Inflation has been going in the wrong direction relentlessly month-to-month since June.

By Wolf Richter for WOLF STREET.

Inflation dished out another bad surprise with a big increase in January from December, which wasn’t a surprise because inflation, once it gets going, is known to do that. This time, the hot spots were durable goods, fueled by the continued massive month-to-month increases in used vehicle prices, and non-housing services, such as auto insurance, admissions, subscriptions, etc. Food and energy prices also jumped in January. Rent inflation accelerated. But at least the CPI for apparel and shoes dropped in January.

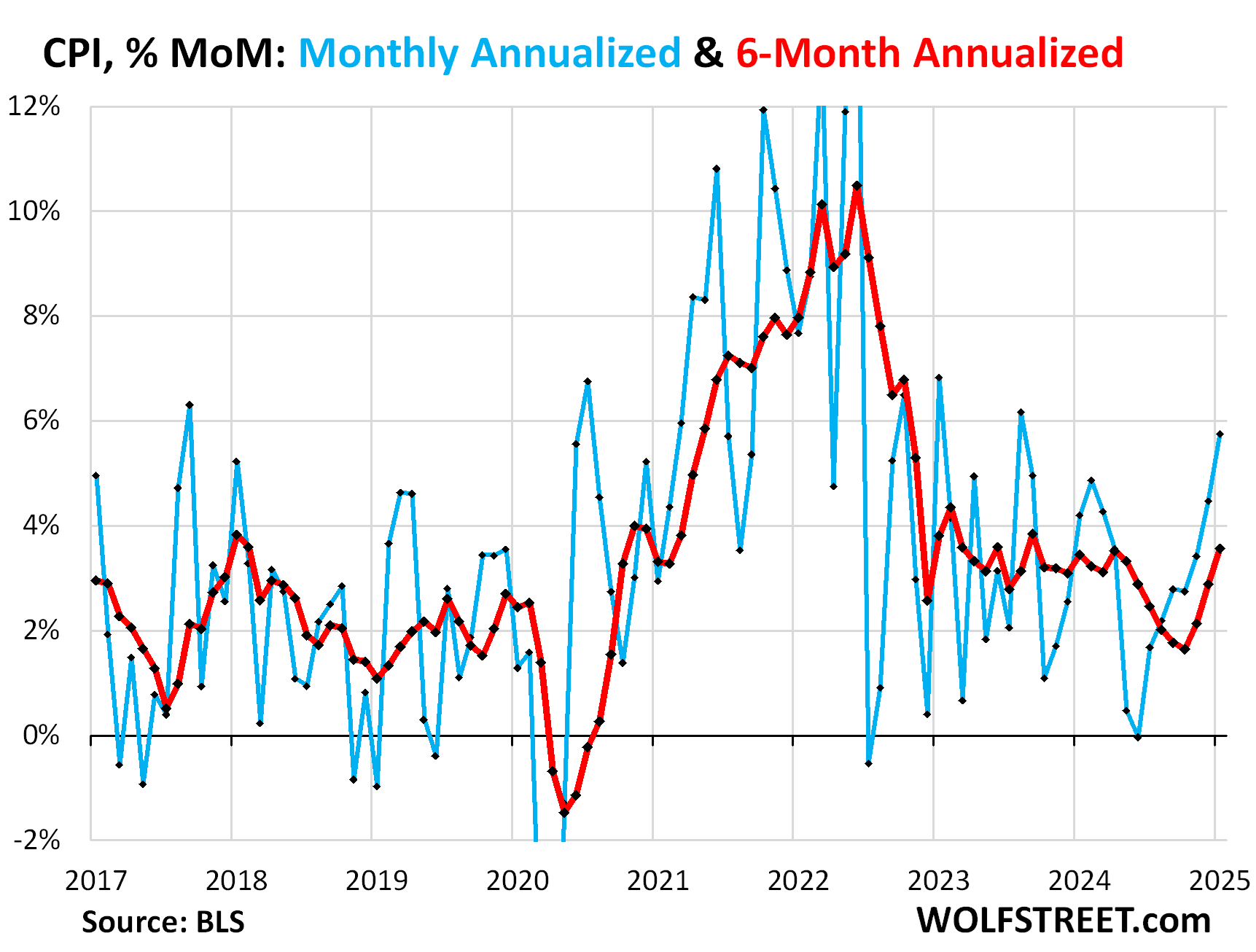

The overall Consumer Price Index rose by 0.47% (+5.7% annualized) in January from December, the worst month-to-month increase since August 2023. It has been accelerating relentlessly since the low point in June (blue). This acceleration pushed the year-over-year increase to 3.0%, the worst increase since May.

- 3-month CPI: +4.5% annualized, sharpest increase since November 2022, and sixth month-to-month acceleration in a row (not shown in the chart).

- 6-month CPI: + 3.6% annualized, worst increase since September 2023. Inflation is going in the wrong direction (red):

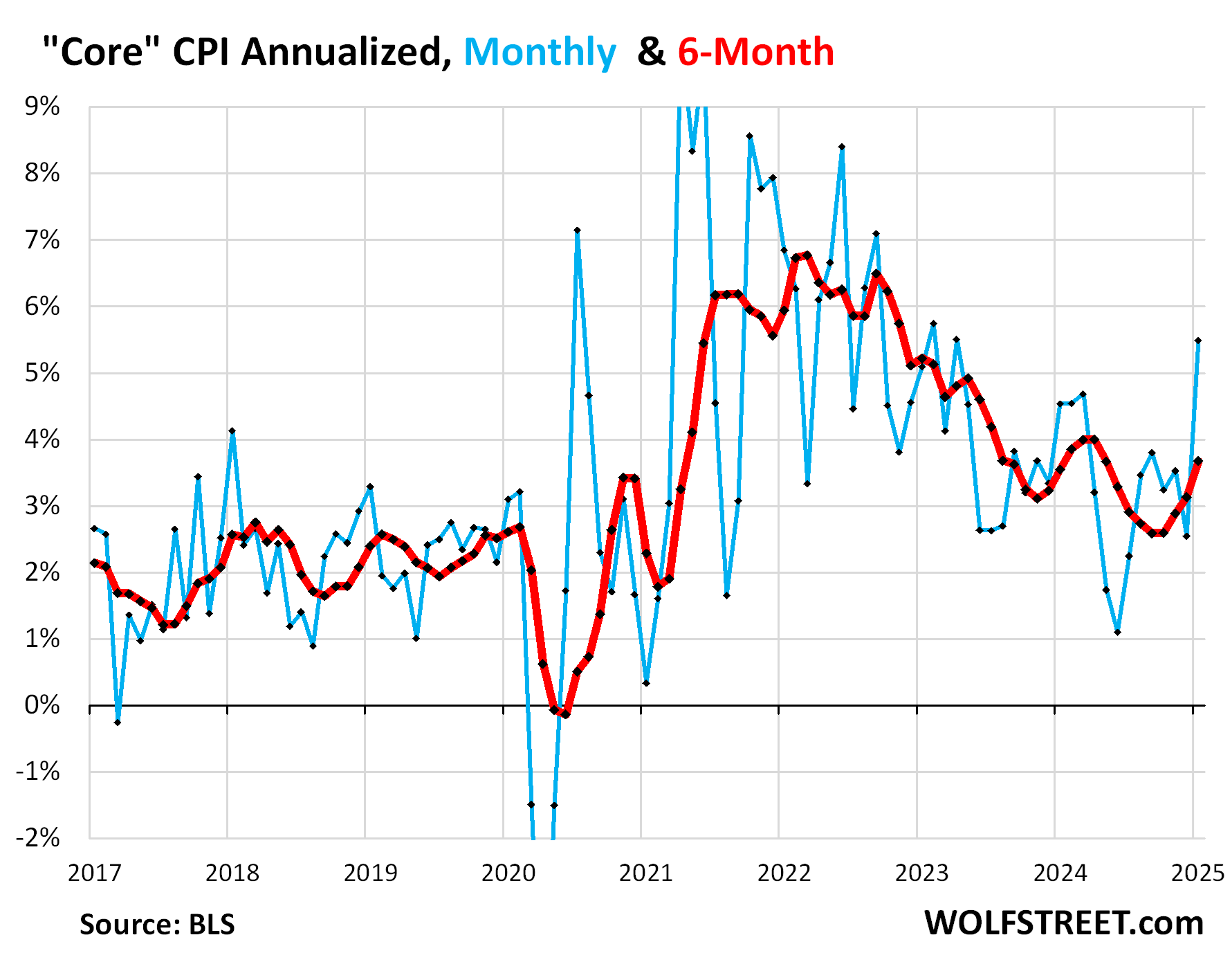

Month-to-month “Core” CPI, which excludes food and energy components to track underlying inflation, jumped by 0.45% (+5.5% annualized) in January from December, the worst increase since April 2023, (blue in the chart below).

The 6-month average “core” CPI accelerated to +3.7% annualized, the third month in a row of acceleration and the worst since May (red).

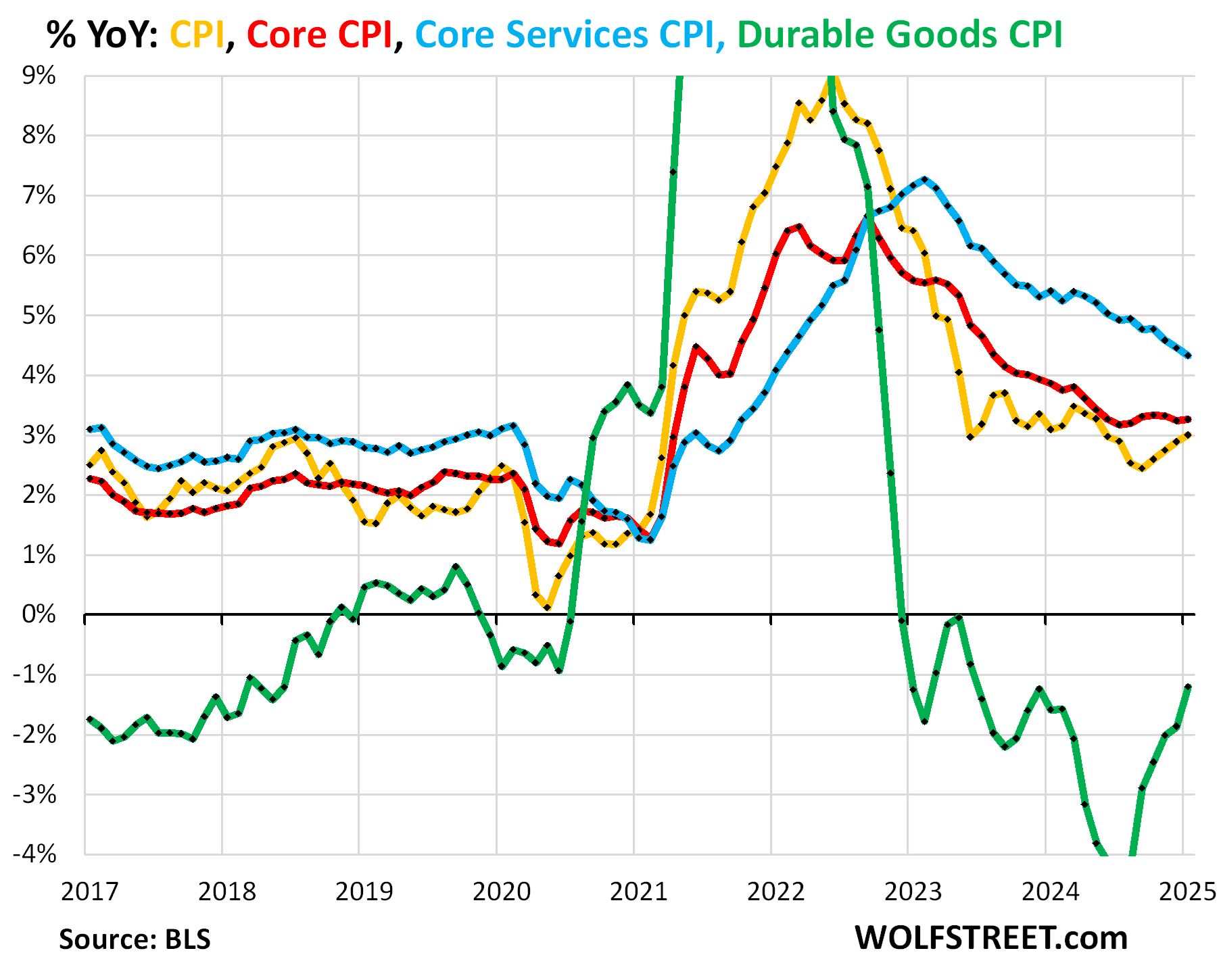

The major components, year-over-year:

