The office-debt meltdown keeps getting worse. The motto in 2024 was “Survive till 2025” via extend-and-pretend. But now what?

By Wolf Richter for WOLF STREET.

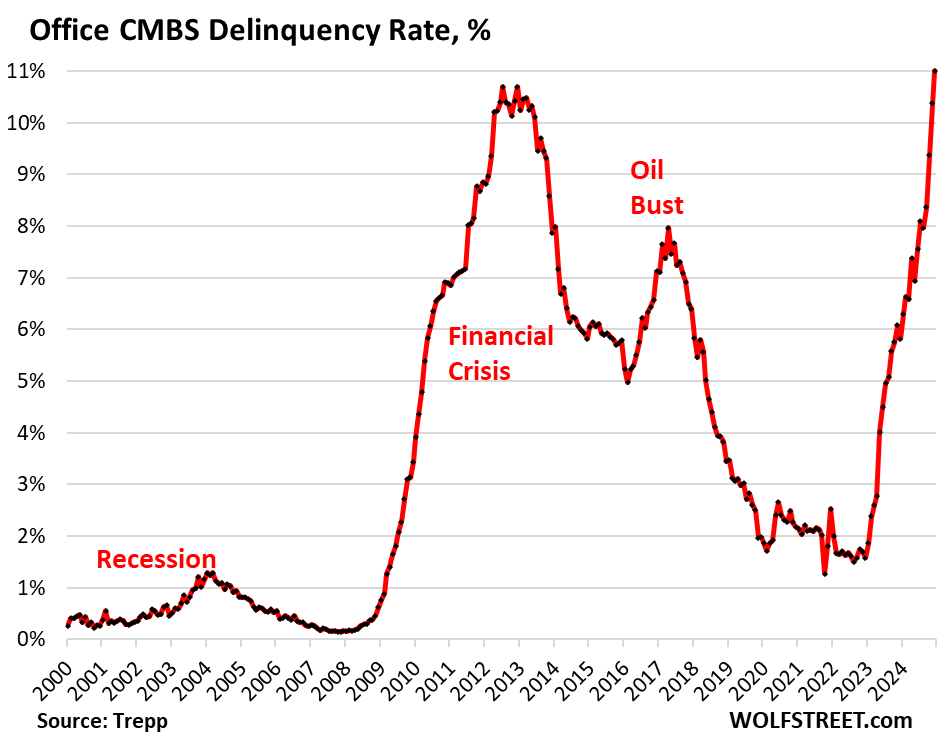

The delinquency rate of office mortgages that have been securitized into commercial mortgage-backed securities (CMBS) spiked to 11.0% in December, a new all-time high, surpassing even the debt-meltdown during the Financial Crisis, when office CMBS delinquency rates peaked at 10.7%, according to data by Trepp today, which tracks and analyzes CMBS.

Over the past 24 months, the delinquency rate for office CMBS has exploded by 9.4 percentage points, from 1.6% to 11.0%, from everything-is-just-fine to disaster.

The office sector of commercial real estate is in a depression, and office debt just keeps getting worse: an additional $2 billion in CMBS office debt became newly delinquent in December.

Of the major sectors in CRE, office debt is in the worst shape, with its CMBS delinquency rate of 11.0%, compared to lodging (6.1%), permanently troubled retail (7.4%), and multifamily (4.6%). But CRE debt on industrial properties, such as warehouses and fulfillment centers, thanks to the continued boom of ecommerce and the brick-and-mortar infrastructure it requires, remains in pristine condition with a delinquency rate of just 0.3%.

The “flight to quality” split the office market in two. High vacancy rates in the latest and greatest buildings allow companies to move from an older office tower into new fancy digs, while downsizing office space at the same time. As they leave older office towers, new tenants to replace them are hard to find, and the vacancy rates of those older office towers skyrockets, thereby speeding up their demise. It’s those older office towers that are on the problem list, not the latest and greatest towers.

Mortgages count as delinquent when the landlord fails to make the interest payment after the 30-day grace period. A mortgage doesn’t count as delinquent if the landlord continues to make the interest payment but fails to pay off the mortgage when it matures, which constitutes a repayment default. If repayment defaults by a borrower who is current on interest were included, the delinquency rate would be higher still.

Loans are pulled off the delinquency list when the interest gets paid, or when the loan is resolved through a foreclosure sale of the property, or a sale of the loan, generally involving big losses for the CMBS holders, or if a deal gets worked out between landlord and the special servicer that represents the CMBS holders, such as the mortgage being restructured or modified and extended – the infamous extend-and-pretend.

Extend and pretend has been a feature in 2024, and as a result, the problems are getting dragged into 2025. Extend and pretend can get lenders through a temporary crisis, but not through this kind of structural reckoning.

Extend and pretend came with the motto, “survive till 2025,” because, you know, in 2025, the structural problems of office CRE would somehow go away as the Fed would cut interest rates back to zero, or whatever.

The structural problem is that no one needs all this office space, amid huge vacancy rates in office buildings across the US. Landlords default on their interest payments because they don’t collect enough in rents in their semi-vacant buildings to pay interest and other costs. And they can’t refinance maturing loans when the building doesn’t generate enough in rents to cover interest and other costs. And they cannot sell the office tower and pay off the loan because prices of older office towers have collapsed by 50%, 60%, 70%, or more, and in some cases, office towers sold for land value.

The glut is a result of years of overbuilding amid hype of an “office shortage” that led companies to grab office space as soon as it came on the market to grow into it later. But during the pandemic, they realized they don’t need this unused office space, and they put it on the market for sublease, adding to the office glut.

The Fed has cut interest rates by 100 basis points, but at its December meeting projected only 50 basis points in cuts for 2025, and during the press conference, Powell threw some doubts on those, lamenting that the Fed still had “some work to do” amid re-accelerating inflation in an economy that is growing well above its 15-year average.

A lot of CRE loans are floating-rate loans whose interest rate is pegged to short-term rates, such as an average of SOFR. Lower short-term rates bring some relief, but won’t solve the structural glut of office buildings, and owners of nearly empty older office towers still won’t be able to make the interest payments even at lower interest rates.

A good thing for US banks is that a big part of office mortgages has been broadly spread across investors around the world, via CMBS and CLOs, or directly. They’re held by bond funds, pension funds, insurers, private and publicly-traded office REITs, mortgage REITS, PE firms, private-credit firms, and of course foreign banks. Those mortgages not held by US banks pose no threat to the US banking system.

