A normal cost of capital is a form of much-needed discipline for governments and investors, after years of free money turned their brains to mush.

By Wolf Richter for WOLF STREET.

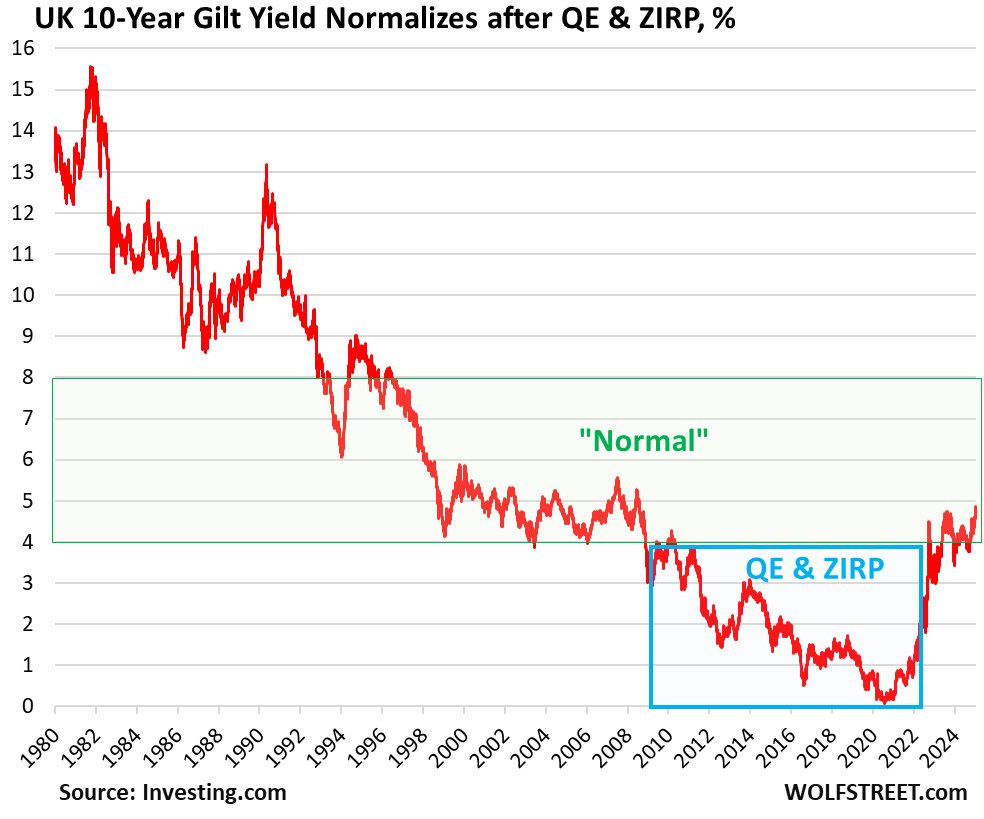

The 10-year yield of UK government securities rose to 4.82% today, the highest since July 2008. The 30-year gilt yield rose at one point today to 5.47%, the highest since 1998, though it backed down to 5.38%. So the UK is a little ahead of US Treasury yields (4.69% and 4.93% respectively).

There was a lot of handwringing in the financial media today and recently about those surging yields, with terms like “gilt market rout” getting into the headlines, and some even seeing a “return of the bond vigilantes,” etc. etc. But wait a minute…

Back on July 29, 2020, the 10-year gilt yield had dropped to an all-time low of 0.09%, back when everyone holding gilts was clamoring for yields to go negative because these holders would benefit from falling yields because bond prices rise when yields fall, and that path into the negative would be the necessary and logical continuation of the 40-year bond bull market and make it an eternal bond bull market, with yields falling ever deeper into the negative, or whatever.

But that final descent from the range of 4-5% in 2008 to near-0% in 2020 was caused by global interest rate repression, with the Bank of England cutting its Bank Rate to near 0% and keeping it there for 14 years (ZIRP), accompanied during some periods by large-scale QE.

Then inflation took off in 2021. The BoE eventually hiked its Bank Rate to 5.25%, and QE flipped to QT. After two careful rate cuts last year, the BoE’s Bank Rate is still 4.75%.

But the thing is, today’s 10-year gilt yield is back in the normal range – normal before ZIRP and QE. It’s actually at the low end of the normal range, and just barely above the BoE’s short-term Bank Rate. It’s at the low end of where it should be in normal times.