- Overall CPI: +3.0% (yellow), worst since May 2024

- Core CPI +3.26% (red), has not improved at all since June 2024

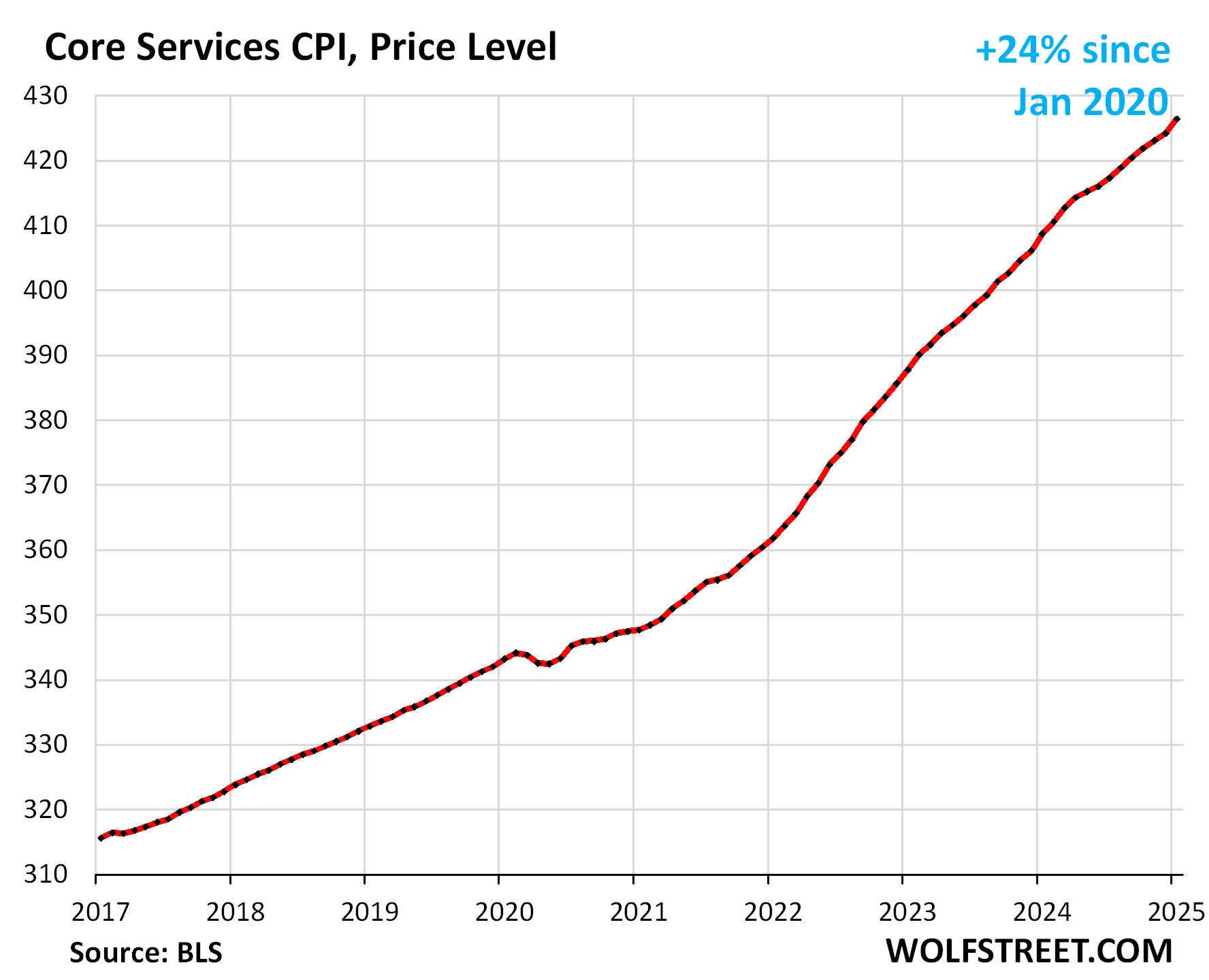

- Core Services CPI: +4.33% (blue). As we’ll see in a moment, month-to-month, it spiked by 6.35% annualized, the worst increase since February.

- Durable goods CPI: -1.21% (green). Month-to-month: +4.6% annualized on a spike in used vehicles, which sharply reduced the year-over-year deflation in durable goods.

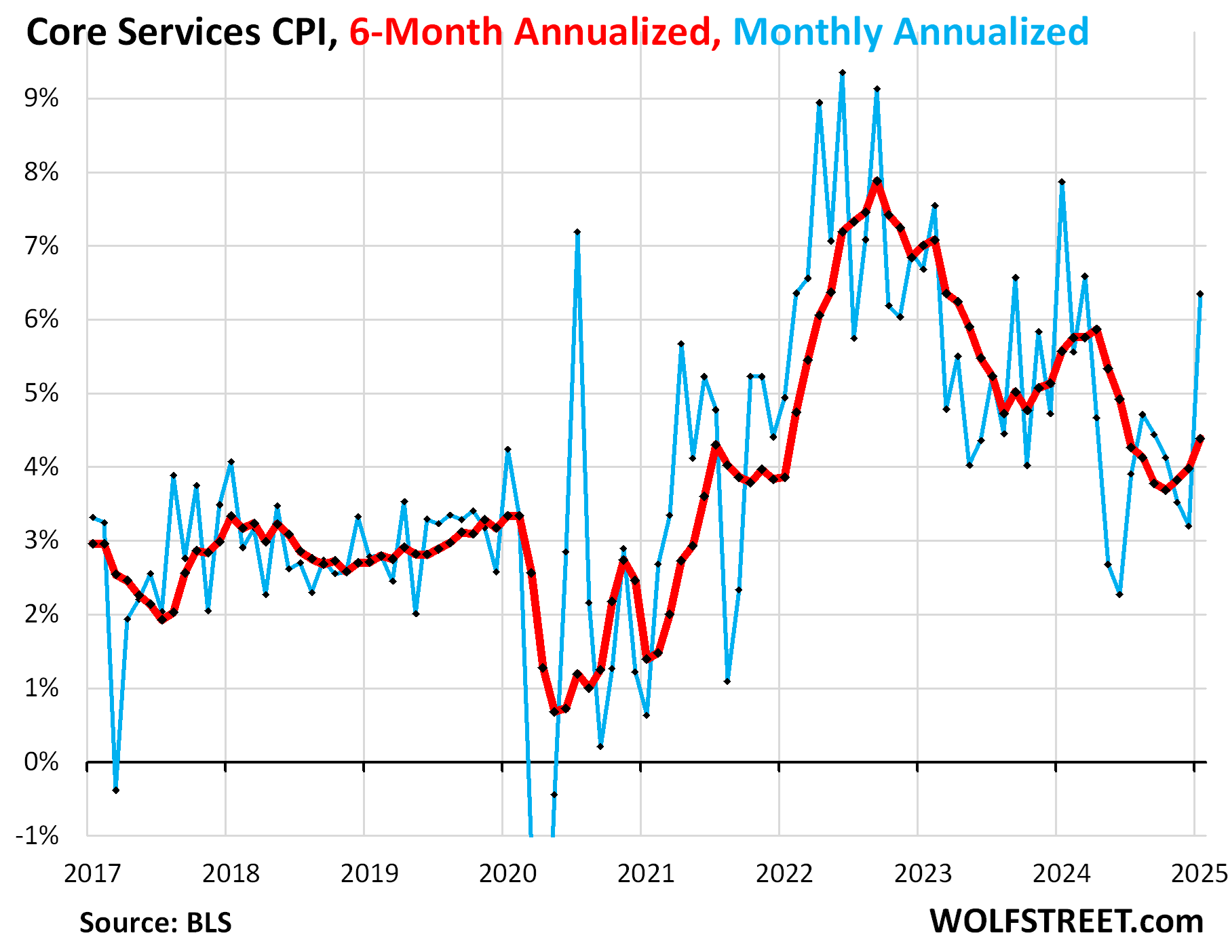

“Core services” CPI.

Month-to-month, the core services CPI, which are all services less energy services, spiked by 6.35% annualized (+0.51% not annualized) in January from December, the worst increase since February 2024 (blue line in the chart below).

The three-month core services CPI accelerated to +4.35% annualized, the worst increase since October.

The 6-month core services CPI, which irons out a lot of the month-to-month squiggles, accelerated to 4.4% annualized, the worst since June (red).

Some services raise their prices annually in January, and those price increases then help produce the spikes of the services CPI in January and February. But we did not see those kinds of price spikes in the Januarys and Februarys before the pandemic; they’re signs of persistent high inflation in services that had not occurred before the pandemic:

Housing components of core services.

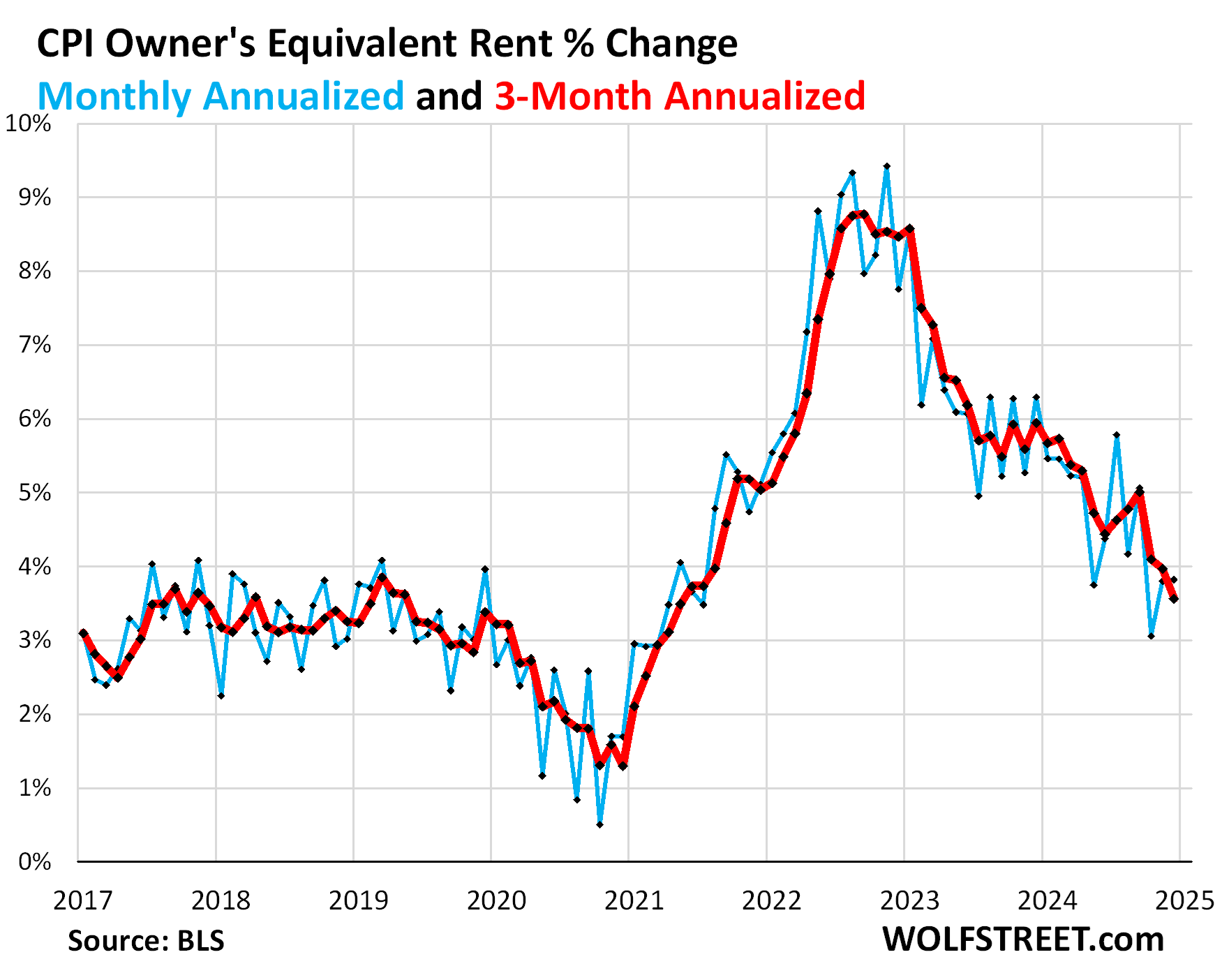

The Owners’ Equivalent of Rent CPI accelerated slightly to +3.8% annualized in January from December (+0.31% not annualized). The three-month average decelerated a hair to +3.6% annualized.

OER indirectly reflects the expenses of homeownership: homeowners’ insurance, HOA fees, property taxes, and maintenance. It’s the only measure for those expenses in the CPI. It is based on what a large group of homeowners estimates their home would rent for, with the assumption that a homeowner would want to recoup their cost increases by raising the rent.

As a stand-in for homeowners’ insurance, HOA fees, property taxes, and maintenance costs, OER accounts for 26.3% of overall CPI and estimates inflation of shelter as a service for homeowners.

