And how the decline of the yen & rupee impacted USD investors in Japanese and Indian stocks.

By Wolf Richter for WOLF STREET:

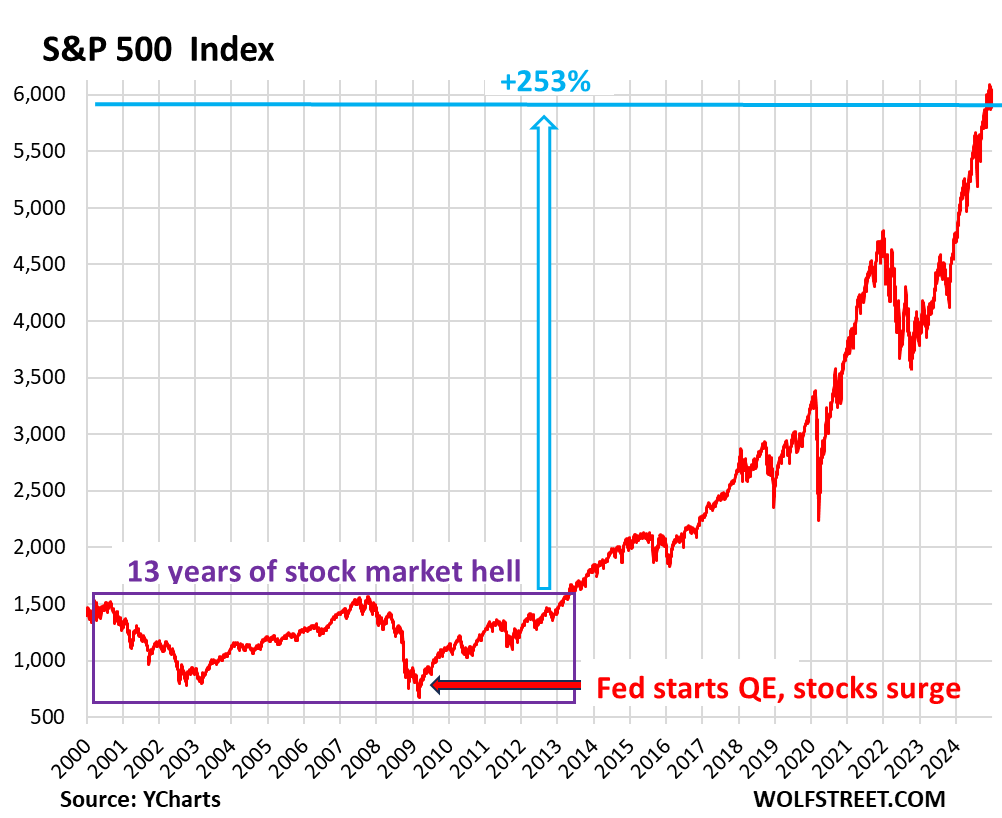

The S&P 500 gained 24% in 2024 and 53% over 2023 and 2024 combined, which was a huge two-year gain, reminiscent of the Dotcom bubble at the end of the 1990s, after which the S&P 500 spent 13 years in stock-market hell on a rollercoaster to nowhere with two 50%-crashes in between (purple box in the chart below).

But money-printing fixed all that. The S&P 500 has surged 253% since May 2013, which was when the S&P 500 finally surpassed its March 2000 high in a sustained manner (index data via YCharts).

Since the Fed started bombarding the markets with liquidity via QE in 2009, and other central banks followed in its footsteps, the S&P 500 has become the global standout amid the major foreign markets. But the Fed switched to QT and has so far unloaded $2.1 trillion; other central banks have switched to QT as well, including the ECB, which has unloaded €2.48 trillion.

Foreign stock markets.

Stock markets are valued in local currency. For USians investing their USD overseas, exchange rates are part of the bet. So we’re also going to look at the impact of USD exchange rates for USD investors in Japanese and Indian stocks.

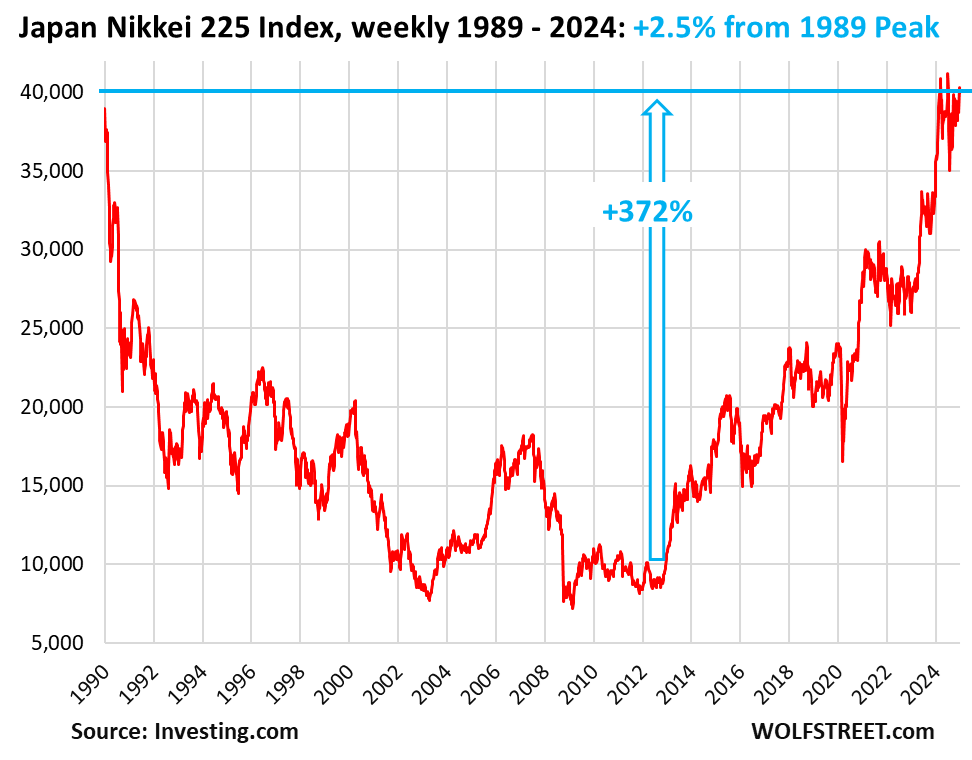

Japanese and Indian stocks have surged in local currency since 2010, but the currencies have seen large-scale declines over the years against the USD, and that has tarnished the returns for USians (all data below via Investing.com).

Japan’s Nikkei 225 ended the year 2.5% above the 1989 peak:

- Closed 2024 at 39,895

- Gain in 2024: 19%

- Gain in 2023: +28%

- Gain since 2012, start of Abenomics: 372%

- Gain since December 1989: +2.5%.

