Bring on the supply of new houses! Prices drop, as homebuilders try to sell the inventory, but are still far too high.

By Wolf Richter for WOLF STREET.

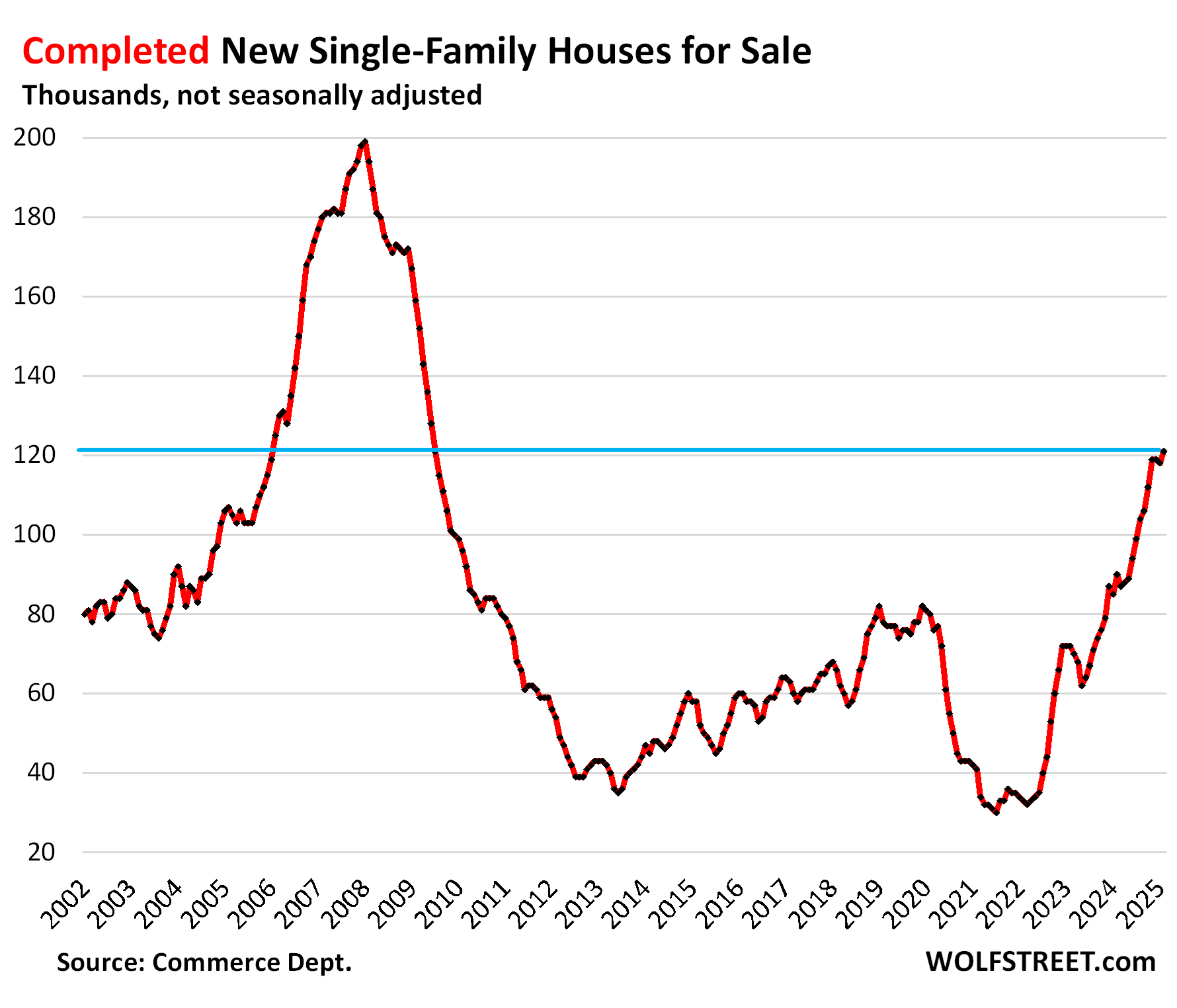

Inventories of completed new single-family houses for sale in February jumped by 34% year-over-year, and by 55% from February 2019, to 121,000 houses, the highest since July 2009 during the Housing Bust, and roughly where they’d been on the way up in February 2006, according to data from the Census Bureau today.

These are “spec houses” that were built without buyers lined up. Homebuilders are motivated to sell this inventory of spec houses quickly because they’ve sunk a lot of capital into them.

From the buyers’ point of view, this is a good thing: Bring on the new supply of essentially move-in-ready houses that builders really need to sell – more choices, lower prices, and bigger incentives.

For the overall housing market, this is also a good thing. It needs this surge of new supply. It’s competition for homeowners selling or thinking about selling their homes, including their vacant homes they’d moved out of years ago but didn’t put on the market to ride up the price spike all the way.

But the publicly traded homebuilders have been singing the blues, and their shares have careened lower from their highs in September, for example, DR Horton [DHI] -33%, Lennar [LEN] -33%, KB Home [KBH] -34%.

