30-year Treasury bonds sold at auction on Friday at highest yield in at least 16 years despite Fed’s 100 basis points in rate cuts.

By Wolf Richter for WOLF STREET.

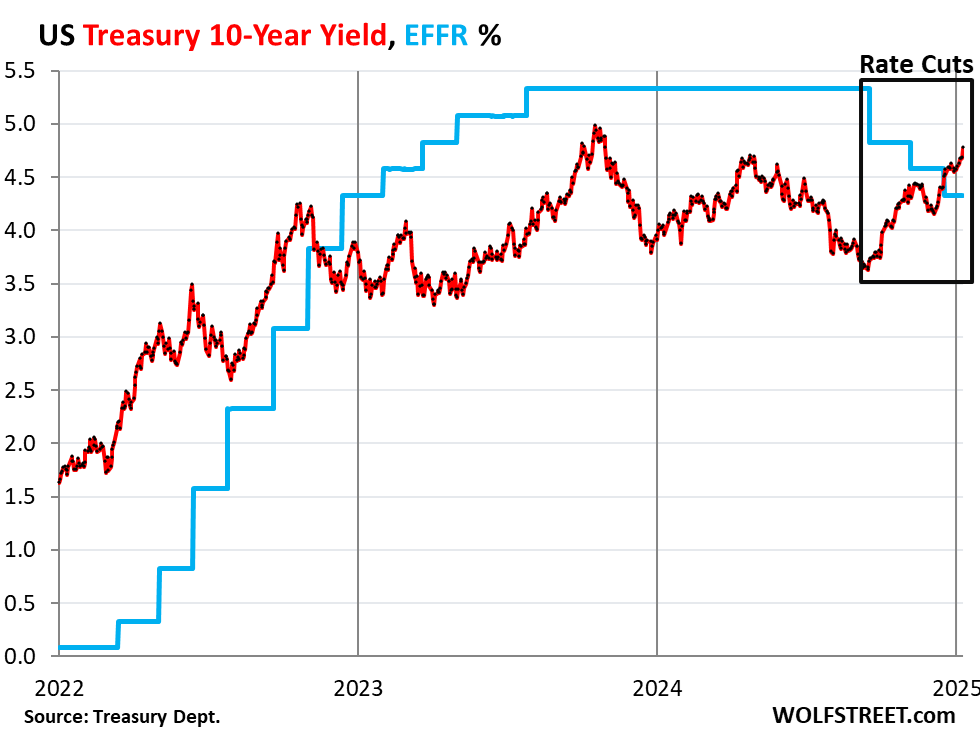

Since the Fed’s 100 basis points in rate cuts, the 10-year Treasury yield has risen by 114 basis points, including by 9 basis points on Friday, to 4.77%, the highest since November 2023, upon news of a continued solid labor market in an economy that is growing substantially faster than the 15-year average growth rate, with inflation re-accelerating in the wings. And seeing these upside risks to inflation, the Fed is gingerly shifting back into its wait-and-see mode.

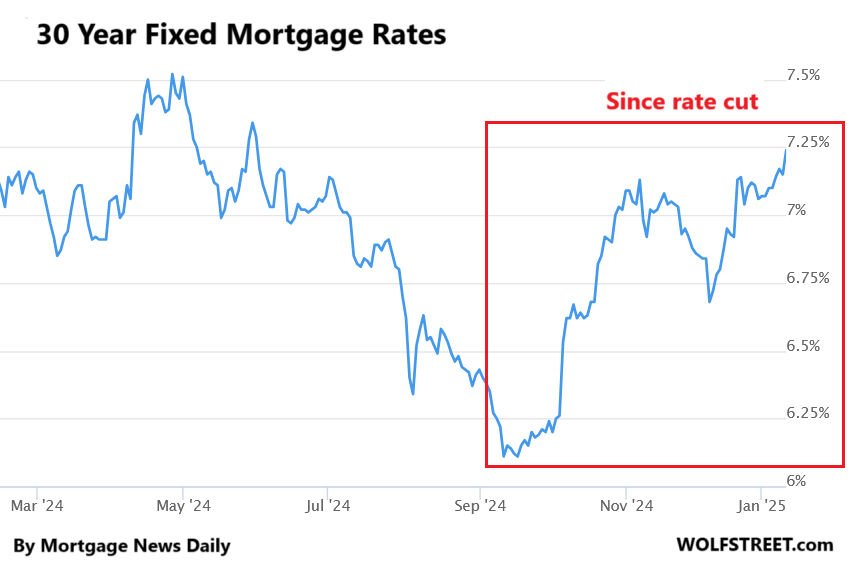

Also on Friday, the 20-year yield rose to 5.04%; the Treasury Department sold 30-year bonds at auction with a yield of 4.91%, the highest auction yield since before the Financial Crisis; and a daily measure of mortgage rates rose to 7.24%.

The Effective Federal Funds Rate (EFFR), which the Fed targets with its policy rates, has remained at 4.33% since the December rate cut, down by 100 basis points from the pre-cut levels (blue). I’m not sure we’ve ever seen anything like this before – a 114-basis-point surge of the 10-year yield while the Fed cut by 100 basis points – but there’s a good reason for it.

The reason for this phenomenon of the Fed cutting by 100 basis points while longer-term yields soar by over 100 basis points is the unusual situation the economy went through, and why the Fed cut rates.

Normally the Fed cuts rates when it sees a recession on the horizon. And the bond market, also seeing a bad economy ahead, begins to send longer-term yields lower.

But this time around, the Fed cut without a recession in sight, with a solid labor market and above average economic growth despite the highest policy rates in decades. It cut by 100 basis points because inflation cooled a lot from 9% in 2022. But it cooled a lot without a steep recession and big job losses, it cooled despite the economy growing at an above-average rate, which is another rarity. It caused major recession predictors that normally work well to produce false positives.

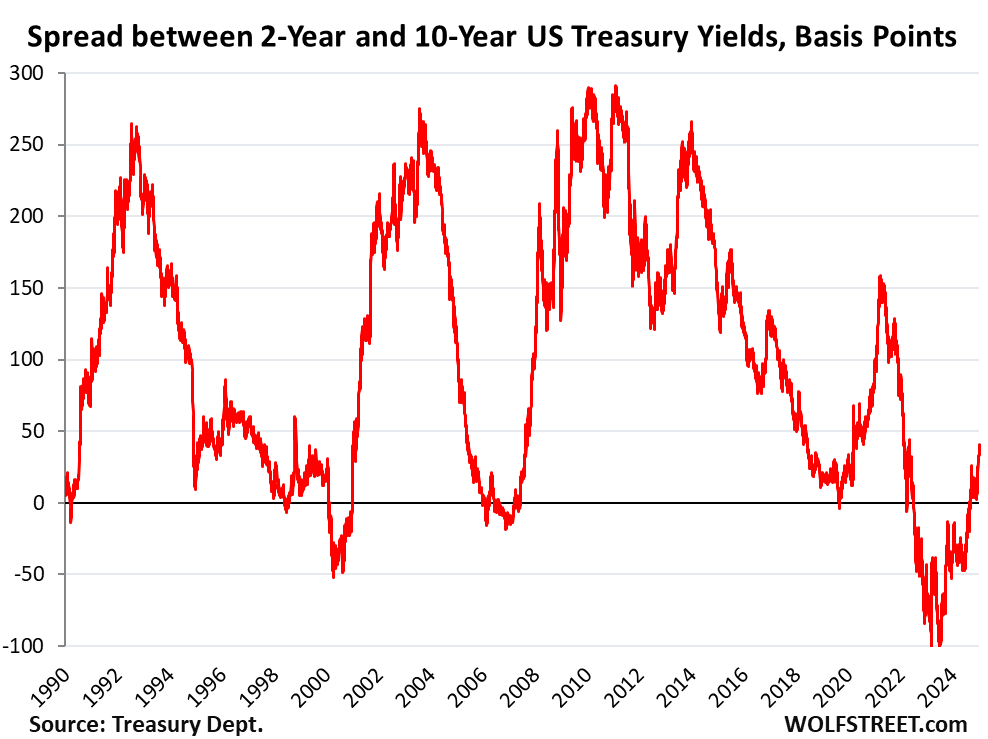

The yield curve un-inverted last year and is steepening nicely.

Short-term yields haven’t really budged since before the December rate cut, which had already been fully priced in at the time. Now there is no more rate cut priced in within the short-term window of those securities before they mature. For example, on Friday, the 3-month yield was 4.32%, same as in the days just before the December rate cut.

