Listings YoY: San Diego +66%, Los Angeles +47%, Orange County +79%, Riverside-San Bernadino +51%, San Jose & Silicon Valley +56%; San Francisco metro +40%, Sacramento +55%, Fresno +42%.

By Wolf Richter for WOLF STREET.

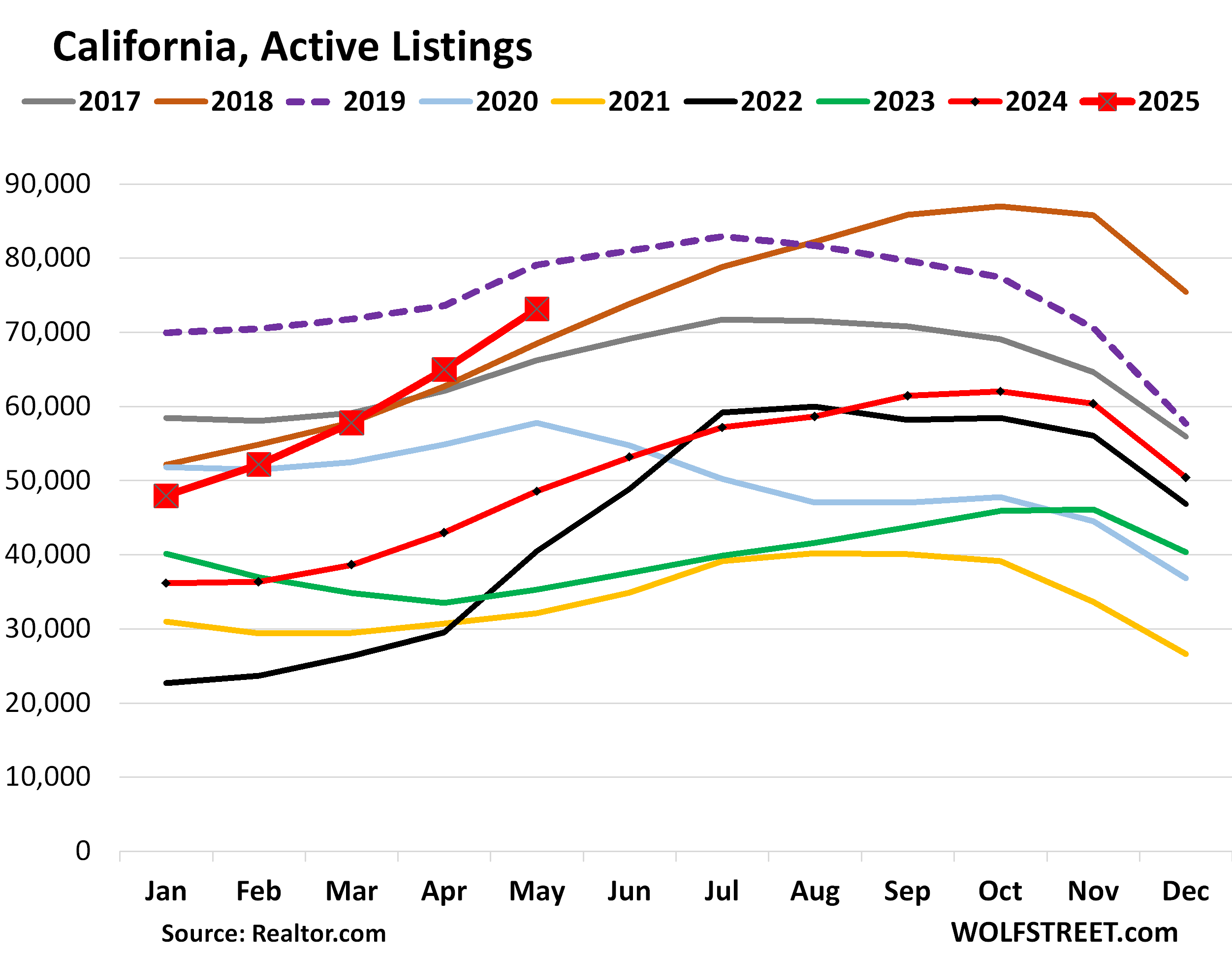

The problem is demand in California. It has essentially collapsed. New listings aren’t that high. But because the inventory of homes for sale doesn’t sell, and new listings are added to it, the total piled up. And it has been doing that for three years, albeit from very low levels. But now active listings are ballooning at an astonishing rate. For all of California, active listings in May have surged by 51% year-over-year and marked the second highest May since 2016, behind only 2019. Active listings are surging in all of the largest markets, but in some more so than others.

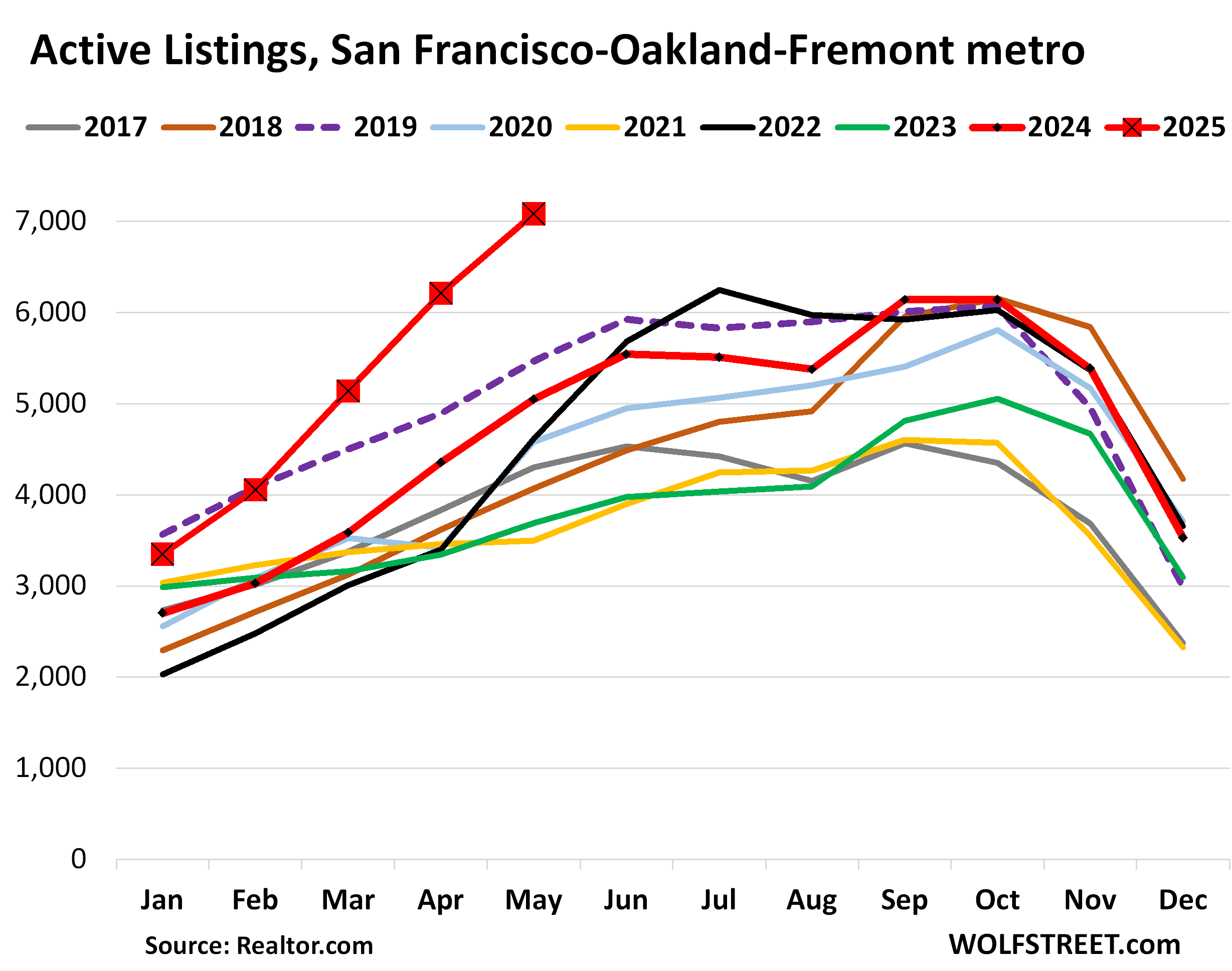

San Francisco-Oakland-Fremont metro: Year-over-year, active listings jumped by 40% in May, to 7,080 homes for sale, by far the most for any month in the data from realtor.com going back to 2016. Compared to May 2019, the second highest May in the data (purple dotted line), active listings were up by 30%. Amazing how fast that endlessly hyped “housing shortage” has become a housing flood.

This metropolitan statistical area (MSA) includes the counties of San Francisco and San Mateo (which includes the northern portion of Silicon Valley), part of the East Bay, and part of the North Bay.

Active listings are homes for sale that do not have a pending sale. They’re the “unsold” inventory. Total inventory, on the other hand, includes active listings (unsold inventory) plus inventory with a pending sale (sold inventory).

