More people, more workers, higher incomes, more spending. Banks eager to lend at high rates and collect swipe fees.

By Wolf Richter for WOLF STREET.

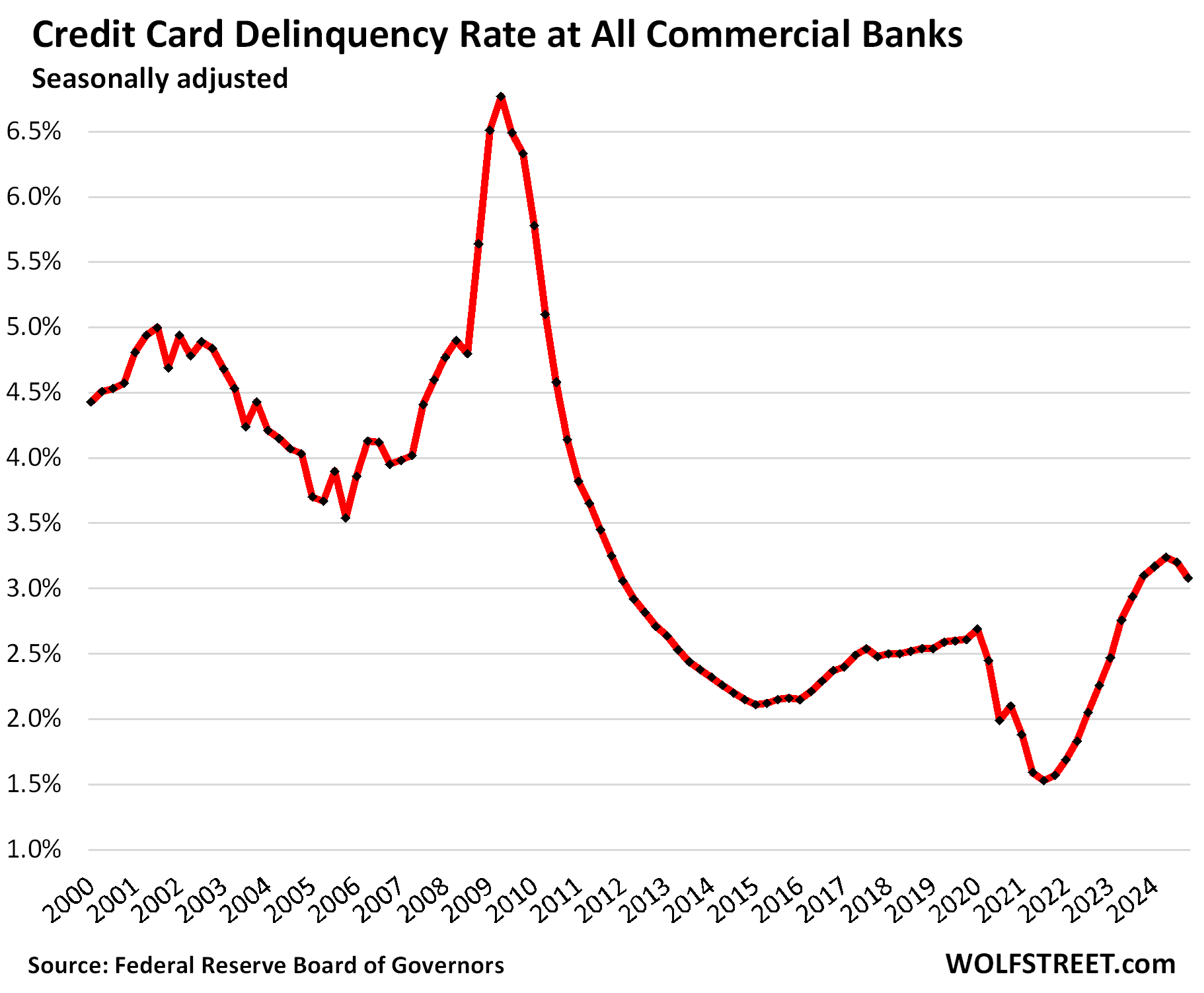

Delinquency rates for credit cards 30 days or more past due declined for the second quarter in a row, to 3.08% of total credit-card balances at all commercial banks at the end of Q4, seasonally adjusted, according to Federal Reserve data on yesterday. This includes credit cards issued to prime and subprime-rates borrowers.

The plunge in delinquencies during the pandemic was a result of Free Money flooding households which helped some folks get caught up; and it was also driven in part by limited options of spending, with restaurants, flights, cruises, entertainment venues, etc. being largely shut down.

