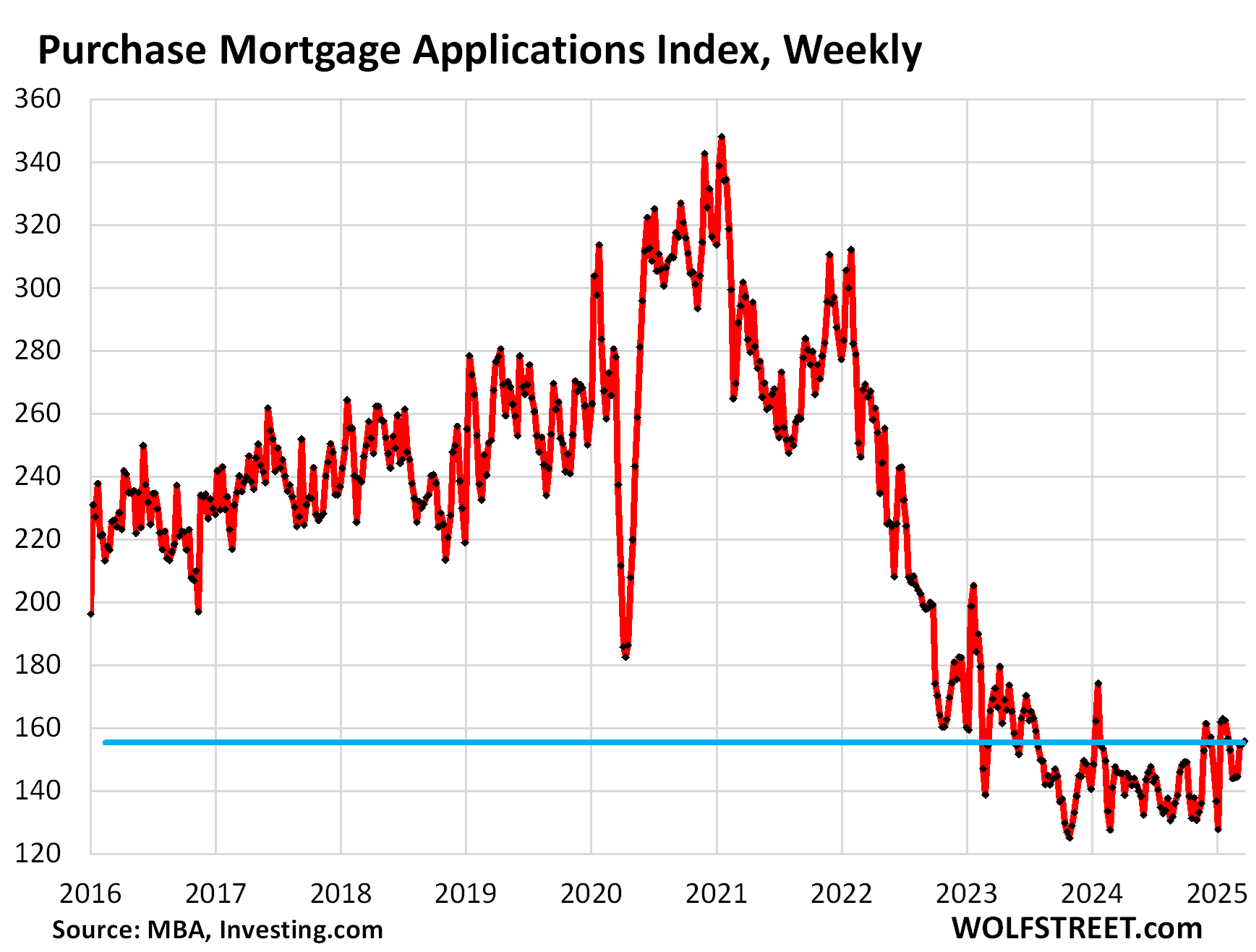

Demand for mortgages to purchase a home has plunged by nearly double the rate of sales of existing homes.

By Wolf Richter for WOLF STREET.