But US banks also hold a pile of office loans, and some have already disclosed big write-downs of their office loans, so some of that stuff is getting cleaned up, but lots of troubled mortgages were extended in 2024, and now there’s 2025, and regulators are getting impatient with this extend-and-pretend.

The office-debt write-downs dent or demolish earnings for a quarter or two, and the stock drops, and maybe some smaller banks will choke on their office debt and collapse, but that hasn’t happened yet.

Office debt alone isn’t big enough – at less than $1 trillion, it accounts for only about 16% of total CRE debt – and is held too broadly by investors, such as these hapless CMBS holders, to do serious damage to the US banking system.

Office-to-residential conversions are only feasible for some office towers. See my discussion and figures at the top of the comments below.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’ll just add here what we’ve said before:

Conversions of office towers to residential are taking place, and the numbers are growing but minuscule because many office towers cannot be converted for a variety of reasons, including their large square floorplates and the costs of conversion to where it would be cheaper to tear them down and start from scratch with a modern building.

Office buildings converted into residential across the US, by year, based on their dates of completion, according to data from CBRE, cited by the WSJ:

There are now 71 million square feet of conversions planned or under way. But that’s only 7.9% of the 902 million square feet of vacant office space in the US, according to estimates by Moody’s.

true and NOT TRUE

reason is simply city/county planners DO NOT WANT THEM

ex. huge 100,000+ sf kmart

perfect location in Tucson for said conversion(many others now available)

could take out entire floor of concrete/put in infrastructure, etc.

make 250 1 bedroom/2 bedroom LOW INCOME sect 8 housing

nope leave empty instead

When you tear down the existing building and rebuild something completely new on that empty land, that is not a “conversion”.

Unless you think that you can install a bunch of interior walls inside a 100,000 foot k-mart and expect people will want to live in dungeons without any sunlight or direct exit in case of fire?

Zoning restrictions may be a problem in many cities, but zoning can do nothing to fix the infeasibility of turning most commercial buildings into residential buildings

sure wouldn’t want to put in windows and other amenities like plumbing

and if it is LOW INCOME sect 8 housing why are we concerned

of course we can just push them into homeless encampments around cities

take a look at many big apartment complexes – they are hotel/motel with no views/just 1 window and courtyard

so few have VISION

and understand infrastructure

Empty K-Marts make nice storage facilities if they are not in a prime commercial location. If work from home for jobs not designed for work from home is more productive for an organization then the companies would not finally be waking up and bringing people back.

KMART stores are NOT office buildings jd!

Having done cost analysis for remodel works for hundreds of ”stores” as well as at least a hundred ”office blds” over the last 30 years, especially from 2000 to 2020, I can testify SOME of each ARE able to be converted to residential, but many fewer of the ”big boxes” will be financially feasible for various reasons.

Each and every such candidate must be analyzed carefully for structural challenges in addition to the financial challenges.

Probably why I was getting recruited recently after being fully retired from this exact work many years.

Whoever would have thought that the end of QE is like the fifteen or so years of QE on the way up, only in reverse.

No Joe that’s not how it works. If you want 250 apartments you need 250 and toilets. An office building doesn’t have the plumbing for 250 toilets scattered here and there across the floorplan. What about bathtubs and showers? Again, nobody built the plumbing for that when they designed a building to fit cubicles into.

That’s one reason why the math pencils out that it’s better to just knock the whole thing down and build apartments on the land instead of trying to convert most office buildings. As Wolf says, certainly some can be converted – but as I demonstrated it’s not always that simple.

Why take out the concrete? Those buildings have 20-30′ ceilings. Build on top of a perfectly good foundation (raise the floor for sewer and water). Easy, I’ll do it.

Retrofitting to data centers is a less expensive solution than conversion to residential. All of the objections to converting to data centers fail because warehouses, even customized warehouses, are less costly and less trouble than residences for professional complainers.

Yes, and they’re already doing some of it. The problem is getting that kind of power to a bunch of data centers in the central business district. Data centers are huge power hogs. That’s why the big data centers are in open areas to which the utility can run high-voltage powerlines.

In terms of the city itself, conversion to data centers would further suck the life out of the central business district. Data centers have relatively few employees, compared to an office tower, and they’re just a dead area. For the cities, it would be far better for investors and lenders to lose their shirts, for a developer to buy the building for land value, and to demolish it, and to build a new residential building. That will make these downtowns very lively again. And we’re going to see some of that, but it takes many years.

I’d guess CMBS holders are pressuring large businesses and the govt to bring workers back into the office. As far as the govt goes, some DoD installations have repurposed their office space or sold off all their cubicles and couldn’t bring people back full time right away. Other agencies, like OPM, have used home work for many years (well before Covid) as their employees spend their days processing paperwork, with little interaction with other workers. Their performance is easily monitored remotely. They don’t have facilities to bring people back to. SS, Medicare, IRS are probably in the same boat.

As an ex Federal civil service employee I can also say that anyone who expects large numbers of civil service employees to quit if forced back into the office knows nothing about civil service culture.

A lot of this vacant office space was unused before the pandemic. Companies had hogged office space as soon as it came on the market, amid this hype about an office shortage. And they sat on large amounts of unused office space when the pandemic hit, which is when they decided they wouldn’t need that unused space after all.

It’s not that work from home emptied out those offices; they weren’t used before the pandemic. But the pandemic did away with the hype about the office shortage, and suddenly everyone opened their eyes all at the same time. And they put their unused office space on the sublease market. And then some space was piled on top of it that had previously been fully occupied but could be shrunk amid working from home.

Sounds like the Canadian federal government return to office mandate in Ottawa, because Tim Hortons, Subway and other franchises were complaining that there was less foot traffic in the mall.

Just another way to force consumers to spend money for the oligopolies profit. Can’t have Canadians saving too much money; that’s for car insurance, gas, rent and junk food at the mall.

Gen Z,

We had the same in Sacramento with the mayor doing it. He pressured the governor to bring people back from 100% telework to 2 to 3 days a week to save downtown businesses. Still a smaller footprint with hotelling versus dedicated cubicles but generally not well received. Not a lot of quits or retirements from what I have seen. People too busy getting to the 20 years or greater and getting the extra 2% per year of service, which is underfunded. Many people I work consider their job to be UBI so just inconvenienced by having to go in twice a week. Soul sucking culture in most places I have seen.