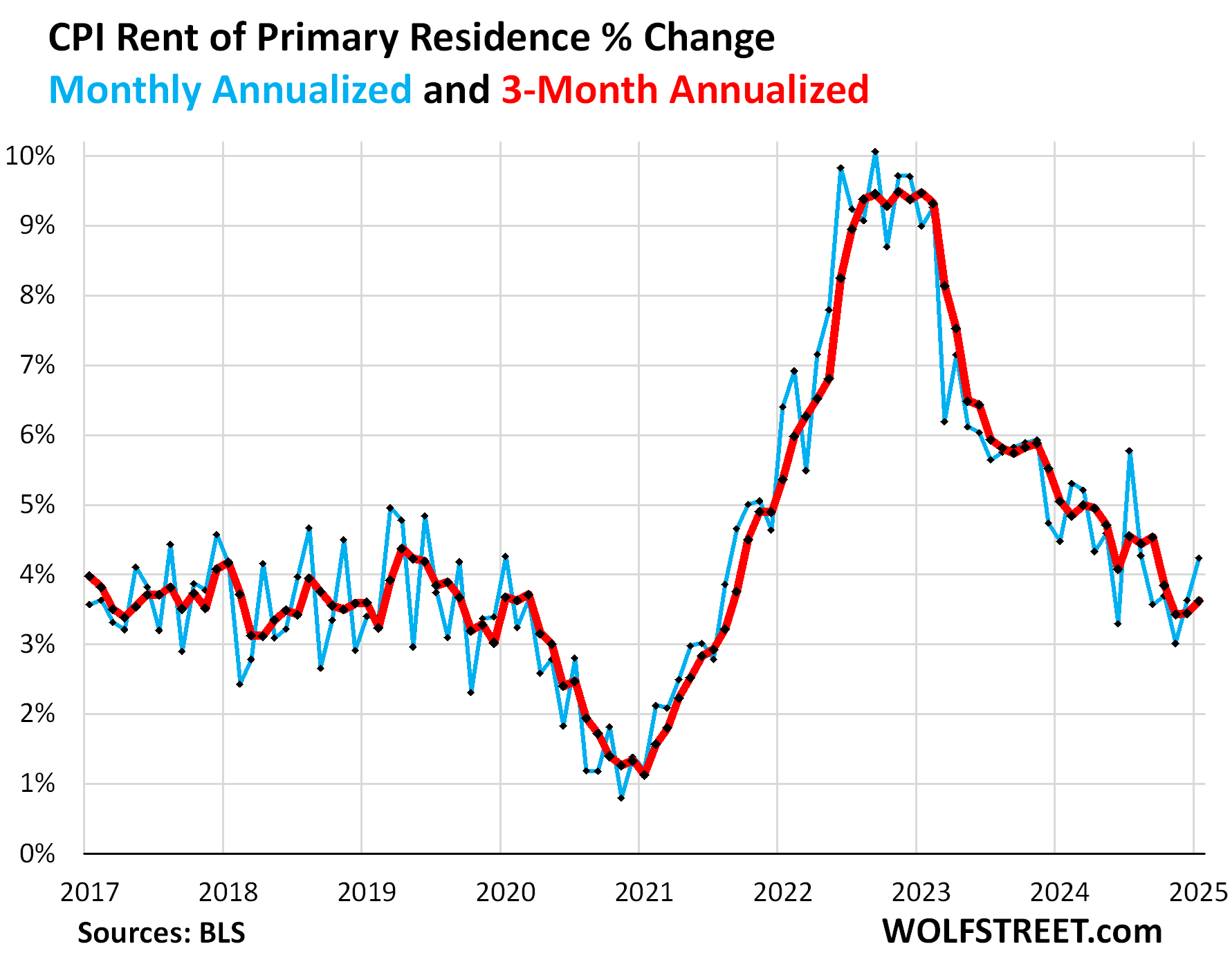

Rent of Primary Residence CPI accelerated to +4.2% annualized in January from December. The 3-month rate accelerated to +3.6%.

Rent CPI accounts for 7.5% of overall CPI. It is based on rents that tenants actually paid, not on asking rents of advertised vacant units for rent. The survey follows the same large group of rental houses and apartments over time and tracks the rents that the current tenants, who come and go, pay in rent for these units.

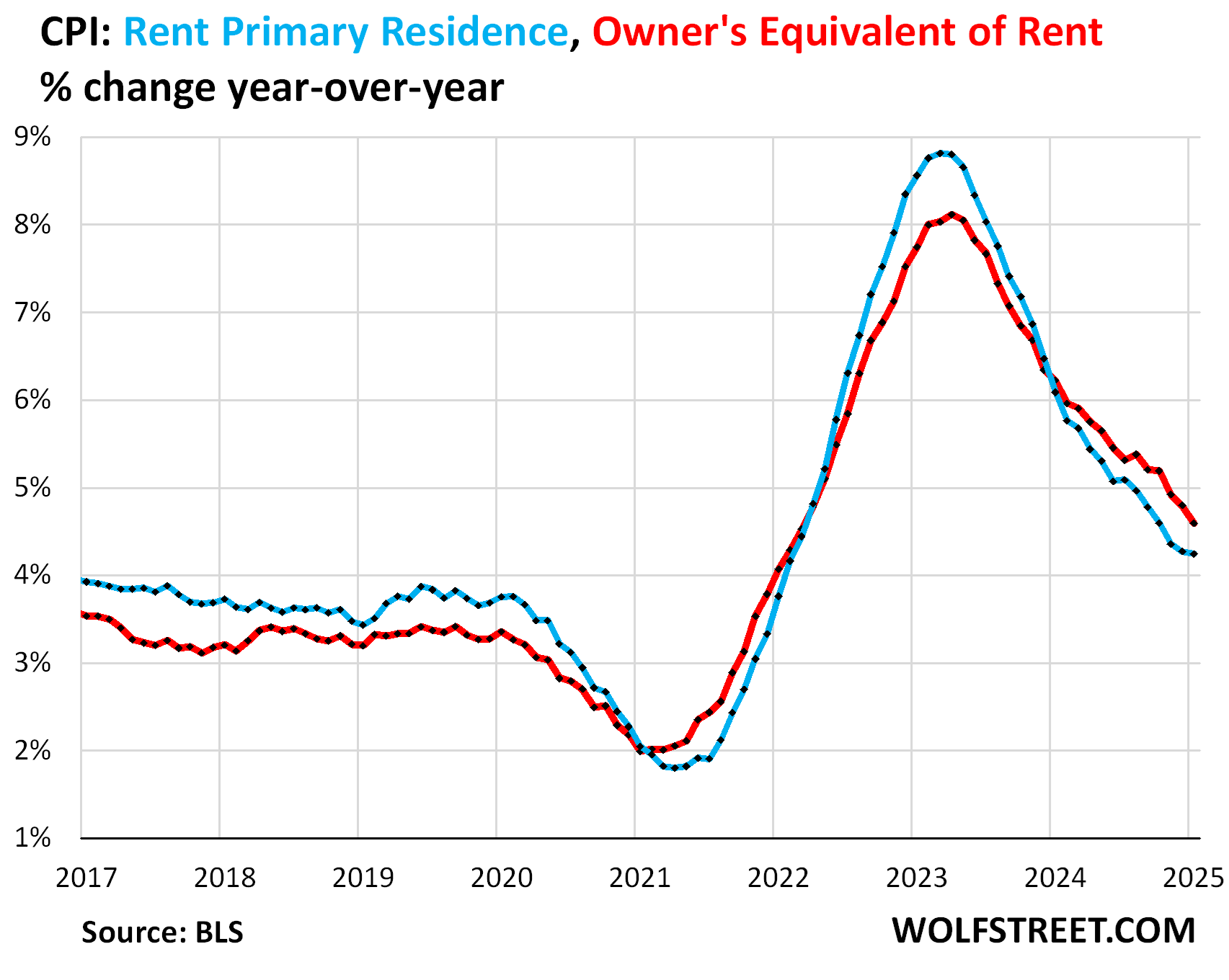

Year-over-year, rent CPI (blue in the chart below) barely budged in January at +4.24% from +4.27% in December. OER CPI decelerated to +4.6% in January from +4.8% in December (red).

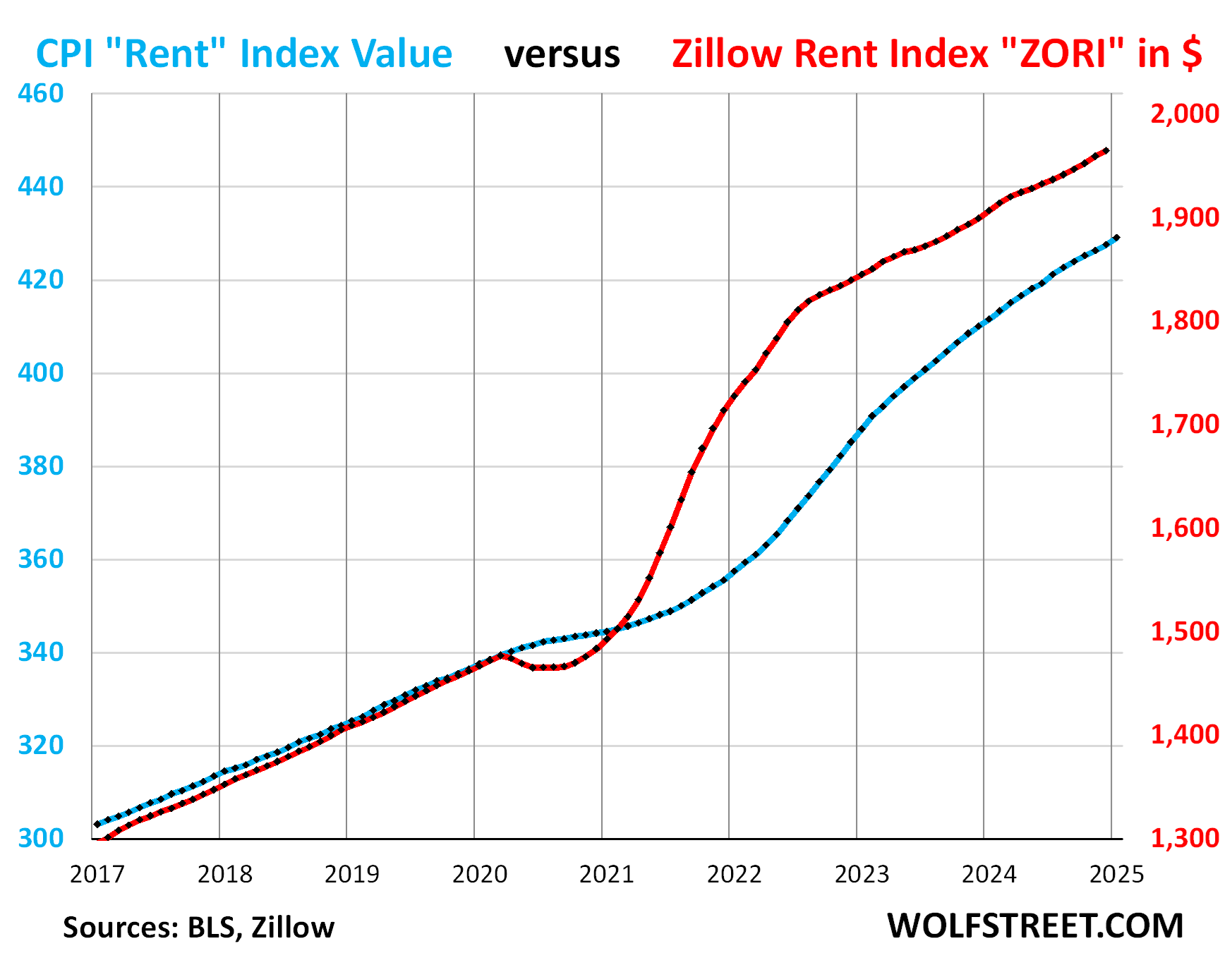

“Asking rents…” The Zillow Observed Rent Index (ZORI) and other private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market for rent. Because rentals don’t turn over that much, the spike in asking rents through mid-2022 never fully translated into the CPI indices because not many people actually ended up paying those jacked-up asking rents.

For December, the ZORI (seasonally adjusted) rose by 0.28% month-to-month and by 3.4% year-over-year.

The chart shows the CPI Rent of Primary Residence (blue, left scale) as index value, not percentage change; and the ZORI in dollars (red, right scale). The left and right axes are set so that they both increase each by 55% from January 2017:

- Since January 2017: ZORI +52%, CPI Rent +42%.

- Since January 2020: ZORI +34%, CPI Rent +27%.