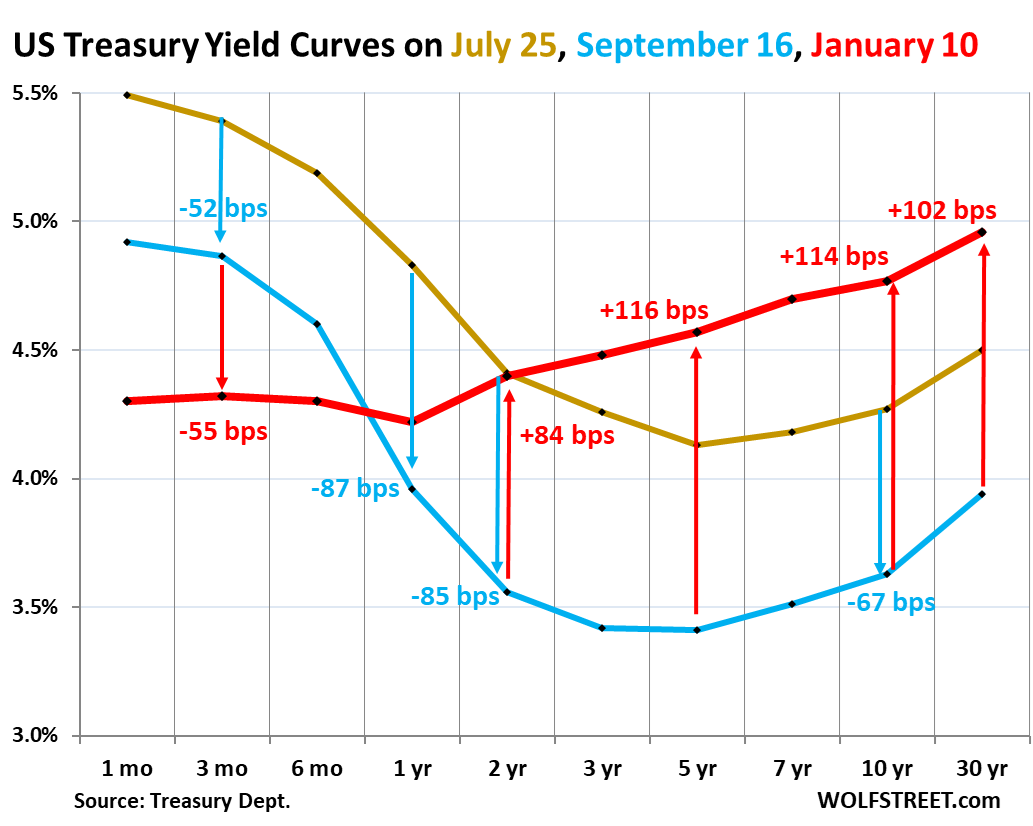

But everything from the 2-year yield and longer has risen substantially since the rate cut. This caused the yield curve, which had gracefully un-inverted entirely just before Christmas, to steepen.

The yield curve had inverted in July 2022, when the Fed’s big rate hikes pushed up short-term Treasury yields very fast, but longer-term yields rose more slowly, and so the short-term yields blew past them.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: July 25, 2024, before the labor market data spiraled down (which was a false alarm).

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

- Red: Friday, January 10, 2025.

This yield curve is getting closer to looking healthy again, though it remains relatively flat and the steepening process still has some ways to go:

The yield curve is still fairly flat and has some ways to go.

With a spread of only 37 basis points between the 2-year yield (4.40%) and the 10-year yield (4.77%), the yield curve remains fairly flat. A spread of 100 to 200 basis points is kind of the normal range, which could happen either with the 2-year yield falling or the 10-year yield rising, or both.

For example, if the 2-year yield remains at 4.40%, the 10-year yield would have to rise to 5.40% for the spread to widen to 100 basis points.

The relationship between the 2-year yield and the 10-year yield is inverted when the 10-year yield is below the 2-year yield, and the spread is negative (below the black line).

The 2022-2024 yield curve inversion broke all kinds of records in terms of length and depths. And the un-inversion is just at the beginning stages.

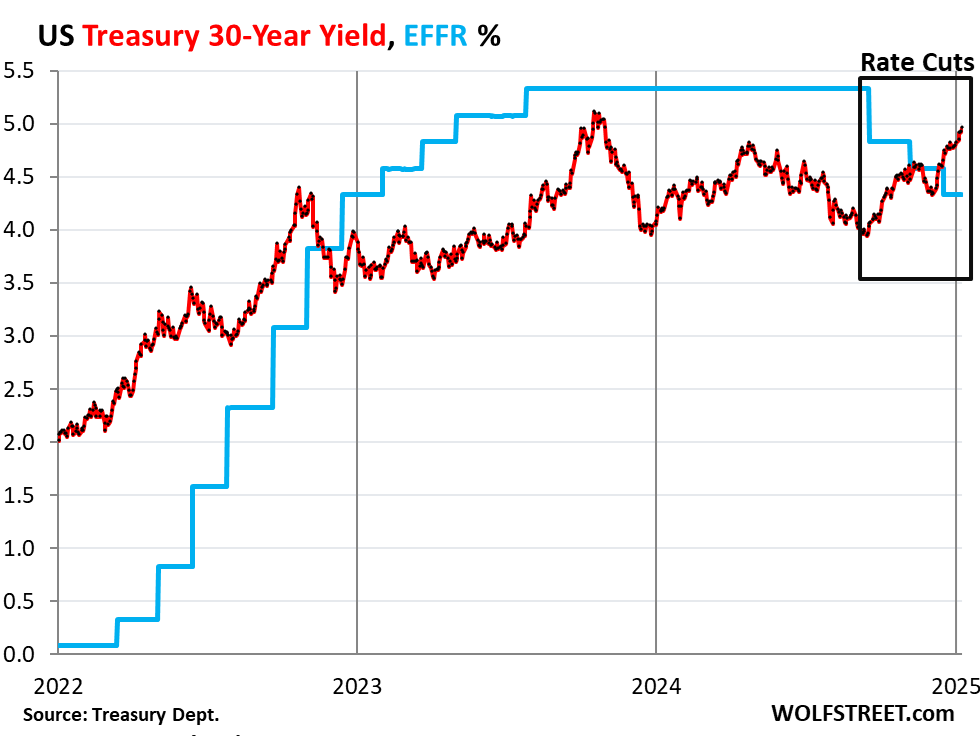

The 30-year Treasury yield rose to 4.96% in Friday’s trading, the highest since October 2023, and except for those few days in October 2023, the highest since September 2007. This is a “constant maturity yield” that is calculated from various trades based on a formula.

But at the Treasury auction on Friday, the government sold 30-year bonds at a yield of 4.91%, the highest 30-year auction yield since at least 2007.

The 30-year auctions in September, October, and November 2023 produced lower yields. The October 2023 auction marked the high with a yield of 4.84%, 7 basis points below Friday’s auction yield.

The 30-year bonds are normally sold with a substantial term premium, as investors demand to be compensated for taking the risks that inflation and interest rates might rise over the 30-year period. Before the rate hikes started in March 2022, the 30-year yield was about 200 basis points above short-term yields. That’s the term premium. Currently, the term premium is about 60 basis points. So there is still a long ways to go.

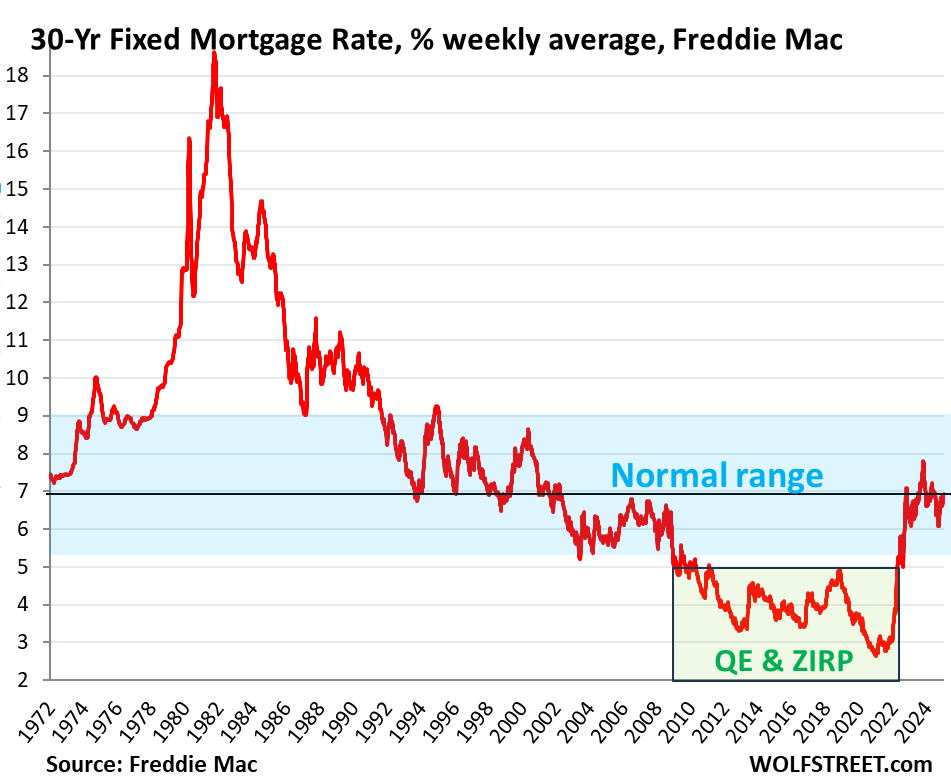

Getting used to the old-normal 6% to 8% mortgages?