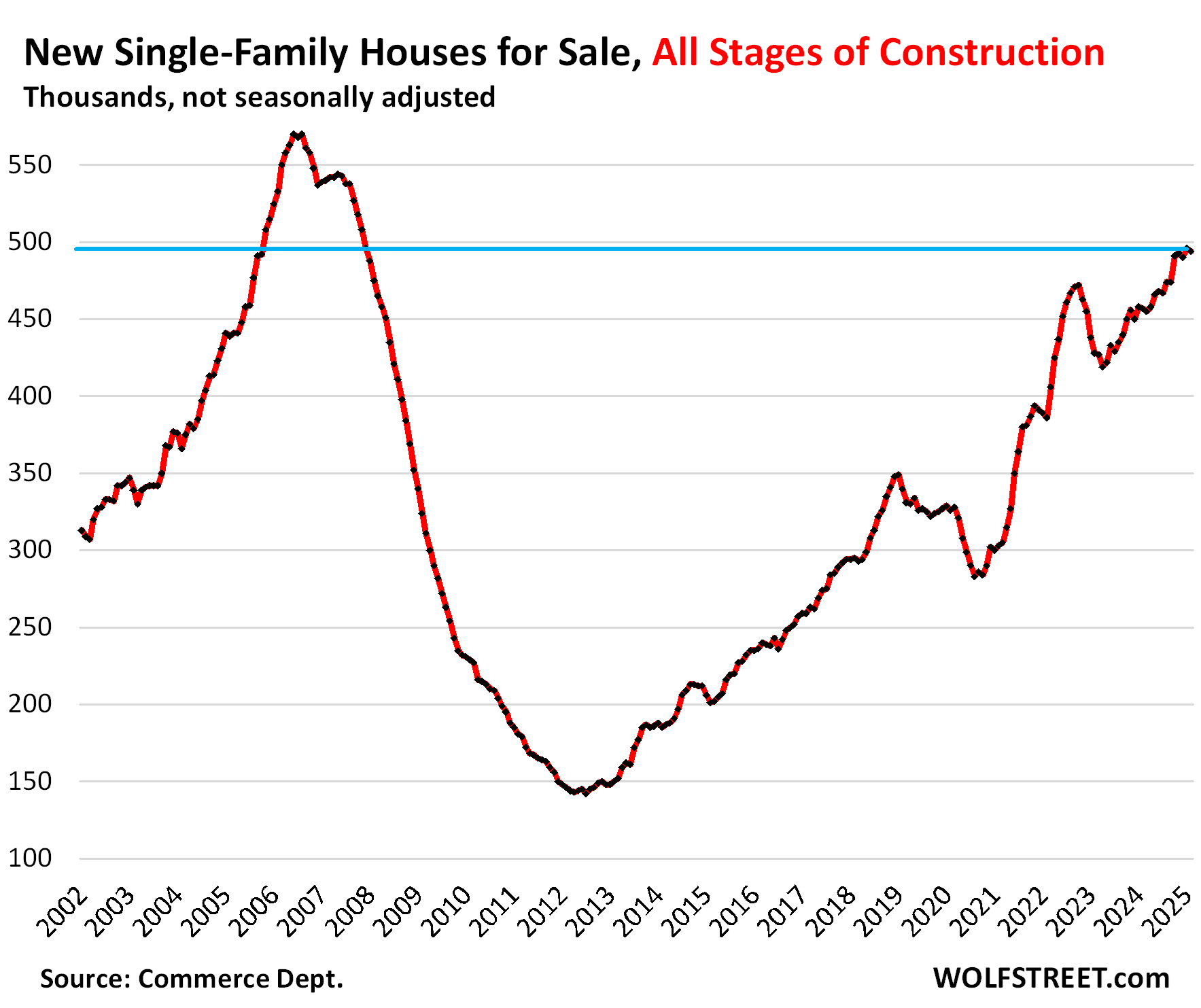

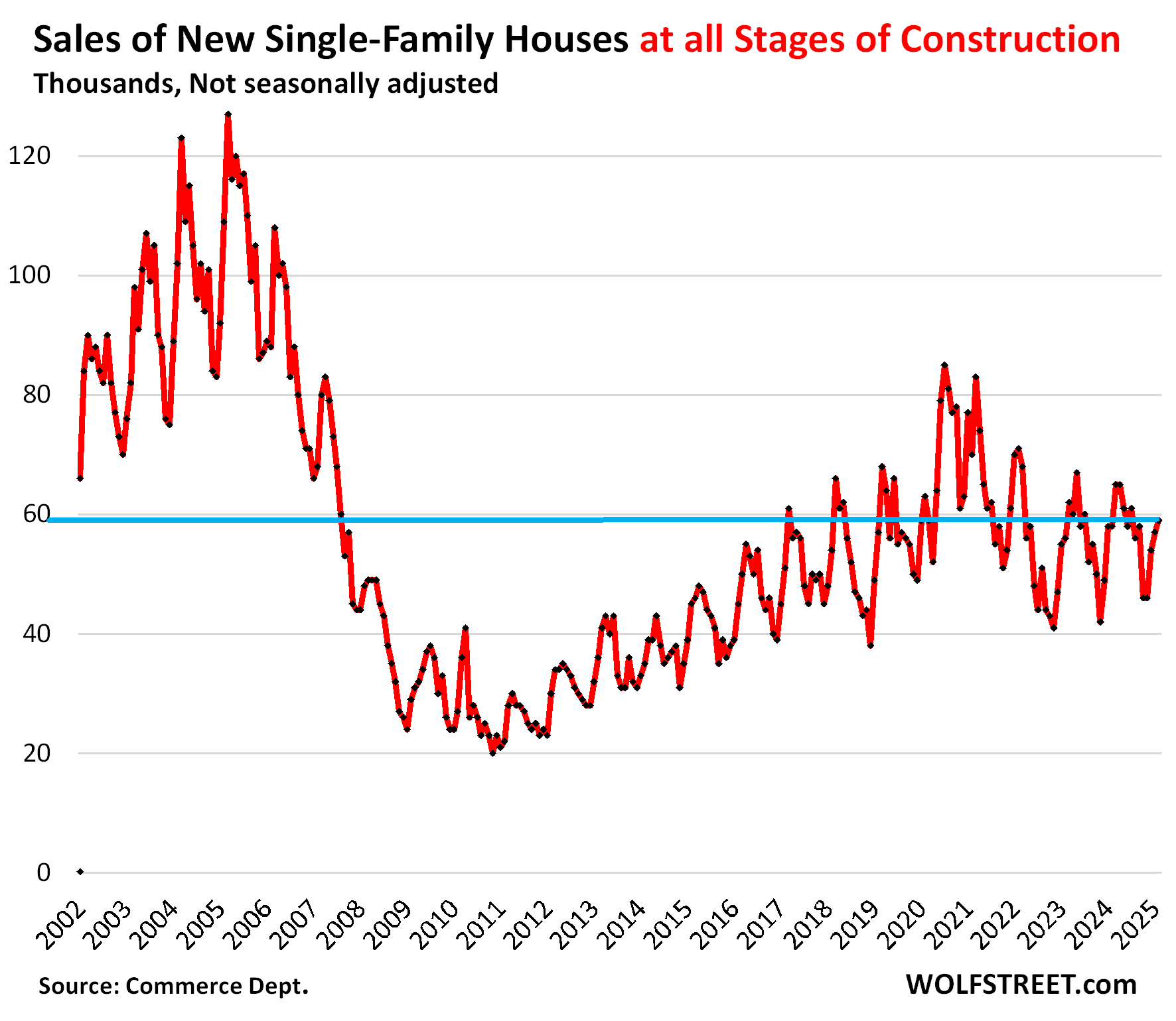

Inventories of single-family houses for sale at all stages of construction in February was essentially unchanged at 494,000 houses, up by 8.1% from the bloated levels a year ago, and up by 45% from February 2019.

Inventories of the past five months have been at the highest level since December 2007, during the Housing Bust.

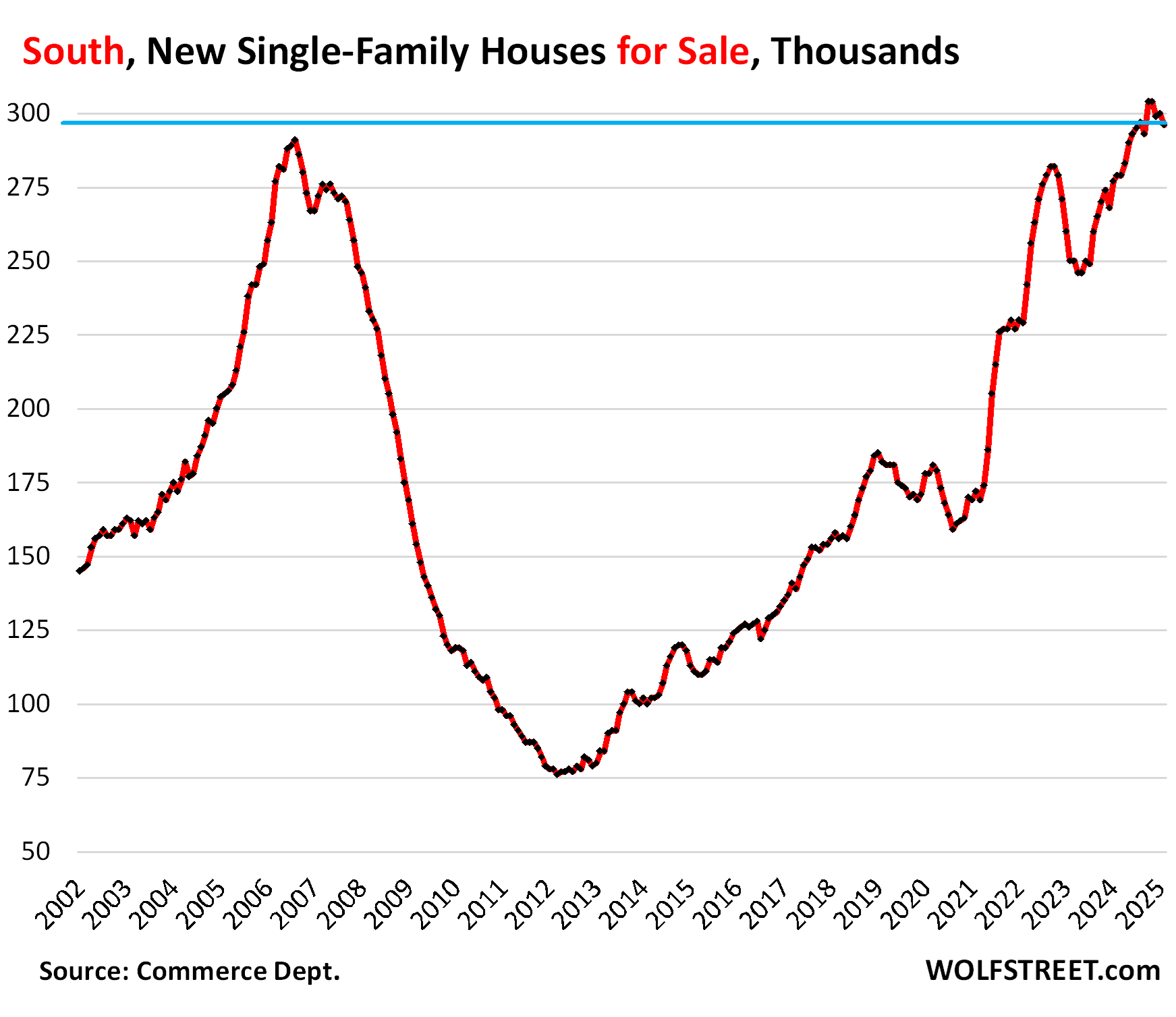

South: new houses for sale at record highs for months.

In the South, inventories of new houses for sale at all stages of construction have been at record highs for months – at 290,000 to 304,000 houses for sale – having surpassed the highs of the Housing Bust for the first time ever in May.

In February, inventory for sale of 296,000 houses was up by 6% from the already bloated levels a year ago, and by 72% from February 2019!