It took the huge amount of money-printing by the Bank of Japan starting in 2012 under the doctrine of Abenomics, including equity ETF purchases, to get this index to recover to its 1989 bubble high.

Now inflation is back in Japan. The BOJ ended QE in the first half of 2024 and started QT in the second half of 2024. And the yen has plunged against the dollar.

Back in early 2012, when the massive money-printing spree took off, the JPY-USD exchange rate was ¥90 to $1. Now it’s ¥158 to $1. In other words, over those 12 years, the yen’s value against the dollar has collapsed by 43%. A substantial portion of that collapse took place over the past three years.

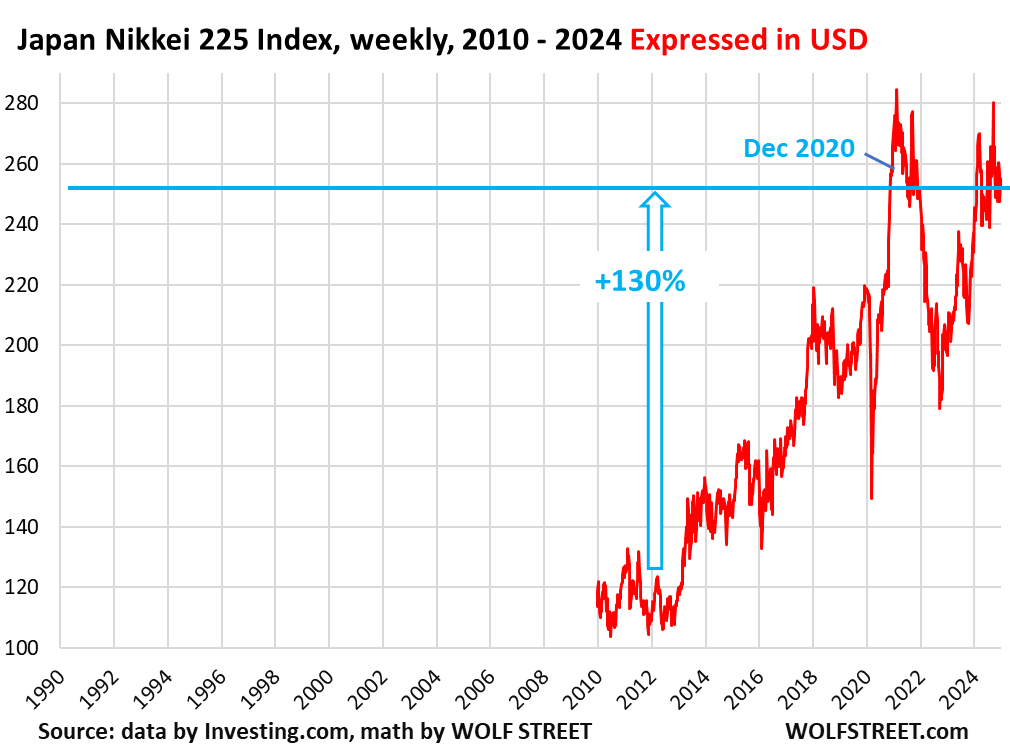

For USD-based investors in Japanese stocks, that 372% gain in yen since the beginning of 2012 shrivels to a gain of 130% in USD terms.

Here is the Nikkei 225 index expressed in USD since 2010. I left it on the same time axis as the chart above to make it easier to compare. Note how the massive plunge in the yen over the past three years left USD-based investors below December 2020 (each Nikkei 225 value adjusted by the exchange rate at the time):

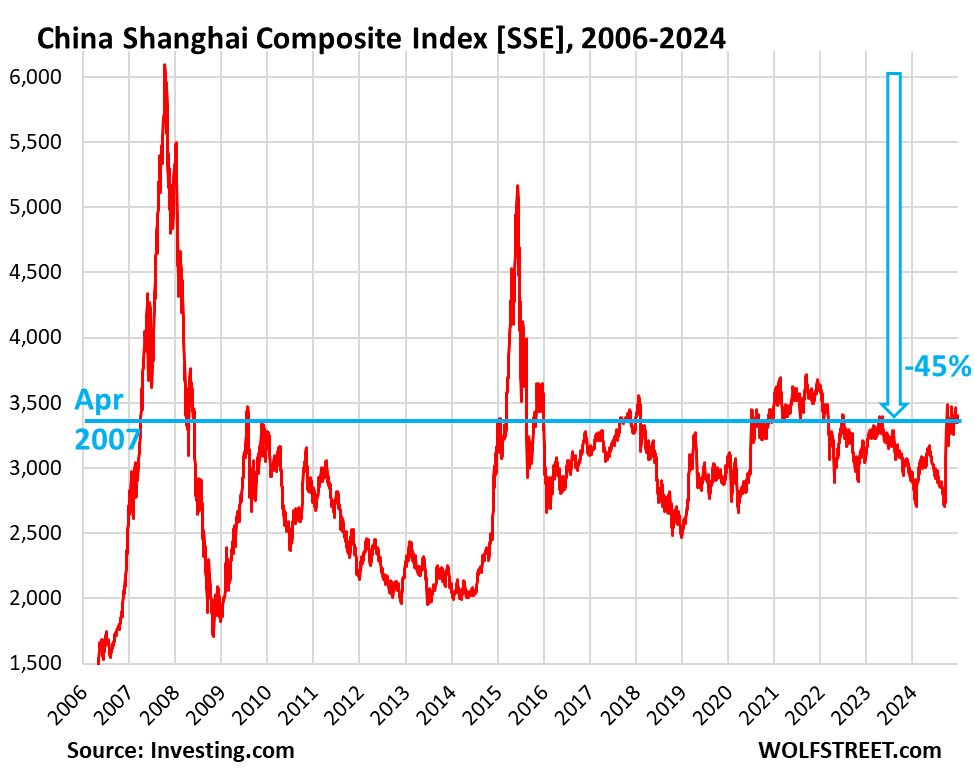

China’s Shanghai Stock Exchange (SSE), -45% from 2007 high:

- Closed 2024 at 3,351

- Year-over-year: +12.6%

- From October 2007 all-time high: -45%

- Back where it had first been in April 2007

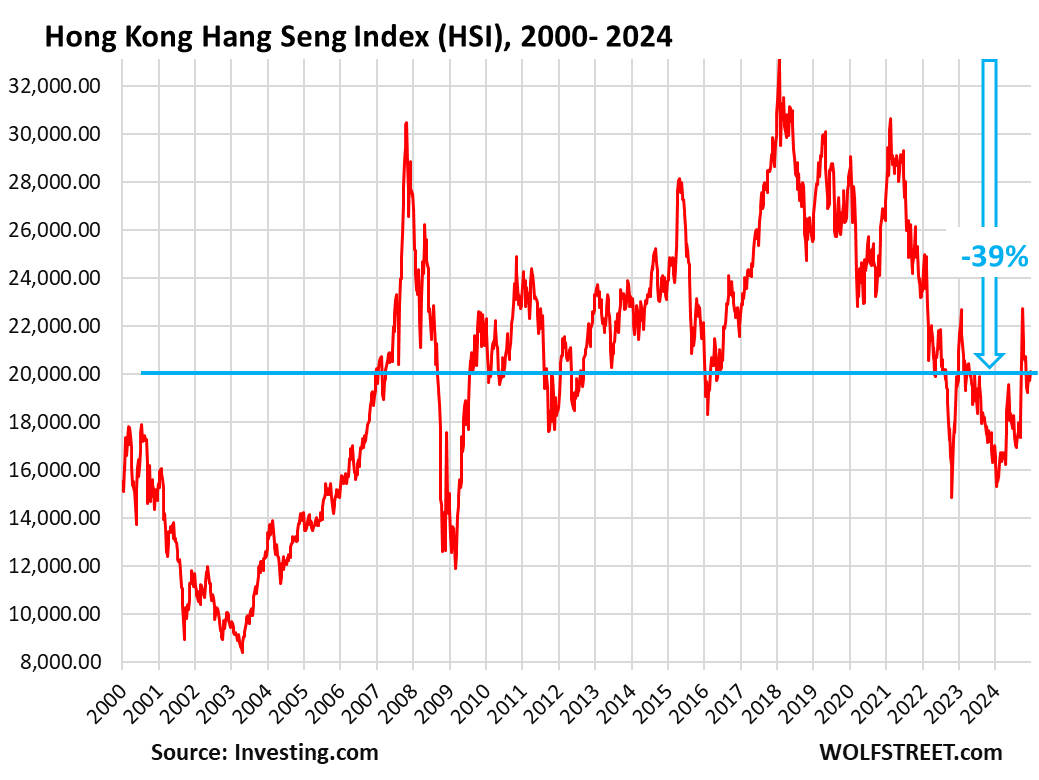

Hong Kong’s Hang Seng Index (HSI), -34% from the 2007 high:

- Closed 2024 at 20,059

- Year-over-year: +21.3%

- From all-time high, January 2018: -39%

- From prior all-time high in 2007: -34%

- Back where it had first been in December 2006.

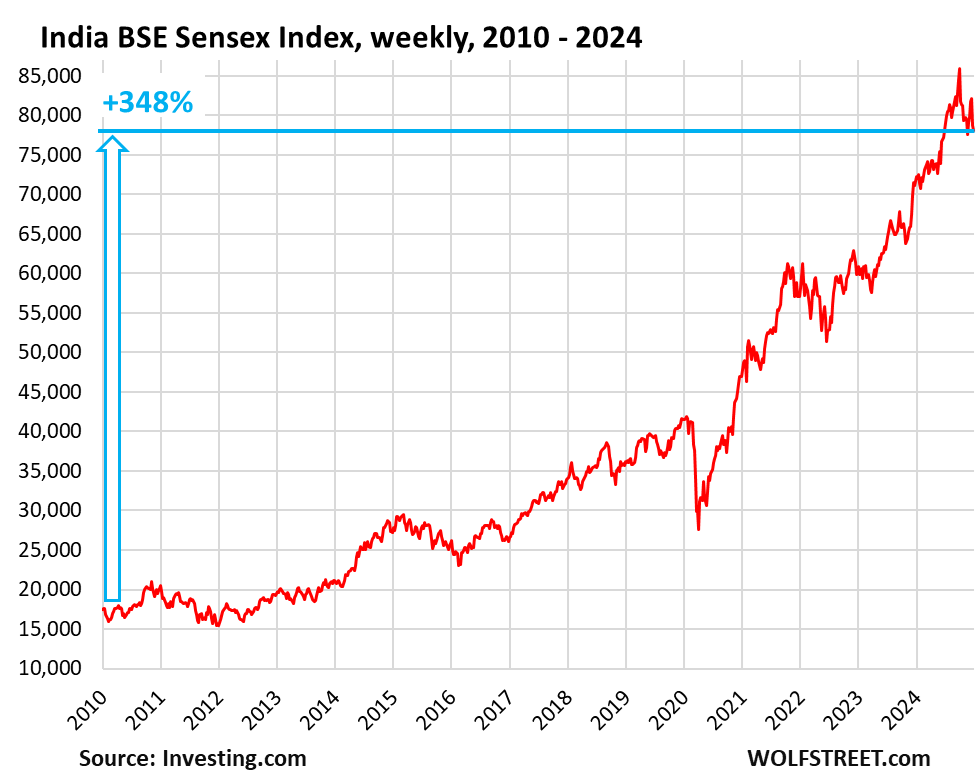

India’s BSE Sensex Index, +348% since 2010. But the rupee swooned.

- Closed 2024 at 78,169

- Year-over-year: +8.2%

- Since all-time high in Sept 2024: -9.1%

- Since 2010: +348%

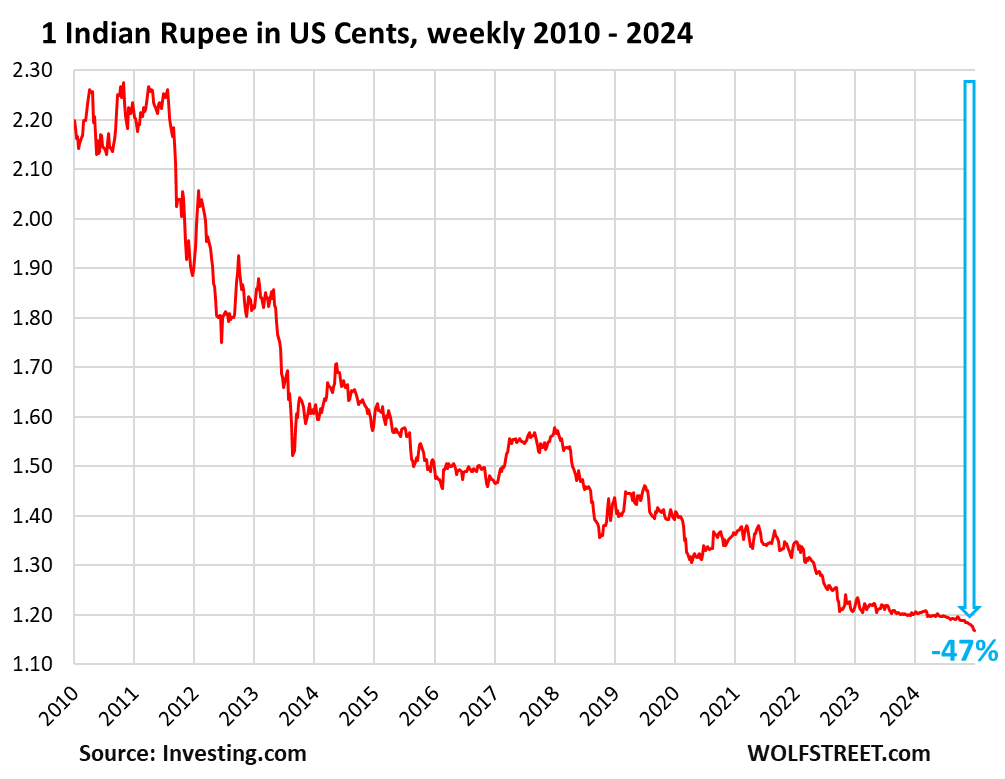

But the Indian rupee lost nearly half its value against the USD since 2010:

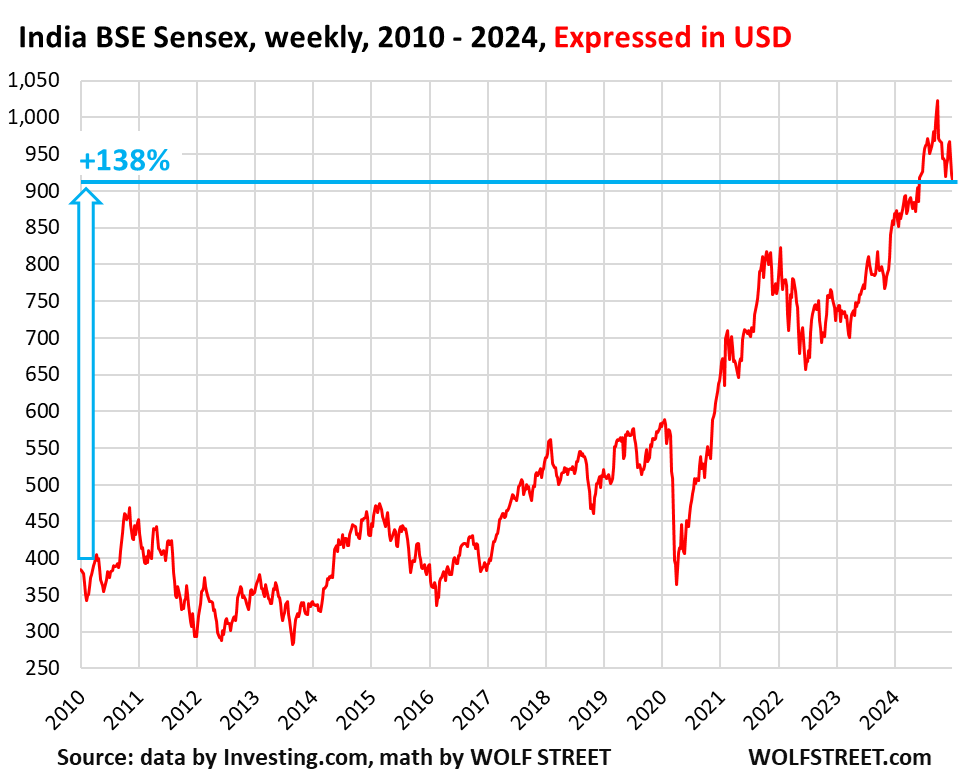

Expressed in USD, for USD-based investors, the BSE Sensex was up 138% since 2010.

- Year-over-year: +5.1%

- Since all-time high in Sept 2024: -10.7%

- Since 2010: +138%

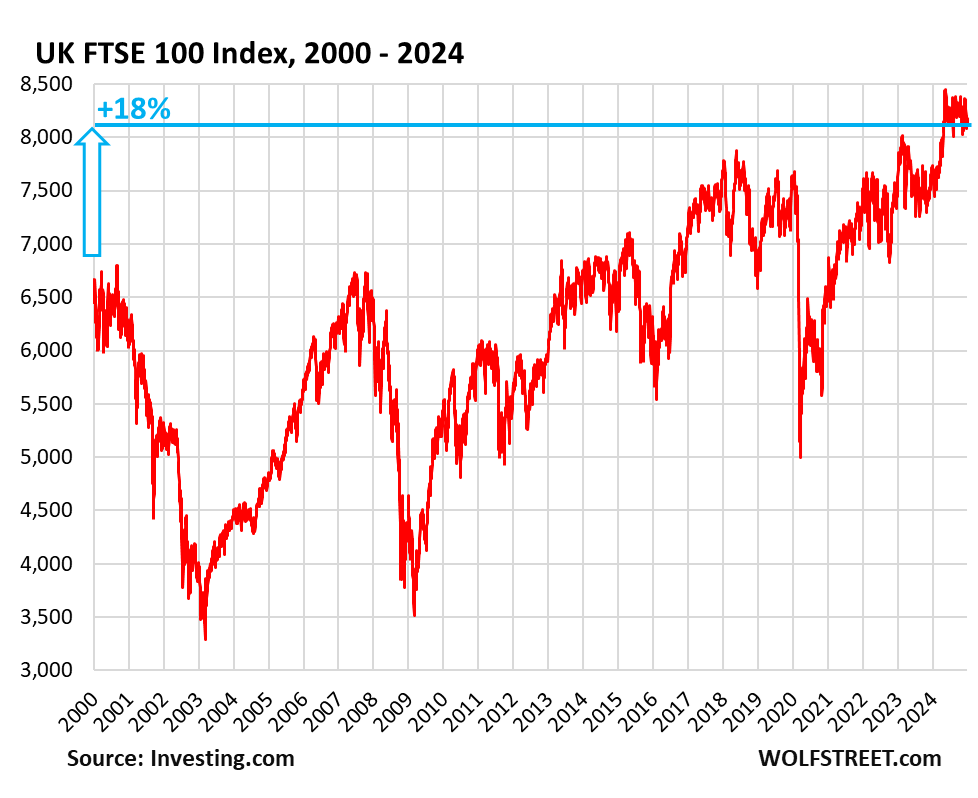

UK’s FTSE 100 Index (FTSE), +18% since 1999.