The return to normal, after those crazy years, should be seen as a good thing, even if sorting out some of the excesses of those crazy years isn’t always easy.

And a normal cost of capital, provided by the bond market, is a form of much-needed discipline for governments and investors, after years of free money had turned their brains to mush.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Evidently calling it the British pound “peso” now I was reading.

The real peso is the Canadian dollar which seems determined to make a trip below 70 cents. I can remember when it was actually worth $1.04 US. That seems like a lifetime ago and how did they manage to screw things up so much since then?

It’s not complicated. Oil was over $140 a barrel.

The Canadian peso is heading to 50 cents

Just because both currencies are “dollars” doesn’t mean they’re the same or should have any kind of “par”. They’re as unique as the Euro or Swiss Franc.

I don’t know what is or should be a fair exchange but never expect or compare it to 1.0 and assume it’s “screwed up” because it’s far from that.

A floating currency is a feature, not a bug.

Bretton Woods collapsed over 50 years ago — how long is it going to take for the average punter to grasp the implications?

70 cents is a good news story in our current environment, just ask my neighbour who returned to work this past Monday after a very very short Christmas break. I have seen winter downturns go on for months in years previous. Right after New Years flatbeds were hauling renewed/repaired heavy equipment back to the bush. Neighbour works in the logging industry making $150K per year. And, the low cdn dollar also incentavises Canadian’s from making mindless purchases from other countries. Add to the destroyed fire ravaged LA housing the last few days, and ongoing…..logging will continue non stop and flat out all across the Country.

It will be interesting if the current 14.5% tariff on cdn softwood lumber will be raised to 25%, or if 25% will be added on to the existing tariff….all paid for by US consumer with higher prices.

Paul S

“all paid for by US consumer with higher prices.”

BS. Tariffs are a direct tax on the profit margins of the Canadian producers and on US importers. Chances are that they cannot pass them on because there is a huge competitive lumber industry in the US, and it faces no tariffs, and it’s going to win this competition with the Canadian producers because it doesn’t get hit by tariffs, and your production will go down, and ours will go up, and your profit margins will take a hit on the lumber you do export to the US. You foreigners never get anything right about tariffs. You’re just steeped in wishful-thinking BS.

Wolf,

If you don’t think that the US lumber industry will take the opportunity to raise prices in the absence of Canadian competition, then I guess the US consumer won’t “pay the price”. But somehow that seems a little unrealistic…

The “US lumber industry” is not monolithic, but lots of companies spread around the US that compete with each other for business. There is a lot of anti-tariff BS being promoted by globalization mongers and some corporations (big homebuilders in this case) that want to fatten up their profit margins from offshoring production.

Homebuilders have been reducing prices of their houses for two years because they cannot sell at higher prices, and they have unsold spec homes now coming out of their ears, and they said that they will cut prices further to sell those homes, and so how exactly are they going to pass on any higher costs?

They can’t. They eat these higher costs, and their profit margins, which have already shrunk, will shrink further. That’s how that works in reality.

Here is some data on homebuilders’ spec houses coming out of their ears, and on their shrinking profit margins. READ IT and quit spreading BS about tariffs:

https://wolfstreet.com/2024/12/23/glut-of-new-completed-single-family-houses-for-sale-spikes-to-highest-since-2007-prices-drop-to-lowest-since-2021-still-way-too-high/

There is no evidence that tariffs increase inflation and prices. This is bullshit that quack economists like Krugman have promoted to serve their capitalistic masters.

These are the same guys that promoted outsourcing in a big way in the 80s and 90s. They promised higher wages for Americans…move up the value chain they said. China would export goods to US and import technology from the US. That was what was told to the American people.

A 40 year experiment is for all to see. Average American did not move up the value chain. It just went down in more debt. The average worker has been screwed over….thanks to these quack economists.

Let us hope more people will use their brains in 2025

Canada’s per capital GDP is now on par with West Virginia.

Is there actually that much speculation in the bond market? I always thought the bond market was where you parked your money.

Plenty of speculation in the bond market.

But it is funny that Bonds are traditionally viewed as the safe investment. I guess 40 years of conditioning will do that but will be interesting if that though process changes when bonds have another couple years like 2022

Well, when you leveraged yourself to the hilt speculating that yields will go down, a return to historic norms is a disaster.

“And a normal cost of capital, provided by the bond market, is a form of much-needed discipline for governments and investors, after years of free money had turned their brains to mush.”

Exactly!