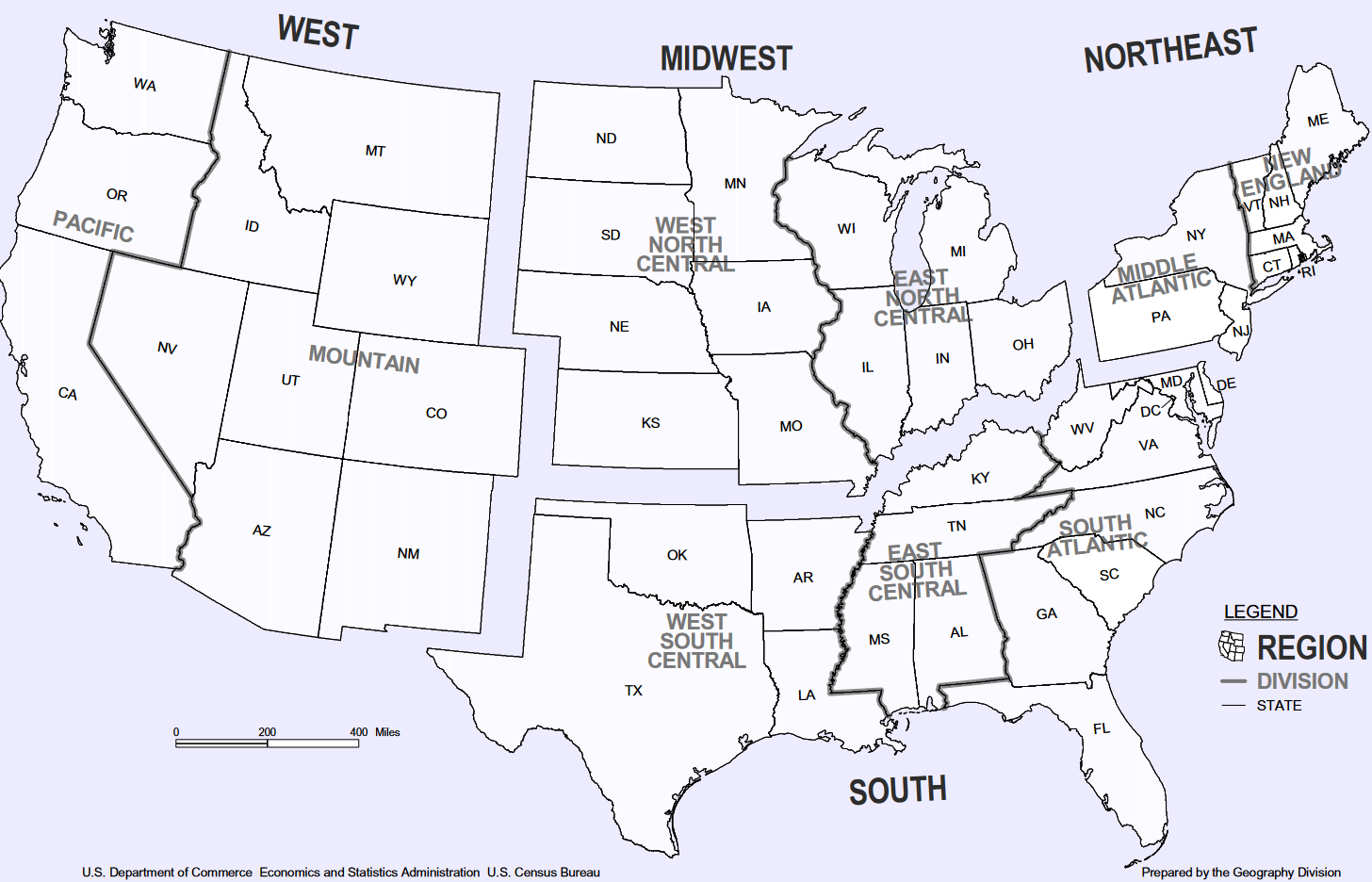

The housing market of the South, a huge Census region, is dominated by Texas and Florida (see map of the four Census regions at the top of the comments). It’s by far the largest market for new houses in the US: In February, it accounted for 60% of new houses for sale in the US, and for 66% of US sales of new houses.

Massive incentives and lower prices by homebuilders have stimulated sales. In February, sales were up by 18% year-over-year.

And supply dipped to 7.6 months, but this was still 38% higher than in 2019.

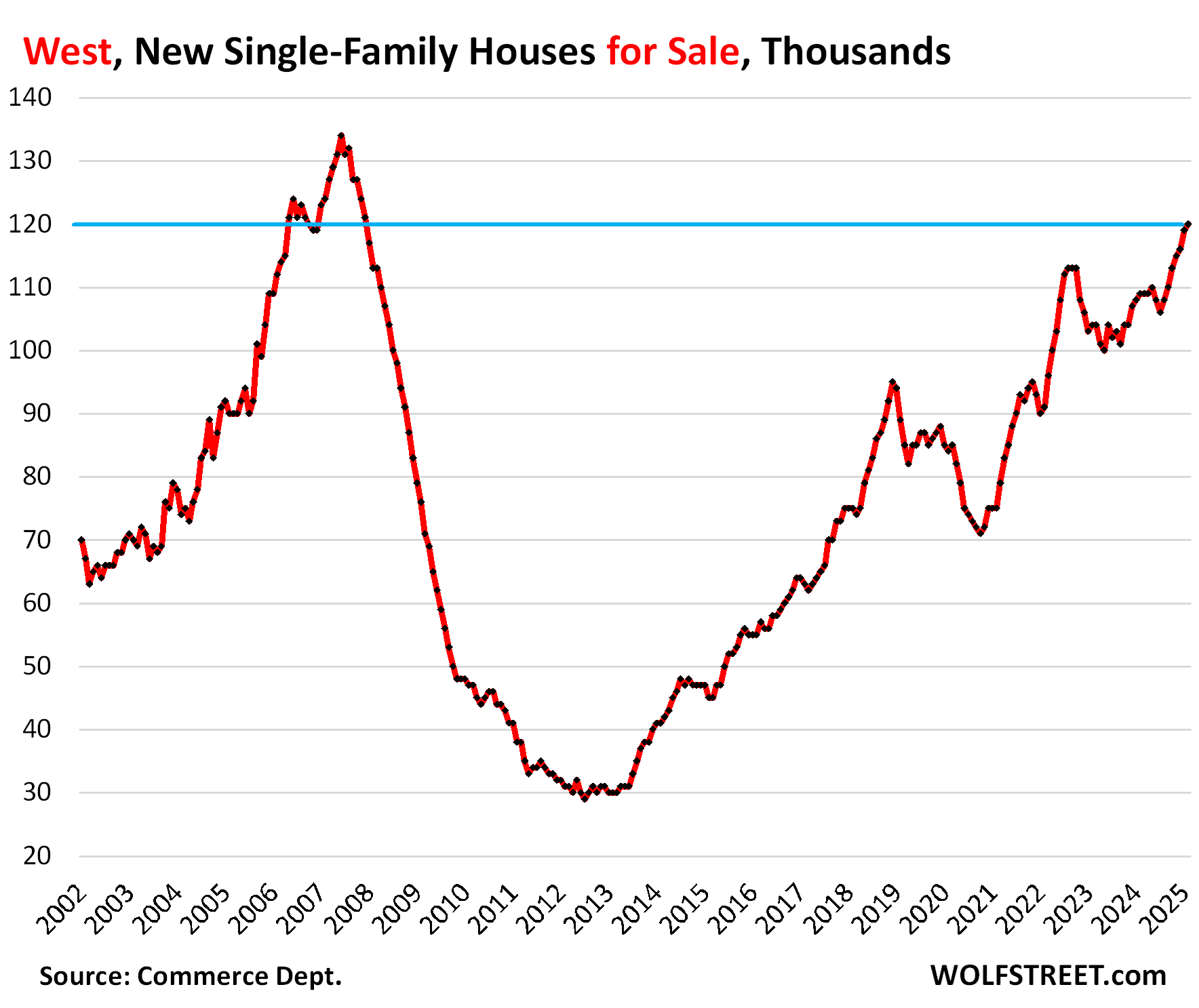

West: Inventory surges to highest since December 2007.

Inventories of new houses for sale at all stages of construction rose to 120,000 houses in the West, the highest level since December 2007, and up by 10% year-over-year, and up by 60% from 2019 (see map of Census Regions at the top of the comments below).

The market for new houses in the West, the second-largest in the US, accounted for 24% of the US inventory of new houses and for 20% of US sales of new houses.

But sales in the West fell by 14% year-over-year and by 25% from February 2019.

Supply in February rose to 10 months, the highest of any region, up by 28% from a year ago, and up by 80% from 2019! Homebuilders need to sharpen their pencils to get this inventory moving:

The other two regions.

The South and West combined accounted for 84% of new house inventory and 86% of new house sales in the US. They move the needle.