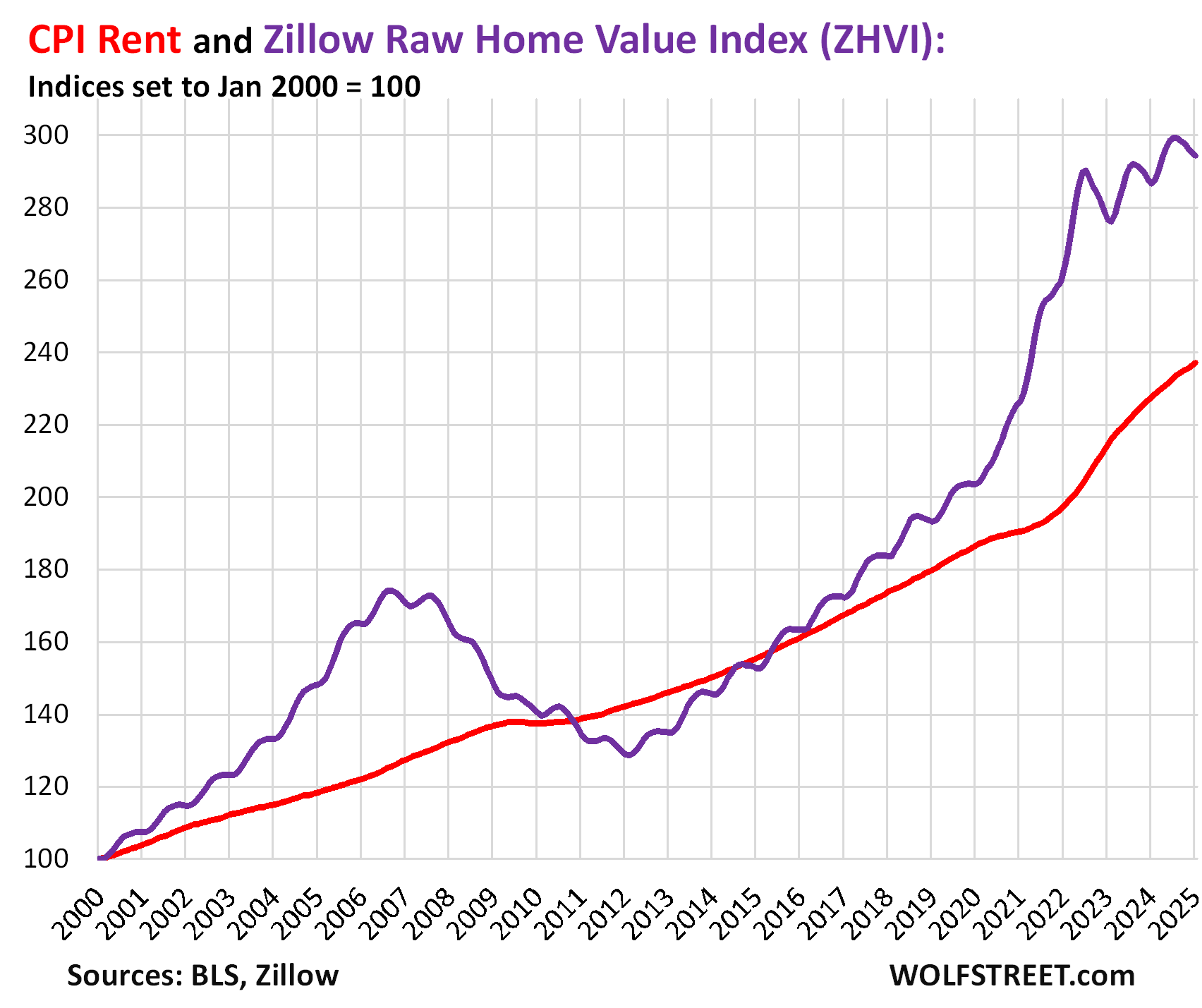

Rent inflation vs. home-price inflation: The red line in the chart below represents the CPI for Rent of Primary Residence as index value. The purple line represents Zillow’s “raw” Home Value Index for the US. Both indexes are set to 100 for January 2000 [home price inflation by metro: The Most Splendid Housing Bubbles in America ]:

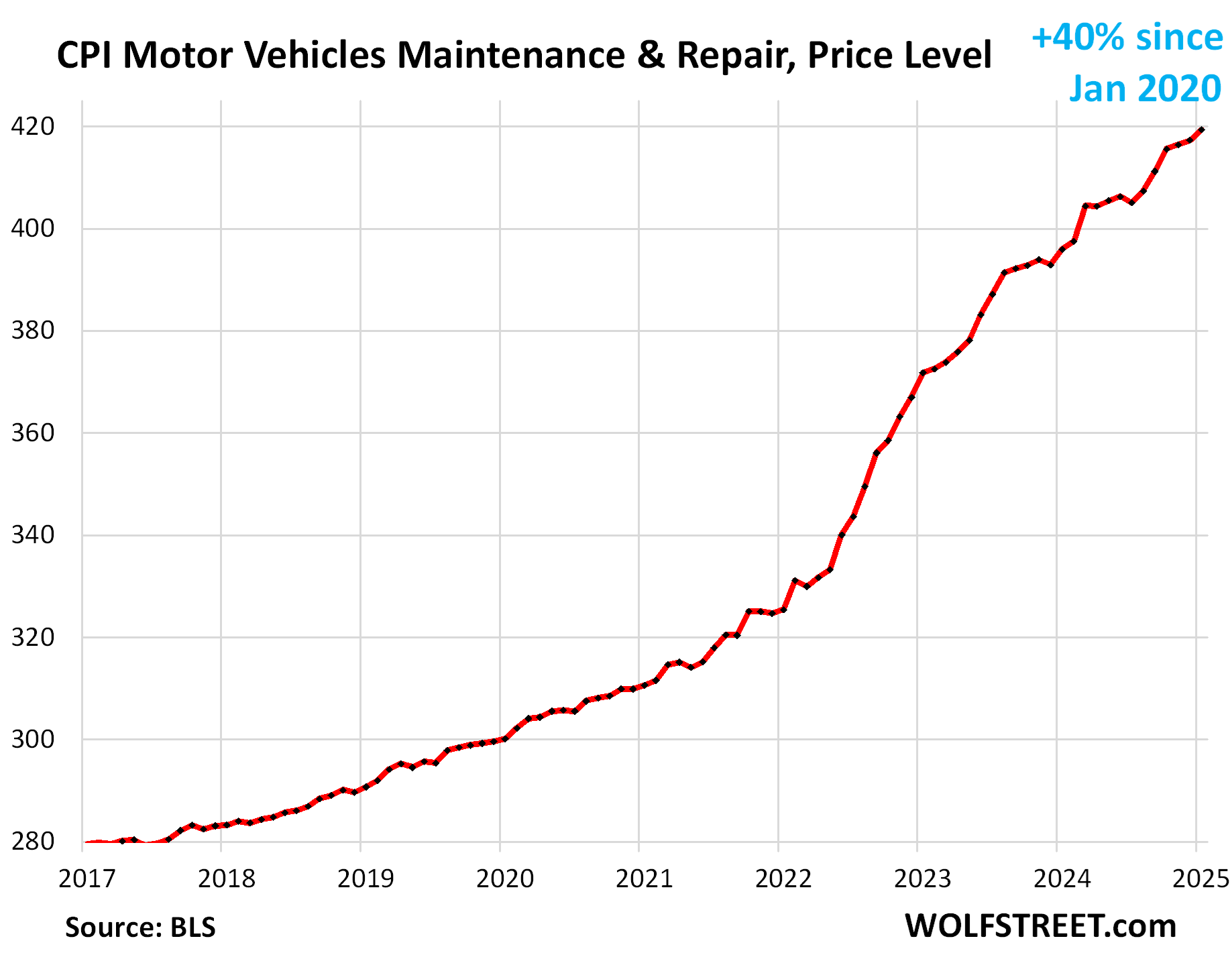

The CPI for motor-vehicle maintenance & repair jumped by 6.2% annualized in January from December. Year-over-year, the index rose by 5.9%, the worst increase since May. Since January 2020, the index has surged by 40%. This chart shows the price level, not the year-over-year percentage change:

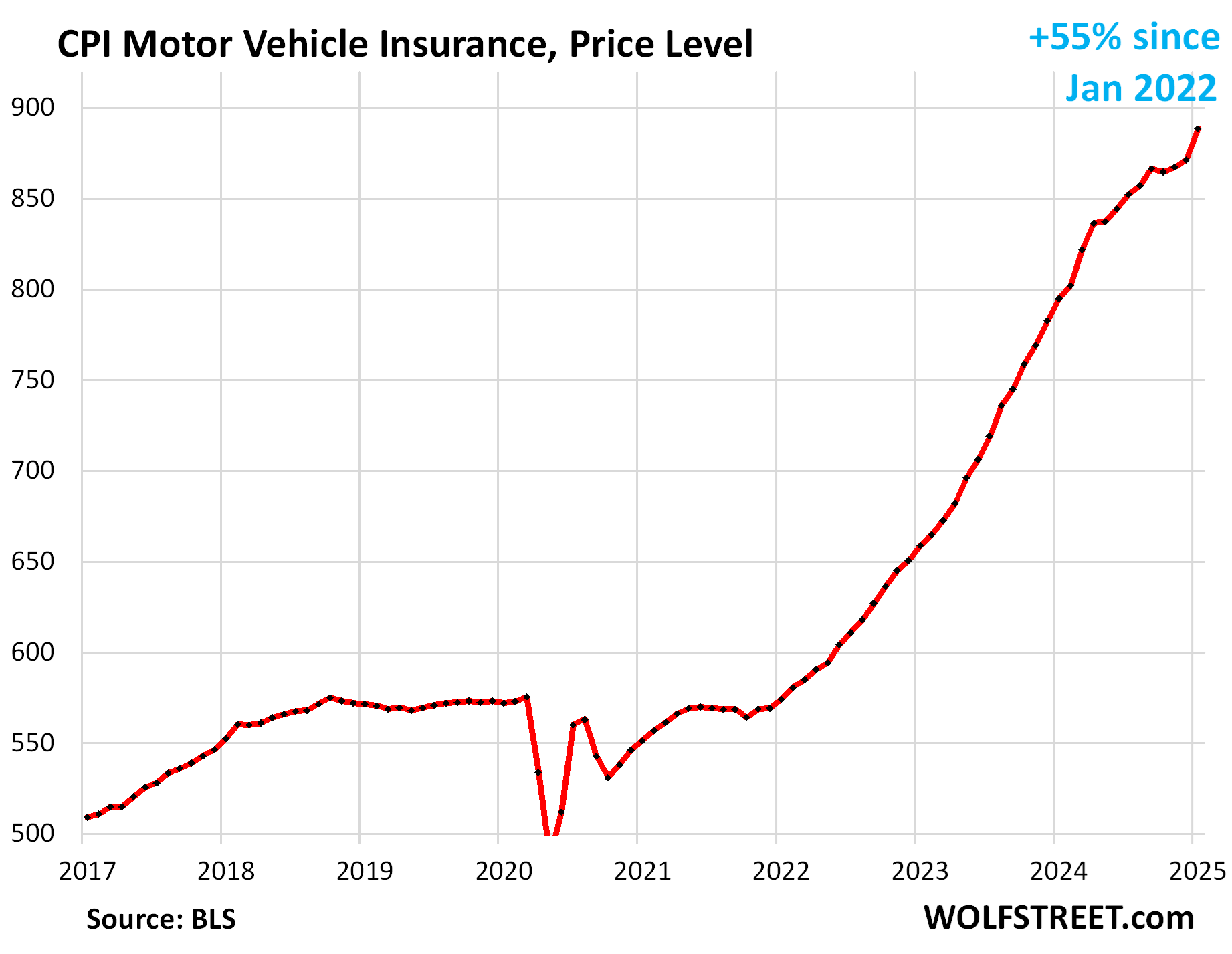

The CPI for motor vehicle insurance spiked by 26.7% annualized in January from December (2.0% not annualized), the worst increase since March 2024. Year-over-year, the index spiked by 11.8%.

Since January 2022, motor vehicle insurance prices have exploded by 55%, fueled by the historic spike in used vehicle prices in 2021 and 2022 (=replacement costs for insurance companies) and by surging repair costs.

Note the spike in January:

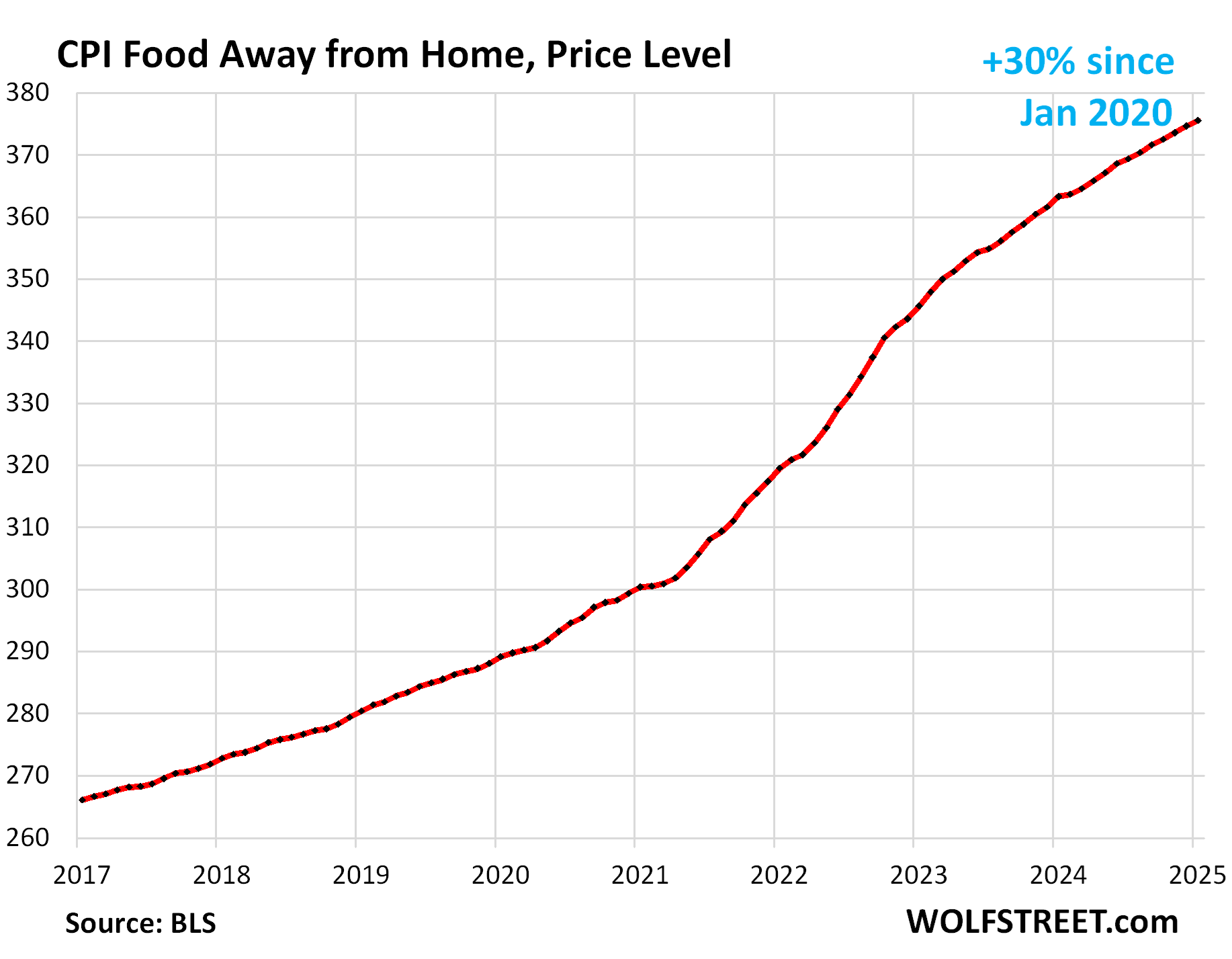

Food away from Home CPI rose by 2.9% annualized in January from December, and by 3.4% year-over-year, the smallest increase since July 2020.

