Inflation is still in services, no progress in 6 months. Another bummer: Durable goods deflation, a contributor to cooling inflation, may be over.

By Wolf Richter for WOLF STREET.

Powell addressed the PCE price index situation in advance when he was asked during the FOMC press conference on Wednesday – as the S&P 500 was tumbling after the rate cut and Powell’s not so soothing words – how much the Fed is “looking through” some of the high inflation numbers that came out recently. And Powell replied, tinged with his dry humor:

“We always try to be careful about not throwing out the numbers we don’t like. It’s just an occupational hazard to say, ‘look, oh, those high months are wrong.’ What about the low months? We have a very low month potentially in November. It’s estimated by many to be in the mid-teens for core PCE. So that could be low. We try to look at not just a couple or three months. We shouldn’t. Our position shouldn’t change based on two or three months of good or bad data.”

And the month-to-month increase of the November core PCE price index was indeed “very low,” even lower than in the “mid-teens” that Powell had cited: The core PCE price index decelerated to +0.11%, so that would be the “low teens,” according to the Bureau of Economic Analysis today. Annualized, 1.4%. This deceleration came after the sharp acceleration the month before (blue line).

The six month-average however, which irons out some of the month-to-month squiggles, accelerated to 1.89% annualized (red), and the year-over-year reading, as we’ll see in a moment, also accelerated to +2.82% (from +2.79%).

And Powell added on Wednesday: “We have a long string now of inflation coming down gradually over time. As I mentioned, I think the 12-month headline is 2.5%, 12-month core is 2.8%. That’s way better than we were.”

And he added: “We still have work to do though, is how we’re looking at it. And we need policy to remain restrictive to get that work done, we think.”

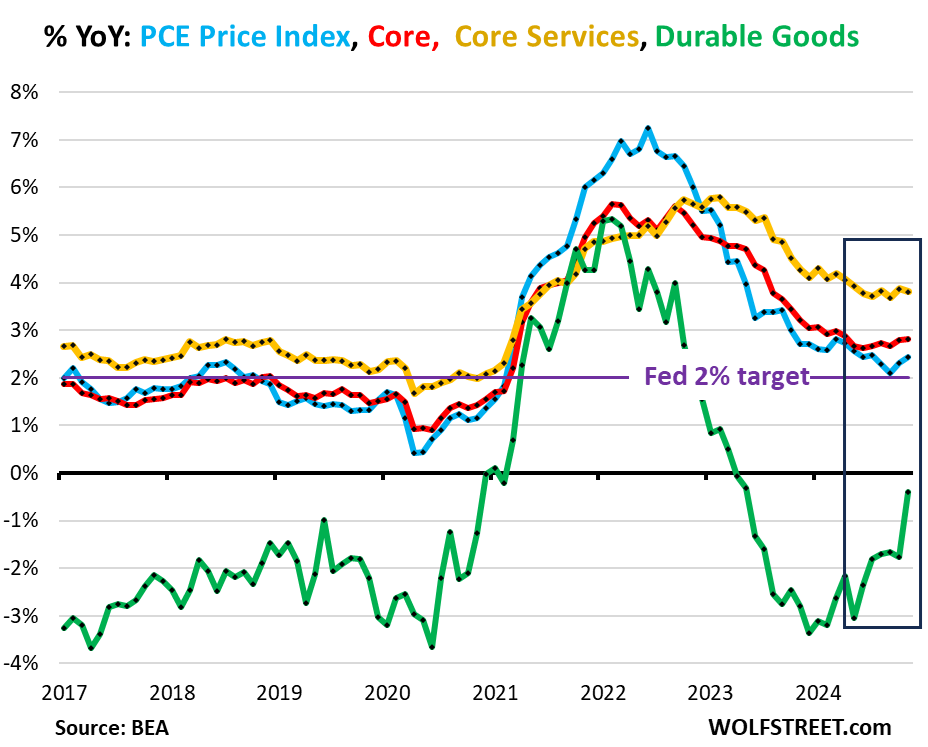

Year-over-year, the big change is in durable goods (green in the chart below). Prices of durable goods – new and used vehicles, appliances, consumer electronics, furniture, etc. – have stopped plunging, after the huge price spike in 2020 to mid-2022. With months of slight month-to-month increases and decreases under the belt, the 12-month PCE price index for durable goods was barely negative at -0.4% in November.

The falling prices of durable goods since the second half of 2022 had been a big contributor to the deceleration of inflation, but that’s now over.

As a result, the core PCE price index (+2.8%, red) and the overall PCE price index (+2.4%, blue) accelerated further year-over-year in November.

