QE has produced years of hangover.

By Wolf Richter for WOLF STREET.

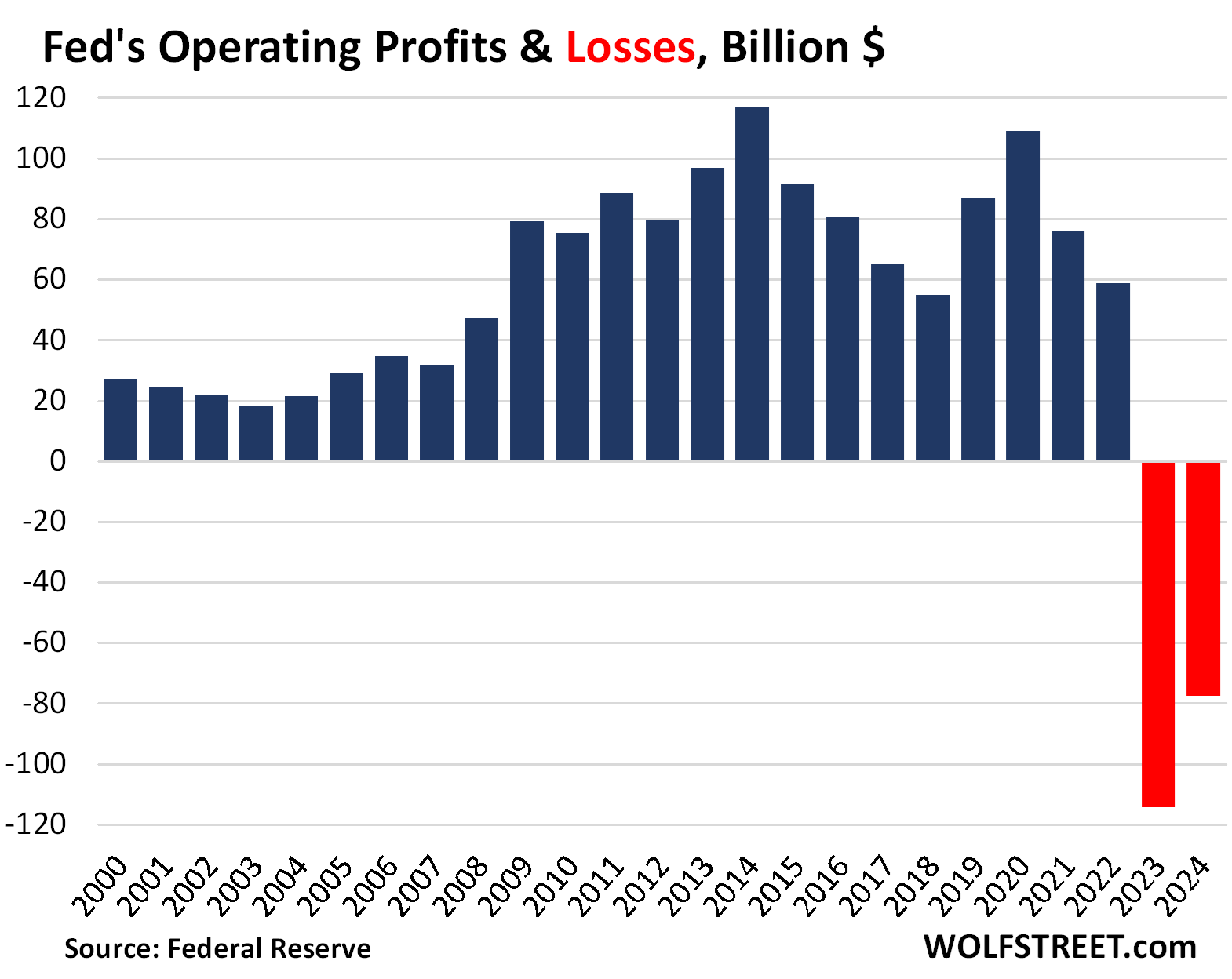

The Fed disclosed two types of losses in its audited annual report today: An operating loss of $77.6 billion for the year 2024, substantially less bad than its operating loss in 2023 of $114 billion. And cumulative “unrealized losses” of $1.06 trillion at the end of 2024, on its holdings of Treasury securities and MBS, up from $948 billion at the end of 2023.