These food services include full-service and limited-service meals and snacks served away from home, such as in restaurants, cafeterias, at stalls, etc.

The table below shows the major categories of “core services.” Combined, they accounted for 64% of total CPI:

| Major Services excluding Energy Services | Weight in CPI | MoM | YoY |

| Core Services | 64% | 0.3% | 4.8% |

| Owner’s equivalent of rent | 26.3% | 0.3% | 4.6% |

| Rent of primary residence | 7.5% | 0.3% | 4.2% |

| Medical care services & insurance | 6.7% | 0.0% | 2.7% |

| Food services (food away from home) | 5.6% | 0.2% | 3.4% |

| Motor vehicle insurance | 2.8% | 2.0% | 11.8% |

| Education (tuition, childcare, school fees) | 2.5% | 0.2% | 3.6% |

| Admission, movies, concerts, sports events, club memberships | 2.1% | 1.5% | 4.0% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.6% | -0.5% | 2.3% |

| Public transportation (airline fares, etc.) | 1.5% | 0.7% | 4.9% |

| Telephone & wireless services | 1.5% | 0.2% | 0.0% |

| Lodging away from home, incl Hotels, motels | 1.3% | 1.4% | 2.2% |

| Water, sewer, trash collection services | 1.1% | 0.7% | 4.4% |

| Motor vehicle maintenance & repair | 1.0% | 0.5% | 5.9% |

| Internet services | 0.9% | 1.1% | -0.5% |

| Video and audio services, cable, streaming | 0.8% | 2.0% | 3.2% |

| Pet services, including veterinary | 0.5% | 0.1% | 5.9% |

| Tenants’ & Household insurance | 0.4% | 1.1% | 2.1% |

| Car and truck rental | 0.1% | 1.7% | -3.6% |

| Postage & delivery services | 0.1% | -1.2% | 7.6% |

The core services CPI overall has risen by 24% since January 2020.

Prices of Goods.

The used vehicle CPI jumped by 2.2% not annualized (29.7% annualized) in January from December, seasonally adjusted, the fifth month-to-month increase in a row, and the worst since May 2023 (red in the chart below).

Not seasonally adjusted, the index jumped 0.5% not annualized (6.5% annualized), though it would normally decline in January (blue).

The surge over the past five months has flipped the 10% year-over-year plunges in June and July into a year-over-year increase of 1.0%, the first year-over-year increase since October 2022 back when the historic price spike was unwinding.

The plunge of used vehicle retail prices from early 2022 through August 2024 was a powerful factor in the cooling of CPI inflation. But this U-turn has now become fuel for the re-acceleration of overall inflation, amid structurally tight retail inventories, strong demand, and surging wholesale prices.

Prices are still up by 33% from January 2020, and it now seems unlikely that they will give up more of the pandemic price spike.

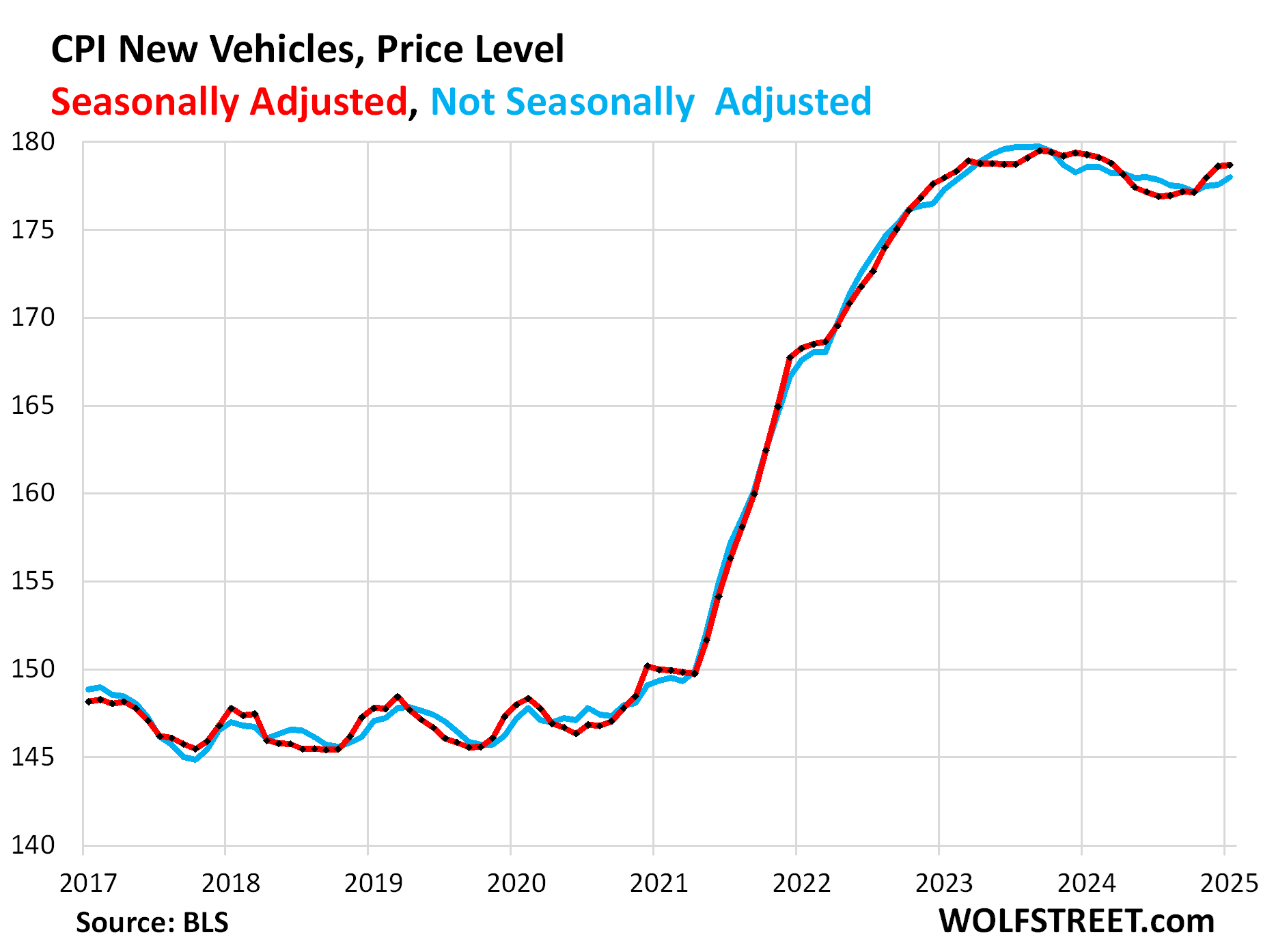

New vehicles CPI edged up by a hair in January from December, seasonally adjusted. Not seasonally adjusted, the index rose by 0.26% (not annualized). This whittled down the year-over-year drop to just 0.3%.

New-vehicle prices have been sticky, unlike used-vehicle prices, despite abundant supply of new vehicles now on many lots, as automakers and dealers are trying to preserve their profit margins. The big incentives and discounts in recent months mostly just undid part of the increases in MSRPs. Since January 2020, the index is up 20.7%.

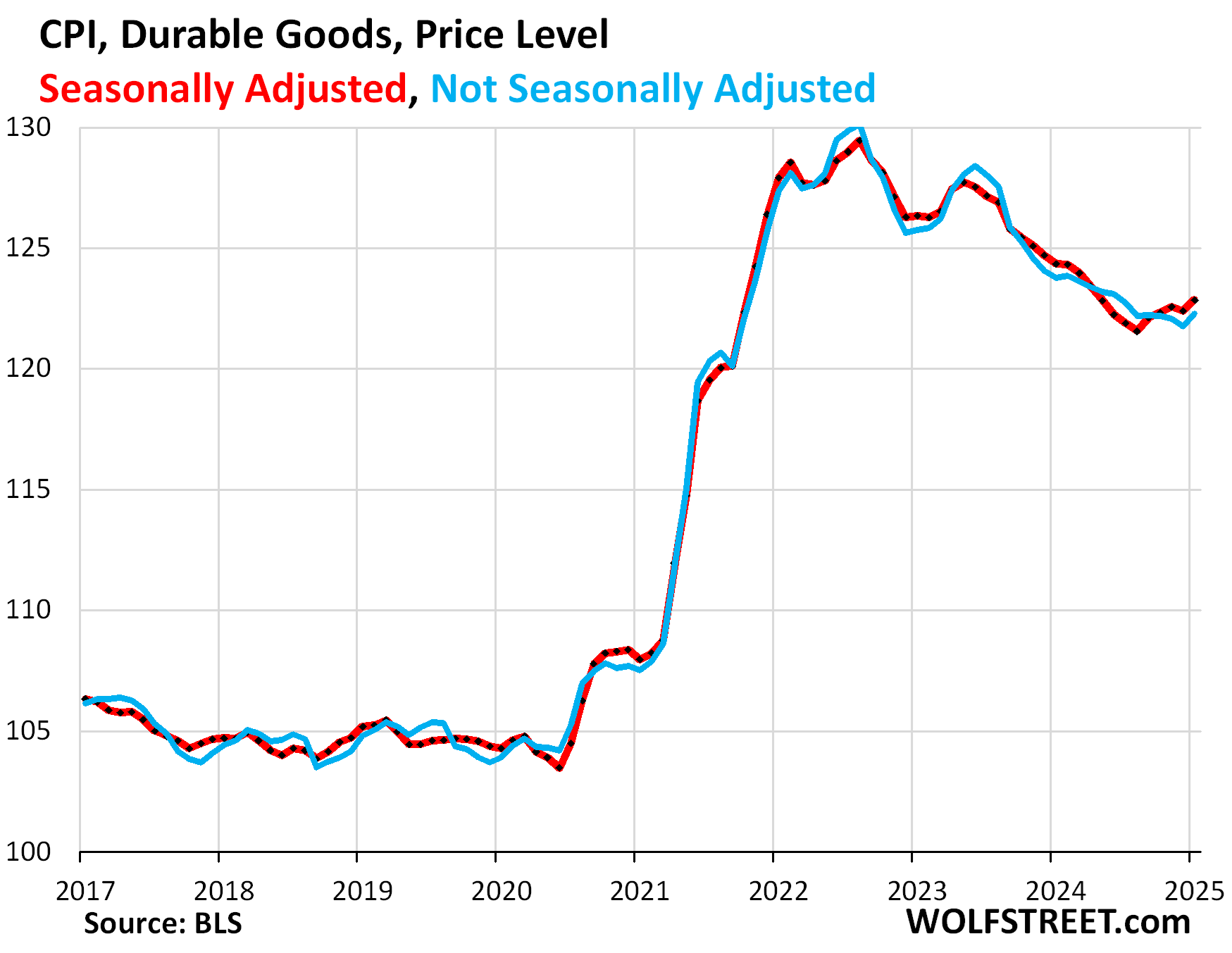

Durable Goods are dominated by new and used vehicles. Starting in mid- to late 2022, all major durable goods categories experienced price declines (deflation), off the price spike during the pandemic. But the month-to-month price drops in motor vehicles ended months ago, and prices have risen since then. And the other major categories of durable goods prices have slowed or ended their month-to-month declines:

| Major durable goods categories | MoM | YoY |

| Durable goods overall | 0.4% | -1.2% |

| New vehicles | 0.0% | -0.3% |

| Used vehicles | 2.2% | 1.0% |

| Household furnishings (furniture, appliances, floor coverings, tools) | -0.2% | -0.9% |

| Sporting goods (bicycles, equipment, etc.) | 0.2% | -3.8% |

| Information technology (computers, smartphones, etc.) | 0.0% | -8.2% |

Food Inflation.