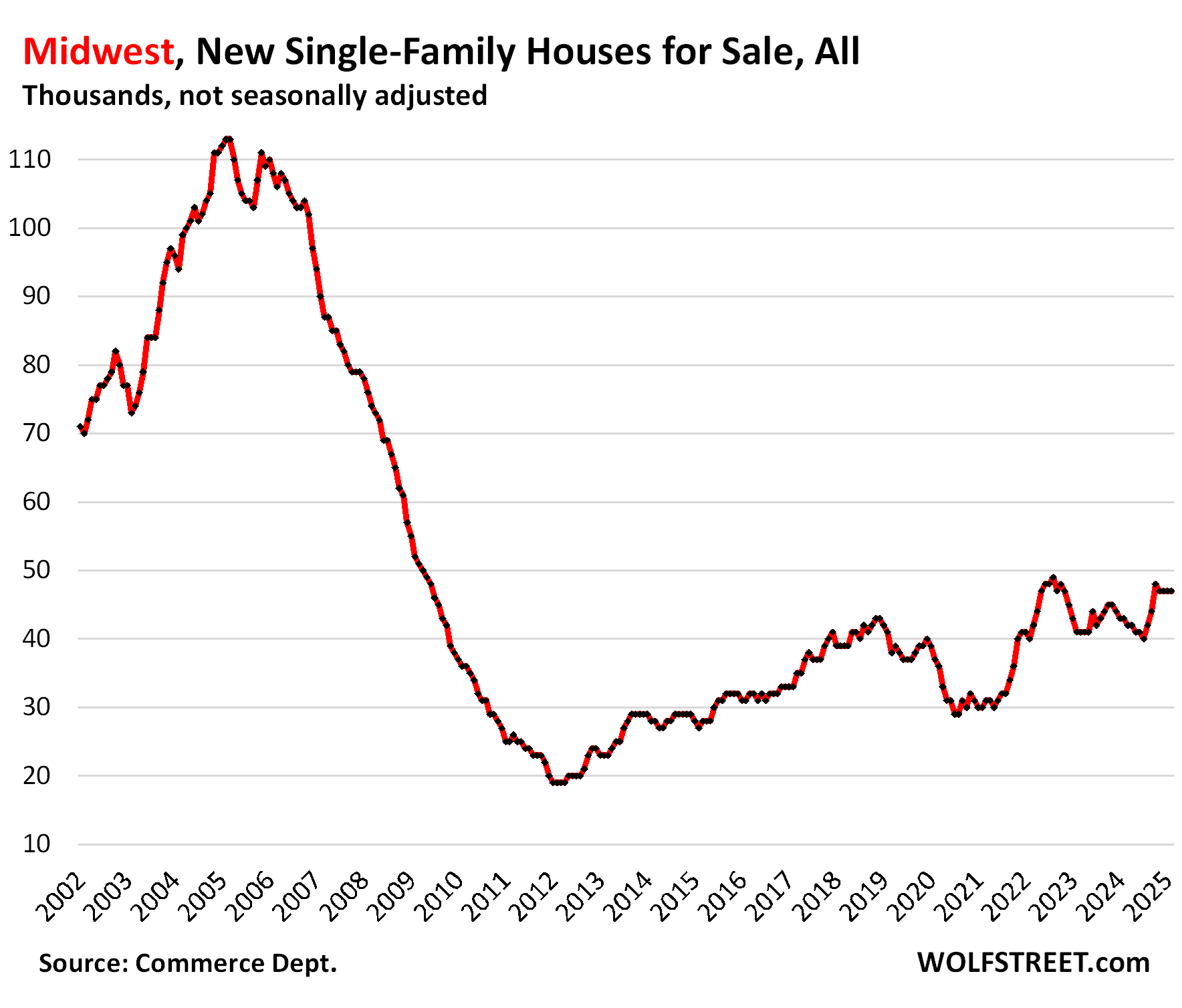

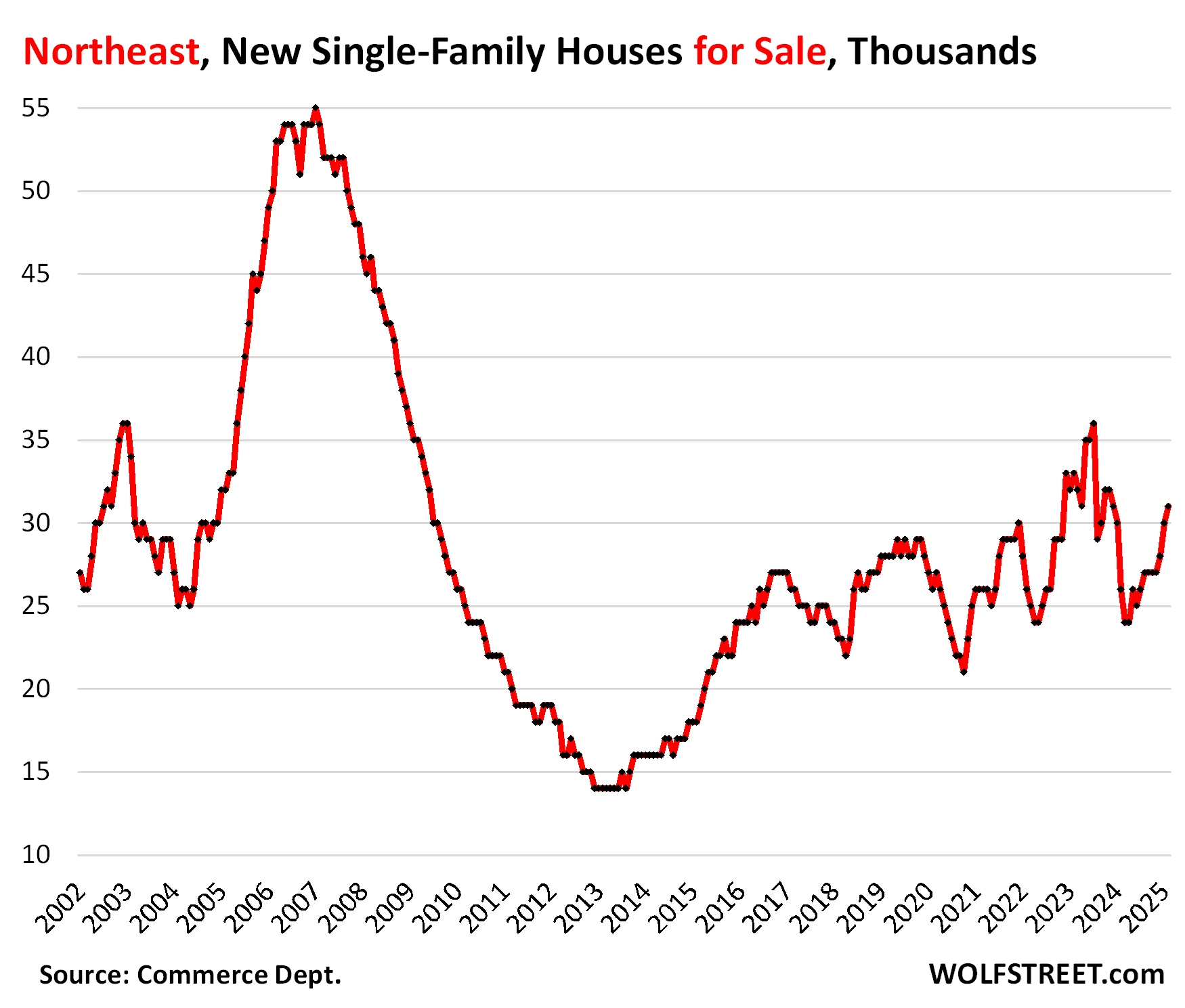

The Midwest and the Northeast carve up amongst themselves the remaining 16% of the new-house inventory and 14% of new-house sales. Some of the big states in those regions have lost population over the years, the cities are already dense and huge, and big new developments are not a big priority.

Inventory in the Midwest remained for the fourth month in a row at 47,000 new houses for sale, up by 9.3% year-over-year and up by 15% from February 2019.

Sales at about 6,000 houses in February were down from a year ago, but roughly the same as in 2019. Supply remained at about 8 months.

Caution with these small numbers of sales: Census rounds its sales estimates to the nearest 1,000: these “6,000” sales could mean anything between 5,501 and 6,499.

Inventory in the Northeast rose to 31,000 new houses for sale, up by 19% year-over-year and up by 11% from February 2019.

Sales of about 2,000 houses in February were down from a year ago, likely the bad weather. Supply remained at about 8 months.

Even greater caution: There are minuscule sales figures rounded to the nearest 1,000.

US sales dip YoY despite price cuts & incentives.

Sales of new houses at all stages of construction rose in February by 1.7% year-over-year, to 59,000 deals, not seasonally adjusted, driven by the sales increase in the South that more than made up for the drop in the West. Compared to February 2019, sales were still down by 6%.

These sales are based on contract sales, not on closed sales. Things can happen that prevent contracts from closing, such as not being able to get affordable insurance or financing falling through.

