Listing prices, YoY: Miami -11.7%, San Diego -9.1%, Kansas City -8.5%, San Francisco -7.7%, Austin -7.6%. Active listings explode in Tampa, San Diego, Miami, Seattle…

By Wolf Richter for WOLF STREET.

In August, “the housing market slowed considerably as both buyers and sellers patiently wait for a lower mortgage rate environment,” Realtor.com reported today, along with dropping listing prices, waves of price reductions, surging – or exploding – active listings, and rising days a property spent on the market before it was sold or pulled off the market.

While August home sales will be reported later, starting with pending sales later this month, we already know that pending sales in July plunged to the lowest level in the data going back to 2001. So based on what Realtor.com was saying today, August may yet be worse. Sales that closed in August – so deals that were done mostly in June, July, and August – were near the lowest levels of the Housing Bust.

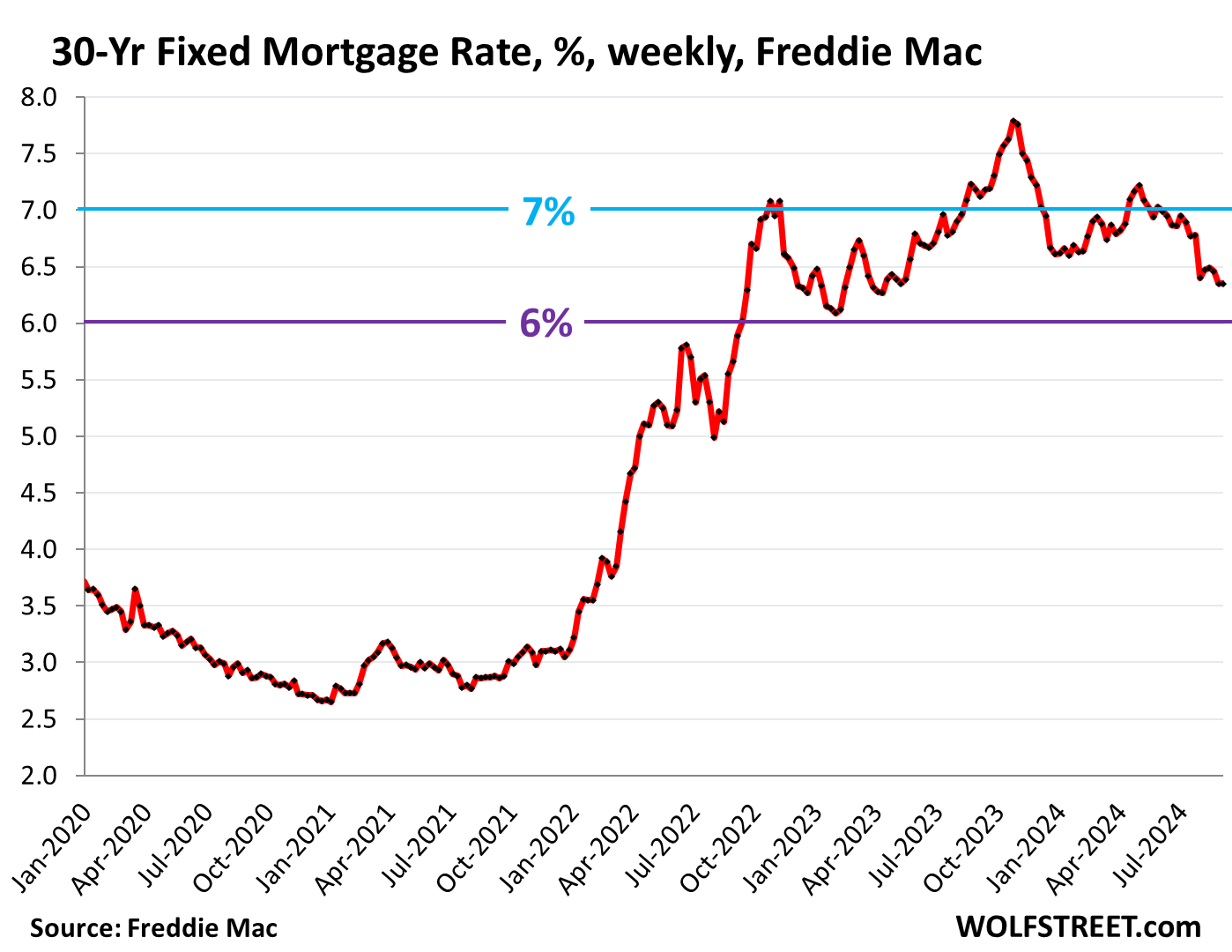

Turns out, prices are way too high, and potential buyers have gone on buyers’ strike even as mortgage rates have been zigzagging lower for the past 10 months. In the current reporting week, the average 30-year fixed mortgage rate was 6.35%, same as in the prior week, and down by 1.44 percentage points from the peak in late October 2023, according to Freddie Mac today. Six rate cuts have already been priced into mortgage rates, and yet sales continue to plunge.

