Short-term Treasury yields of 6 months or less stay put above 4%.

By Wolf Richter for WOLF STREET.

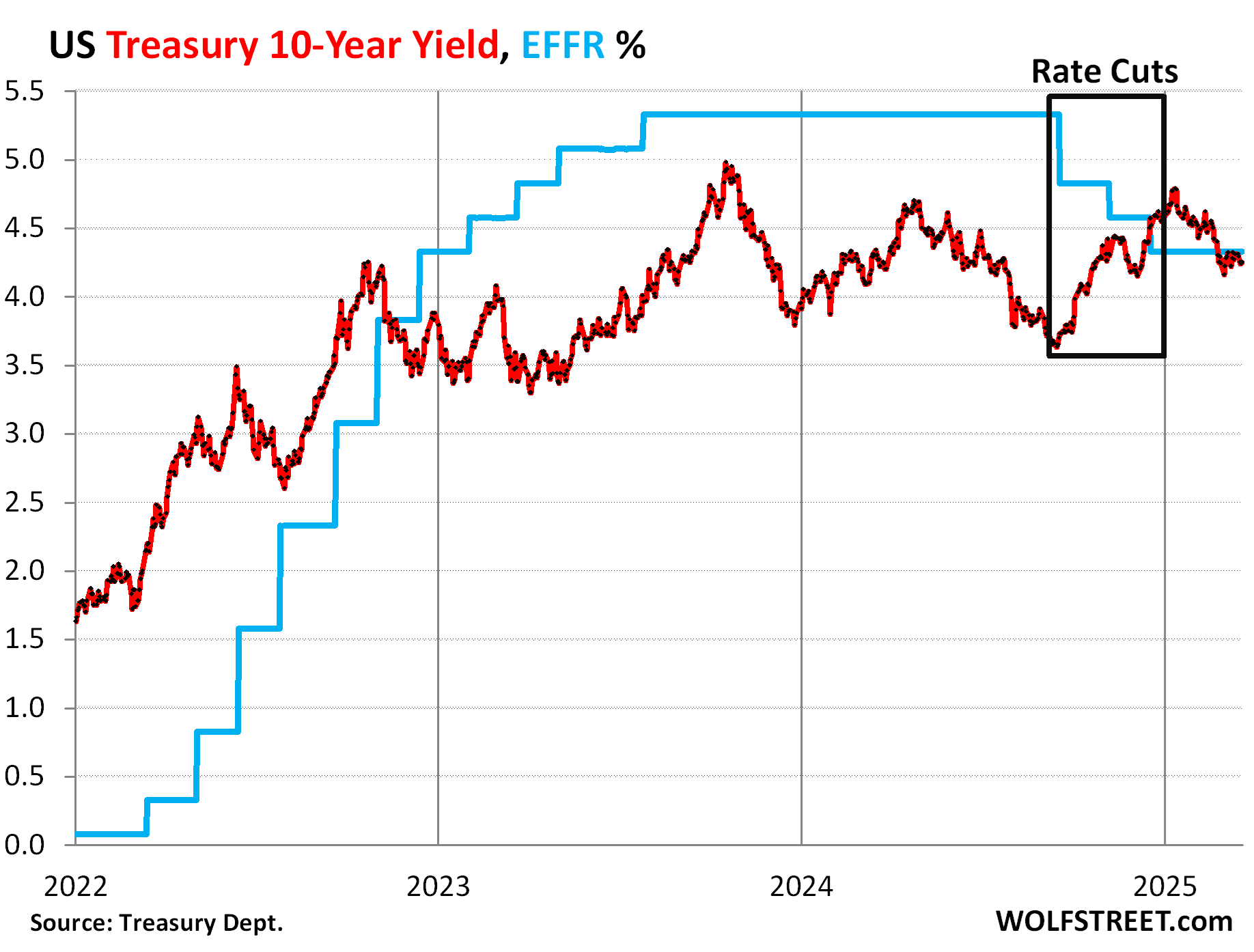

The 10-year Treasury yield has careened lower from 4.77% on January 10 to 4.16% on March 3, and has since then wobbled a little higher to end at 4.26% on Friday, just a hair below the effective federal funds rate (EFFR) that the Fed targets with its short-term policy rates. This decline in the 10-year yield isn’t a coincident.

The government has been trying to push down, talk down, swat down, and wish down long-term Treasury yields to make funding in the economy for businesses and households less costly – the stated policy of Treasury Secretary Scott Bessent.

These efforts have been fortified by the Fed’s more hawkish stance on inflation and interest rates, which put the bond market at ease. The bond market had gotten spooked by the Fed’s 100-basis-points in rate cuts despite re-accelerating inflation, which triggered a bond selloff that had caused the 10-year yield to spike by 114 basis points, even as the Fed cut by 100 basis points. The long-term Treasury market fears out-of-whack inflation more than anything.

That ironic situation when the Fed cut its short-term policy rates by 100 basis points, while the long-term Treasury yields spiked by over 100 basis points, has now been partially unwound.

Despite all the drama and irony of rate cuts accompanies by surging yields, the 10-year Treasury yield has remained in its two-year range and is now in the middle of that range.

We can see the strategy here to get long-term yields down:

- Obviously, the Fed gets more hawkish about inflation and puts rate cuts on ice, after its rate cuts amid accelerating inflation spooked the long-term bond market.

- Treasury reduces supply of long-term securities by shifting issuance to T-bills, which it has been doing for over a year. During the debt ceiling, new supply is on hold anyway.

- Treasury talks down the 10-year yield, which Bessent has been doing.

- The Fed slows the QT of Treasury securities from $25 billion a month to $5 billion, starting in April, though QT of MBS will continue to run at the current rate.

Long-term yields matter to the economy. They’re the base for borrowing costs for businesses and households. While there is some debt with floating rates, the majority of the debt has fixed rates that roughly parallel 10-year Treasury yields, but are higher. A rising 10-year Treasury yield increases borrowing costs for new debt in the economy and tighten financial conditions and eventually slows the economy.

But a lower 10-year yield boosts the economy and might add some fuel to inflation, which would be in line with the Fed’s three-year mantra “higher for longer” – higher Fed policy rates and higher inflation.

