are selling US assets and repatriating their proceeds to deploy elsewhere. Let’s not forget all of the drama over the budget fights which are coming to a head.

Even if it passes with little drama, a lot of bond investors are not going to like what it does to our finances. Then there is the old axiom that greater risk demands greater reward. Clearly both political and financial risk are increasing. Meanwhile, commercial real estate is under a lot of pressure to include retail, office, and even multifamily. Lastly, supply is about to go up significantly, and supply and demand have not gone out of style. I think the 10-year will be priced to yield around 5% by the end of the year, and perhaps sooner.

All Treasuries of all durations were over 5% for a few days less than a year ago. 20 year bonds are very close to 5% now.

The way to lower policy rates is to follow a tighter monetary policy. That’s what Powell is doing.

Desert Dweller,

I think most governments make decisions that are in their best interests, US currently excluded. They will keep buying treasuries if the math works, and that seems to be the case with their purchases and current yields. I think rates could fall and they would continue to be bought up. Not suggesting this will hold the rest of time but countries pivoting away from the dollar will be slow.

Hopefully we can limit our involvement in the war in the Middle East but they will clearly add more to the deficit.

And yet the 30 year auction was great

Do MMF include High Yield Savings Accounts?

No, they’re included in total deposits, last chart.

I am in the lower and then higher by year end. Powel is in a very problematic spot at the moment. Stagflation is the most likely scenario.

wolf,

Why does some leaders keep saying 50% of Americans do not even have $400 as savings? I feel we underplay the wealth of this nation. What is your view?

No one other than the clickbait media says that. They’re citing reports that define how people pay for something. Most people don’t even have “savings” accounts. They may have $1 million in a 401k, and they have a brokerage account, and they have checking accounts, and credit cards. When they need a $400 repair, they don’t pay it out of “savings,” but with a credit card, and by due date they pay off the entire credit card balance out of their checking account, but the media idiots never put that in the title, they put that way down in the article, and all people ever read is this bullshit about American’s not having $400 in “savings” for emergency repairs.

And when they have bigger cash needs, such as a three-month job loss, they end up selling some assets.

I sorted through this here:

https://wolfstreet.com/2023/05/27/americans-ability-to-pay-for-emergency-expenses-or-three-month-job-loss-with-cash-or-cash-equivalent-by-selling-assets-by-borrowing-or-not-at-all/

Bottom line; RISK is being repriced globally.

Hedge accordingly.

These are big numbers. Is it to early to ask, what comes after Trillions?

I believe Ounces comes after Trillions.

Am I reading the article correctly by thinking that there is a total of around $29 trillion of cash in all of the savings?

Total bank deposits (last chart) include savings, CDs, and transaction accounts, such as by big companies that need hundreds of millions of dollars in their payroll accounts every time they make payroll. That’s the last chart, $18 trillion, it includes ALL deposits, including CDs (charts #3 and 4).

Then there is $7 trillion in total money market accounts.

Thanks, then $25 trillion is hard to imagine as ready cash. But there it is in black and white.

A lot of this cash is in constant flux from account to account and is not just sitting there. It may sit in a payroll account for one day and then get spread to 20,000 employees, and then get spread from there to pay for credit card statement balances, mortgages, groceries, cars, etc., and spread from there via these companies to other companies and payroll accounts….

Too bad the government can’t use a wealth tax to help pay off some treasury debt. Do people really need all that money in their CD’s and MMF’s? Maybe they are saving it for retirement or to give to their kids. But if the government can’t handle it’s debt what kind of country are they leaving their kids?