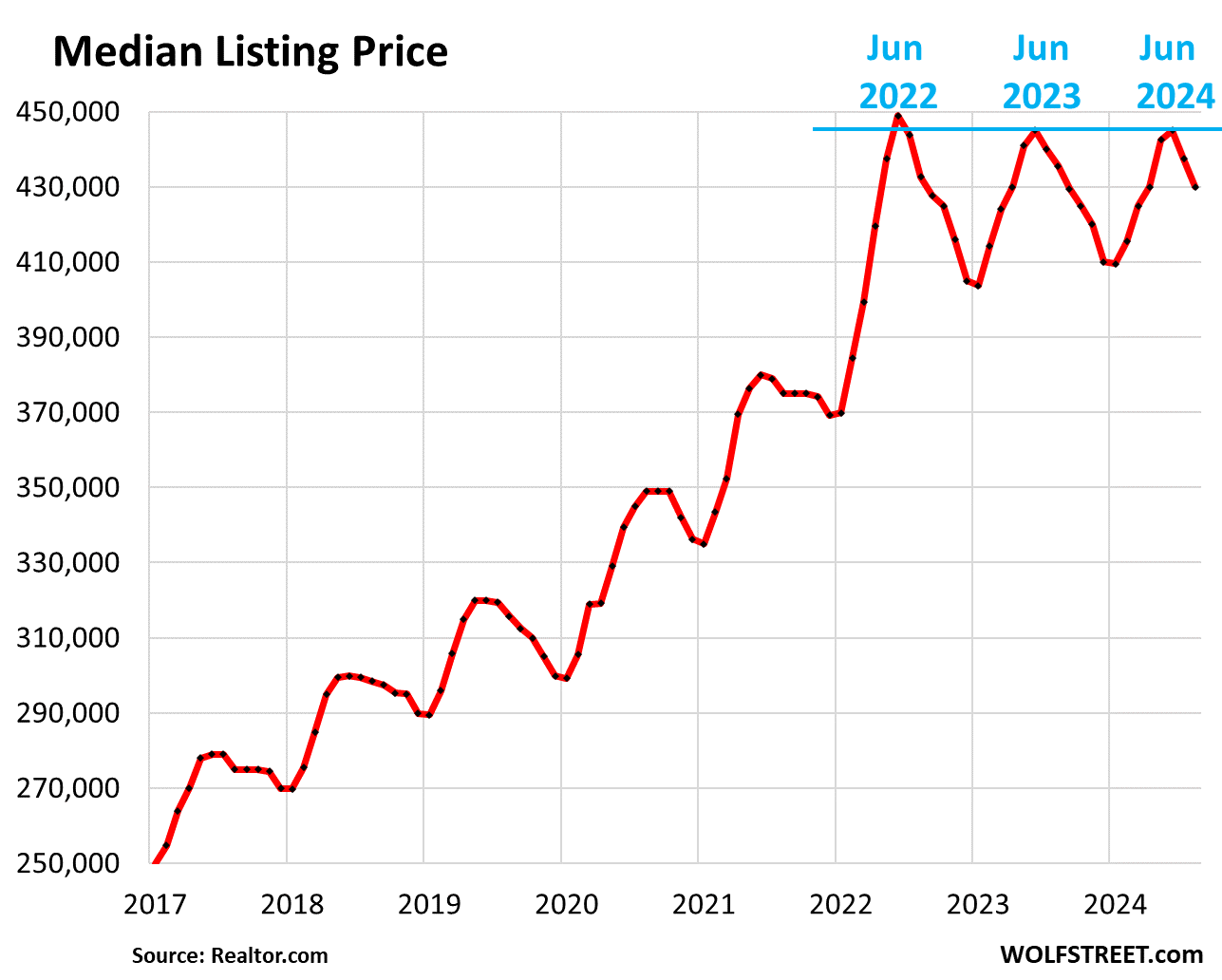

The median listing price in August dropped for the second month in a row from the seasonal peak in June, which had been lower than the all-time peak in June 2022, and flat with June 2023. Year-over-year, the median listing price was down 1.3% (data via Realtor.com):

Even in metros where listing prices have dropped, they clearly haven’t dropped enough to make sales happen even at these lower mortgage rates, as sellers cling to their notion of what prices should be, while buyers have lost interest at those prices.