Since the initial rate cut in September, the average 30-year fixed mortgage rate has risen by 113 basis points, to 7.24% on Friday, according to the daily measure from Mortgage News Daily. Mortgage rates generally track the 10-year Treasury yield but are somewhat higher.

Freddie Mac’s weekly measure of the average 30-year fixed mortgage rate rose to 6.93% on Thursday.

Over the long term, the average 30-year fixed mortgage rate didn’t drop below 5% until the Fed started buying MBS in early 2009. Trillions of dollars of QE and near-0% policy rates eventually pushed mortgage rates below 3% during the pandemic. Those mortgage rates were quirks of history and are unlikely to come back. So maybe it’s time to get re-used to these mortgage rates that were normal before 2008.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If it is time to get reacquainted with rates of 08, then where are the prices of 08? Greed son. Just greed all over. No one can fathom taking a loss … but they will. Everyone takes the loss in one way or another. Even the vast swath of boomers without grandchildren. Pretty sure they don’t care and would rather play pickleball.

Well, first of all, there’s been inflation (and there needs to at least some small amount to keep capitalist economies functioning well). Compounded over 16 years, that’s going to give you noticeably higher prices. And for housing specifically, Wolf has consistently argued that owners are holding on to houses refusing to accept that sellers are no longer buying at the same high prices. Once owners capitulate, we’ll see housing prices come down more substantially.

Median home prices have increased more than 2x inflation since 2008. We would need housing-crisis style price drops to bring them even close to the levels inflation would predict.

The owners will capitulate on price only once they need the money from a quick sale of their home. Driven by financial necessity, and shaped by larger market forces, they will take their diminished places in the tapestry of the economy with poorly disguised ill will.

Great keep rates higher. Good for savers, good for the dollar and helpful for inflation

True. Bad for interest expense though.

Good point, should interest be taxed as a capital gain instead?

Speaking of cap gains, why aren’t they indexed for inflation? Soc Sec benefits have been indexed with COLAs since the 70s!

The bond market at least is acting as it should: signalling risks and costs (of credit) through a market mechanism, rather than being snowed under by the noise of a hyperactive rate-cutting, asset-warehousing Fed, as it was roughly ’08 to recent days. It will take awhile for this to shake through the economy, there will be somewhat lucky/unlucky winners and losers (though often, depending to some degree, a hopefully increasing degree, to their own prudence and discipline), but hopefully the trend continues.

I agree, and no more QE, that’s what got us into the mess we have now IMO!

FED needs a recession to get out of this.

A recession will ballon the deficit.

Anything balloons the deficit. Good times, bad times.

Ballooning the deficit is the only option now for the US economy. Just know how and when to jump ship.

The national debt is only 36 thousand billion dollars. That’s not much, right? It’s unrepayable, which is why the goal is now inflation.

There is theoretically a way to thread the needle by some combination of inflation, time, and new production. It would mean partly paying the debt and partly inflating it away. But we have gone pretty far down this road, like the family that kited credit cards and checks. There is a hangover and a restructuring of behaviors and markets. If you didn’t get to take part in the big drunken punchbowl party, well, we are where we are. Recovery has to happen some time, which is a time of discipline, absent some new miracle of productivity. I’ve been living with limits and austerity my whole life, thank you.

Never happen with consistent high employment numbers. Plus, didn’t Yellen say “no more recessions”?

Same Hellen that apologized for spending trillions .lol

Excellent summary of the constellation (issuers and maturity) of US government issued/backed interest rates.

Given the failure of the government-backed mortgage subsidization efforts of the late 20th century (culminating in GFC, repositioning of FNMA and Freddie under government wing, and previously unthinkable purchases of mortgage paper by Fed), is there any chance that the government one day swears off of the mortgage subsidization business?

Much pain has come from government direction of mortgage lending…

During/After the GFC, the government became custodians of Fannie and Freddie after bailing out banks who gave too many residential mortgages with too loose standards. The officers of these banks are now living on their yachts since nobody was held accountable. To be fair, these banks paid back their bailouts over time with the generous help of the Fed lowering rates and QE. My loan was owned by Countrywide who failed and was acquired by another bank. My only hassle was mailing my check to someone new. Nobody lost my loan in the chaos.

Now that the US government owns and backs the majority of home mortgages, I only feel a little safer. If things crash again, the results will be the same and I will just have to mail my check to someone new. The difference may be the number of snowballing foreclosures. The government will step in with programs to bail out the mortgage holders rather than the banks like last time.

The new US government is looking to kick the GSEs loose again. Does this mean the government will not be backing mortgages? Does it mean more bank CEO yachts and another snowballing of foreclosures before the government steps in?

Another thought.

If the new US government no longer backs residential mortgages like they did before the GFC, there is more implied risk with anyone offering home mortgages.

Mortgage rates will very likely go up.

In a sane economy, home prices will go down.

Bob E.-

“Now that the US government owns and backs the majority of home mortgages, I only feel a little safer.”

Not sure how the government owning or backing one’s home mortgage makes the borrower any more “safe.” Federal loan guarantees help the lender in the event of default, and they help the packagers of mortgage securities belch out more MBS, and they help realtors sell more homes at ever-rising prices. But if your original mortgage provider hits the skids, it’s a certainty that some new entity will stand ready and eager to accept your monthly principle and interest payments. You will still own the house, and still be obligated to make the payments, won’t you?

I think I must be missing your point on this.

I agree with you on the connection between less subsidization via the GSE’s in the mortgage industry and higher mortgage rates, and that this could/should prompt a re-examination of the residential real estate valuations. The decline in home prices you predict is the fondest wish of many WS commenters.

John H,

Sorry, I could have been clearer.

If I continue to pay my mortgage, other than sending the check to a new address, there is no change.

The problem would be if I lost my job and couldn’t pay the mortgage and couldn’t sell if the house was underwater.

In 2008, mortgages were not backed by the US government. Banks foreclosed on underwater homes and the mortgage payer was kicked out. If the bank failed, then another bank picked up the assets for pennies on the dollar and sold the foreclosed house at a fire sale price. Housing prices crashed causing more foreclosures. The bigger banks were bailed out with taxpayer loans. The mortgage holder lost the house and whatever down payment.

Since the government started backing loans, given the forbearance during the pandemic, I think the government will forebear payments rather than take the house and kick the mortgage payer out and sell the house at a discount. It would come at huge taxpayer expense but it may avoid another GFC.

BobE –

I see what you mean.

To me, the knock-on effects* associated with a policy of broad-based foreclosures, are even more scary that the prospect of a disorderly home-prices market. Relying on foreclosure relief would be nearly as damaging to market discovery as relying on the “Fed Put.”

* effects include the co-opting of property rights, disassociation of consequences from the actions of property owners, bond market dislocations, inflammation of inflationary fears, etc.

Well, with those rates should be a correction in housing prices soon , just checking Miami, one of the most inflated markets, according to Redfin Data until January 5 2025 (months of supply) 53 weeks, (national average) 17 weeks, for this last report you can see a decrease in prices as well, and it’s happening fast

Miami numbers are skewed because of the 30 year old condos being dumped on the market. These are the condos that didn’t get appropriate maintenance for 3 decades. New regulations require that professionals be hired to evaluate building conditions. Without maintenance, buildings decompose – sometimes slowly, sometimes abruptly.

In hindsight, having volunteer condo boards for 30 years wasn’t the best idea. It’s one of those things that . . . seemed like a good idea at the time.

And now, people that opted for that are paying the price ( a drop in values) for 30 years of deferred maintenance. Owners are bailing out because the total of all the costs (inspections, required reserves, repairs, monthly fees, insurance, taxes) is overwhelming.

If values drop far enough, the units will either be scooped up and rehabbed (if salvageable) or demolished for land value.

Frankly, I don’t think anyone really knows where all of this is going. Between the new political regime, budget deficits, recent major climate impacts (Hurricane Helene, LA wildfires), Ukraine, Israel/Gaza, Iran, Syria, China, Russia, BRICS, and so on, there seems to be a plethora of moving parts.

CHAOS

My read is that almost all of these things you mention imply higher future interest rates.

Not to the FED.

The long bond market is always worried about inflation. The fed slashing 100 bp in the face of a strong economy increases their worries. The 20 year yield is over 5 percent now, but the spread between it and say the three month bill has to go higher. As wolf said, the curve is still relatively flat. It needs to steepen, which means long rates have to rise, which is happening. A substantial premium has to be paid to account for inflation risk over a ten to thirty year period.

I am waiting to enjoy the same benefits my Silent Generation parents had in the 1980’s! Go 18% 30 year and then I can retire like dear old dad and grandpa.

Us Boomers need some break to live better than previous generations.