Then the spending boom took off, the Free Money ended, and delinquency rates normalized, then overshot a little. The high point was in Q2 last year (3.24%), and the delinquency rate has dropped since then:

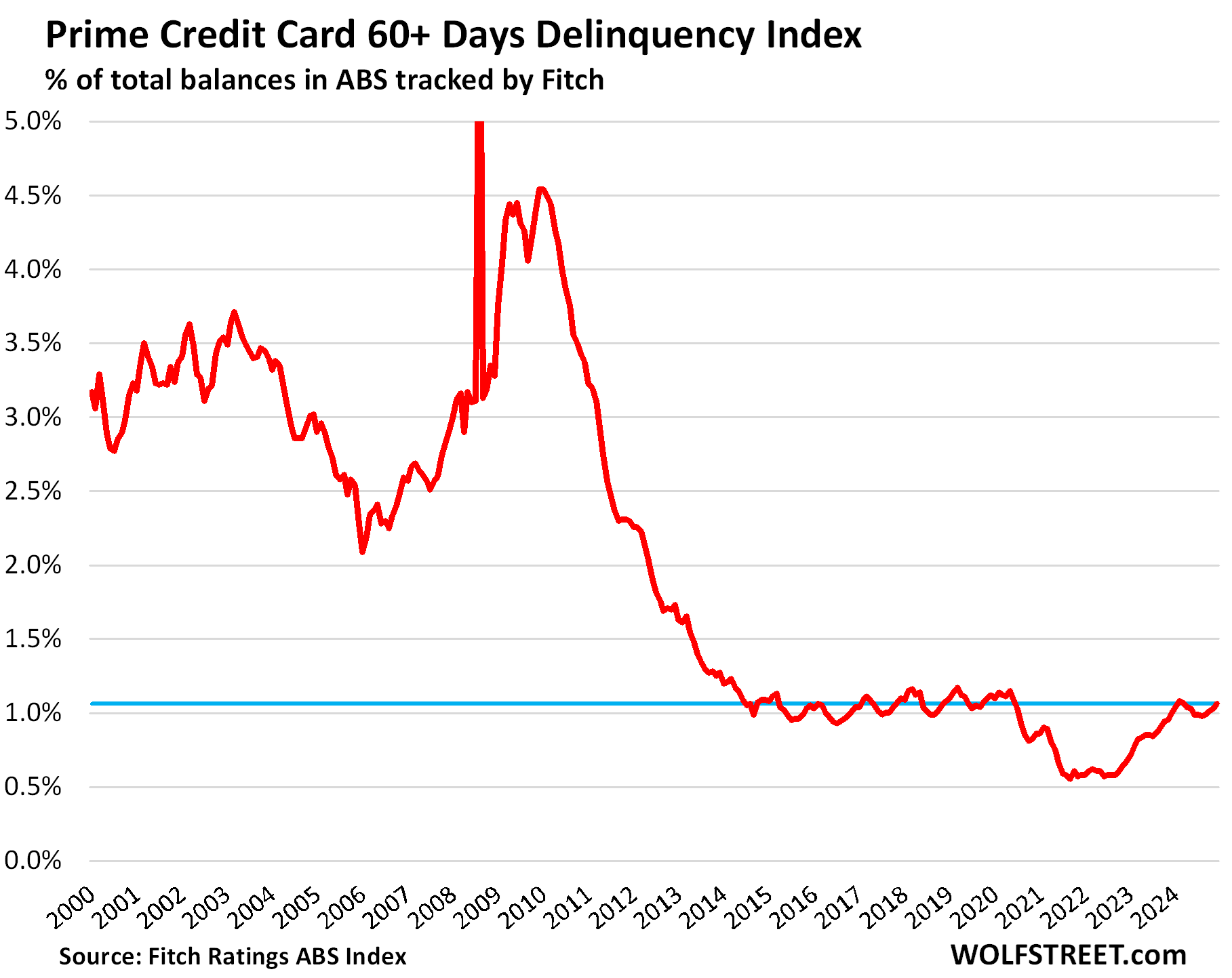

For prime-rated cardholders, delinquencies of 60-plus days have hovered at around 1%, sometimes a little under sometimes a little over, not seasonally adjusted, right where they had been before the pandemic, according to data from Fitch Ratings, which tracks the performance of Asset Backed Securities (ABS) backed by prime credit card balances.