The operating loss of $77.6 billion derived mostly from its interest income being far lower than its interest expenses.

The Fed reported:

- $158.8 billion of interest income from its shrinking portfolio of Treasury securities and MBS, whittled down by $2.2 trillion in QT

- $0.3 billion in other income and losses, including $1.4 billion in losses from “foreign currency translation,” and income from various services it provides to banks and government agencies.

Minus…

- $186.4 billion in interest expense — Interest on Reserve Balances — that it paid banks

- $40.3 billion in interest expense on overnight reverse repos (ON RRPs) that it paid to its counterparties, mostly money market funds.

- $9.9 billion in operating expenses, including:

- $2.7 billion for the Federal Reserve Board of Governors including printing and managing the Federal Reserve Notes (the paper dollars)

- $4.2 billion in salaries

- $663 million in costs of the Consumer Financial Protection Bureau.

Interest rates on reserves and ON RRPs, among the Fed’s five policy rates, started rising in 2022 with the rate hikes. But the dollar amounts got smaller as the Fed shed securities via its QT program: By the end of 2024, ON RRP balances were largely gone, having dropped by over $2 trillion from their peak in 2021, but reserves were roughly unchanged and still over $3 trillion.

In addition, the rate cuts in late 2024 lowered the amounts in interest that the Fed paid on reserves and ON RRPs. Hence the smaller losses in 2024.

On a quarterly basis, the Fed started booking operating losses in Q4 2022.

The “unrealized losses.”

The Fed’s cumulative “unrealized losses” on its holdings of Treasury securities and MBS rose to $1.06 trillion at the end of 2024, from $948 billion at the end of 2023.

The losses got bigger because longer-term yields rose in the final months of 2024, following the Fed’s monster rate cut in September 2024. Higher yields mean lower market prices for longer-term bonds.

These cumulative unrealized losses are the difference between the securities’ amortized cost (which will be equal to face value by the time the security matures) and their market value at the end of the year:

- Securities at amortized cost: $6.75 trillion

- Market value at year-end: $5.69 trillion

- Cumulative unrealized loss: $1.06 trillion.

The Fed bought most of these securities years ago when yields were far lower than at year-end 2024. As yields on Treasury securities and MBS rose starting in 2021, their market values declined.

As Treasury securities get closer to their maturity date, the unrealized losses diminish and become zero when the securities mature because the holder gets paid face value.

MBS are paid back mostly via passthrough principal payments as the underlying mortgages are paid off when the home is sold or refinanced, and as regular mortgage principal payments are made. When the pool of underlying mortgages shrinks enough, the MBS are “called,” and the holder gets paid face value for the remaining balance. It’s unlikely that any of the MBS will still exist by their maturity date; the Fed will get its money back much sooner.

Unrealized losses represent the losses the Fed would have incurred if it had sold all its securities at market prices at the end of 2024.

If the Fed never sells any of these securities, but waits till they mature, at which point it gets paid face value, those unrealized losses vanish without a trace.

The dividend.

Despite the losses, the Fed paid the statutory dividend, as required by the Federal Reserve Act, to the shareholders of the 12 Federal Reserve Banks. The annual report describes the formula laid out in the FRA for how the dividends are calculated.

In 2024, the Fed paid $1.62 billion in dividends (up from $1.48 billion in 2023).

Losses don’t matter to the Fed but matter to the Taxpayer.

The Fed creates its own money and therefore cannot become insolvent. So to the Fed, these losses are just a visual blemish.

