With the free money gone, the hangover is getting worked off.

By Wolf Richter for WOLF STREET.

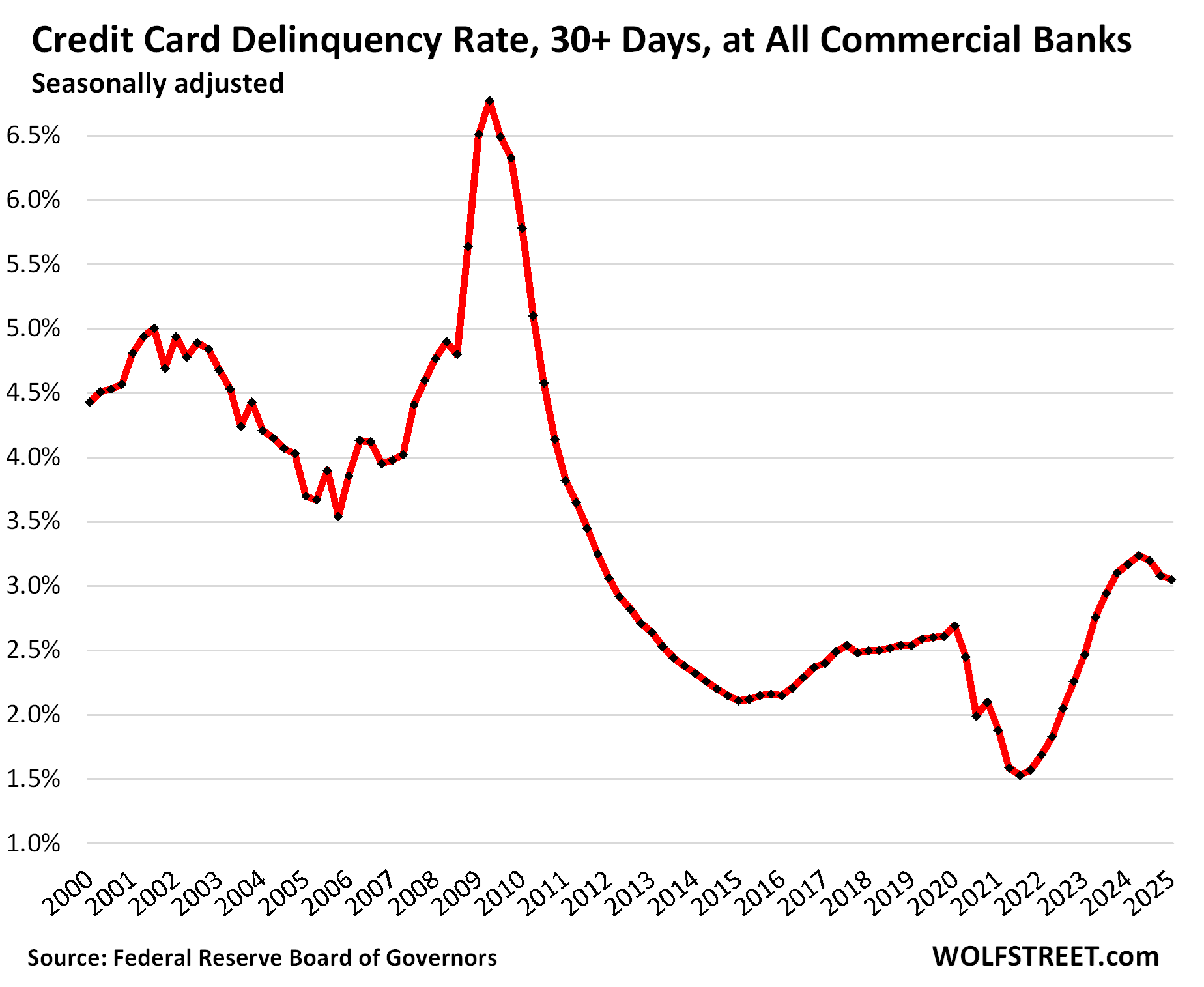

The 30-day-plus delinquency rate on credit cards issued by all commercial banks declined to 3.05% in Q1 seasonally adjusted, the third consecutive quarter of declines, and was below the delinquency rate in Q1 last year (3.17%), according to data from the Federal Reserve today.

The plunge in delinquencies during the pandemic was a result of Free Money flooding households, which some folks used to get caught up; and it was also driven in part by limited options of spending, with restaurants, flights, cruises, entertainment venues, etc. being largely shut down, which caused credit card balances to plunge (see further below).

When the Free Money was gone, the delinquency rate overshot, crested in Q2 2024, and then declined as the hangover has been getting worked off. Our Drunken Sailors, as we lovingly and facetiously have come to call them here, are a hardy bunch!