Here are the 29 metropolitan statistical areas of the biggest 50 with year-over-year drops in median listing prices, according to Realtor.com today, with Miami (-11.7%) and San Diego (-9.1%) on top:

| Metro Area, August 2024 | Median Listing Price | % YoY |

| Miami-Fort Lauderdale-Pompano Beach | $530,000 | -11.7% |

| San Diego-Chula Vista-Carlsbad | $999,000 | -9.1% |

| Kansas City, Mo.-Kan. | $398,050 | -8.5% |

| San Francisco-Oakland-Berkeley | $969,000 | -7.7% |

| Austin-Round Rock-Georgetown | $525,000 | -7.6% |

| Oklahoma City | $315,000 | -7.3% |

| Cincinnati, Ohio-Ky.-Ind. | $349,900 | -6.7% |

| Tampa-St. Petersburg-Clearwater | $415,000 | -6.2% |

| Denver-Aurora-Lakewood | $620,000 | -6.1% |

| Nashville-Davidson-Murfreesboro-Franklin | $550,000 | -5.7% |

| Orlando-Kissimmee-Sanford | $435,000 | -5.2% |

| San Jose-Sunnyvale-Santa Clara | $1,399,000 | -5.1% |

| Sacramento-Roseville-Folsom | $640,000 | -4.8% |

| Dallas-Fort Worth-Arlington | $444,990 | -4.3% |

| Phoenix-Mesa-Chandler | $515,000 | -4.3% |

| New Orleans-Metairie | $325,000 | -4.2% |

| San Antonio-New Braunfels | $342,500 | -4.1% |

| Jacksonville, Fla. | $409,850 | -4.1% |

| Portland-Vancouver-Hillsboro | $615,000 | -3.6% |

| Atlanta-Sandy Springs-Alpharetta | $415,000 | -3.5% |

| Seattle-Tacoma-Bellevue | $775,000 | -3.1% |

| Minneapolis-St. Paul-Bloomington | $439,990 | -2.8% |

| Washington-Arlington-Alexandria | $599,900 | -2.5% |

| Indianapolis-Carmel-Anderson | $330,000 | -2.2% |

| Raleigh-Cary | $454,900 | -2.2% |

| Pittsburgh | $245,000 | -2.0% |

| Baltimore-Columbia-Towson | $370,900 | -1.7% |

| Boston-Cambridge-Newton | $834,500 | -1.1% |

| Columbus | $384,900 | -0.3% |

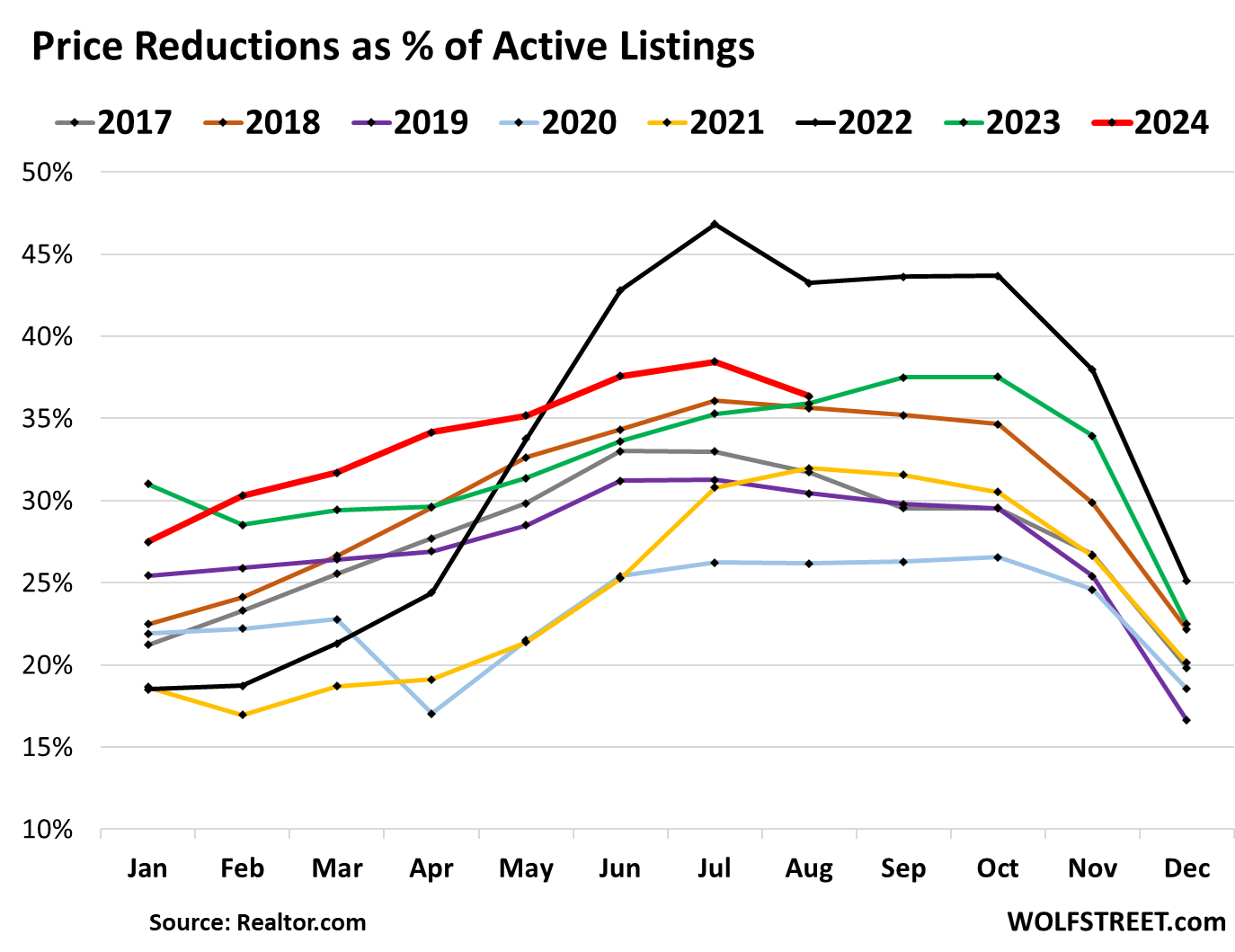

Price reductions: The share of active listings with price reductions in August of 36.3% was the highest rate for any August in the data going back to 2017, except for August 2022. But those price reductions clearly aren’t enough to bring potential buyers into the market (data via Realtor.com):