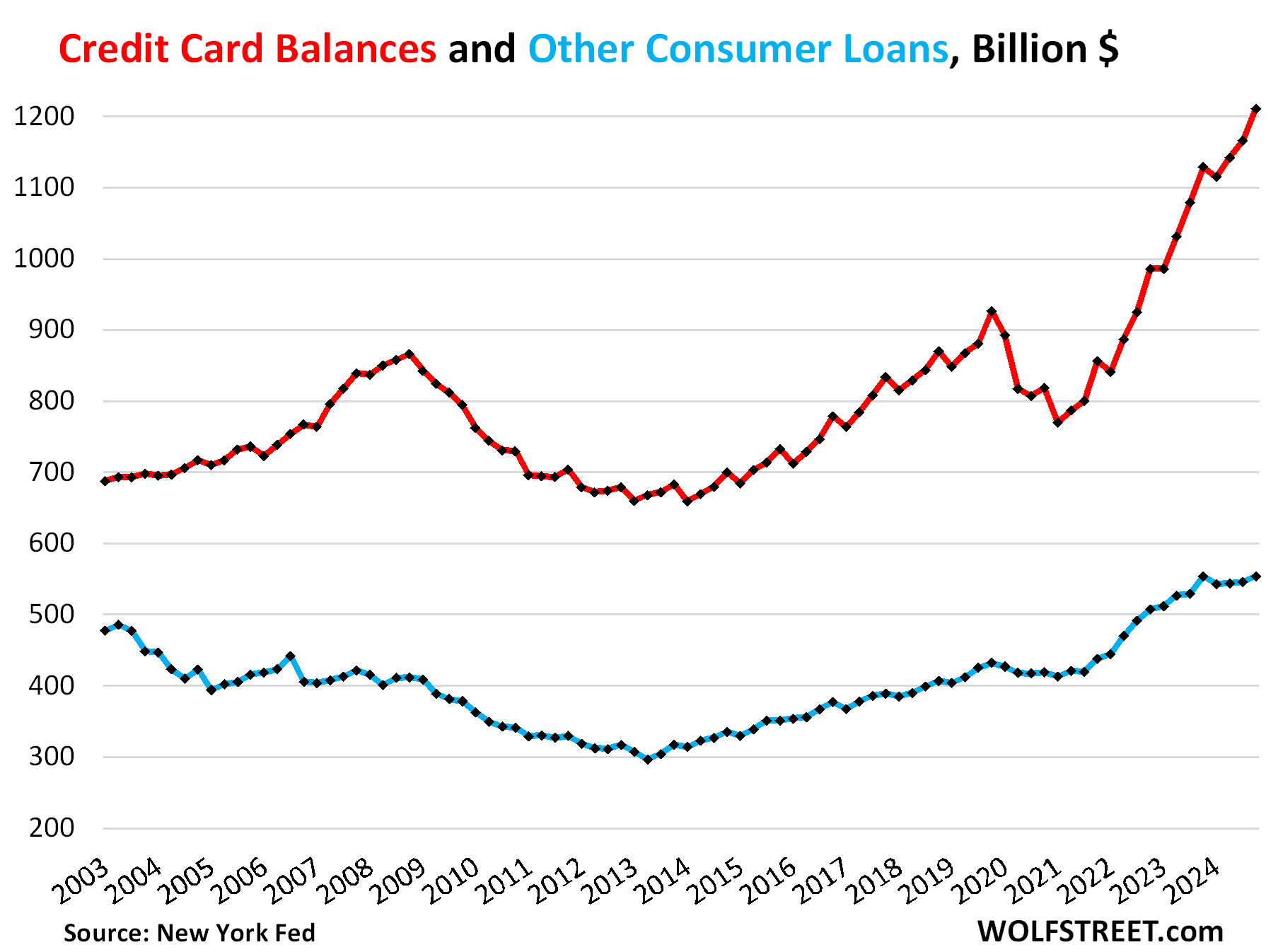

Credit Card Balances are a measure of spending, not of debt.

Credit cards are the dominant payment system in the US, and credit card statement balances therefore are a measure of spending – including for expensive business trips that are reimbursed.

They’re not a measure of borrowing because most balances are paid off by due date and never accrue interest, but allow cardholders to get their 1% or 2% cashback, airmiles, and other loyalty benefits.

Of the roughly $6 trillion a year that flow through credit cards, only a small portion doesn’t get paid off every month by due date. Credit card balances that are “revolving” – meaning becoming an interest-bearing loan – amounted to $645 billion at the end of Q3, according to the Philadelphia Fed’s report in January. Big-ticket items, such as furniture to equip the new house, are a common example of balances getting run up that then get paid off over the next few months.

Lower-income people rarely have access to credit cards, and usually have to make do with debit cards, or if they have access to credit, the credit limits are low. So in aggregate, they cannot run up the revolving balances; it’s the young high-income dentist with five credit cards, each with a $30,000 credit limit, that can put a dent into those balances.