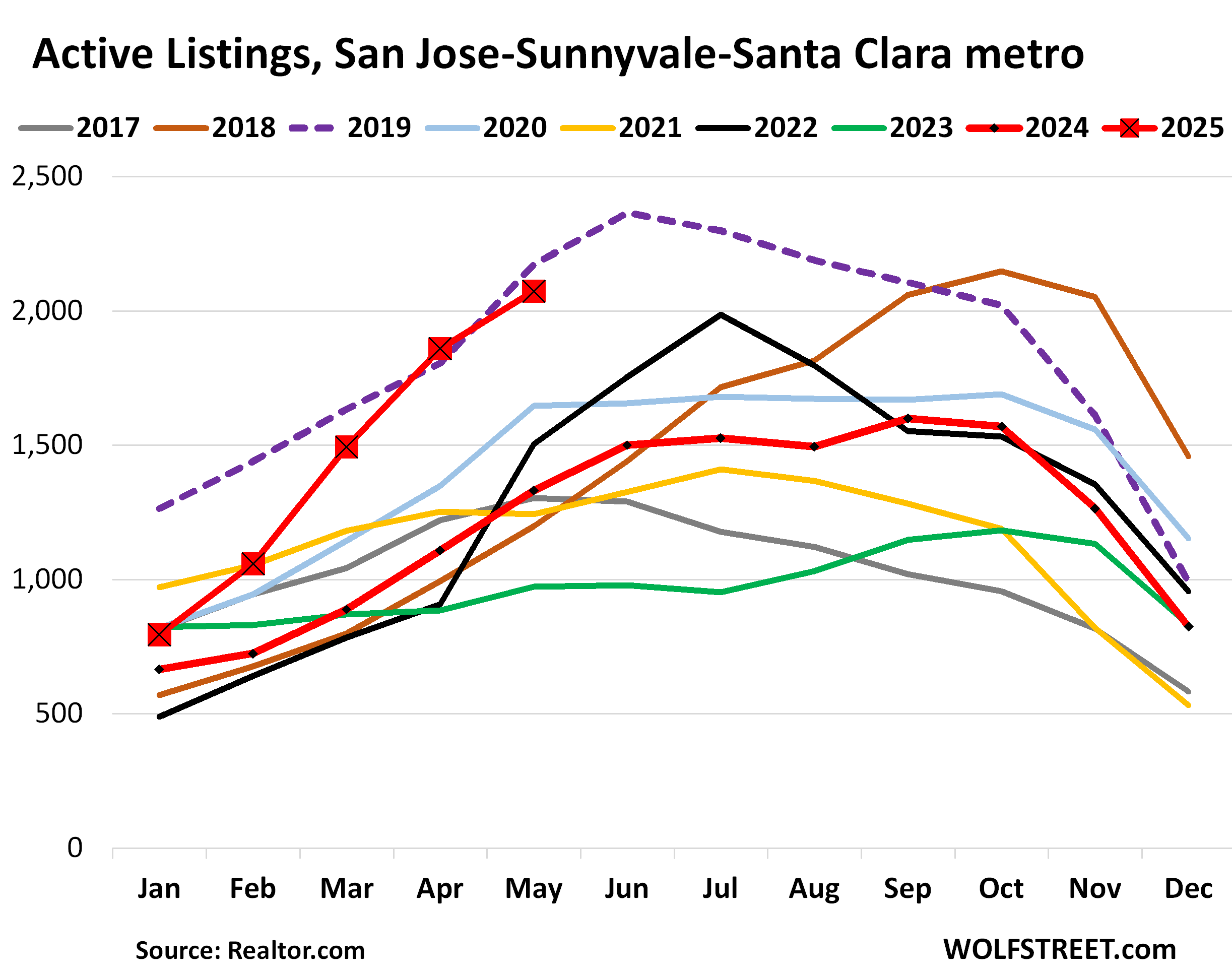

San Jose-Sunnyvale-Santa Clara metro: Active listings spiked by 56% year-over-year in May, to 2,074 homes for sale, the most for any May since the surge in 2019, in the data from realtor.com going back to 2016.

In January, active listings had still been down by 37% from January 2019. Now they’re neck to neck, even though they’d also surged in 2019.

In 2018, the Fed was hiking rates, and the average 30-year fixed mortgage rate rose to 5% by November 2018, and home sales stalled, and inventories piled up in the second half of 2018 (brown line) and into mid-2019 (dotted purple line), by which time mortgage rates had come down:

The MSA includes Santa Clara County (San Jose and the southern part of Silicon Valley) and goes south into rural areas.

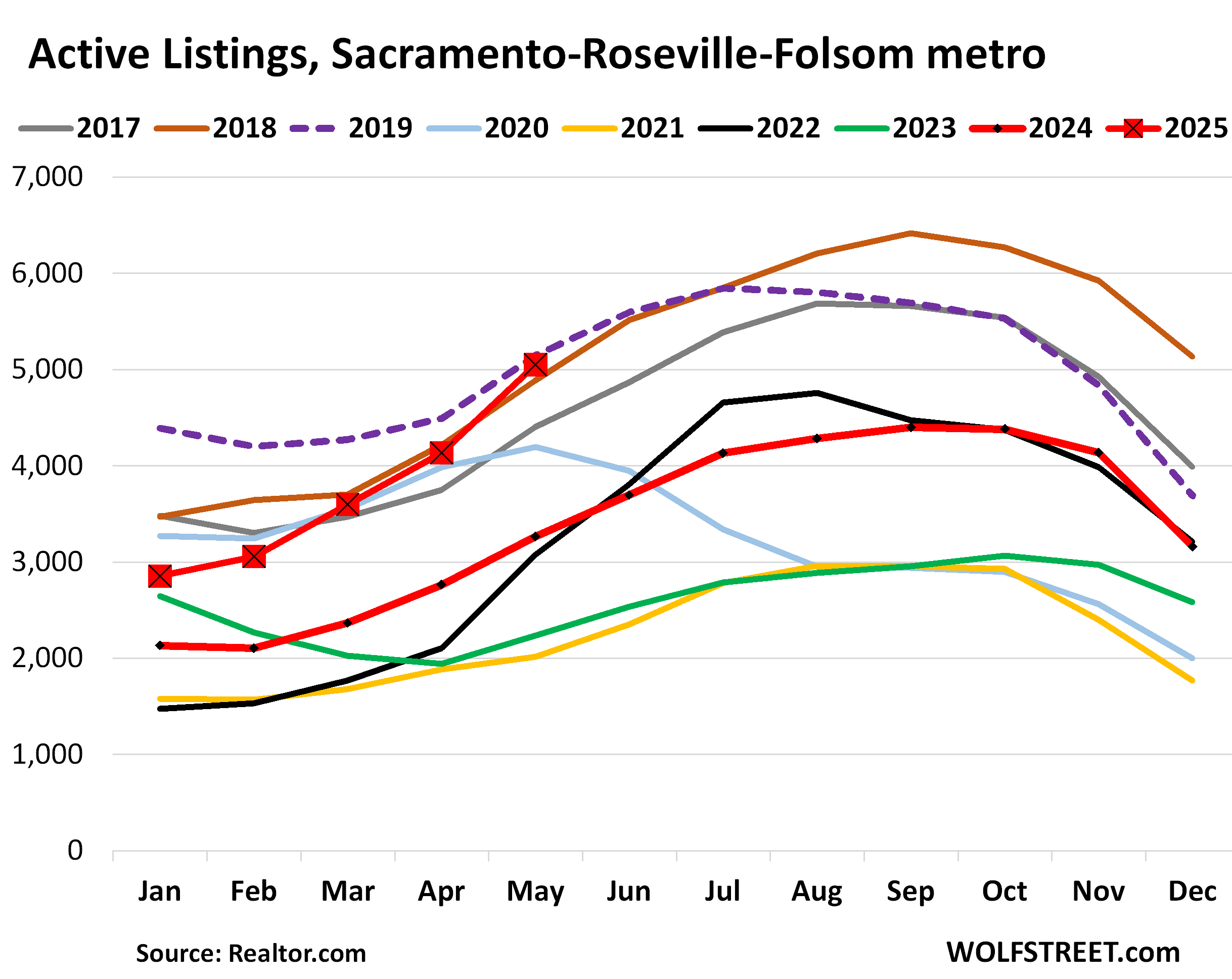

Sacramento-Roseville-Folsom metro: Active listings spiked by 55% to 5,050 homes for sale, the second highest in the data going back to 2016, just a hair below May 2019 (dotted purple line)

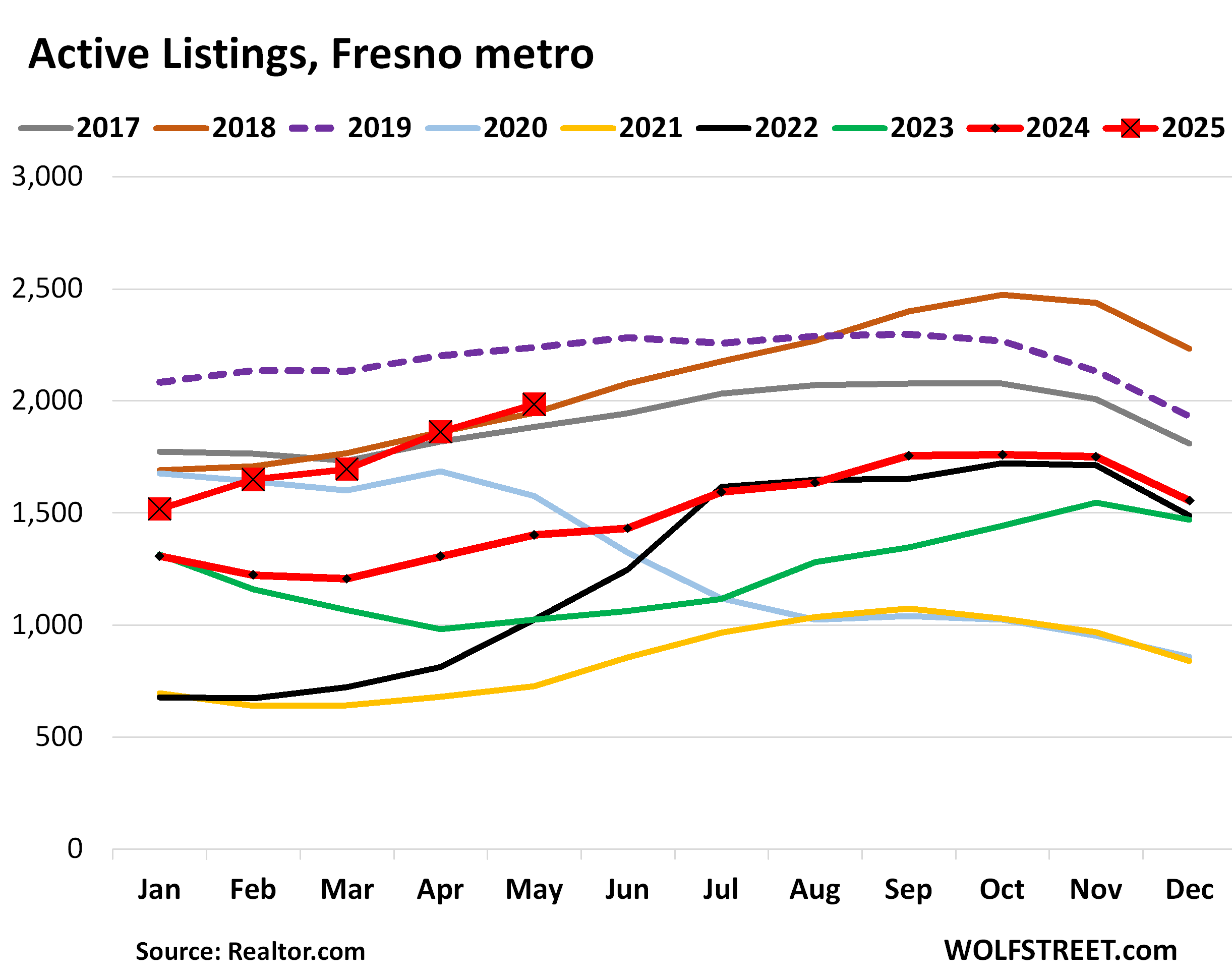

Fresno metro: Active listings spiked by 42% year-over-year to 1,984 homes for sale, the second-highest in the data going back to 2016:

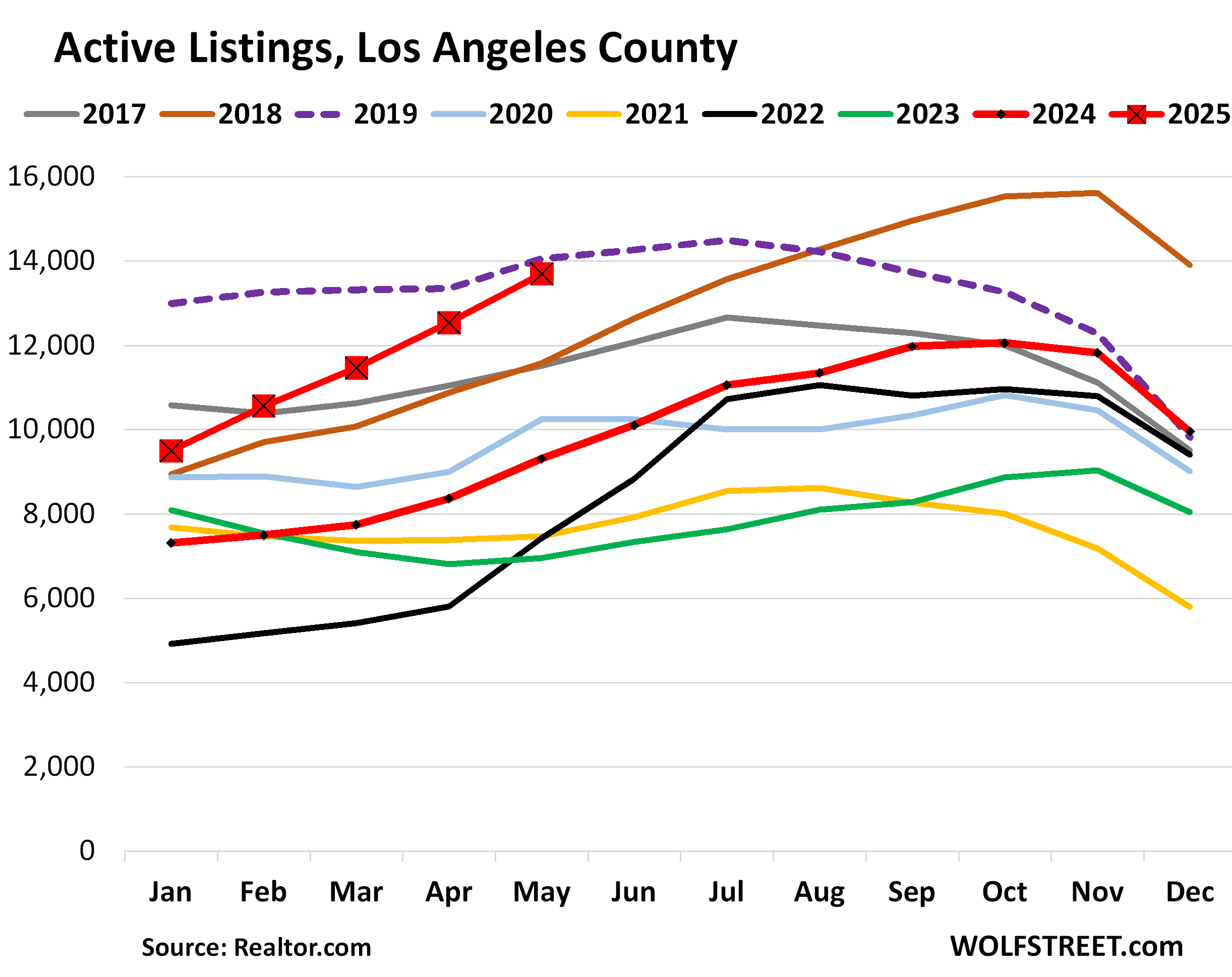

Los Angeles County: Active listings spiked by 47% year-over-year in May, to 13,695 homes for sale, the most for any May in the data from realtor.com going back to 2016, except 2019 (dotted purple line).

Back in January, listings were still 27% below those of January 2019. In May, the difference shrank to just 3%.

In the second half of 2018 (brown line), inventory ballooned as mortgage rates hit 5%, and this continued into 2019. That’s the inventory level that 2025 is setting up to blow by.

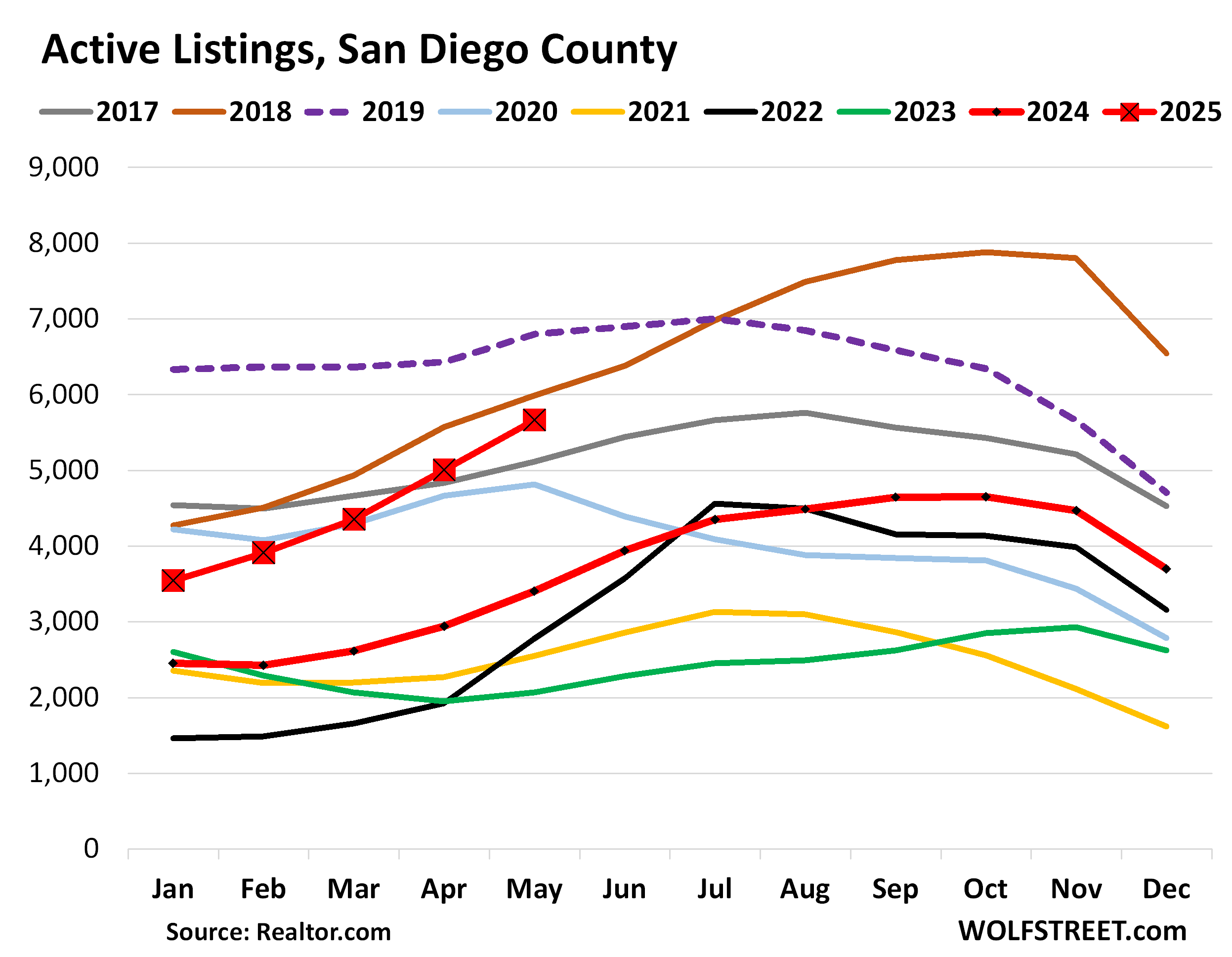

San Diego County: Active listings spiked by 66% year-over-year, to 5,664 homes for sale, the highest for any May since 2019 (dotted purple line) and 2018 (brown line) in the data going back to 2016.