I live of on my MMF and CD so what do you consider wealthy and why do people tout wealth redistribution? The key is to boost GDP and have federal state and local governments support all businesses without stuffs that Wolf points out like the tech industry subsides for chips . And I doubt the rich have enough to tax to make a dent they can just donate all into their charitable trusts or get their trusts to buy more tax free . I doubt their money sits in MMFs many businesses keep their cash there also

re: “The key is to boost GDP” That’s what supply side economics was all about.

https://wolfstreet.com/2024/06/03/eyepopping-factory-construction-boom-in-the-us-semiconductors-auto-industry-and-everyone-else/

spoken like a true socialist ( give the gov’t x$ and they will spend 2x$ )

A communist has entered the comments page.

The government ran a wealth tax for most of the past 15 years, by keeping interest rates below inflation.

All we got from that was pissed- off savers and a doubling of the national debt, with little actual improvement in per person real gdp.

History teaches that the best way to get the government to handle its debt is to run a tighter monetary policy – one that makes it obvious that new debt comes at a high price in reduced spending capacity.

The 1980s-1990s were a time of higher interest rates, when government was tightly constrained by high interest payments as a share of tax revenue, and politicians of all parties competed on ideas to bring down the deficit.

How about the government learns to live within its means, like I do? Or maybe we could just confiscate your wealth.

This sounds just like the former Deputy PM stating that the savings from Canadians WFH would be used to boost the Canadian economy in the case of a downturn.

And at the same time, another politician advising that his government will not let Canadian house prices go down, because high home prices are good for foreign investors.

Wolf — for all types of deposits to decline, there would need to be a contraction in overall credit and/or accompanying recession?

Even QT which destroys money couldn’t necessarily cause a decline in overall liquidity without an accompanying decline in economic activity and credit creation, correct?

The Fed has been taking cash out of the financial system via QT ($2.2 trillion so far). Much of that drained ON RRPs (non-bank cash) at the Fed, and the rest came out of the banking system.

Ford forced to shutter factories amid worrying parts shortages: ‘Hand-to-mouth right now’

China’s trade leverage temporarily shuttered one of Detroit’s biggest brands.

Ford’s CEO, Jim Farley, said his company doesn’t have enough rare-earth magnets, forcing the automaker to halt some production lines.

‘It’s day to day,’ the top boss said in a Friday interview with Bloomberg News. ‘We have had to shut down factories. It’s hand-to-mouth right now.’

See this link, particularly question 5:

https://www.csis.org/analysis/consequences-chinas-new-rare-earths-export-restrictions

So, what has Ford done to secure a supply chain outside China, since these problem has been known since 2010? Apparently nothing. China has been reducing the amount of export REE’s for a long time, and showing preferential access to REE’s for companies that MANUFACTURE their items in China. Look at windmill magnets. Almost 100% or them are made in China.

If Ford has to shutter factories, it will be for EV’s and hybrid cars, not ICE lines. How about the board of directors pose these questions to its loud mouthed CEO.

Boo hoo. They should plan better. What do all their employees at HQ do all day?

It’s not like there are any alternative supplies to plan for. Hello?

SoCalBeachDude,

It’s been come knowledge that China had the market of rare earth minerals. There are time when a country should have solid control of key natural assets, but not the strategy in this country. Nationalized key industries are important for countries. The US didn’t even make sure it had enough for military purposes although guessing that is overstated and we have stockpiles there.

California has a huge supply of rare earth materials, but we have put strict laws in force here to keep them in the ground where they belong for posterity. If you want to use them for magnets and other things you once could get those easily and cheaply from the PRC, though that has become a significant issue today with Trump’s very bad and rude behavior towards the PRC.

If rare earths are not rare, are they very expensive?

Yes, quite. In 2018, the cost for an oxide of neodymium, atomic number 60, is US$107,000 per metric ton. The price is expected to climb to $150,000 by 2025.

Europium is even more costly – about $712,000 per metric ton.

Part of the reason is that rare earth elements can be chemically difficult to separate from each other to get a pure substance.

What are rare earth elements useful for?

In the last half of the 20th century, europium, with atomic number 63, came in to wide demand for its role as a color-producing phosphor in video screens, including computer monitors and plasma

TVs. It’s also useful for absorbing neutrons in nuclear reactors’ control rods.