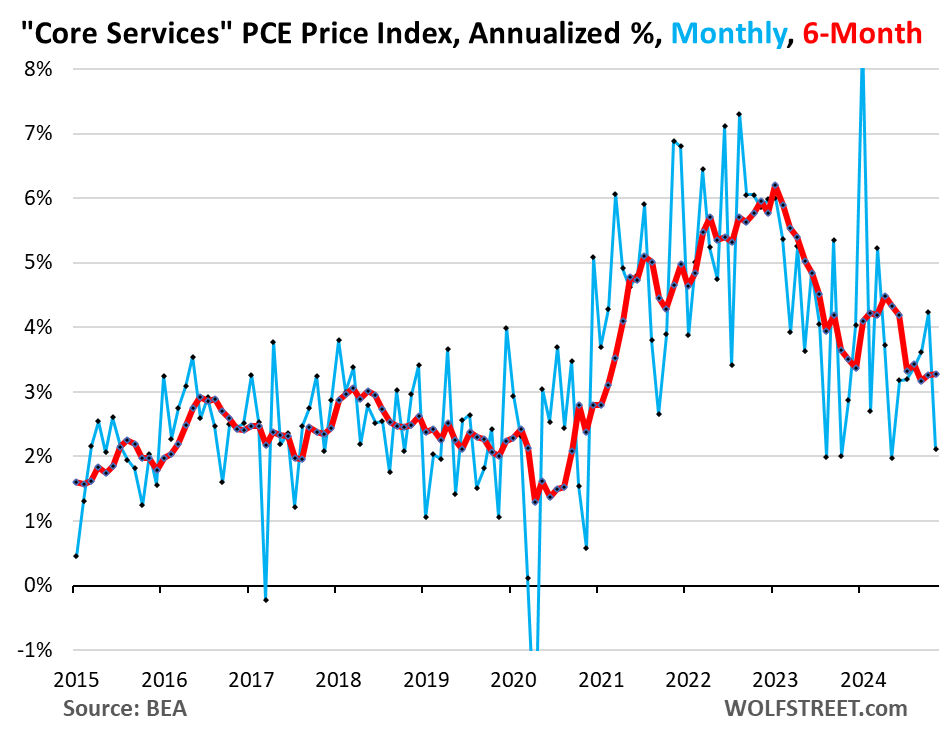

Inflation is still in core services (gold), running far hotter than before the pandemic, including +3.8% year-over-year in November, which was higher than the readings in June, July, and September, and there hasn’t been any progress at all over the past 6 months.

Core services are about 65% of consumer spending and include housing costs, insurance of all kinds, health care, education, subscriptions, transportation, broadband, personal care services, financial services, food services & accommodation, etc.:

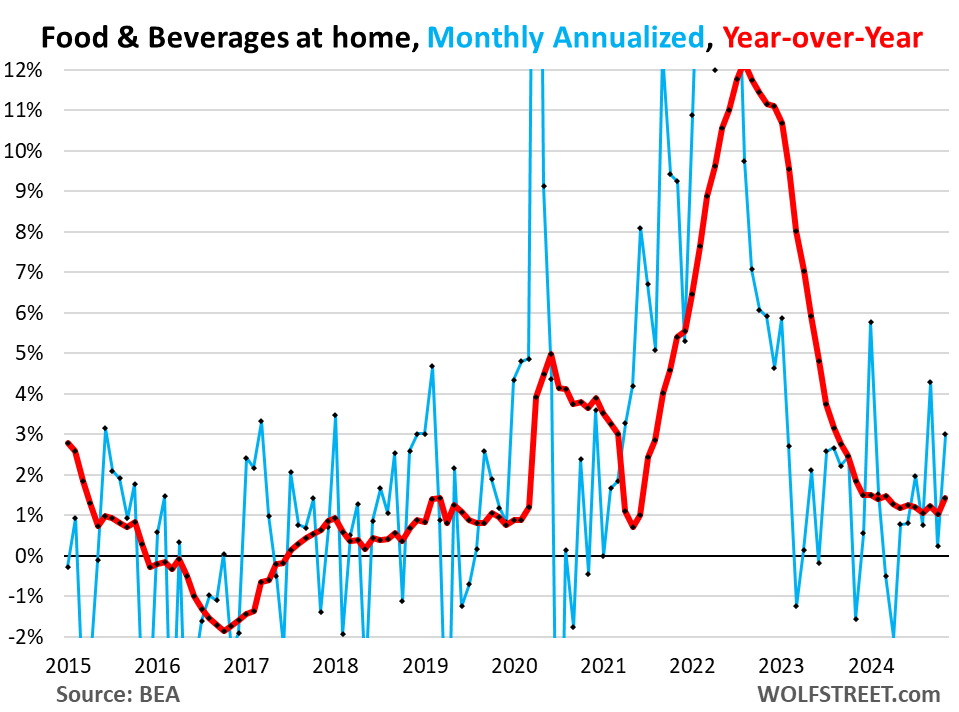

Food inflation has started to accelerate again in recent months but remains fairly low. Inflation is a rate of change, so a deceleration means that it increases at a slower rate. But prices are a level, and that price level is very high, and because of the current inflation continues to creep higher.