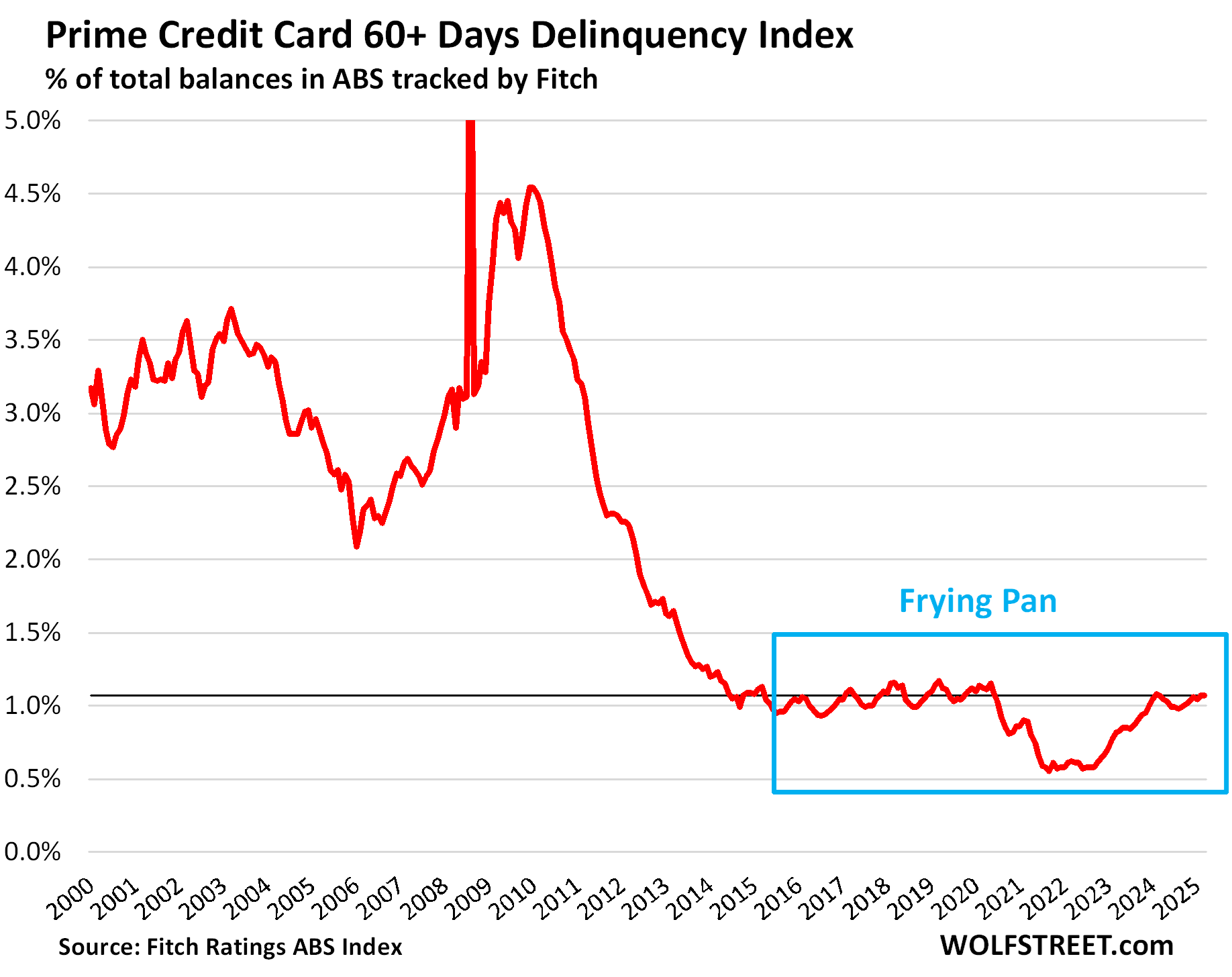

For prime-rated cardholders, serious delinquencies of 60-plus days remained unchanged in March at a pristine 1.07%, not seasonally adjusted, according to data from Fitch Ratings, which tracks the performance of Asset Backed Securities (ABS) backed by prime credit card balances.

This delinquency rate has hovered since December 2023 in the Good Times normal range that prevailed in the five years before the pandemic of just above 1%.

Note the “frying pan” pattern, as we infamously have come to call it here, because we have seen it in so many other credit measures since the pandemic, during which the episode of Free Money altered everything, and when the Free Money was over, the metrics re-normalized.

Credit card balances: a measure of spending.