But these losses matter to the Treasury Department – and thereby the taxpayer. The Fed has to remit nearly all of its operating income to the Treasury Department (similar to a 100% income tax). Those remittances stopped when the Fed stopped generating operating income in September 2022.

From 2008 through September 2022, the Fed remitted $1.36 trillion to the Treasury Department. At Treasury, these funds became part of the flow of tax receipts.

QE was a huge gravy train for taxpayers, as the Fed loaded up on securities, generating remittances of $1.1 trillion from 2009 through Q3 2022. But the flow of these funds to Treasury stopped with the losses in September 2022.

The losses pile up as a negative liability on the Fed’s balance sheet – the negative amount due the Treasury Department – that keeps getting larger.

As of the balance sheet on Thursday, that negative amount reached -$224 billion, representing the total cumulative operating losses from September 2022 through Wednesday.

The Fed’s operating losses will continue to decline for a while, but as long as it has any operating losses, the cumulative negative amount grows. When the Fed starts generating operating income again, it will go against that negative amount and whittle it down over time. Remittances to Treasury will restart after the negative balance has been reduced to zero, and that account then turns positive. This will take years.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“If the Fed never sells any of these securities, but waits till they mature, at which point it gets paid face value, those unrealized losses vanish without a trace.”

But presumably those losses appear in the year to year P&L as the difference between the rate received on those low interest bonds and the finance cost.

Or is the finance cost just zero because they printed the money to acquire them?

The “unrealized losses” do not appear in the Income Statement (what you called the P&L). They appear in the footnotes of the balance sheet (all banks disclose their unrealized losses in the footnotes).

But the “operating losses” are what the income statement is all about. The “finance cost”… I’m not sure what you mean. But the interest expense that the Fed paid is the biggest expense of the income statement, and I listed it. It’s bigger than the interest income, hence these big “operating losses.”

Late to comment, but I think what Michael Droy is getting at, is that while “unrealized losses” never show up if held to maturity, they are nonetheless real losses to taxpayer in the sense of lost opportunity cost or “missed interest”.

The Fed holds a portfolio of Treasuries on behalf of the taxpayer. And this portfolio currently yields far lower than market rate. So each year the Fed gets less interest income than the market would suggest given the size / duration of the portfolio. This manifests itself in the 158.8B interest income being much lower than market and hence contributes to “operating losses”, though I don’t think they mention it anywhere or attempt to quantify it.

Of course this also works the other direction and hence why the Fed balance sheet has been a tailwind to government funding for decades while interest rates have fallen. Though the “gains” they made on their bond holdings were never realized, the Fed returned higher-than-market interest each year to the taxpayer.

The Fed is an interesting yet confusing entity, thanks for some clarity on the subject.

The line item, “Federal Reserve Earnings,” on the deposit side of the Daily Treasury Statement shows for fiscal year-to-date a deposit of $2.5 billion. Small potatoes, relatively speaking, but after having read the article, I would have thought the above figure would be zero.

https://fiscaldata.treasury.gov/datasets/daily-treasury-statement/operating-cash-balance

It’s amazing how much inflation one can create with stupid, but like they said it’s only transitory.

Good grief! They based that statement on historical similarities and that turned out to be wrong. With 20/20 hindsight we can see why it was wrong but it was a reasonable prediction given the data at the time.

They’ve admitted they were wrong. They’ve explained why they were wrong. They’ve changed their policies because they were wrong.

What more do you want? A crystal ball and a time machine?

Most people I know don’t handle being obviously and painfully wrong nearly so well.

people are upset because it was obvious they were wrong at the time, and no the historical similarities were not in line with those projections, and after they admitted they were wrong, they took a painfully long time to undo their mistakes, and are continuing to do that. meanwhile, they spout platitudes about “keeping an eye on things,” all while seemingly taking every step necessary to ensure that the rich get to keep their ill-gotten gains.

Well said, Franz G.