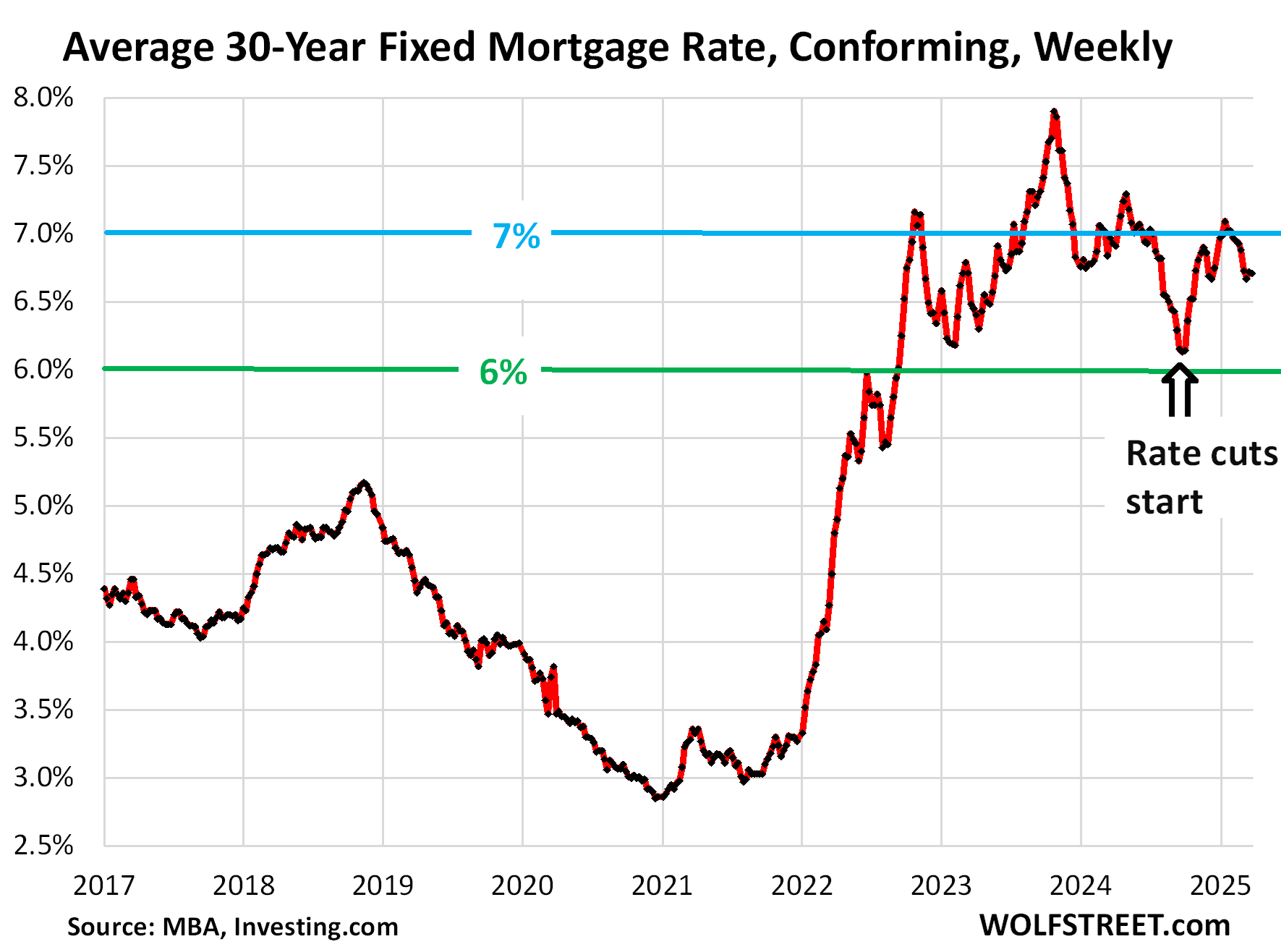

For the past four weeks, mortgage rates have stabilized at just over 6.7%, with the average conforming 30-year fixed mortgage rate ticking up to 6.71% in the latest week, according to the Mortgage Bankers Association today.

The combination of what were normal-to-low mortgage rates in the pre-QE era before 2009 and the fantastical prices today, after the huge QE-fueled run-up in recent years, has whacked demand: Sales of existing homes plunged by 24% last year from 2019, and this year doesn’t look much better, with February having been the worst February since 2009.

But demand for mortgages to purchase a home has plunged by nearly double the rate of sales of existing homes: by 42% from 2019.

Between mid-September and mid-December, the Fed has cut its short-term policy rates by 100 basis points, just as inflation had started to re-accelerate. A dovish Fed in face of rising inflation spooked the long-term bond market, and long-term yields shot up, including mortgage rates.

The MBA’s measure shot up by nearly 100 basis points, while the Fed cut 100 basis points, widening the spread between the two by 200 basis points.

The market essentially told the Fed that was considering further rate cuts in this inflationary environment: “Go ahead, make my day!”

Did the market teach the Fed a lesson, that cutting rates in an inflationary environment can push up long-term rates, fast? At any rate, it turned hawkish, putting further rate cuts on hold and talking tough on inflation, and long-term yields eased off a bit, but not much, and after the initial drop, mortgage rates have been hung up at 6.7% for the fourth week in a row:

Mortgage applications to purchase a home have been wobbling along since October 2022 not much above the record lows of November 2023 and then again of February 2024 (the data goes back to 1995).

In the most recent week, they ticked up a hair and were up by 6.9% from a year ago, which had been near the record-low of February 2024. Compared to the same week in 2019, purchase mortgage applications were down 42%.

This 42% plunge in purchase mortgage applications documents to what extent the housing market remains frozen because prices are still too high and buyers have gone on strike – though prices have started to come down in a number of markets.

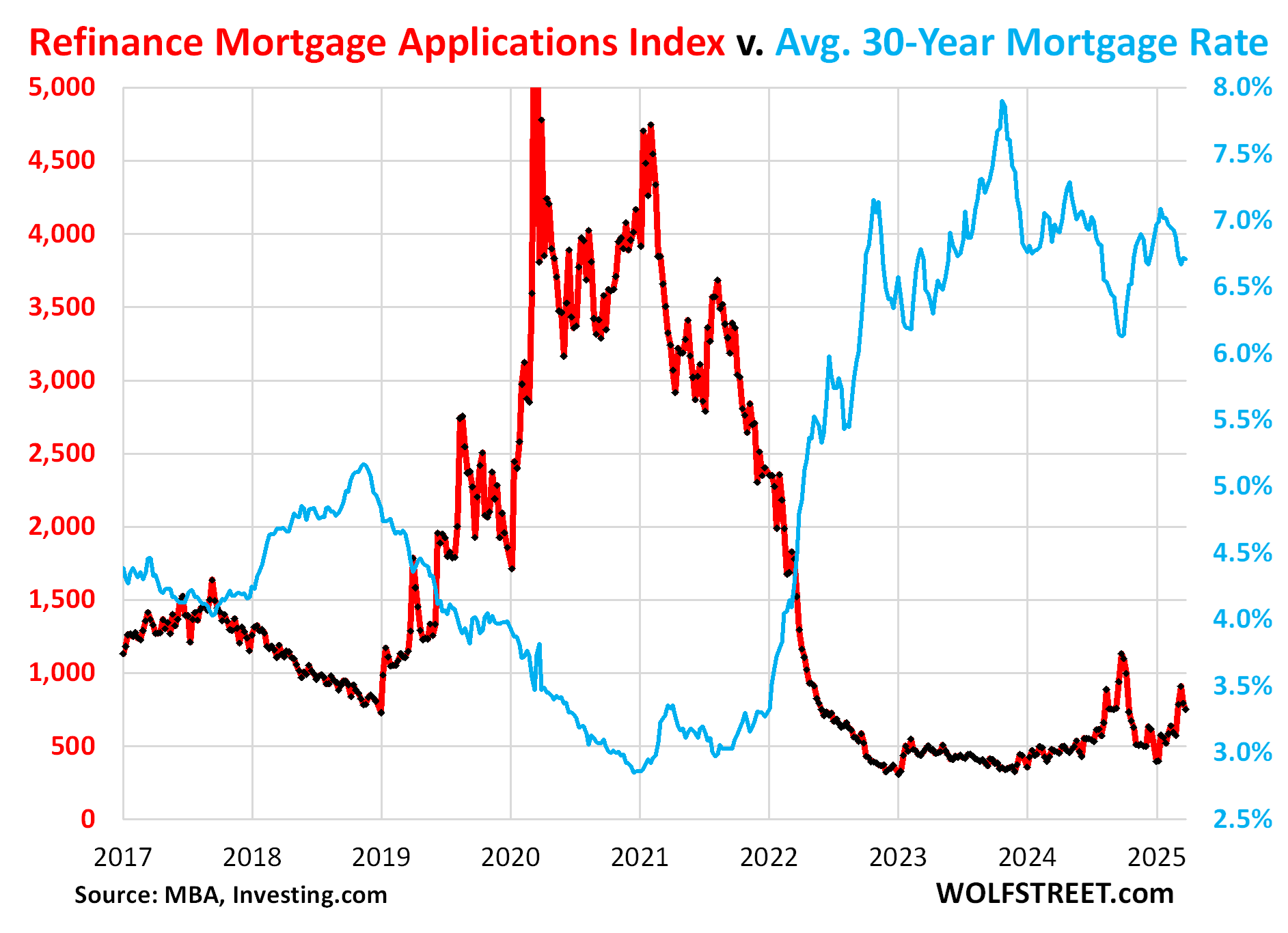

Mortgage applications to refinance a home began collapsing spectacularly when mortgage rates started rising in 2022, following the huge boom during the 2.5%-3.0% mortgage-rate era.