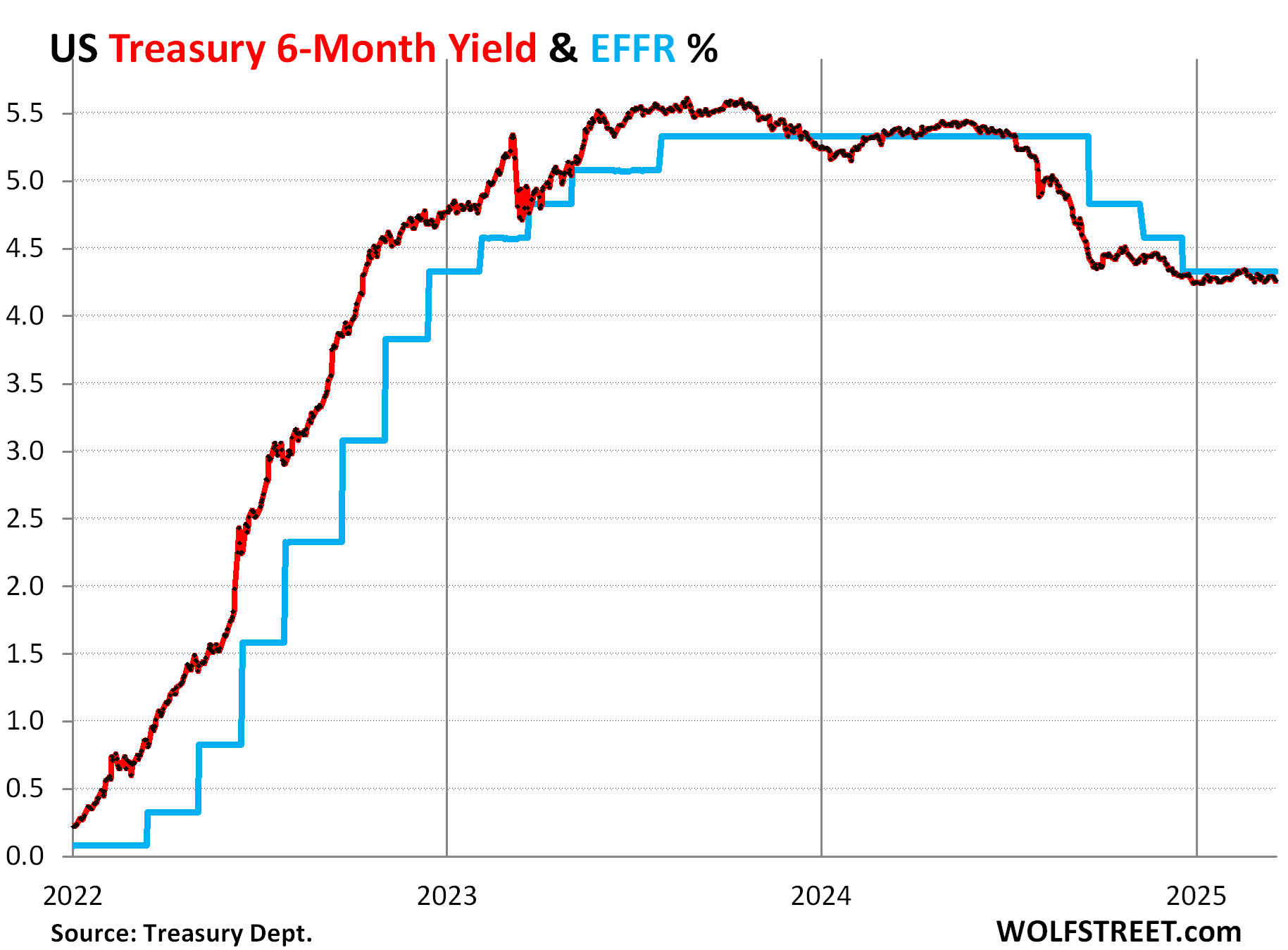

But short-term yields of 6 months or less stay put above 4%.

The six-month Treasury yield had already priced in a big part of the 100-basis-points in rate cuts by the time the first rate cut happened, having dropped by 90 basis points from 5.4% in May to 4.5% just before the September cut.

Today, it’s at 4.23%, still glued to the underside of the EFFR, pricing in only a minuscule chance of a rate cut within its window over the next few months.