I wouldn’t count on it. First off, the US 30-year bond has NEVER hit 18%… it was briefly above 15% for a short time in the summer of 1981 but even for that year the average 30-year was 13.34%. Sounds great until you realize that their very high 30-year’s came as a result of a preceding DECADE of 6-13% inflation… and only worked out for their retirement in the 1980s because inflation dropped below 4% for the next FOURTY YEARS starting in 1982.

25-30 years from the year you take Social Security is a long time to plan for… but it is how long a retirement lasts. There is nothing wrong with putting yourself in a POSITION to “seize the day” if those conditions recur near your retirement date… save up a lot of cash and do your spending (house, car long-term care insurance) now while interest rates are low… but it isn’t the situation you should PLAN for because it is not likely to recur. Nor is it the situation your father and grandfather thought they were getting into when they retired in 1983.

Great! I want to buy a house, can pay cash, but refuse to pay these inflated prices. Home prices should come down, now whether they do…

Yup, just hold on a moment. People thought I was nuts in 2006 for not buying. I would just show them the Schiller home price index graph. They would say “there’s never been a housing crash.”

Nah this time is different as they say..so far they have been right, just like how all traditional forecasting tools have failed…yup this time is different

They are right until they aren’t anymore. Even if we avoid a recession and tons of job losses, there’s still an insurance market thats careening towards a collapse and a STR bubble popping as rental prices go up and more cities limit the number of units.

With appreciation slowing, all the above starts making residential real estate less attractive to investors. Get the investors out of the market and price discovery can happen.

I’m in the same boat.

If there is a recession or depression then prices will come down.

From all the research I’ve done it looks like we’re in the everything bubble and it’s just been pumped and pumped and pumped and now it looks like we’re at the point where they can’t pump it anymore.

The 10-year and 3-month and 2-year have both uninverted and are climbing higher, and almost every time this is happening a recession followed with in the year.

Keep your cash ready in that high – yield savings account and when we’re at Rock bottom when all the news media are telling us it’s Armageddon and the world’s coming to an end, that’s the time to deploy your cash. Cuz you know what will happen next, the fed and government will come in with bazookas shooting cash in every direction and they will inflate your purchasing power away again.

I think more and more people are starting to get onto this scam or whatever you want to call it is Ponzi scheme all the people at the top know how it works.

Glad I bought rather blindly in 1994. Interest rates were rising, and nearby, Orange County CA was going bankrupt as a result. Also ignorantly I took the option for a floating rate mortgage (lower monthly payments), but then the interest rate increases flattened and I came out OK with my dumb luck, again being bailed out in ’08-’09 with the Fed’s interest rate suppression (until I got a little wisdom and converted to a fixed, very nice as I recently paid off that mortgage). Who knows what I would have decided? I will tell my young students, I didn’t start into a house until I was 37; when I came out of school, interest rates were double-digits. We wondered how we could ever get anywhere. Housing prices had inflated crazily. There will be no perfect moment.

Elsewhere, I have the (wild?) conjecture, some segment of organized elite investors may decide at some point to do another roll-up of housing stock, maybe as a hedge against the disruption of AI? Real assets are hard for chat bots to duplicate or scale up like digital stuff.

@John Daniels: I couldn’t agree more about being very solvent, savings or short term treasures (6 month max), as there is just waaay to much exuberance in the market today. Why? According to FT, the “exceptional” US is drawing funds at a rate of over $1T yearly from other financial markets.

How will the rest of the world look at the US in 3 months? 6 months? a year?

What happens if they start to pull out?

Time to be safe, my friend.

I think most don’t realize ho unusual the US housing market is–specifically with true fixed rate mortgages.

Anywhere else in the world, when you agree to a fixed-rate mortgage, you agree to X years of payments at the agreed interest rate. You can prepay, but you still owe the interest. Most buyers have adjustable rate mortgages and refinancing isn’t really a thing, as you still have to pay off the interest you signed on for.

Adjustable rate mortgages naturally adjust to the level of economic stress an economy is under. There is a recession and the Fed cuts rates? Great, your monthly mortgage payment goes down. Inflation is up and the Fed raises rates? Property owners have their spending power reduced through higher mortgage payments.

It’s a real weakness in the US system in my eyes. All these lock-in effects and similar that discourage true market dynamics.

Here, here. I know my home isn’t worth what Zillow says it’s worth. That tells me the rest of the market is much the same…15-20% correction is coming. If not, too bad, I’ll stay here and pay off my mortgage. IDGAF. 😬

We are in that boat as well. Ready to retire to a slower lifestyle away from major urban Socal, but not going to pay these prices.

Is it possible to say that the 30y has now after 16 years officially moved beyond the Financial Crisis of 2008, and other rates will slowly follow? A very steep and straight curve from 4% to 7% might be here soon. That red line, currently labeled “January 10” might tilt more and more with each passing month. Sort of like the Titanic standing up in the water..before it broke in half and sunk.

I like normal

Since the interest rates and mortgage rates are returning to normal, over valued equities, houses, services etc might have to adjust and if i might add – learn to believe in gravity. But the economy has pulled so many surprises in the past 3 years so predicting anything at the moment is a fool’s errand.

I don’t think anything other than market sentiment matters for the S&P. Price is market sentiment reflected in a chart. We think it’s earnings/rates etc… yeah for people who care about that stuff… like valuation… but the stock market has proven again and again it doesn’t care about that unless it’s a small cap equity. Once sentiment changes, ie everyone ASSUMES it’s going downhill from here and begin to sell, that’s when things finally enter recessionary period. What will it take till we get there? Who knows.

It will take a selloff or significant bear market in which the federal reserve and/or US government does not enact any policies to stop it and/or remedy it. This will demonstrate to people that the risk is actually owned by them, not government or taxpayers, and they will not be as inclined to participate

That happened by 2012 in the housing market,

A 10% plunge per year from 2008-2012, caused many speculators to find another market. My teacher friends were finally able to buy a house to live in. Now they’ve retired and sold with a boatload of cash to live on.

They found another market alright. The stock market

The smart speculators got into the housing market in 2012…

The expansion of the American Empire over Syria, Greenland, Iceland and Haida Gwaii etc. will create the basis for the next leg of the forever bubble in U.S. equities and R.E. All the world is a stage. And all the other pseudo-sovereign states are simply tributary / servitor states to the United States.

There are the endless rounds of marketing messages from AI purveyors to add to that lovely levitating gyrating bubble. As in the dot com era, the promoter rock stars have certainly become experts at the promoting side of it.

There are a lot of people saying now that the. We normal of 6-8% interest rates are just a return to historic rates so don’t worry about it. I would just like to point out that when rates were last this high back in the early 90s, real estate, especially in places like California, was much cheaper relative to annual household income and that made paying a high interest rate possible. Back in the 1990s you could buy a home in a good neighborhood for around $200,000. At the time, a good income would be around $40,000 a year, so that was a multiple of about 5. Today that multiple had doubled in places like San Diego, so while the average income in the county is now about 90,000, the median home sells for $1,000,000. That is a multiple of 11! When you combine that with a 7% interest rates it makes a house totally unaffordable. You can easily do the math. Just looking at simple interest to make the point, 7% on $2000,000 was $14,000 against a 40,000 income. That’s a lot bit possible to pay. On the other hand 7% on a $1,000,000 is $70,000 against an income of $90,000 (not counting down payment here to make my point). Something here has to give.

Agreed. I am in North County San Diego and have watched my own home go up 40% just since the beginning of Covid when rates were dropped to 3%. My dad purchased a home in the East Bay (Cali) for $200K in 1985. His salary that year was ~$50K (4x multiplier). That same house today is ~$2.5M per Zillow etc, but last sale on the books was $2M in 2020. With an average family salary of $250K in that area the multiplier is now 8-10x the salary which I think I read in a previous article that California as a whole is the most expensive state when comparing average income to avg. home prices with about an 8x multiplier (salary to home price).

Your example on the 7% on $1M also doesn’t include the fact that you would also be on the hook for property taxes on 1M as well as Insurance and potentially HOA as most of the newer properties here are going to impose that as well as potential Mello Roos in many area (newer homes in Carlsbad and San Elijo/San Marcos) which would actually bring the effective payment to around $8 – 8500 per month.

We, like many of our friends in this area, are now “stuck” because while I have a boatload of equity in my current place in doesn’t make financial sense to move and take on another payment and higher tax rate as the prices are now so inflated it wouldn’t even make sense to attempt to “downsize” as long as we choose to stay in this area.

You’re seeing quite a bit of the “remedy” now: current homeowners, especially fixed-income ones, can’t find buyers for their $1mill properties, and they can’t just take a hit and move because ALL properties are $1mill properties.

They can take the hit if they want to move to some little rotted-out town in flyover country.

Lol, some rotted out town? Get over yourself. You are talking about the extreme outlier prices. Almost anywhere in the country is cheaper than $1M. Sell that and buy something pretty nice basically anywhere else for $600k and they’ll still have several hundred thousand left after they pay taxes on the difference, to live their life. That’s a lot of tangible money for food, maintenance, medical expenses, and travel. To be house poor just to be in the area you dream of and then can’t afford to actually do anything, is complete idiocy. That’s not living.