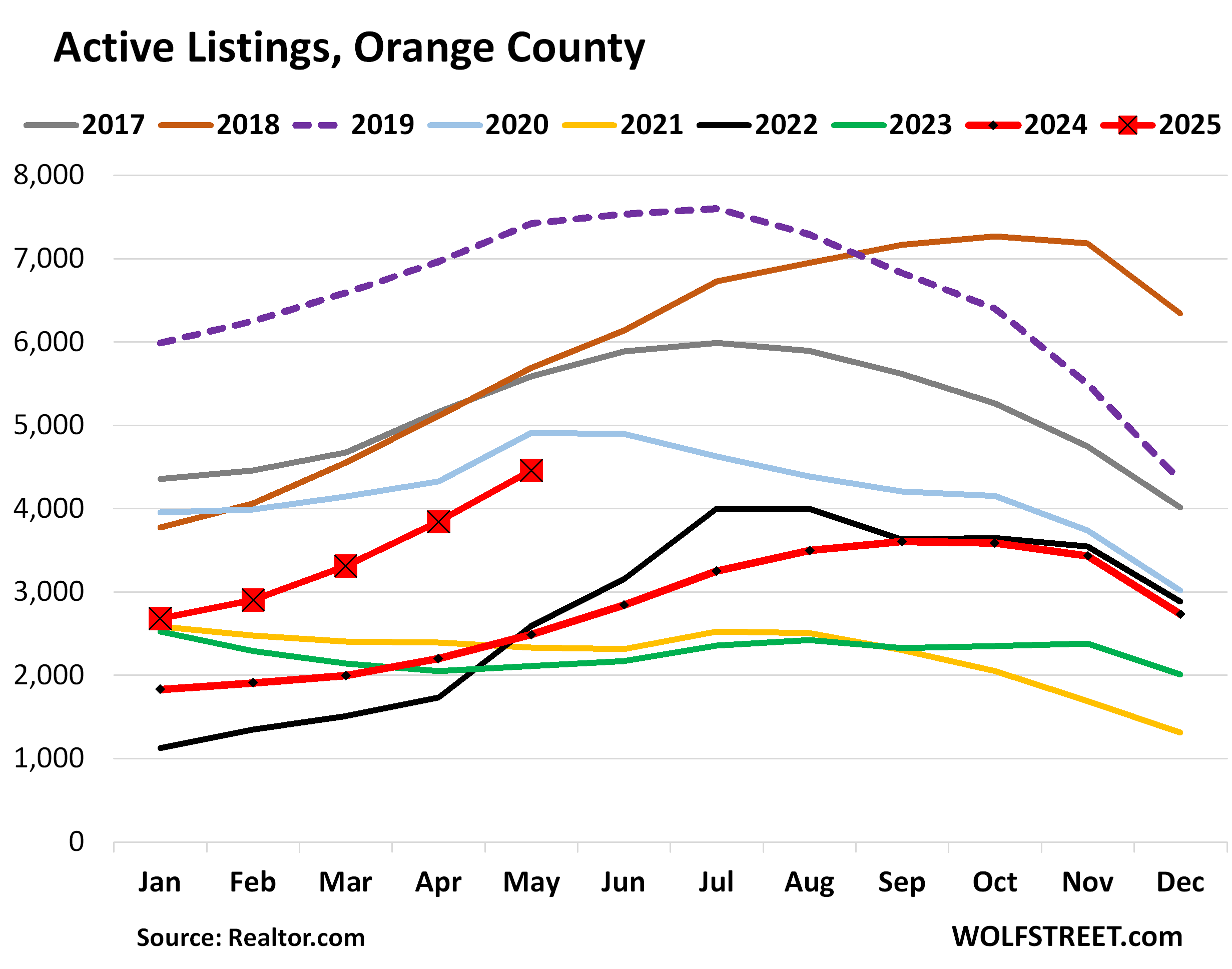

Orange County: Active listings spiked by 79% year-over-year in May, to 4,457 homes. Inventory got a late start taking off and was still very low in 2024, but it’s now catching up with a vengeance.

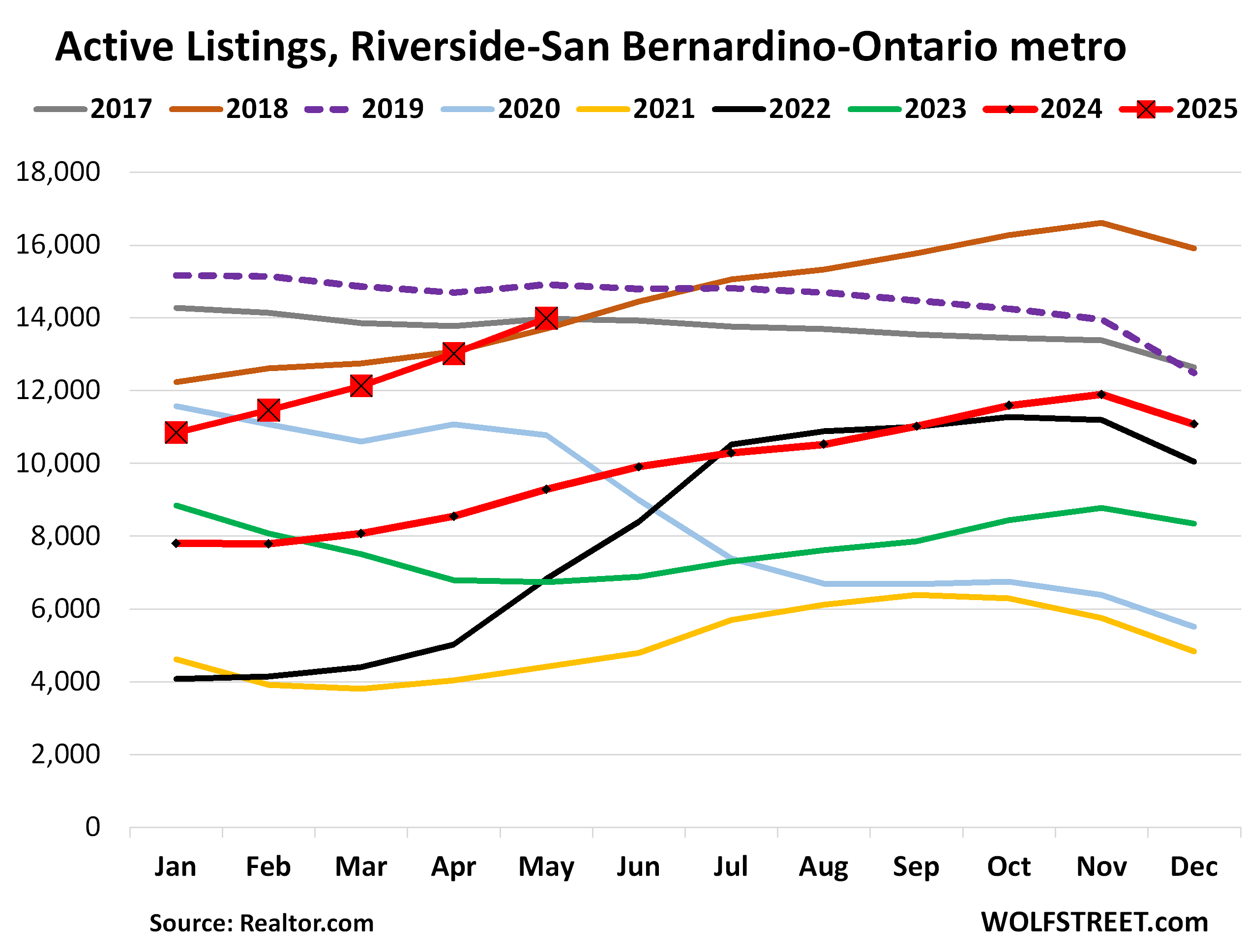

Riverside-San Bernardino-Ontario metro: Active listings spiked by 51% year-over-year, to 13,985 homes, the second highest May in the data going back to 2016, behind only May 2019 (dotted purple line).

State of California: Active listings spiked by 51% year-over-year, to 73,160 homes for sale, the highest for any May in the data going back to 2016, except 2019 (dotted purple line).

In January, active listings had still been 31% below January 2019. By May the gap was down to 8%. That’s how fast this is changing.