I just read a few Reddit posts about this from the Sacramento.

It looked like the public sector workers brought their own lunch in protest, because they believed RTO is a way for them to spend money for the downtown restaurants.

The state workers have a point about RTO being imposed to boost corporate and rental profits

Gen Z,

But completely dumb to punish downtown businesses. Better to just be less productive, although a tricky thing when most aren’t productive anyway.

Glen

Depending on how well paid these pubsect workers are, they’re either selfishly punishing downtown restaurants, or responsibly saving money as the cost of eating out has gone up substantially.

I bring my luch as often as possible because I can’t afford to eat out all the time. But 10 years ago I sure could – back then Subway still had $5 footlongs, and I could get a burger and fries for $6 at the takeout joint around the corner from where I used to work.

Personally, putting aside the posturing, I’m glad that I got to go to work each day. I’m a WW2 baby so a different experience.

Working from the basement had a different connotation then, as does most of the chaos in the world since my generation relinquished the reigns of responsibility, to the next generation. Short of wiping out the human race, they’re not likely to do worse than us.

Yeahhh … the Federal workforce is the most resilient of the American workforce. Majority of the workforce produces very little work of value. They act totally independent and not afraid of being fired.

Ahh? Shuffle paperwork at home? Is not the Gubernment mostly “paper free” If so, it is not the result of the “paperwork Reduction Act” but digitization of the information management.

High technology appears to not increased the productivity of the Federal workforce or reduce response time. Today those who interface with federal agencies file their own forms online; telephone ceased to be a mode of communication since the invention of Voice MAil.; snail mail disappear into Dumbbell Nebula; in person visit is virtually impossible as the federal offices are guarded by gun toting rent a cops reinforced by various arms bearing Federal police forces- YET, the number of Federal workforce keeps increasing a rate greater than population growth.

How did the American public benefit from the advent and utilization of Information Technology by the US Federal Government – very little, if any at all.

“YET, the number of Federal workforce keeps increasing a rate greater than population growth.”

Lots of stupid internet BS circulating out there about federal government civilian employment. So here it is as share of total employment. The temporary spikes are the census takers every 10 years, and Covid-plus-census.

I no longer view this as a money and finance site. This is a Mythbusters site.

And I thank you.

Class A sells at a 50% haircut.

Class B goes back to the bank and bankers are fortunate for it to even re-trace.

Class C gets sold for land value — if that.

Prepare now — ’25 won’t be kind.

can’t wait for the $81B apartment loans coming due

Residential rental rates are not dropping, and vacancy rates are not rising. So why would apartment renewals be anything except business as usual?

Two reasons.

Reason 1: Many multifamily CRE loans are currently ~3% interest. Net operating income on these properties is typically < 2x the interest cost (often < 1.5x) at 3%. But mortgage rates are now ~7%. Lenders wouldn't lend $$ at 7%, because the property doesn’t generate enough $$ to cover a 7% interest payment.

Reason 2: Rental rates are flat or dropping in many metros — and certainly not rising like 2021-2022. Meanwhile operating costs (insurance, property taxes, maintenance, labor) are rising. So operating income on many multifamily properties are trending flat or even falling.

It’s a mess.

I realize all real estate is local, but rental rates are dropping between 10 and 20%, depending on submarkets, in SW FL(Collier, Lee & Charlotte Counties). Vacancy rates have risen from 3 to 5% in 2022 to 12% to 25% today. Renters definitely have more bargaining power than landlords.

The writing was on the wall by Fall 2020…how were borrowers/lenders able to stall for so long…and was anybody else actually served by doing so?

4 years of pretend were probably used to hunt for a lot of bag-holders…and the silent crisis likely worsened losses and delayed healing…really only to serve the interests of the borrowers/lenders who authored the underlying over-valuation disaster in the first place.

The militaristic, surveilance state costs a lot more. We are not spending money on improving the lives of the hapless civil service.

We are spending the money implementing big techs wet dream. Monetizing personality through a dossier of each individual without their consent.

I’m curious if the deep floorplate buildings can be mixed use with residential at perimeter windows and something else near core… Warehousing? Marijuana grows? Data farms? It would be a real bummer if we can’t figure out how to creatively reuse what we have.

data farms going were power is

columbia river – say hood river, OR – no population but huge water and electric(hydro=cheap)

Microsoft, Amazon all like it

residents not so much

taking is still taking

Data farms will eventually go to Canada – where it’s cold and there’s a lot of natural gas.

How much of a data center’s power usage is cooling? A lot. And if you could reduce this cost by building one in a naturally cold environment…

The companies need the power to train their models until they agree with the companies profit point of view which is most accurately described as like a vampire too blood.

Just like a human boot licking session, no dissension allowed. The robots know where their bread is buttered.

“Fix or you’ll be picking up sticks in 2026″….

Hi Wolf,

Can you help me understand this better.

I have been reading recently about “private credit” new firms that “lend money to highly indebted, risky businesses willing to pay hefty interest rates for fast cash, with the potential to generate huge profits.”

These businesses, “Unlike a bank, amass money not from individual depositors, whose savings are protected by the federal government and can be withdrawn at will, but from institutions like insurance companies and pension funds.”

Thus, these new businesses are “legally permitted to finance tricky, highly speculative companies without reporting the details of such activities publicly. And further, without the regulatory restrictions and government oversight.”

It is estimated that close to $2 trillion dollars of private money has been raised by these firms and that it could top $4.5 trillion by 2030. This is just a guess.

I have a few questions I was hoping you could clarify.

I am curious if Trepp has any access to this private information? And how could it, if these new private lenders are not required to report it? If so, then how accurate is Trepps information? Further, how much risky private money is actually in CM, or wherever else? Could it be a lot more than assumed?

With so many new private credit firms competing to make these loans, the average spread on such loans and high-yield bonds has shrunk in the past two years.

Do you think that this new competition for risky high yield junk bonds by private credit has skewed the true price discover of the spread between junk and treasuries?

And finally, do you think that private credit could be a real concern for systemic risk and a possible threat to financial stability?