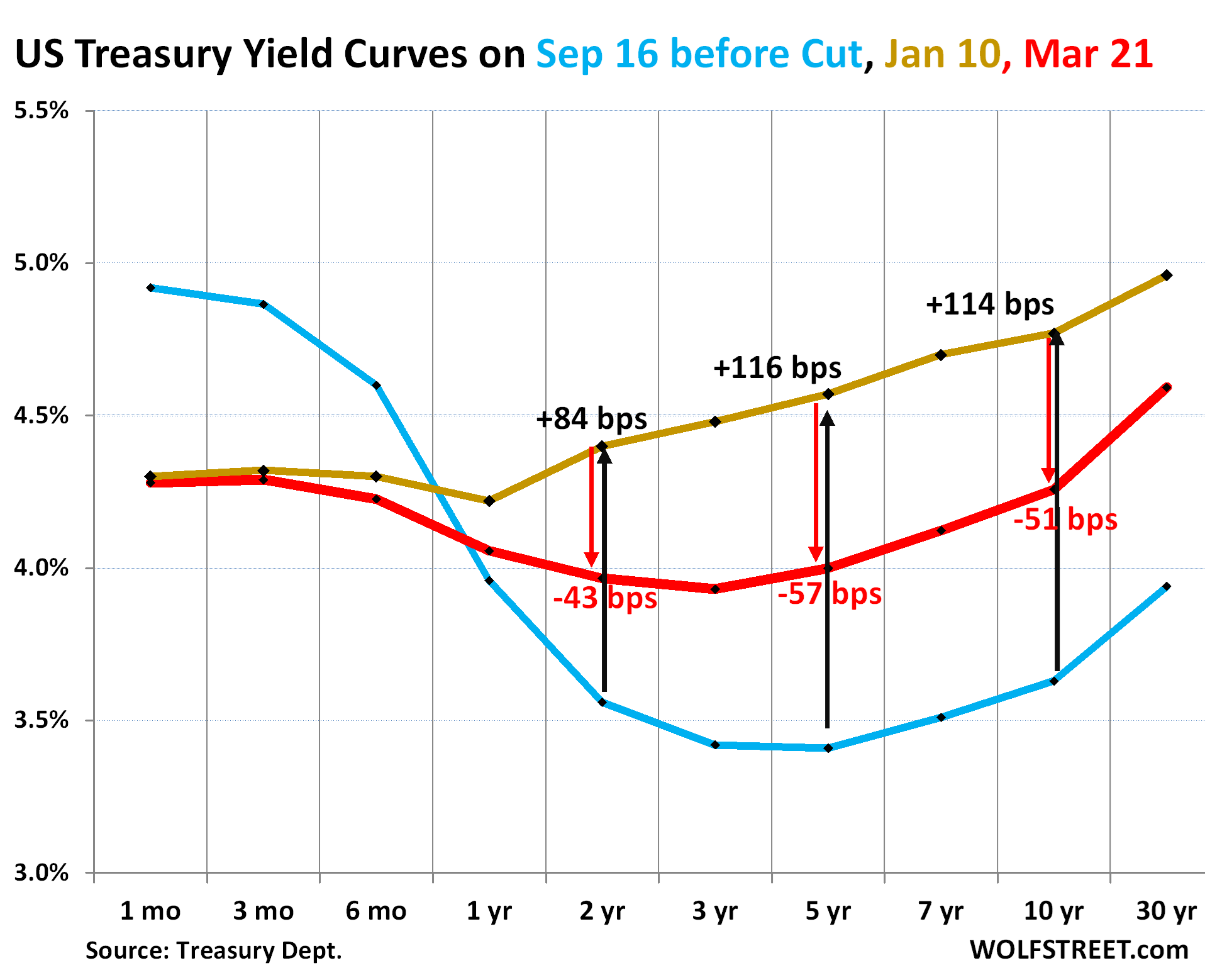

The yield curve has re-inverted with a sag in the middle.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: January 10, 2025, just before the Fed officially pivoted to wait-and-see.

- Red: March 21, 2025.

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

With rate cuts on ice, short-term yields haven’t budged much and remain glued to the EFFR. But longer-term yields have dropped since January 10. As a result, yields from 1 year through 10 years are now all lower than short-term yields, and only the 20-year yield (4.61%) and the 30-year yield (4.59%) are higher than short-term yields, creating this sag in the middle of the yield curve with the low point at the 3-year yield (red line).