In November, the PCE price index for food and beverages purchased for off-premise consumption rose by 3.0% annualized from October (blue in the chart below).

Year-over-year, it accelerated to +1.4%, the biggest year-over-year increase since March, and up from the +1.0% to +1.2% range in the prior months.

Food is not included in the core PCE price index, but it is included in the overall PCE Price index, and the sharp deceleration of food prices was a big contributor to the deceleration of the overall PCE price index, and that may be over as well.

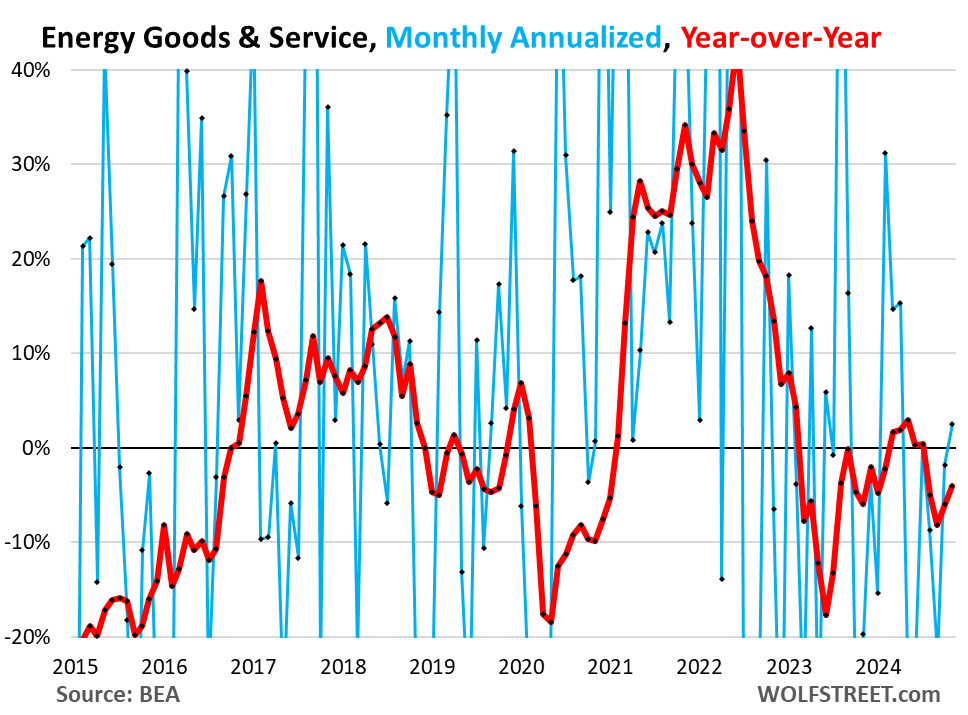

Energy prices increased in November from October by 3.0% annualized, the first meaningful month-to-month increase since April (blue). These are energy goods and services that consumers buy directly, such as gasoline, natural gas piped to the home, electricity, propane, heating oil, etc.

Year-over-year, energy prices are still down by 4.0%, but that’s the smallest year-over-year decline since July.

As everyone knows, energy prices cannot and won’t drop forever, though they’re very volatile and can plunge for a long time, just like they can spike for a long time. Energy prices were another big contributor to the deceleration of the overall PCE price index in 2023 and 2024, and those declines may be running out of steam as well:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yesterday my friend said she was going to buy a new Tundra. The local Toyota dealer offered her the same amount she paid new from that same dealer for her 2018 Tacoma which now has 47,000 miles on it. Now that’s inflation.

And then she really got scalped on the new one – which is a true POS compared to the old one.

We are helping the youngest kid buy her first car (probably the only new one she will ever own). We’ve waited over a year for the new Civic Hatchback Hybrid to hit the streets. Shopped the other day and got quoted around $8k in fees on top of the MSRP.

We took our buyers strike out the door.

