The Atlanta Fed’s GDPNow could be all over the place, but nothing compares to how gold imports blew it up this time.

By Wolf Richter for WOLF STREET.

The U.S. Bureau of Economic Analysis (BEA) will release its first estimate of GDP for Q1 on April 30. The Atlanta Fed designed and maintains a model – an algo essentially – that takes in all kinds of economic data for each quarter and provides a running estimate of the BEA’s first estimate of “real” (inflation-adjusted) quarter-to-quarter annualized GDP growth.

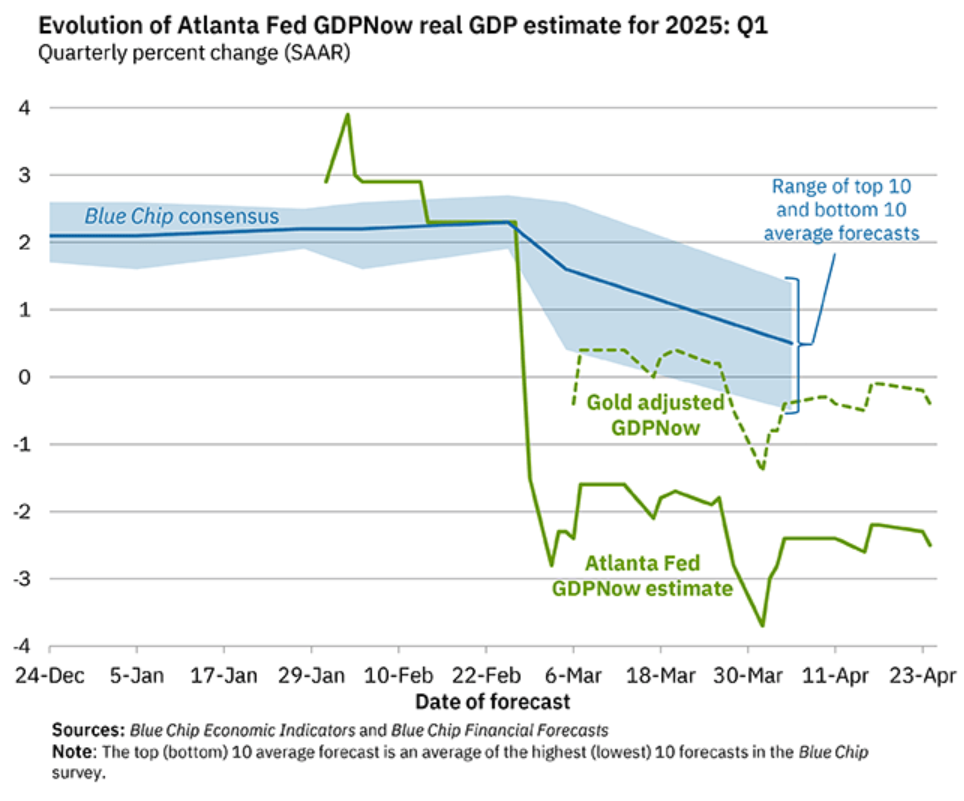

For Q1, GDPNow began providing estimates in late January, and they looked OK, with growth of over 2% annualized. But on February 28, when imports for January were released and taken into the GDPNow model, GDPNow plunged by 5 percentage points to nearly -3%, and went viral. The depression was here, if you believed the clickbait on the internet.

The problem was the spike in imports of gold that investors buy. Imports are a negative in the GDP calculations by the BEA. But gold that investors buy and sell, import or export, is treated like stocks or cryptos that investors buy and sell: It doesn’t enter into the GDP calculation. So imports of gold that investors buy have always been removed from the BEA’s GDP calculation and don’t reduce GDP growth.

But the designers of the Atlanta Fed’s GDPNow model ignored the issue of gold imports. The amounts were small, and it didn’t matter much, until the amounts of gold imports spiked in January, and since monthly amounts are “annualized” (multiplied by 12) to feed into annualized quarterly GDP growth, that one-month spike became a 12-month spike that blew up its GDPNow model, made worse by an additional large amount of gold imports in February, causing the model to forecast a collapse of the US economy.