Oh no! Tax cuts are on the horizon.

When it comes to the G, the line between stupidity and villainy gets pretty hazy.

The G can claim its money printing (rebranded as the Orwellian “Quantitative Easing”) is primarily to stimulate the private sector – but it has the parallel immediate consequence of enabling “any” level of G spending.

(In short, the G spends at perpetual/growing deficit levels for *its* agenda, then has Fed neutralize the short term consequences (spiking interest rates) by printing money to buy engorged supply of Treasury debt – that’s how Forever Wars/Forever Subsidies get “paid” for).

Sure, the G could tax to fund its insatiable spending – but that invites political blowback.

Money printing/monetary fraud has historically done *its* dirty business in the darkness – allowing the G to pin inflation’s rap on private sector actors (see Biden’s senile, twilight attempts).

The internet has made this well worn historical scam more obsolete – but DC will still keep running it (at this late date…what else has it got?).

Government spending is not constrained by interest rates. Nobody in Congress, nor the general public, thinks “What is the ROI for this new road we want/need to build?” Or whatever, you name it. Interest rates are just a way to keep lenders interested in lending the government money irrespective of financial conditions in the economy. Finally, the government can afford to pay whatever rate the market demands to finance its debt.

Unless the govt raises taxes a lot, or doesnt repress rates, which is what it should do if it wants to spend a lot, your reasoning relies on debasement of the currency. No, until recently, the govt wasn’t able or didnt want to pay the market rate, thats why it did interest rate suppression. And we’ll see in the future if it become unable or doesnt want to pay the market rate again. Which hopefully won’t happen as they cause a lot of damage to society with interest rate repression.

I agree with 1234’s statement about currency debasement, and I’ll add this:

debasement = inflation = higher interest = debasement again = …

Uncontrolled gov’t spending was engineered into the problem space with baseline budgeting – and huge future non-discretionary obligations.

Congress needs to restore the quasi(!) disciplined budgeting processes initiated in 1974.

Kinda obvious that the ultimate solution lies in a rational/responsible political process. Sooooo….good luck with that one!

Why do you call the 4-8% yield ‘normal’ when the preceding decade it was much higher and post 2008 it was much lower?

As I explained in the article (go ahead and read it, it’s very short, and it doesn’t bite): post-2008 yields were abnormally low due to QE and ZIRP. Those were new inventions that massively backfired globally, and now we have inflation like we haven’t had in four decades, and it’s sticking around, and it’s messing things up.

If you look back to the 1960s, you will see that 4-8% was normal until very high inflation arrived in the late 1970s.

So since 1960, over those 64 years, there were two exceptional periods, the 7 years of above 8% yields (1978-1986) and then the period of QE and ZIRP (2009-2022) when yields were below 4%.

You’re not looking back far enough to establish the ‘normal’ rate. Rates have been steadily declining since the middle ages in a ‘suprasecular stagnation’. The reason is primarily thermodynamic. After 2008, the wheels came off the growth paradigm and rates were brought down so low to kick the can down the road.

https://cepr.org/sites/default/files/styles/popup_small/public/image/FromMay2014/schmelsingfig2.png?itok=vG5mra2e

Philip posted further down this:

“The past 750 years of bond yields can be found here:

https://globalfinancialdata.com/750-years-of-interest-rates

“Looking at the graphs, I would guess most of the data points are between 4% and 6%. This is data boing back to 1285AD.”

The assertion that there has been a long history of declining interest rates since the twelfth century does not rest upon the choice of statistics in Table 76 or on the particular method employed in creating Chart 78. There is ample evidence that interest rates declined on the average in the late Middle Ages and Renaissance. There is no doubt about the 3% rate for British consols in the eighteenth century and no doubt that this was well below fourteenth- and fifteenth-century long-term interest rates. There is no doubt that the 2.47% decennial average for consols in the late nineteenth century was a new low for English rates and that the 2.31% average rate for long taxable U.S. governments in the fifth decade of the twentieth century was a new low for American rates. There were periods of easy money in the distant past—the downtrend has not been smooth— but twentieth-century lows have been below earlier lows, and twentiethcentury highs have been above earlier highs.