Homebuilders overall have been selling houses at a slower clip than they’ve been building them, which is why inventory levels of new houses for sale in the US overall have continued to surge.

Supply at 8.4 months was up by 6% from a year ago and by 40% from February 2019.

Thanks to the incentives, promos, lower prices, and mortgage-rate buydowns, sales of new houses have held up at decent levels – though they’re nothing to write home about – while sales of existing homes experienced the worst February since February 2009:

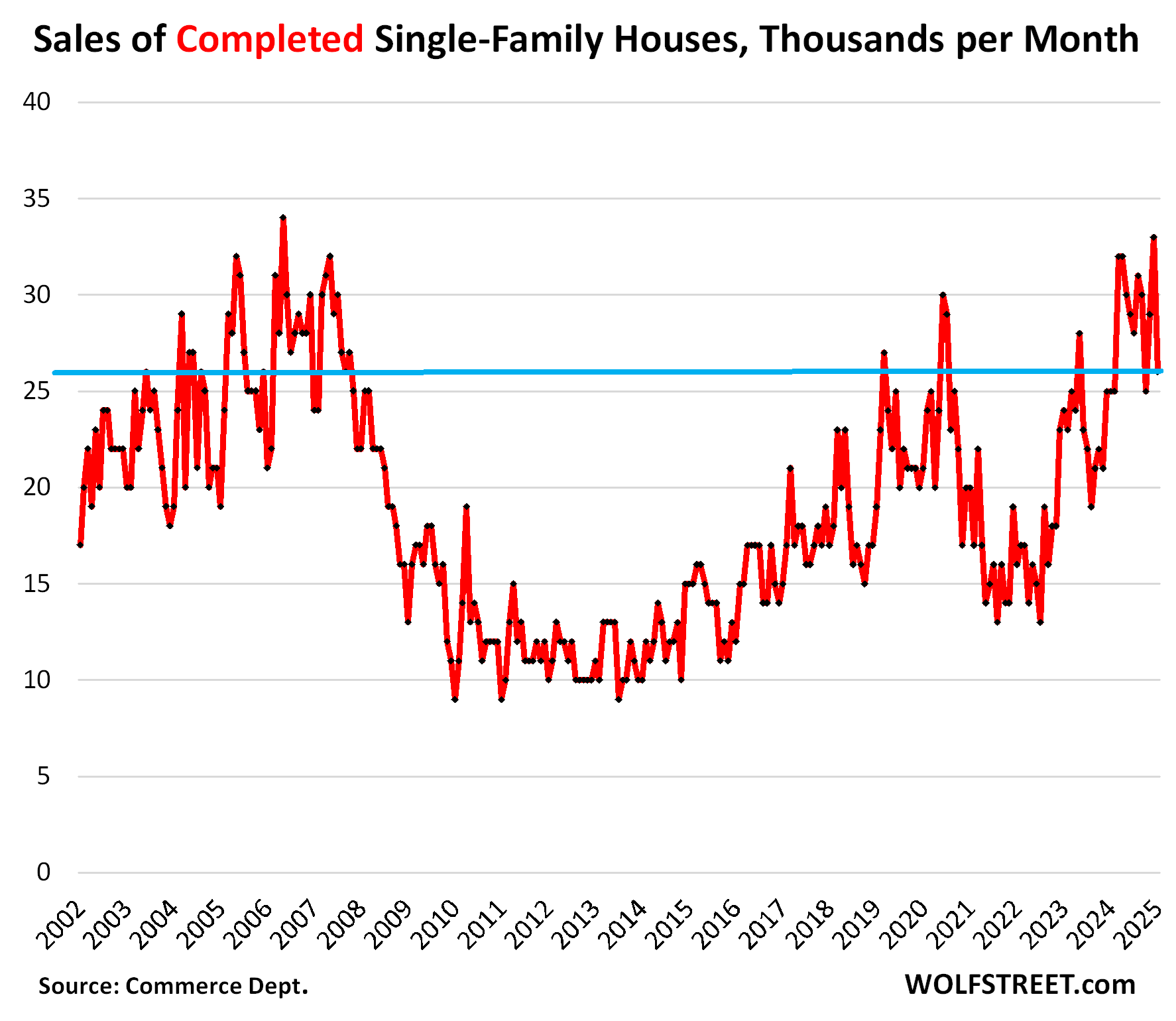

Sales of completed houses rose 16% year-over-year in February to 29,000 houses and were up by 26% from February 2019, as builders have given up profit margins – some of the biggest have given up 2 to 4 percentage points from the fat margins a few years ago – to aggressively sell what they built.

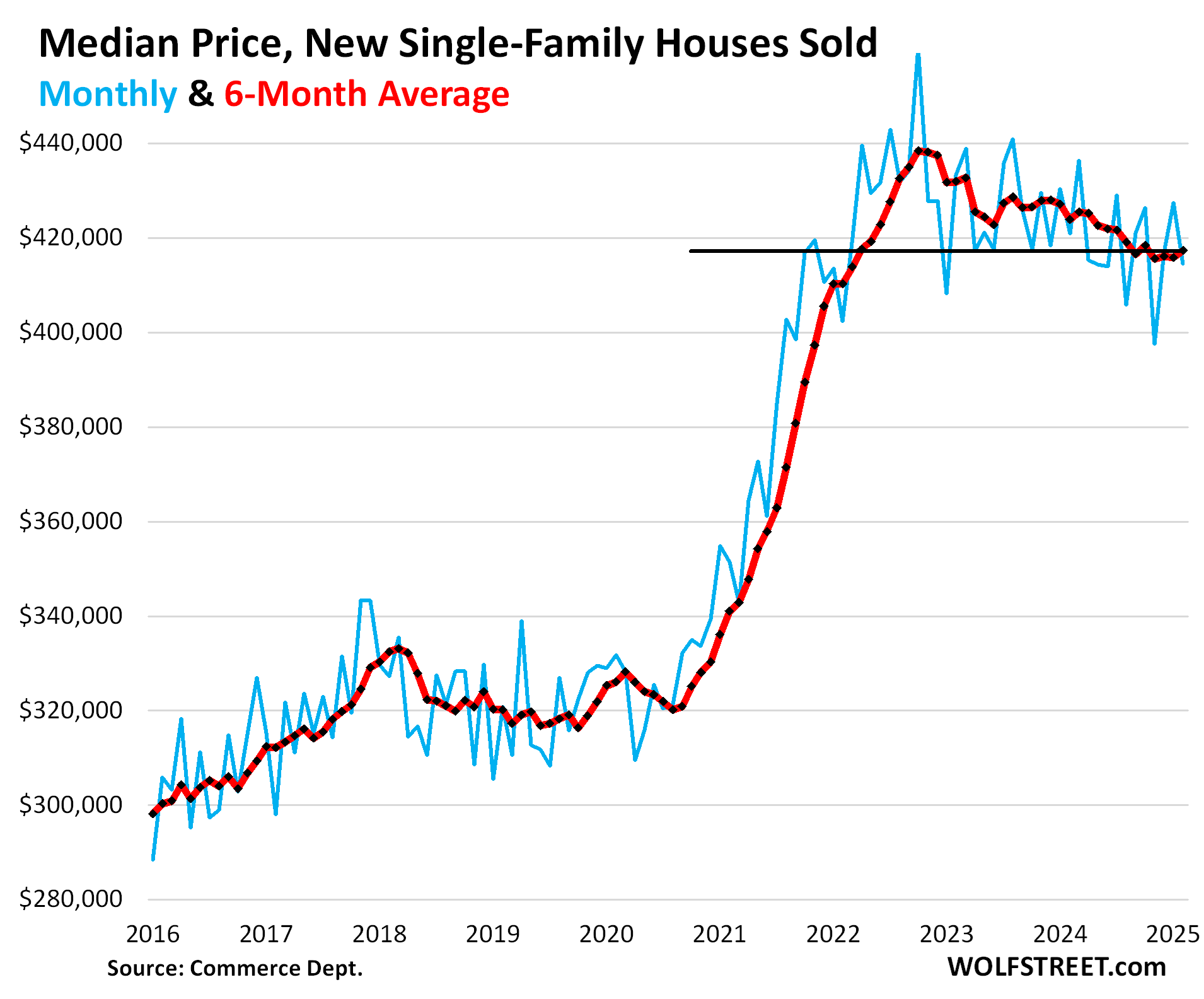

Median price wobbles along below the 2022 peak.

The median contract price of new single-family houses at all stages of construction that sold in February fell to $414,500, down by 10% from the peak in October 2022. January’s originally reported spike to $446,300 was revised down to $427,400.

The six-month average, which irons out the random volatility and the revisions, ticked up to $417,300, below where it had been in October, back where it had first been in April 2022, down by 1.5% year-over-year, and down by 5% from the peak in late 2022. In recent months, it has been roughly stable (red).