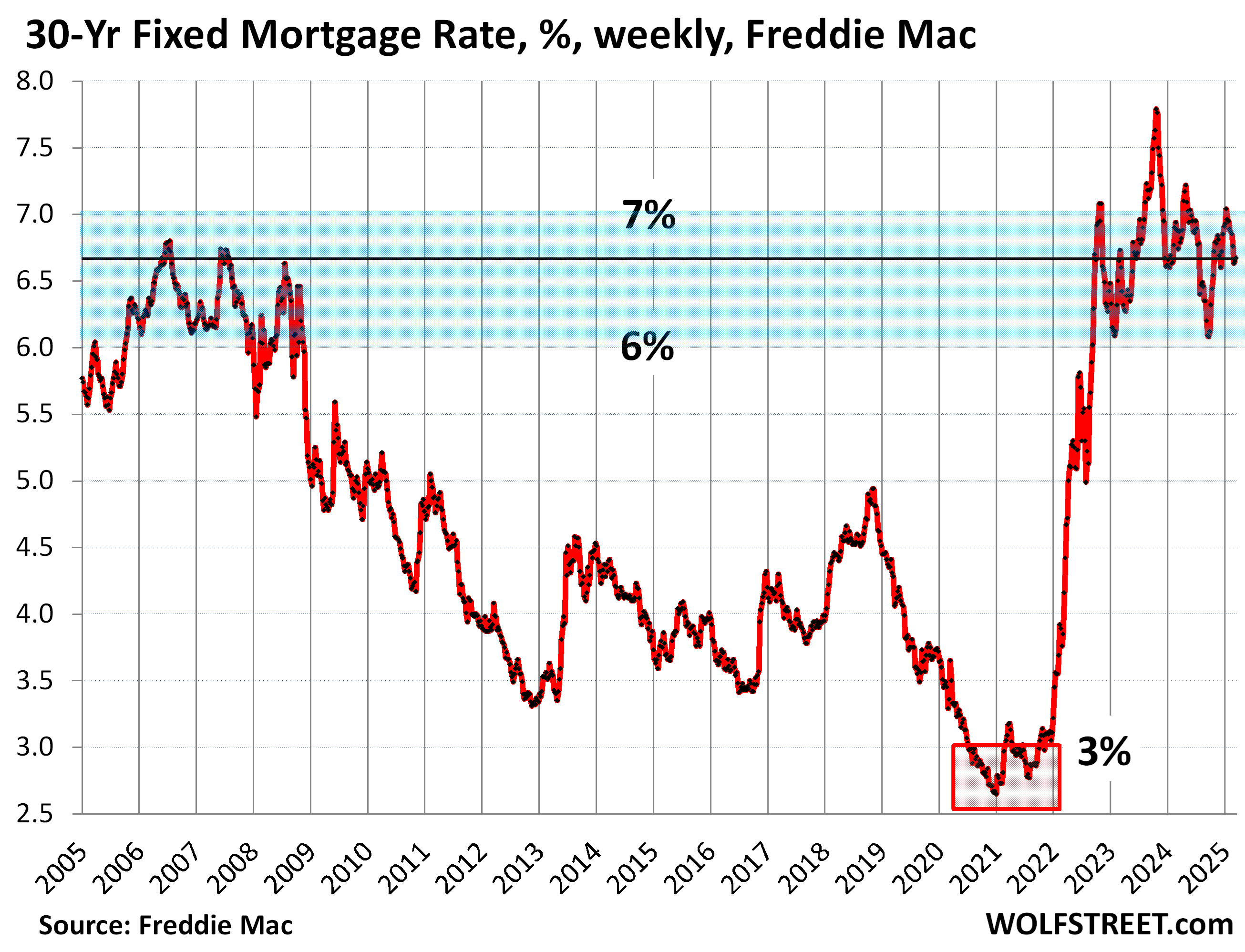

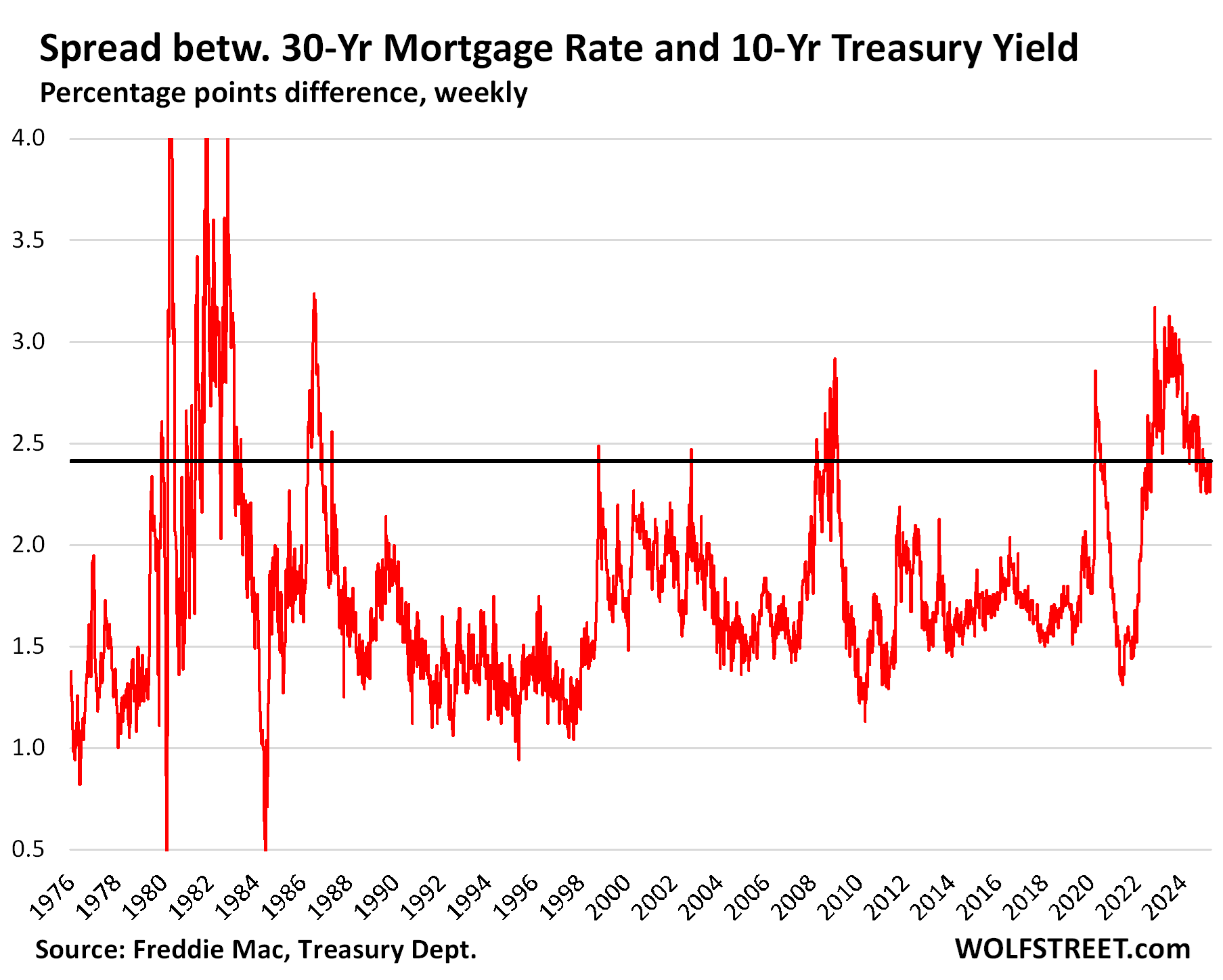

But mortgage rates aren’t fully buying into it.

From mid-September through mid-January, the average 30-year fixed mortgage rate had risen by 96 basis points, to 7.04%, according to Freddie Mac’s weekly measure, while the Fed had cut by 100 basis points, an irony that had perplexed the real estate industry, which had expected the rate cuts to push down mortgage rates.

Mortgage rates have since given up only 37 basis points of this 96-basis point surge – while the 10-year yield gave up 58 basis points, and the spread between the two has widened.

At 6.67%, the average 30-year fixed mortgage rate, per Freddie Mac’s measure, is at the upper half of the 6-7% range that has prevailed since September 2022.

In the three decades between 1972 and 2002, that 7% was the lower edge of the range. For most of that time, rates were above 8%.

The mortgage-rate spread widened.

With the latest move in yields, the spread between the 30-year mortgage rate and the 10-year Treasury yield widened to 2.41 percentage points.

After QT was announced in the spring of 2022 and kicked off in July 2022, mortgage rates increased faster and further than the 10-year Treasury yield and the spread widened sharply, and eventually exceeded 3 percentage points, which was very wide in historic terms, last seen in 1986. From that high, the spread narrowed to 2.41 percentage points now, but remains very wide historically.:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Savers have no friends in this economy

Welfare and medicaid rule.

Savers get 4%+ on T-bills. The Fed has been the savers’ friend since mid-2023, and Wall Street hates it.

Hal needs to stay away from the kool aid. I have been enjoying my >4% in laddered CDs.

Hal needs to catch up with current events.

Bill Clinton eliminated the Welfare program way back in 1996.

Medicaid was cut $800 Billion earlier this month.

The tax cuts for Billionaires coming later this year don’t pay for themselves, don’tcha know.

I’m buying property and just got owner carry at 4%

then again I’m putting down 63%

and my term is 60 months

I just bought a 10 month CD at my local credit union for 4%. I’m buying CDs in a ladder, so that one matures every 3 months. Just like having a 4% savings account. I sleep well at night while the market goes up 500 points and down 500 points nearly every other day. Why anyone would put their money in that casino is beyond me.