I would say a rotted out mind is the real problem here. Couldn’t make it on $1m? I see a Go Fund Me page in the near future..

Strike “rotted-out” and insert “lower cost” and you have the right idea…

Yes, prices are way too high in relationship to incomes and should come down. It’s the prices that are abnormal, not the rates. Rates returned to the normal range, now prices should return to the normal range. That process already started in a bunch of expensive cities.

Help me think about this. I realize I risk the wrath, but I come here to learn / understand. Are houses prices too high? Are houses unaffordable? I’m reading the articles and the comments. Everyone claims “Yes”. But I wonder, and I have a question “is occupancy a good indicator of affordability? This site frequently references CRE occupancy / vacancy and class of structure. It’s insightful and we know it’s bad. Is there similar data for single residential? If”good houses’ were unaffordable, wouldn’t they be vacant? Is vacancy a good indicator? Is vacancy an issue? Thanks.

I don’t follow your logic. But in terms of vacancies: About 14.5 million homes are vacant. About 11 million of them are vacant year-round. The rest are vacant seasonally (Census data).

With the folks now in charge at the federal level, the disclosure rule that would require RE money launderers-investors (many buying vacant properties, kept empty and pristine and used as collateral for loans as part of laundering) to identify themselves to Treasury, will presumably be shut down. It has long been a handy loophole big enough to float an aircraft carrier through, used by international flight capital, people in dodgy businesses that might bring out huge cringes. South Florida I’m told has many of those; New York City too. There is no vetting as banks have to do if someone just shows up with a truck full of cash. Funny thing, plenty of those types of “sophisticated investors” ran a lot of cash through casinos, not least in Atlantic City, back in the day, if one is wondering where some now well-placed Americans enhanced their fortunes. (Not that Delaware was unaware of similar tools also, hey Joe.) Toss crypto on top of that mess, maybe with a little AI strategic legal arbitrage-enhancement, and I wonder what the earnest “little guy” can expect in many RE markets. The much maligned help the feds once upon a time provided to have and sustain a domestic middle class, might seem quaintly appealing. But we have gone so far down that road. Here we are.

After reading those two comments, it seems to me that the word “terrorist” really ought to be redefined……it’s obviously a continuum, not black and white, either or language.

Then again, very little language (if any) or even math is.

Very fluid, this life stuff…….but we are 70% water rocks, and therefore change faster, so it’s kinda to be expected.

Cheers!……..to all the Gooey Rocks that are in the middle of a lasting terrorism continuum , or striving for it….

🙏🙏🙏🙏🙏🙏🙏

I bet when we hit rock bottom there’s going to be like this huge relief, it’s like a lot of people see it coming but it’s like will it ever get here is it ever going to happen, and it always has throughout history so it’s just a matter of time, got to be patient.

I started looking for a house way too long ago I’m too embarrassed to even say.

After my divorce I didn’t have a house I lived in an apartment and paying child support and just trying to survive for many years and then once I had money saved up I started looking at prices and they were going up.

So I thought well, I’ll just keep saving and then at some point when it levels off I will finally be able to buy a house.

Well you know what happened, the market went up went up like rocket fuel, like the biggest rocket ever invented and it just continued to go up and then when you thought it couldn’t go up anymore it went parabolic on the covid stimulus super pump.

And all the time I’ve just been sitting on the sidelines thinking what the heck has happened. To me it feels like I’m living through what people in other countries have lived through when they have hyperinflation, I know we haven’t had hyperinflation but I can see how they felt in a way.

Just stay in your apartment for a while longer, and enjoy Treasuries (short term) while looking Wolf’s charts on declining real estate values.

I tried to get a loan for a house in San Clemente CA, a block from the beach, in 1998. 179,000. My income was good but I was self-employed and single and the bank wouldn’t do the loan (remember those parameters way back when?!). But I thought ok I’ll just work another year and give the lender 30 percent down. Another year and the great bubble had already doubled the price, by the time I moved from my apartment in 2003 the house was listed at over $1,000,000, lol.

Now I think the real reality is showing ! You can’t escape to anywhere! The state or local taxes become the catch all just when you thought you were free! To think we created America to escape the kings tax only to get the king,queen,and the dukes tax only! Home of the free and brave my arse

How will home prices drop without mass job losses ?

In the US housing bust, the plunge in home prices starting in 2005 in some markets and in 2006 in other markets led to the mortgage crisis which led to the Financial Crisis which triggered the mass layoffs and the Great Recession starting at the very end of 2007/early 2008. At the beginning of 2008, the unemployment rate was only 5.0%. It hit 10% in Oct 2009. It’s the housing bust that triggered the Great Recession via the financial crisis, not the other way around. Employment was still strong when the housing market began to topple.

Anton – “On the other hand 7% on a $1,000,000 is $70,000 against an income of $90,000 (not counting down payment here to make my point). Something here has to give.”

– (Existing) house prices are still (mostly) at sub-3% mortgage rates, when said rates are now around 7%. What matters to the shelter-buyer is the monthly “nut,” the monthly mortgage payment. Rates go up and prices go down, and the “nut” remains about the same. Existing / resale / used house sellers will need to cut prices accordingly. In my view, in order to return to at least some sense of affordability, all of the pandemic house price gains need to be erased, which of course isn’t a popular view with existing house sellers and the REIC.

– New house sellers (i.e. builders) are of course not not immune to the current high prices and are providing incentives as well as price cuts, but there’s still a long way to go for price cutting in both new and existing house markets.

– The .gov (including the Fed) “wealth effect” since the GFC and then the .gov pandemic response did this. Free markets would have been just fine, but we have central planning, just like the former USSR, with expectations for similar outcomes without a return to something approach free markets, vs. interventionists.

Yes…I bought a very nice home on 1/2 acre for 2X my modest blue collar wage. 1987. I think the house would fetch 1 million, now. Or about 12X the same salary adjusted for inflation.

Something’s got to give/ Yeah, rent will go upl

Nah rental supply is rising and rents are dropping. This will continue unless the construction boom ends or immigration picks up, it appears. High prices seem to be solving high prices.

Where I am, I’m seeing rental prices dropping back down to where near what I paid years ago, which is a huge step

Rates above 7% will kill the housing market until the prices come down

across the board. That’s not a bad thing

unless your wealth is tied up in real estate.

I don’t invest in bond funds or bonds anymore. The sharpe ratio is negative. I use SGOV exclusively now for cash holdings and fixed income allocation. Given the continued debasement of the US$ I don’t want to hold treasuries long. I want to be an owner not a lender. Bitcoin and equities are my major holdings.

SGOV is my cash account too. I used to ladder actual Tbills, but ran into liquidity issues with some CUSIPs that my broker wouldn’t let me sell. And the added benefit is you can “deposit/withdraw” in increments of $100 instead of $1000.

I also wouldn’t touch duration with a 10 foot pole.

“I want to be an owner not a lender.”

But lenders (bonds) are higher in the capital structure than owners (equity).

Pundits in the media and financial advisers have been consistently wrong the last few years about interest rates, inflation, and the economy. The “old rules” from the Greenspan era of a Goldilocks economy have proven to be garbage. A key reason is the view that “deficits don’t matter”, and they don’t until they do. With the annual interest rate on federal deficit flying past one trillion, the reality has changed for the housing bubble and soon the equity bubble. “Soon” means in the next few years. So Janet Y and Jerome have missed the reality of inflation, deficit spending, and the economy. The new team will likely make similar mistakes, but with new excuses.

The one rationale for the Fed rate cuts is an effort to move investors off of T-Bills and into notes/bonds.

There has been an unbelievable amount of market hysteria/negative hype since Sept 2024, yet the final 4 months of 2024 looked just like the last 4 months of 2023, particularly in the jobs reports.

So, lock in the 5% 20-year? IDK. It’s obviously risky. But risky, too, is a black swan can drop yields to near-nothing in a heartbeat. I do know this: had the Fed not telegraphed butting rates, I’d have not transitioned from bills to notes. Gonna be some pain in this move, but I’m not a market timer.

Good luck.

I’m a transition and value timer.

LT rates seem to be going up. ST rates are still above 4%.

The stock market/RE market is IMHO historically overvalued and tipping toward the downside.

While this transitions, I’ll Tbill and Chill. Like Warren Buffet.

I’ll un-chill and wake up if:

1) If stocks plunge 20-30%, I’ll buy stock ETFs. This happened in 2008 and 2020. The panic plunge happens fast so having ST cash is important.

2) If RE plunges 20-30%, I’ll help my son buy his first house. This may take a few years. ie 2008-2012.

3) If LT bonds exceed 7%, I can live on that and will buy bonds. I’ll sleep at night given the security. This may also take awhile to get to that level.

Currently investment grade corporate bonds are 5.8-5.95% out 20 years. Treasuries are 4.9%ish out 20 years. Historically (last 25 years), these are very high rates! Locking in nearly 6% rate of return is very attractive for that portion of your investment portfolio that you rely upon for income.