More people, more workers, making more, spending more.

Credit card statement balances rose by $45 billion, or 3.9%, at the end of Q4, not seasonally adjusted, to $1.21 trillion, according to the NY Fed’s Household Debt and Credit Report, after blockbuster holiday spending by our Drunken Sailors, as we’ve come to call them lovingly and facetiously. Year-over-year, statement balances were up 7.3% — more people, more workers, making more money, and spending more.

“Other” consumer loans, such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans remained unchanged year-over-year, at $554 billion (blue line).

BNPLs are subsidized by the merchant and are interest-free for the consumer, if they stick to the plan. Merchants like them because the fees can be lower than credit card swipe fees.

Combined, credit card balances and “other” consumer loans rose by 3.1% in Q4 from Q3 and by 4.9% year-over-year, to $1.76 trillion.

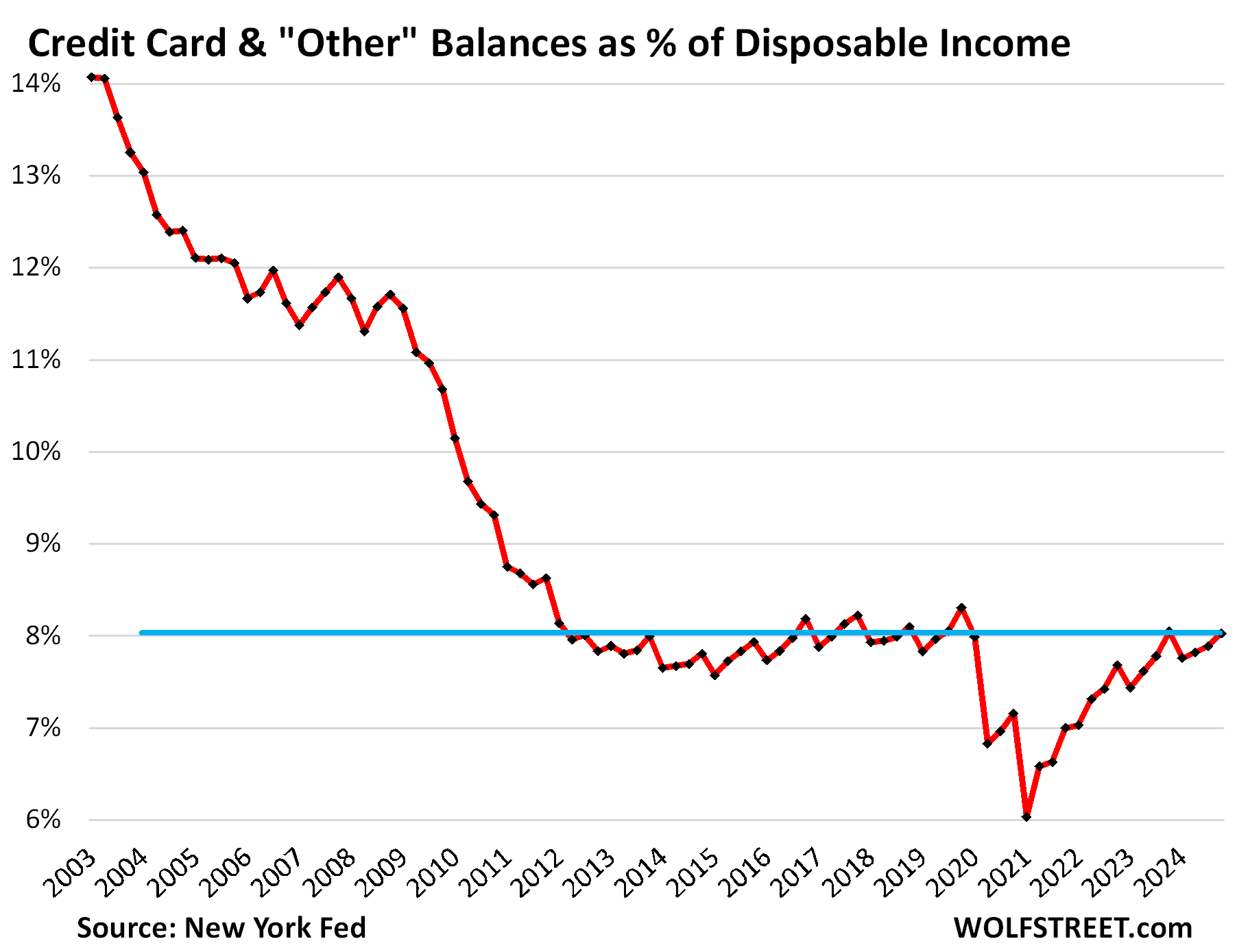

The credit-balance-to-income ratio.