A cube of small neodymium magnets. XRDoDRX, CC BY-SA

Other rare earths are also commonly used in electronic devices today. Neodymium, atomic number 60, for instance, is a powerful magnet, useful in smartphones, televisions, lasers, rechargeable batteries and hard drives. An upcoming version of Tesla’s electric car motor is also expected to use neodymium.

Demand for rare earths has risen steadily since the middle of the 20th century, and there are no real alternative materials to replace them. As important as rare earths are to a modern technology-based society, and as difficult as they are to mine and use, the tariff battle may put the U.S. in a very bad place, turning both the country and rare earth elements themselves into pawns in this game of economic chess.

Until 1948, most of the world’s rare earths were sourced from placer sand deposits in India and Brazil. In the 1950s, South Africa was the world’s rare earth source, from a monazite-rich reef at the Steenkampskraal mine in Western Cape province. From the 1960s until the 1980s, the Mountain Pass rare earth mine in California [closed in 2015] made the United States the leading producer. Today, the Indian and South African deposits still produce some rare-earth concentrates, but they were dwarfed by the scale of Chinese production. In 2017, China produced 81% of the world’s rare-earth supply, mostly in Inner Mongolia,[8][45] although it had only 36.7% of reserves.

In 2018, Australia was the world’s second largest producer, and the only other major producer, with 15% of world production.[46] All of the world’s heavy rare earths (such as dysprosium) come from Chinese rare-earth sources such as the polymetallic Bayan Obo deposit. The Browns Range mine, located 160 km south east of Halls Creek in northern Western Australia, was under development in 2018 and is positioned to become the first significant dysprosium producer outside of China.

The member banks earn a good spread on their IBDDs, 4.40%. That’s more than they make on a lot of loans. Ted Cruz has recommended that the payment of interest on reserves be rescinded.

SGOV an ETF of 1-3 month Treasuries. Currently 4.1%, instant liquidity, as safe as it gets. Super easy to buy/sell through any brokerage. No it’s not FDIC, it’s better – Treasuries

I am a simple person with intuition, common sense, and a knowledge of history.

Lowering short term interest (this is what the fed controls) will exert pressure on raising long term inflation which means long term rates will rise. We have seen this when the Fed recently lowered short term rates and long term rates rose in response to potential inflation. The bond vigilantes weren’t fooled.

I am in in ST 4.3% bonds now. I’d like 5% so I can live my retirement to the fullest. If the Fed Chief is browbeaten or replaced and forced to lower ST rates further(We used to have a capitalist society and now some idiot in government is controlling everything. We might as well turn communist).

Anyway, if LT rates rise to 6+% because of this idiocracy, I’m going all-in on LT bonds gradually. Gradually, because if sanity takes 2 or 4 years to prevail, I might get 12+% on my bonds just like my parents did in the late 70’s.

I’m not hoping for the destruction of America. I just hoping for rational management of the economy.

Many money market funds have expense ratios of over a third of a percent, that is a LOT, even with money market funds they screw you as much as they can, that’s what banks, brokers and most of corporate America are in business to do, take consumers to the cleaners. I’ve never been a fan of money market funds. In my opinion, much better off with a treasury bond fund such as TLT, higher yield, lower expense ratio, and the interest is exempt from state and local taxes. It does have a bit of risk, but until CDs pay 5% again, if the stock market is not for you, I’d go with TLT over a money market.

The short term interest remaining high despite record MMF deposits is a pretty bad sign to me. It indicates a weak economy. Banks don’t see opportunities in lending the money out to the private sector (too risky for their balance sheets), so they pay less interest on savings accounts than the government does on it’s bills. Not enough demand for riskier long term loans for the government to issue more bonds, either. Too much money in the wrong hands (those that don’t want to take on risk, i.e. invest). Only a matter of time until the SHTF.