Maybe the Fed should just reorganize and become the next hot meme stock. Valued at 100x P/S (Interest Income), they could repay the national debt and solve all our problems! :-)

I feel confident in saying that the Fed seriously considered that QE would affect their predictions on inflation but it was new and they had no historical data to follow.

Their “gut” may even have told them of the danger but when you’re managing a country, you follow history and science as best you can anyway. It may not be correct, and wasn’t in this case, but it has a GREATER CHANCE of being correct than a gut feeling.

If you are given so much power and resources then just admitting being wrong and sorry is not enough.

If in my Job I do this then I’d be fired.

Also fed didn’t suffer but the common people still suffering from their stupid mistakes but rich became richer.

Well of course we all know that, statistically, they were correct.

So hitting one’s head against the wall until the facts change is likely too cause an unplanned outcome.

Experts on business channels and regular people like me were saying they should have stopped QE at least three months before they did because it was obvious they were pouring more gas on the fire of a recovered economy. Never will understand why these highly educated folks couldn’t figure that out also…

“Everyone loves an early inflation. The effects at the beginning of inflation are all good. There is steepened money expansion, rising government spending, increased government budget deficits, booming stock markets, and spectacular general prosperity, all in the midst of temporarily stable prices. Everyone benefits, and no one pays. That is the early part of the cycle. In the later inflation, on the other hand, the effects are all bad. The government may steadily increase the money inflation in order to stave off the latter effects, but the latter effects patiently wait. In the terminal inflation, there is faltering prosperity, tightness of money, falling stock markets, rising taxes, still larger government deficits, and still roaring money expansion, now accompanied by soaring prices and an ineffectiveness of all traditional remedies. Everyone pays and no one benefits. That is the full cycle of every inflation.”

— Jens Parsson, Dying of Money

It’s small in comparison to the overall federal deficit and debt, but the postponement of remittances to the U.S. Treasury is reprehensible. It’s an accounting gimmick.

interesting, need to add that to my reading list.

it lines up with what the u.s. experience. some economists have said that the 2016 and on prosperity is really an austrian crack up boom. guess we’ll see in the next 15 years.

The Austrian’s are wrong in their understanding. The FED creates both the boom and the bust.

IE: 2020-2022 Trump opec production cut deal,10%/100Mb cut from the market that caused record high oil and gas prices

So, as I understand it the Fed paid $1.62 billion in dividends to commercial banks while having an operating loss of $78 billion.

So what does this mean from the annual report?

“A member bank is liable for Reserve Bank liabilities up to twice the par value of stock subscribed by it.”

Yeah, the shareholders are on the hook to lose half the par value of their stock holdings in the Federal Reserve Bank of which they hold the shares. But that par value is minuscule because it hasn’t been changed. These are not publicly traded shares. So for example, if you and I hold shares of Misbegotten National Bank, and the bank collapses, your and my loss can be 100% with our shares becoming worthless. But the losses of the FRB shareholders are limited to 50% of par value.

The Federal Reserve exists in a political limbo, its actions neither mandated by the legislative branch nor imposed upon by the executive branch. In the economic sense, its goal is not only to mitigate inflation but to support the continuation of positive economic environments across the U.S., and thereby the world. Considering its importance to global GDP, it would be only reasonable if the other countries of the world had a say in it.

No offense intended, Dark Sport. The second half of your post is highly ironic to me, but that is because I am quite cynical. The idea that the “goal” of the Fed is to mitigate inflation is truly laughable given its performance in over the last seventy years.

–Geezer

Other countries have central banks and if the economies of other countries were as big as the US, those central bank decisions would affect the rest of the world without any input too. In my opinion Japan’s Central bank influence in the world may be a tad exaggerated along the UK’s.

Member banks of the US Federal reserve include some foreign banks if I recall correctly.

AGREE totally with NJGeez on this subject:

The FRB was set up for one and only one reason: TO PROTECT THE BANKSTERS at the expense of workers and savers.