The burden of debt on households – accounting for more people, higher employment, and higher incomes – can be tracked with the debt-to-disposable-income ratio, a classic measure of the borrowers’ ability to deal with the burden of debt.

Over the past 20 years, disposable income has surged by 144%, a result of higher employment with workers making more money on average, while balances of credit cards and “other” consumer loans combined has risen by only 58%.

Disposable income, released by the Bureau of Economic Analysis, represents an after-payroll-tax cashflow from all income sources: Household income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc. This is the cash consumers have available every month to spend on housing, food, debt payments, etc. But it excludes capital gains.

In Q4, driven by holiday spending, statement balances are always higher, and then they dip in Q1 as spending sags, seasonally. These balances are not seasonally adjusted:

- In Q4 from Q3: credit balances +3.1%, disposable income +1.3%.

- Year-over-year: credit balances +4.9%, disposable income +5.1%.

As a result, the burden of the combined credit card balances and “other” balances, in terms of the debt-to-disposable-income ratio, increased quarter to quarter due to the seasonal spending burst, but declined year-over-year, and is very low by historical standards, as our Drunken Sailors have learned a lesson coming out of the Great Recession.

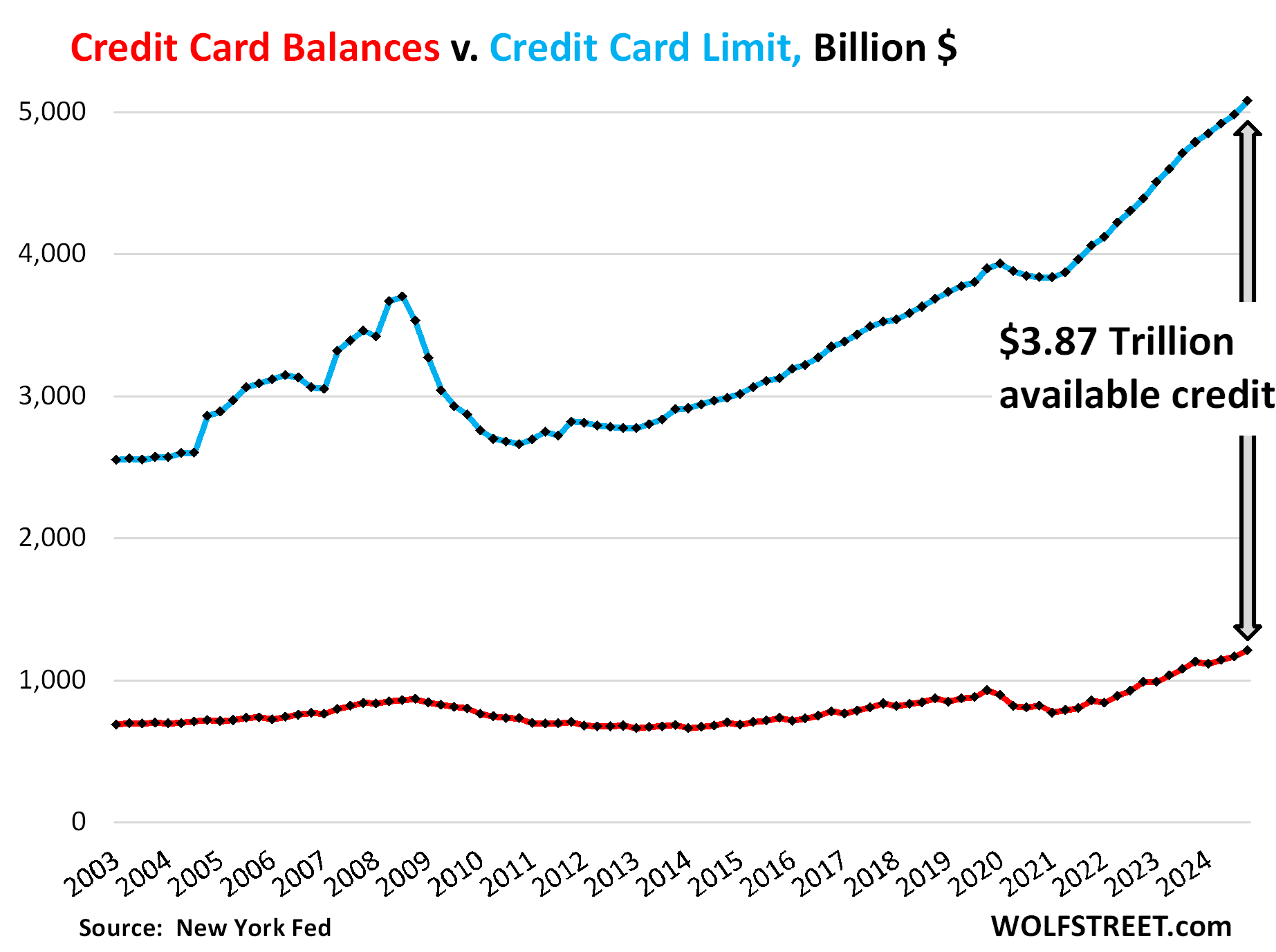

Banks eager to lend at high rates and earn swipe fees.

The aggregate credit limit rose by $269 billion year-over-year, to $5.08 trillion, as more card accounts were opened by more workers, and as credit limits were raised on existing cards (blue line).

Over the same period, credit card statement balances rose by $87 billion, to $1.21 trillion (red line)

And the available unused credit surged by $182 billion year-over-year, to a record $3.87 trillion. Following the Financial Crisis, credit tightened as banks were skittish, and available credit plunged by $1 trillion:

In case you missed the earlier parts of the debts of our Drunken Sailors and their debts in Q4:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Although only a tiny portion of the total, it would be interesting to see the history of revolving balances. Does that tell us anything about the state of the economy? Also, the average cc interest rate vs the prime rate. I’ve always thought of cc companies as a bit like drug pushers. “Here, use this card at 0% interest for the next six months”, then we’ve got you hooked for 20+% until you can pay it off . . .

Revolving balances underly the same principle: more people, more workers, higher wages, and the results will be roughly the same: the burden was very high before the Financial Crisis and is now low.

my wife and I are looking to upgrade our RV and so we went to RV event at local fairgrounds