But people still need to do refis for various reasons, including to draw cash out of the home, and interest rates on refis are lower than rates on HELOCs or other types of loans. So the refi business has picked up some, having roughly doubled from the low point in early 2023, but remains at depressed levels.

In the latest reporting week, refis were up 49% year-over-year, but still down by 42% from the same week in 2019, and by 77% from the same week in 2021.

This chart illustrates the inverse correlation between mortgage refis (red) and mortgage rates (blue).

And yet, supply has surged to the highest in years. Supply of unsold existing homes on the market in February, at 3.5 months, was the highest for any February since 2019, and higher than in February 2018.

In terms of new single-family houses for sale: Inventory has surged to the highest since the peak of the housing bust, and in the South has been above the peak of the housing bust for months.

So buyers remain on strike. They’re waiting for prices to come down, and they’re waiting for rates to come down, though in an inflationary environment, that may not happen to the extent they’re hoping for.

And while they’re at it, they’re waiting for their household incomes to rise, and in the current inflationary environment, that’s happening faster than in the prior decades, but it will take years before it makes any significant difference. So the buyers’ strike, already in its third year, may last a while longer.

But a combination of lower prices and higher incomes would work wonders over the years in helping the housing market get over the ridiculous QE-fueled price spike and return to some form of normality.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My real estate friend whom I have known for years has told me things are frozen up here in the Houston, TX area. A few unbuilt lots near me (new development) have been graded and set for the foundation, but have been sitting idle for several months now. I think the builder (Lennar) is delaying starting these homes until they move some completed ones (which are discounted and moving slowly).

These are starter homes selling at around $225,000 – $275,000 ($175 sq/ft).

Anthony A.

After the next hurricane season, look for insurance rates on these prospective new homes to double and triple, to rates which exceed the principle and interest payments on the mortgage. Insurance companies are way behind on adjusting their rates for the new risks associated with the severe weather. Of course, no will tell the suckers that buy these home these unpleasant facts.

Swamp,

They’re not having to adjust to the risks of severe weather… That risk hasn’t changed. They’re having to adjust to the effects of INFLATION of construction costs, which has changed A LOT. I can draw a straight f’ing line for almost all the issues in this country… this WORLD… to massive, uninhibited credit emission from consumers, banks, national treasuries… you name it. Until people finally realize math matters, we’re utterly screwed and will never be able to keep up with rising, nominal prices for anything.

I’m not holding my breath, and am grateful I’ll be dead relatively soon so I can quite living in this crap. I feel sorry for my kids, though.

We had hurricane Beryl hit last year. I’m 50 miles inland and had no damage. My smoker blew over in my back yard!

My renewal this year was $1,200 for homeowners standard policy. If you live here, the further inland you are makes a huge difference. If I was south of Houston, I could see $5 K policy rates for my small house.

I’m not saying policy rates won’t go higher, just saying it’s not happened up until now. I’ve been here 30 years now.

There is the crowding out of the private sector as the gov’t sells more securities, raising interest rates above levels that would otherwise exist, and raises taxes curbing spending.

I doubt that slightly lower rates or slightlt lower prices will fix this mess. All the other costs of owning a home are up double digets.

With the uncertainty of the economy and inflation very much alive and well, many will continue to avoid the homeowner trap.

I do not know how big a price drop needs to happen, but 5 to 10 percent is not enough.

I am soon to sign a lease on an apartment. I read Wolf’s articles almost daily and check Zillow here an there in my region. This buyer has his checkbook stiffly secured in his pocket. My hand isn’t yet hovering over it in a quickdraw position. I am certainly not buying with a 10% discount on current prices. 25%? Now we’re talkin’.

Anecdotally, my barber told me he is going to refinance his home soon. I didn’t ask why, because that’s his business, but it’s an example that people do indeed refi (he purchased his house within the last year).

Why would somebody refinance if rates go down a mere .4%? The origination costs eat up the savings. It’s a sign some people are over leveraged and can barely make the current payments.

Bobber, that is one of my hypotheses. The other is that he bought at peak mortgage rate around 8%. So a reduction from 8% to 6.7% might make it worth it.

Some newer mortgages contain contain a refi clause that allows borrower to refi w/o much cost. My office manager has one. Just a few hundred bucks to refi a 500k loan.

5-10٪ price drop, as opposed to the 5-10٪ yoy increases we have been seeing, would be a welcome relief as someone who is looking for a home.

But I do have to wonder, if the drop is due to a slowing economy, will the money keep coming in to support such a purchase.

the money will come in for people who were responsible. not the paycheck to paycheck people, who are whom the u.s. government caters to, in all income brackets

Cost of “owning” a home certainly went up but if someone is renting, those costs are being passed down to them anyway. The bigger picture is mortgage rates, which are now where they were before 2008. People got used to once in a generation extreme low rates and think those will come back. They might, but under conditions where most people would be afraid to buy.

they’re not always being passed down. if you bought at the peak in 2022, it’s likely the rent of your tenants is not covering your costs.

@Franz G the number of people that “bought at the peak in 2022” with “tenants is not covering their costs” rounds to zero (since the people that bought with loans would have to show that rent MORE than covers costs – including the loan and the people that bought without loans are doing fine.

Home builders need to downsize. The closets in today’s homes magnify the long-standing change in wealth. The history of the average square footage has more than doubled. There are plenty of cheap vacant lots in the inner cities on which to tear down and rebuild.

spencer,

I don’t have enough space. I am remodeling my bathroom so I can put an 85″ TV in front of bidet.

@Glen someone just tols me that 85″ is the new 60″…

Our young family was looking to buy a home in Western PA for about 2 years now. We gave up our last search after losing nearly a dozen offers due to other buyers waiving inspection and going well over asking. The former being something we would never do due to the age and lack of care of many homes Western PA.

I suspect many of the buyers who were also not able to buy (our fellow losers, if you will) have left the real estate market much like we have. We are fortunate that our incomes are healthy enough that we can continue to rent AND grow our cash/treasury fund balances.

We are just sitting on the sidelines letting this play out. For now, we don’t feel the need to participate in the craziness that has engulfed the housing market, particularly in Western PA. We’ve been able to successfully arbitrage renting versus home ownership. I think in the worst case, our rent may be costing us an addition $100-200 a month over buying. Of course, that’s under a lot of assumptions since I have seen many inspection waivers regret their decisions due to costly repairs needed a few years after buying their inspection free home.

My son is in your situation. He is currently renting at about half the price of a mortgage for the same house. I believe that rents will go up and house prices will go down further in the future like they ALWAYS do to create a balance.

He and his friends are no longer bidding on houses. They are waiting for terms close to sanity before they buy.

Wolf has great charts showing when this happens. It was a no-brainer to buy a house in 2012 if you were employed and had a down payment. Save and stay employed. History repeats itself.