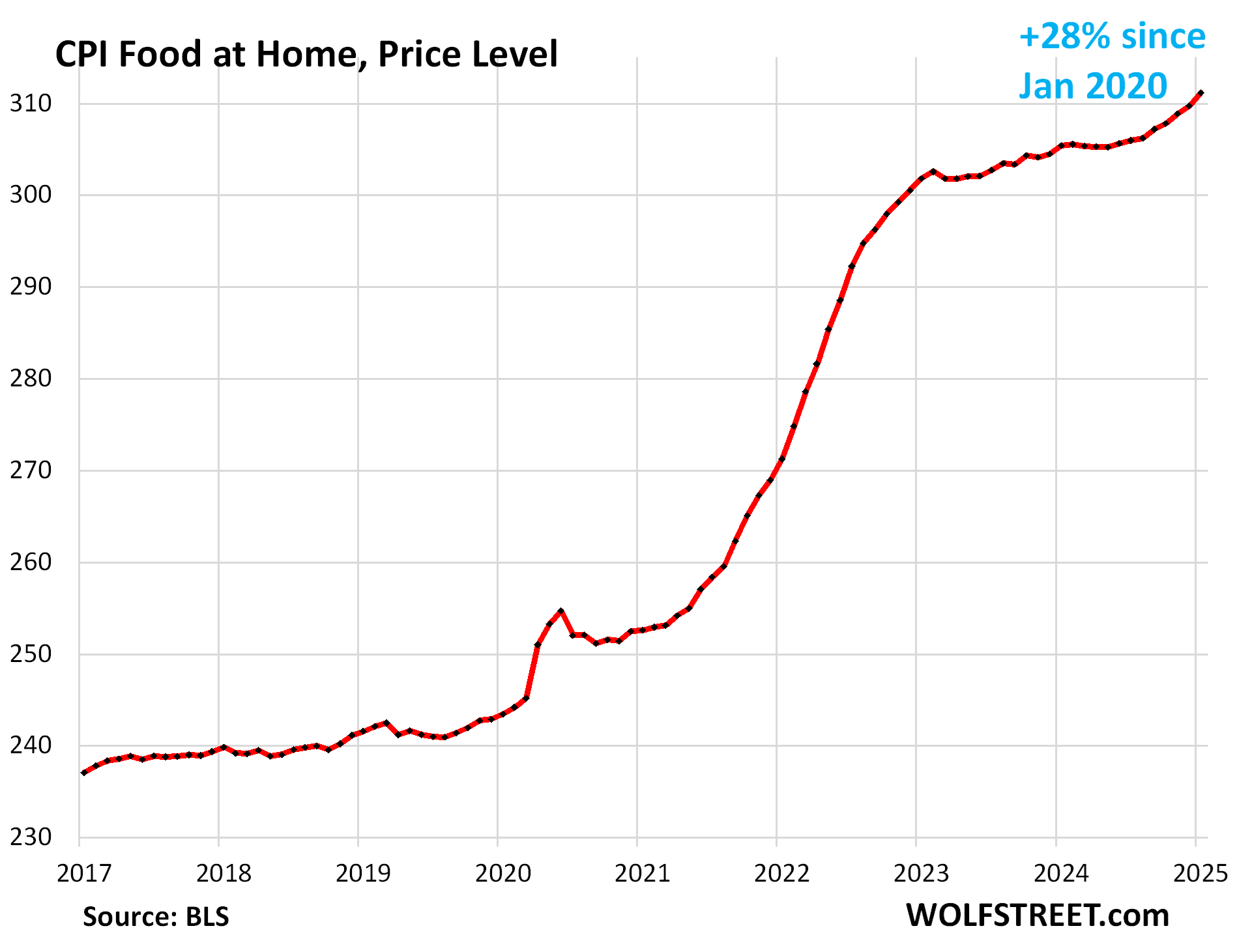

The CPI for “Food at home” – purchased at stores and markets and eaten off premises – jumped by 5.7% annualized in January from December (+0.46% not annualized), the worst increase since October 2022.

This pushed the year-over-year price increase to 1.9%, the biggest increase since October 2023. Since January 2020, food prices have surged by 28%.

After a brief lull at painfully high price levels, food price inflation has been re-accelerating sharply for the past five months.

Part of this re-acceleration is due to the spiking prices for eggs, where the avian flu has been wreaking havoc since early 2024.

Beyond eggs, big month-to-month increases also occurred with beef, pork, fish and seafood, fresh fruit, and juices and nonalcoholic drinks.

| MoM | YoY | |

| Food at home | 0.5% | 1.9% |

| Cereals, breads, bakery products | -0.4% | 0.4% |

| Beef and veal | 0.7% | 5.5% |

| Pork | 0.7% | 2.8% |

| Poultry | -0.1% | 0.4% |

| Fish and seafood | 0.8% | 0.9% |

| Eggs | 15.2% | 53.0% |

| Dairy and related products | 0.3% | 1.2% |

| Fresh fruits | 0.5% | 1.4% |

| Fresh vegetables | -1.7% | -0.6% |

| Juices and nonalcoholic drinks | 1.1% | 1.9% |

| Coffee, tea, etc. | -0.1% | 3.1% |

| Fats and oils | 0.1% | 0.4% |

| Baby food & formula | -0.3% | 1.1% |

| Alcoholic beverages at home | 0.1% | 0.8% |

Apparel and footwear.

The CPI for apparel and footwear dropped by 1.4% (not annualized) in January from December, which reduced the year-over-year increase to 0.5%.

Energy.

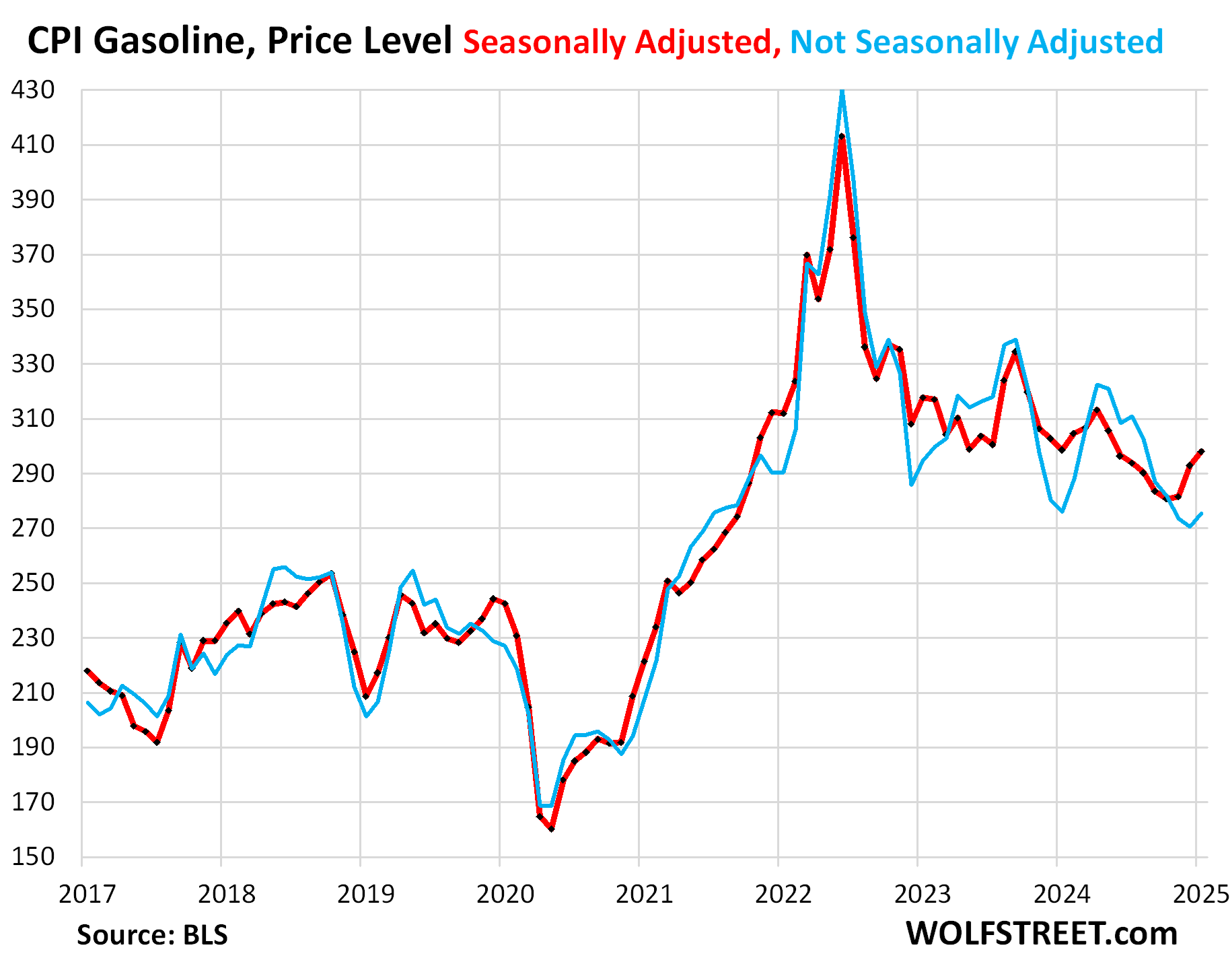

The CPI for gasoline makes up about half of the overall energy CPI. It jumped 1.8% in January from December, seasonally adjusted, which about ended the year-over-year decline.

Not seasonally adjusted, gasoline also rose, when it normally declines during the low-demand winter months.

Compared to the peak in the summer of 2022, gasoline prices plunged by 28% seasonally adjusted (red), and by 36% not seasonally adjusted (blue). This had been a big factor in the deceleration of overall CPI inflation.

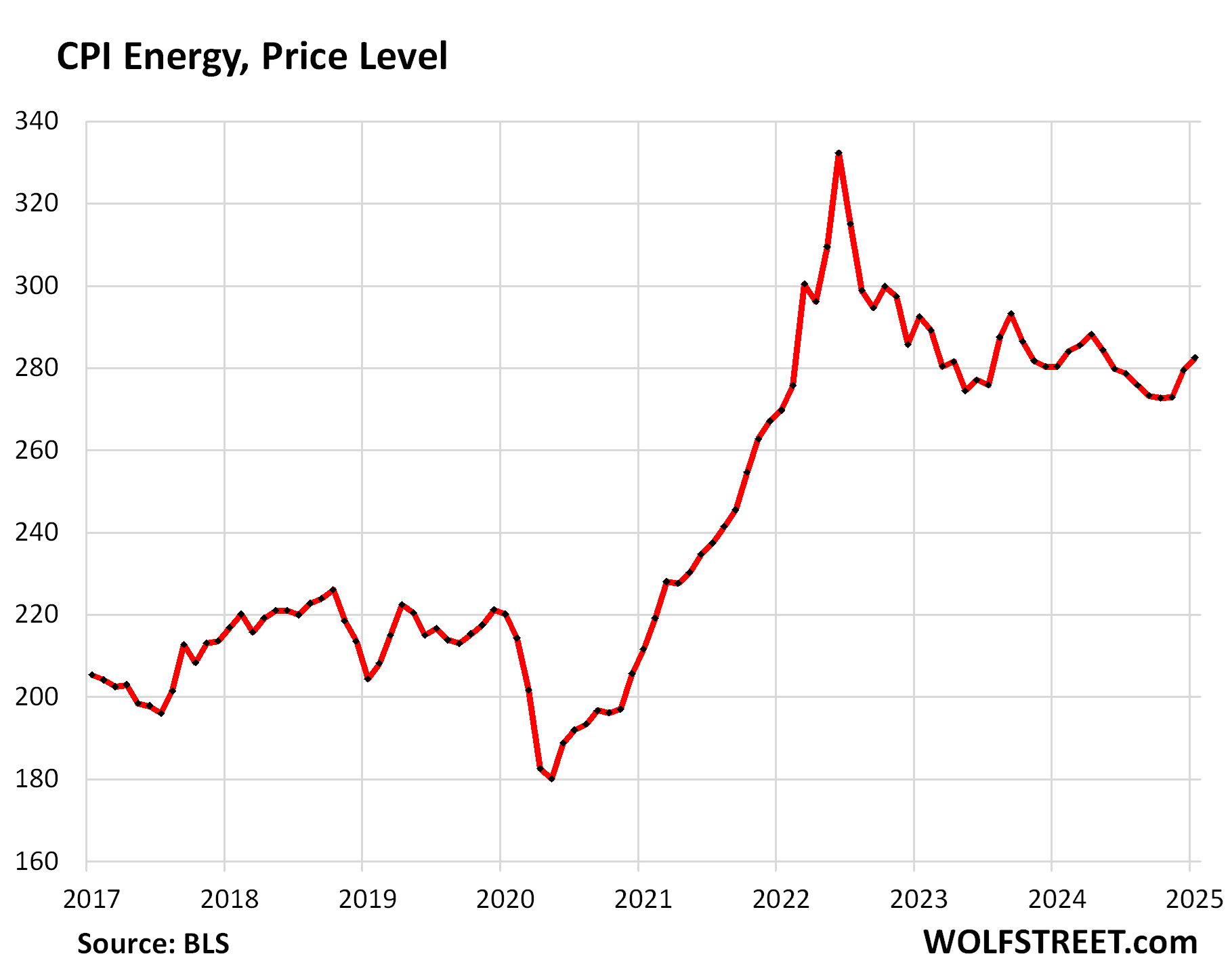

The CPI for energy, which covers energy products and services that consumers buy and pay for directly, including gasoline, jumped by 1.1% in January from December, and rose by 1.0% year-over-year, the first year-over-year gain since July.

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | 1.1% | 1.0% |

| Gasoline | 1.8% | -0.2% |

| Electricity service | 0.3% | 2.5% |

| Utility natural gas to home | 1.8% | 4.9% |

| Heating oil, propane, kerosene, firewood | 4.1% | -1.3% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

and yet stocks are barely affected. there is just too much money chasing too few assets, and every dip is seen as a buying opportunity. if a report like today doesn’t make it drop 2-3%, what will?

i think it’s likely stocks don’t materially drop, but just trade sideways for the next 5-10 years.