On March 6, the Atlanta Fed began calculating an alternate GDPNow (the green dotted line) that treats gold imports and exports correctly, by removing them from the GDPNow model. That “Gold adjusted GDPNow” has ranged from slightly positive to slightly negative. The last estimate, released on April 24, was -0.4%. The final estimate will be released tomorrow, April 29, one day before the BEA will release its first estimate of Q1 GDP.

Ignoring gold imports in its GDPNow model went unnoticed until there was an unusual spike in gold imports. And that happens with models: They’re working fine, until they aren’t. The pandemic blew up all kinds of models, including seasonal adjustments and of course infamously on WOLF STREE the CPI for Health Insurance. And those models then have to be fixed in some way.

Last week, the Atlanta Fed published an explanation of what blew up its GDPNow model and how it fixed that in its “New GDPNow Model.” The current GDPNow model will die on April 29. The “New GDPNow Model” (described in detail in this 10-page PDF) will start on April 30.

The Atlanta Fed described the issues and complexities that felled its GDPNow model, and how it included them in its “New GDPNow Model”:

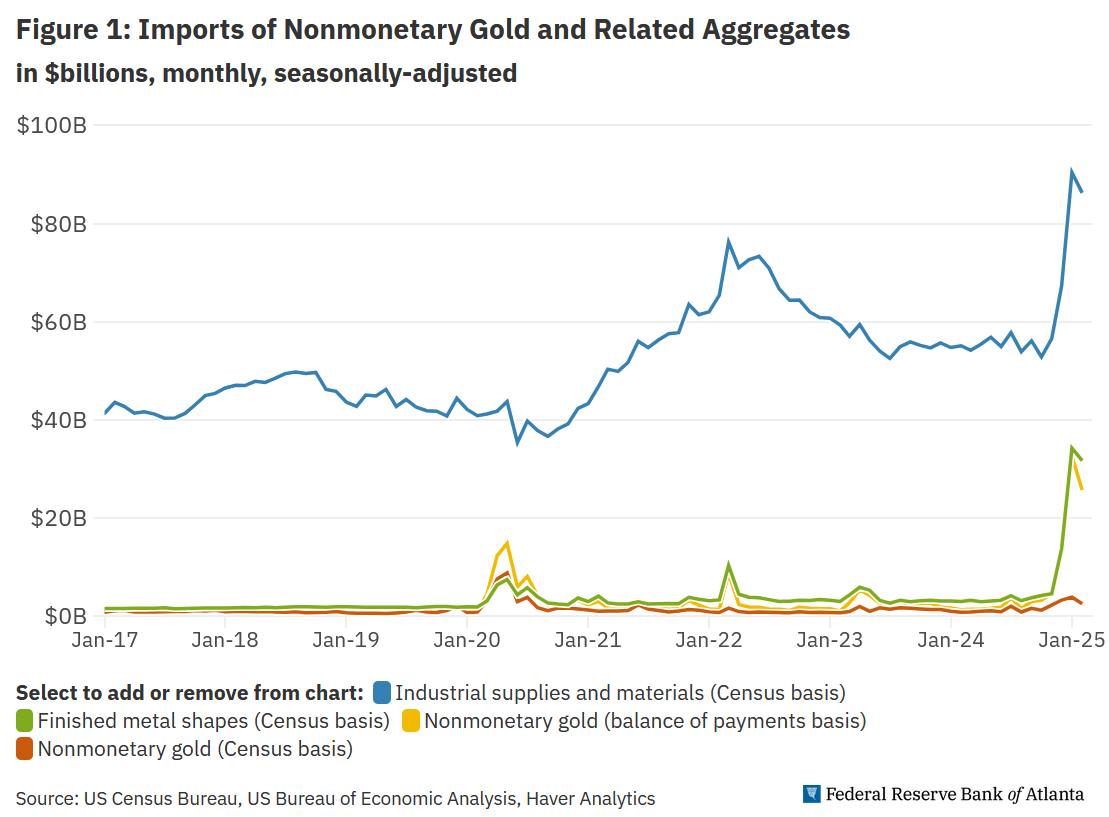

“The measure of nonmonetary gold imports, tracked by the orange line in figure 1 and whose monthly value has never exceeded $9 billion in its 35-year history and has never exceeded $4 billion since 2020, is reported … jointly by the BEA and the US Census Bureau…. Not included in that report, but released [two hours later by the BEA] is a second ‘balance of payments’ (BOP) measure of nonmonetary gold imports. That measure spiked to a monthly average of $29.1 billion for January and February of 2025 (the yellow line in figure 1).”