Prices will follow. It’s the good times for the renter using logic the Fed used about 10 years ago. What cannot be articulated is a floor price. With currency debasement through the roof, I think people will have a hard time processing the floor price is where it’s at. 300k? 400k? We have a better chance seeing a rise in wages than all out depression. That would happen if prices collapse.

We bought our house sight unseen during “coming soon”. Totally unlike us, but the best thing we ever did.

Not that I’m recommending it. Especially in W. PA.

This fiasco should be a reminder of the price that we pay for having the Federal Reserve Bank. Their power to manipulate interest rates and the money supply allows them to distort the economy in many ways. But it seems that nobody wants to discuss making any changes. Many young people are blaming the Boomers. Maybe they are right. They curse the high prices, high interest rates, and wages that don’t keep up with the price inflation. Many Boomers are sitting pretty, unless they want to move. I was thinking about it the other day. But the rent is too darn high!

If you are a boomer, it is the cost of maintenance and repairs that is the killer. You may own your home outright, but $50K for a new roof is a stretch. Many older homeowners are hoping they will not be around when these bills come due.

And of course, if you live in the NYC area, you may be looking at $25K a year in property tax.

We are getting a new roof next month. 3100 sqft (of roof) for $13.6k including tear off and haul away. Two quotes came in at exactly the same price… Live in NYC? There’s your problem!!

re: “it seems that nobody wants to discuss making any changes”

That nobody is the American Bankers Association. They own the bank’s legislation.

We’re boomers looking to move and downsize. Like many others, there’s still one last kid to launch and rents are high enough to create difficulties there. We look at the smaller homes on larger lots in areas far away from job centers and the prices are still insane, but showing downward movement. A smaller house on a larger lot is about the same price as a large house on a small lot. Why would boomers give that up? It’s not a reasonable trade. The math at this interest rate only works if the replacement house is 20% lower in price.

“Americans have suffered under crippling inflation, and the Federal Reserve is to blame,” said Rep. Massie. “During COVID, the Federal Reserve created trillions of dollars out of thin air and loaned it to the Treasury Department to enable unprecedented deficit spending. By monetizing the debt, the Federal Reserve devalued the dollar and enabled free money policies that caused high inflation.”

“Monetizing debt is a closely coordinated effort between the Federal Reserve, Treasury Department, Congress, Big Banks, and Wall Street,” Rep. Massie continued. “Through this process, retirees see their savings evaporate due to the actions of a central bank pursuing inflationary policies that benefit the wealthy and connected. If we really want to reduce inflation, the most effective policy is to end the Federal Reserve.”

“The Federal Reserve has not only failed to achieve its mandate, it has become an economic manipulator, directly contributing to the financial instability many Americans face today,” said Sen. Lee. “We need to protect our economic future, end the monetization of federal debt that fuels unchecked federal spending, and put American money on solid ground. We need to End the Fed.”

Agree, would be great for the nation if Massie’s fellow Congress members and the voters all acted as one to achieve that.

If I understand your article correctly, Mortgage applications are down much more than sales. My conclusion is that the difference is the buyers that are paying cash. Last month, in our county, 65% of sales were to cash buyers.

Yes cash buyers are part of the difference. Cash buyers account for about one-third of the buyers. Lots of people with enough money pay cash. It’s hard to earn 6.7% tax-free and low-risk in the fixed income market. And that’s what it means if you don’t get a 6.7% mortgage but pay cash. And if you’ve got enough money, and don’t have a mortgage, you can self-insure if you understand the risks that the house is exposed to, and have the money to lose it. That additional savings increases the return on your investment. But it adds some risk. People make that calculus after they pay off the mortgage as well.

The other part of the difference is that not all mortgage applications lead to actual mortgages. The application might be rejected, sales fall apart, etc.

I live about 10 miles inland in Florida. Across the Indian River Lagoon from Cape Kennedy. I keep a solid roof on the house and have hurricane shutters. My homeowner’s insurance has a deductible of $30,000, but I pay $1200/year on an older house. My neighbor has a $3000 deductible and pays $7200/year. My neighbor is betting on a much higher risk of a catastrophic hurricane in the next few years than I am, since there hasn’t been one here in recorded history (first settled in the 1840’s).

I heard there are close to 1 million NPL’S on FHA’s books? That were in foreclosure forbearance, some as much as 30 months delinquent. If these clear, how much will it affect home prices? Thanks

That’s not much higher than before Covid. FHA always has a pile of NPLs. It’s the government’s subprime-mortgage insurer. They modify the mortgages, add the missed payments to the end of the mortgage, so it lengthens the remaining term of the mortgage and increases the remaining balance of the mortgage. But nearly all these houses have gone up in price over those years, by 50% in three years many of them, they can be sold at a price above loan value even with the additional tacked to the end, and the mortgage can be paid off, leaving the homeowner some cash to play with, and no one loses any money. That’s why there are so few foreclosures. There is a lot of clickbait nonsense circulating about this suddenly, like someone just woke up.

Mortgages don’t become a problem until home prices plunge massively across many markets below loan values. Which is what happened during the housing bust.

My spouse and I are still on strike. We are retired and own our current home. We were looking to retire elsewhere but are staying put for now until prices come down. We don’t care about interest rates. We do not want to buy a home that’s selling for 30-40% more than it was worth 4 or 5 years ago. Instead of looking for homes, we’re going to travel more.

If you can sell your existing home for 30-40% more, why do you care if the home elsewhere is also 30-40% more? It’s a wash. If they both lose 30%, it’s still a wash.

@UrsaTaurus I was having a similar conversation with a college friend that would not pay $12 for a glass of wine since it was “too expensive” (even after I reminded her that she is making about 5x more than she did in the early 80’s when she was happy to pay $3 for a glass of wine.

right, as people get more advanced in their careers, they like to actually earn more in real terms, not just keep up with inflation.

We’re looking to move to a different region of the country and we’re not going to get a comparable home for the same price. We’ll have to pay $50-$60k more for a comparable home. If home prices were lower, we wouldn’t have to pay as much premium.

With persistent inflation on everything “home-related” it is making less and less sense to be a homeowner anymore. Have you tried getting anything remodeled or repaired lately? Services Contractors are literally asking more than my real estate attorney (who charges $350 an hour) to change a damn light bulb. One of my borrowers, I am a private money lender, just got a quote for homeowners insurance for the year at $4K to insure a $500K replacement cost!! (Not sure if I wrote that right). And property taxes haven’t gone down at all from all time high in my area. I’ve really been weighing the advantages of renting over owning lately, and man, there sure are ever increasing advantages in being a tenant!

Where does this go????

I’ve seen much worse on the insurance hikes, it’s got to be pushing people to their breaking point – where will the money come from?

Coming up…cash out refis to pay insurance and property tax inflation on absurdly inflated home prices…

If you need to hire out your light bulb changes, you have no business owning.

I hear rentals also have light bulbs.