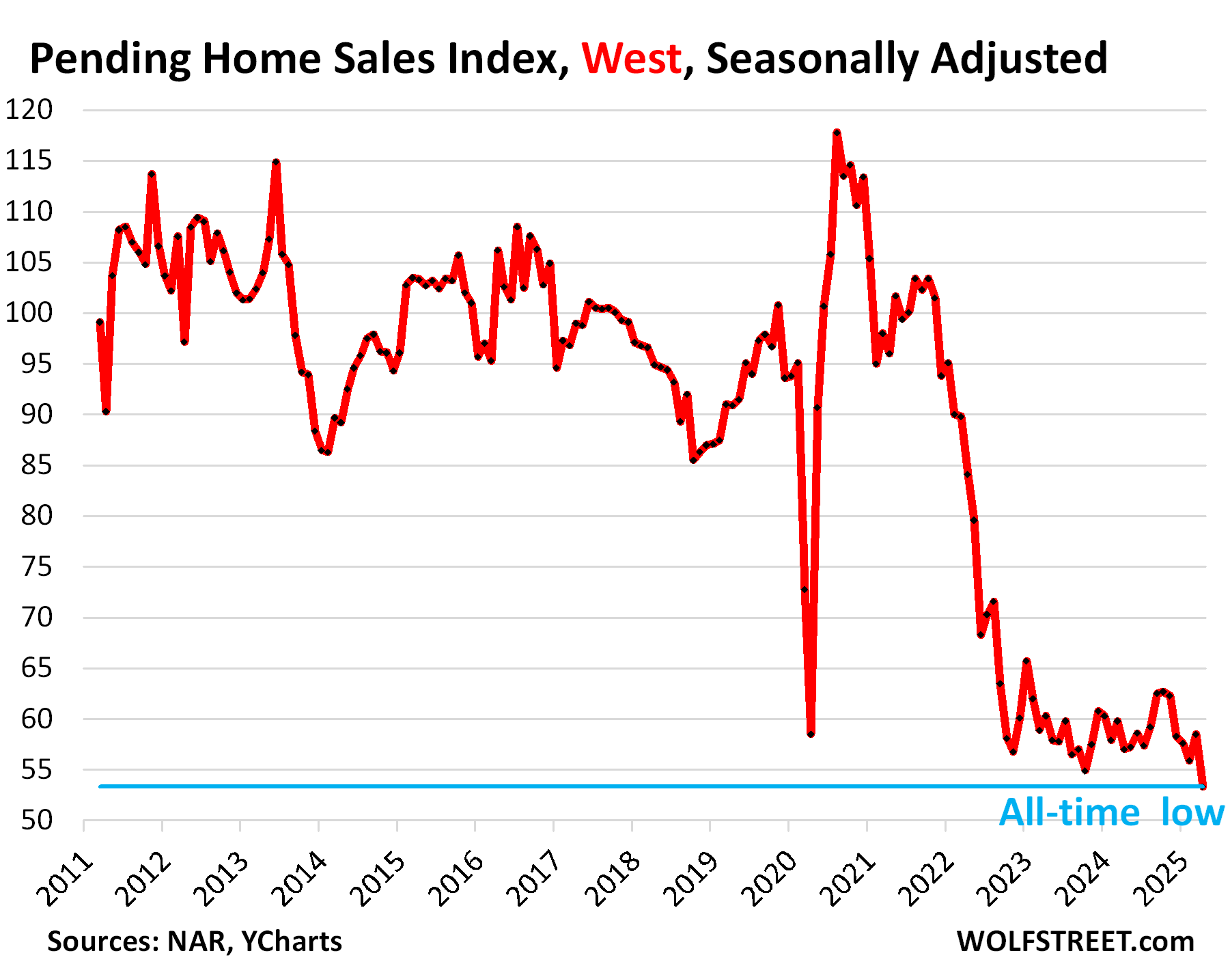

The problem is that demand has essentially collapsed. Pending sales of existing homes in the West, a vast region dominated by California, plunged by 8.9% in April from March to the lowest sales rate since at least 2011, the extent of the data from the National Association of Realtors, and were down by 41% from 2019 [read: Pending Home Sales Plunge in All Regions, Inventories Surge. In the West & South, Collapsed Sales Meet Spiking Inventories].

Demand collapsed because prices have spiked to unsustainable levels, driven by reckless monetary policies. Now demand destruction on a massive scale has set in, a fundamental economic principle. Demand destruction caused by high prices has a functional solution: Rolling back the price spikes. Sellers will be able to sell just fine by pricing their home down there where demand emerges.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here in the 209 lately I have seen quite the increase of listings.

Have a fantastic weekend !

I live in a part of Silicon Valley where homes would usually sell in under a week. I’ve lived in the same house for 35 years. The only ‘bad’ time was just after we bought our home in 1990 and a speculator dumped the home right next door. It dropped our home value by 20+% and we had to pay for mortgage insurance. Now appears to be the first time since then that home values are likely to drop significantly. Across the street from us is a home that went on sale about 1 week ago. It is priced according to the good-old days. I don’t think it will move anytime soon and if it does, it will be far below the asking price.

Silicon Valley is notorious for overpriced homes. I expect if anywhere in America can resist the implosion in prices, at least partially, it’s there.

Well…I have an opinion on this matter.

I moved to California from Metro Detroit in 1999.

I transfered from Sacramento to Petaluma due to the out of control homeless & crime. That was hard on me as I met my wife here, our kids where born here.

I’m in Petaluma & all the homes in Sonoma country are unaffordable. Most of my colleagues promptly leave California when they retire.

From Los Gatos to Santa Rosa to St. Helena, Families can’t afford silicon valley or the Wine country.

The franchise tax board is going to miss me in 3 years from now when I take my family of 5 to South Dakota where it’s cheaper & safer.

Buyers have an obligation to properly price a home & not FOMO into a pump & dump.

Honestly. I cant help but to feel anger as I drive by endless homeless & millionaire homes on highway 101

I guess whomever has these homes for sale doesn’t really have to sell. Normally if one needs to sell they keep lowering the price. These sellers feel no such urgency…..

Many of those could be STR investors, they can wait while they continue to rent. The people who MUST sell likely need those funds for their next purchase. One has more runway than the other.

It wouldn’t be difficult to show an AirBnB for sale in one of the off-days when it isn’t filled as a STR, and no pesky personal possessions to be worried about moving, because they’re aren’t any.

Travel is down, you’d be surprised how many STR rentals need a pretty high occupancy rate and pretty high nightly fee to stay cash flow positive.

At least here in CO where there were constant get rich quick seminars on how to buy a property with 3% down and airbnb it – then when it’s value goes up pull out your equity and buy 2 more. 25-30 year old bartenders would do this and pool their money for the down payment and to hit the income limits. Super common. In 2021 I heard a bunch of lifties (ski lift operators who make $20/hr) in Vail bragging to their friend about it and how he should go in on the next one with him and his they were gonna retire by 35 – these are $1M+ properties out there on the low end. STR may get into trouble the fastest. I also know multiple people who could not cover their primary mortgage and 30% of the STR mortgage. Lots of people bought a second home at 3% thinking that’s cool I’ll Airbnb it and never have to pay that mortgage.

Sounds like a pyramid scheme tbh

Most start like “how rich we’re going to get”.

The risk they are taking on is astronomical

There is definitely a lot of this. I visited Severville, TN a while back and noted that the whole town seemed to be made up of STRs. I bet a lot of those cabins are going to be heavily discounted. I hope the buyers set up an LLC for their little ventures.

I live in Sacramento; moved here in 1988 from Sunnyvale, CA. I was born in Mountain View, CA in 1961. I’ve seen a lot of changes in CA between Silicon Valley & Sacramento. The worst change was what happened during covid with everyone panicking and taking advantage of the extremely low interest rates which made alot of people make rash moving & real estate decisions. I’m expecting the market to crash in Sac. My house was valued at $380 in 2019. Zillow had it valued at $480 by Aug 2020 & it kept climbing to $530 by mid 2022. It was an 840sf small home near downtown. It’s now dropped to $480 & will most likely end up where it was valued at before covid hit the fan!

I think that’s true to an extent, but also oversimplified. It’s not that they don’t have to sell over the long term. Many of them likely do. It’s just that they can afford, in absolute terms, to wait 6 months. They figure the market will recover and they’ll be able to sell for their aspirational price. You’ll see them starting to panic when there’s the sense that the 2022 pricing isn’t coming back anytime soon. Then they have to decide if they want to hold it for the next decade or cut their losses now.

Right, once the down trend is clear and it becomes get out now because next year could be even lower we’ll start to see some behavior changes. It may even turn into I should get out before I drop below my cost basis for those who bought in the last 5 years

If I don’t need to sell then I won’t put my home for sale in the market.

The efforts to put up with this is too much with staging.. People coming in and out .

So yes they have to sell.

Well, I think that’s true to some extent, but not entirely. Around here, in the Miami area, prices temporarily doubled during the post-pandemic years, and those increases, being unsustainable, are now unwinding.

I think there are at least SOME people who, for example, bought for $800k in 2018 and are thinking “Well, if someone is dumb enough to pay me $1.7 million for this house, I’ll suck it up and move. Otherwise, I’ll stay put.”

But to your point, this is an enormous pain in the butt and staging, people viewing with no real intent on buying, and all of that makes it undesirable.

What a great news to help kickstart the weekend, and to see OC and SD on the list is like cherry on top :)

Hopefully next up price will go down double digits just as fast as inventory is piling up. No doubt some of the able sellers might end up pulling their listing off the market and maybe hope for another miracle rescue by next spring season.

Mainstream narratives and articles surely have shifted to FOMO to more like iceberg is on the horizon the last couple of weeks..interesting..

Yeah hoping this consistently becomes the mainstream media narrative. Better yet another 2008 on the horizon since they typically flip from one narrative to another

Home prices here north of Sacramento are dropping like a stone. I bought in January 2020 and although I have no plans to move and I’m glad prices are coming down, I’m starting to get a wee bit nervous that my kids will be inheriting a white elephant lol.

@Bongo if you are just a little north of Sacramento (like Lincoln or even Yuba City) you should be fine but in rural places like Quincy and Chester 100+ miles north of Sacramento will have a tougher time with jobs continuing to disapear (the sawmills are not coming back) and fire insurance going higher and higher (I paid more in fire insurance for our Tahoe area cabin in the last two years than my parents paid to “buy” their first home on the SF Peninsula in the early 60’s)

I have homes in San Diego and I really want them to come down in price so that normal folks can afford and raise family.

Yes Sac would go down as well.

If you have bought your home as a shelter then all would be fine so what even if the prices go down

holy crap i didnt think listings would pile up this fast and demand go EVEN lower, but here we are. Like Wolf said – Mortgage rates are here to stay and prices need to come down. Impressive.

Only amazing thing is that it took as long as it did.

For 20 Years ZIRP turned the US *housing* market into one giant interest rate speculating machine.

Rising rates in 2022 signaled the closure of the casino, the cut-off of the fool fuel.

I know this is an article about for sale houses (IRTFA) but as someone who checks both for sale inventory and houses for rent, I’ve noticed a lot more rental houses on the market too the last couple of months. Also at ridiculous rent prices, although still less ridiculous than the purchase prices for equivalent houses. I guess the landlords would rather sit with an empty house than lower the price too. I’m hoping prices of one or the other crack soon. I’ve been looking at houses since 2020!

Those are all the houses where the owners realize they can’t sell for their dream house, so now they have decided to rent. (after all, how hard can it be to be a landlord) and just wait out the decline……………..

I’m sure it will all be fine.

Agree on the absurdly inflated rental home/AirBnB pricing.

Hard to imagine that very many people take up such offers at such prices (although presumably some must).

To a certain extent, I really wonder if a lot of these putative landlords have made such horrible purchase price/financing decisions, they simply price extremely high out of desperation – they need insane rates to salvage their insane purchase deals (although that is how loan death spirals start).

And who knows what crapola “yield optimizing” software is pumping out for these landlords – those algorithms are based off of *historical demand* (causing pricing screw-ups as demand curves shift) and can be very, very sensitive to landlords’ “target revenue” goals (to the point of generating hallucinatory price suggestions).