- Closed 2024 at 8,173

- Year-over-year: +5.7%

- From December 1999 high of 6,930: +18%

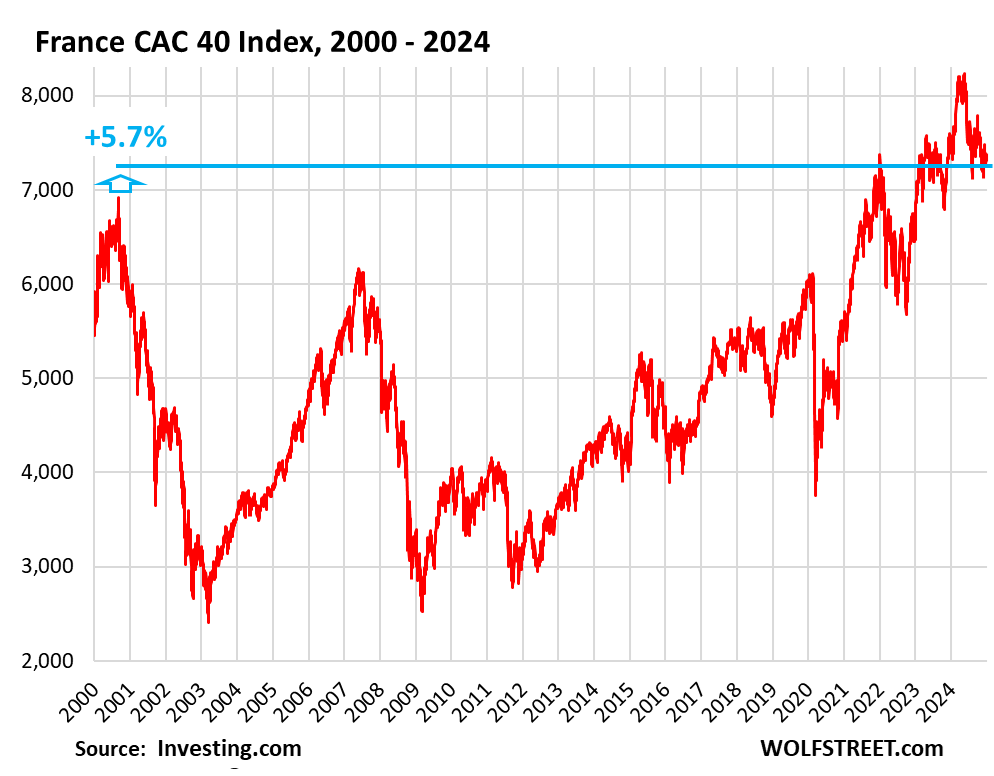

France’s CAC 40 Index, + 9% in 24 years.

- Closed 2024 at 7,380

- Year-over-year: -2.2%

- From all-time high in May 2024: -11.2%

- From September 2000 high: +5.7%

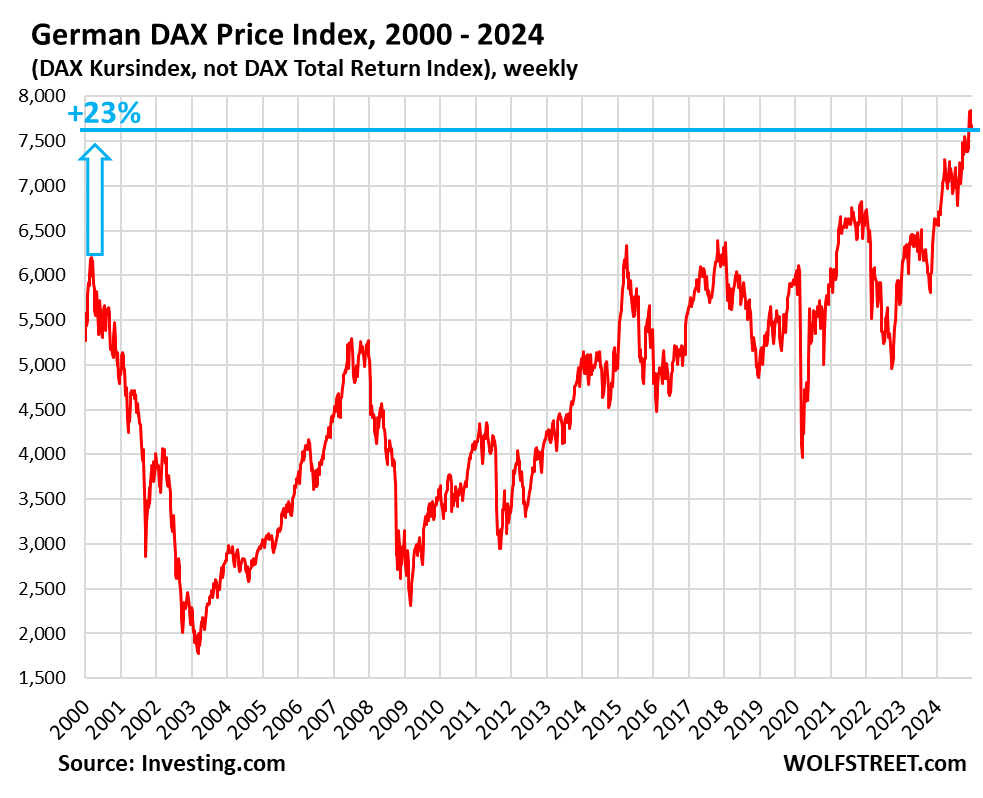

Germany’s DAX Price Index (DAXK), +23% since 2000.

The most widely cited German stock market index, the DAX, is a “total return index” that includes dividends and is therefore not comparable to a “price index,” such as the S&P 500 Index, and all the other indices here, which do not include dividends.

But the DAX Kursindex (DAXK) is a price index, and does not include dividends, and is comparable to the S&P 500 Index and all the other indices here.