That’s a bargain on the house insurance. Here in San Antonio, it would be over $5000 a year for the insurance on a $500,000 house. Then the property tax would be another $4300. About $10k a year combined.

$400,000 house, $1,000/year insurance, $5,000 deductible. Eastern PA.

Actually, I’d like to see a lot more examples of insurance costs from around the country.

Some of the financial sources I follow indicate a *lot* of churn/activity in all the insurance markets, but mostly in the background so far.

I’m aware of the chaos in the FL home insurance/condo assessment market due to home price inflation and mandatory structural retrofits (in the wake of the condo building collapse a few years back) but I’m getting vague indications of insurance market spikes/disputes from across the country and in many different insurance markets.

I’d like to hear stories from Wolf’s readers.

Raleigh NC area, less than 5 yo house, ~450k now. Insurance went from $900 to almost $3k in just 3 years.

It’s still not as bad as folks in coastal areas pay, but it still hurts. I used to pay less than $2k/year for house + auto combined, now it’s close to $6k with more rate hikes supposedly on the way.

I think my total salary inflation adjustment last year was in that range (+2-3k or so), and it looks like it’s all going straight into the insurance companies’ pockets. To say I’m not happy at all would be an understatement – I used to be happy about getting even small raises, but I don’t know how much of a raise I would “need” to just stay where I am…

They should be more careful. Once people realize how easy it is to do some services in their own, they’ll never buy those services again.

Men’s haircuts, brake work, mowing and landscaping, house cleaning, car wash, home repairs, etc.

I have clippers but mostly still pay for haircuts at basic places because I don’t get them frequently and it seems the stylists don’t make much, so it helps them get by. Similar to charity, choosing to pay more occasionally, modest restaurants being another example, to help lower income workers.

I check FB Marketplace for 2nd hand tools and surplus building materials. I watch how-to videos on YT at night before bed. Menards has “11% off everything” if you remember to mail in the rebate form. You can even rent their pickup truck to bring your purchases home. Does anyone invest in sweat equity anymore?

One item I’ve observed here in the midwest in an attitude of high price entitlement among sellers. My neighbor with a similar house got this price when he sold a while back and therefore I should too. I think (some of) the RE agents are a factor in this attitude.

The sellers need to realize it isn’t 2022 anymore. That was a unique selling environment. It has changed. And many potential buyers are seeing more value in waiting. I still think paying (anything close to) current listing prices continues to carry a relatively high degree of risk.

Any potential buyer who is old enough to have observed the 2008 – 2012 RE era first hand will be understandably cautious.

i can assure you that that isn’t limited to the midwest. that’s everywhere, and that’s why prices are dropping so slowly outside of austin and a few others. no one is willing to accept that they missed the peak.

the paradox is, the reason 2022 prices were so high besides mortgage rates being 3% is that people weren’t selling, so inventory was low. but if everyone had tried to sell at peak 2022 prices, then prices wouldn’t have been where they were.

Busts in equities are pretty common. Real estate busts are far more rare.

In the history of the U.S. there have only been 4 real estate crashes while the stock market bounces around like a ping pong ball. IMO the real estate market has gotten tight because of all of the corporate ownership, 3% mortgage holders, homes owned outright and vacation rentals.

People are disinclined to sell performing assets!

Overbuilding new homes hurts the builders and those that lose their jobs and have to sell. Mortgage rates are not likely to go down with tariffs raising the cost of literally everything. Those costs are real and pervasive.

I’m not holding my breath for a real estate crash, softening? Perhaps 10% at the most (with the exception of Florida), Florida is a disaster waiting to happen!

“Real estate busts are far more rare.”

That’s not correct. Real estate busts are very common in specific regions or metros, following local bubbles. “There is always a housing bust going on somewhere.” There is a long list of those local or regional bubbles and busts, some of the busts lasting decades.

You don’t own the national median home at the national median price. You own a home in a specific market, and those local markets dance to their own drummers, and many of them had big long housing busts.

My favorite example is Tulsa because I bought a condo there during the bust in 1989, from the bank that had ended up with it after the prior buyer had defaulted on the mortgage. It bought at price that was 60% below the amount of the defaulted mortgage. So the bank took a huge loss. And the bank had mortgages out on a bunch of units in that tower. Then the bank collapsed, and my neighbor bought his condo, mirror image of mine, for 20% less from the FDIC. I sold in 2000 nearly doubling my money, but still got 25% less than the bank had financed on it in 1985, but that was kind of an interim peak, and then those buyers sold in 2014 (now on Zillow) for 30% less than I got, and about 45% below the bank’s mortgage balance in 1985. It’s just last year that the condo sold at an asking price higher than the bank had financed in 1985. It took nearly 40 years!

There are many other markets like this all across the oil patch, some of which recovered a lot faster, and others never did. Then there is rust-belt cities, such as Detroit, where the housing busts lasted many decades. There were housing busts in Southern California when the Cold War ended and the defense industry cut back. There are many other examples of local housing busts.

So you don’t own the national median home at the national median price. You own a home in a specific market, and those local markets dance to their own drummers, and many of them had big long housing busts.

But to have these bubbles and busts happen across the entire country all at the same time is rare, and that’s the result of monetary action because mortgage rates are national, and when low mortgage rates started driving up prices in the early 2000s, the bubble and bust became a near-national issue.

But still, there were some exceptions, such as the oil patch I just talked about, specifically Texas. Cities in Texas had gone through a big housing bubble in the 1980s and then the bust starting in mid-1980 and going into the 1990s, taking down a whole bunch of bank, including MBank, the largest bank in Texas where I had an account. So by the early 2000s, they were just recovering from it and people and lenders had been burned and were careful, and so there wasn’t much of a housing bubble in 2003-2006 in Texas, and not much of a housing bust in 2006-2012. There were some price declines, but it wasn’t much. But after 2012, they went back to the races, driven by national monetary policies, especially during the pandemic, and now some of the cities in Texas are on the leading edge in a housing bust.

Here’s Austin. More Texas cities are here:

https://wolfstreet.com/2025/03/17/the-most-splendid-housing-bubbles-in-america-feb-2025-the-price-drops-gains-of-33-largest-costliest-housing-markets/

And here are some big city condo busts are underway.

https://wolfstreet.com/2025/03/21/where-condos-already-came-unglued-10-big-cities-with-price-drops-from-10-to-22-from-peak/

And we are starting to see a mini housing bust in the DC burbs

“buyers sold in 2014 (now on Zillow) for 30% less than I got, and about 45% below the bank’s mortgage balance in 1985. It’s just last year that the condo sold at an asking price higher than the bank had financed in 1985. It took nearly 40 years!”

That’s probably one of the most important facts you’ve ever put on the site. So much for “real estate only goes up” (pretty much the received, biblical wisdom pre 2008…and post 2012…)

And now we can contemplate the implications of 20 years of ZIRP doing battle with the fundamental economic reality underlying the US economy/international competitiveness,

i agree prices may not drop as much in places that only went up by 10-20%, but in places like nashville, florida, austin, denver, and places that doubled during covid, they’re going to crash hard.

there simply isn’t enough income in those areas to sustain those prices. work remote is largely gone, in my anecdotal experience.