Because my properly allocated casino has already paid me 8% this year.

Why not 4.2% in 1-3 month T bills? More liquid and a higher rate. Treasury direct. I put in the annual known expenses (property taxes, insurance etc) in it and wind it down through the year.

thanks for reminder

I’m doing Jumbo 60 day at chase tomorrow

need few extra $$ for close in May

yes earning yield on the s&p500 is 3.5% that is incredibly expensive — I will also take 4% and know I will get my money back.

You’ve already said why. The price volatility that you mentioned in that casino is what allows those that know what they are doing to walk away happy on a daily basis.

Some of the stocks and closed end funds I bought during the pandemic are up 100%, and paying 7-8% interest. We need to be ready for those extreme dip buying opps.

and since that time in mid-2023, the nasdaq is up nearly 30%. looks like wall street is still sitting pretty.

Frank,off topic but wanted to mention your response to my ownership of gold(another article) and it’s rapid price rises bugging me a bit is because I do not want to see huge economic hardship for others as you mentioned,will be happy if me gold just stays a inflation hedge and does not need to rise dramatically.

I try and have a few different baskets of monetary storage to hopefully cover me butt,would be glad if never truly needed them and life chugs along at a nice pace for all,just can’t count on that!

The Great Fed Chicken-Out of the spring of 2023–bailout of uninsured Silicon Valley depositors followed by pause in rate hikes–sent an unmistakable “party is back on” message to the markets. The markets didn’t miss that message, although others did. Stocks back up, crypto back up, housing back up.

Yes,but they were unfriendly thru 14 years of 0% rates…

RRPO has wound down banks are going to have to pony up the interest and bank reserves are falling with QT. Its S&L Deja Vu, again but somewhere they always find the money. Just wait for a revenue and expenditure mismatch. maybe by a lot.

nah, there is still at least $1.5 trillion to much in reserves. If banks start relying on the Fed’s reborn SRF for their daily liquidity balancing, like they used to before 2009, reserves could drop a lot further, by maybe $2.5 trillion, and the Fed would have to reimpose “reserve requirements,” which it paused in 2020.

Yes, things have gotten better for savers since the spring of 2022 when the long night of ZIRP started ending.

But…

“In the three decades between 1972 and 2002, that 7% was the lower edge of the range. For most of that time, rates were above 8%.”

Since banks (largely) pay depositors out of their loan interest proceeds, the Fed’s more-or-less 20 years ZIRP saw mortgage rates cratered (hello housing bubbles 1 and 2) and savers essentially expropriated to pay for it (and gut the interest due on DC enormous, accumulated debt/perpetual deficits).

My assets say bring the hyperinflation

This may be one of the rare times when savers in longer term treasuries will be vindicated. The most likely scenario for the good old USA is a recession and the agnostic Fed will lower interest rates to 3.1 and the value of the 10 or 20 year will rise 10X pct in value.

If the recession scenario doesn’t work out as planned, the sweet 4.25 pct return while the asset market bubbles collapse under their own weight, is on it’s face an even bigger win for your mindless characterization of the population of the USA, the savers.

Unless inflation continues to take off and the dollar’s loss of value accelerates

dang

Buy them with 10 to 1 leverage and make a killing when the recession hits.

What would you do?

$100000 2 yr 4.3 %

or

$100000 5 yr 4.1 %

Billionaires rule and they are going to take everything they can get.

Let the looting begin!

It will not help them.

“welfare and Medicaid rule” … Funny how a year ago we heard nothing in these comments about Medicaid and welfare. I guess they weren’t pushing that nonsense on fox state media at the time. $4.5 trillion debt increase for tax cuts for billionaires is what actually rules the day. Just saw a study that showed blue states contribute 60% of the tax base but red states take 47% while only contributing 40. Then complain about the programs their states use a greater percentage of. I look forward to hearing what the lemmings start complaining about next.

Red states have blue cities and blue states have red counties. Most welfare is appropriated in cities

I lived in a deep red rural area of Texas for many years. Hardly anyone except the illegals did any work. Nearly everyone was cooking meth!

Who in their right mind, would loan money for years at these rates? Way too much uncertanty and that forever transitory inflation.

I for one welcome our new saggy diaper Treasury yield curve. As long as the left side of the diaper stays firmly attached to baby’s waist, I’m a happy investor.

I like this metaphor. Especially given the fact that diapers sag when they are loaded with crap.

Sitting in money markets seems wise.

Inflation and supply disruptions are all but inevitable as manufacturers are reluctant to commit to production.

Equity traders know that tariffs will affect margins and stock values – which is a sell signal.

Consumers are key decision makers and while they have been spending, there are clear signs that they are weakening.

The border is closed and deportations are proceeding.

Farmers are assessing what to plant in springtime with the awareness that export demand for their products may evaporate. (Making their decision more difficult is that there may be no subsidies for their losses).

CRE oversupply is coming to a head and defaults are proceeding quietly.

War in Ukraine and Israel/Gaza continues.

Interesting times…

Frosty-

You’ve made good points, well stated.

I’m not sure, though, that these points argue all that well for keeping one’s entire savings “sitting in money markets,” versus diversifying one’s portfolio risk into:

— some longer duration Treasury securities to lock in income for protection from the possibility of a period of lower rates if recession breaks out,

— reliable dividend paying stocks (to keep one’s income stream growing with inflation),

— well-cared-for real estate to protect one’s self from (rent) inflation.

Laddered short to medium treasuries, modest allocation to a mix of cash-flow oriented stocks, substantial home equity, SUPPLEMENTED with a money market stash, seems sensible for most long-term investors, IMHO.

(Perhaps you were advocating keeping just a portion of one’s portfolio in money markets… not all? If so, I stand corrected.)

Respectfully.

John,

My comments are relative to my personal situation for certain and have taken profits on about 40% of my highly appreciated long term portfolio, (mostly the tech stocks). Long term taxes on those are a hit, but I’m comfortable with our tax rates given the extraordinary country and culture we live in. Sure there are issues, but look around the planet and be thankful!