Anyone looking at the vast and ongoing destruction of the value of the USD since the inception of the FRB, now worth approximately 1/33, ONE THIRTYTHIRD of what it was in 1913, and considering any other reason for the continuing existence of the FRB is fully immersed in that river in Africa, ”de Nile.”

Laughably and totally false assertions.

LOL, 1913? My parents hadn’t even been born then. The world has changed. I don’t give a hoot about how much anything cost in 1913. Lots of the things we pay for and benefit from today didn’t even exist back then, from health insurance and airline tickets to modern motor vehicles and this website, or any website. And don’t tell me that life in those good old times of 2013 was somehow better than today because, you know, a haircut cost 50 cents or whatever.

Agree, I also think its wrong how much theyve debased the dollar. It makes our nation look more like one of the dysfunctional countries out there. And the fed has also enabled congress to carelessly drive up the debt on the people to a crushing 36 trillion by “buying” the gov’t debt with money printing. And we don’t know what future problems that debt will bring. The fed should have let that debt face the free market so interest rates would’ve rightfully spiked to attract real buyers. When those rates would hit consumer loans, the business owners who donate to congress and the public would have told them to cool it with the overspending. Devaluing the dollar makes me want to live frugally out of concern about the countrys future.

Dark sport,

The idea that the economic growth here is somehow well intended to help the rest of the world misses what this country has been doing since its founding to build its wealth and power worldwide while benefitting only a fraction of the society it represents. The example are endless with regard to economics and foreign policy. Bring productive forces to countries rather than labor and natural resource extraction would be far more beneficial but far less profitable, which is all it comes down to here.

Actually, they do through the basket of currencies which treasury supplies with dollars to balance the excess money printers, the free riders like Japan.

They do have a “say in it”

They can bonds of other countries & stop buying Treasuries if they get upset enough about it.

I keep on hearing that China & Japan are no longer buying like they used to….to say nothing about Russia & Iran not buying Treasuries.

Here’s who is buying Treasuries:

https://wolfstreet.com/2025/03/18/who-holds-the-ballooning-us-government-debt-even-as-the-fed-and-foreign-holders-unloaded-treasury-securities-in-q4/

The Fed exists to make banks richer. $226.7B in free money just for sitting on reserves or lending them back to the Fed after they piled up all the money from QE. RRP ON are moving back higher.

I can only wonder how soon it will be that the Fed ends QT and then starts buying assets again to keep its balance sheet stable like they did from 2015 – 2018?

T: Temporary

R: Rising

A: Abrupt

N: Notable

S: Short-lived

I: Impulsive

T: Time-bound

O: Occasional

R: Reversible

Y: Yields (as in, yielding to normal levels)

$4.2 Billion in salaries? Losing money for two straight years? The creation of 25 percent cumulative price inflation in just a few years? Unprecedented income and wealth inequality?End the Fed!

100% Agree, they have an army of PHDs to tell them to raise or lower interest rates and start and stop QE/QT

They, with congress have decimated the poor and middle class.

I think they do more harm than good. I am all for abolishing the FED and roll any deputies that are critical into the Treasury.

Well, the Federal Reserve whose primary role is to regulate and ensure the safety of banking was created by an act of Congress and fortunately will be with us for the foreseeable future.

I believe the Fed will cave and immediately drop the FFR at the first sign of financial distress in the domestic economy.

We are in a period of unfounding the Constitution by the Continental enemy, the aristocracy.

I’m thinking that we have a government that a completely disengaged citizenry deserves. We lost interest in the republic is an accurate description of how we got to this point in history.

We have allowed ALL our elected representatives to be sponsored, and aren’t very interested at all in who sponsored them…..much less why.

But we do know who sponsors most all our favorite NASCAR drivers…….it’s on their cars and racing suits.

We probably do act on that collected knowledge, so we aren’t completely disengaged from this country….assuming we are busy learning what to buy.

It’s a form of participation.

Help the US have the strongest economy in the world.

Prevent systemic banking failure and Great Depression 2.0 in 2008 due to shady bank behavior.