It might be more accurate to say that sellers are on strike. If they WANTED to sell they’d lower the price until the house sells.

Buyers WANT to buy but simply can’t. They’re like people who want to work but can’t find a job that pays enough to live on. That’s not a strike by workers, that’s a strike by employers.

This is insightful.

I put my house up for sale 5 months ago. My realtor has suggested lowering the price, which I am not inclined to do. The house is paid off and the listing agreement expires in May. I will take the house of the market at that point and wait. Cheers.

This reminds me of my friend.

During hb1 his listing expired many times.

He finally sold his home after 2 years but for 40 percent off the original listing price. During that time he rejected many offers slighlt less than the asking price .

This is called chasing down the market.

I see that happening right now. I could show you listings that go down 1% every 2-4 weeks like clockwork.

When the starting price is 40% too high, it takes a long time.

We sold to a cash buyer four weeks after listing having reduced the price twice (Phoenix). We bought the place in 2021 at the peak. I knew I was going to lose some money if we sold within 5-10 years. After commissions and closing costs we lost 2%. I was happy with that. Carrying costs would have been 2% and opportunity cost about 3% after taxes.

“Which I am not inclined to do.” I guess you don’t really want to sell the house, do you? Success requires making reasonable adjustments. What is holding you back – is it greed, or something else?

During Housing Bust 1, it was always delusion. Despite obviously plummeting nationwide house prices, everybody just *knew* that their house was special, their neighborhood was special, their city was special. So they scoffed at offers slightly below asking, but by the time they lowered their ask those offers had disappeared…

This time? It’s hard to say. Since there’s no housing bust (yet), the only real motivation for any non-distressed seller to lower prices is early mover advantage–but that only motivates people who believe that prices will actually go down in the future, and not many people believe that (yet).

There is no housing bust for sure but home prices in some of the hottest markets have plummeted by 20% or more despite the economy being good.

The general direction is down and think what would happen when and if the recession hits.

Despite the good economy, homes prices are trending down albeit slowly is because of historic un affordability.

I never understand when people talk about saving money renting. If you plan to move every couple years, of course it makes sense to rent, given that buying, moving, and selling all cost a small fortune. But I can’t get past the old cliche that renting is throwing money away. I mean, it really is – it is money purely consumed with no lasting benefit.

And for those renting to save for a house: consider living in a cheap place if you can find one. I don’t understand renting a fancy place if your goal is to save for a house. Again, money consumed with no lasting value.

And yes, I know “they” are colluding to totally screw you on rent as well, and they don’t make many small or cheap apartments. Maybe more demand from renters of choice would help?

This is just me. I realize people think differently. I’ve yet to really empathize with other thinking on this matter, although I am open to try.

The catch is you have to invest/save the difference between renting and buying. In that case it’s equivalent to buying, in the sense that the principal you pay down after interest is equivalent to your cost basis for whatever stocks/bonds/ETFs you purchase with the money you save by renting.

Renting is like insurance. You know your max out of pocket. You didn’t throw your money away. You had a roof over your head. You had flexibility to leave.

Most of the time, it works out about like buying an annuity instead of keeping a diversified portfolio. However, there is a clear reason to take that side of the trade.

The house I live in in San Diego cost $4500 to rent. To purchase the house it would cost me $12k per month.

I’d love to buy. But the policies of the reckless fed has priced me and people of similar age out of the market.

My neighbor always talks about how I should buy when he bought is house in the early 90s on a teacher’s salary. I make five times what he makes and still can’t afford it.

Everything is out of whack.

When you rent, you are paying for a place to live. It beats living in your car, and a car has costs. Maybe sleeping on a park bench is a better idea?

My family of four live in Southern California and rent a 1500sqft 3/2 tract home for $5300/month. The same house to purchase would be $2m, leading to a mortgage payment of around ~$15k/mo. After doing the math, I think it makes sense to rent for the long-haul and invest the difference. I know this is contrary to the “renting is throwing away money” argument, but I currently am unable to make the numbers work for buying, unless house prices continue to skyrocket, or rents quickly catch up.

Leaving aside govt policy, you can’t have a major real estate recession without an overall recession. It’s too large a component of the GDP.

That’s a misconception. The US Housing Bust of 2005-2012 (start and end dates vary slightly by local market) CAUSED the Financial Crisis which caused the Great Recession. The recession started in December 2007, two years after the Housing Bust and mortgage crisis had begun. Smaller mortgage lenders were already blowing up in 2006, and about that time, MBS began imploding, by which time the Financial Crisis was already there for all to see if they just looked. Employment and GDP kept growing throughout, even as the housing market was imploding, then employment PEAKED in December 2007 and began declining in January 2008. So that’s how the beginning of the Great Recession was in December 2007.

‘The US Housing Bust of 2005-2012 (start and end dates vary slightly by local market) CAUSED the Financial Crisis which caused the Great Recession.’

Agree.

This is a very interesting post, at least for me personally. In the summer of 2007, I was watching one of the national news programs, which was doing a segment on how home prices in CA were increasing at about 20% a year. My first thought was, “But peoples salaries aren’t increasing at 20% a year, this is all going to come crashing down.” I moved my 401k’s out of stocks to safer investments. In the summer of 2008, the stock market was going higher and higher. I gritted my teeth and stuck to my intuitions. Then the s**t hit the fan in October.

I hope history does not repeat itself here.

IMO: The worst of GFC could have been avoided. It was grossly incompetent of the Fed to let Lehman go bankrupt. They didn’t realise that under UK law, where Lehman had a huge presence, when a bank declares BK it must cease trading, not just that second, that nano second: ‘now’. Hundreds of millions were suspended in mid air. If another bank had just sent Lehman’s currency desk millions of dollars for pounds, they were now an unsecured creditor. That’s when banks stopped lending to each other. Fire the bankers, sure, but don’t stiff third parties.

Given the damage about to come, the Asset Relief Bill, or whatever it was called, injecting 700 billion, or about 2 months of today’s US deficit, seems chintzy.

I bought my family residence in Sept. 2007 and remember very clearly the imploding process. In 2005, there is no sign of weakness in the housing market. In 2006, some weakness were seen but housing prices were still rising and madness was still everywhere. My wife worked for mortgage loans at that time and told me how insanely poor quality the loans were and how people didn’t even care about valuation of the properties.

By the time I bought my house, the prices were already on the way down but I pretty sure I bought very close to the peak.

Nick Kelly,

The US deficit is bad enough at a projected $1.9T in fiscal 2025. No need to double it.

Mortgage interest, property taxes, HOA fees, buying/selling costs and maintenance required to keep your house in the same condition are all also “money purely consumed with no lasting benefit”.