- Closed the year at 7,649

- Year-over-year: +16.5%

- From prior all-time high in March 2000: +23%%

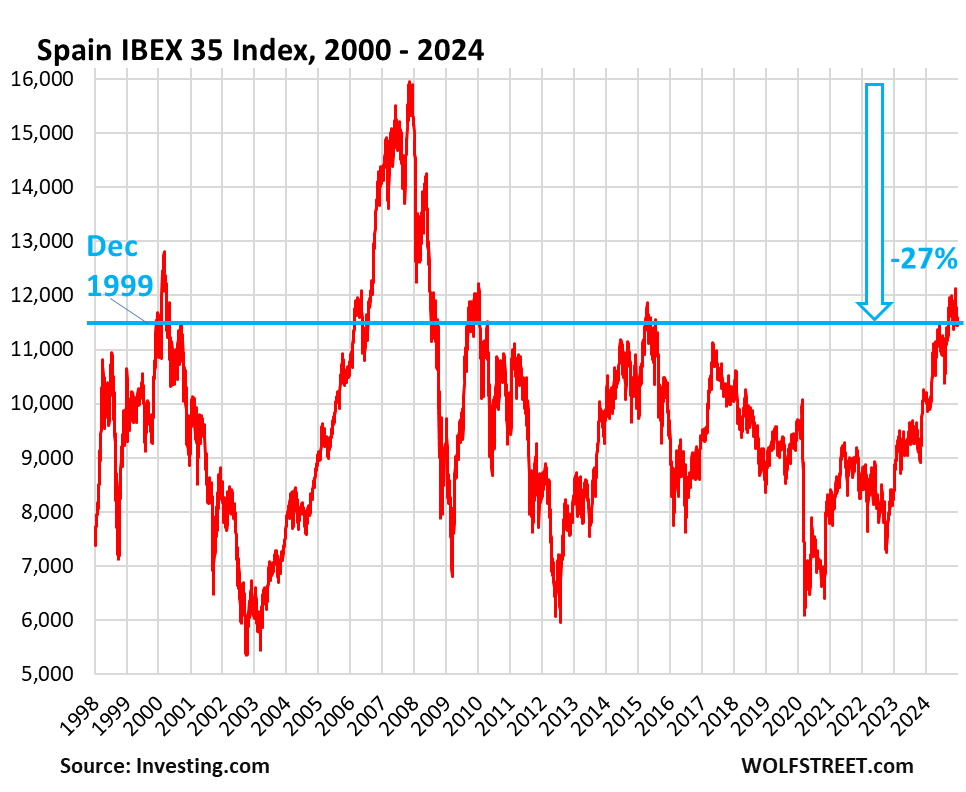

Spain’s IBEX 35 Index (IBEX), -27% from 2007, back to 1999:

- Closed the year at 11,595

- Year-over-year: +14.8%

- From all-time high in Dec 2007: -27%

- Back where it had first been in Dec 1999

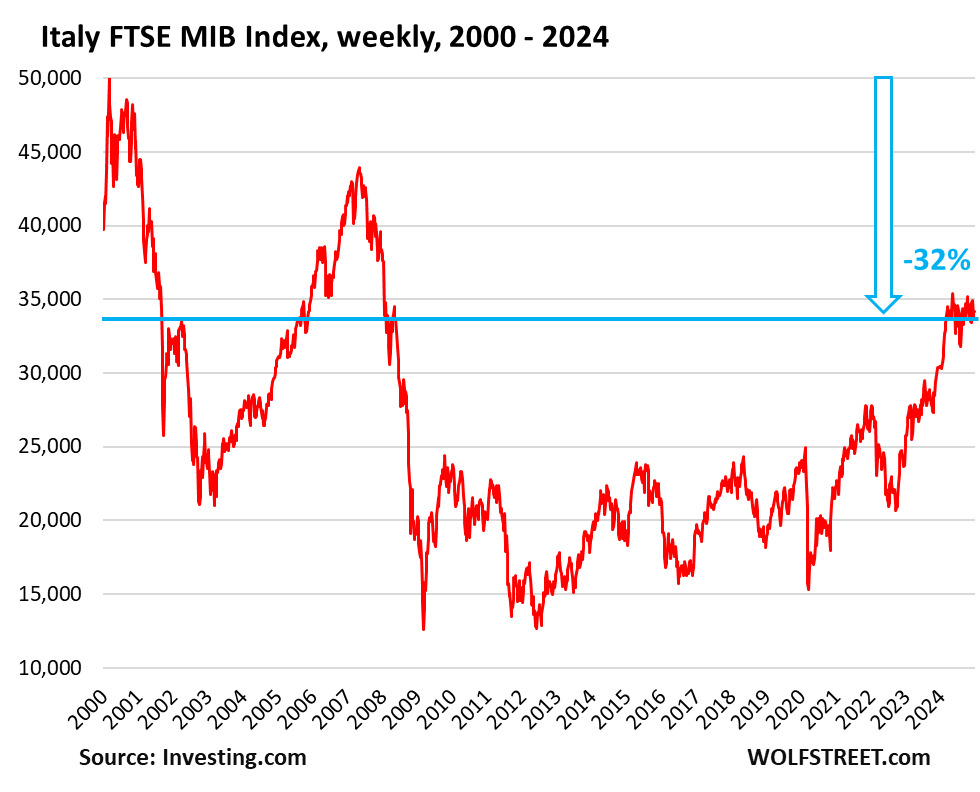

Italy’s FTSE MIB Index, -32% from March 2000.

- Closed the year at 34,186

- Year-over-year: +12.3%

- From all-time high in March 2000: -32%

- Back where it had first been in 1998

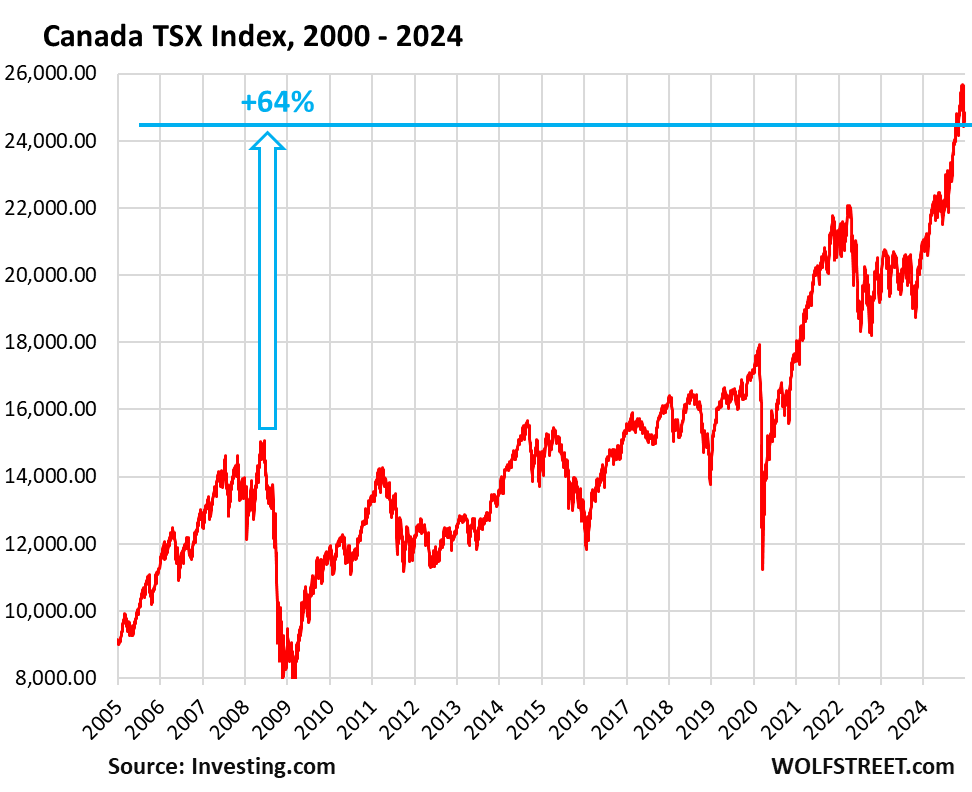

Canada’s TSX Composite Index: +64% since 2008 high:

- Closed the year at 24,728

- Year-over-year: +18%

- From March 2008 high: +64%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So if I’m reading the graphs right, I bought low now I should sell high.