Too much liquidity in the system and no exogenous shock ala 2008 to cause massive and immediate repricing.

Maybe a couple bad hurricanes in a few key ports across the Gulf might do it? Best I can come up with. I’m buying Bitcoin still – entropic store of value, people!

The price of the home that I was looking at buying in 2009/2010 in Southern Arizona hasn’t changed in value in 15 years (according to Zillow).

As a Millennial, I am not getting the same deal that my parents got (not that I’m doing bad – But I’m the exception).

What town are you talking about? I don’t live in Tucson but do follow the R.E. market there and they are in a full-blown Real Estate mega bubble. And in the 2007 R.E. bubble, Tucson had not really gone crazy like most of the state (Phoenix etc.). So I am curious where you are finding real estate at 2010 prices in S. Az. Ajo? Douglas? Nogales? Willcox?

5-10y of trading sideways might be the most painless way out of this mess to be perfectly honest. I think the Fed would take that scenario.

Should be interesting to see the politics versus economics dynamics play out…

Inflation is pretty hot, but Trump wants lower interest rates – If he gets what he wants with the Fed and short term rates, it’ll drive higher long-term rates which seems likely to do the opposite of what he’s hoping for…

As we know from his billionaires that run the shop, Trump really wants lower LONG-TERM rates. The Fed’s policy rates don’t matter that much except for SOFR-linked floating rate loans. Most other debt is linked to long-term Treasury yields. If the 10-year yield rises, like it did today due to inflation, then long-term rates across the board are going to rise, and borrowing gets a lot more expensive (fixed-rate bonds and loans of all kinds).

To get lower long-term rates, inflation must come down and stay down.

So what can being down inflation down at this point other than a recession?

Maybe stop the printing presses?

David,

The printing presses have been turned into shredders and since mid-2022 have shredded $2.15 trillion of that printed US money. And there are also big shredders going BRRRR in other countries.

Shredder goes BRRRR:

I was about to ask this same question- it seems like inflation is entrenched and unless we get a shock to the economy, what The Fed is doing isn’t working anymore.

Cheaper energy will bring costs down bigly. Reduced govt fraud and waste will help with funding and rates as well. Sounds like we are going to be getting cheap commodities from Ukraine which will go into the sovereign wealth fund and go towards lower taxes for working people.

It’s a very clear path to prosperity from here and the stock market will bleed out as financialization dies and real honest work gets compensated.

Next level sarcasm Domo, you had me for a sec there 😂

Which part of his comment do you think is sarcasm?

>Cheaper energy will bring costs down bigly.

Absolutely true. I’d argue cheap natural gas is a big reason we’ve avoided recession recently.

>Reduced govt fraud and waste will help with funding and rates as well.

Also true. Bond investors won’t demand higher yields if they’re not as worried about inflationary gov’t spending.

>Sounds like we are going to be getting cheap commodities from Ukraine which will go into the sovereign wealth fund and go towards lower taxes for working people.

I’d argue Russian energy returning to the world stage is more impactful here, but both countries will benefit from the end of the war. Hell, anyone who isn’t part of the military industrial complex should want the war to end.

The *expectation* of a recession would bring inflation down, even if it’s not actually followed by a recession.

Come to think of it, isn’t that the story of 2023 and 2024?

“Reduced govt fraud and waste will help with funding and rates as well”

“as financialization dies and real honest work gets compensated”

The statements are true. The idea that anyone can honestly say they think the US is heading in this direction is laughable.

The Fox, et al, cheerleaders all are still yelling “promises made, promises kept”, to the faithful, but most all I see is (like dustoff) a possible stock buy in Sharpies……..They also like to show coastal elite snowflakes like me being extremely upset, which the fans must enjoy….but I’m not upset….what’s done is done….time to watch….read WS.

They all seem to be having fun at the Whitehouse, so something must be going well…..for someone……

From Wolf’s article, I betcha nobody there, or at Fox, talks about eggs, though.

Agree 100%

That’s why the disconnect between economic reality and political theater has caught my attention…

What Trump (and Co) really wants is long-term interest rates to come down, but when he’s talking about what the Fed can control, those are the short term rates.

Still, here he is with the political theater:

“Interest Rates should be lowered, something which would go hand in hand with upcoming Tariffs!!! Lets Rock and Roll, America!!!” the president said in a morning post on Truth Social

You were expecting coherence?

Long-term lurker. My understanding is that the Fed won’t stop quantitative tightening or lower rates until the markets are showing signs of distress. What kind of stress are they looking for? Also, keeping rates high helps with inflation right?

“ You were expecting coherence?”

Sadly, no – Mostly just pointing out the inconsistencies…

Fed rates matter a ton for those of us that don’t want to chase the ponzi stock market. If Trump gets his way, the poor and middle class will suffocate under inflation.

It’s interesting for sure.

Trump is surrounded by Billionaires and people say he works for them.

Trump is big Pro Tariffs. But Billionaires hate tariffs. Billionaires want all things to be made in cheaper location with no regard for human working condition or ecosystem.

And consumers just want cheap goods at all cost, matter where it comes from or the inhumane conditions there.

Humans kind of suck, not just billionaires.

Speak only for yourself!

After a few ”cheap” tools were broken quickly, an older carpenter told me to find THE BEST QUALITY tools, even if it meant buying only one per pay check when I was apprenticing OJT in the 1960s.

I still have and use some of those made by the BEST companies in USA from that era, and many more from until the 1980s when I geared up to provide tools for my employees.

Maybe part of the informal education sadly lacking these days???

VVnVet,

I hafta say, I’m impressed with the quality of some of the “cheap” stuff at Harbor Freight. It’s hit or miss for sure, but reading reviews ahead of time you can avoid the known junk.

Recently invested in their Hercules system of power tools at a fraction of the cost of DeWalt, Milwaukee etc. They seem well enough built for someone who’s an amateur DIYer and not a real mechanic.

I know a lot of folks don’t like Craftsman since they were bought out by Lowes, but I inadvertently tested the strength of their half inch ratchet recently… ended up breaking the tip off with a cross-threaded bearing pusher tool and a 3 foot breaker bar on the end. The only reason we were using the ratchet is because it was too much torque even for my buddy’s full size Milwaukee impact.

You honestly believe other president’s were not surrounded by the business leaders running the show.

There has never in my lifetime been a businessman pulling the puppet strings to the extent Musk is doing now.

Mike G,

Perhaps not as *publicly* as Musk is doing…

Wait, you mean if you lower interest rates and the economy is roaring along, prices increase?!?! Whoa! Hold the presses! Someone please tell

Jerome Powell. I don’t think he knew this!

Is it roaring though? A lot of sectors are still severely repressed compared to the 2010s. Hiring in some previously strong sectors (eg tech, finance) is nonexistent. It doesn’t feel like it is roaring, more that there is still too much liquidity and the inflation of 2021-2022 is still making its way through the system.

GDP says the economy is doing quite well.

The economy is doing great for about 70% of the population. For 30%, it’s doing awful. Problem is, that 30% is a lot of friends and family of the 70%. And a lot of those people feel poorly about their less well off friends and family. So the general sentiment isn’t reflective of actual GDP growth, hence Donald Trump.

Raise the interest rate!

Which interest rate?!

Wolf, Thanks again for a very informative report on inflation.

I have a request: could you add a section on health insurance CPI? I’ve seen several tweets about how the BLS methodology for that sector is bizarre and has produced not-beievable decreases in the last few years. And it’s a big major part of the economy.

Not going to discuss it anymore until they come up with a better system.

Here are two of my prior articles on this topic, they explain the situation of the screwed-up data of 2021-2023, including charts:

https://wolfstreet.com/2023/11/14/the-collapse-of-the-health-insurance-cpi-how-it-became-chickenshit/

https://wolfstreet.com/2023/08/10/a-word-about-the-odious-ridiculous-massive-adjustments-to-health-insurance-cpi-which-now-collapsed-to-jan-2019-levels/

What they’re now doing is that they just left the screwed-up data of 2021-2023 as is and said forget it, not fixable.

And now they focus on trying to get month-to-month and year-over-year figures somewhere close to right because that counts in CPI.

Health insurance CPI was up 0.74% (9.25% annualized) in January from December. That might be about right.

But the prior years are and remain screwed up, and I’m done talking about it

Ok

Random tariff proposals are creating instability in businesses that import materials or products. Let’s be clear, China or Mexico do not pay the tariffs, it it the companies that import the products that pay. They either eat the costs or pass them on to the consumer. Then the nations hit retaliate. An example is China shifting their buying of soybeans, corn and wheat to Brazil or Argentina and American farmers having to be subsidized by the U.S. government. So the tariff angers the importers, the targeted country and the farmers. Argentina and Brazil won in the first round of tariffs back in 2018. U.S. manufacturers could not pass the costs on and their margins suffered. Our farmers saw prices collapse and the BRICS became an economic force. U.S. consumers used to import deflation by buying products that were subsidized by China. I’m not seeing much “Winning” in the first round of tariffs.

No stability for our companies in this round as the only benefit can come from moving the manufacturing home and isolating the U.S. and its labor force from the world economy.

I expect the CPI to go up from all of the tariffs and increased costs of building plants and sourcing materials from home.

Time will tell…

Some vendors to my company are already imposed price increase in ANTICIPATION of tariffs.

Change vendors on the spot.

Hard to change from using products from companies like Rockwell. I suspect that other industrials will be following suit. We’ll see how much we can pass on to our customers, but this will feed on itself.

Brewer I know says beer prices are going to go up substantially with the aluminum tariffs, time to start hoarding

This is the kind of stupid ignorant bullshit that makes me laugh.

1. There are only a few cents of aluminum in an aluminum can. The tariffs are applied to the purchase cost of the bulk aluminum (without transportation costs) that the importer pays. A 25% tariff on the cost paid by the importer might raise the cost of a can for the can manufacturer by $0.01 (1 cent, or 6 cents per sixpack). If your brewer thinks he’s going to get away raising prices by $1.00 (1 dollar per sixpack), over a minuscule increase in aluminous costs, then make my day, go out of business.

2. Beer consumption is plunging, and they’re going to raise prices? Sure, make my day, go out of business. Couldn’t happen to a better guy.

3. If push comes to shove, the can manufacturer might want to buy US-made aluminum, often from recycled products, LOL. And actually, they probably do, and then the tariffs don’t apply, and your story is just made-up BS.

“Time will tell…”

I agree. Just a FYI, When Trump started tarrifs during his first term, the inflation didn’t increase.

I support Trump on tarrifs and agree with WRs stance on this.

Argentina’s crops aren’t looking good, barring some serious rain soon, so that might not be an option for everyone.

This could get interesting if farm exports drop as the result of reciprocal tariffs while farm subsidies to US farmers also drop by way of Elon Musk’s chopping block. That could get a bit awkward for everyone since these very same folks are also likely to be staunch supporters of the current administration.

Trump also wants a weaker dollar. He’ll push Powell hard for lower rates.

B

Biden got kicked out due to high inflation… Bidenflation. Trump will have Trumpflation to contend with if he does what you say, and people will hate him. He can see that too. His billionaire handlers that run the shop have already said that Trump actually wants low LONG-TERM rates, because they really matter, not the Fed’s short-term rates. And low long-term rates require low inflation. The Fed doesn’t set long-term rates, the market does. The 10-year yield (long-term rates) spiked 10 basis points today on this inflation data. Other long-term rates followed, including mortgage rates. And that really matters, not short-term rates.

Funny how we call it Bidenflation when nearly every western economy in the world had the same exact issues post-Covid.

But that aside, facts matter much less to Trump and his followers. We’ve seen over and over again how republicans feel about the economy when a republican president is in vs how a democrat is in (and no its not nearly the same vice versa). In his first term he openly bragged about reducing the deficit when he did nothing of the sort.

He’s playing nice now because its the start of his term but that position will erode the longer he is in power. He won’t be in a rush but he will want to reduce later.

This probably needs address by the White house.

From Politico: The Voters were right about the economy.

Many in Washington bristled at the public’s failure to register how strong the economy really was. They charged that right-wing echo chambers were conning voters into believing entirely preposterous narratives about America’s decline. What they rarely considered was whether something else might be responsible for the disconnect — whether, for instance, government statistics were fundamentally flawed

I don’t believe those who went into this past election taking pride in the unemployment numbers understood that the near-record low unemployment figures — the figure was a mere 4.2 percent in November — counted homeless people doing occasional work as “employed.” But the implications are powerful. If you filter the statistic to include as unemployed people who can’t find anything but part-time work or who make a poverty wage (roughly $25,000), the percentage is actually 23.7 percent. In other words, nearly one of every four workers is functionally unemployed in America today — hardly something to celebrate.

the CPI also perceives reality through a very rosy looking glass. Those with modest incomes purchase only a fraction of the 80,000 goods the CPI tracks, spending a much greater share of their earnings on basics like groceries, health care and rent. And that, of course, affects the overall figure: If prices for eggs, insurance premiums and studio apartment leases rise at a faster clip than those of luxury goods and second homes, the CPI underestimates the impact of inflation on the bulk of Americans.

ru82,

Bullshit article — written for people who don’t know better to rile them up. Clickbait bullshit like this, that then gets spread around endlessly on the internet by these people because it feeds some stupid narrative, should not be funded by the taxpayer, so it’s a good thing that the White House is yanking these taxpayer funds from Politico.

clykke, the difference was that the previous administration actively made it worse by throwing in more money on multiple occasions after it was clear that the spending was unnecessary and going to be inflationary. and when the people called them out, they gaslighted the public telling them how great things were.

ru82’s response is on point. it’s not necessarily the numbers that are the problem, but that people felt poorer and worse off. the current economy is great for the rich and the upper middle, not so much for everyone else, regardless of what pay increases they’ve gotten.