As always, thanks for all you do.

well there is lots of expensive $$ out there to lend

I even take occasional mortgage(owner carry) when feasible

just did one few months past

of course the buyers had 35% DOWN

now making 2nd profits via interest on mortgage backed by real estate I’m willing to re-own if they default

expectations of default = 25%

They likely won’t default unless it’s worth less than close to their -35% down after commissions, in which case there goes your hedge.

The whole “Private Credit” thing is either regulatory arbitrage or sales-oriented financial engineering (i.e. fraud).

The official explanation is that the Bank Regulators have made it so that the banks have to keep big reserves against loan losses, which means that the banks aren’t making money off of plain old boring business loans any more. Since the private equity guys can make loans using much less capital, they get better return on equity. The question is “When we get another financial crisis and the over-leveraged parties are going broke, will the federal government bail them out?”

The not-so-nice explanation is that the banks are dumping their toxic waste into these unregulated entities, such that the people buying then will be the Bag-Holders when the next financial crisis happens.

Either way, it sure looks like the insiders are transferring their risk to somebody else.

Very well said and I agree entirely.

It is very, very scary that investors/regulators seem to be intentionally ignoring (again) the inherent adverse selection/shitty underwriting issues that are created when loan makers/underwriters are able to freely/quickly offload those crappy-at-birth loans to third party investors.

Why haven’t investors learned? Yield starvation via ZIRP is one thing…but 35%+ hits to principal are much, much worse.

And why do regulators refuse to act?

A scary possibility is that DC sees the cyclical, doomed “grift” as the last “viable” American industry.

I truly mourn for everything we have lost and will lose.

Needlessly, through blindness and cheap illusion.

I’m assuming these are some of the same private creit mutual funds I invest in. There are funds that specifically focus on sr. secured loans and BDCs for example.

Some of them pay very nice dividends. The highest yielding fund in my portfolio has a 19% annual yield, although most of them are in the 8-12% range.

Still a nice juicy spread vs corp bonds, but certainly not without risk.

Well, the phrase private credit means that you are about to be sheared. Just like the old days. Sheesh.

Great report, Wolf. From 0 to 50bp cuts in 2025, there is no place to hide. There is where price discovery will find your safe space, not just office, but everywhere. For me, the odd duck is always the submarket of self-storage. When I think folks are going to pull out their junky treasure and collapse, I am pleasantly surprised. Not really retail, but not really industrial. USA and their love for junk.

I am bullish on 2025. I did two kick ass deals in 2024. 2025 is the year where folks will say “No mas!” and cash will win the day.

Happy New Year and Good Luck!

I have been watching with astonishment how the Junk Storage sub market has been growing in US for decades now. As a casual observer of the market, in the early stage of the pandemic, I expected COVID to force retrenchment of the market.

Exact opposite happened;

…the multi-decade growth trend in self storage accelerated during the COVID pandemic and demand spiked to a new high …. Self storage vacancies fell below 3%, well below the industry standard of 8%, triggering an unprecedented 40% increase in move-in rents from June 2020 to March 2022.

Since 2022 vacancy rates dropped slightly but the future is bright, according to industry analytics groups.

Interesting how the median size of teh American home increased to about 2300 sqft in 2022 from 1500, 1970, and family size decreased, during the same time period a “self storage” industry became into existence.

My cynical observation …. Hoarding, defined as “accumulating unnecessary tangible items for the sake of ownership” , could be a phycological condition. Certain stigma remains attached to seeking psychological treatment. But care is expensive and unaffordable for majority of the population. Self storage spaces costs are still very modest , say $50-200/month for average storage space. For that price range, one cannot obtain competent psychological care. So, the self storage of junk is the solution because the disease is controlled/treated more cost effectively with monthly self storage fees than psychological care/advice.

I feel we are disease free when it comes to renting a storage facility to store our “stuff”.

We managed to keep it all within arms reach in the house, garage, attic, basement, side yard and in the trunks of our 5 cars. Oh, we had stuff at the daughter’s house too (not quite arms length accessibility though)!

I think a substantial part of the increased storage demand, my case also, is high housing prices. Prior to the big spikes in sfh and rents I could afford a bigger place on my own with enough room to store everything, Since then, I’ve downsized to room rental or shared to save more and need to rent storage for stuff I don’t have space for at home. But with big storage rents increases, it’s not a lot of savings, so debatable.

1:04 PM 12/31/2024

Dow 42,544.22 -29.51 -0.07%

S&P 500 5,881.63 -25.31 -0.43%

Nasdaq 19,310.79 -175.99 -0.90%

VIX 17.17 -0.23 -1.32%

Gold 2,638.00 19.90 0.76%

Oil 71.80 0.81 1.14%

Wolf I assume the subtitle is supposed to be extend-and-pretend (not extent)?

Great coverage love your work!

Yes, thanks.

This is a very interesting article. I’m curious to see how this trend continues in the next few years.

I’m thinking it’s a tough call. Workers closing in on retirement might be best served sucking it up and returning to the office to run out the clock. The younger ones may be more inclined to do the Great Resignation thing and find a remote position where they can raise a family cheaper.

Either way, every body knows RTO is shorthand for either “we need to reduce headcount” or “we need to protect the CRE markets”. Possibly both.

It seems to me office-to-retail conversions can hit three big birds with one stone, which has been discussed here and elsewhere: #1 is raising the inventory of affordable housing; #2 is attracting people into the city core to revitalize downtown retail (e.g. to offset the loss of daily commuters due to remote work); #3 is restoring downtown construction investment (which must be in deep recession now?).

Note that HUD just released a report that the U.S. homeless population went up almost 20% in 2024, on top of a rise of 12% in 2023, so the housing problem in getting more and more dire. [ https://apnews.com/article/homelessness-population-count-2024-hud-migrants-2e0e2b4503b754612a1d0b3b73abf75f ]

Downtown is where this synergy of needs and capabilities exist. Location, location, location!

This is obviously a complex issue and needs a lot of thought. Not everyone wants a tower next door with a high density of poor people. This has been tried and often does not work out well.

The “Affordable housing” biz also seems rife with corruption and hidden costs, such as the $600K + units being built in LA with CA tax dollars. These conversions can and should be much more cost effective.

The need and the opportunity are in plain sight. What is needed is creativity — and most of all political will — to put all the pieces together in a cost effective and sensible way. Easier said than done!

Huh? How does office-to-retail conversion increase the availability of housing, affordable or otherwise?