I’ve been driving a Civic LX for a decade. Has a 142,000 miles so I figure it might still be useful for a high school kid or something. Really want the new Civic Sport Hybrid. The dealer listed it at $30,300, took $1000 off then added $1900 in “dealer fees” plus taxes. Would give $4500 for my car. I said drop the dealer fees and we have a deal. They said no. They only had one in stock, so I figure I’ll try again when they build some inventory.

Since new cars are about the worst investment you can make, deprecating as much as 30% just driving it off the lot, why not teach her some financial responsibility and get one a few years old?

To Brian (below) – the hatchback hybrid is brand new, no older models exist (otherwise we`d be shopping used.) Closest comparable vehicle is the Prius, which holds its value extremely well used. There’s only $2-3k difference between new and used. All things considered, extra year of warranty and battery life, there is no reason to choose a used low mileage Prius over a new Civic Hatchback Hybrid.

We are leaving the area in the next year and her Dad really is laser focused on getting her into something as reliable as possible so he doesn’t have to worry.

“Since new cars are about the worst investment you can make, deprecating as much as 30% just driving it off the lot, why not teach her some financial responsibility and get one a few years old?”

This reasoning drives me nuts, no pun intended. Why are cars considered primarily as an investment? They’re not stocks, they’re a necessity that gets you from point A to point B. You do your research, buy a new car, take care of it, and it will last 15-20 years. And if you take care of it you can still get a good price for it when you finally want a new car.

I bought a Toyota Yaris for $13k out the door in 2008 and sold it in 2020 for $5k. It was NEVER in the shop because I knew its history and its quirks. There’s your investment.

If you’re a car person do what you want, but stop this propaganda about new cars being a rip-off because they depreciate. It’s ridiculous.

Cars are not an investment, they are an expense.

@Jack –

Whether a car is an investment (asset) or an expense depends greatly on how it is used.

If it’s used to produce more than it costs, it’s an investment. Think about truck drivers, taxi drivers, people who drive to commute to a better-paying job than they can get to by other means, etc.

If it’s not used productively it’s a waste.

“Sport hybrid” – Honda, what are you even doing??

Same with the regular “sport” civic, which is actually one of their low-end trims… a slow car with the base engine, but a “sporty” exterior…

Your friend doesn’t know what a buyer’s strike is. Only 47,000 miles?

I hear Stellantis has great deals. /s

At the very least, her purchase would add 1 to the used car market.

So basically she’s theoretically moving from Washington state to Yellowstone park. 😆

Wonder how much of stock declines is inflation picture and how much is drama around government shutdown. It never happens but I suppose the odds might be higher now. Markets like consistency and gtidlock and not sure the next two years will be that. They do like deregulation and tax cuts so hard to say what anything will look like.

PCE came in less than expected, market rocketing higher. Love how interest rates on mortgages, car loans, and credit cards aren’t factored in inflation, we’d be well above 2% if so. Need another financial crisis to clear the excess to get us below 2%. Don’t worry govt. would be right there anyway. Haves are growing the pie for themselves while little guy puts in 30 years for the pie crumbs.

Told my wife 20 years ago the United States was moving to a country of ‘Haves” and “Have Nots” and we need to make sure we are in the latter group.

I agree with Powell. The heavy lifting is already done. We’re down from over 7% to 2.4%. Honestly, who cares if its 2.5% or 2.2% or 2.0%, besides the media and gamblers playing the markets. The war is won. It’s minor adjustments at this point.

What we need to worry about is that unexpected crazy event that triggers a recession.

I’m starting to think you are right. He’s done a good job so far. Now if the red haired one doesn’t try to push interest rates to zero, we should be OK, except for the huge government debt and spend-crazy Congress.

While I agree with the current FOMC presence, we are ignoring the elephant in the room:

Overpriced assets, which simply cannot be allowed to fall by 50 pct plus or minus to the fair value by calculation.

“Fair value” is just an historical average. This country has never had a greater population, been wealthier, had lower taxes in the modern era, greater government spending, nor a much wealthier world looking to the US for investment. Those factors may lead to a fair value with a higher P/E for awhile. I know this is a “this time is different” post. But in reality it is.

I start getting worried the more I hear about this time being different.

It is the same everytime.

This is Wall St talk because FED itself has said they care taking to 2%. This is reflected in various statements including FOMC meeting.

Who cares is American People care. Today you can say who cares for 2.5 then 3 and then one day you can who cares about inflation.

Most people hate inflation. That too prices went up so crazy, people still are catching up on thier wages and incomes. Most important is if people think FED doesn’t care inflation expectations wont be anchored too and that will be bigger issue.