Stop economic collapse in 2020 as a result of a global pandemic.

Reduce rampant inflation and keep pressure on to keep heading towards the 2% goal without breaking anything.

Yes… End the Fed.

They’re not perfect, and the inflation problem is largely of their own making due to the previous two actions, but we’re a damned sight better off with them than without them.

The economy before the GD was self-correcting.

Yes, and it self-corrected PAINFULLY. The Fed doesn’t prevent swings in the economy; it smooths it out resulting in less pain. Pain, I’ll note, that was mostly felt by the working classes as the rich had an easier time riding it out.

Brian-

“ …we’re a damned sight better off with them [the Fed] than without them.”

The growing level of Federal debt is largely a byproduct of central bank meddling and price fixing in the U.S. Treasury markets, IMHO.

Hyper-indebtedness will break itself some day — then you might need to rethink your analysis.

The federal debt is 100% caused by the US Congress and nobody else whatsoever is to blame for that intractable problem.

SoCalBeachDude,

Then by extension, American voters are 100% responsible.

SCBD-

“The government has been trying to push down, talk down, swat down, and wish down long-term Treasury yields to make funding in the economy for businesses and households less costly – the stated policy of Treasury Secretary Scott Bessent.”

— Wolf Richter, ”Yield Curve Re-inverts….”

So, besides free-spending congressman, the U.S. Treasury stimulates economic growth via lower rates. The connection of rate fixing to debt expansion is obvious.

Same argument for Fed rate cutting to fulfill its max employment mandate.

Everyone’s in the debt expansion act. When it comes to real systemic debt growth, it appears to “take a village.”

THIS!

So true. Blue collar worker here. So grateful to have the fed even out the panics and depressions.

The idea of a central bank is a good one.

The problem however is that once you concentrate power, you also invite misuse. The Fed was supposed to intervene in bank crisis….and now has become the driver of the economy. Nearly everything hinges on the speech a bureaucrat delivers once every month. How smart is Powell that we have given him such control of our lives….is he deserving?

The important question to ask is why do we believe the Fed can introduce prosperity? Are interest rates and money supply the only two things that matter?

I like the idea of a Fed as Bagehot defined….to provide liquidity in crisis against good collateral. And I want a Fed that provides no guidance. No open mouth operations from the Fed….that would be a good start

Congress could have stopped the Fed from perpetrating QE. Congress can limit — and has limited — what the Fed is allowed to do. It could have passed legislation that prohibits the Fed from buying securities, directly or indirectly, including lending to outfits, such as SPVs, that buy securities. Congress has never done that. Congress has been fully on board with QE, no matter who is control of Congress. However, Congress has barred the Fed from buying stocks.

“…at $275K a pop, those speeches must have been Shakespearean!….Surely you would want to at least share some of the highlights!”

4.2b is 4,200 million, right? How many employees do they have?!

What’s your problem???? The number of employees at the Federal Reserve System (ca. 23,000) is MINUSCULE compared to Walmart (2.1 million).

23,000 employees — so salary costs come out to be $185,000 per employee. That’s probably low for a highly educated workforce.

My apologies for a hurried, knee jerk post. After I posted I did some googling and found that they had around 24,000 employees in 2023. I had no idea their workforce and scope was so large. I was thinking they maybe had 1,000 or so.

$4.2B / 24K employees gives an average salary of $175K.

Look like DOGE needs to get in there and clean up.

$4.2 billion in salaries? What is the context for such a high number?

It’s really not that high for a large organization. That could be roughly 20,000 to 40,000 people depending on average compensation–$100,000 to $200,000, respectively. Presumably, the number includes retirement benefits and healthcare, so a lot of people at the equivalent of a federal GS-14 at a high step with locality pay would run up to $200K easily.

Remember, the Fed isn’t just a dozen people in a room deciding the interest rate. They are a federal regulator for a wide variety of banks and bank holding companies (which means doing lots of institution-specific examinations), they run payment clearing systems, etc. The monetary policy side also generates a lot of research papers and statistics.