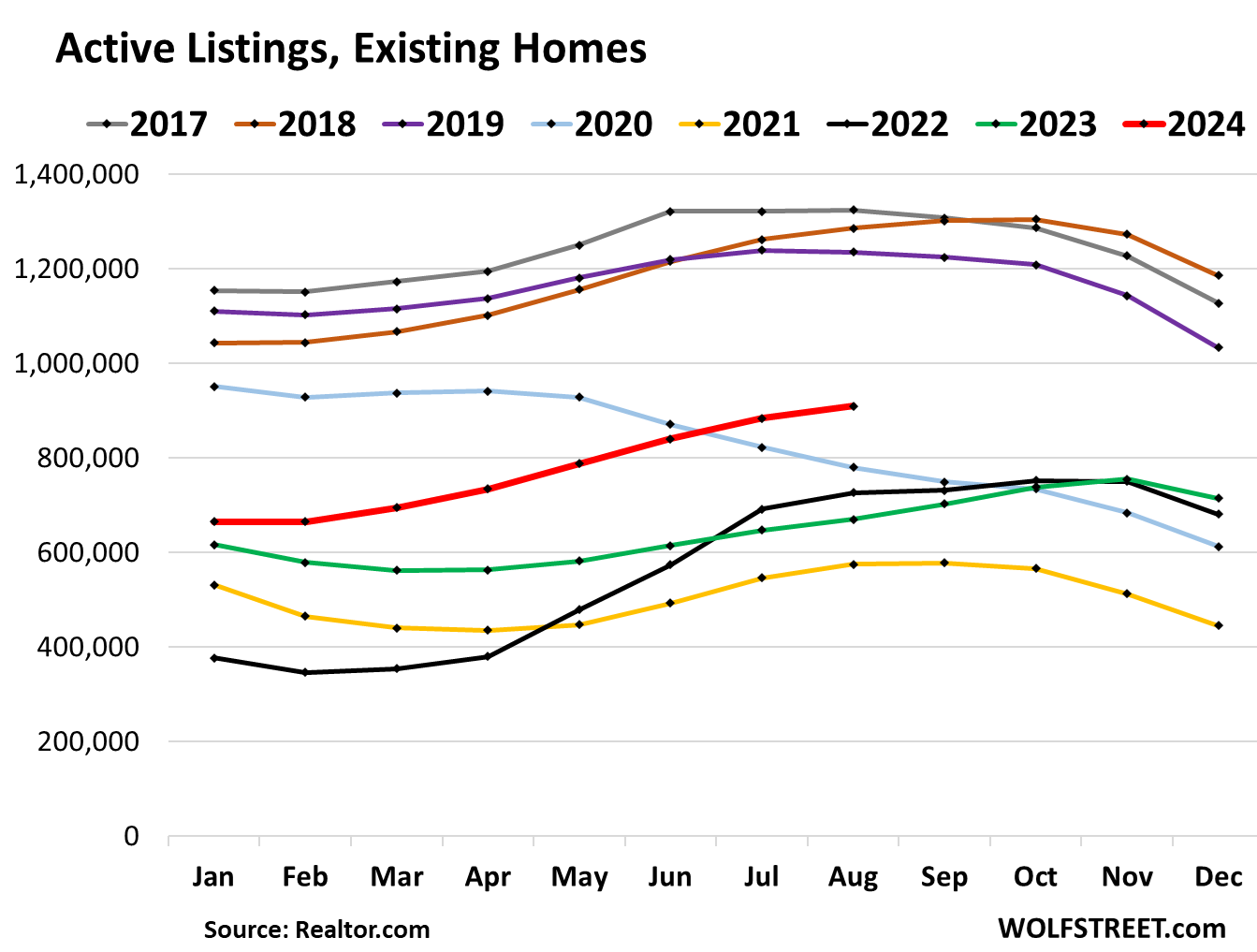

Active listings (total inventory minus listings with a pending sale) surged to 909,300 listings, the highest since May 2020, as sales have plunged and as inventory gets stale. There simply is no demand at these prices, they’re way too high, and it’s up to sellers to figure this out (data via Realtor.com):

Active listings exploded year-over-year the most in Tampa (+90%) and San Diego (+80%).

Active listings have piled up largely because demand has collapsed at these prices, and homes are not selling. Sellers are piling properties into some markets, with new listings up 19% year-over-year in San Diego and 30% in Seattle, for example. But in other markets, sellers are trying to tell themselves that this too shall pass, and are hanging on to their vacant homes, waiting for better days.

These are the metros of the 50 biggest metros where active listings have surged the most. Changes in new listings in the right column; data for Las Vegas and Rochester metros not available (via Realtor.com):