“#1 is raising the inventory of affordable housing; #2 is attracting people into the city core to revitalize downtown retail (e.g. to offset the loss of daily commuters due to remote work); #3 is restoring downtown construction investment (which must be in deep recession now?). ” Frankly, the usual pablum with a historic record that is exactly what the money should not be wasted on.

The number one thing is family level wages and health care. The kernel that made America the golden goose. I’m surprised that the people running the government are so distant from that sentiment that they appear ignorant of our history.

Why was so much totally unneeded and unwanted office space built?

Great question!

There are a lot of things like that.

To house the swarms of undocumented individuals from every country in the world flooding across the southern border, I guess….

I thought everyone learned in 2007-08 that infinite growth is not possible. Guess not.

“Why was so much totally unneeded and unwanted office space built?

Partial answer: The lowest interest rates in 5000 years of recorded history.

Thank you, FRS.

I remember reading about all these firms who redo office space in manhattan.

They get in architects and advisors, spend millions. Apparently all to draw in large corporations into long lease deals.

It must make some sense mathematically for a profit margin, but then again, maybe it’s just an excuse to come to manhattan for whichever country owns the company do the “redo”. People like to party there

Perhaps because the interest rate was too low which encouraged excess construction which is now surplus. At the same time, e commerce was supplanting the brick and mortar traffic, their life blood.

Which is my current position.

Bingo

For the same reason that too many malls were built in decades prior, I guess. Certainly the subsequent results parallel.

Now that I think about it, the same could be said about the canal construction boom/bust in the UK in the 18th century and the railways in the US in the 19th century.

Something, something, because capitalism?

The real money is made in the development and construction. Those guys are long gone by the time the bag holders go under.

Real money is not made in the development and construction – I was thusly informed by a manager of a large firm. There is profit, but it is not a lot given the amount of risk involved.

1. Take a break from hard work everyone. Wolf from commenting and the everyone else from writing articles

2. Work From Home (WFH) ends soon even for federal workers. So, in the DC area, CMBS will be steady soon.

3. The offshoring (sending jobs to other countries) may be reversed by the new administration. Then CMBS will be high back 2025.

4. The world is changing and at a faster rate after 2020. The rate increases in 2025 (not the fed funds rate) or I am getting older.

5. Happy new year to Wolf and Commenters.

6. With all the powers vested in me by the constitution of USA, I pardon Engels of all his comments past, present and future. Even the other alternate dimensions.

“May your shorts mature in time, Longs go higher and your waist be thinner, bank balances be fatter…we get wiser”

DC Beltway traffic has been back for a few months pretty heavy. Can definitely feel it. All the people sitting in traffic is such an energy waste, like cryptocurrency.

Imagine an animal that spends significant portions of its life trading its energy for dollars to buy gasoline, only to pump it into the atmosphere while sitting in a tin can on a highway for a couple of hours every day. Madness.

Imagine being a bee, a honey bee spending its days working collecting money, to have the government come and take it all ….not so sweet.

To bee or not to bee….At least the bee gets it’s housing paid for…

And where do you suppose that money “the government” takes originated in the first place, Mr Toad?

Here’s a clue — read what’s printed on a US dollar; your picture isn’t on there, is it?

Why are you surprised by this? All humans everywhere want to consume as much energy as they possibly can. Standard of living is literally defined by how much energy you consume to control the environmemt around you.

Poor people in developing countries would love the opportunity to sit in a tin can for a couple hours a day burning gas.

DC beltway traffic is worse than even since the pandemic ended. If the WFH federal non-workers return to the office then the commuter traffic will get worse. What we need now is a transit strike. I don’t have to commute on the beltway anymore so I am not affected.

WFH Federal workers… they will continue to “simulate” work from home or elsewhere. They are unlikely to return to the office anytime soon. Federal workers are a resilient bunch. Well protected. Immune from firings. Personally, I live in the Washington DC area and I like the fact that morning traffic congestion reduced significantly since the Federal workforce changed the venue of their low/non productive activities to home or away from the office. In teh event they do return, they will demand fancier office space, which will cause delays and increase workspace expense. BUT, with a former real estate mogul in the White House, relocating forcibly Federal workers into Class A office spaces, at approximate price range of $50-60/sqft/year. That should help the commercial real estate sector.

Offshoring will continue. Too much money supports this practice. The new administration is mostly powerless to shape business policy for free enterprise. Soviet Union type tactics did not work for them; will not be attempted here. We are not well versed in history, but we are not ready to emulate the Communists and/or the German Nazi Party’s economic policies.

Something to think about … Republican party is holding extremely thin majority in the House; elections are two years way … so, the campaign already started. Trump thinks he has mandate, but, reality will become an awakening very soon when he finds that he is not a dictator and cannot defacto act as one. The cost of his dictatorial victories will be wins at great expense resulting from compromises to please both sides. In other words, the way politics has always been done in the US.

Mr. Wolf writes: “Extend and pretend can get lenders through a temporary crisis, but not through this kind of structural reckoning.” There seems to be no reason that the banks cannot just keep extending until the loan is due, just like the Federal Reserve doesn’t recognize any loss until the note is due.

“Extend” means that the loan already matured, and the borrower couldn’t pay it off, and couldn’t refinance it, and so would have headed into a repayment default. But the borrower started talking to the lender ahead of time like, “this sucker is yours if you don’t work with me,” and so the lender “extended” the loan, and maybe restructured it.

There is no loss of any sort whatsoever on US Treasuries which are held to full maturity. Why would you think there was or would be?

“ …no loss of any sort whatsoever on US Treasuries…”

Errrr, what about loss of purchasing power? Consider the real return on a 3 year Treasury Note bought at auction in 2020…

RTO public pensions are broke.

Loan modifications and deals will be made to extend and pretend further.

In this new economy, implosions are delayed indefinitely by infinitely deep pockets of interested parties.

The lenders, investors, and borrowers all pray that by the time the crash comes, it’ll already be over.

Yep, everyone who has lived through previous bubbles is waiting for the krakatoa type extinction level financial event, when private equity, hedge funds, pensions and even governments get incinerated Hiroshima style.

Until then it’s party on, fartcoin to the moon.

It’s the US dollar propping it all up – the sacrificing of the dollar, that is. All of the working class and the poor get to pay for it through inflation. RICH PIGMEN MUST NOT LOSE – EVER.