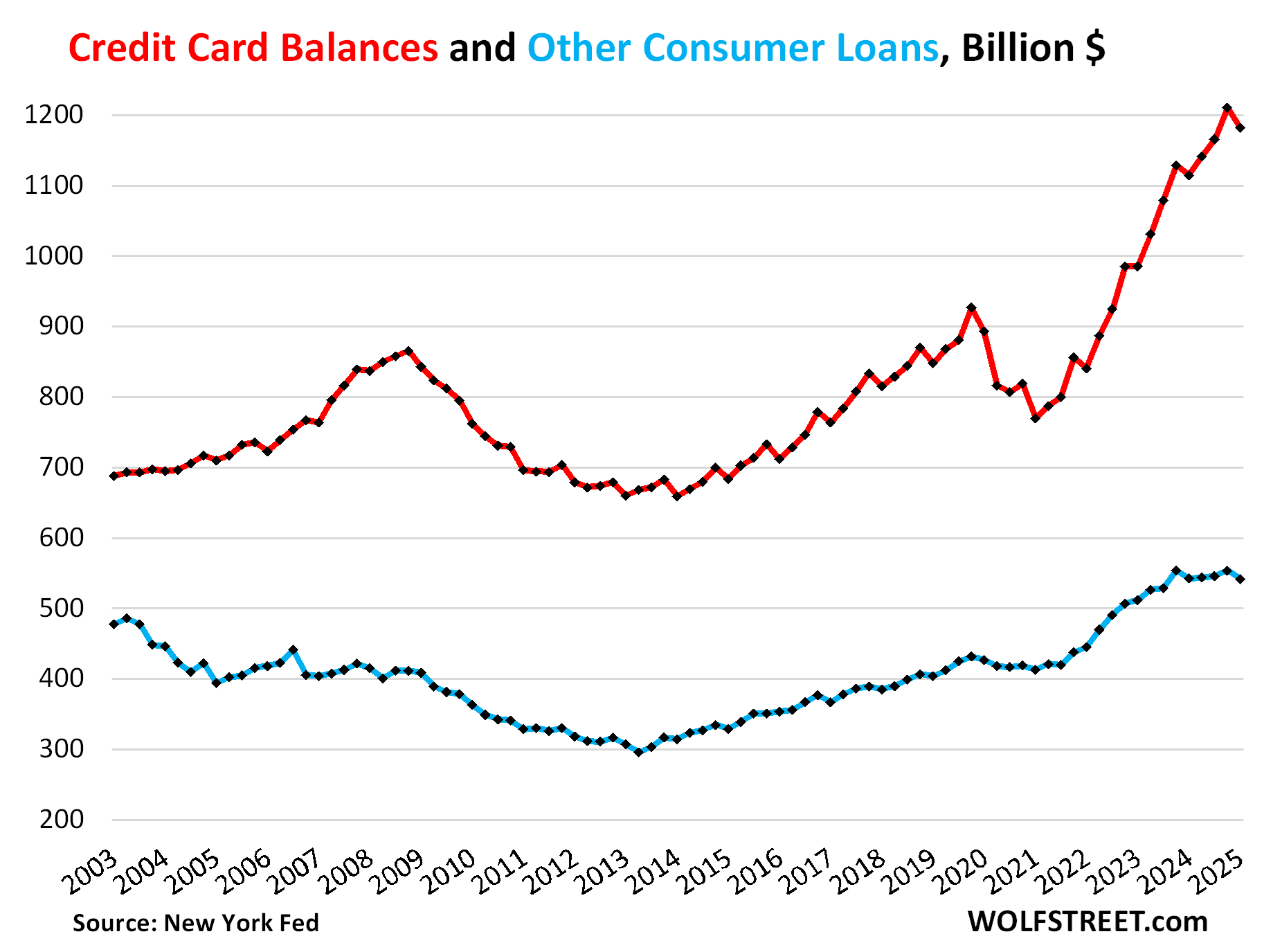

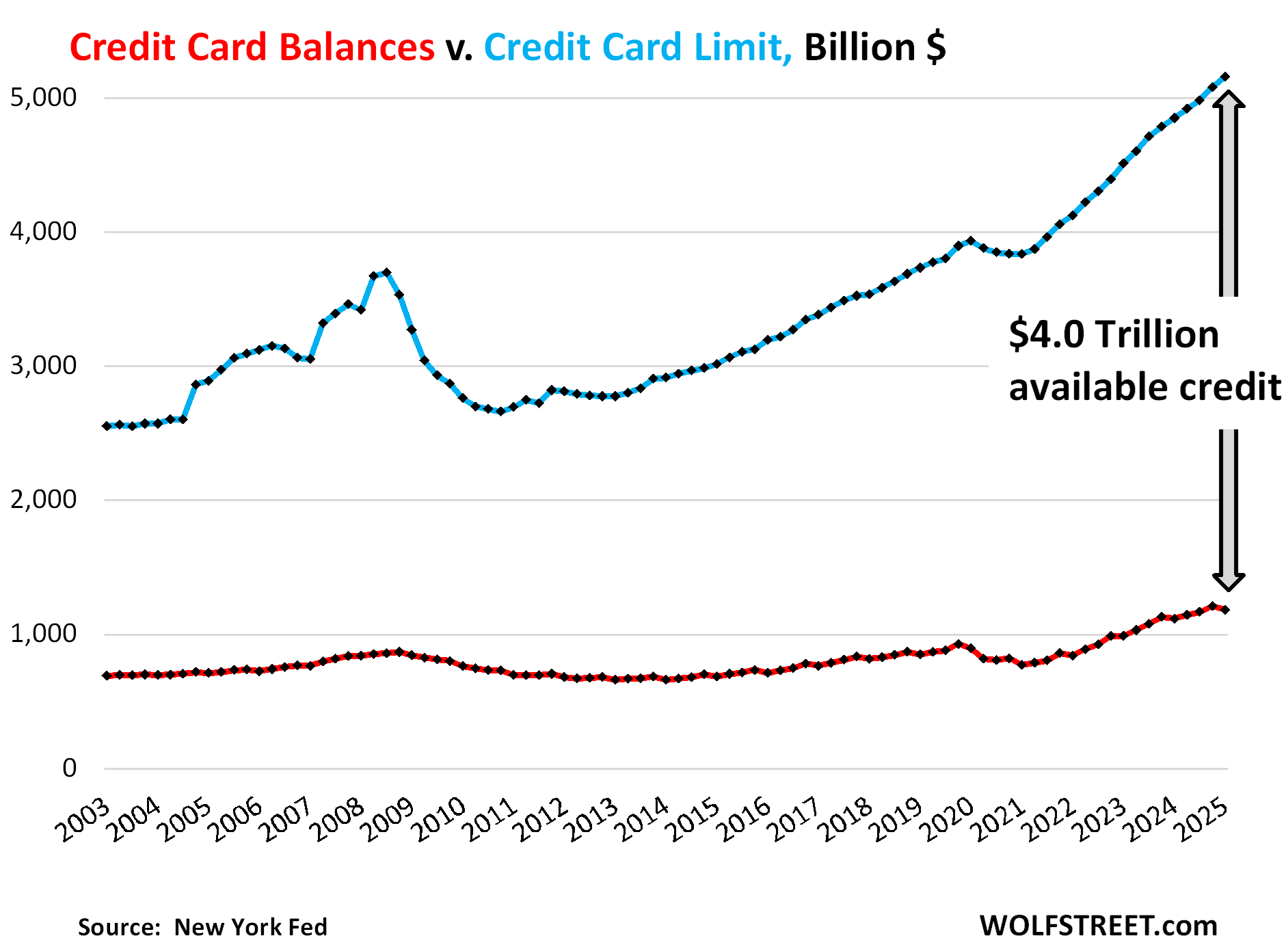

Credit card balances (red line in the chart below) fell by $29 billion in Q1 from Q4, to $1.18 trillion, according to the New York Fed’s Household Debt and Credit report. The decline was largely seasonal as credit card balances typically decline in Q1 from Q4.

Credit card balances are statement balances before payments are made.

Year-over-year, credit card balances rose by 6.7% on consumer spending growth and price increases.

Credit cards are a measure of spending, not a measure of borrowing; they’re the dominant consumer payments method in the US and largely replaced checks and cash. They’re used to pay for anything, from parking meters to business trips that get reimbursed. Credit cards were used for nearly $6 trillion in transactions in 2022 (Nilsen).

“Other” consumer loans (blue line), such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, dipped by $1 billion in Q1 from Q4 to $540 billion, and were roughly unchanged from a year ago. Balances have barely risen over the past 22 years, despite the growth of the population, income, and spending over the period.