guy wasn’t pushy per se, but he kept going back to taking out 10-15 year loan at 7-9%

I don’t even want that for income producing property

of course always willing to be one receiving said income

Those rates make an RV even more expensive. The pandemic RV boom is over, and it seems like you should be able to find some deals.

Wolf’s site was out of commission for the last 3 days

LOL, no it was not.

Have you run into difficulties accessing the site or getting your emails?

There was a glitch I’ve never seen before with the site. Something like URL not available when trying to get in via the e-mail link. Everything else worked on my PC at the time. Now the site is working OK.

I just posted an article about this. This is “Kink #2” — after having changed email service. Please read this, it shows you how to deal with the issue (Kink #1 is not an issue for you since you’re getting the new emails):

https://wolfstreet.com/2025/02/20/dear-wolf-street-email-subscribers-i-changed-the-email-service-provider-and-some-readers-have-run-into-some-kinks/

Wolf – received ‘url not found’ msg. when trying to read yesterday’s, and prior posts on my longtime Yahoo email. Resubscribed, and here we are today in a slightly-different format)…best.

may we all find a better day.

I just posted this. Pease read this, it shows you how to deal with the issue.

https://wolfstreet.com/2025/02/20/dear-wolf-street-email-subscribers-i-changed-the-email-service-provider-and-some-readers-have-run-into-some-kinks/

Just put wolfstreet.com in your browser favorites. But I guess maybe accessing the site through their email is how people get notice of new articles and correspond for comments.

Is it safe to assume the delinquency here is the group of card holders who didn’t pay anything and missed their due dates? Do you also have the numbers for people who just pay the minimum interest? I think that would give us a more complete picture.

I have love/hate relationship with cc

last week paid $10k on cc

next day had $2k balance already

———–

if so many consumers are late/delinquent then why do we not see ‘deals’ out there

talked with realtor friend – said Tucson had 2,500 new listings in Jan and 985 closed deals(pending is not your friend)

lots of realtors are taking listings off market for 30 days(to show new/fresh)

and then relisting

seeing lots of ‘stale’ listings were virtually now showings taking place

focus now on summer vacay – gonna be 110 soon enough

Wolf you missed a word: “that can [put] a dent into those balances”

“ result of Free Money flooding households,”

Which is the DOGE/ Musk/ Trump strategy again?

The jawbone mill churned out the possibility of doling out all the “savings” from the gained de-fficiency.

I was aghast at the direct deposit of the pandemic. Moreso at the 3P-Oh, “loans” and other myriad free money/ fraud enabling schemes enacted at the time.

I had assumed my kids would be paying for it, but the rooster came back the very next year (or so).