| Metro Area, August 2024 | Active Listings

% YoY |

New Listings

% YoY |

| Tampa-St. Petersburg-Clearwater | 90% | -1% |

| San Diego-Chula Vista-Carlsbad | 80% | 19% |

| Orlando-Kissimmee-Sanford | 77% | 6% |

| Miami-Fort Lauderdale-Pompano Beach | 72% | 10% |

| Seattle-Tacoma-Bellevue | 69% | 30% |

| Jacksonville | 68% | -8% |

| Denver-Aurora-Lakewood | 67% | 5% |

| Charlotte-Concord-Gastonia | 62% | 9% |

| Atlanta-Sandy Springs-Alpharetta | 58% | 7% |

| Dallas-Fort Worth-Arlington | 51% | 12% |

| Phoenix-Mesa-Chandler | 50% | -36% |

| Raleigh-Cary | 49% | 0% |

| Sacramento-Roseville-Folsom | 49% | 11% |

| San Jose-Sunnyvale-Santa Clara | 45% | 5% |

| Memphis | 45% | -3% |

| Los Angeles-Long Beach-Anaheim | 42% | 16% |

| Cincinnati | 39% | 31% |

| San Antonio-New Braunfels | 38% | 2% |

| Riverside-San Bernardino-Ontario | 38% | 9% |

| Oklahoma City | 37% | 3% |

| New Orleans-Metairie | 36% | -5% |

| Columbus | 35% | 11% |

| Richmond | 34% | -6% |

| Louisville/Jefferson County | 33% | 7% |

| Houston-The Woodlands-Sugar Land | 32% | 11% |

| Birmingham-Hoover | 31% | 8% |

| San Francisco-Oakland-Berkeley | 31% | 10% |

| Indianapolis-Carmel-Anderson | 30% | -5% |

| Baltimore-Columbia-Towson | 29% | 4% |

| Portland-Vancouver-Hillsboro | 29% | -2% |

| Providence-Warwick | 27% | 1% |

| Boston-Cambridge-Newton | 26% | 5% |

| Austin-Round Rock-Georgetown | 26% | -13% |

| Minneapolis-St. Paul-Bloomington | 26% | -5% |

| Nashville-Davidson-Murfreesboro-Franklin | 25% | 23% |

| Pittsburgh | 24% | -1% |

| Washington-Arlington-Alexandria | 24% | 2% |

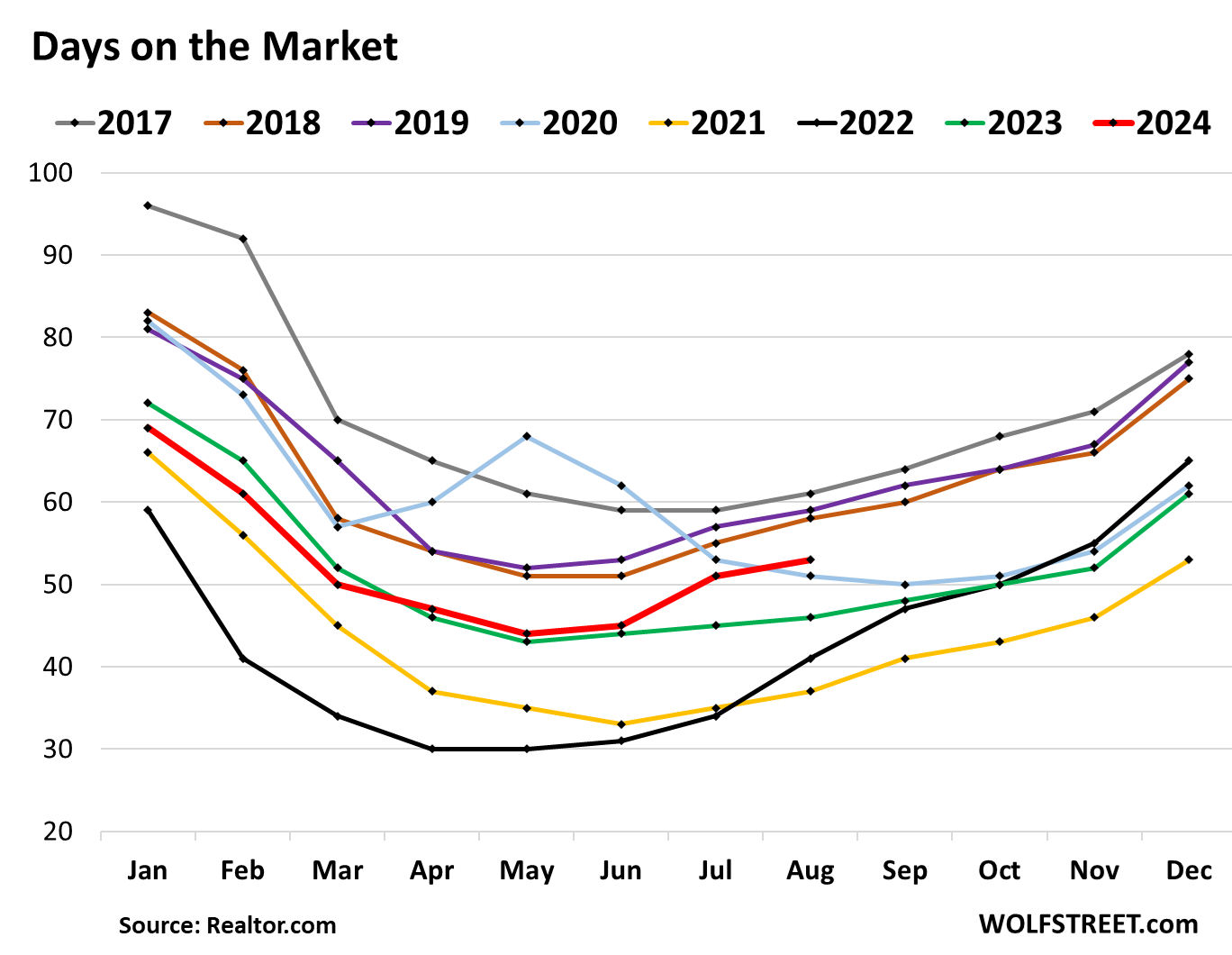

Median Days on the Market: The median number of days a property sits on the market for sale before it sells or before it is pulled off the market rose to 53 days, the highest for any August since 2019.

This number is kept down by sellers pulling their home off the market when it doesn’t sell after a few weeks, to then relist it later for sale at a lower price, or to try to rent it out, or turn it into a vacation rental (good luck on both), only to then relist it for sale.