Klaus Kastner

There are 12 regional Federal Reserve Banks plus the Federal Reserve Board of Governors. These are huge financial and regulatory institutions that do a lot of stuff that you just don’t know about, from regulating all federally charted banks to managing our physical currency.

Are older MBS commonly called when market value is below par? In that situation who eats the loss? Will the rise in interest rates mean that fewer MBS will be called than has historically been the case?

1. No

2. If MBS are called, they’re called at FACE value, not at market value, and there are no losses involved. The Fed and other holders will get their money back if they bought at issuance.

3. Yes, but mortgage payoffs continue, just at a slower pace than during 2020-2022. There are fewer refis, and fewer sales that entail a mortgage payoff, but there are still some refis, and people still sell homes and their mortgage gets paid off, and people still make mortgage payments. So the process is still moving forward, but at a s lower pace.

In follow up to number 2, if MBS are called when market value is below par and then the underlying mortgages are repackaged into a new MBS which would be sold at market value, wouldn’t there be a loss on the part of the MBS issuer to offelset the windfall received by the MBS holder because of the call?

1. There are no losses involved. The underlying mortgages are not traded. The GSEs never sell them. Any mortgage that is paid off, is paid off at the remaining balance, not market value. There is no market value for these mortgages.

2. By the time the MBS get called, for example after 10 years, the remaining 30-year mortgages in that pool now have a 20-year remaining lifespan, and the principal has been reduced by 10 years of principal payments, and it’s that remaining principal that goes into the new pool.

3. The yield at which the new MBS that contains a few older mortgages will be sold is slightly impacted by the older mortgages (up or down), but this is always the case, and these government-backed MBS yield substantially more than Treasury securities, which is why investors find them attractive, despite the hassles of the unpredictable pass-through principal payments and call feature.

If the MBS with rights to receive pass thru mortgage payments with a market value of 90 (because of a rise on interest rates) are called at 100 but are then repackaged and sold at 90 someone is taking a loss.

Which indicates to me that MBS backed by low rate mortgages may be less likely to be called in the future as compared to historical practice.

No, please re-read my comment, but carefully this time.

It’s like Dr. Philip George rediscovered. It’s stock vs. flow. As Dr. Philip George says; ““When interest rates go up, flows into savings and time deposits increase” ( the ratio of M1 to the sum of 12 months savings ).

This results in a double-bind for the Fed (FOMC schizophrenia: Do I stop because inflation is increasing? Or do I go because R-gDp is falling?). If it pursues a rather restrictive monetary policy, e.g., QT, interest rates tend to rise.

This places a damper on the creation of new money but, paradoxically drives existing money (savings) out of circulation into frozen deposits (un-used and un-spent, lost to both consumption and investment). In a twinkling, the economy begins to suffer.

But C-19 is different. There has been a “flight to liquidity” according to Shadow Stats. This will circumvent a recession.

First off I just want to say this is a great article and I wanted to say thank you for all you do!! I have been reading your stuff for about a year now and will continue to do so!

I’m curious of what your opinion is on how the Fed has and is handling things. In my opinion society puts too much blame on the Fed for Inflation and economic conditions. Yes they play a factor in it but isn’t the real root cause for all this a combination of the Financial crisis and Covid? I mean if we hadn’t shut down the US economy during Covid we wouldn’t have needed all the stimulus. Everyone loved those stimulus checks and being paid to sit at home but where did they think that money was coming from and that it wouldn’t be painful to pay it back. Plus we are still feeling the ramifications from the financial crisis. Realtors knew long before 2020 that inventory levels were headed into a massive shortage. Most of the builders went under after the crisis and we have not been building an adequate amount of new housing ever since. The housing inflation was inevitable, it was just exposed when we had those historic low rates in 2020-2021.