With a tidal wave of money after the GFC, no one knows exactly where the risk actually is. Only a recession will show the “great” economy of 2025.

We’re on the way to a $40,000 billion deficit.

Those treasury auctions financing our debt are almost daily and usually 2 issues.

Ultimately, the piper will be paid and my guess is that the payment will prove extremely painful.

B

Most of the auction activity is to refinance maturing securities. There are $6.5 trillion in T-bills outstanding, with maturities of 1-12 months. A 1-month T-bill matures in one month and then another 1-month T-bill is sold at auction to replace it, and their settlement dates line up. So if you hold 1-month T-bills on auto-rollover, you don’t even notice much, except that you get the interest payment every month. So that $6.5 trillion in T-bills rolling over constantly is a big part of the activity, and you see that when you look at the auction results: huge T-bill auctions one after the other to just roll over existing T-bills. It’s a well-oiled machine.

Yep, I get my interest payment every month. Then I pay 37% federal income tax plus 3.8% NIIT on that interest. So I get to keep 59% of the 4.3% interest I get on my t-bills, or 2.54%. Which almost keeps up with inflation, so I only lose a small bit of purchasing power every single month. It’s great, isn’t it?

You pay income taxes on all your income. Why the F is it suddenly different when you pay income taxes on your income from bonds? At least you don’t have to pay state income taxes, but you have to pay state income taxes on all your other income.

So you lose 50% on your stocks over 3 years, plus you lose 15% of the remainder due to inflation, now you don’t owe income taxes. But you’re nearly wiped out. Are you happy? The only time you don’t pay income taxes on income is when you don’t have income. Losses are even better in that regard, LOL. Why do you people always bring up income taxes with Treasuries but not with all the other stuff you pay income taxes on?

Wolf, it’s not income if it’s just keeping up with inflation, at least not real income. And tax rates are lower for dividends and capital gains, not to mention the exemption of tax for real estate profits and the step up basis for passed down assets.

Biff tanner et al.,

Dividends are taxed at regular tax rates, federal and state. Dividends on average are lower than inflation rates, so they’re worthless anyway, and just throw them away, would be less hassle than paying taxes on them.

Capital losses are not income either, and inflation eats into the remainder.

You people need to use your brain. The big difference between Treasuries and stocks and cryptos is RISK, not taxes. I have no idea why this BS about taxes keeps copping up with Treasuries. You people have no concept of risk and are distracted by taxes.

@Wolf

Qualified dividends, which is the kind most investors receive (for example, 96% of VOO dividends are eligible for qualified status if held long-term), are absolutely not taxed at regular tax rates. The MAX rate you pay is 23.8%, and much lower for most earners.

I am concerned that the author of this does not know the difference between qualified and ordinary dividends. Because my strategy is the same as his. Hold short term treasuries and wait for corrections in the stock market and housing market.

So far, I have missed out on 50% gains in the S&P and have suffered living with in a rental unit with shared walls. In the process I have accumulated a lot of cash equivalents and paid a ton of tax.

Every single “this is what always happens when rates do X historically” indicator has stubbornly failed this time. I am about to throw in the towel and buy a house in cash and throw the rest in the S&P and eat my huge loss on TLT.

It is great if you’re already in the highest Federal tax bracket, which starts at income over $626,000 for individuals and $751,000 for joint returns in 2025, before you receive any interest income on your t-bills.

KevC,

I agree. If you are in the 37% tax bracket, you are treading water with effective TBill rates but living like a king with that high of an income (Unless you have child support, alimony, a yacht, a jet, etc…)

The rich people I know are in Muni bonds which are tax exempt at both state and federal. They pay a lower actual rate but effectively yield a higher rate after taxes. They are slightly more risky than Tbills but less risky than stocks and dividends.

My plan is to retire in the 20-24% tax bracket. My lifestyle and minimal amount of toys will keep me in that bracket. Tbills, LT capital gains and dividends will keep me ahead of inflation.

By CA state tax calculations, I would pay less taxes since they consider that poverty level.

Somebody notify the Plunge Protection Team that they are to get back on the job with the market before things get out of hand.

I know. It’s already dropped like 5%. I’m surprised they are OK with this and the world isn’t screaming ‘DO SOMETHING, or the ECONOMY will collapse!!!’

Poor rich people. I hate it when they lose money. Thinking about sending them my money directly since taxes alone aren’t enough!

It’s a healthy correction. S&P is wayyyy too overvalued

Bond bulls gonna get rekt in 2025.

The FED is undeniably pro-inflation. Talking 2%, but enacting inflation accelerating policies before 2% is achieved.

Can’t wait for the return of “transitory”.

In the sense that they’d rather deal with 3% inflation than 1%, you’re dead-on. But frankly, as a citizen/investor, I’d rather have slightly higher inflation than risk deflation.

Spoken like a true homeowner.

Hahaha you don’t like it when prices go down? I do

Well my wage income is much higher than my consumption and derives from selling products to Americans, so yes, I’d rather prices rise and I receive more revenue than prices decline and I save a smaller amount on what I spend.

I’m a thrifty person, so inflation has almost no effect on me other than increasing my wages and asset values.

I am not sure what Fed “inflation accelerating policies” you are referring to. The Fed has broken the back of inflation so that it is running about a half point higher than it was in 2019 (pre-COVID). Yet its FF rate remains 2.5% higher than the end of 2019… AND it is continuing to downsize its Balance Sheet through Quantitative Tightening which it had abandoned (temporarily) in 2019.

The inflationary policies that this nation currently faces were brought on by a series of spend-thrift Presidents and Congresses… not the Fed. The Fed is doing its part… it is time for the politicians to do theirs.

After checking with the 2 and 10 year treasury yields, I’ve discovered they’ve both been in a deep slumber and in need of a stiff drink before they know their proper role.

But I wouldn’t expect them to act normal after being dug up and dusted off.

If I can live for 20 years at a 5% rate, I’m going all in.

I’d like some buffer for inflation over those 20 years so i am holding out for 7-8%. I am still envious of my parent’s 18% in the 80’s which allowed them to retire comfortably. That greed has clouded my judgement.

Otherwise, I’ll stick with a majority in the risky stock market which has averaged this. I’ll TBill and chill to cover the down years with the minority rest at 4% for now.

What bonds did they own at 18%? Because they weren’t US Treasuries… those are urban myth I am afraid. As I said to your post higher above, US 30-year Bonds peaked slightly above 15% in the summer of 1981 but averaged Maybe corporate bonds went that high in 1980-1981… but in that case you are taking on additional risk (such as that they are callable).

The AVERAGE 30-year Treasury Bond in the “double digit” era of 1979-1984 was about 12%… still REALLY good from today’s perspective but it also corresponded to an era of 6-13% inflation… so there is that!

https://www.macrotrends.net/2521/30-year-treasury-bond-rate-yield-chart

Ultimately we have high rates until something breaks.

The fed could have held at 5.5% until there were actual recession signs.

Or now the fed cuts driving long term rates higher which ultimately will cause a recession.

There’s no way to lower long term rates with above avg gdp and historically low unemployment.

Now they’re trapped. I personally think letting the recession happen sooner than later and getting it over with would have been the smarter move.

Similarly if I was a politician, I’d want the recession to happen the first year of my term so I could blame everything bad on the prior administration and be the hero. Also crisis give opportunity to act quickly and use executive orders.

I think 2025 will be interesting.

I think long rates could come down if the Fed threads the needle. They’d need to keep the economy in low growth mode while avoiding recession. That means avoiding large asset price drops but making sure they don’t rise either. Companies would have to grow into their valuations and corporate profit percentages would have to decline over time. Wages would have to grow at inflation or better. Fed would have to deceive the public with a 2% inflation target while getting 3-4 over a decade. They’d also have to keep the threat of QE alive. Market needs to know the Fed will inflate quickly in response to defationary crisis.

Chances of that happening are not good. Bubbles have a tendency to pop, not deflate. People are reactionary.

How exactly do they keep the economy in low growth mode?….high interest rates. That was my point.

They can cut, but we’ll get high long term interest rates

Or the can hold or raise and we’ll get high long interest rates.

There isn’t a scenario with low unemployment and strong gdp that produces low long term interest rates

Yes if the labor market cooled and growth slowed interest could possibly be lowered, but cutting will just re-accelerate the growth and thus up long term interest rates because of inflation fears.

Only way out is recession and job losses. Hard to slow and economy with 4.1% unemployment and massive immigration. Too many people spending

Long term GDP growth potential is 2% or less, right? 1% productivity growth plus 1% population growth. This suggests long term rates should be no higher than 4% over time.

See Lacy Hunt’s work.

Once the current speculative fever is checked by a stock market correction, we could easily be in a low growth, low rate mode like 2019. It’s what the Fed is hoping for.

We have to be careful about projecting today’s speculative nonsense into the future. A recessionary threat could arise very quickly.