So this metric doesn’t really show how long it takes to sell a property, but how aggressive sellers are in pulling their property off the market if it doesn’t sell. If sellers get more desperate to sell the property, they’ll leave it on the market and reduce prices until it sells.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Seems completely logical. If rate cuts play out then likely everything heats up in the Spring.

RTGDFA? See the mortgage rate chart? Six rate cuts have already been priced into mortgage rates, and yet demand has collapsed.

And if the Fed doesn’t cut as much as has already been priced in, then good luck all around.

The problem isn’t mortgage rates. The problem is PRICES. They’re way too high, and buyers are saying, forget it.

What will increase sales volume? Substantially lower listing prices and bigger price reductions.

AMEN!

I forgot to add:

You can refinance the mortgage if rates drop, but you cannot re-buy the house at a lower price. You’re stuck with the price, not with the rate.

And an overpriced house is expensive in other ways: insurance premiums and property taxes are also higher.

There was a mania for a few years, and any buyer now is just letting sellers off the hook at peak profits. I think potential buyers are seeing that.

Agreed.

Along these lines it would be interesting to see the 2 metro charts (median listing price/%change yoy and active listing %change yoy) combined into a single list.

Basically, increased listing supply should be dropping prices (roughly eyeballing it, it looks like it does) – but combining the lists would easily show the supply effect metro by metro.

Obviously the hiccup is that we are still working under abnormally low listing supply (4-5 years in) so that even marked listing supply increases yoy puts us 25% below historical norms.

Rather amazingly.

(I’m sure it surprises the hell out of the Fed and various MMT’ers who believe they can control the macroeconomy like a digital microwave).