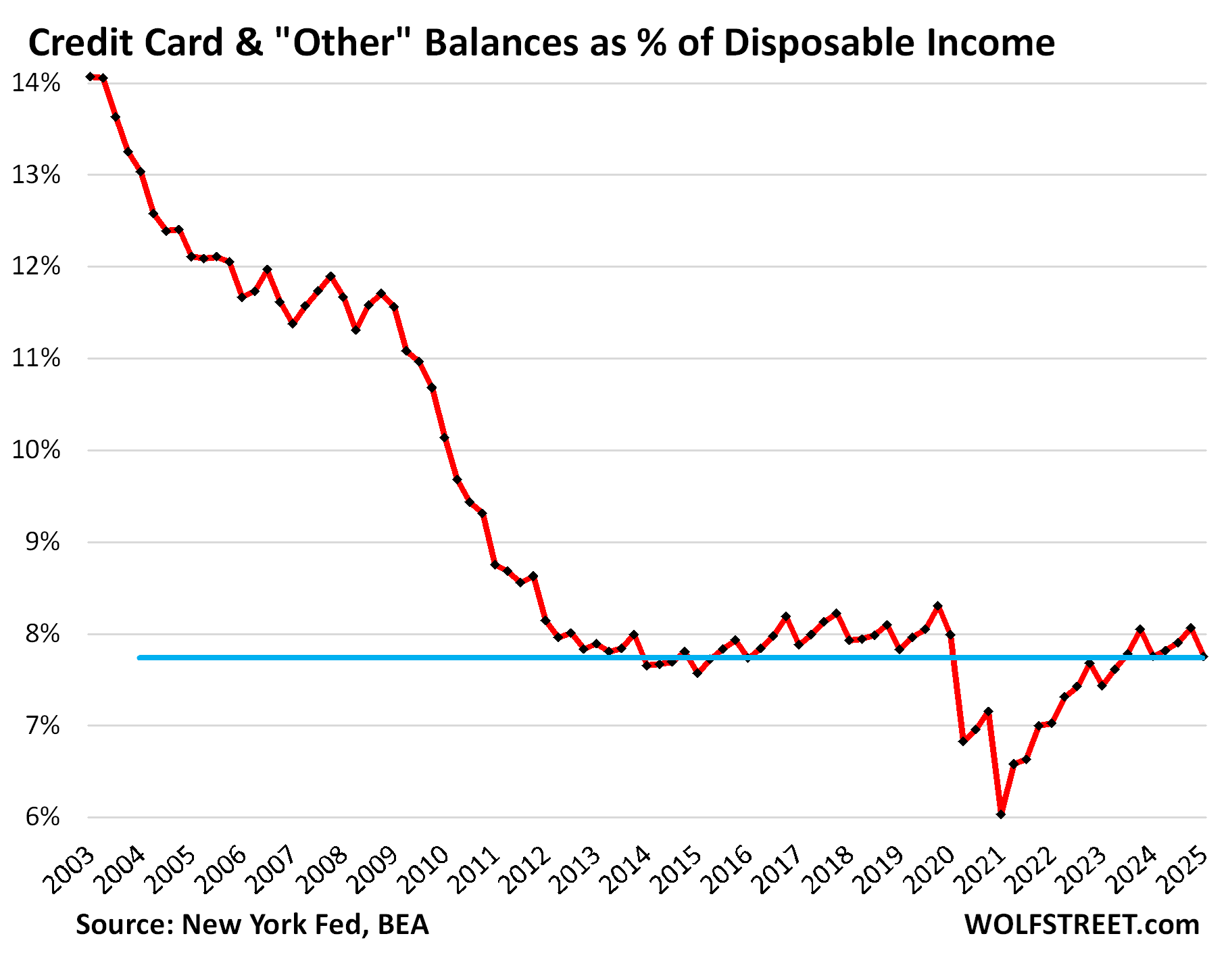

The burden of credit-card balances: debt-to-income ratio.

Credit card balances (red above) and “other” consumer debt (blue above) combined declined by $41 billion, or by 2.3%, in Q1 to $1.74 trillion. Year-over-year, they rose by $66 billion, or by 4.0%.

To track the burden of these balances on consumers overall, we look at their relationship to disposable income. Debt-to-income ratios are classic measures of borrowers’ ability to deal with the burden of their debt.

Disposable income is household income from all sources except capital gains, minus payroll taxes: So income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc. It represents the cash households have available, after payroll taxes, to spend on housing, debt payments, food, fuel, and other expenses.

- QoQ: disposable income +1.6%, credit card & other balances: -2.3%.

- YoY: disposable income +4.0%, credit card & other balances: +4.0%.

Combined balances declined to 7.8% of disposable income in Q1 from Q4, same as the ratio in Q1 2024.

The ratio has now come back up from those free-money record lows when a lot of travel and entertainment spending was cut, and is back at the low end of the range of the Good Times before the pandemic, and far lower than any time before in the data going back to 2003, when the ratio was 14%.

Credit Limits & Available Credit expand to new high.

Banks are trying as aggressively as ever to get people to set up new credit card accounts, and they have raised the credit limits of existing accounts, and the aggregate credit limit has surged from record to record and in Q1 hit $5.16 trillion (blue in the chart below).

So the total available unused credit – aggregate credit limit (blue) minus credit card balances (red) – surged to a record $4.0 trillion. During and after the Great Recession, banks cut credit limits, closed accounts, and licked their wounds, which caused aggregate credit limits to plunge by 28% through 2010. But there has not been any sign of this happening now; on the contrary:

And if you missed it:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m calling it now. The consumer isn’t even close to being tapped out.

These Drunken Sailors have defied everyone and everything.