I remember plenty of people blaming Obama back in 09 so don’t be too sure. I also am very interested in the direction of inflation and interest rates and this is the first place I look for that information.

my chart of the yield curve shows that the benchmark on the YC is about 1.00. YC is still inverted. This might explain why bond yields and fed rates are inversely corr. it might also be the QE hangover. Friday was a bad day for bank stocks. Heres a question for the new treasury secretary (in the anything goes administration) if you were accepting bitcoin as collateral on bonds, what premium would you demand?

Wonder how this Fire in SoCal will change the dynamics of this market for months and years to come. Probably not for the better as there might be spike in buying demand after, especially with a lot of rich folks looking for a replacement house, also this will likely drive up rental demand as displaced families need to look for housing…don’t see how it will deter more demand unless insurance get absolutely insane, which could be a real possisbilities…

Another word, probably more dark time ahead for SoCal market when it comes to affordability and price will forever be going in…

Lots of people will take their insurance money and permanently leave the area and the state. Too risky, insurance too expensive. California was already losing population. This will speed it up.

And the Land remains, always the land remains.

This will speed up the exit I believe as well . Over time the homes will be rebuilt but the folks that had thought about relocating have an opportunity to cash out from insurance payments (I assume most have insurance ). Much of the value for these properties I would assume was the land value. In Houston a 2000 sq ft home including lot can be built for under 200 a sq ft. That is no 1 MM . I suspect the areas burned will be quickly purchased from those interested in selling and homes rebuilt and sold for what the market will bear . Houston had 10 percent of their housing and businesses flooded in Harvey hurricane in 2017 and those will refurbished or torn down and replaced . Lots of great paying jobs in CA and wonderful weather . I doubt the nice areas of LA will have much trouble rebuilding. The 3 percent mtgs will disappear however

Ah yes, leaving the firelands of LA for the floodlands of Houston. Thing is, they will be shocked how low wages are in Houston and door dash is just as expensive.

I also agree a lot of people will leave CA. Many of the rest will move or rent nearby, and next door in Orange County the realtors are already going haywire that fire refugees wanting to move away a bit, but not too far, will put upward pressure on both purchases and rentals in the OC.

We have friends who lost their home in Palisades. They recently inherited a home in small town in NorCal, which they were working on fixing up to sale when the fire broke out. They are going to keep that house now and move there. The insurance money makes a nice cushion.

I don’t see much enthusiasm to rebuild, too risky and no chance of getting insurance now.

I am sorry for your friends’ loss. Watching the aftermath of Hurricane Katrina on the Gulf Coast, there is a lot to be said for the “move and start over” decision when something like this happens. For us it wasn’t a wildfire, it was a 34-foot storm surge that obliterated housing.

While most (if not all) of the Gulf Coast states instituted subsidized “Named Storm” insurance pools following Katrina… that doesn’t make it easy to justify rebuilding in an area prone to extreme natural disasters. Few people want to go through THAT again… even if they are going to be financially reimbursed. Nineteen years after Katrina you can drive along the beach highways down here and still see that the ocean front property is remains unoccupied up to a half mile inland in some places.

In the very near future, we are going to see inflation rise substantially. Mortgage rates will rise into the double digits. Personally I hope they go up to 15% and absolutely annihilate greedy home sellers. The wisest of them will dump their houses for anything they can get because those who hesitate will lose everything. It’s going to be a bloodbath of epic proportions!

Escierto

Sounds good. It’s equivalent to the commander in NAM who said:

“we have to destroy the village in order to save it”

“The wisest of them will dump their houses for anything they can get because those who hesitate will lose everything. It’s going to be a bloodbath of epic proportions!”

But, but, but….why not just live in the houses? What a novel idea!

Housing is not too expensive. Your expectations are too high.

Find something you can afford and your life will be much easier.

Those fine homes are for those who can afford them. That is the American way.

Are you actually this out of touch or is this parody?

Pea Sea,

In lots of cities, decent single-family houses can be bought for $200k or less, nice cities too, such as Baltimore, Memphis, Tulsa, OK City, Rochester, Wichita, Cleveland, St. Louis….

So yes, people can find something they can afford, it’s just not going to be in the most expensive cities in the US.

My MIL just died in Edmond OK god rest her soul at 89 years and my wife her sisters will be listinging a beautiful home on 1 acre in a nice old neighborhood that could sell for as little as 100 per square foot. I think the home is move in ready though the interior needs

Completely agree with Wolf lots of affordable homes in great cities available should one decide to locate in Oklahoma Texas Ark etc

Send your kids to public school in Memphis and Baltimore.

Wifey says no to all those places.

That was the point. It’s a choice. You CHOOSE to live in unaffordable places.

BTW, there are good schools in all those cities I mentioned. But not all schools in those cities (or anywhere) are good. I know Tulsa pretty well, lived there for decades, went to high school and graduate school there, and still have lots of friends there. Even your wife might like it. Has some very good schools. And the Arkansas River with many miles of park alongside it. And hills. And it’s nice and warm too. I highly recommend it, and people have been listening, population started growing again, and home prices have doubled since I started recommending it, but are still low compared to other cities.

EVERY major city that I am aware of (including those that Wolf listed) has nice suburbs that you can send your kids to public school in. Where you choose to live is where you CHOOSE to live… be it an expensive place or an inexpensive place.

You’re overthinking. Per capita GDP of cities and price per sqft of residential real estate are highly correlated, and these correlations reflect the overall better economic and social environment of top cities, with a little natural/cultural amenities layered on top.

Sure, there are some corporate jobs in Memphis that pay six-figures, but you better hope FedEx or International Paper don’t have layoffs as otherwise you’re up a creek and forcing your family to relocate. Obviously the Mississippi mudflats and educational/cultural capital of the Memphis exec crowd compares to Boston or Berkeley poorly.

Yes, for the median middle class buyer there isn’t much of a difference, but the marginal buyer in places where housing prices have exploded are not in that class and are willing to pay for experiences that can’t easily be priced.

For example, do I want my teenage kids’ dating pool to be the kids of surgeons or the kids of auto parts store managers? How much am I willing to pay for the former?

Heck, if we’re going to do this whole “there are nice places everywhere” thing, we should all be decamping for Mexico. Home prices in Tijuana are 1/4 that of San Diego, yet you’ll find few who will move there, though there has been a mini property boom in TJ in the last few years.

William McDonald

“For example, do I want my teenage kids’ dating pool to be the kids of surgeons or the kids of auto parts store managers?”

Oooh…. sweet memories.

1. I just checked, and there are, to my greatest astonishment, hospitals and surgeons in Baltimore! The per-capita ratio of surgeons in Baltimore may be even similar to other cities. And I assume, but don’t know from personal experience, that these surgeons have a similar number of dateable kids as in other cities. But yes, median household income is less than half of what it is in San Francisco. But homes are a lot cheaper too, and there are some very nice areas of Baltimore. And by Axela Express, it’s a 30 min commute to Washington DC Union Station just across from Congress.

2. I was a poor kid and might have been shocked to find out that some parents thought I was too worthless to date their daughter. But I was really cute, and their daughters, charged up to the gills with hormones, WANTED to date me, LOL. So I didn’t care what the parents thought about me. Not one iota. Never entered my mind. My hormones were running the show with one goal in mind, and they didn’t care about social complexities.

“If we’re going to do this whole “there are nice places everywhere” thing, we should all be decamping for Mexico.”

Yes, many many Americans, including some commenters here, a bunch of my readers, and one of my authors (RIP) have already done so.

Mr. Wolf writes: “And seeing these upside risks to inflation, the Fed is gingerly shifting back into its wait-and-see mode.”

Sounds very proactive and encouraging, the Federal Reserve is sure on top of this next inflation excursion.

Pilot to passengers: “The ground out your window looks like it is coming up, this is not a landing, the crew is going to wait and see what this is all about.”

Back in mid-2020 & early 2021 there were 2% mortgages (0.99% variable 5-year teaser rates in Canada) and 0.50% long-term CD/GICs.

Up until late 2023, a 5-year GIC was about 4.5% per year.

Before than, in the 1980s, they were around 19% interest.

I’m very interested in your “lock in” AND “draw” investment. Can you explain further.

This reply was intended for chris. (Below). Thanks

In the early 1980s (with the exception of Vancouver) people were paying C$80,000 for a home in the Greater Toronto Region while a single person on full-time minimum wage worked for about $10,000 a year, not counting tax credits and low income government grants.

Back in early 2022, a starter home was reaching C$2,000,000 while minimum wage was only C$14.25/hr, or about C$30,000 a year.

And this time, Canada became flooded with temporary foreign workers and fake students which helped drive down wages.

There’s agencies demanding a degree with several years experience in algorithms, macros and automation , but only offer a measly C$16/hr at that time, when a comparable job in the States is about US$100,000 or more a year.

Here’s a plan for your nestegg for anyone retiring. Normally they suggest withdrawing 4% a year out of your account and it SHOULD last 30 years, no guarantee. Well, when bonds get over 5%, lock in and withdraw 6% a year, your account will go down less than 1% a year and it’s basically guaranteed to last 30 plus years. “Past results are no guarantee for future results” unless you have fixed assets. Remember, nasdaq hit 5000 in 2000, it took 12-14 years to reach 5000 again after the dotcom bust, a person that retired at 65 at that time had to wait until they were 75-80 to relax, I don’t want to play that game, Murphy’s law..