“Why the disparity in these measures of gold imports?”

“As the BEA notes in an FAQ, the BOP measure of gold includes a portion of ‘finished metal shapes’ imports (the green line in figure 1) that are reclassified by the BEA as gold. Recently, the most important of these commodities by far is identified as harmonized system code 7115900530: ‘Articles of precious metal, in rectangular shapes, 99.5 percent or more by weight of precious metal, not otherwise marked or decorated, of gold.’ In other words, gold bars. According to data from USA Trade Online, these imports surged from $2.08 billion in November of 2024 to $28.69 billion in January 2025 before falling back a bit to $22.96 billion in February 2025.”

“In the 8:30 a.m. (ET) international trade report, the finished metal shapes imports that include these gold bar imports are all classified on a Census basis within “industrial supplies and materials.” These also spiked recently, as can be seen in figure 1 (the blue line). Industrial supplies and materials imports are of interest because they, along with five other sub-aggregates of goods exports and imports, are included in the Census Bureau’s Advance Economic Indicators (AEI) report often released about a week before the full international trade report.”

So how to deal with this mess in its New GDPNow model?

“Unfortunately, the AEI report does not separate gold bars or finished metal shapes from the remainder of the industrial supplies and materials imports aggregate, and this affects our methodology. Is there a way we can utilize the international trade data in the AEI until the full report is released?

“A number of analysts have noted Swiss gold exports to the United States have surged. According to Swiss-Impex data and Federal Reserve Board exchange rates, Swiss gold exports to the United States spiked from under $400 million in each of the first two months of 2024 to $17.2 billion in January 2025 and $14.8 billion in February 2025.

“The reason for the spike is likely due to the move of smaller gold bars, stored in London, to Switzerland, where they are refined into the larger gold bars acceptable in the New York market. These Swiss data are often released about a week to ten days before the AEI, and Comex data on gold inventories are available even earlier.

“Nonetheless, because this data is not available from US government sources and the industrial supplies and materials trade data in the AEI is not further disaggregated, we discard that trade data when using the report to forecast net exports. We do, however, use the remaining trade data in that report as described here”….

Long live the “New GDPNow Model.” Until the next thing blows it up.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

When GDPNow breaks down, at least the economists don’t eat the tourists.

one matter of concern, money that goes into gold is leaving the economy.

The amount that the buyer pays is the same as the amount the seller receives, minus fees, spreads, etc., received by the middlemen. So the buyer takes money out of the economy, and the seller puts it back into the economy? But maybe the buyer’s cash was never in the economy, it was in a bank account, and the bank had put that cash on deposit at the Fed (as part of its “reserves” to earn interest on), and thereby removed it from the economy. So that buyer’s cash wasn’t “in the economy” in the first place. There are $3.4 trillion in reserves at the Fed right now. There are other possibilities here too. Nothing is simple.

Hi ambrose,

My wife was a manager for Deak Perrera through its transition to Deak International and an eventual Thomas Cook takeover of their FX/precious metals business.

Back in 1980 the Hunt Brothers tried to corner the silver trade and the precious metals market blew up; $50/oz silver and $900/oz gold. Those were the days.

Then came the inevitable bust. Keep in mind gold trades per se don’t directly affect the economy any more than equity or debt trades do.

There are an estimated 250,000 tons of gold above ground, half of which is in jewelry. That’s $25T or so at today’s spot. Contrast that value to BTC; 21 million at $90K or $1.9T.

What killed the Hunt’s trade was the above ground jewelry and coins. Higher prices creates more supply in the medium term than demand, in my experience. Making any guesses as to the effect of fluctuating gold prices on the economy is an uncertain endeavor in my view.

Regardless, best regards to all and RIP Nicholas Deak.