The FED and Congress have decided that the US dollar shall be devalued to the extent that rich pigmen never have to experience even the slightest dent to their net worths. Unacceptable that they should have to endure such a hardship. “It’s a big club, and you ain’t in it.”

Well, if you listen to Chris Sununu he says nothing to worry about the extremely wealthy with conflict of interest or money as they have so much it doesn’t matter and they just want to do the right thing! Always amazed at the delusional nutjobs who get elected.

He gets paid to say stuff like that….in campaign contributions. I read the other day that each US senator has to raise on average $11,000 per day to finance their next election campaign. A Governor who is looking for future rewards? Priceless.

Regular working people are not contributors so they don’t matter to pols.

I am always amazed at the delusional nut jobs who vote for them!

Thanks again DC, for adding this time and many times ”the cold and hard” truths that most folx cannot and perhaps more importantly will not look at clearly.

But, and it is definitely a HUGE butt,,, that’s pretty much the way it has always been, from the times in all of our heritages when WE the PEEDONs were actually ”owned” by the rich folx,,, through the times when we were just ”obligated” unto our deaths, usually by force of arms, etc., to today when WE are ”wage slaves”…

”The American Experiment” has definitely helped US, but really has not changed all that much in the overall scheme of things, YET.

Wolf’s Wonder definitely helps move things toward equality of opportunity, at least for us who might and do benefit if we read carefully, eh?

The dollar relative to other currencies is near the top of its post-1990 range.

Maybe it’s off the wall, but I am reminded of that weird moment in 2020 when the oil price went below zero. As in (if I got this right), it was more costly to just hold the stuff, than to pay someone to take it and bear the related costs. Is that too farfetched to imagine here? Wolf mentioned commercial property sales for mere land value, but that would require demolition in some cases, to do something with the land, right?

There are similarities, but I’d advise staying away from such a generic metaphor since crude oil is a physical commodity that has little in common with real estate. One could draw a lot of foolish consequences by comparing the two.

Oil price went negative only in the US, since it had the worst demand elasticity – and also the most financial speculators who never read the contract terms. You cannot really buy CRE and then afterwards say to your broker that you don’t understand what a 50-story skyscraper is.

Traders can blow as many MBS bubbles as they want (just like they did in 2007-8), but it’s so much more regulated now than back then. And as Wolf draws the conclusions regulators have all their eyes on these debts.

No primary producer’s price was changed because of this glitch that was all about a few speculators getting caught by other speculators. The first guys were long the oil contracts and either didn’t know they were for delivery or assumed they could sell their positions, even at a loss before the trading day ended. They couldn’t and as you heard there was no storage available. So they had to pay to have it taken off their hands.

The words ‘when oil price went negative’ because of this one day event at the US hub is like a tabloid headline. No tankers turned around.

Natural gas prices in the Permain had been zero or negative at several points in 2024.

Always well researched and thoughtful, Wolf. Credit card deliquencies are peaking too!!??

https://wolfstreet.com/2024/11/19/credit-card-delinquency-rates-balances-burden-and-available-credit-in-q3-2024/

In San Francisco there is a massive new office building at 6th and Howard that has sat nearly vacant for a number of years now. Even the “flight to quality” has its limit when there is such a massive glut of vacant space like in SF.

what kind of “massive new office building” is at 6th and Howard? Do you have an address? There are some new-ish apartment/condo buildings there, and a historic office building and some other old stuff.

How are CMBS reits holding up?

I have a collection of mortgage REIT stocks that are down a lot but I’m not reinvesting the dividends due to concern of bankruptcy or even further losses.

The Federal government sold $36 trillion of debt. All of it was sold in the market, every last penny.

That $36 trillion spent by the Federal government has put the US economy, and even parts of the world economy, on steroids.

I don’t need to wait for this house of cards to come crashing down to know that it’s going to happen.

The people at the FED and the Treasury will be the first ones to know, but they won’t tell the rest of us about it until after it has already happened and the Nancy Pelosi’s of the world have already sold everything they own to unsuspecting investors.

I feel terrible about what the Federal government has done to run up $36 trillion of debt with no inclination whatsoever to pay it down or even spend less.

But the marketplace will put a stop to their nonsense very quickly once the market wakes up and stops feeding Humpty Dumpty.

The market did it to NYC in 1975, and I’m certain they’ll do it again. They’re now just waiting for someone to break their group trance.

Because social insanity only lasts so long.

And once the Treasury can’t sell their debt in the free market, and the FED steps in to buy it, we’re going to see inflation on a scale we’ve never seen before.

Because playing with fire will always get you burned.

Up until now we have ameliorated our unnecessary self-imposed economic hardships largely through massive transfer payments to non-productive recipients. Deficit financing by the Federal Government provided the principal source funds. As we all should know, there is a finite limit to this “remedy”.

“The Federal government sold $36 trillion of debt. All of it was sold in the market, every last penny.”

Incorrect. Treasuries are also held by primary dealers which are required to make markets.

This process is neither widely known, let alone understood, in the public discourse — I believe this lack of awareness and understanding is consequential; in my darker days I wonder the extent to which outright obfuscation is at play …

Short TLT

You’re spreading BS here. Primary Dealer holdings are reported every Thursday in the afternoon except holidays. You can just look it up, instead of spreading BS here.

eg… the bigger the BS, the more people go ra-ra-ra. People love BS, and it’s hard to keep this comment platform clean. So here I go again with mop and bucket:

Primary dealers net holdings as of the last report on Dec 18:

— $251 billion in Treasury notes and bonds

— $119 billion in T-bills (out of $6.4 trillion)

— $3 billion in Treasury Floating Rate Notes

— $7 billion in TIPS

Total: $380 billion, about 1.1% of the $36 trillion!

Here’s who holds the remaining 99% of that $36 trillion:

https://wolfstreet.com/2024/12/24/who-bought-and-holds-the-recklessly-ballooning-us-national-debt-even-as-the-fed-is-unloading-its-holdings/

Mr. Jacobs, is former Senator Richard Burr (R- NC) one of the Nancy Pelosi’s of the world?

Re: “ Extend and pretend can get lenders through a temporary crisis, but not through this kind of structural reckoning.”

I think there’s lots of structural resets, like this, that won’t name a lot of sense for 2025. The game of extending will end with a vast amount of losses.