But note: these are contract prices that do not include the costs of the mortgage-rate buydowns (which show up on builders’ financial statements in gross margins as a cost) and certain incentives, such as free upgrades. So these median prices are not a great reflection of how aggressive actual pricing – including mortgage-rate buydowns and incentives – is in the market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s really funny to see how polar opposite the two sides are in terms of what this data can mean. Case in point, one look at sub-reddit REbubble, with a graph of this data and the headline is “Supply of New Houses for Sale Totals 500,000 the Highest Level Since 2008” then if you hop over to REbubblejerk which makes fun of the non-house humpers, you see the same graph and this is the headline “Ignore the population increase guys, crash coming for real, I can feel the crash”

Just find it really hilarious especially since both posts were on top of one another on my reddit feed.

Interesting to see the West went up quite a bit too but I am sure for some, LA/OC/SoCal exceptionalism will set in and this “west” somehow doesn’t include those region…cause not in my hood…

Despite the California optimism and sunny demeanor — surf’s up! radical! — high home prices have driven buyers OUT OF STATE to places like Phoenix and Seattle, and will continue to do so as long as Californians dwell in a state of rapturous illusion. To move those houses, as Wolf says, prices must come down. This is a bubble we’re in, and only the ultra-prosperous are paying those prices.

My parents (SF Bay area CA) have been looking to downsize into a single story as they get older. There is indeed some new construction available in their area, but it’s all larger 2 story stuff.

Also, they are totally spooked by the possible uninsurability of these new houses, which are invariably a little further out of town and more in the hills.

Looks like it’ll be a stair lift or elevator or something.

California is not optimistic and hardly sunny in their daily outlook. Seems to me they are more dog eat dog.

Given the hunger for profits by the Silicon Valley sociopaths it’s understandable.

Realtors are really scumbags for being so greedy and have been forcing bidding wars in a market that should have never have gone so high when back when interest rates were at 2 percent. If you even want to look at a house, the pushy realtor shoves it down there throat and overly agrees about the property when a person has even looked at them. I am sickened that they fought rent control in California. It is issue that was not their except it might hurt prices from going up. Well rents are falling now so even though law didn’t pass, they wasted their money. See you greedy realtors if price would have stayed the same is better then bubble where nothing sells. If you really want to blame people, I would have say Trump had no busy getting involved with rates being cut when they overreacted with COVID 19, and these dirtbag realtors that really do not have a job with much of a skill except the fact that they know how to rip people off through illegal price gauging not supply and demand which it should be. People stop believing these pics crap realtors!

Went to a random open house in my neighborhood – a place that I knew was crap, and wanted to see for myself – just because a beautiful antique house I needed to see was open at the same time. After I told the realtor I was a Lookie-Lou neighbor, she actually said what people on here always say realtors say (but I thought was an exaggeration): “if you don’t buy now, you’ll be priced out forever.”

Realtors are parasites.

“But the publicly traded homebuilders have been singing the blues, and their shares have careened lower from their highs in September, for example, DR Horton [DHI] -33%, Lennar [LEN] -33%, KB Home [KBH] -34%.”

We can pontificate about the morality of the US housing market, making fresh highs in price while the sales set fresh lows. The builders can’t sell their product at the ask price because the bid price is at the buyers affordability level that is at least forty pct lower.

Isn’t that saying the same thing?

That spells trouble for the retirees and their existing home prices.

I am old and am thinking about selling my house that I’ve owned for 30 years. The last thing I’m worried about is making a profit on selling my home.

I would like to buy a more appropriate house for my age as opposed to this large family home now that my children who filled the space have left the nest.

Here is a map of the four Census regions:

Wolf,

So in the Northeast census region, there’s one new

house sold per month for every 30,000 people (plus

or minus 8,000), and in the combined West and South

there’s one new house sold per month for every

4100 people. No wonder I often get that “not-in-my–

area” vibe when reading your housing posts, which

often put emphasis on the West and South.

Although to be fair, the difference is probably

exaggerated a heavy seasonal component to new

house sales, just like used houses, so relative sales

in the Northeast and Midwest are now at seasonal

lows.

J.

—————————————————-

I am assuming that the 2,000 and 6,000 regional

sales matches up to the 59,000 total sales reported

in the article.

How many new houses do you need to sell when the population stopped growing or is declining? In theory, none.

It’s a question of demand, and there is no demand, which is why there are so few new houses sold. Inventories are rising even in the Northeast, which means builders are building more than they can sell, which is a sign of slow demand for new houses.

True, but I moved out of the NE years ago because the prices were too high for housing stock that was too old.

Don’t worry soon all those people fleeing high cost California and other high cost blue states will buy a lot of those homes.

I don’t think that the massive movement from those high cost states and those with cold, rotten weather will stop any time soon.

Those cheaper, new home just provide more incentives.

Give it a year and let’s see what happens.

Warren Buffet once commented that annually about 1 million new homes are needed in the US on average, to replace old / damaged homes and the demographics need of people moving and migrating.

Homes, not houses. Homes includes multifamily (apartments and condos). Total housing starts in 2024 were above 1.36 million housing units for the fifth year in a row:

https://wolfstreet.com/2025/01/17/bring-on-the-supply-single-family-housing-starts-in-2024-rose-to-2nd-highest-in-17-years-amid-budding-glut-multifamily-starts-plunge-from-multidecade-boom-amid-oversupply-cre-depression/

A big reason the Big10 went on an acquisition spree, the demographic trends of their core conference membership awful compared to the SEC.

Does “The West” include Alaska and Hawaii? If not, are they their own regions?

These four Census Divisions cover the lower 48. Hawaii and Alaska are included in the “Pacific” region, which I don’t discuss as a region, though Honolulu is included in my 33 “most splendid housing bubbles.”

Great analysis. Thanks!

Time to return to ZIRP and get this inventory moving!

Time to lower prices further and get that inventory moving.

Time to let interest rates go up and create another FOMO panic to move the inventory.

That is what I’m concerned about what they are going to do. A prophylactic solution. A band aid for a gushing wound.

I guess these projects builders want to keep their good workers/teams busy. Try and keep them thru the tough times. They can’t grow if they can’t build – profit for another day.

Yes, there are certainly a lot of new developments around where I live (north of Houston, TX) and the houses are selling with appropriate builder discounts and goodies added. Houses probably in the thousands being built. Seems like most of the buyers are young families with small children and the vast majority are Hispanic.

Jobs are quite plentiful here and traffic is nuts during rush hour. So I guess it’s all good around here.

I didn’t mention this in the article, but Lennar paid 13% of its revenues in incentives in the last quarter, roughly double from before the pandemic and the highest since 2009. But it also booked a small sales gain.

KB Home, which is trying to maintain its profit margins, booked a sales decline.

Those are the two approaches homebuilders are taking. It’s one or the other.

And their stock prices are imploding….

Yes, either way, LOL.

Lennar just acquired the builder who built my 2 year old home last month (Rausch Coleman). They (Rausch) were in business for 65 years and have (had) several new home developments in process here. Lennar is spreading its wings here in the area.

I’m in College Station. Lots of new builds and no price wars to speak of.

Theyre builing garbage and selling what they can at huge profits so got lots of room to discount em.

Probably ride the retirement wave as long as they can then prices may moderate. Lots of cash in those hands still. Meanwhile rent seeking systems for the rest of em.

Banks still tighter lending standards seems like, so might miss out on the big foreclosure crash n burn this time. Long slow burn in progress.

“Theyre builing garbage”

I’m out of patience with this BS. Everybody rails about how unaffordable homes are, and then you get these goofballs that complain that new houses are built at a lower cost to fit realistic budgets.

in his defense, people say all the time that the build quality has gone down (they don’t build em like they used to) and that the builders throw them up quickly and without attention to quality control. that isn’t about building at lower costs, that’s about cutting corners.

The thing is builders like Lennar aren’t “throwing them up”. That’s not how any of this works. Builders like Lennar hire local contractors and local inspectors are the ones that keep those contractors accountable. The quality of any new build is location-dependent and has almost nothing to do with the home builder company.

It is extremely difficult to vet these contractors. Almost none of them have Google reviews and those that do likely received fake 5* reviews from their employees and family. Half the contractors that built my home don’t even have a website.

Then whatever local inspector you have is just a reflection of the local government. They can range anywhere from inspectors that will sign off on anything to inspectors that follow local codes to a T.

Dan,

“It is extremely difficult to vet these contractors.”

Well…it is Lennar’s/etc. name on the front door…and, allegedly, they are in the home *building* business…

I don’t doubt that you are mostly right about the big builders mostly using local contractors…but you sort of make it sound like those mega-builders ought to be held harmless for build quality (variation on “It is just so hard to find good help nowadays”) and that the mega-builders are almost an accidental/incidental participant in the process (who? what? me?!).