The “tapped out” narrative has been circulating since the GFC and it’s way past the sell by date. It probably was true for years, back when, but that’s long in the rear view at this point. Doom porn websites kept it on life support all this time, though.

The Balances as a % of Disposal Income and the chart showing how prime delinquency rates have been permanently shifted from ~3% prior to 2008 to ~1% following (permanent here meaning the run rate during ‘normal’ times) are very eye opening. Americans have a reputation of being irresponsible with money, but that reputation is much too generalized.

Thanks Wolf, great article as usual.

They’re not tapped out because they are hunkered down paying their puny 3% mortgages in homes they could never afford at 7%. 👌🤑

Hey! I’m one of those. It is like a cheat code

Of course, when I was 25 and paying 13% nobody pitched a bitch about the FED not helping us out, or gave us “assistance”. You can’t afford where you want to live? Move where you can afford it. You don’t want to move? Then figure out how to increase your earnings. You do what you have to do or adjust your expectations.

Wolf,

Thanks for your excellent reporting. Invaluable!

I understand that the Department of Education is now going after student loan defaulters following the multi-year repayment abeyance. Do you believe that this could have a non-trivial effect on aggregate consumer spending?

Thanks for your thoughts.

Nah. Too small. It might reduce the savings rate a tiny little bit maybe. But I don’t think that we will see anything that will stand out from the regular noise.

There will be a different kind of noise, however. We WILL hear many sob stories from “journalists” about how disgusting it is to expect borrowers to repay their loans.

What about people actually having to start repaying their loans? Lots of people’s loans have been frozen the last 4+ years with the pandemic and then while the SAVE program was tied up in court? Will that have any impact?

There are many ways for banks to make money. I have heard that a certain large bank is holding $70 billion in unused rewards on their credit cards. Of course, this is a liability on their books that they have to fund, but until the cardholders claim their rewards, the CC division can invest the money and earn whatever the treasury rate at that bank is.

I’m not surprised they’re keen on issuing credit cards.

How does that work? Do banks put money on the side as it’s technically a liability-and then invest it? Credit Card points are essentially currency created by credit card companies and not actual money. The one that makes money from rewards waiting to be used is Starbucks.

Starbucks actually takes money from its customers when they pre pay and rewards them with extra points on purchases. They essentially offer a discount on their over-priced-drinks after making several purchases. It does not pay interest on those deposits and the customer is only rewarded if they give Starbucks more money. How do credit card rewards make the banks money while they wait for their customers to convert them without them being actual money?

Franwex-

What constitutes “actual money” has been a perpetual enigma in modern banking. Consider this from an esteemed 20th century economist:

“We must have a good definition of Money,

For if we do not, then what have we got,

But a Quantity Theory of no-one knows what,

And that would be almost to true to be funny.

Now, Banks secrete something, like bees secrete honey;

(It sticks to their fingers some even when hot!),

But what things are liquid and what things are not,

Rests on whether the climate for business is sunny.

For both Stores of Value and Means of Exchange

Include, among Assets, a very wide range,

So your definition’s no better than mine.

Still, with credit-card-clever computers it’s clear,

That money as such will some day disappear,

Then, what isn’t there we won’t have to define.”

From the fertile mind of Kenneth Boulding c. 1969 (when the U.S. was approaching the “grinding higher” and “lurching” forward phases of the inflationary 1970’s)

Gotta love economists who spin Shakespearean sonnets… sorry for reprinting this open several times in last couple years.

Oops: “open” = “poem”

The accounting works like this:

The credit card company accrues the expense of credit card rewards (technically contra revenue if we want to get into the weeds). This creates an expense on one side of the ledger (which goes to the P&L), and a liability on the other side of the ledger (which goes on the balance sheet). This liability is for expenses they’ve incurred but not paid out.

However, they don’t have to give up the cash until the reward is redeemed. A balance sheet always balances (assets = liabilities + capital in the case of a bank), so the bank has assets in the amount needed to pay off their liabilities and can invest those assets until they need to pay their liability. Business cash flow 101 is to collect your money as soon as possible and delay paying your expenses as long as possible to get a “float” like this to work with.

There are those that use credit cards — the ones not living paycheck to paycheck — and those that abuse credit cards… the ones strapped for cash who need that last bit of financial juice to get by. The former can benefit from buying airline tickets and reserving hotel rooms with their cards. The latter can suffer in hell.

wolf,

Since I came to America in 1989, I keep hearing “Americans live paycheck to paycheck”. In my view, the situation has actually improved. In 1990s most companies were not offering 401k, paid vacation, sick leave, parental leave and there was no Obama care and Medicaid was not available. Today, Amazon and Walmart two biggest employers provide not only benefits but also college education. Similar with many companies. Hence, in my view an average worker has more benefits today than in 1990s.