My friend bought a home 9 months back for 1.2 million and renting it for 4.5k per month.

People have gone crazy .

It is interesting to sometimes try and quantify the “crazy”

(I’m ignoring a bunch of details below for the sake of speed – but the math is going to be (big) ballpark accurate)

1) At $4.5 per month, that’s 54k per year (if rented every single month – likely impossible, but we’ll go with it).

2) A 5% mortgage (not available for a couple years, but we’ll go with it) is going to require $60k in *interest alone* per year.

3) So even at that very high $4.5k rental price point (varies by market but pretty darn high in 95% of US markets), the owner isn’t close to even breaking even – ignoring all the zillions of costly details that landlords have to deal with for as long as they own/rent the property.

4) There are fairly convoluted tax breaks and financing hiddly-diddly that can help reduce costs but they are time consuming to fully grasp and always contingent upon politicians.

Yet these…slender reeds…are usually what reassure RE investors as they accelerate over the cliff on purchase prices.

5) Alternative, could have put $1.2 mil in US Treasuries and got $60k per year while sleeping by the pool.

Or, if the interest speculating type, could have put $240k down payment in Treasuries and got $12k per year while sleeping by the pool.

6) I know there are a ton of complicating factors that can make the RE option look better – but, at bottom, – they are much more complicated and much more contingent.

7) People really don’t realize that the purchase price they paid is the absolute key factor in whether a deal is going to be a benefit or a curse – all other deal factors tend to be pretty minor/enslaved to that purchase price.

8) That is exactly why it is so nuts that a pretty big subset of US investors have been ZIRP-suckered into paying basically insane prices for SFH (twice…).

9) These demented landlords then attempt to spread the misery to their tenants by asking unsustainable rents in order to try and salvage unsave-able deals.

10) This is what the Fed views as “economic stimulus” every time it inflicts ZIRP.

Think I’ve noticed that.

Rents are dropping lots of places too!

Just a couple of anecdotal comments from some knowledgable folks, but they highly collaborate what you’re saying.

No not anecdotal, rents were down 5.8% yoy in Denver this spring

Where I live, foreclosures increase the costs of housing; my observation is that the banks don’t discount the price at the foreclosure sale and end up buying the property, and do what is needed to prepare the property for sale, and then list it. They are not motivated because the banks have deep enough pockets to keep it on the market until they get a price to make money or not take a loss. I have read that banks don’t like to own properties,….sure seems like they do where I live.

It is a fair question to ask, just how many of the 8 *million* foreclosures from Bubble 1 (2008+) managed to actually get resold by 2012-2018.

SFH prices slowly recovered during this time, but existing home sales volumes were nothing earth shattering (ok – but not earth shattering like 2003-2005).

It is definitely possible that some banks took a very measured pace of selling out their foreclosure REOs, so as not to crater market prices from 2012-2018.

Hmmm. That’s not what happened in 2008. Foreclosures were cheaper than comparable properties, typically sold at auction as is.

I think some of the lack of demand is due to those moving out-of-state.

Cousins of mine moved to Texas about four years ago.

There is also a huge – even huger – pileup of inventory in Texas due to lack of demand. And prices have started to sag. In Austin, they’re already down 22%, in San Antonio 9.1%, in Dallas: 6.7%.

https://wolfstreet.com/2025/05/18/the-most-splendid-housing-bubbles-in-america-april-2025-the-price-drops-gains-in-33-of-the-largest-housing-markets/

With how massive Texas is, and how the cities all are inland and can support expansion in all 360 degrees, there was no good reason for the runup. At least in Miami, coastal California, Boston, Seattle, of the world, you are limited by geography in expanding and building new housing.

“no good reason for the runup”

Completely agree – 65% of (enormous) Texas is flat, easily buildable land with sufficient water.

I’ve written of the Austin re-locatee madness before.

Hundreds/thousands of miles of cheap, buildable land within very reasonable commute distances of Austin.

But the relocatee nitwits from CA (looking to save money – good idea, horrific execution) absolutely insisted on putting 90% of new large corporate HQs within 2, 1 mi square areas.

Thousands of square miles to choose from, 2 chosen.

It was like they were *trying* to screw up the relocation cost savings.

Same for California in San Diego

Lot of land available if you don’t consider coastal neighborhoods

Cas127, I assume you’re talking about the area right south of the state capitol building? I haven’t been there in years.

Tsonder305,

Basically, you can go 4-5 miles South, East, North of Downtown Austin and start seeing fairly large *empty* patches of land.

(West is subject to borderline baloney “recharge zone” restrictions but even those are cope-able if absolutely necessary).

(North is the most developed relatively speaking – but “Texas Developed” equates to like 10-20% of CA/NY “developed)

(Go 7-8 miles south or east of downtown Austin…and you can basically run a nudist camp without fear of discovery…it is just raw land, land, land).

People see some main road-side businesses and assume an area is “developed” – but go off road a 1/4 mile and it is all raw land, land, land.

“That which can’t go on…stops.”

Should be carved in the forehead of every monetary/fiscal authority like the Nazi at the end of “Inglorious Bastards.”

Yeah many are and have been relocating to TN with the outcome of ruining the state by additional traffic onto the roads where it used to be a pleasure to drive on but not anymore and increasing the house prices outrageously along with property taxes. Native TNens don’t want them here and I totally agree

I think it was dustoff who pointed out that since most ALL west coasters originally came from back east, they are really just returning home.

Missed it…….I guess.

But, I promise I’ll tough it out here to the very end….has to help y’all out some.

You’re welcome.

Raleigh, NC is catching a lot of exodus from Florida, CA and AZ.

Scary to think that the upper middle class in California can’t sustain or afford these markets. Orange County median price is only $1.2 million. Last I visited Cali was in 2012 spent a week at the Luxe Hotel attending Corporate Business Leadership conference at UCLA. I rented a van so every evening our group drove to the beaches for dinner and tourism. The degree of smugness and looks we got from some folks I will never forget. Stopping for gas and not realizing you can’t pump your own gas may have been the culprit. Lots of convertible BMW’s and Mercedes waiting in line that’s for sure. I demand to know where are all the wealthy real estate investors from peak market in 2022. Liquidity has not dried up in the stock market. Maybe buying RE on margin not a good option right now? Is $3M for a home in SF really too much to ask?

What would you rather have a home or a US Treasury bond, a stock or a home, a home or another piece of paper? You can live in or rent the home regardless of what markets or the US dollar do. My point, paper assets are always dubious, a home is there, you live in it. It will always have some value.

Yes, you need one home sized to the number of family members After that all your assets can easily be stocks and bonds

And…. you can always sell one house [in CA] and move somewhere else.

But everyone has to live somewhere. Where I live [98053] houses still sell quickly at 100% of list. Some under, some over. But with more houses coming on market that might change.

“or a home”

90% of people think they bought a “home” but when the SHTF what they’ve really bought is a *mortgage*.

If the choice is between a couple renting a 1 bedroom apartment or buying a 5 bedroom house, the decision is a *helluva* lot more fraught than the ZIRP-stoned perma-bulls make out.

Even with kids.

We live in a country with 32 *million* unoccupied SFH bedrooms – a stupidity facilitated by ZIRP.

@California Dreaming you have always been able to pump your own gas in CA it is only OR and NJ that don’t let you do it.

Most gas stations in Oregon allow you to pump your own gas these days. Full service is no longer mandated.

I loved the mid-1950s gas station scene in Back To The Future!

Last time I was down there, Thursday nite was beach dinner (bonfire food) night at Corona Del Mar in OC….maybe you just accidentally went on a nite reserved for something else and got in someone’s way?

When in Rome, ya know?

One reason you did not mention for home sales in California being so depressed is that the home insurance market is pricing many, many people out of the market. It’s one thing to have the 20% down payment, it’s one thing to find a mortgage, it’s one thing to have a good job to be able to qualify and make loan payments, but on top of all these hurdles, the home insurance market, due mainly to wildfire risk, is pricing middle income people completely out of the market. 12K/year on a 500K home is not uncommon in California.

Not priced out from insurance costs but it is getting VERY expensive. Live in the Sierra mountains and there is no commercial fire insurance available. So for fire the only choice is the California FAIR plan plus a difference in conditions policy (which covers everything except fire and was alos extremely difficult to get). Bought about 7 years ago and premium today is 3x when i bought ($120/month to $400/month). Despise Prop 13 real estate taxes are up about 20%+ as well. Including utilities, I’d estimate that monthly costs are roughly double in 7 years. Death by 1000 cuts.

And a anecdote: talked to a couple 6 months ago who were under contract to buy a house on Donner Lake (near Truckee California) until they had an insurance estimate that was going to be as much as the mortgage. They pulled the offer

@Desert Pirate I’m not saying that nobody is paying $12K/year to insure a $500K home but VERY uncommon (I bet CA has more guys over 7 feet tall than prople with $500K homes paying over $12K/year to insure them), I’m on “NextDoor” in Tahoe and people complain about the insurance cost increases all the time and using the CA “Fair Plan” for fire insurance the combind cost of Fair Plan + a Liability policy only gets over $12K for high risk homes worth over $2mm.

I haven’t seen 12k on a 500k home. We’re paying 2k for our 500k home in Sacramento metro. It was 1k on 300k five years ago. Might go up another 20% this year.

My MIL was seeing 6k on her 500k cabin in the Plumas forest where wildfire risk is high.

She stopped paying for fire insurance 2 years ago on her other cabin worth 300k when her insurer withdrew from the market and all she could find was 5k per year. She insured a year later with the Calfire insurance at 3k.

CA Mil has two “cabins” worth 800k? Does she also have a SFH ? I’m assuming she is not married anymore which means she is property rich ! Good for her. CA real estate I wanted to move to Valencia in 1983 but never could figure out a down payment . Should have anyway!

Also, let’s not forget if you want any kind of earthquake insurance, then it’s another big expense hence quite a few homeowners are riding naked on that.