It is the mega builders *business* to find decent quality local contractors/police build quality/etc. – not just cash an (enormous) check and vanish in a cloud of smoke.

20 years of savings-destroying ZIRP made those builders incredibly rich and apparently irresponsible to the point of no longer understanding what their actual business is.

France G

“Cutting corners?” You do NOT understand a thing about bringing costs down.

Bad workmanship was present in older buildings too. It’s present everywhere because mistakes are made, and sloppy work has always been part of it. That’s no reason to have this elitist approach about houses. For most people, a house is a place to live in, not a work of art-and-crafts. You people are bitching about unaffordable houses, and than you post this elitist crap???

wait, hold on a sec. i’m not talking about being snobbish about upscale buildings. there’s nothing wrong, for example, with reducing costs of new houses by using formica instead of granite or marble or whatever is expensive these days

i’ve been to construction sites from lennar and horton. they hire contractors who hire subcontractors, who all the way down, hire illegal immigrants who don’t speak a word of english.

i’ve seen cabinets put on crooked, outlet plates not screwed in correctly, and so forth.

there’s nothing wrong with reducing costs by using less fancy materials and appliances. but work should still be done correctly.

So who else do you want to do the construction work???? Software engineers?

There are also occasional building materials issues: remember Chinese drywall, and polybutylene pipe?

Some materials “advances” — whether for improved efficacy or for cost — don’t work out so well in the long-run. These failures give a black eye to the industry and seem reprehensible in hindsight, but really just represent “the market” trying to figure out the cost/performance optimum.

Franz, I am a retired engineer and owned seven houses all over the U.S. during my career. We have lived in *expensive* houses in California and Connecticut. One I built using my own cherry picked subs (Conn). What I learned is you have to have eyes on contractors and inspect their work to end up with a good product. I know construction, having built large oilfied facilities for years.

Two years ago, when my wife died, I sold the Big house and bought a “new build” in a respectable area as a downsize event. Most used homes were in bad shape for the price I wanted to pay. Plus, I am in the 8th decade of my life and really just wanted simplicity and no hassles with houses. This 1,459 square foot single level house I bought is pretty nice for $175 per square foot. It’s very energy efficient having a max $100 power bill in the hot Texas summer. Heat in the winter is a $50 bill per month (natural gas). It’s tight, has double pane windows, lots of insulation, a big two car garage, and is comfortable. Oh, it’s roof is also built to survive a hurricane as there are hurricane straps in the framing.

Thew town I live in a nutty about conducting building inspections. They were all over this builder at several stages of construction. I was there for the framing, electrical and plumbing inspections. No issues were identified that could not be fixed that day. I have had NO issues with anything that was installed. Everything works and the house is pretty nice for the money. I have quartz counter tops, LED lighting throughout, raised panel doors, all appliances included by the builder, etc, etc.. While the yard is small (thank you!), it came with grass, some plantings, and three native trees per the city requirements. We also have new internet fiber into the development with speeds available up to 2.0 gigabyte/sec. (nice and fast!).

The only thing I made a mistake on is that I should have picked a smaller house, say 1,200 square feet in size as I don’t need two rooms here.

I recall reading many economic cycles ago about the decreasing quality of housing.

That complaint echoes through milenia, the romans already felt ripped of by builders. At least some of those structures have survived, especialy the infrastructure.

Roman concrete still lives on to this day…think about it.

TRUE enough far damn shore Pedro:

Having been a licensed, etc., contractor and then a certified building inspector, I can testify that ”they don’t build them like they used to” is ABSOLUTELY TRUE: Usually these days, they build them much better…

In some locations, there has been, and apparently from the results of the latest storms, fires,,, still is a TON of corruption, crony or otherwise.

In other locations, municipal plans reviewers and building inspectors are not only honest, but well or very well qualified, and do their job.

Some Locations might actually BE overly cautious, and IMO, that is a good thing for the vast majority of WE the People,,, and should include EVERY location where structures have been majorly damaged recently, whether damage due to fires, OR hurricanes, OR earthquakes.

Prices are still this high with all the inventory, wow! When the fed lowers rates house prices are going to moon!

When Fed lowers rates further, mortgage rates will spike, as we have seen. The Fed cut by 100 basis points, and mortgage rates spiked by 100 basis points. So, the market is like, make my day. Maybe the Fed should try hiking rates, to see it that brings down mortgage rates.

Haha!

Good Reply WR!

People with vested interests have been hoping that FED cutting rates would bring down mortgage rates but the opposite is happening.

I can’t fathom how home prices can go up with affordability historically low.

“I can’t fathom how home prices can go up with affordability historically low.”

Well, the logic is that ZIRP 3.0 “solves” the affordability problem the same way that ZIRP 1.0 and 2.0 did (by destroying savers earning power in order to create the doomed illusion of affordability via manipulation of monthly mortgage payments downward, so as to empower the idiotic increase in home prices far beyond Americans’ earning/repayment power).

Yes, what’s left of an actual market is, perhaps, forcing the Fed’s Hand here. Rates need to go up, it the spring of 1978, again…

Interesting times…

Fed action to lower its short term benchmark rates used to be viewed with alarm as it implied lack of inflation-fighting conviction, hence driving up longer term interest rates. We saw that again recently, as you point out. I view that as the same lack of confidence in the Fed to fight inflation. We should not be surprised when St rates go opposite of Lt rates as they’re impacted by different expectations.

I have been monitoring Western NC, Eastern TN, Eastern KY, Western VA, and Southern IN since pre-pandemic. Inventories are up but the quality of inventory is poor in the mid-priced range. Sellers of existing houses are ridding themselves of rentals, airbnb, poorly done flips, flood zone locations (at least as modeled by Flood Factor), and seemingly long vacant inventory held for appreciation. Any decent “homes” are on the market only a few days and sold at or near asking even if the location is not the best. Even houses at flood risk are going pending relatively fast if in a hot location — however, starting to see more discount on asking price and often “back on the market at no fault of seller”. The impact of recent floods and insurance company rates/denial of coverage, methinks.

Before you get too carried away with this not-in-my-area stuff, this article had zero to do with existing homes. It was all about NEW houses. And new-house inventory is up even in your area.

My son is trying to rent in NYC. I don’t know how the rental market correlates with new home data sets, but rentals in that space are plagued with all the sorts of extortions that come to life when demand exceeds supply…

8 million people on a small island…you do the math…

NYC, the land of Dreams. Every year more people show up for the Dream. Every year the same amount of people seem to be exiting the Dream. From 1980 to 2020 (using Census numbers), the population of NYC has grown by about 24%. That’s about 0.54% compound annual growth per year.

Per NYC Comptroller: Housing Units in 1980 were 2.9M. Housing Units in 2020 were 3.6M. That’s just right at 24%.

Nothing has changed, except the market has figured out how to make the Dream more enticing. NYC housing is very complex, but if it wasn’t for people like your son, it would all collapse. Thank you for keeping NYC alive.

nunya, you cherry picked your time periods. 1980 was the low point, after years of suburban flight. 2020 was the high point. instead use 1930, where the population was basically the same as in 1980, and 2024. using those dates, nyc had 22% growth over nearly 100 years!

Franz,

Keyboard warriors to the rescue! I picked 1980 because the NYC Comptroller’s data that I found only had data going back to 1980. No cherry picking here, load up your keyboard warrior shotgun and try again.

The moral of the story is that the population growth seems to match the housing unit growth. What I was really trying to point out is that nothing seems to have changed in terms of population ratio to available housing units. Meaning that, at least on paper, the demand has been equal for the time period shown.

COVID, WFH, the high rise boom in Midtown/Hudson Yards/Mega Towers. immigration, the barely half full offices, housing people in hotels temporarily, etc. have surely caused havoc in the NYC housing market. Not to mention the newly opened train lines (Grand Central Madison) that did not really get a fair chance due to WFH, and the newly planned rail expansions that are yet to come.

Me thinks that every real estate article like this should have its title amended to say

“Danger Will Robinson, Danger,” before the title.

The current housing market is such that Mr. Free Market is like Wyatt Earp in Tombstone when he says “You tell ’em I’m coming, and hell’s coming with me!”

No soft landing this time. NO SOFT LANDING.

I can order 40 tiny houses off Amazon for $415k.

With starter home sales almost non-existent. Skewing up the median price(math) of all sales. Is house prices as measured as bad as it looks, Wolf? I really enjoy your articles, thanks.

yes. only the high end seems to be moving, because the people buying those are flush with stock and bitcon gains.

tale of two economies, just like with cars.

The Case-Shiller Index exists for this reason, though Wolf (rightfully) criticizes it for lagging. It’s currently +4% YoY as of January.