Filing all that vacant space with profitable enterprises ain’t happening next year or the next decade.

Happy New Year?

Lots of losses have already been taken. But there are more coming.

Happy New Year all you WolfStreet Filthy Animals! 🎉 🍾

The days of the office tower are over.

If you could move all these empty unused buildings to another country, almost any country, they would find thousands of uses for them. But not here in the USA….no,no,no.

Wouldn’t want to bend the codes or break the regs.

Could be wrong? Maybe other countries are facing the same issue with work from home and empty bldgs?

Yes. Other countries face the same issues, and the same problems converting office towers into residential. It’s difficult and costly everywhere.

Here is an example with Bulgaria, Eastern Europe.

In the capital Sofia, the vacant office spaces are 14 percent for class A and 17 percent for class B.

Construction of office buildings continues

As far as I remember, Wolf wrote that in the United States the vacant areas are about 37 percent and this leads to a crisis.

But there is no crisis here.

I guess this is because there is massive money laundering going on.

Do you really think that there’s a pent up demand of businesses looking to lease all that empty office space for top-dollar, but they’re being blocked by “codes and regs”??

Sounds far-fetched.

I think his angle was that the “codes and regs” prevent the repurposing of existing space into alternate uses.

Isn’t China dealing with its own overbuilt high rise crisis, but in housing?

Different set of subsidies, but leading to a similar overproduction glut.

Was wondering, does that mean rents and or condos are cheap in China? Has there ever been a glut in decent places to live here in the USA leading to inexpensive homes and rents. Also, seems prudent to have office buildings designed, built to be easily convertible to residential. That would be a *good regulation.

Happy New Year, Feliz Año Nuevo! Out with the old, in with the new.

Pretend to work from home while skiing, hiking and biking is proving to be quite costly in a multitude of ways.

If you can get the work done, do you really need to be remotely monitored and supervised? The work is what counts. For example, if you’re a computer programmer, you could easily do the job from home. If you’re working on modules of a complex program, the coding time can be estimated and benchmarked for. Of course, there are delays and snags; but this is built into the project specs…

My son in law works from….for years now. He starts work each morning at 6:30am and finishes at 3:30 in order to link across time zones. He is evaluated by his production. The main benefits are he wears decent clothes from just the waist up….maybe sweats and shorts waist down. (lots of computer link ups). He eats lunch in the kitchen. No commute. Converted bedroom for a decent office as opposed to a cubicle. And no office BS politics. Can pick up his daughter after school if the weather craps out.

Wolf works from home and I have never ever seen anyone so productive with research and follow ups.

This idea of skiing and biking on company time is a myth from what I can see. And as for being on the job and in person…reminds me of a boss I once had. He was described as ‘someone who works like a horse’, (the only human who regularly sleeps standing up).

My friend’s son graduated Wharton Business about 6-7 years ago. He landed a job in San Diego in Federal Civil Service. Now he’s GS-16 and work from home in Hawaii until he was offered a job in the office on Oahu. With cost of living bennies, etc. he makes $170k+ and works maybe 15 hours ‘at the office’. He said after lunch you can’t find an officer higher than a Captain on site. He hasn’t worked 40 hours in office in the last 6 years. What does he do? He laughs at that and responds “It’s classified.”

You can add…running, shopping, and the ultimate productivity enhancer…”simulating work simultaneously for another economic entity and getting paid therefor”

I live in teh Washington area and noticed that during working hours, the running trails are overpopulated with 30’s something’s running, hiking… average age of the shoppers dropped to probably 11, when one factors in the age of the toddlers being dragged along to shop at Whole Foods, Trader Joes and otehr upscale food markets. 20 years ago, both places s were utilized during working hours by population fitting mostly into retired category.

That doesn’t mean anything. One of the benefits of remote work is the flexible schedule. Build time into your day for a trip to gym, grocery store, etc… I duck out for an hour to run errands all the time and make it up by starting earlier or working later.

Also, not all work happens in front of a screen. I spend a lot of time thinking, that’s work and I need to do it away from my desk.

Why is this a problem? CEOs and upper management has been doing this for decades. They even buy/lease fancy planes and upscale lodging on company dime for upper management to travel and relax. Must be very hard squeezing calls to tell someone else what to do between golf and dinner at four seasons. The average Joe is just emulating what they see. This needs to get much much worse for it to get better. Cause there is no way upper management leeches will let their sweet setup go, and thanks to social media everyone knows what they really do.

Down this way, the golf courses are loaded with WFH guys and gals. But they do take their cell phones with them on the course. Some even drag their kids along in the cart to offset paying a sitter.

Happy New Year to all ! And thanks for a great year of content Wolf. You’re pretty awesome.

Happy New Year everyone 🎇🍾😍🎉✨🎊🎈🍸

Goodness it’s getting late! Gotta go.

Let the fuckers holding this toxic shit fuck off and die already. Let real markets prevail and deflate the assets already!

WB

You need to watch your f$ckin language. This a family friendly site.

I am not sure some urban centers are going to survive what is coming. A knock on effect of all the lost commercial office property value is erosion of the property tax base . Even the fully leased buildings, who are making their loan payments, are appealing assessments as the market value of their properties decreases. And they are winning their appeals.

There are estimates that some cities are going to lose upwards of 25% of their property tax base. There are numerous reports of urban school districts in these areas facing considerable deficits due to the combination are dropping property tax base due to reduced assessments of office buildings, and increased spending rates driven from the Federal Government rug pull of temporary Covid funds.

Since government spending reduction is never an option, this is forcing increased tax rates and shifting of the property tax burden onto the remaining residential and commercial properties. Making it even more economic to use suburban space outside of the center center taxing jurisdiction. Creates a vicious cycle of both commercial and residential flight, reduced values, assessment appeals, etc.

There is one large urban center (not Chicago) where both the 2025 county and school district property tax rates were raised about 30% due to lost tax base combined with higher spending. The rate of commercial property assessment appeals is stunning. Almost all are being won. Local papers are commenting that city center is in a true death spiral with situation expected to get worse, abandonment continue as leases expire, and the crisis likely culminate in 2028. Expectations are that the city center will have completely collapsed by 2028, school district may go bankrupt and that at about 40-50% of the existing 10+ floor office towers in the city center will need to be demolished. No one is sure who is going to foot that bill. As is noted in previous comments local papers comment that only 1 in 5 of the office towers can possibly be converted to residential. But with the property tax rates who would want to do that? Cheaper to build multi-family in the adjacent suburbs.