Sorry that was from Sidney Homer’s A History of Interest Rates. It seems maybe that the suprasecular period of low interest rates has also been associated with more interest rate volatility?

https://archive.org/details/a_history_of_interest_rates_4th_edition/page/560

👍👍

4-8% seems defensible, with occasional and unpredictable overshoots on either end, as evidenced by the prior 80 years. (WWII, 1970’s, QE-mania)

Anecdotally, Mark Twain’s Judge Thatcher put Tom Sawyer’s $6000 reward money out “at interest” at the midpoint of Wolf’s range, 6%, providing Tom with spending money of $1 per day the whole year around! (Presumably these investments were “high quality” corporates, not treasury securities, though.)

Long-term history supports your “normal” comment. Just checked out Sidney Homer’s A History of Interest Rates (available on archive.org and some charts in the link below). For most of recorded financial history, bond yields only went below 5% during periods of prolonged deflation or rampant speculation due to easy money (e.g. South Sea Bubble in 18th century England)

https://globalfinancialdata.com/7-centuries-of-government-bond-yields

https://archive.org/details/a_history_of_interest_rates_4th_edition

Academic question: I understand your response from a data point-of-view and failed theory (e.g., MMT). Does the response implicitly conclude that risk evaluations (play a role in capital cost) in debt and equity markets also follow some normal mean over the long haul? The question, I concede, may have little consequence since the gov’t also influences risk calculations.

Working my way through how cost of capital is driven and from whose perspective: gov’t versus, say, corporate investors, etc.

“Why do you call the 4-8% yield ‘normal’ when the preceding decade it was much higher and post 2008 it was much lower?”

If only there were a word for numbers that are neither abberantly high nor abberantly low…

Well, there may have been some undue distortions. Just MAYBE though.

Janet Yellen even admitted that the pandemic stimulus (another *possible* distortion?) MAY have contributed “a little bit” to inflation.

Then we see the rotation in governing powers, by election, resignation… REelection. I seem to remember a (more than?) slight panic in the Gilt market a few years ago based upon this? (Oct. ‘22)

The US 10 year is obviously in higher demand (as the article notes the slightly lower yield). I can’t imagine another reason why the UK would have a higher yield? Certainly not on growth expectations.

“The US 10 year is obviously in higher demand. I can’t imagine another reason why the UK would have a higher yield?”

That IS the reason. Less demand.

Treasuries are the gold standard for pristine collateral – not Glits.

Maybe treasuries have been the “gold standard” during the 20th century when the British empire collapsed (ironically the period when the gold standard was abandoned), but before that British government debt was considered safer than American government debt? The British empire was self-financing whereas the American revolution was a tax revolt and the American military-industrial empire is more debt financed?

“The US 10 year is obviously in higher demand (as the article notes the slightly lower yield). I can’t imagine another reason why the UK would have a higher yield? ”

Yup! At this moment it looks like no one wants to hold gilts because they feel the UK is going to be Argentina or a third world country soon. Given the quagmire they seem to be in and the squabblers running the show, they do ot seem to be wrong either.

Not a finance person here, but being resident in the UK, all I can say is this government is on fire from all directions, so perhaps bond buyers are worried about ever getting paid back at all, thus the higher premium demanded. Just saying…

We print our ‘money’ so they will get their money back.

Whasthepoint:

The US 10 year had been referred to as a “return free risk” for the zirp/nirp period.

I am not sure anything has fundamentally changed, but it looks nominally better (4.8% this morning, with “official” inflation below that), at least showing a positive yield.

Great, but I was referring to the UK, where we’re basically in a recession and heading deeper, with the bond market in revolt not to mention pensioners, farmers, employers, and anyone who isn’t traditional Labour, as in public sector and unions ….it’s back to the 1970s. IMF here we come!

“A normal cost of capital is a form of much-needed discipline for governments and investors, after years of free money turned their brains to mush.”

Well said.

Lines up with the belief that a mortgage rate of 6 -7 is abnormally high, when it is actually a return to normal.

Nick Kelly-

Not meaning to quibble, but isn’t it “normal” for the mortgage rate to spread above 10 year treasuries by 2-3%…. making for a “normal” mortgage range of 8-9%.

Otherwise your point is a good one.

your math is off. the 10 year treasury is around 4.75%, so the 30 year fixed mortgage is between 6.9-7.1, right where you said it should be.

Unclear post on my part.

I was thinking of Wolf’s midpoint guesstimate of “normal” (6% midway between 10 year gilt range 4% to 8% on his chart) plus 2-3% = 8-9%

Yields will crash this year. There is a global recession starting. China is in trouble because the global consumer is in trouble. They make the world’s things. The first place that gets it are the manufacturing hubs.