Then there’s also HOA which even a lot of houses comes with now and that will be an escalating cost over time, never heard of HOA going down ever or in a sustain way and some HOA are pretty ridiculous. Then if you’re lucky enough to be in certain cities in south OC, let’s not forget about Mello-Roos..

But hey if you talk to the blind faith believer in housing, for some reasons all those factors are not as big of a deal to them, I guess the prospect of only thinking of housing can only go one direction up can make you willfully ignorant of other factos.

On top of Mello Roos and all that, you have continual school bonds that every time repeat the same essential repairs that did not get done last time. The school bonds have been used for new construction in lieu of backlogged maintenance needs. The bonds are paid by property owners through property taxes.

Add further lease-leaseback revenue bonds. Cities lease city hall, the library, fire station etc. to a created finance authority for $1 a year. The finance authority uses the properties to obtain bonds and leases the properties back to city to service the debt. Principal, interest, admin. costs, and insurance. This is all to avoid the constitutional debt limit on longterm debt without 2/3 voter approval. Rather than solely maintenance and capital improvement, cities are using the bond funds to now pay things like ERP software.

Consultants (who are making ripe fees) push new bonds that pay off existing debt, but obligate city another 25 years in the future. Some cities are doing this every 2-4 years, continuing to stack up debt obligations. These are of course paid at the end of the day by the property owners.

My friend bought a new home for 1.5 million 2500 sq ft in San Diego

First year insurance was 2200

Second year was 4100

Third year quoted was 20k

On top of this he pays 2k per month for hoa and additional fees apart from mortgage.

holy crap that is awful

I live in a high fire danger zone in the Sierra foothills. 1 million home. My std. home ins. policy ( no fire ) is 2 grand a yr. My Cal fair plan with the 5 grand deductible is 8500 a yr. I changed my deductible to 20 grand which changed my premium to 4400 a yr. ( a 20g deductible is not an issue for me to pay. I wouldn’t put in an ins. claim unless the place burned down to the ground, and at that point the extra 15g I’d have to pay would be the least of my problems )

“Amazing how fast that endlessly hyped “housing shortage” has become a housing flood.”

Much like San Francisco’s epic Commercial Real Estate shortage before the pandemic. “Insufficient building. Land constrained.” Lol! Turns out there was a ton of hoarding of empty buildings, similar to the current housing situation.

Southern California home owner here. Last weekend I had to point out all the for sale relator signs. It seemed like every corner had a sign out. Even he started to point them out. So from the trenches this is really happening. I don’t dare look at the prices yet because they are likely still sky high. His best friends family is moving to Georgia in pursuit of a better job and cheaper cost of living. I’d love to upgrade our home and will keep an eye for the market to adjust like the article pointed out. Thanks Wolf

“moving to Georgia in pursuit of a better job and cheaper cost of living”. Yeah, about that…..If y’all think that jobs here in Georgia are plentiful and real estate is cheap, you’ll be in for a big surprise. Traffic is unbearable because like someone said above, they co-massed all the big companies in a few sq miles so everyone is trying to get to and from the same places during rush hour. The last time the infrastructure was expanded in ATL was right before the Olympics.

I always have a good laugh when my clients moving in from CA ask me for a big 5000 sq ft house with 1 acre of land in the middle of (Alpharetta, Marietta, Roswell, “insert nice area name here”) for around $400K-$500K.

Welcome to Atlanta y’all!

Hi,

In Kuwait, the Persian Gulf, we suffer the same.

Avg. house/residential plot prices are $1+ million, actual prices exceed $3+ millions. Over the TOTAL income of a highly paid worker from work to retirement.

Market size by value and sales is the lowest in the region. A month’s sales in Kuwait equals a day’s sales in any other neighbouring country, sometimes less.

Mainly a result of monopoly and fuedalism.

One other feeder into the inventory….Boomers continue to die. Families of dead boomers put house on market and want top dollar for their inheritance. They may be waiting awhile.

Just sold my MIL home in Edmond ok in 5 days home was 50 years old and 15 year old roof good bones but not updated ever. New homes sell for 200-300 a sq ft this home sold for 130 sq ft . We did not give home away but listed to move based on realtor advise

Most people are not smart like you and your wife. To use your numbers, most people would see new homes selling for 200-300 per square feet and list their old home with nothing done at 240, and then wonder why it doesn’t move.

In 2024, California’s per capita personal income was $85,518. This figure is significantly higher than the median household income of $96,334 in 2023.

The median household income in Berrien County during the same period was $63,152.

In 2025, California’s median home price is projected to be $909,400, representing a 4.6% increase compared to 2024. (This forecast is based on the California Association of Realtors). The increase is attributed to rising demand and limited housing supply. The overall average price per square foot for homes listed in California is currently around $484. For basic, builder-grade homes in California with standard finishes expect to pay between $200 and $400 per square foot.

The median home price in Berrien County, Michigan is approximately $285,152. The median price per square foot is around $162. One source states that the average price per square foot for new build homes in Berrien County is $201 for new homes in 10 communities in the county, with an average overall price of $424,165.

“This forecast is based on the California Association of Realtors). The increase is attributed to rising demand and limited housing supply.”

LOL, they just switched it around, didn’t they, for promo purposes, from collapsed demand and surging supply, to “rising demand and limited supply.” These RE promoters never give up, and when faced with reality, will redouble their efforts. I guess that’s their job, that’s what they’re paid to do is to lie out of both sides of their mouth.

I’m surprised you unquestioningly posted their lie into this article that is all about “surging supply and collapsed demand.” Did you forget to read the article in the heat of the battle?

Wolf – do you think this is some of the vacant inventory coming back on the market now that prices are coming down? You have talked about the number of vacant homes for some time. Thanks

Hi Wolf,

The average home price and income data I posted was lifted from Google’s AI. The mention of the CAR in the parentheses was my way of pointing out the biased source. Irony is my favorite form of humor.

What piqued my interest was the disparity between the California and our local SW Michigan real estate market and levels of household income.

I see. thanks.

A man will believe anything to earn a commission.

Lawrence, is that you?

Why does this sound like a genAI comment?

Maybe if home prices come down, assessed values will decrease with a corresponding cut in property taxes. Oh my, what will the local governments do when they can’t increase assessed values 10-20% per year (Indiana) to feed their coffers?

Already happening in Colorado, my primary home and ski condo both had 3% decrease in taxes due to lower assessed value this year, and I am certain there will be further reduction in upcoming years.

The fish is always rotting from the head. The most expensive areas will blow first, with spectacular explosion

So any guess on how long it will take for growing inventory to turn into declining prices ?

I read interesting comments here about different reasons why some of the inventory may be indifferent to how long the house remains unsold. Some of the inventory will go onto the rental market.

However, I doubt the institutional holders are as indifferent to ongoing losses as many believe. The feasibility of rentals rests on how much debt the house is having to carry and greater supply will mean lower rents.

Increasingly a rental as an investment seems to only really pencil out if it carries very little or 0 debt. Otherwise, it is the bank that is collecting most of the profits and cashflow.

It maybe the FED is more constrained that we think in it’s ability or willingness to lower rates. Thus 7% mrtg rates and even higher may be with us for much longer that anyone imagines. A tipping point in time will come and prices will tumble…and then we will be talking about that as a crisis.

If you read the Airbnb sub on Reddit there are lots of tales of investors cutting prices to compete with other rentals and being squeezed terribly – those lower prices attract a more questionable clientele. The bottom of an overly saturated market is getting out of the business. So is anyone whose business model is crumbling with travel to the US being down.

If you have super tight margins, STR are no longer a viable business model. Rising insurance costs play here as well.

I purposely book hotels when I travel now whenever possible because I’d like to see full-time Airbnb of what should be residential sfh fail. Also it’s typically cheaper now that cleaning fees are ridiculous. If more people would consciously choose hotels I feel like it would home prices fall faster…

I liked Airbnb in its early days, but I agree now. The list of “rules” from the hosts was the final straw for me.

Airbnb was great when it was someone with a residence they didn’t use all the time and wanted to make some extra cash and defray expenses. When ignorant “get rich quick” investors started getting involved and buying units SOLELY to Airbnb them out, it went to hell in my experience.

I dont book abnb for its outrageous extra fees which shows up during check out

Right @TSonder305, I had no problem with the initial Airbnb plan of people renting out homes they lived in or used part time. This didn’t take units of housing away. When people started buying homes solely to run like hotels that changes the property from residential to commercial and is against its zoning rules. That’s what I have a problem with. All the STR rules don’t do much either because there’s no real consequences so the only thing that will make it go away is a decline in demand for the rentals.

I have no way of knowing, but i’m thinking that AirBnB investors are Bitcoin players too.

You are assuming “institutional holders” borrow at the same rate as you do. They borrow considerably lower, generally, and the smart ones locked the fixed portion of their debt for a fairly long term, only floating rate after that.

They may not be under much pressure at all. And the real institutional players aren’t listing the places they want to sell on Zillow or whatever. They look to sell groups of them to other institutions.

Right. That’s why CRE is in trouble – those long term long fixed interest rates that big investors always lock in. Lol

Blackrock just sold a home in Miami for 410k which it bought 2 years back for 530k

It was listed in public website .

Institutional investors are much smarter

No, it didn’t. BlackRock ha never bought SFH. You are probably thinking BlackSTONE. Giant difference.

“So any guess on how long it will take for growing inventory to turn into declining prices ?”

They already declined in a bunch of markets in CA, such as Oakland, San Francisco, San Diego, etc. San Diego just started, condos are now down YOY, and house prices are giving up YoY gains but are still positive YoY, seasonally adjusted.

Sure.

But, these declines are minuscule compared to the bubble. There’s a long way to go.

Certainly some noteworthy inventory bifurcation going on with LA finally hitting its prepandemic normal but The OC still far below normal. It will be interesting to see where things end up come November when inventory begins its seasonal turn. Also, the slope on some of the 2025 lines looks quite concerning. Fun times.

It does not matter whether some or even most sellers cling to their high prices. Market prices will drop anyway. A small segment of motivated sellers will set the prices for transactions that close. Many sellers don’t seem to understand this basic principle, consistent with the last RE sell off.