It is amazing to compare the +253% gain in the US S&P 500 and Japan’s Nikkei 225 indices versus European and China’s stock indices. India too has seen solid growth the last 15 years, even with the drop in rupee value versus USD.

From these charts, it seems that world investors are bullish on the US, Japan, and India. How much of that is due to /perceived/ value versus actual value remains to be seen. Then again, perception is reality.

Returns in USD from India in that period work out to about 6.35% per annum.

A lot of corporate debt in the US would have beaten that with much less drama.

And the returns are 6.35% when the ending valuations for India market are at their highest EVER in every metric one can think of.

So yes. Stocks are best investment over the long term. It has to be….because they don’t make much sense in the short term.

I guess you didn’t read Wolf’s chart that shows foreign investors in the Nikkei are DOWN since 2020 when priced in USD.

Chris, from 2020, yes, that is correct.

If comparing from 2020 to present, the Nikkei is down in USD. Thank you for pointing that out.

I was not specific enough—I was looking at the graph from 2010 to present. Regardless, one would have been better off investing in the S&P 500 instead of the Nikkei back in 2010.

So perhaps in addition to being in an ‘everything bubble’ we might also be in a USD bubble too.

This is why I only invest in dividend paying blue chips. We could have decades of market stagnation. At least I get paid to wait. It’s enough to live on if I’m careful.

When I was a young punk I traded tech stocks back and forth. You all can have em.

But if blue chips are overvalued and fall 50%, your dividend is halved And you have to wait 10-15 years before it goes up to the point you bought it to cash out at even.

You know worst case scenario

Gotta put your money somewhere.

I am sort of with Harrold. Blue chips are less volatile in general. The more conservative stance there makes up for my very aggressive allocation into equities, I figure.

I also appreciate dividends, even though I’ve always DRIPed all my stocks. It feels like the companies that pay dividends are at least serious, whereas high flying stocks with no dividends might just be using you (more than the rest).

How do you define a “dividend paying blue chip”?

This is eye-opening and contrary to what all of the etf gurus are spouting.

Be it Fidelity or Vanguard I’m always hearing that my investment strategies are lacking foreign investments. I’ll earmark this piece of wisdom and forever laugh at that advice. many thanks W.R. !

It is interesting that we can draw entirely different takeaways from the same article. Your conclusion seems to be that the US market will continue to dominate going forward thus avoid foreign stocks. My takeaway is that the US market is probably overheated and if/when the USD weakens then exposure to foreign equities will begin to pay off.

I don’t believe foreign markets are going to gain when the bloated US markets implode.

Well that have been rough for awhile. One should diversify in them a bit, just in case us stocks stagnate and those foreign markets go crazy up up up. It’s a good hedge.

Past returns are not necessarily indicative of future performance.

It’s kinda hard to pick only winners every year….

I invested in a South African ETF in 2019. Held for a few years; consistently had a negative return. I cut my losses and sold. Didn’t bother looking elsewhere in the world to replace the funds because the US market has been booming.

Great topic and presentation, Wolf!

Would using the RSP or some other equal-weighted U.S. Large Cap index with a suitably long track record alter the picture of US stock outperformance vs other global markets? I suspect not much, but would be interested in your thoughts.

Also, you mentioned that the DAX includes dividends, but the other indexes don’t. Any other color you can add to that subject? Specifically, are the dividends in any other countries significant enough to alter general conclusions?

Thanks for the unique service you provide.

Note that I used the DAXK (“DAX Kursindex”) which does NOT include dividends and is therefore comparable to the S&P 500 and the others. I did NOT use the DAX for that reason.

Just wanted to point out that most of the rise in the S&P500 can simply be attributed to multiple expansion, with trailing P/E going from about 15 in 2012 to 30 today. Although much of this insane devaluation can be attributed to investors’ being made numb by the Fed’s easy money policies, it does serve as a stark reminder to the fact that there is very little macroeconomic justification (or if you like, foundation) to the broad market’s eye-popping returns over the past dozen years. In other words, what you see is mostly thanks to speculation.

that’s absolutely right, and absolutely true most of the 50% gain in the past two years. investors, both domestic and foreign, and absolutely convinced that there is no better place to invest than in u.s. stocks, and will buy at no matter what the valuation. they’re similarly convinced that the fed will ride to the rescue.

if enough people believe it, it becomes a self fulfilling prophecy, until someone happens to shake that belief. then watch out.

You must also consider that 80% of the market is bots buying automatically with no regard for fundamentals, valuation.

P/E expansion is justified when LT interest rates are dropping because of the stock price discounting effect. From 2012 to 2022, rates were generally dropping, which explains the massive rise in P/E.

Conversely, P/E ratios should retract when LT interest rates are rising. Because they have not retracted in the face of LT interest rate rises the past couple years, stock markets are scaling a tightrope from Wall Street to the Heavens.

Investing these days is more religion than science. It requires faith in our Lord the Money Printer to part the ocean and avoid all future recessions.

This, too, is 100% correct.

It was the bayonets of ZIRP and yield starvation that doubled PEs (dubiously).

Now those doubled PEs are Wiley Coyote, 10 feet over the cliff – holding an Acme anvil.

“most of the rise in the S&P500 can simply be attributed to multiple expansion, with trailing P/E going from about 15 in 2012 to 30 today. ”

Thanks, Max – this can never – ever – be repeated enough.

I realize the S&P is highly manipulated, hocus pocus, smoke and mirrors. But looking at these charts has me wondering why almost all canned financial advice has a standard portfolio with 30% equity allocation to foreign stocks. That doesn’t even seem like it would have worked out well for my parents or grandparents. Of course, now that I said that, I’d be afraid to get rid of mine in case all the US lossie-goosieness blows up in our faces…

Foreign stocks crushed US stocks during the 1970s and 1980s.

From 1968-1982, the S&P 500 (including dividends) lost value in real terms (ie, after adjusting for inflation).

It is part of the S&P index strategy. They rebalance and remove the losing stock each year and replace them with growth stocks. That is why Buffet says it is hard to beat the SP500. It is filled with the best 500 US stocks YOY.

Basically, the argument for foreign stocks is diversification, the widest possible diversification – in the name of lowering volatility of returns, therefore maximizing aggregate return over time (the math behind equity diversification really is fairly solid over time).

But the diversification argument tends to ignore foreign exchange rate movements – especially those generated by nations desperately trying to keep their export levels up by depreciating their own currency. That macroeconomic legerdemain was not historically something that diversification arguments took into account.