“Tell me you’re a bond bull without telling me you’re a bond bull”

This will undoubtedly be true given enough time. That is always the tricky part of investing.

Joe specifically quoted “this year” as his timeframe.

No poroblem – someone’s gotta wanna sell me those TLT puts.

Not if we’re entering a stagflationary recession period like the 1970s

For “stagflation,” we’d need the “stag” — stagnation — in the economy. But the economy has been growing well above the 15-year average rate.

More like stagflation, business stagnation accompanied by inflation.

Business earnings are increasing steadily and approaching the highs reached at the end of 2021 (inflation adjusted). They’ve roughly doubled in the last 15 years, which is about a 5% annual rate of increase (again, after inflation adjustment).

I agree with Wolf. The past 750 years of bond yields can be found here:

https://globalfinancialdata.com/750-years-of-interest-rates

Looking at the graphs, I would guess most of the data points are between 4% and 6%. This is data boing back to 1285AD.

Back when rates hit an artificial bottom, a London banker opined that they were the lowest REAL rates in 5000 years.

Back to now, a Canadian couple has decided to sell house and downsize to condo because their 5 year term is up. It was at 2,2 % !

That’s like a rate from the early 19 hundreds.

The bank has been way underwater on that deal for at least 2 yrs.

RBC’s GIC was 4.6 % two years ago.

With realistic yields….I still believe RE will eventually return to more normal sale prices as interest rates stay higher in all areas. Surprised it is taking so long.

I just don’t see condos as ‘the price solution’ as taxes still have to be paid, insurance is on you, and then there are strata fees/HOAs and the mind numbing meetings to attend to keep said fees in check. I would think it more a lifestyle choice as much as anything.

In Hawaii we have seen condo HOA fees rise about 400-600% in the past 10 years… For a multitude of valid reasons. Moving to a condo on a fixed income is like running into a busy street to pick up a quarter.

You can see where the Ottoman–Venetian War (1463–1479) really messed up interest rates.

Personally, I think the clearest, most spectacularly relevant historical years for our present situation are 1389 (Dead Peasant Bounce), 1494 (Smallpox Boom), 1535 (Royal Housewife Bust), 1670 (Incendiary Household Stimulus), 1776 (Tea Party Unpleasantness), 1883 (Birth of Keynes), and 1962 (Birth of Jim Carrey).

Those are the telling axes of Economic History, people!…

Cas127,

+1000

You win this thread!!!!

(It seems these days people with a sense of humor are in short supply)

I read an academic report of past term interest rates some time ago.

The gist of it was: interest is a risk premium associated with uncertainty about the future and a data deficiency to make informed decisions.

As technology progressed the available informtion increased, thus the risk premium decreased steadily. The future stays unknown but lenders can quiet well label someone as credit worthy or not.

I am looking for more historic bond yield data. I have about 30% of my savings in Treasury Inflation Protected Securities (TIPS) and ZERO in nominal bonds. Thus, I care more about real (inflation adjusted) bond yield and don’t care about nominal bond yields.

The world was on a gold standard up until 1933. When evaluating the 750 years of bond data:

https://globalfinancialdata.com/750-years-of-interest-rates

For 1285AD to 1933AD the real yield is the same as the nominal yield. Because the whole world was on a gold standard, there was no way to inflate the currency, except by mining gold. Thus the 4% to 6% average yield in this series is the REAL yield in that time frame.

Post-1933 there is inflation. The money supply can be expanded without mining more gold. The current inflation rate is about 2.5%, my 10-year TIPS yield 2.5% and the nominal 10 year bond yields 5% (thus, 2.5% plus 2.5% equals 5%).

However, adjusted for inflation, real yields are at least 1.5% BELOW the historic average from 1285AD to 1933AD.

I can’t find REAL yield data going back past the 1990s. Only NOMINAL yield data goes back past the 1990s.

Wolf, are you aware of any data series for REAL yield going back into historic time?

I bought a dozen eggs at Kroger and they $5 — shelves bare.

A quick search reveals that a tsunami of farm workers will be leaving jobs before deportation raids begin.

That eventually will connect to yields drifting g higher, as a perception and expectation that inflation will stay elevated and the deficit interest costs will grow.

I honestly thought inflation might surprise to the downside this qtr — my eggs tell me I’m wrong.

$5?? Lucky you. Trader Joe’s here has been out of eggs for weeks. I went to Costco on Saturday, and they were out of eggs too.