There’s another principle in play as well. People sitting on easy winnings have a tendency to keep them in play. But, hardly anyone comes home from Vegas with extra money. Some of the folks betting on RE today are no different than gamblers at the roulette wheel, fixated on results of past spins.

Losing your winnings is more tolerable than losing your hard earned money.

This is a really important point – not only do individuals want to “keep their winnings” they expect MORE. I look consistently at a few areas in California (Bay Area and Tahoe Region) and Montana; their are vanishingly few listings that aren’t at least 15% (and typically 20-25%) above a 2022 or 2023 price. So individuals paid top dollar AND have a historically low interest rate but still want another 20%+ for living in the house for three years.

I’ve done the math before – but once again (with feeling):

The move from 3% to 7% increases the monthly mortgage payment by roughly 55%. A seller who bought in 2022 wants another 20% on top of what they paid. So the monthly payment is now 66% higher than three years ago. Don’t even factor in increases in insurance, PMI, additional down payment, etc. Very few people can increase their monthly housing cost by 66% over a three year period. PITI at 3K requires 90K in income (PITI at 40% of pretax income which is a stretch); PITI at 5K requires 150K in income.

Sellers can ask for any price (and there’s an agent that will assure the seller that they really can get 25% more than they paid in 2022), but realistically MANY places are doomed to sit on the market as simply unaffordable at asking prices.

The other factor is that many houses are coming on the market that haven’t had any work done in decades. So not only is the seller asking absolute top dollar, the buyers could be looking at enormous additional expenses. A house built in 1998 with everything original is looking at most if not all of the mechanicals at the end of life.

I’m typically early but I think this fall is when prices finally start to break.

Well, it’s not necessarily that people’s housing costs will increase by 66%. The aspirational sellers can be figuring that they’ll sell to people much wealthier than they are themselves.

But there’s a limit to those number of people out there.

How can it be that prices are not declining? What if Concessions are being packed into the sales prices. If appraisers verify their market data and take out the concessions, then, prices are declining.

See my comment with the four charts above – Oakland, San Francisco, and San Diego. Prices in many cities have started to decline.

Agreed, Wolf. I think his point, however miscommunicated, was tthat the illegal trend of builders not baking concessions into their sales reportings are skewing the data even farther, where it would show even lower numbers if updated correctly.

This makes it that much worse, because potential sellers are generally that much more disconnected with reality, until the gap is forcibly closed

The realtors will continue to push the “offers due by ..” narrative for as long as they can. It’s in their best interest. However, this cannot go on indefinitely. We’ve been going up in the housing market to unsustainable levels. I’ve been closely following housing prices all over California since 2002 so I know what I’m talking about. The fluctuations here are much more pronounced than anywhere else in the world as far as I know. I’m not hoping for a housing market collapse. I’m just hoping we return to prices that are more aligned to most people’s income. Everybody’s stretching themselves like it’s 2006 all over again.

Even North East market is starting to change with Westchester County, NY total inventory up 119% yoy.

Westchester is interesting in that there is tons of buildable land up north, but most of it is off-limits, so there is very little actual new construction.

It’s all doom and gloom on this site. Buyer demand is still there (I’m in the mortgage business and it’s busy), and it’s only going to take a slight drop in rates for prices to start climbing. In the mean time we will see prices flatten a bit and perhaps drop a touch in some areas but a “bottom falling out” is not I. The cards. July we will see bank deregulations occur allowing more funds to flow into treasuries to treasuries and rates will come down.

“I’m in the mortgage business and it’s busy”

LOL, you’re such a bullshitter and RE troll.

Purchase mortgage originations down nearly 40% from the same period in 2019 and refi originations down 79% from 3 years ago. Also, 38% of the employees at nonbank mortgage lenders gone since the peak in 2022.

Got some charts for you to look at here on purchase mortgage originations and refi originations:

https://wolfstreet.com/2025/06/04/demand-in-the-housing-market-just-got-even-worse-as-supply-piles-up/

The plunge in employment at nonbank mortgage lenders is charted here:

https://wolfstreet.com/2025/05/12/housing-bubble-bust-1-and-2-as-seen-through-employment-at-mortgage-lenders-they-shed-jobs-again-38-gone/

Oh but you forgot….not in his neighborhood apparently. He is special or we’re just bunch of doomers and all the data is also doomer bias apparently.

I do love his talking point of rate cut around the corner, glad to see RE hasn’t abandon their trusty propaganda just yet..

What a load of 💩. Do you have a single bit of data that can support your narrative of people being able to afford houses en masses? .ost existing homeowners couldn’t afford the house they live in if having to purchase again. You think they are selling and losing 6-10% to somehow buy something more or the same price, despite having less money than what they already can’t afford? You think renters are all of a sudden going to all have 50-10% greater down payments and discretionary cash flow to match depsite all the inflation since 2020, plus shorter time frames to pay for that house? Someone 35 looking to pay a house off by 65 doesn’t all of a sudden get an extra 5 years of working life when they have to wait til 40+ to buy the house. They know it, but more importantly, banks know this.

In 2008 the catalyst that finally brought home prices down was the exponential increase in defaults. Now with tighter regulation, what would be the catalyst today? I don’t see any catalyst that can drop prices significantly in a similar fashion, but I do see them being flat for sometime after they’ve already had a somewhat gradual decline. Defaults are not rising in any noticeable way and people always put their money to pay their house first before anything else.

Other way around. Home prices were sinking, some people (mom-and-pop investors!!!) were underwater and walked away, so the foreclosures began, which pushed down prices further, and volume collapsed, and then the layoffs started and people lost their jobs and couldn’t make the payments and couldn’t sell the home because prices were well below the mortgage balances, and they just sent in the keys (jingle mail), and the cycle continues. Five years on the way down.

And people were refinancing the house up to their gills back then for new cars and vacations and everything.

So when the value plummeted and they were underwater they stopped paying and also went into foreclosure.

People forget how long the housing market collapse took before it bottomed out. Why it’s always best to check the past data carefully to confirm priors and assumptions, as Wolf usually does.

The stock market is hyperspeed in its volatility, in comparison.

An increase in unemployment could cause some big moves. That’s why the tech hubs have gotten hit so hard. A decrease in travel could cause highly saturated airbnb markets to drop significantly.

I think the commonality with 2008 is everyone knows housing is over priced, a lot of people jumped in and saw housing as a good way to get rich, and a lot of people think their $1M+ housing valuation is their retirement plan…

Yes back in 2008 there were also responsible homeowners who bought back in the 80s and 90s who had tons of equity and there’s plenty this time around too.

In 2008 lots of people knew the market was overvalued. Not many people predicted how it would crash or the subsequent downturn.

Will it crash again? Hard to say….but I think it’s apparent to everyone we’re in a bubble.

I learned about one of the most ridiculous government programs today, that involves giving subsidies to many wealthy homeowners sitting on housing gains (potential sellers). It also has the impact of dampening home sales transactions.

In Seattle’s King County a homeowner age 61 or above can get a property tax abatement that reduces property tax by up to 90%. To qualify, your income must be less than $83,000, including social security. That is substantial income, so many people will qualify under this program. In fact, when the program came out, there was a deluge of applications.

I investigated this after leaning a homeowner was paying only $2,000 annual RE tax on a home worth $2M.

The goal of the program is to allow people over age 61 to stay in their home, but I’d say with income of $83k you should be able to fend for yourself without government assistance. Worst case, you could take a home equity loan for a small portion of your home’s value to pay the RE tax. And for those at age 61 to 70, they could simply consider getting a part time job for supplemental income.

It is completely unnecessary for county government to intervene in cases like this. These people sitting on $1M to $2M housing gains are wealthier than 90% of the population.

Probably got the politicians re-elected. Every economic decision has political elements or one could say almost all economic decisions are political. Good data and common sense rarely in play.

I might be okay, depending on the details, if people with an income below a certain threshold and over a certain age, instead of paying property taxes, could instead have the taxes “accrue” against the equity in the house, meaning the government would get a lien on the property, that would be paid off when the owner sold or died. It shouldn’t be free money, and it should bear interest.

Ordering 1 inflation report!

:)

There seems to be a narrative that the RE roller coaster (aka the market) has gone over the top of the track and will now travel on a straight level path at this new level. Problem with this narrative: just like stocks, it’s a market.

Just saw this, well guess that put my mind at ease… If he tells me this rocket ship will resume back of this year then it just be true.. Truly insulting to call this guy an “economist”

“National Association of Realtors® Chief Economist Lawrence Yun has said that he believes home sales will pick up in the second half of the year and that national median home prices will grow 3% in 2025.

Home prices are not on the verge of a nuclear crash,” said Yun, pointing to low levels of serious mortgage delinquencies as a sign that few homeowners will be forced into distressed sales.

His forecast hinges on mortgage rates easing to 6.4% by the end of the year, alongside continued labor market growth with 1.6 million jobs added to the economy across 2025.”

Mortgage rates easing down to 6.4 percent won’t many dent to historical low unaffordibility.

It would be nice to know how much of these are investor owned vs primary owner. I wonder if investors are trying to get out and come back after the collapse.

The biggest single-family landlords, such as Invitation Homes, have been disclosing in their earnings calls that they have been selling individual houses that they had bought in 2012 because they’re making a lot of money on those sales even if they cut the price a lot, and because those individual homes are expensive to manage. What they’re now doing is replacing those individual homes with build-for-rent communities, often with hundreds of houses, with their own leasing and maintenance offices and common amenities that are a lot more efficient to manage. Build to rent is a huge thing.

But this inventory data is based on Multiple Listing Services (MLS), and these big investors might sell them direct, rather than listing them and paying brokerage fees. They’re selling them also to their own tenants directly. And then that inventory for sale wouldn’t even be included in these figures here.

I’m luvin this. The wife and I have 4 properties all paid off in Florida. Even tho this is showing up in cali now, Florida is soon to follow. $150 square foot? Lower dem taxes desantis now:) all those helocers are you listening? lol

After almost every shortage, the glut.