You aren’t wrong but today’s USA is not without problems. Namely, absurd housing and medical costs, and unsustainable levels of government and corporate debt. So let’s not sugarcoat it too much.

Over growth is the problem. A contraction will break the will of producers

Obamacare and Medicare made high-quality health care essentially costless for me for 10 years now. The cost was maintaining excellent personal health with diet, exercise and stress control. “[U]nsustainable levels of government and corporate debt” seems pretty abstract for “an average worker.” But yeah, housing, I was spared that, as it started reasonable and is paid off now. But I showed up 40 years to work and only missed 5 days, and never missed a payment on anything. Cruising through the metro today shows mid-rise and high-rise housing (ugh) going up all over the place. Everything has its cost.

Not at all and it is something to recognize. Progress on these things is often bumpy. I’m really hoping deregulation and a better energy policy will help somewhat.

Making the tax cuts permanent or semi-perm is just politics. Once taxes are lowered it is basically impossible to raise them again.

I definitely want a budget that is closer to historical deficit norm. I want less defense spending and less wars. I want much lower obesity rates which should lower medical costs in the future or at least slow the rate of growth.

I want politicians to recognize SS and Medicare/caid are unsustainable at this level of funding. SS is running out of people to pay into it and will become insolvent in my lifetime if there is no reform.

I’m hopeful we can achieve these goals but time will tell and it will be choppy.

Ram,

I think it is more an expression but 34% do live paycheck to paycheck, while 54% have enough money to cover 3 months of expenses. This according to the Federal Reserve. I am not in these positions but it is not difficult to understand the unease many have, and why it doesn’t take much for people to not being able to meet basic needs.

“…according to the Federal Reserve.”

No, the Federal Reserve’s report says zero about “living from paycheck to paycheck,” that’s a clickbait media twist of what the Federal reserve actually said — you have to read the article and not just a clickbait headline to understand what the Federal Reserve report actually said:

https://wolfstreet.com/2023/05/27/americans-ability-to-pay-for-emergency-expenses-or-three-month-job-loss-with-cash-or-cash-equivalent-by-selling-assets-by-borrowing-or-not-at-all/

US nominal consumer debt is at Financial Crisis levels. At some point, the consumer can’t spend anymore. By January 2008, it ended and the tide pulled out. Imo, its started again. This time flyover America will get it. Yup, that is the key understanding American politics over the last decade. Now 2026 will be 1994 in reverse.

“US nominal consumer debt is at Financial Crisis levels. At some point, the consumer can’t spend anymore.”

No BS shortage ever. There’s always a glut of BS. Trump should put a 100% tariff on BS. You people don’t understand that there are a record number of workers, and their incomes are at record levels. It multiplies… population growth, job growth, income growth… Can’t do the math? Look at the pictures:

https://wolfstreet.com/2025/05/13/household-debts-debt-to-income-ratio-serious-delinquencies-collections-foreclosures-bankruptcies-our-drunken-sailors-debts-in-q1-2025/

Compared to 2020, many Americans have more disposable income and lower housing costs (refi’d mortgage at 3%).

Given those spenders, it would take a tremendous economic shock to destabilize the economy.

Liberation Day tariffs would have been such a shock, and we saw the holders of capital react accordingly and the holders of political power backtrack in response.

Traditional credit looks solid, but what about private credit for the consumer? American addicts got off crack and moved to narcotics over the last 25 years. Are American consumers moving to private credit to get high? The trad Data is assuring that we are nowhere near going into a recession. Let the Fed raise rates!! Also the gig economy keeps credit card balances down, people who gig pick up extra income from a marketplace app have access to liquidity on demand. It’s the new American way; extra work when you need extra money. Thanks for posting the data!

“..but what about private credit for the consumer?”

“Private credit” is included in the 3rd chart from the top, blue line, “Other Consumer Credit.” What you call “private credit for consumers” is not new, it has been around longer than banks. So look at the chart — almost zero “private credit” growth in 20 years, despite surging disposable income.

Thanks Wolf. Yes, raising credit limits makes everyone solvent…

NOT.

Interestingly, I have experienced a few more requests to put rent on a credit card, which I do not accept. The county is looking for another 6% increase in property taxes. As usual, equitax and I will put them back in their place. Regardless, also as per usual, any property tax increase will be passed along to my tenants.

As others keep mentioning, debt levels are “unsustainable”, yet here we all are, sustaining them…

Interesting times.

Can you not counter by saying, sure, you can pay by credit card, but I charge an extra 3.5% fee to cover my costs, and see what happens. People just don’t like writing checks anymore, and I get that. And people love making 2% on their credit card transactions. A $1,500 rent payment = $30 kickback if they pay by credit card. What’s not to love? And setting up rent as automatic payments through the bank account is a hassle, especially if you move a lot. So young people are looking for convenient modern payment options. Writing checks is just beyond outdated fossilized folly for young people today.