But LOL, this has nothing to do with farm workers or the yield curve or whatever, but with the avian flu that has been raging for months. Did you somehow miss it?

We bought eggs on Amazon for $2.50 per dozen in the last month and they came in perfectly for Amazon Fresh delivery.

AND, if or when the avian flu mutates in to a contagious to humans form, it will not be the price of eggs we will be worried about.

The egg thing is funny. Yes obviously eggs cost a lot more and the flu is a major part of that. Cumulative inflation of the last few years (+20%) also means $1.49 will now be $1.79 and it’s not going back. Once the hen numbers recover I do expect sub $2 eggs again.

One political party said the price of eggs was indicative of an economy that was collapsing and leaving the middle class behind – an exaggeration. The other political party said the voters were too stupid to understand that although the price of food had skyrocketed, their house value and investment portfolio was also up and just stop whining about inflation. Of course renters and people without assets were left scratching their heads. A real insult. The election results speak for themselves.

The price of eggs (and gas) on the morning of January 20 will be a very important political number for the next several years.

I recently invested in a company that is making poultry masks. I see big potential here unlike my failed mad cow investment choices. Riding it all the way up.

Higher coupon yields are simply a predictable reversion to the mean.

#ShortTLT

MSN: BANK OF AMERICA Braces for Massive Bond Losses as Yields Soar

SoCalBeachDude

Add in Wells Fargo, which owns a lot of mortgages in the LA area.

CNN: A zombie mall store king is born as JCPenney merges with Forever 21 owner

JCPenney is merging with a company that owns a number of other once-bankrupt clothing stores, including Forever 21 and Brooks Brothers, to form a new company that will hold significant sway over the future of America’s malls.

The 123-year-old department store chain anchors the new company — a joint venture with Sparc Group, which also owns Lucky Brand, Eddie Bauer, Nautica and Aeropostale. The merger will form a new company called Catalyst Brands, representing a gamble that combining the beleaguered brands will create a new powerhouse of mall staples … that also happen to have America’s largest mall operators as major financial backers.

Catalyst represents a new chapter for JCPenney, the historic chain that filed for bankruptcy in the height of the pandemic in 2020. It was later bought by mall-owner Simon Property Group and real estate developer Brookfield in a $1.75 billion deal.

…’Make Malls Great Again’ caps appearing soon?

may we all find a better day.

“A normal cost of capital is a form of much-needed discipline for governments and investors”

It took 10 years and sticky inflation to understand this at the central banks. Ask any housewife, who has a tight budget to run a household, anywhere in the world about cost of capital and disciplined spending. They would answer it in a jiffy. Just goes to show an ounce of common sense is worth more than all the PhDs in the world and common sense cannot be taught at Universities.

Sadly, these clowns have the keys to the house and run the monetary policy circus without this basic understanding.

I was thinking the exact same thing myself today. Why didn’t the Democrats realize that they were going to get hammered by inflation? Instead of doing something about it, they just added more fuel to the fire. Talk about clueless.

Because the Democrats response to everything now is simply to say “don’t worry your pretty little head” and then go bury their own in the sand. They only hear what they want to hear

Stick around, see if it gets better or worse.

There was a recent study where they did focus groups among swing voters etc, and asked them, when they think of the Democratic party, what animal comes to mind. One of the top responses was the ostrich, because they always have their head in the sand.

I lean left myself, which means I frequently find myself yelling at the TV going wtf are you guys doing??? Your opponent is setting a rather low bar! It should not be this hard!!

Because they aren’t really getting hammered (so they think). Notice how the Uniparty and their cronies pass massive debt bills over and over while sadly fooling the people to think that they’re getting change. But in the end, truth wins and corruption loses, so they are actually hammering themselves.

kpl-

You said> “Sadly, these clowns have the keys to the house and run the monetary policy circus without this basic understanding.”

Related quote:

“Giving money and power to government is like giving whiskey and car keys to teenage boys.”

— PJ O’Rourke

Don’t blame the clowns for being clowns when it is us who wishes to to see a circus.

Louie – …a sager statement never made…

may we all find a better day.

If you believe that operating a central bank is related in the slightest way to running a household budget, you are terribly ill-informed.

It’s the equivalent of drawing conclusions about an entire electrical grid based upon your experiences with the light switches and electrical outlets in your own home.

Good grief …

eg – …makes me wonder what McLuhan knew about Dunning-Krueger Syndrome…

(…an old joke accredited to Sam Clemens: “…those folks who think they ‘know everything’ annoy the HELL out of those of us who do…).

may we all find a better day.