I can only imagine that the administration who was in charge at that time was far more reckless than the current one.

Also, I see almost no chance (or reason) of any more free money programs… but I am usually wrong on future predictions!

I suspect this is another teaser, like all the vaporware announcements by Musk/Trump over the last 10+ years. The contingency of the numbers and dates is telling.

My more paranoid self says this is a precursor to a cash buyout to be offered to subprime Americans — a trade of their patrimony (such as future SSI/Medicare claims) for a few bucks. up front. Biggest rug-pull since the USSR did something like this, early ’90s. This would mirror the layoffs-consciousness flooding Washington.

Everybody is hanging on a few toss-off remarks from Elon/Don. reading more mysterious prophecy into it than the old decodings of Beatles songs.

Audio of Pink Floyd Dark Side Of The Moon with video of The Wizard Of Oz.

Make sure to start DSOM right when the MGM lion roars in Wizard of Oz for proper allignment.

“I can only imagine that the administration who was in charge at that time was far more reckless than the current one.”

You mean the administration whose biggest concern was putting the name Donald Trump on the checks? After downplaying the pandemic making it exponentially worse than it had to be? That administration was pretty reckless but this one seems more corrupt.

Both R and D administrations did enormous money printing and rate suppressing operations (the deceptively named CARES Act under Trump and American Rescue Act under Biden) so theyre both extremely reckless and now we have the same R admin back again so I wouldnt put any foolish action past them. To suggest another stimulus shows they are just as socialist as the D party and dont give a cr@p about inflation and it could be a scheme to cause the inflation they actually want. They could claim its not their fault, and it was the people that wanted it. That would be BS. Musk and Trump are the ones who suggested the insanity and real leaders do whats best for their people and any savings should go to lower the deficit.

Call me an optimist (shocker), but what I see in the data is people starting to put their credit cards away and/or irresponsible people cannot access credit as easily. However, looking at the aggregate credit limit, the banks really want the people with good credit to go hog wild! That chart is just insane. Tell me again how these are not predatory institutions?

LOL!

DM: Forever Gone – Popular fashion chain closing 200 stores in second bankruptcy… ANOTHER victim of Temu

A fashion retailer – which was once a fixture in every mall across America – is to close 200 more stores as it prepares for second bankruptcy in five years. Shoppers will be able to get clearance deals as stores sell off clothes cheaply.

Thank you Wolf for the interesting information!

I am solidly in the middle class.

My credit card usage has gone up significantly over the last 5 years. Credit cards have replaced cash and checks for as much as I can. I don’t buy more things so I don’t think I’m drunken sailor, but my overall spending has gone up with inflation. As you noted, many pay off their cards every month.

My rational for using a credit card is:

1) More businesses take credit cards. Even some utilities take credit cards now without an extra fee vs cash. My favorite food truck ONLY takes credit or debit. Having a card is much more convenient and my back feels better not having a wad of cash in my wallet.

I don’t have to carry a checkbook.

2) Credit cards give 1%-6% cash back. Why pass on free money?

3) My bank account pays 4+% and I am effectively floating all of my expenses monthly making that extra interest. More free money.

4) I get an itemized statement of all of my expenses at the end of the month so I can easily track if I am spending more than I should. I pay it off every month.

5) I buy more online where a credit card is required.

6) I have a great credit score if I ever need it.

I still carry some cash for the rare places that don’t take credit or if the business charges 5+% to use a card.

I can understand why credit balances are growing. Inflation is making the monthly totals grow. Cash back takes the edge off of inflation.

I am still buying the same things I was 5 years ago but both balances and cash back are higher.

Sadly, I cannot pay my mortgage with a credit card. That would be an interesting to get cash back and float the payment every month. My effective mortgage interest rate would be less and I would become a King of leveraging.

I can pay my insurance with a credit card now. That helps.

Yeah, but insurance companies just hide that in their rates. They have to. They are in business to make money. Ain’t no free lunch.

True but there’s no discount for paying by check/ACH – so might as well just use your card and get the points.

There are services that let you do it, but they charge a larger fee than what you’d get in points, so there’s no arbitrage opportunity.

I just wish I could pay my property taxes online at all without incurring a fee – my city even charges extra for an ACH bank transfer because they still think it’s the 90s.

But nearly every other bill I have to pay (other than mtg) is payable by credit card with no extra fee.

ShortTLT, Exactly!

Property tax, income tax, and the DMV charge too much to use credit.

I did run into a moral dilemma yesterday when I purchased my yearly Girl Scout cookies with a credit card. I don’t think the Girl Scouts make any less for using credit.