And the listing build up has been so slow (waiting/hoping/praying for that Fed pivot) that very little price cut stampeding has occurred.

Without some more “panic” those potential sellers are going to remain anchored in their absurd, ZIRP era overvaluations (thanks again, Fed, for the phantom – nay demonic – wealth effect, Round 2).

If you look in the past at the previous bubble. How long was your window to buy a house at a good price?

If I recall it wasn’t until 2013 that sellers finally relented and lowered their asking price by 100’s of thousands.

Then perhaps you had 2013-2017 to acquire a property at a decent price.

Who can plan to buy during a small 4 year window during a larger drawn out window (2006-2012 and 2018-present day).

Wait for it, wait, wait… 😣

Hi Wolf, what event will trigger a massive cut in housing prices? IMO, I will say a massive unemployment, e.g. 10%. This forces people to liquidate their assets and sell houses at a lower price (because they can’t afford the mortgage).

It happened in Great Financial Crisis in 2008, and I believe it will happen again.

Time.

@_mile_road: Not affording the mortgage is not the only reason. Home insurance and property taxes have soared over the last few years. Together, they can place a huge strain on homeowners who stretched themselves to buy their homes. Unfortunately, this is going to come back to bite them.

Housing is an essential sector. People cannot put off home buying beyond a certain point and sooner or later they will be pushed into making this huge financial commitment even though some of them may know the elevated risks.

This is why the Fed should move away from QE and low-interest/zirp policies. And the Federal Government should institute policies that provide incentives for owning a primary home and strong disincentives for speculation in the housing market.

But then, our Fed and the Government is run by affluent folks who rarely run into these issues themselves and can be made to look away by the financial industry and the lobbyist groups.

So here we are again staring at financial distress much like 2008. If the housing market collapses, it is going to cause enormous societal distress.

Sean,

The NAR and Chamber of Commerce always occupy the number one and two spots for annual lobbying dollars spent. Each usually spends $40M to $100M per year.

How much do 50 million renter households spend on lobbying? I’ll guess zero.

Big problem.

@Sean Shasta: “Housing is an essential sector. People cannot put off home buying beyond a certain point and sooner or later they will be pushed into making this huge financial commitment even though some of them may know the elevated risks.”

Ummm, have you heard of renting?

Just today a house listed in my area (San Diego) with a price history showing it tried to rent at $7500/mo. all summer, but didn’t, so they listed it today for $2,850,000. with 20% down, that works out to a payment of $18,541 a month… for a home they couldn’t find a tenant to rent for $7500/mo.

The math here isn’t complicated, and buyers are figuring it out.

House prices weren’t going to zero in 2008.

Elizabeth Duke said in 2009, in released Federal Reserve minutes, “So I think if we spent enough money, got enough of a hit right now, it would look like a floor on house prices, and we might have something every bit as good as a floor on house prices.” With that, and the REO To Rental program, in which FHFA partnered with big financial companies to turn foreclosed properties to rentals instead of sales, they turned housing into a “can’t lose” investment. A can’t lose investment quickly becomes a bubble because it can’t lose.

Profit builds updrafts, then narratives solidify bubbles, and a narrative plus vast spending and manipulation of the financial environment (lowering interest rates, balance sheet expansion, purchasing mortgages thereby injecting money into the housing market) by the central bank and government at multiple levels create profit and narrative and thus bubble.

I get that they don’t want to let house prices drop. Many are heavily invested and reverse wealth effect and “debt deflation into depression” are the bogeymen they fear on top of personal investment. I have some questions about the wealth effect, suspecting it is a small updraft / downdraft as it requires actual cash for people to spend, not just imaginary cash; and debt deflation into depression as people stop paying their mortgages – I can’t imagine that happens this time as so many have mortgages they value, at low rates (2008 a lot of people with prime loans stopped paying).

I suspect sparking and sustaining a bubble in housing is a net negative for society, and ultimately for politicians.

A mild recession that causes a significant decrease in travel. Hard to find numbers but as of 2021 there were 2.5 million active Airbnb listings in the US. I’m sure it’s higher now.

Similarly when people who have been leaving homes empty holding out for higher prices see prices start to drop there will be a race to the door.

I’m not sure we need a significant increase in unemployment, just a very financially constrained consumer.

@shangtr0n: “Have you heard of renting?”.

Unfortunately, that strategy has not worked for the last 30+ years with the Fed blowing successive bubbles and making sure that housing prices keep going up.

Perhaps you own your home already. But most people have realized to their dismay that renting prolongs the agony. I am not saying people should buy homes now – just that it is not an easy decision to continue renting while the Fed actively works against people who exercise prudence.

but but but…date the rates but marry the house? Guess they never factor in that if both are unattractive then abstinence is the only way to go

Regardless of the potential Fed cuts being “priced in,” what’s more important is the average spread between the 10 year govt bond and the 30 year mortgage rate. It has alternated between 1.5% and 2% with occasional spikes above 2% for relatively short periods since 1990. The FRED chart is on the below link.