So you don’t think that inflation was high in other countries because (1) they followed similar policies (ie, very loose fiscal and monetary policies, and (2) the US as the largest economy, most important currency, and by far the largest importer of goods didn’t globally impact prices by increasing and drawing forward demand?

Franz G, I do agree, his big signature policies didn’t help the situation. Although it must be said if he had gotten the tax increases he wanted through that would have done. While inflation fell regardless.

And you’re right it is all perception. I had a family member annoyed about property tax increases despite the fact I pointed out to him the increases he was talking about over the length of time he mentioned was below inflation, while his income and investments had all increased above inflation.

The case is the same for many workers, they got wage increases far in excess of cost increases, but they were furious the costs increased at all. Its nonsensical.

But rather than pinning that all on Biden, its worth pointing out how nonsensical it is, they need to realize the logic does not flow with their inherent biases. Instead we have people blaming Biden, with republicans taking advantage of the whole situation, despite the fact many many people were better off. Its backwards.

“the current economy is great for the rich and the upper middle, not so much for everyone else, regardless of what pay increases they’ve gotten”

I’ve noticed my standard of living has dropped about 20% since Bidenflation took off in 2022. All the things I have to buy are up 10 to 12% per year since then. Then there are some shocking increases in home insurance, car insurance, medical ins, property taxes, etc. And how about the dealer prep charge which went from $500 to $800 when you buy a used car from any dealer here in Maryland.

“From Politico”

I stopped reading after that.

It was the foolish reaction to covid …outrageous stimulus…much of it fraudulenty used…not covid itself.

When people talk about interest rates, they should clearly tell us if they are talking about short term or long term rates. These are different animals. With treasuries, the short term rates are determined by the Fed. The long term rates are determined by the market. Wolf has made this abundantly clear.

Trump was probably talking about lowering long term rates, he being a real estate guy. But long term rates will not come down with inflation rearing its ugly head. Some suggest the Fed can lower inflation by slowing the economy by raising short term rates. So, in a way, Trump was indirectly asking the Fed to raise the Fed funds rate in an attempt to lower inflation, which will lower long term rates.

“ So, in a way, Trump was indirectly asking the Fed to raise the Fed funds rate in an attempt to lower inflation, which will lower long term rates”

Seems like this is a fairly liberal (in the literal sense, not the political one, but I am appreciating the irony) and optimistic interpretation of the following statement from Trump…

“Interest Rates should be lowered, something which would go hand in hand with upcoming Tariffs!!! Lets Rock and Roll, America!!!” the president said in a morning post on Truth Social

In the context of his direct statement, he is clearly pushing for something to happen in the short term (hand-in-hand), not as a result of other, more indirect actions which might drive down rates in the longer-term…

Trump seems to be a Rorschach test – he can say almost anything he wants, and then people (particularly his supporters) will often interpret it as something very different, but which conforms better with their own beliefs…

Just dropping by, I think Trump is amusing. He is a kind of shoot-from-the-hip kind of guy, very intuitive. But then later his team have to clarify what “he was really trying to say”. I am sure Bessant (Sec. Treasury) will clue him in on how short term and long term rates work eventually. The only ones who should fear him are illegals, government workers, and criminals, and well they should.

Thurd2, I would bet good money that you are a decent, intelligent, well reasoned person.

As are many other Trump supporters, I am quite sure.

But it’s that “shoot from the hip “style of trumps that allows him to pretty much say anything he wants and then have it translated into just about whatever his fans want to hear.

It’s not all that uncommon for him to say what are generally opposing statements about a particular issue. At that point it’s pretty much like an all you can eat buffet where people go and pick the statements that they agree most with, and Rorschach test their way through the ones that they don’t.

This example of the interest rates is the perfect example. He actually said one thing, but you’ve turned it around almost 180% because you probably can’t imagine how it could possibly make sense otherwise.

In any case, best regards. So often, it’s about the lens we use to look at the world…

Just stopping by,

It’s Bessent who explained what Trump had meant, that he’d meant low “long-term rates,” not the Fed’s policy rates.

Hi Wolf, I was actually referencing Thurd’s statement:

“So, in a way, Trump was indirectly asking the Fed to raise the Fed funds rate in an attempt to lower inflation, which will lower long term rates.“

As well as one of trumps own statements about lowering rates hand-in-hand with the tariffs.

I’m sure I’m losing track of which points of emphasis were in which post, but the gist of things is that I was also replying to his reply to me.

Regards

Just dropping by, Wolf’s concise response is completely in line with what I was saying. Also note that Trump is no longer trashing the Fed as Bessent teaches him about how interest rates work.

In general, don’t get too excited about what Trump says initially. Wait a few days for clarification. Also, Trump is all about makng deals and sometimes making an initial outlandish statement is a way to get the deal making going. The deals he eventually makes usually end up being reasonable.

Thurd

“In general, don’t get too excited about what Trump says initially. Wait a few days for clarification. Also, Trump is all about makng deals and sometimes making an initial outlandish statement is a way to get the deal making going.”

This is exactly my point. It doesn’t really matter what he says, somebody’s going to clarify it, adjust it, make it palatable, or maybe he’ll say the opposite thing, or whatever.

I will go back to the “all you can eat buffet” concept – he puts so much out there that his supporters are sure to find something that they like in almost any issue, regardless of whether or not he says something contradictory at a different time.

Doesn’t matter, they generally will just choose the words/ideas that they feel most comfortable with

and ignore/forget the rest.

I am wondering Powell keeps saying their target remains 2% inflation blah blah…

But why no one asks him how many years have to pass and is he willing to wait to get to that goal?

They’re not in a hurry to get there. They like where they are, higher inflation, higher rates, and higher economic growth than pre-pandemic. Higher inflation and higher economic growth are needed to deal with the huge government deficit and debt. And higher rates are the price to pay for it.

The message is stay underweight long duration. Short duration assets are better pick

So, depending on if we believe the words coming out of his mouth, or we believe the interpretation being presented by his staff while they are performing damage control… he **actually means** one of the following:

– Trump wants the Fed to lower short-term policy rates, which would be bad for inflation and therefore bad for long-term rates.

OR

– Trump wants the Fed to lower long-term rates, over which they have no direct control.

Either way, it seems his macro economic financial literacy is lacking, yet he insists he’s smarter than the Fed voting members and wants to make their decisions for himself. Let’s hope that never happens.

There’s a shortcut: Have Elon Musk destroy the confidence in America honouring bond payments and the USD will become as good as the RUB.

Good thing this will never happen because Treasuries are still the gold standard for pristine, risk-free collateral.

I dont drive much and I pay $1 a mile for insurance. On the plus side the hybrid I bought three years ago is still worth what I paid for it.

if you’re paying $1 a mile for insurance, you either are getting ripped off on insurance and need to shop around, or you drive so little that you’d be better off getting rid of your car and taking rideshares or renting cars for the few times you need it

I would use the same word to describe this report as last months… Broad

Increase almost everywhere. No rate cuts this year.. unless we see job market weakness then emergency 50bips cuts.

I hope Trump actually sticks to doing tariffs but so far looks like a negotiating tactic.

“The CPI for motor-vehicle maintenance & repair jumped by 6.2% annualized in January from December. Year-over-year, the index rose by 5.9%, the worst increase since May.”

We need a reverse hendonic quality adjustment for this category to account for the horrible quality of shop labor these days.

Not only have the prices gone up, but you get sloppy work – missing bolts, bolts not tightened down properly… reusing old drain/fill plugs and crush washers, or re-using bolts without cleaning off the rust… failing to grease or anti-sieze on rust-prone fittings… I could go on.

That car repair inflation is real my car max warranty paid out 7k for repairs on my x5m, glad they covered it.

What kind of work was done for $7K?

Replaced the engine air and rotated the mud in the tires. Threw in a coffee filter check for free. Head rest alignment was advised. Body was dustmopped at the back end.

All that work but you re-used the old flux capacitor?? Shame…

No choice. UPS refused to handle the delivery of the Mr. Fusion from Amazon. Some noise about no profit margins in giving away free energy. Go figure?

Howdy Folks. 2024 CPI 3.1 3.2 3.5 3.4 3.3 3.0 2.9 2.5 2.4 2.6 2.7 2.9 2.9

2025 3.0. I was not surprised by CPI. Were You?

I think the deportations and the threat are slowing the economy.

Finally – the first time I can remember in the last few years – the MSM inflation headlines and Wolf’s take on inflation actually align. After reading MSM’s “uh oh hot CPI” articles in the am, I thought that I’d read Wolf’s excellent monthly CPI report and it would somehow tout a massive progress on fighting inflation. I’m thinking that Wolf was right all along.

WR hit the nail on the spot-The Fed wants the inflation which it prefers to deflation. That seems to be the only way for nominal growth rates, and it dilutes money-such that they can pay back the debt with cheaper dollars. They are not in a hurry…Powel said it in his testimony to Law makers. Seems to me they are willing to pay the price of stagflation, but what do I know…I’m just Dumb money.

It looks like Mr. Wolf was right – higher for longer.

HIGHER 👏 FOR 👏 LONGER

Leave rates alone and increase treasury QT to $50B a month. Keep MBS QT unlimited like it already is. The Fed just needs to sop up all this extra cash sloshing around since 2009.

Compliments to the author’s writing. Both AP and WSJ switch between annualized, quarterly and monthly percentage changes and fail to report the comparison time period.

Reducing liquidity avoids the headlines of interest rate actions associated with tightening monetary policy by the Fed. Yet the Fed is only modestly reducing liquidity. Oddly, we have a stock market that is creating more wealth than the Fed can absorb through its QT programs. A self reenforcing trend for inflationary pressure. The pendulum will change directions, it always does and the daily chaos created by this administration is doing nothing for this investors confidence in the stability of our nation or markets.

No small wonder that gold prices and gold mining shares are going up.

the stock market isn’t wealth. wealth is productivity.

Tell that to the guy that buys a new pickup truck because his Robinhood account has gone up 200%. Somebody built that truck, somebody supplied the resources and parts to build it. Consumption is stimulated through the “Wealth Effect”.

i didn’t say that the stock market can’t create a wealth effect. but that’s different than saying that asset bubbles themselves are wealth. they’re not.

wealth is about a society’s ability to produce.

That guy’s an idiot then. Unless he actually locked in his gains and sold to fund the truck – in which case he’s still an idiot.

Cashing out of an appreciating asset in order to overpay for a depreciating asset is wealth destruction plain and simple. Nothing wrong with splurging $$$ if one has the means, but that’s what it is.

Interesting discussion. I think that we have different definitions of wealth. I define wealth as an individuals security in their ability to provide security for themselves and their family. The asset we build cart our wealth so to speak. When I consider your perspective I see the connection that a society can perceive its wealth as its ability to produce. Constructive in both definitions!

Respect!

i guess he’s my theory. suppose, in a ridiculous hypothetical, that every working person died at once, and all you were left with were retired people with tons of assets.

those assets would immediately become worth nothing. assets are only wealth to the extent that they can be traded for actual productivity, or money that is then traded for productivity.

i realize that it’s an academic discussion, but if the stock bubble pops and loses half its value, society hasn’t lost half its wealth, because those assets could not be traded for productivity in any large number, or the prices would go up.

what makes a society “wealthier” is more output per person. not asset bubbles.

let me know if this makes sense, as it’s hard to put my thoughts into words.

“those assets would immediately become worth nothing. assets are only wealth to the extent that they can be traded for actual productivity,”

I think this is only partially true – you need to differentiate between assets with inherent value and those without.

In your example, things like stocks, gold, and buttcoin might become truly worthless, but what about houses and vehicles? Food, gasoline, alcohol, other consumables…?

People can still trade between themselves to keep the value afloat if the thing has enough demand due to it its inherent usefulness.

NB, I agree with your general sentiment that bubbles are bad and we’re in one rn.

During the U.S. Golden Age in Capitalism (which was not optimized), the annual compounded rate of increase in our means-of-payment money supply was about 2 PER CENT. And during this same period, 1955-1964, the rate of inflation, based on the Consumer Price Index, increased at an annual rate of 1.4 PER CENT. Unemployment averaged 5.4 PER CENT.

Powell has a long, long, way to go to get rates down.

There’s been several comparisons of today’s inflation trends compared to the 1970s. When you compare the two charts the similarities of the graphs are stricking. Would you look into this and let us know your thoughts in a new post? Is it just a coincidence that this decade of inflation is following the exact same path as the prior decade?

When put on the same axis, there are scant similarities between the 1970s inflation and today’s inflation. History doesn’t like to repeat itself. It tries to come up with a new thingy each time.

Sure, if you make a left axis for the current period and a right axis for the 1970s to manipulate the magnitude just right, and two x-axes to manipulate the time line just right, you might be able to move the second y-axis and the second x-axis just right until it overlays somehow. But that’s fanciful bullshit.

Big bouts of inflation tend to come in waves when measured yoy (that’s part of what yoy calculations do). But beyond that, forget the similarities. The causes were different back then from the causes today, so you can expect the result (inflation) to manifest itself differently.