A cashless society is close to reality.

In all fairness, some businesses are strting to charge a fee for credit. I used my actual debit card for the first time in forever while xmas shopping at a couple places this past season – no fee for debit which makes sense.

I just don’t understand why they surcharge for bank transfers when getting a check is the EXACT SAME THING – they’re just getting the account & routing numbers off the check and then running an ACH debit.

Seems like the city either wants to encourage residents to mail a check (why?) or they’re just trying to make extra $$ off folks who don’t know any better.

I don’t use credit cards unless I have to. Any business that doesn’t take cash earns a top placement on my boycott list. When I shop on-line I use a store bought $500 debit card to avoid compromise. Using credit cards lulls you into spending more money, and screws up budgeting. When you pay by cash and run out of money then it’s time for you to cut back on spending. I do use credit cards for periodic billing only like Internet, ADT security, Sears appliance warrantee, Heating & Air service contract etc. I just destroyed my Wells Fargo Visa card and celebrated.

Hope you don’t have plans to visit Fenway park in Boston. Cash is literally useless there – might as well be toilet paper.

So be it. I don’t need them, they need customers. Once plastic is the only medium/means of exchange, we’ll all rue the day.

I’m with you. I have returned to using checks and cash if at all possible.

“Sears appliance warranty” just aged you and gave us the likely generational reason that you have for how you feel about various methods of payment. Not everyone has trouble budgeting by paying with cards. In a similar way as you mentioned with cash, you can easily look at your credit card balance anytime and compare it to your bank balance to see if you should be done spending.

Got a question: the NY Fed puts out a quarterly report that reports 90+ day delinquency rates across different categories. Credit Cards are consistently tracking materially higher there than what you’re showing. Maybe it’s the “Commercial Bank” difference, but I can’t tell. The 90+ day delinquency they show is 11.4% as of Q4, well above the 60-day you’re showing above.

No, no, no, the NY Fed does not put out “delinquency rates,” (=level at a point in time) except for mortgages. What it puts out is its own invention that it calls “TRANSITION INTO DELINQUENCY.” This is an ANNUAL FLOW into delinquency (not a level) without considering those that are leaving delinquency. It’s the most misquoted number ever because these journalists and bloggers are too lazy to look it up and just want to create clickbait.

I discussed this in detail here:

https://wolfstreet.com/2024/08/09/credit-card-delinquency-rates-drop-for-4th-month-despite-confused-reporting-on-the-ny-feds-transition-into-delinquency-rates/

Pretty sure you’re mistaken. I downloaded the data to follow the breadcrumbs and what you’re saying doesn’t match the data itself.

If you look at the data (page 12 data) the 11.35% is reported as percent of balance 90+ days delinquent. Page 13 data shows the newly delinquent by loan type (CCs at 8.96% here). Newly serious delinquent (i.e. transition into >90 days) on page 14 data = 7.18%. This 7.18% also matches the data on tab 27 (if you look at column H, row 103, there’s the 7.18%) under the “Transition into Serious Delinquency”.

Also, you can call things clickbait as you wish, or lazy, but that isn’t penciling out upon further inspection.

I thought you asked an honest question. Instead you engage in spreading BS you picked up from morons on the internet.

Go to the NY Fed “data dictionary” for the household credit data:

https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/data_dictionary_HHDC.pdf

Scroll down to where is says:

“New (seriously) delinquent balances and transition rates. New (seriously) delinquent balance reported in each loan category. For mortgages, this is based on the balance of each account at the time it enters (serious) delinquency, while for other loan types it is based on the net increase in the aggregate (seriously) delinquent balance for all accounts of that loan type belonging to an individual. Transition rates. The transition rate is the new (seriously) delinquent balance, expressed as a percent of the previous quarter’s balance that was not (seriously) delinquent.“

Then go to the actual report from the NY Fed in PDF format that shows the charts:

https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2024Q4

Then go down to page 14 in the PDF (page 17 in the browser), where it shows the chart of the data you referred to, and what is the title of that chart??? Transition into Serious Delinquency (90+) by Loan Type

There are many “Transition rate” charts in this document. These are NOT delinquency rates (level), but annualized flows into delinquency that ignore that outflow, as I explained. I don’t know why the NY Fed still releases this stuff since much of the media keeps misreporting it.

Since I bashed this reporting a few months ago, the WSJ and CNBC have corrected their reporting on it and now correctly call these rates “transition rates” not “delinquency rates.”

The websites where you picked up this BS are run by clickbait conveying ignorant morons. Fine with me, but don’t drag this BS into here.