Here are 5 reasons by I stopped using the Case-Shiller Home Price Index:

1. The Case-Shiller index only covers 20 cities. So it has a “20-city index” that underweights Texas (with only one market), overweights California (3 markets), and lacks other big markets entirely, such as Philadelphia. So the 20-city index EXAGGERATED the housing bust price decline because Texas didn’t have a housing bust, but it was underweighted. So the 20-city index is NOT a national index. And do NOT confuse it with a national index.

2. To fill in the gap for a national index, the CS adds the data from the FHFA house price index, which is based on prices from mortgages that have been securitized by Fannie Mae and Freddie Mac. It doesn’t include data from sales where Fannie and Freddie mortgages were not involved (cash deals, jumbo mortgages, VA mortgages, etc.). So this FHFA house price index is systematically skewed to Fannie and Freddie mortgages, and it systematically skews the CS index. To include this data is unforgivable, and for that reason, I have never ever used the “national” Case-Shiller index.

3. The CS indexes for the 20 cities are available only as index value, with that value set at 100 for the year 2000; and not as dollar prices. So by looking at the index of each city, as I do, you have no idea how expensive they are in relationship to each other.

4. The CS was invented by three guys at a university in 1991 on a shoestring. It was a huge advancement at the time over median prices. The three guys – Case and Shiller being the two lead guys – formed a startup company and commercialized the index, and then sold the company. It has changed hands several times since then and now is part of S&P. Neither the prior owners nor S&P invested in the index to gather data on more than the 20 cities and to use modern data collection technologies. So it has been left behind.

By contrast, Zillow has invested billions of dollars to build its “Database of All homes,” and it continues to invest in it. This database contains everything… property tax records, MLS records, data from the local Realtors associations (especially useful in Texas which is a non-disclosure state), data from Zillow postings, pictures of the properties, transaction histories, etc. It has everything the CS has (sales pairs) plus a gazillion more data points on individual properties in all markets.

5. The CS uses an algo to weight the sales pairs. That is the shortcoming of the sales-pairs method. You have to assign weights to the sales pairs, depending on when the prior sale occurred. For example, a sales pair where the prior sale occurred a year ago is weighted heavily. A sales pair where the prior sale occurred 20 years ago is weighted much less. These algos are decisions, and not current market conditions. With the sales-pairs method, there is no way around these algos, but these algo are just human-designed algos, and so part of what you’re seeing is the calculation of these algos. And I have seen it produce some strange results.

6. The Case-Shiller lags 3-4 months, which is unforgivable with today’s data-gathering technologies. It’s just outdated.

Thanks for pointing this stuff out!

This could be a whole article. I know you wrote about your decision to use Zillow instead of Case-Shiller before, but maybe not with all these details succinctly stated.

I think about 16 people would find that interesting. If I count myself, LOL. But I’ll think about it. Some of that geek stuff finds an audience.

Make it 17

Meh, I don’t feel sorry for home builders. If they get into too much trouble, they can announce, like GME, that they will buy bitcoin with their cash and watch their stock sky rocket. Life in the fast lane I guess…

You’d think Homebuilders would have backed off by now; surely they have executives to predict this type of thing. And by tamping down supply, they could keep prices high or even go higher?

But I guess other builders would continue on and the ones who backed off would lose out. This is competition, I guess. But I would expect some under-the-radar collusion out of these companies…

Collusion? Yeah, like in all competitive business. I sold bulk copper water tube years ago and we “priced accordingly”. LOL!

MussSyke

I love the homebuilders for piling on the supply. That’s exactly what this housing market needs. We need a glut of new houses for years. And then, if they want to sell them and stay in business, they can cut prices to where buyers cannot refuse.

I really don’t give a hoot about their stock prices.

Like Wolf has stated in the past, homebuilders cannot stop building. If they stop building, they go bankrupt. Their business is to build homes and sell them for a profit. Can’t sell something that doesn’t exist (putting Enron aside, they figured it out, but some went to jail).

They take higher losses up front from old builds, then the new pipeline of homes gets built cheaper, so they lose less money on future sales. Loss per home will hit a max at some point. Then the losses should swing back and start to decrease. At some point, they should find equilibrium and then come out the other side with some bruises, but still alive.

Then, maybe in the distant future, they can start making money hand over fists selling for higher margins to future generations. For now, margins are lower than before, and headed lower. Some may go into negative territory at some point before they get out of this phase.

Look at KTM motorcycle company. Their executives had no clue.

Byron,

That is definitely a headscratcher. I’ve been riding motorcycles for 20 years, and always admired KTM for their sheer performance, but not so much for their maintenance costs. When their inventories started to balloon I started keeping my eyes open for “deals” thinking that they would start cutting prices. The price cuts never came and my idea of getting a new KTM at 50% off MSRP vanished.

What’s interesting is that they came out recently and actually admitted to “miscalculating demand” after COVID. I’ve bought plenty of 2-3 year old Japanese bikes which were 40-60% off MSRP due to the Japanese misjudging demand, creating weird models nobody wants, etc. The Japanese seemed to react quicker in the past.

I think the homebuilders have lots of tools at their disposal and hopefully their scars from Housing Bust #1 help them navigate the next 4-5 years.

Wolf, there was an WSJ article on how the Government has essentially held back foreclosures from occuring since 2021….hundreds of thousands of subprime mortgages out there not being paid and the government re-allocating the bill to the end of the mortgage.

I wonder how the lack of existing foreclosure homes hitting the market from the bottom end has affected this supply, and whether that would force the hand of many to drop prices.

That was a BS OPINION piece in the WSJ, run in the WSJ’s opinion section. It suited people’s political narratives, such as yours, and so it went viral, and people are citing what they think it said though they have never read the article. I have crushed this piece and people conclusions about it here several times already. Go look for my old comments on it. Not wasting my time on it anymore. Basing any conclusion on this BS piece turns the conclusion into BS, such as your entire second paragraph.

What is going on in housing cannot be viewed separate or independent of larger economic forces going on with the US and rest of world. We are in a fourth turning period that is involving the US losing its unipolar status. The new economic power of China as well as resource rich countries like Russia, can no longer be ignored by the US if we want to maintain dollar hegemony.

This means the Fed, Treasury and all else involved with economic goals are being forced to do things contrary to what has been done in the past or that we might predict.

This means there will be no QE in the future (IMO) and lowering of rates will also be unlikely as the US has lots of debt to sell in the coming months/years.

Housing will adjust to these new realities and it will be painful. Essentially, prices will slowly grind down from here as sellers will have to give in if they have to move. I’m seeing this already on the ground in western NC. Not moves downward that would compare with the craziness upward a few years back, but signficant give ups in price with each seller as compared to the mentality that they went in with….housing prices always go up.

“such as not being able to get affordable insurance or financing falling through.“

Or ANY insurance in the West, or even the southeast. Fires and floods are apparently a new thing and unable to be insured against by any major insurance company?

In my pock of la-la-land I don’t think there’s many spec homes going up, but construction is still booming! I swear once the shovel hits the ground for the 4 seasons it’s a “look out below” moment… but I am just a Struggler.

The spike riders are starting to get nervous and people are cashing out all over the place from their ”used homes” (trying anyway). Since it’s all sky high luxury market, it’s humming along with cash deals, as people just want to park their money somewhere.

Prices are still ridiculously too high though.

“Fires and floods are apparently a new thing and unable to be insured against by any major insurance company?”

f you check history, fires, floods, hurricanes, tornadoes, etc are not a new thing.

Your access to this site has been limited by the site owner

Your access to this service has been limited. (HTTP response code 503)

If you think you have been blocked in error, contact the owner of this site for assistance.

If you see that it means you’re using a VPN that assigns you IP addresses that it assigned previously to comment spammers that got blocked. Stop doing business with VPNs that do that, or stop complaining about your IP address getting blocked, or turn off your VPN.

https://wolfstreet.com/2025/02/24/dear-wolf-street-readers-are-you-using-a-vpn-heres-why-you-might-get-blocked-and-what-you-can-do-if-you-get-blocked/

Locally small town middle of nowhere Wyoming, there has been a boom in construction and numbers of people move here. Last year we even had the first classic model home subdivision open for business. Prices starting at $420k….This year – work mostly ends for outfits like this through the winter – it’s prices starting at $380k.

Otherwise prices remain solid, but very little is selling. People cant accept they missed the top and are determined to get those crazy prices. It’s unpredictable how long it will take to break that fixed idea. Probably it will take a rise in unemployment around here that forces people to sell for what they can get. For now they are mostly aspirational sellers.

or maybe living through a couple of bitterly cold Wy winters will send a few homeowners packing.

What I would like to know is what the aggregate impact the open border policy of the last admin has been on the housing market. If the native born population is low or zero gtowth,then the apparent increase in demand must be tied to international immigration, I would think. I see many high density housing complexes in jax,fla. A whole article on getting to the truth on that would be most helpful. Huge amount of research would be needed though.