I feel your angst. However, We have to get out of bed and live each day.

Under fire the whole time.

As someone with a 2.7% mortgage, I agree. 3-4% inflation is fine.

You agree with what benefits you, hardly surprising. There’s no need for us to worry about what may hurt you. Recession is a part of the business cycle.

“Recession is a part of the business cycle.” Except, since 2008, we learned the granddaddy of Fed puts is always one button-press away. So recession becomes this slow stretched out thing, a bill papered over now, and sent more to the future. Then again, that relied on governmental access to credit at a certain price, and we’ve spent a lot of seed corn since then. So maybe recession DOES return as a reality.

But I thought he was always selling gold? I need to re-check?

Looks like the long duration treasury market may finally be coming to terms with the future. Likely another bear market rally coming soon. But it seems the bond market may finally be figuring out that depending a bigger risk premium makes sense because (1) Trump wanting to remove the debt ceiling completely (or at least for 2 years), (2) the inflationary effects of tariffs, (3) the inflationary effects of cutting corporate tax rate to 15% and (4) all the spending cuts that DOGE is supposed to push through look small in comparison to the deficit.

TLT in bear market for almost 5 years. At some point the bond vigilantes are going to be back. Feels like waiting for Godot at this point… but today is likely a preview of things to come.

I’m probably bias, but I think TLT has a lot more room to fall.

The bond market is still selling leverage as benign.

Leveraged debt is the most risky. It may be my impression that the financial dregs are over priced. When long term interest rates rise, leverage deals capital losses to the bond owners.

T bill and chill

It appears to me nobody is fooled in here. Too many dollars chasing too few goods and services. Inflation. Trump will have none of it. Just another in a long line of klownsians. Will it ever stop?

Trump will have none of it…hmm

Very much looking forward to this magical wand that Trump possess.

Wolf,

IF PPI Data gets revised and has been revised higher so far, how come there is no later revised data for Headline PCE and CORE PCE ?

PCE data gets revised too. When the revisions are big (not often), I discuss them, for example here in July:

https://wolfstreet.com/2024/07/26/large-upward-revisions-of-core-services-pce-inflation-pushed-six-month-core-pce-inflation-to-3-4-worst-in-a-year/

or last year in September:

https://wolfstreet.com/2023/09/29/pce-inflation-index-revised-higher-going-back-2-years-core-services-pce-price-index-was-much-hotter/

Jerome Powell is right about time eliminating inflation, no one worries today about the Roman currency inflation of 200 – 300 AD.

Gary-

“ …no one worries today about the Roman currency inflation..”

Diocletian worried back then about inflation and instituted price controls.

Today we institute interest-rate controls (“interest” being the price of money, of course).

Not much changes under the sun.

1. It isn’t an open forum. Your dishonesty about this already makes you look bad.

2. Comments aren’t taken down because of views expressed. Comments are removed generally for factual reasons. People who continually sprout unsupported nonsense have their comments removed.

I said them jacking up interest rates on already inflated pricing has further increased the price of said pricing. If I bought a house 2.5 years ago at $600k at 4% my payment is x, I buy same $600k home now at 7% my payment is x+n, that’s not factored to accurately account for this increase to new buyers.

Do believe that enough to put your money where your mouth is? I would like to profit off of your wrongness.

Trump policies will increase durable goods prices and now he wants to end the debt limit ceiling along with cutting government spending. I don’t even think AI could figure this out.

I’m still driving my 2005 Ford mustang that I paid cash for in 2006.

I’m also sitting on a pile of cash waiting to buy a house. I feel like we’re already in a recession and it’s just going to get worse and worse and worse this is going to be the biggest bubble pop in history.

Once it pops and you hear on all the news 24/7 that the world’s coming to an end, that’s when I will be out buying my house.

Dropping the prime rate is not indicative of restrictive fiscal policy. It is a good indicator of Powell doing something he hope will make Trump happy.

Inflation is not going to ease up unless interest rates go higher and another $3-$4 Trillion in money floating around gets burned.

We spent the entirity of Joe Bidens Presidency under a “Continuing Authority” without a Federal budget. Congress needs to get it’s act together and become fiscally responsible.

” It is a good indicator of Powell doing something he hope will make Trump happy.”

You people are so ridiculously funny with your the-Fed-does-partisan-politics BS. At first Powell dropped rates weeks before the election (which won’t have any impact on the economy for many months) to get Democrats reelected, and when they lost, he dropped rates to make “Trump happy?” 🤣🤣🤣🤣❤️🍾🥂