There numerous methods of direct payment outside of checks! LMFAO!!!

Come on Wolf. When a 20-something wants to pay by credit card it’s because they just got it in the student union.

“During and after the Great Recession, banks cut credit limits, closed accounts, and licked their wounds, which caused aggregate credit limits to plunge by 28% through 2010.”

Leading up to 2008 I had a Capital One Visa where the credit limit was increased to over $100,000 in a few short years. My monthly bill never exceeded a couple grand on that card but they kept increasing the limit. And offering me balance transfers.

When the GFC hit they chopped the limit to $25k where it’s been ever since. B of A acquired Cap One and I’ve never had any problems using the card a couple dozen times a year to keep it active. I use other rewards cards for most things. Haven’t paid cc interest since the 90’s.

I wonder if some of the posters here are confusing the gift cards that many stores sell. You want to buy someone a gift, but don’t know what. So you buy them a gift card as a present instead.

The store hopes that the card will be lost (or never used). The store then gets to keep the money spent to buy the card.

I wonder if this would be a good place to mention: “In the US, the wealthiest 10% of earners account for nearly half (around 48%) of all consumer spending. This means the top 10% of earners drive a significantly larger share of the economy’s consumer spending compared to the remaining 90%.”

“In the US, the wealthiest 10% of earners…”

That was not the word of God, but an analysis by Moody’s, the same outfit that failed to downgrade the US credit rating until last Friday, 11 years behind S&P and two years behind Fitch. Moody’s “wealthiest 10%” report has already been debunked. But too late, it was turned into clickbait and still gets endlessly spread because it fits some narrative.

But yes, in general, the big spenders are the people with money. You don’t expect the household making $50k a year to spend $500k a year on luxury living. Thankfully, the wealthy do spend some of their money, rather than just hogging it all, which keeps that part circulating.

Thanks for this. There is something I am trying to understand, no BS involved.

The chart on this page from the Fed (click on the third chart down titled “Percent of Balance 90+ Days Delinquent”)

https://www.newyorkfed.org/microeconomics/hhdc

shows that all delinquencies are up in Q1. Yet, in the info under the chart it says that “Transition rates into serious delinquency, defined as 90 or more days past due, remained stable for auto loans and credit cards”, yet the chart shows an increase in auto loans and credit cards for Q1. And your chart shows a decrease for delinquencies, but you are measuring 30+ days.

I am sure there is a simple explanation that you are elaborate on as these all seem to disagree. Thanks!

The NY Fed’s homemade “Transition into delinquency” rate is NOT a “delinquency rate.” I explained their “transition into delinquency” rates in some detail here:

https://wolfstreet.com/2024/08/09/credit-card-delinquency-rates-drop-for-4th-month-despite-confused-reporting-on-the-ny-feds-transition-into-delinquency-rates/

Some years ago, economist at the New York Fed came up with their own metric that they called “transition into delinquency,” which is an ANNUAL RATE (so quarterly, multiplied by four) of a FLOW INTO delinquency, without considering the flow OUT OF delinquency.

But delinquency rates are a LEVEL not a FLOW. Delinquency rate = delinquent balance at month end divided by total balance at month end.

“Transition into delinquency rates” add up all the balances that went newly delinquent in the quarter (that’s a FLOW), without taking out the balances that were cured as people made the payments. And then to get an “annual rate,” they multiply it by four.

It’s a useless misleading concept, but it keeps getting put out there. It’s the most misquoted and misstated thing out there (it keeps getting quoted as a “delinquency rate,” and it is constantly turned into clickbait by people who don’t even know what they’re looking at. That thing should never be cited because people don’t understand what it is and what purpose it serves, if any. And the NY Fed should trash that metric.

So read my article about it. It will answer your questions.

Gift cards have stopped working for a lot of things I used to buy on the Internet. About 50% of the purchases have been rejected. The reason: Most of these vendors want subscriptions: Like “Balance of Nature” Vitamin suppliments. They want a continuous source of income. Gift Cards don’t cut it. So I’m back to using old fashion credit cards. I destroyed my Wells Fargo Visa cards recently to protest their criminal bank screwing up my whole checking account and stealing money from me from forged checks. I’m done with them as well.

The only Person to impress is Yourself,

Ego can be ones worse enemy spiritually and financially.

Yes everyone seems to be flush and able to buy whatever they want. But it’s also odd. Someone who worked hard to save $100,000 in a savings account, used to feel they had a real asset. Now it will barely buy a modest Pickup.

Someone who saves all their life and has 1,000,000 in the bank used to feel like that had some real options, but now it will barely buy a house.

So in many ways we are rich but asset poor. Like: “you will own nothing and be happy”.