The Fed has a tough job in my opinion. They have to clean up all the messes we make. We show them gratitude by blaiming them. Could they have done things slightly different, yes but so far they have brought down inflation, we haven’t had a recession yet, the job market is still healthy.

Hell do they have anything to do with the price of eggs? Do they impose tariffs? Did they create mortgage backed securities that required no down payment with no verification of income, assets or employment for people with 620 credit scores?

Andrew:

Totally agree! Thank god for the FED!

Their primary job is to clean up the messes created by irresponsible administrations and even more irresponsible congressmen. It is a hard job and frankly a thankless job.

You are right to highlight that the government has played it fast and loose for too long. However this behavior wouldn’t have been possible with the Fed’s support.

By buying long dated treasury securities, the Fed encouraged over spending and more issuance by the government. These distortions over 15 years has likely reoriented the economy. It responds to where the demand is. It is not going to be smooth to get off the public teat.

“Slowing further or stopping redemptions of securities holdings will be appropriate as we get closer to an ample level of reserves. But in my view we are not there yet because reserve balances stand at over $3 trillion and this level is abundant,” Waller said

“There is no evidence from money market indicators or my outreach conversations that the banking system is getting close to an ample level of reserves,” Waller said.

And he’s right.

This comment could have been under all the dot plot stuff.

Someone from another country reading about the vote of these private banks might think the Fed consisted or was composed of them. And that when an emergency like GFC or covid occurred, they all chipped in. They don’t and the Fed is a separate creature. Only it can create money.

Of course their input is sought. The Bank of Canada confers with the Big Six but there is no vote by them on BoC action. Same with BoE.

A casual observer might think the GFC crisis was resolved the same way JP Morgan resolved the crisis of 1907, when he locked the finance CEO’s into his library until they agreed on a bailout.

Wolf,

I am struggling to understand how MBS get called early at face value. Who is providing face value money for mortgages that are now worth far less given current mortgage rates?

“Who is providing face value money for mortgages”

1. The underlying mortgages. They’re not traded. The GSEs never sell them. Any mortgage that is paid off, is paid off at the remaining balance, not market value. There is no market value for these mortgages. And there are no losses involved for anyone.

2. Separately, defunct mortgages get pulled out of the pool at the remaining principal balance, not market value, just like paid-off mortgages. If a mortgage goes bad and leads to foreclosure, the GSEs take the losses of that mortgages.

3. call features are never at market value. Bonds are contracts with specific terms. For bonds that are callable, such as MBS, the terms include the details of the call features.

Wolf,

It is those callable bonds/MBS that I am struggling to understand. Your write “When the pool of underlying mortgages shrinks enough, the MBS are “called,” and the holder gets paid face value for the remaining balance.”

Is that call automatic (specific in the terms), when the remaining mortgages drop to a certain value? Or is it a decision (“callABLE”) made by the issuer? Why would any issuer exercise that right, if it means they must hand over face value on mortgages worth far less on the market?

It’s a decision by the issuer.

In terms of your second question, re-read #1. it gives you the answer.

The reason for calling them is that the pool of underlying mortgages shrinks so much (average 30-year mortgage is paid off within 7 years AT FACE VALUE = remaining principal) that it’s more economical to call the MBS and spread the remaining mortgages into new pools, than maintaining the MBS

Wolf,

Why is the Fed now paying interest on bank reserves, reverse repos, and money market funds deposited at the Fed?

Thank you.

The Fed has five policy rates that are designed to lock in short-term rates in the money markets. It’s called “rate control.” For example, the EFFR has been very steady since it started doing that. Before then, the EFFR would bounce up and down a lot. The rate on ON RRPs provides a floor for those rates, the rate on reserves and the discount window rate provide a ceiling.

@Wolf

Do we know the contents (or a general breakdown of these) of the MBS portfolio, i.e., is there any CRE therein?

The Fed holds $8 billion in multifamily CMBS that are guaranteed by Fannie Mae (taxpayer), so-called “agency CMBS.” That’s the only CRE in the Fed’s portfolio.