It’s very similar in principle. A parent that wastes their families money on drunkenness or gambling or whatever leaves their family going hungry and getting evicted.

The investors are picking up the brainrot from the zoomer generation giggity skibidi no cap

The yield spreads between gilts from the developed and the emerging markets are becoming narrower. As wolf mentioned in his previous article, the returns from foreign investors in dollar terms was flat or negligible due to the decline of foreign currencies against dollar. There is some sobering to be had for the foreign investors, expect them to bring back their dollars into the US equities and bonds..

MW: LA wildfires to cost insurers more than $20 billion. Three companies are likely to foot most of the bill.

J.P. Morgan doubles previous insurance-loss estimate; Allstate, Chubb and Travelers most affected.

Insurance companies are bracing for more than $20 billion in insurance losses from the wildfires raging in the Los Angeles area, analysts at J.P. Morgan said Thursday, doubling their insurance-loss estimates from a day earlier.

LA wildfires have caused more than $135 billion in economic losses — and counting…

Is that good or bad news? Losses lead to rebuilds, corporate profits, and increases in GDP in the short term. Wall Street might be quietly cheering.

Oh yes, we should stake our nation’s economic and financial health on the Broken Window Fallacy.

Best wishes to those impacted by the fire. Hopefully insurance coverage and FEMA support is adequate to rebuild the communities.

I heard reports that several insurance companies pulled coverage last year. Not good timing for some folks.

Best wishes, indeed to those in the stricken area and to our southern neighbor who I understand has dispatched some of its own firefighters to aid our own domestic mutual aid efforts.

(with regards to insurance corps, I can only wonder at the realistic data-presentation tensions, adequate staffing and funding struggles found between those in the actuarial risk analysis departments and the financial suits in management. Recall my eighth-grade history teacher decades ago commenting to the class that insurance companies were notorious for poor investing in the financial markets…).

may we all find a better day.

Insurers are pulling out of Southern California. The politicians there have gotten a grade of ‘F-” in forest management. They have refused to budget for forest maintenance and especially cleaning up the underbrush. Instead they wasted money on high speed rail boondogles, DEI, etc. They are living in an age 60 years ago when there was not as much development near these fire prone areas. This was a time bomb ready to go off and they failed in basic risk management. Homeowners will see their premiums triple after they rebuild their homes and lives in these fire prone area. A lot of them will never move back there.

Clueless as always Paul Krugman thinks bond yields may be rising due to an ‘insanity premium’…

Sweden should really consider placing expiration dates on their Nobel prizes in economics.

Thanks for that one.

Johnny5 gets my vote for comment of the month :)

You mean the “Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel?”It’s awarded for outstanding contributions in Economics or Social Sciences and is selected and sponsored by the Swedish Central Bank.

It has nothing to do with Alfred Nobel, nor his legacy and has been openly repudiated by his heirs. It’s as grotesque an example of “stolen valour” as you will ever encounter in this fallen world of ours.

The story of how Economists came to purchase the right to use Nobel’s name reads like a mob movie. They actually have to pay the Nobel Institute each year to be include on their website. You can see a clear difference in the page and language.

I wonder if Japan regrets hiring Krugman a consultant 10 years or so ago, now that the currency has collapsed.

When you pitch short term solutions that simply steal prosperity from the future, it blows back on you at some point.

The Nobel family has already asked it be withdrawn. It was never part of Nobel’s intent, it was a last minute addition by the Bank of Sweden. The Long Term Capital gang were Nobel guys. Their near crash was averted by emergency Fed action, a precursor to the GFC.

All folks talking about bond yields centuries ago…this was on a strict gold/ silver standard. Fiat money hadn’t been invented until late 1700 hundreds with scammer John Law, treasurer to King of France.

No one traded bonds 750 years ago. Sure, there was money, i.e. gold. lent at interest, but this did not constitute a functioning market in debt.

Reason ONE: the monarchs would repeatedly renounce the debt, and retreat to argument by force of arms,

Not sure about 750 years ago, but it is a matter of historical reoced that almost 250 years ago speculators made a fortune buying up US Revolutionary War debt. I seriously doubt that Americans invented debt speculation…

Your last sentence is the clue to the misguided notion that “the gold standard” was ever some singular and eternal thing — there have been as many “gold standards” as there have been monarchies (and other forms of government, for that matter) issuing gold coins, along with all the rules for their composition and redemption in the form of tokens.