After being priced out of real estate until my late 20’s, I have owned multiple homes most of my life and created a great deal of sweat equity, rental earnings and appreciation along the way, it is all paid for. Collector cars, art and other assets round out what I thought I would never achieve.

Over the years I have added high quality, dividend paying gold mining stocks. Recently I noticed that the mining stocks and the Van Eck gold mining fund GDX has significantly underperformed. It only pays a 1% dividend so that is not particularly desirable but I think it has room to run with the current political and financial situation.

Appreciate your response and of course Wolf for providing a thoughtful well informed forum,

Regards

Fed chair Powell sez “the most likely outcome is that higher inflation in 2025 will be a “transitory” impact from tariffs.”

A 4% return after tax is about 3%. After 3% inflation it’s nothing. What’s great about that?

As Gundlach said this week, the Fed might be downsizing QT to tee up QE. The Fed has done some crazy things to curtail asset price drops, and a drop is now threatening.

Inflation applies to all assets!!! Including stocks, which are down this year, not up. So you lose money to inflation, lose money to stock losses, and lose money to taxes. Why do I constantly see this BS about inflation and taxes only applying to T-bills?

Gundlach has been wrong since August 2020 when he predicted negative yields. He is a bond-fund manager and MUST have falling yields to make his funds look good. Why is anyone still taking him seriously? Because it fits your narrative????

I’m not saying there’s anything better. But what that means is the Fed is still applying a form of financial repression by tolerating a high inflation rate for long periods (5 years now!). People shouldn’t say that 4% rates are great or even acceptable in a 3% inflation environment. That’s BS cheerleading.

The Fed needs to bring inflation down. The results say they aren’t trying hard enough.

agree. they’ll never admit it, but i think the fact that they keep throwing the asset markets a bone every time a correction looks to be coming shows that they’ll tolerate high inflation, and societal destabilizing wealth inequality, in order to avoid a recession.

our economy is now built up around the wealth effect spending of the rich. that’s why so many car manufacturers, hotels, and other businesses now cater to the top, leading to a dearth of affordable options.

sure, in a vacuum, the fed might be willing to let stocks and housing crash. but if they can’t do that without a major recession, which i believe they can’t, they’ll prevent both.

Agree.

b

For what it is worth, treasuries are state-tax exempt, effectively bumping up their yield some fraction of a percent depending on which state you live in.

I don’t know if it is on purpose and part of their grand plan to get rates down but sowing economic uncertainty is also playing a role.

Consumer confidence down due to various things but including all the DOGE drama and tariffs is also helping to push rates down.

I think lower rates is an additional benefit to their recent actions and “uncertainty”. This is what they want.

We just came back from dinner… Chestnut St. in San Francisco, where there are a lot of restaurants clustered together, including in the side streets. We couldn’t get last-minute reservations at any of our favorites, so we tried our luck as walk-ins. The 8th place on our list of restaurants we like had two spots at the bar where people had just left. And we grabbed them. Minutes later, people were waiting outside… The sidewalks were packed with people. If there is a slowdown in the restaurants business and consumer spending, it wasn’t here. I’m not sure I’ve ever seen it this packed. Drunken sailors all over again.

Top 20% still riding high on the various bubbles eh?

Checking my crystal ball to figure out what’ll bring down those ‘animal spirits’ and figure it’ll be awhile before the political instability catches up with that bunch.

The bottom 50% don’t seem very happy but that only counts in elections apparently. I suspect a fair amount of them are starting to regret their support considering red states get more govt funds than blue from what I read. Will see if they get heard as the demolition of democracy and progressive redistribution progresses.

Government trade policies previously favored blue states. Subtract out defense

spending and the federal dollars to red states looks more in line.

Been curious why with all the crying about fraud and abuse, defense never gets looked at seriously. A red state skew might help explain why.

This past year was very up and down. From time to time all the shopping areas and restaurants would be wall to wall people. But then during peak summer travel it was so quiet I almost couldn’t believe it. The previous year 2023 had been insane everywhere during summertime. Summer was quiet but fall 2024 was super busy again. It seems to be a time of consumer binging followed by temporary sobering up and then repeat.

Wolf-

Your portrayal of the Drunken Sailor atmosphere as you searched for an open table identifies an era.

I remember my folks (RIP), both born in the 1920’s, having great difficulty spending their wealth, which reticence was largely responsible for the wealth they did have. Their generation was known as the “depression babies,” and their disposition toward savings and frugality was legendary and almost irreversible.

Old financial habits instilled by years of luxury OR deprivation change slowly, if at all, I guess.

Thanks for your articles and your active involvement in the comments thereafter.

Dear John H. You described a squirrels life very well. They work till retirement and start spending more, saving more. Hard to do

Sober Sailor

I will say a Saturday night is probably most popular,feel many not dining out as much but still treat themselves occasionally.

My favorite spot jammed day and night weekends,during week sometimes wonder why they bother to open,me guess is just enough regulars to break even and the weekend the profit bonanza,place used to be packed all nights during week excepting maybe Monday.

I will say while not cheap not high end price wise,great food/large servings and a very friendly/attentive staff along with large servings(doggy bag at times!)keeps them rolling.

Same here in Naples Florida, the sailors are eating and drinking and paying big $$$ to enjoy the spring break fun.

Restraunts and bars packed and mostly sold out.

Happy days.

Sounds like you found the better half of the haves and have-nots. Was there a good amount of folks looking for crumbs around the corner as well?

Look, this site is about the economy, it’s not a social studies site.

Tax refund season. Always packed restaurants during this time. Maybe not big difference in high dollar area like sf but definitely in middle america.

Same at my Irish Pub. I have to get there at 4:PM to get a seat. Spent $80 for two including drinks. The Drunken Sailors are alive and well. No one here seems to care that 37,000 Federal workers just got fired. Actually, a lot of people here are salivating.

And it is in this context that the fed is looking to cut rates, and has already reduced QT. A true friend to savers, indeed.

That’s a great area, have spent a fair amount of time there. Good times.

QT has no impact at all on short-term rates, such as the Fed’s rates, T-bill rates, money market rates, or CDs of 1 year or less.