You also forego interest/investment returns on any down payment or other cash you put into the house.

It is definitely possible to save money renting in certain scenarios.

Take a look at amortization schedules. The lucky homeowners who are sitting on 3% or less mortgages saw there principal go down significantly on the first mortgage payment In 2.5 years about 50% of the monthly payment goes towards principal. So those with low interest rates not only get the bennie of lower payments, they get to watch their loan principal drop big time every month.

With a 7% loan that 50/50 day payment doesn’t arrive until year 20. That’s why banksters luv higher rates. Most folks sell within 7 years so they are perennially in debt because it’s like getting a credit that comes with a maxed out $500,000 debt the day the card arrives in the mail.

You should make sure your loan has a “recast’ provision as well. You can look that one up. Understanding how mortgages work should be taught extensively to high school students.

I rent, could “afford” to buy, but renting is cheaper than buying right now, the money I save by renting goes into investments. It’s certainly not throwing money away, it’s throwing money in the bank.

They will get lower prices, they wont get higher incomes, but may get lower rates as the recession forces the Fed’s hand.

UCLA Anderson, which has been issuing forecasts since 1952, said the administration’s tariff and immigration policies and plans to reduce the federal workforce could combine to cause the economy to contract.

Its analysis was titled, “Trump Policies, If Fully Enacted, Promise a Recession.”

Nick Kelly,

Let me start out with this: I love you Canadians, and I love having you on my site.

As Canadian, you know this. But I USian didn’t know this until yesterday when I listened to Alberta Premier Danielle Smith’s passionate speech about the new Prime Minister Carney’s stupid “treason” remarks (you know what I’m talking about). When I listened to her, all lights went on, so now I will share this with my readers.

In the process of crushing Carney, Smith said that there had been a consensus among all Canadian political groups and everyone else in Canada that all Canadian politicians and everyone else should reach out to US politicians, US media, US influencers, US bloggers, etc., to try to manipulate them into an anti-tariff stance.

I didn’t know this was a top-down organized all-out propaganda effort to manipulate US policies to Canada’s liking.

But what I did see was a flood of Canadians commenting, or trying to comment (and subsequently blocked), on this site to spread their anti-tariff message, cloaked in the BS that tariffs were bad for USians when in fact they’re bad for Canada.

Premier Smith likely exaggerated as to how bad it would be for Canada as some production returns to the US (loss of jobs and business in Canada but gain of jobs and business in the US), but she was clear that it would be bad for Canada – not for the US. So this is known in Canada.

But you aggrieved Canadians here don’t pitch it that way here in the US and on this site. You dig up BS to say that bringing production back to the US would be bad for the US.

I resent being used as a political tool by a foreign propaganda operation! And yesterday, I learned that that’s what it was. I have put nearly all Canadian commenters that have said this stuff, dozens of them, much of it blocked, on my “Aggrieved Canadians” list, so that I can filter their comments; propaganda gets blocked, the other stuff passes.

Not sure if you saw this. A week ago I replied to you and all aggrieved Canadians. So I’ll just repeat it here. What I didn’t know when I wrote this was that this was a national propaganda effort that WOLF STREET had become subject to.

There are a lot of aggrieved Canadian commenters here — including you. And I understand why you’re aggrieved. And I love you all. But this is the USA, it has two HUGE deficits:

— the trade deficit in goods of $1.2 trillion in 2024, (including $63 billion with Canada)

— and the ballooning fiscal deficit.

And I have been screaming about both deficits ever since I started this website over a decade ago. They’re HUGE problems.

Then Trump 1 became the first President ever to try to do something about the trade deficit when he imposed some tariffs in 2018.

Then Biden followed in his footsteps and largely kept the tariffs in place. But Biden decided to throw many tens of billions of taxpayer dollars at companies to incentivize them to manufacture in the US.

Trump 2 doesn’t like this taxpayer rip-off and decides to impose taxes on the gross profit margins of importers (tariffs) instead, to give them an incentive to manufacture in the US.

In addition, Trump is addressing the fiscal deficit. He is finally taking seriously what I have been screaming about here for over 10 years.

So you aggrieved Canadians need to say: “We hate these tariffs because they hurt us Canadians.” And I respect that, and I agree with that. Those tariffs might hurt you Canadians because some of the Canadian production will shift to the US.

But the tariffs don’t hurt the US because production shifting to the US from foreign countries doesn’t hurt the US but is one of the best economic moves ever, given our huge goods trade deficit.

So if you aggrieved Canadian keep trolling this site with BS about how tariffs hurt the US, I will put you on my “aggrieved Canadians list,” with a lot of love, and I’m going to do some gentle handholding here so that this BS coming out of Canada about how the tariffs hurt the US will stop. Enough is enough. You’re big boys up there, you can handle the tariffs, suck it up.

Wolf, what does “ anti-tariff stance” mean?

“ Smith said that there had been a consensus among all Canadian political groups and everyone else in Canada that all Canadian politicians and everyone else should reach out to US politicians, US media, US influencers, US bloggers, etc., to try to manipulate them into an anti-tariff stance.”

If I was Canadian, and I’m not, I wouldn’t be quick to dismiss Trump’s comments about trying to annex Canada.

I view him more as a mob boss than as a politician, so the idea of him trying to weaken an entity in order to take it over or shake it down doesn’t seem wildly uncharacteristic.

I could see a Canadian feeling like this was putting them on the path to an existential crisis.

Next next potential response might be something like we saw from Ontario (?) where they threatened to shut down power exports to the US entirely.

And outside response like that would certainly hurt a segment of the US.

You are viewing this through a trade lens, I’m not sure that Canadians aren’t viewing this as more of an existential one.

I know I would be. Trump seems much more aligned with the might makes right type of governments – when he talks about takeovers, seems like a good idea to either take him seriously or do some serious bet hedging to make the prospect painful.

Just dropping by,

yeah but… Your comment has nothing to do with what I said. You took a short phrase out of context and went on flight of fancy.

Read my comment in its entirety, all the way down.

Wolf, my post actually started off as a request for more information about what you were considering to be an anti-tariff stance.

As I wrote it, though, it became more about my visualization of why some Canadians might feel they need to have an all hands on deck approach to the topic.

You wrote a fair amount with the general idea of

“Enough is enough. You’re big boys up there, you can handle the tariffs, suck it up.”

At the risk of belaboring the point, it really seems like you see this as just business. And I totally get where you’re coming from on multiple points.

But if I were a Canadian, and with this particular president and his apparent comfort level with territorially aggressive foreign leaders, I would probably be seeing it as a first step towards what could very possibly become a much more existential threat.

I don’t honestly know what specific messages you were seeing that offended you so much so it’s hard for me to understand the propaganda concept bery thoroughly.

But if Canada feels so threatened that they shut off power to portions of the United States, wouldn’t that hurt Americans? Or if they limited supplies of potash for American farmers?