No what killed the Hunt brothers was down to two simple facts:

1. The COMEX changed the rules.

2. The Hunt Brothers bought silver futures and not physical silver.

Had they bought physical silver the rule changes would have no effect on them and they would have been okay.

When you have an exchange that can unilaterally change the rules and force cash settlement of a futures contract at a price that they alone can establish then you are in trouble.

With all commodities, especially gold and silver, of you don’t physically own it, it isn’t yours and it isn’t real.

“The measure of nonmonetary gold imports, tracked by the orange line in figure 1 and whose monthly value has never exceeded $9 billion in its 35-year history and has never exceeded $4 billion since 2020, … that measure spiked to a monthly average of $29.1 billion for January…”

Boy, that’s ripe for a little internet disaster porn. Heading over to Zero Hedge.

Interesting, that’s definitely a massive revision to the upside. It still leaves GDP projections in the red though.

Bad news is much less bad, but still bad.

The new version of GDPNow (“gold adjusted”) is in the red, but only slightly (-0.4%). I think a slight negative reading in the BEA’s GDP is a possibility.

I just want to point this out here in terms of general imports:

When you buy a $20 item from Temu, shipped directly from China, that $20 boosts consumer spending and is added to GDP, but it also boosts imports by $20, and the entire $20 import is subtracted from GDP. So GDP impact = +20 -20 = 0. This is why Temu’s direct sales have not boosted GDP, and why the collapse of Temu’s sales will not reduce GDP.

If you buy the $20 product from a US manufacturer, and none of it is imported, than the $20 is added to GDP, and nothing is subtracted (no imports), producing a net increase of $20 for GDP.

This is the best example I have found that explained how imports reduce GDP. They don’t. They just cancel out the foreign production based consumption.

You misread this to fit your own narrative. Imports ARE a negative in the GDP formula, and thereby wipe out a positive, such as consumer spending. Imports are insidious when they get large.

This is also a good illustration of why GDP does not equal “the economy”.

A fictional “balanced” economy that imported everything it consumed and exported an equal value of product would have a GDP near zero. And yet everyone would be busy making stuff.

Arguably, if you draw a line around an area in the US and calculate its GDP, it would look a lot like this. Some county in West Texas produces little more than cattle that are exported out of the county, and almost everything they consume comes from outside the county. All that work for zero!

“All analysis is a model” – Nobel Laureate in Economics Dr. Ken Arrow.

I think the economy is stronger than gDp shows:

Manufacturers’ New Orders: Nondefense Capital Goods Excluding Aircraft (NEWORDER) | FRED | St. Louis Fed

March retail sales were very strong too.

With 6-7% fiscal stimulus, loosey goosey financial conditions (thanks to Fed created reserves), if the economy is not booming then it means America is screwed.

The true health will only be revealed when policies normalize….if they ever do.

i don’t know how honestly it’s presented, but there’s an article cnbc now about how the wealthy increased spending while others cut back. it seems that my theory that the top will continue to spend as long as the stock bubble is maintained, which the media has made the average american think is necessary for their own survival.

Franz G,

“The others” have not cut back — see the huge boom in used vehicle sales and new vehicle sales all year. But the big spenders are what really matters to the economy because they spend so much, AND because they make economic decisions because they run or own companies, and they make employment decisions, investment decisions (new factory), etc. If they cut back in their spending and their companies’ spending and investment decisions, the economy tanks.

okay, but let’s say we all agree wealth inequality is a problem. if the top, whose spending and investment decisions are driving the economy, how do we deflate the asset bubble and mitigate wealth inequality without tanking the economy?

Franz G, “okay, but let’s say we all agree wealth inequality is a problem.”

It’s not a problem for the wealthy. It’s called capitalism. Wealth inequality is a problem for socialists and communists, until they become wealthy.

thurd2, if the inequality happened organically, i would agree. in this case, it’s a result of poor government policy.

the question then becomes, are we obligated to maintain the stock bubble, and thus, inequality, to prevent the wealthy from stopping consumption and causing the economy to tank?

In Monty Python and The Holy Grail there’s a scene:

SIR LANCELOT: Look, my liege!

[trumpets]

ARTHUR: Camelot!

SIR GALAHAD: Camelot!

LANCELOT: Camelot!