Yes, agreed that QT does not impact short-term rates directly, but it’s more about the overall market support. It certainly can impact long-term rates for those savers, and the housing market through their purchases of MBS – also still too slow IMHO, should be outright selling those as they never should have bought them to begin with.

Thanks for your thoughtful response.

The captain is drunk too. Nobody is watching the ship as it heads towards an iceberg.

$2-$3T deficits during the good times? Ridiculous!. Financially speaking, nobody should have anything good to say about anything while that is going on. It’s unsustainable and getting worse by the quarter.

The captn is just having a few beers in the wheelhouse. He’s not drunk and you’ll see the iceberg pass by on the stbd side in a few. Carry on deckhand.

I see packed restaurants and hard-to-get tables here in Southern California as well…but I also see longtime favorites calling it quits at a frightening rate. I really don’t know what to make of it, or what to make of that recent retail sales report that had restaurant sales down, while everything else went up, after accounting for price changes.

There are said to be 7,000 restaurants in the city of San Francisco (a foodie town). They’re in CONSTANT flux. One reason is that they get old and tired and need renewal, and that is usually when the 10-year lease comes up for renewal. Another is that when the 10-year lease comes up for renewal, the landlord says, I want double the rent, and the tenant says, make my day. And that happens a lot. The natural attrition rate of restaurants is huge. Which is why in a dynamic restaurant city, there are always lots of new restaurants. And you see it here. A place closes, and not much later, there is another restaurant in it. There are a bunch of new restaurants on Chestnut Street (topic of my comment above), and there are a bunch of new ones in North Beach. Change is good.

We saw this at our local Chilis here in town. The kids like to go and the food quality is great at ours. Anyways, I got the last parking spot and we got the last booth. And I even had a beer; but not enough to be a Drunken Sailor!

“From that high, the spread narrowed to 2.41 percentage points now, but remains very wide historically.” Very interesting article. Seems like there’s still room for the spread to narrow. Ignoring other variables, it’ll be interesting too see which end compensates or if they’ll meet in the middle. I’ll guess mortgage rates are more likely to drop to catch up with recent decreases in the 10y yield, but hope that’s not the case. Wouldn’t be surprised to see the spread stay pretty large for a while, as long as the 10y yield is being pushed (manipulated?) down by these factors.

“ Seems like there’s still room for the spread to narrow.”

There is, but, QT on MBS remaining unchanged may inhibit the spread with the 10-Year narrowing materially. Maintaining the status quo in this regard appears to fall outside of the “strategy” and may foreshadow the next policy move in QT on MBS; or maybe it will be satisfactory for the headline mortgage rate to simply fall in line with the 10-Year (assuming it does), notwithstanding the spread.

“Manipulation” is an overwhelmingly more apt description than “strategy. Too much tactical engineering, and perhaps virtue signalling, is creeping in. The dissenting vote on the FOMC should not be underplayed in my opinion.

Will this hold?

Or will it revert back to the inclined ‘normal’ curve when the TGA is refilled, or the inflation prints come out hot, or whatever?

I see no reason to believe that inflation is truly finished yet, and I see no reason to buy medium or long-term bonds if inflation truly is going upwards. Recession or no recession.

i don’t see how long term yields can come down much more without more printing.

“inflation truly finished yet”. Worth noting here that inflation is our current policy and has been for decades if not forever and will always be forever.

(The official policy is 2% per anum). Plan accordingly; it’s not hard to plan once the plan is understood.

I’m not very knowledgeable about these sort of things. What is the implication of the mortgage rate spread increasing or just remaining high? So the Fed drops rates but mortgage lenders don’t follow suit. It seems like mortgage demand is very low so you’d think lenders would need to give more competitive rates. But they aren’t. Does that imply they see increased risk in lending? Or is there some other mechanism at play here?

Great article! Thanks!

The mortgage market may have a better grip on the long-term implications of future inflation and rates than the day-to-day casino that is the trading in the Treasury market?

A wider spread means relatively higher mortgage rates, compared to 10-year Treasury yields.

Thanks for the reply! That would make sense to me. Seems like the lenders have the most skin in the game so they be more in touch. I’m interested to see how this developes over the next few months.

Long-term interest rates have always approached a limit (“a value that a function or sequence “approaches” as the input or index approaches some value”). That “value” is also about the “arrow of time”, viz., “directionally sensitive time-frequency decompositions”.

The cause of all bond proxy movements, i.e., characteristic movements (putting 2 and 2 together) is always a posteriori knowledge.

The Donald wants lower rates. “Careful for what you wish for!”

b

The forces that shape the spread between mortgage rates and 10y treasury yield changed when banks essentially left the mortgage market with the pandemic. There is less competition now. It’s unlikely that the spread will go down unless competition goes up back to normal too.

Bond yields are about average historically for a deflationary economy, 1925-1955, EFFR historically close to normal, and the yield curve inverted, and Real Interest rates rising, which is typical in an inflationary economy. Meanwhile household debt levels are falling, and govt policy to reduce debt includes households (who own stocks) result the mother of all balance sheet recessions. Unemployment turns up (cant go much lower) and Fed cuts EFFR, and bond yields rise again b/c debt is being paid down. Theres a lot of cash in MM accounts.

“….for a deflationary economy,..”

🤣❤️

where does this stuff still come from, amid all this inflation we’re having???

LOL! Deflation? WTF are you talking about. It’s 1979 again!

Wolf, This off topic, but I am hearing a lot of claims that excessive FHA home mods are slowing down price discovery. Do you have any info?

Mortgages have always gotten modified. It’s a standard procedure. Forbearance is another option. No lender wants the house. They want the interest. They do what they can to help borrowers keep the mortgage running if they have a temporary issue, including natural disaster, job loss, etc. If you fall behind on your mortgage, call your mortgage servicer and see if you can work something out.

This happens massively in CRE, where it’s called extend and pretend. It’s a much bigger deal there, with huge mortgages, than the relatively few and small residential mortgages that get modified. Banks have always done this because the absolutely last thing they want is end up with the property.

There cannot be any major problem in mortgage land until home prices drop a whole bunch from the price that borrowers financed, and those mortgages are deeply underwater. That’s when problems occur. Right now, there is only a very small crop of buyers that bought at the absolute peak of prices in some cities where prices have dropped a lot, and whose mortgages are substantially under water, and that have trouble making the payment.