Even if they’re being irrational, couldn’t get the right amount of fear actually harm the United States-ians?

I did read your message by the way, although it was on the small screen of the phone. And I reread it, and I’m trying to treat the topic with at least some of the substantial amount of respect that you and your site deserve.

Regards

I despise Trump as a person but love his policies.

Finally a POTUS with balls to stand up and do something for the Americans following common sense.

Of course, not all his polices are flawless.

People say, he is a president and friends of billionaires. Most of the rich people are hating him right now.

It is still possible to sell a house in this market. I listed my house for sale in January, had an accepted offer in two weeks and closed the sale in February.

The secret was simple: Research the market and price to sell. Most of the active listings in my area had rather aspirational asking prices, so I priced my house’s asking price at slightly below the other 4 bedroom houses in the area, and with a better location and larger lot, had no trouble finding a buyer at above my asking price.

It also helped that in this area, real estate is a very seasonal business with the bulk of the listings during the summer. Not a lot available in January, so there wasn’t a lot of competition for the buyer who needed a house *now*.

The market in parts of SoCal is still white hot. Homes in the 750k to 1.25M range in decent areas sell quick. On redfin I see houses with 15,000+ views in just a few days, never even seen it that high before. Harder and harder to find good deals in areas like Palos Verdes and the IE

PV was my old stomping grounds. You are right it is getting harder there and I suspect the Palisades refugees will exacerbate the problem as it translates nicely for anyone looking to relocate.

This really reinforces Wolf’s point that a lot of Real Estate economies are localized and a recession in one spot might not mean the same in another.

GOOD Points cyn:

Perhaps WE should add to the familiar RE meme, ”location, location, location,” another factor:

”timing, timing, timing.”

Certainly has been relevant in the dozens of ”hoods” I have been involved in buying, fixing/rehabilitating, and selling houses over the last 50-60 years.

and that, my friend, is how prices decline gradually. take standard 4 bedroom houses that were $500,000 in 2019 and sold for $950,000 at the peak in 2022. today, people list them for $900,000. you were smart and listed at $850,000 and it went quickly. as time goes on, the people who listed at $900,000 see that the comps are lower, and lower theirs, but it’s not an immediate process.

then, when all the listings are $850,000, the next person like you lists his for $800,000, and down we go. rinse, repeat.

Yes I an a boomer and own my homes. Was thinking of getting something smaller, but all the costs due to RE paradites eat up any advantage of a smaller place.

Now I am thinking of renting something nice. I know rent will go up, but if I sell I could easily pay the rent for the next 30+ years and not have all the home owner crap to deal with. Renting is looking better all the time.

Realtors are out of work. They may want to look for a new profession. Right up the road from us is New Jersey. They still have a law prohibiting drivers from pumping their own gas. You get a fine of $100 if caught. I almost got hit with the fine because I didn’t know the law. So they are looking for more dudes to man the gas station pumping stations. A new career opportunity awaits.

Maybe ‘waiting for lower home prices’ is like waiting for Hell to freeze over. 🤔

You don’t own the national median home at the national median price. You own a home in a specific market, and those local markets dance to their own drummers.

Here’s Austin. More markets here:

https://wolfstreet.com/2025/03/17/the-most-splendid-housing-bubbles-in-america-feb-2025-the-price-drops-gains-of-33-largest-costliest-housing-markets/

And here are some big city condo busts are underway.

https://wolfstreet.com/2025/03/21/where-condos-already-came-unglued-10-big-cities-with-price-drops-from-10-to-22-from-peak/

While I feel housing if for most part still TOO DAMN HIGH am considering West Virginia.I am semi-retired,can buy cash easily and do not care about best schools ect.(would like all schools to teach kids to think!).

For 300 I can buy a 3 bed/2 bath on 80 acres,room for a large workshop/some chickens(eggs)/goats(milk-butter)/a good sized garden and a on the move shooting range.I also love hiking/fishing/hunting so seems may be the winner for me.The land would also allow me to have a no kill animal shelter,feel that would be a great way to spend the final chapters of me life.

Yes,could wait and see if prices drop but also want to have me final home set up,will see the next few months when I hook up with a bud that lives in the region and if I buy will post.

An interesting observation is that less demand do not translate to lower prices in the case of mortages.

Put to the point it could be said that the mortage market is not working as less demand for mortages do not translate to lower prices (interest rates on mortages).

“Less demand” is already doing a lot of heavy lifting a lot of markets. Note the charts above… how could you have missed them.

See here:

https://wolfstreet.com/2025/03/17/the-most-splendid-housing-bubbles-in-america-feb-2025-the-price-drops-gains-of-33-largest-costliest-housing-markets/

And here are some big city condo busts underway.

https://wolfstreet.com/2025/03/21/where-condos-already-came-unglued-10-big-cities-with-price-drops-from-10-to-22-from-peak/

Less demand have not resultet in lower prices (interest rates on) mortages. The high cost of mortages have worked on the price of housing, not on the price of mortages.

The housing price part of the market is working, the pricing (interst rate) part of the market is not working. With less demand the interest rate should go down of it was a working supply – demand market.

I think more free market rates is working by making the payments too high so prices then need to come down and higher rates deter one of the worst behaviors in housing, using cheap debt to hoard houses for investments. The lower prices from higher rates reward savers who’s high down payments avoids big interest expense. Mortgages aren’t actually high if you support free markets. They are still subsidized because rates would have to go higher if the feds mbs went to the real market.

Sadly it’s just going to take a while and there will be pain all around buyers renting and waiting, sellers angry and confused. The damage done between 2020 and 2024..and really since 2009 .. so much money printed to hold up asset values as production and quality jobs kept going overseas. Young people today DO have one thing on their side – time. They can refuse to buy houses, refuse to buy stocks, refuse to play the game for a while until prices come back down relative to incomes. Five or ten years maybe.

I think housing will be flat/down for the next five or more years. People will pay 2022 prices in 2032. People who bought in 2022 with their 2.75% mortgages will wonder where their jackpot went..

Stocks – personally I think the S&P is at least 50% overvalued. If I was under 40 I’d sit in cash making 4-5% until a MUCH better buying opportunity came along. All these old folks want to cash out at the top like it’s owed to them.

the s&p is more than 50% overvalued. it’s held up by a handful of tech stocks that will see their profits and values plummet the moment a recession starts.

Music to my ears. The healing gain would far outweigh a little pain for the USA and world to get those corrections in residential RE and stonks.

Trump just announced that all homeless tents on federal lands are being dismantled. Once that’s done the mayor will be assisting to remove the tents on private property. DC is starting to look better every day. As the Swamp predicted, the Nation’s Capitol will enjoy a boom in the next 4 years, even with all the firings and shutdowns of federal agencies. People who were WFH and doing nothing for God & country and working 2 and three jobs on the side in the last 4 years have now been forced to get off their sorry a$ses and report to their offices and earn their pay like the rest of us.