PATSY [the serf]: It’s only a model.

Ah, I thought I spotted an arbitrage opportunity when I saw that. I thought GDPNow was adopting a change in method not used by the BEA. So thanks for setting me straight.

There’s still a chance markets crash on Wednesday because even after the adjustment it looks a lot like a recession announcement.

And I wonder about the effects on PCE, reported the same day. March CPI was low so the combo effect of falling GDP and PCE could look very recessionary to those who don’t read wolf street.

There was an arbitrage opportunity. Gold prices had been about $20 lower per troy oz in London compared to New York.

J.P. Morgan alone moved $4 billion in gold reserves from London to NYC this February.

Traders moved about 400 metric tons of physical gold to the New York prior to the tariffs.

Chris B,

“… even after the adjustment it looks a lot like a recession announcement…”

Recessions in the US are called by the NBER, not the BEA. “Recessions” have always required a broad economic downturn, including in the labor market, and there has been no downturn of the labor market. A negative GDP reading alone — such as caused by a surge of imports and a big change in private inventories that have nothing to do with an economic downturn — never triggered a recession call before. We’ve already had a few of those.

So for a recession call you need to see a substantial series of big increases in weekly initial unemployment claims, a couple of nonfarm payroll declines, etc… a group of data in the labor market that show that the labor market is turning down. And so far, that hasn’t happened. It could happen, but it hasn’t yet despite the government job losses.

I should have said “recession warning signal” to be more clear. Sentiment is in the garbage can. Investors are primed to see one quarter of negative GDP growth and interpret that as the likely start of a recession to be announced by the NBER in a year. A clap of thunder can set off a stampede, even if it is a misread of a statistic.

You are right that surging imports did this before. It happened in 2022 IIRC. Investors took the opportunity to flee. In hindsight… what a buying opportunity!

Tariffs had nothing to do with it.

The gold was needed to settle demand for physical settlement.

Australia also exported a lot of gold to the US during that time period as well.

My new formula: GDP = Mindless Consumption (C) + Inbred Corruption + DisInvestment (I) + Market Lurches (M) + New Forms of Predation on Unprotected Consumers (F) + Continued Government OverSpending (on different cronies) (G) – Collapsing Exports (X) – Collapsing Imports (M) – Toilet Paper Currency Gyrations

The really important question is who bought the huge amounts of gold which were imported. The buyer clearly had very, very, very deep pockets. Was it the US Treasury or Fed?

Well we will never know.

There have been huge physical delivery out of the COMEX over the past several months.

As this was classified as non-monetary gold it should NOT have been the Fed or the US government.

Had it been monetary gold then the price of gold would have soared by thousands more as would have indicated huge trouble with their supposed gold holdings.

This is the first article about Gold I think I’ve read on Wolf Street – and it’s not exactly about gold. At least not about Gold as a monetary metal.

Lots of reasons floated for why Gold is leaving LBMA and coming to US. Some say there is an arbitrage play, but that seems to have been there for decades and is kind of the underpinning of the whole Gold derivative paper trade – or at least thats what some articles assert.

Some way it was a tariff scare.

Some say it is a reflection of a run on Comes Gold liquidity as Futures contracts are stood for physical delivery in increasing volumes.

I don’t have any idea what the truth is. The FED and “mainstream” economists assure me that Gold has no monetary role any longer. I don’t know the truth or falsehood of that either.

But can we still agree the price is some sort of signal ? Probably, but good luck on finding any agreement on what it’s signaling. Every answer has an element of “talking your book” to it.

So much noise, so little information.

“This is the first article about Gold I think I’ve read on Wolf Street…”

March 31 was the most recent article where gold played a major role and appeared in the title, and it also sort of answered one of your questions:

https://wolfstreet.com/2025/03/31/status-of-us-dollar-as-global-reserve-currency-central-banks-diversify-into-other-currencies-and-gold/

April Fed Reserve I think has reduced QT down to MBS and 5 billion roll off treasuries. I did not understand why the Fed slowed QT this was before tariff discussion maybe to soften the tariff scare .

If GDP is lower as a result of deficit spend then the front run tariff buys may be the reason for the negative GDP and can be explained away