I’m nearing that stage, I think the 4% rule says you increase withdrawals by inflation each year. My calculations show that pot you described as is zero at 23 years with 2% inflation, and you need to reduce the 5% return by investment costs. And inflation may be a lot more than 2%, so you should probably look to add some inflation protection. Not financial advice but just check your sums.

I agree retiring right now and relying on what you have in stocks with valuations at current level leaves you at heightened sequence of return risks if price earnings ratios revert to mean.

I’m also reading that tax rates will need to increase to pay off the deficit longer term, or they will need to inflate it away, probably both, so factor that into your calculations.

I don’t follow.

If you buy something that pays a 5% coupon, you can’t withdraw 6% without drawing down the pricipal, aka selling some of them. And if inflation and rates keep going up, you’ll be selling some of the bonds at a loss.

I think this could work if you laddered the bonds, but then not all of them would be >5%… unless you’re saying wait for the entire yield curve to be >5%.

Everyone talks about a housing collapse, but perhaps the scenario is that home prices move sideways or modestly down and sellers remain on strike until inflation+rising wages go up enough to make the same priced home affordable at 7+% rates?

“Everyone talks about a housing collapse”

No one here is “talking about a housing collapse.” Price declines, sure. But not collapse.

Here are some examples of what price declines look like, and we’ve talked about them here:

Lower for Longer is Folly.

What a sham. Total jackassery.

Reestablish the $60B runoff.

Yields are moving up nicely even with lower QT cap.

Fed is ok with an orderly rise in coupon rates but they don’t want them blowing out.

Not overly curious but wondering if fire victims who take insurance money and sell their land have to pay any gains they might have made or it is treated differently?

Lots of different rules on cap gains tax and personal homes plus investment properties. Just like Wolf says paying tax means one made a profit . Paying tax is terrific ! Income and profits ! Don’t avoid paying taxes

From a macro standpoint, I am curious how much of a factor housing is in the U.S. economy, taking both the direct and indirect contributions into account. We have housing sales, and all of the supporting functions, including lending, real estate agents, lawyers, etc. Of course then the loans are bundled into financial instruments, etc. But we also have everything that goes into the house: furniture, appliances, fixtures, carpets, etc. Home improvement industries. Plus the lawn/garden, etc. Home improvement and HVAC contractors. Solar systems. And on and on and on. In the end, it adds up to $X per year contributing to GDP, compared to us living in caves with bearskins and knives. On the whole, consumers put a lot of irrational money into their homes (above the basic function of a home).

It seems that a lot more is at stake economically, and the government has a strong incentive to facilitate people pouring irrational money into their homes. It seems this is an area that the government will subsidize effectively, versus just leaving it to the free market to sort out.

Exactly. Just Home Depot is in the top-20 most valuable and top-20 most employing companies.

This is what a realtor think that government won’t not allow home prices to go down and thus price won’t go down ever again . The prices would keep going up and up so what it is totally un affordable and has risen 60 percent plus in most of America in just last 5 years .

But WR articles has shown that home prices in some of the hottest markets have fallen 20 percent or so from their peak.

This too in super hot economy.

Who knows what would happen if and when a recession hits

The US economy is significantly propelled by fire these days (Finance, Insurance, Real Estate). It’s a very big portion of GDP. Much larger than ridiculous old school things like ‘manufacturing’. So yes, everyone wants the music to keep playing there.

I wonder what the total percentage of GDP is attributed to home ownership? It certainly is quite large, in that there are lots of people who live in much smaller homes, and are surviving just fine:

https://worldpopulationreview.com/country-rankings/house-size-by-country

Essentially, we have 2X-3X of the home-driven GDP that is luxury–not at all necessary to survive. So it will be volatile, intrinsically, since we do not actually need it.

Real estate is only a big factor in GDP because of CONSTRUCTION, residential and nonresidential construction, which is huge in the US. The value of a newly built structure enters GDP when it is sold (= “fixed investment”). And the amounts are huge. That’s what goes into GDP.

Selling existing homes has essentially no impact on GDP. A small portion entered GDP when those who earned fees and commissions on the deal spend this money they earned (= “personal consumption expenditures.”)

Yeah but just homes existing and their value increasing boosts GDP significantly right? Isn’t imputed rent part of GDP? That makes up like 2 trillion I thought, which is approaching levels comparable to all of mfg here. Gets somewhat artificially inflated during housing bubbles too I would think.

Maybe that’s the direct accounting in GDP for real estate, but there’s a lot more that would disappear from our economy if we all lived in mud huts (or the equivalent). So what I am asking is what is the total economic impact of residential real estate? It goes way beyond construction. The construction (and remodeling and additions) enables decades of consumer spending, over our building mud huts. From a political standpoint, the government is supporting a lot more than just construction when it gets involved in home ownership (it could just leave it totally to the private sector).

Sales of existing homes (85% of home sales overall) are a big economic stimulus due to all the improvements/remodeling, etc. that the new homeowners make. The resale market in residential RE is 5X the new home market.

A very active residential real estate market is stimulative due to increased sales of durable goods and increased services to upgrade the home (painting, new rugs,etc.)

What affect will a trade war will have on home prices? New construction could be a lot more expensive.

President Trump has the people in power to get anything and everything he wants and he loves tariffs.

Possibly, not certainly. Homebuilders profit margins, which had been egregiously fat during the pandemic at the expense of homebuyers, have been shrinking over the past two years as they cut prices and offered deals to sell down the huge inventory of completed houses that instead continues to grow. They cannot pass on higher costs, they have to eat them, and their profit margins will shrink further. Tariffs are a direct tax on foreign producers’ profit margins and on importers’ (homebuilders) profit margins. And a lot of times, they end up eating the tariffs because they cannot pass them on. The US needs to raise taxes to deal with the deficits, and tariffs are the best way to raise taxes. Trump has been right about that since 2016.

Agree with most of the material in this article. However, two items of concern are the unusually strong jobs report from last Friday – almost twice what the analysts were predicting. The other is the debt ceiling, which the conservatives and Trump are pushing to raise. Adding more debt to the almost 40 trillion in US debt that is already out there.

The strong jobs report is inflationary. Raising the debt limit is inflationary. Both of these items are causing the 10, 20 and 30 year Treasury Bond yields to increase. As investors flee the volatile stock market for the safety of the US Treasuries, the economy will slow down. We are greatly overdue for a recession. Remember, recession, recovery and growth are all cyclical. An adjustment is coming Are we all ready for the roller coaster to plunge?

What’s your proposal that is an alternative to raising the debt ceiling? Tax increases? On who? Where would you cut spending?

“Where would you cut spending?”

DoD spent $1.2B on office furniture between 2020 and 2022.

I’d start there.

Ok, you’ve eliminated 1B. Only 1,999 more to go before you’ve crushed the deficit.

1.2B and I could find many other examples.

If you’ve ever been handed the company credit card, you know how much easier it is to spend someone else’s money.

What is R* now? There is no longer an excess of savings over real investment outlets. The O/N RRP is at $178.8b.

It’s a blatant error. Contrary to the accountants at the Board of Governors of the Federal Reserve System (in contradiction to the presupposed Generally Accepted Accounting Principles, GAAP, the sale of securities by the FRB-NY’s trading desk decreases both the assets and liabilities of the Reserve Bank. It is not just an “exchange in liabilities”. The asset reflects an exchange in ownership.

Just based on that, interest rates had to rise.

1. “…sale of securities by the FRB-NY’s trading desk decreases both the assets and liabilities of the Reserve Bank”

EVERYONE at the Fed knows that and says that. This is why assets and liabilities on the balance sheet decline in equal measure during QT.

2. sale of securities by the NY Fed “is not just an “exchange in liabilities”.

NO ONE at the Fed says that it is “just an exchange in liabilities.” Where did you get this crazy idea that anyone at the Fed said that??? No one said that.

The “exchange in liabilities” on the Fed’s balance sheet takes place unrelated to the Fed’s securities holdings. It takes place for example during the debt ceiling, when the government draws down the TGA (liability), which then increases reserves (liability) and/or ON RRPs (liability). That’s the exchange of liabilities, but it has nothing to do with the NY Fed’s securities trading or the level of total assets and total liabilities on the Fed’s balance sheet.

All I know is I borrowed every last dime first republic bank let me borrow in 2021 at sub 3% and now all that money is invested in blended instruments yielding nearly 7%. Thanks!

Risk premium coming back? Let’s hope so, but we got a long ways to go…

Only two way out of these mess:

Let inflation keep above the target levels without raising rates and that way the debt/gdp ratio gets under control.

Or

Hike rates, create a recession, defaults, lower prices, destructive creation.

It seems number 1is more popular for politicians. Kick the can down the road…. but first consequence is rising populism all over the world.