There are a lot of desperate, fundamentally rotted through economies out there – using money printing and other financial manipulation to paper over their fundamental lack of intl competitiveness.

Thanks, Wolf, for the reminder that currency valuations matter. The financial press is full of screamers and shouters that tout Emerging Markets and other rotten investments. The chart that shows investors are DOWN after adjusting for Yen weakness if they put money in Japanese equities is very revealing.

There is a lot of shrill advice. But surely it is straight forward to understand when looking at overseas stocks there is the extra variable of currency exchange rate to consider.

Which at times is not a bad thing at all.

Dog food for me, steak and lobster for thee.

Dog food eater works hard, is kind and generous..says hello and smiles. Lobster boy is fat and greedy and and a real ass.

I no longer want to be dog food eater,

I’m going to hang out with lobster boy and learn the secrets of this market madness.

Thanks wolf.

And lobster used to be considered the poor man’s protein. Times are a changing.

It has been said before – but imagine just how hungry the first person to eat a lobster was.

That’s like seeing a foot long cockroach and thinking mmm.

”’Actually”’ HT, according to some folx who have studied the dog food versus lobster diet, ya really might be better off ”being a dog” as one book has it recently.

OTOH, who, repeat, who would want to be a dog if they did not know anything about the GREAT WHEEL(S) on which some think ALL ”sentient beings” grow and go back and grow again until reaching ???

Of course, others think ALL beings are on a similar path, and both can supply TONS of apparently sincere data to support their beliefs…

Just have fun with it,,, ALL of it, is my current ”belief.”

Anyone want to comment on the fact that corporate profit margins are up 50% from 2000 and 3x since the 1990s?

https://fred.stlouisfed.org/series/A466RD3Q052SBEA

Meanwhile the S&P 500 is up roughly 75% since 2000.

Question is, how long can the price gouging continue?

The rise in $ profits has overwhelmingly been driven by:

[1] A drastic fall in bond interest rates — making it cheaper for businesses to borrow (from 15% in 1980s to 3% in 2021).

[2] A drastic fall in the EFFECTIVE corporate tax rate (from ~35% to ~13%).

[3] Increase in revenues (driven by the booming US adult population and, partly, by US corporations selling more abroad).

Operating profit margin % surprisingly did not expand much. In other words, growth in $$ profits have less to do with “price gouging” than some politicians would want you to believe.

Items 1-3 alone mechanically explain something like 90% of REAL (inflation adjusted) explosion of corporate profits since the 1980s.

Will the tailwind trends of items 1-3 continue over the next 20-30 years? I’ll let you answer that.

1) Bond interest rates fell dramatically (ZIRP) starting in 2010, but it was only in 2022 that profit margins exploded.

2) Trump’s lower tax rates took effect in 2018. FRED margin figures are pre-tax.

3) Business sales increased about 28% starting in 2021–inflation would have accounted for 20% of that. The rest would have either been increased volume or price gouging.

I tend to agree with Isabella Weber that greedflation was taking place. She examined the data. Most mainstream economists denied that oligopolistic industries would ever dream of gouging their customers!!!

https://www.newyorker.com/news/persons-of-interest/what-if-were-thinking-about-inflation-all-wrong

I think Congress has failed to do its job. They have allowed monopolies to emerge in all sectors resulting from ZIRP. Large organizations raised debt and bought out their struggling competitors.

Consolidation in healthcare, services and lo and behold car washes too.

FTC has been sleeping although Lina Khan revived it a bit. But I suspect that will also end now.

High profit margins are also a result of fiscal debt. Overspending by government will pad profit margins.

Average Joe has been screwed over. US economy now resembles quite that of India (where I grew up). Labor is paid salary and it is quickly polished away by corporates who have been given monopoly power in various industries.

Adani is a great example. The company has zero IP but in a matter of decades it has grown to be one of the largest country in India by getting monopoly rights and zero cost debt guaranteed by the government. Plus the government made sure public projects were all executed via the company.

In the US the government is not actively involved but is surely a bystander allowing all of this to go on.

We need the rich. We need to keep them rich and maybe even richer.

After all it is their spending that keeps the economy going. We owe them. So let us not complain :)

“Question is, how long can the price gouging continue?”

It’s not gouging if you have a choice and pay it anyway.

Suggests to me that valuations are pointless or at least not a good indicator of much for investment purposes. As long as USD is best game in town along with low tax rates things will just continue to rise, until of course they don’t, and then the cycle starts all over again. Hard to envision any time in the next few decades where it isn’t the best bet. The US government will ensure the corporate sector and markets are protected. At least revenues for government will be higher with capital gains over 2024. Probably will save California budget issues for a year.

Valuations are not a good short term indicator but are pretty accurate estimating returns over the longer term. Based on historical performance, he current very high valuations predict low returns over a period of about 10-12 years. Hussman’s articles have a lot of explanation and charts.

“predict low returns over a period of about 10-12 years.”

Or just a fall off the cliff with a faster return to reasonable annual returns.

It isn’t like equity markets historically were a series of “permanently high, if stagnant, plateaus.”

Busts are more common.

More like mornings at the vomitorium, after the drug-induced orgy.

Wolf,

The Canadian to US dollar briefly dipped down to 0.56 on Dec 21, 2024. What could have caused this?

Vuk

I have allocated 25% of my long-term investments to international stock index funds (VTIAX and FSPSX), 55% to U.S. stock indexes, and the rest to bond and money market funds. International has lagged U.S. stocks since the global financial crisis, and maybe U.S. dominance will continue because of Silicon Valley, but past performance is no guarantee of future performance. If the dollar falls or U.S. equities plateau, international stocks may outperform.

Why do you think the dollar will fall?

You really need to look at total return, because dividend levels vary majorly between markets. USA and Japan about 1.5%, Europe about 3.5%. Makes a substantial difference over the long run, though USA would still be ahead of the pack.

even with dividends reinvested U.S. stocks have dominated international.

over the past ten years, the average annual total return (dividend reinvestment included) of Vanguard’s S&P 500 index (VFIAX) was 13.06%, versus 5.06% for the total international stock index fund (VTIAX).

https://advisors.vanguard.com/investments/portfolio-construction-tools/compare-products/result?selection=VTIAX,VFIAX

I have no idea whether the dollar will fall, but international exposure will provide better returns than all domestic if the dollar does fall, or if the us economy lags the world economy in the future.

No correction for dividends?

Some things look less bad if dividends accounted for?

Check Argentina. Bought when Milei was elected.

Check the ARS in which this stock market is denominated.

When I look at QT by the FRB and think about the multiples expansion such as Tesla and the rise of PE and the private debt markets I am very surprised at the amount of liquidity that still sits in the financial system . Maybe the PE debt has something to do with the availability of credit