Sovereign currencies are a form of state power (as you will find to your cost if you run afoul of their counterfeiting laws) and it’s been fiat all the way down going back to the Bronze Age palace/temple complexes setting their weights and measures and operating their spreadsheets BEFORE even the invention of writing.

(the archaeology of money is pretty fascinating, really)

NB: Debt predates money. By at least 2,500 years.

If you haven’t already, read “Debt: The First 5,000 Years” by David Graeber, published in 2011. There are written records of debt from Sumer in 3500 BC.

See ‘Archimedes principle’ and the problem he solved- to determine if a crown was pure gold or whether the maker had cheated the king.

The ancients were well aware of what was pure gold.

The biblical denarius was originally a fixed weight of silver.

Of course there was debt in ancient times, and no doubt many private deals where debt was sold. This is not the same as a functioning market in debt.

Hell, the euro looks like the Argentine peso!!!

ECB politicians have gone mad!

They’re all delightfully colorful compared to greenback

It means that prices of RE will fall, right? RIGHT?!

DM = EM

-M. Every of Rabbobank

Mr Wolf why are futures down

I’m shocked and appalled that they are. How dare they, on a day like this!?

Market temper tantrum – the hot jobs report means no more rate cuts for you, now eat higher yields!

We’re now in a repeat of the Jimmy Carter economy of the late 70s.

1. Rising Inflation

2. Rising interest rates

3. Rising crude oil prices

4. Hostages

5. Declining quality of basic services.

6. Completely incompetent Federal reserve

7. non-functional Congress

8. Federal spending out of control

9. Military bases used to house illegal immigrants

Only things could be even worse now because back then we didn’t have the massive Federal Debt (35 Trillion) and annual budget deficits (2 Trillion) that we have now. Even Paul Volcker and Reagan would have trouble straightening out the mess that we are in now.

I don’t understand the hysteria over this either. Appreciate the historical background and perspective.

PAYROLLS GROW BY 256,000; MUCH MORE THAN EXPECTED…

TREASURY YIELDS SPIKE… DOW TUMBLES…

DM: Huge surprise in jobs report sends stocks plummeting – here’s what it means

Fears of a rise in inflation led to stocks falling fast on Friday morning after the monthly jobs report was way off predictions by experts.

Wolf,

any reaction to “news” that BoE is artificially stoking the rate spike by QT…they are actively selling ~GBP100Bn of gilts (not a “run-off”, like the US)…..

They’ve been doing this from the beginning of QT. They hold super-long-dated bonds, some of those bonds don’t mature until 2080, and they cannot wait till they mature. So they sell them.

I discussed this already back in 2022 when they started selling bonds outright. But I was ignored by those crybabies? And now they turned their ignorance into a conspiracy theory? LOL. These little shits.

May 2024:

https://wolfstreet.com/2024/05/25/bank-of-england-to-sell-all-remaining-bonds-and-use-repos-instead-to-manage-liquidity-financial-stability/

January 2023:

https://wolfstreet.com/2023/01/12/bank-of-england-sold-all-bonds-it-bought-last-fall-amid-pension-crisis-first-big-central-bank-to-sell-government-bonds-outright/

November 2022:

https://wolfstreet.com/2022/11/01/bank-of-england-sold-bonds-outright-today-to-speed-up-qt-will-sell-more-at-regular-auctions-first-major-central-bank-to-sell-bonds-outright/

From my article in May — the second chart shows you how they’re selling bonds across the maturity spectrum:

Many Thanks!

Thanks, Wolf! You’re just about the only economics writer who remembers the long-ago prehistoric archeology of Babylonian economics, which ended many many millenia ago in 2008.

Seriously, why do so many writers take us for fools? Some of us are ancient and decrepit enough to remember what life was like before writing and printing and the wheel and fire, way back in 2007.

Why? Because the corporate and financial media tailor the news to their liking versus telling the unvarnished truth.

Polistra – …reckon it’s a result of that human (…nay, animal) characteristic many of us seem to have of believing the world, natural and/or anthropoid, did not really exist until the moment of our birth…

may we all find a better day.

Rates may be returning to “the low end of normal”, but debt levels are not. The low end of normal for rates is likely too much for current debt levels.

It would probably all still be managable if Federal Spending were simply frozen, while regulatory burdens were eased and and other measures taken to promote growth.

No matter what, military spending will have to be cut with a complete rethink of defense policy.