At least in Denver, families have been fleeing to suburbs where housing is cheaper (and environs perceived safer). That means declining school enrollment which results in less funding from the state since it is per pupil. Schools must be closed which fuels more urban flight.

It’s 2025! The year of the MAGA. Buckle up.

Tax breaks extended.

No tax on tips, social security.

Tariffs

Deportations

End of wars

Drill baby drill

Gas prices halved

No regulations

No prosecutions for the politicians or rich

End of climate change

End of NATO threats

End of education department

Compromised intelligence departments

Bitcoin reserves

It’s going to be a wild ride

Maybe one of those items is accomplished.

Bet none come to fruition.

I think you can bet large on tax breaks for businesses and the wealthy. Those folks expect results from their donations.

Everything else is laughable.

No. Not going to happen.

No prosecutions for politicians and the rich seems plausible, but wasn’t that also true in 2024, lol? Meet the new boss with impunity, same as the old boss with impunity

Oil is going down but natural gas is going up.

Drill baby drill is generally good if you want lower primary energy costs. But it’s bad if you want your oil & gas equities to go up.

I know the talk about conversion sounds good and there may be a few luxury places it would work.

Would you want to live in or near one for low income? Sounds kind and all that, but do we really want to build vertical ghettos!

You could just tear them down and create green spaces for tent cities and the homeless. The end result would be about the same.

Nearly all office-to-residential conversions are for higher-end condos or rentals, the reason being that they’re very expensive to do, and they don’t pencil out for lower-end housing. Simple as that. In General, no one builds lower-end housing unless the City creates low-income housing and the taxpayer subsidizes it. If you want a lower-end apartment or condo, you have to go to an older run-down building in non-great areas of the city. Everything new, built with private funds, is automatically higher-end.

“In General, no one builds lower-end housing unless the City creates low-income housing and the taxpayer subsidizes it.”

I wish more people realized this — the absence of this kind of public investment in low income housing has to be connected to the increase in homelessness over the past 20 years or so.

Over borrowed and overbuilt.

Warning label for crystal balls*:

Actual outcomes may differ than those predicted by this device.

*Required statement by US Federal law: FTC, NIH, Consumer Financial Protection Bureau (CFPB), SEC,

Good one cheeky,,,

”Keep it up”

HAPPY NEWEY YEAR TO ALL ON WOLF’S WONDER!!!

Reminded me of another warning label:

“Caution: Cape does not enable user to fly.”

— Mark J. Grant, author of Out of the Box, quoting a warning label on Batman costume

Which my little brother discovered at the cost of stitches in his forehead when we lived in Bedford, Massachusetts in the mid-60s …

Saying this CRE mess doesn’t threaten the banking system because the banks mostly don’t hold the mortgages seems too nuanced.

The banks may not hold most of the loans, but they have clients with large accounts (>$250k) who hold the loans.

When their clients start taking the hits and drawing down their accounts to cover their CRE losses, the banks will see a flight in deposits.

This could happen quickly, just like SVB. Word might get out again (on X and elsewhere) about certain banks experiencing the biggest drawdowns, triggering another bank run (or runs).

Then the banking system will be threatened, and the FED will inflate to bail them out, either directly or indirectly. QT will reverse into QE instantaneously just as it did in September 2019 and in March of 2023 so long as inflation is not in the double digits.

Has anyone investigated which pension funds, investment firms, etc. hold 20% of the toxic CRE assets? With whom do they bank?

Only in your wild imaginations.

I agree, there’s a good probability that the CRE collapse is the lit match to the next crisis and we’ve just been watching the fuse slowly burn.

Black rock sold some of its junk to the University of California pension fund that they had gated the exit to investors due to a no bid environment. I think part of why they did that was to delay a mark to market that would have tanked their reit portfolio. Then Larry Fink does a 180 on bitcoin, going from calling it trash to having an ETF that is one of the biggest owners of it in the world at 20 billion. The 24 election saw a lot of donations via crypto. Could turning it into a strategic asset be a backdoor bailout? Seems likely.

Josie and Pancho,

It’s just hilarious how people WANT the banking system to collapse so badly that they dream about it, and fantasize about it, and they spread BS about it, instead of understanding the facts, and I gave you plenty of facts about it in the article that shoots down your BS in advance.

Pancho, in terms of your CRE being the “next crisis,” LOL, you haven’t been paying attention, have you? It HAS BEEN A CRISIS for two years, maybe wiping out $1 trillion in value, and it continues to be a crisis. It’s already here!!! And the economy and the financial system is still fine. To find out why, RTGDFA. I told you why.

What I want to completely collapse is the collective net worths of all billionaires and hundred millionaires. I don’t care if it means a total confiscation of their assets, I want to see these a**holes on their knees weeping for what they’ve done. Give them the choice of working a minimum wage job or prison. That’s my version of MAGA.

DC

Don’t hate the player, hate the game.

I’m a partner in a commercial real estate finance company and brokerage firm in the Coachella Valley. Although we have financed office buildings throughout CA in the past, we are currently focused on cannabis CRE and destressed conventional CRE in the local market.

Last March, we were hired as property manager and the listing agent for a large cannabis CRE property in the valley. It was appraised for $17.9M in April 2022 by one of the best appraisal firms in the country. We just put out the purchase and sales agreement for signature at $6.2M. In fact, we feel lucky that we were able to get this price which is near the top of our estimated price range. The appraisal valued for the building was $661.34 per square foot in 2022, versus today’s sale price of $229.06 per square foot. Ouch!

In Palm Springs, we were recently interested in a foreclosed mid-century boutique hotel, these are very popular with guests who come from around the world. I was talking with a private money lender that I have done business with for 15 years about buying the property. He cautioned me and said that he has 4 similar properties in PS that are all in arrears due to lower stays and lower rates that are way down from last year.

For those who are not familiar with Palm Springs and much of the surrounding area, this is an upscale tourist destination that attracts about 14M middle class and up visitors per year. I also brokered the sale of the largest sports bar in the valley a few years ago, it was in operation from more than 20 years in the same location. It went under this summer.

Granted these are limited observations in a limited market area, with that said my view of the world is a lot less optimistic that what is reported in the major financial press and the corporate media.

Happy New Year.