There was an opinion piece in the WSJ with a clickbait title and subtitle that were shared. The piece was also larded with BS. And it made the rounds. That’s where all this BS came from.

Thanks Wolf for the insight on CRE forbearance. I always wondered over the years about long time vacant retail commercial properties and who was losing because no money was being made. how are the property taxes being paid?

This is my 3rd time series. And my least reliable. But there seems to be a confluence of inflection points around the end of April. The recent drop-in rates will be reversed in spite of the Treasuries ability to drain its account with the Reserve bank, and in spite of the need to replenish it in August?

Long-term interest rates hover around (1) long-term money flows, which turn up then. And the (2) moving average of long-term money flows also rises at the same point as the (3) 3rd seasonal inflection point, May 5th (my birthday).

https://www.cmegroup.com/markets/interest-rates/us-treasury/30-year-us-treasury-bond.quotes.html

May 4th, is the time to sell short.

May the 4th be with you.

There are 6 seasonal, endogenous, economic inflection points each year.

(they may vary a little from year to year):

Pivot ↓ #1 3rd week in Jan.

Pivot ↑ #2 mid Mar.

Pivot ↓ #3 May 5,

Pivot ↑ #4 mid Jun.

Pivot ↓ #5 July 21,

Pivot ↑ #6 2-3 week in Oct.

All interest rates need to go up relative to the 4-week T-bill. Better to have the choice to do it now, before the second wave of inflation hits. Springtime of 1979…

I see they now plan to sell US gold reserves to buy Bitcoin. Ugh ..

Where did you come up with that nonsensical false notion?

Try a simple search, maybe ‘U.S. may sell Fort Knox gold for Bitcoin’

The crazies have as much chance of getting that passed as some woman in Waterbury confining her stepson to a lockup for two decades. We know that’s not possible in a rational world.

BuySome, I read that article. What a terrible thing to do to the kid. They should lock her up and throw away the key.

I was raised in Waterbury and it’s now turning into a slum as all manufacturing has been shut down or left.

Face the facts when it comes to restaurants, people do not want to cook at home. A lot of people don’t know how to cook a dinner at home. The proliferation of fast food and restaurants in the last 50 years is mind blowing. Probably had a lot to due with more money in peoples pockets due to cheap foreign imports.

wife and I have 130k income and 2.2M in soon to be tapped retirement. No vacations except1 week per year to scout retirement locations. Maybe Chic Filet once per week. Last time I tried my fav cheap authentic Primos Taco I found a thick black hair in my gringas, hoping beard over alternatives. A Gen-X, I fix my own appliances and minor car repairs. Mow my own lawn, spread my own mulch, spray for termites each Spring. We cut our own hair and wife does her own hair dye. Wish I could afford a nice dinner out but I have priorities. Hopefully once retired in TN things will loosen up a bit, if I’m not afraid to spent a little after all this endless saving.

CitiBank increase the 8M CD to 4.35% and also 18M to 4% much better than BOFA or Chase, seems that it going to be in that range for a while.

Why is everyone bashing sailors?

“Drunken Sailors? ”

“Sailors and dogs keep off the grass”

I was once a sailor. I don’t get it.

Swamp creature:

It’s jealousy, pure and simple. Sailors know how to work and they know how to have fun. FYI, jealousy is a sin you know :)

Perhaps both the dogs and sailors have relieved themselves on said grass?

Plus ‘WE drunken sailors’ probably is more correct, given the readers…

Goldie and Wolf:

Another reason CRE foreclosure and property sales not happening is regulators are not pushing banks to clean up. Banks are suffering from unrealized losses and lack of capital to eat both loan losses and securities losses. FDIC fund inadequate to cover. Most importantly, the FDIC does not have the staffing or talent available to close many banks. Regulators are supporting extend and pretend. It’s not pretty out there in CRE land. Zombie borrowers owing too much to zombie banks. There is very little true price discovery. Be careful

Some serious bank problems and a bear market in stocks are in the works for the latter half of this year into 2026. Not sure when the recession hits, but likely not too far behind that. Stay tuned.

“Fitch Ratings became the second of the three major credit-rating firms to remove its coveted triple-A assessment of the United States government’s credit worthiness, a move that spurred debate in Washington about spending and tax policies.

Fitch cited the federal government’s rising debt burden and the political difficulties that the U.S. government has had in addressing spending and tax policies as the principal reasons for reducing its rating from AAA to AA+.”

In July 2023, Fitch ratings changed. Trump’s DOGE is a long time in coming.

If QT is supposed to raise interest rates and make borrowing more expensive (agreed that is the plan), then why has the QT implementation starting in June or 20222 resulted in and increase of about 50% in the SP 500?

In theory, if borrowing is truly more expensive (and we do not have other liquidity, like “printing money”), the QT should have tanked this market.

How can the Fed claim that there is QT here when the results show differently?

You’re not connecting the right dots. QT and rate hikes did cause long-term rates to soar, with mortgage rates more than doubling.

But years of QE left trillions of dollars in excess liquidity sloshing through the markets. QT has removed only $2.2 trillion of it so far. The rest is still out there. But in 2023, QT had just gotten started, and then there was the bank hiccup in March 2023, and in 2024 QT continued. So now finally, ON RRPs have mostly been drained by QT and QT is now going after reserves, and that’s liquidity in the banking system. That’s a different ballgame now.

Wolf, where is your data that supports we are in QT?

See the https://fred.stlouisfed.org/series/NFCI

According to the Federal Reserve of Chicago, “Negative NFCI values: Indicate that financial conditions are looser than average, which would be the opposite of the effect of QT. ”

As you can see from the graph, NFCI has been negative since March 24, 2023.

We are not in QT.

Maybe QT has started again in Jan 2024, not sure yet.

Your comparing apples to Orangutangs. Like whatever.

Here is the data on the $2.2 trillion in QT that you asked for:

https://wolfstreet.com/2025/03/06/fed-balance-sheet-qt-54-billion-in-february-2-21-trillion-from-peak-to-6-76-trillion-lowest-since-may-2020/