Using Wolf’s mortgage number, the spread is now about 2.6%, which places us squarely in line w/ spreads from 2006 – 2008. It’s obvious lenders perceive higher risk now. If prices decline, with the 10 year now around 3.75%, that would imply the 30 year mortgage going down to 5.25% over time.

The article you linked was from 2022. So the chart in it is way outdated. Here is a current chart of the spread:

Thank you, Wolf. I said it in a recent article and I’ll say it again: I’m one of those buyers who is on strike. We have the ability to move, but damned if I’m paying the asking prices.

I see most homes now being listed for 30-40% more than it last sold for in 2018 or 2019 with either too much upgrading for the local market (seeing a LOT of this), or, clearly no updates in the last 10 years.

No thanks. We’ll hold on to our 1,800 sq. ft. 1929 colonial with no mortgage and enjoy the freedom it gives us, even if not in the perfect neighborhood.

Unless you have a sizable Wolfpack or a need the extra space for your massive library or something, 1800 sq ft should be more than enough? That’s roughly two small 2 bedroom apartments. 1929 at that — sounds beautiful, especially if it has the original bathrooms. Nothing compares those big beautiful sinks from then

Amen

@hreardon,

Exactly. Prices have gone only from completely ridiculous to somewhat less ridiculous. The prices are not good by any means – only less bad.

Less bad is still bad, and paying current prices runs a risk of “going underwater” on your mortgage loan.

A full scale recession would alleviate this situation. But between the ongoing drunken sailor spending and the labor market conditions it does not appear that is in the cards anytime soon.

Only if employment stays high, which I doubt. Then you have no demand and a Wiley Coyote moment. Everyone is expecting buyers to come out, but most as DG and CostCo and others show are living paycheck to paycheck and don’t have the money for a downpayment. In the Bay I expect layoffs to continue with the realization that the Cloud is done and there are currently no killer apps for AI. If AI is so good, why are phone trees so bad and why is texting support so awful. It’s ridiculous.

I could not agree with you more. AI is massively over hyped and Nvidia also by extension. If AI can’t even do the very most basic customer service functions that any barely English speaking high school dropout can perform, like managing a drive through burger order, then it’s all speculation.

No.

Expecting prices to keep going up when they shot up during QE and sub 3% rates is not logical. We will (hopefully) never see that again in our lifetimes. Home prices need to return to reality.

Not if the cuts are because of job losses

An acquaintance of mine is a realtor, frequently bragging about his large commissions. When he mentioned a property has been sitting for 4 months with no offers, I mentioned the price is too high.

Crickets.

Some realtors are still in denial and helping to keep sellers in denial.

It will be super interesting to see how fast the air leaves this bubble now that sentiment has tipped to fear of overpaying.

Feels like it will be a slow deflation. Sellers will drop 5k-10k here and there until there is interest. Mania is over but the seller’s memory of the prices in last couple years will stay.

@Painted Poly: Not so. As Wolf has pointed out in his articles and comments, housing has huge carrying costs – home insurance and property taxes in addition to the mortgage.

People have been holding on and renting their older homes after buying new ones. Sometimes, not just one older home but two or more. There are people who have bought tens of homes to rent them out.

When the tenants leave and new ones don’t turn up, the party stops abruptly. This might happen if the renters of SFH decide to move to multi-tenant facilities which have been over-built over the last few years.

Due to a combination of reasons, I think we will see a wave of homes hitting the market soon.

> This might happen if the renters of SFH decide to move to multi-tenant facilities

I sort of doubt this. Having lived in both, SFH is better in pretty much every way (except yard work if you are responsible for it) than multifamily, particularly with regards to noise through walls(multifamily is usually built really cheap), closeby neighbors that may be undesireable (as MFH is usually cheaper), theft and parking lot issues that aren’t usually a problem in SFH.etc.

As long as prices and location are more or less comparable, SFH wins hands down every time.

@Sea Creature: I agree with you that SFH have significant advantages. But for renters in distress due to layoffs or a host of other dislocations, they may not have much of a choice.

It’s difficult to understand why the agents defend high prices. They work on commission and earn more per transaction, BUT 4 to 6% of nothing is ……..nothing.

It’s not when you factor in the actual seller, if an agent tells their client they won’t sell at their desired price but another agent tells them they can do it the seller will go with that agent. The agent then puts it up and let’s experience help them talk the seller down to a lower price they may sell at. Like you said, 6% of nothing is nothing, RE is cutthroat so they do it like this.

Come to think of it the reno business works like this too, many companies estimate the client a price they know for sure they won’t hit just to get the contract, after cost overages come into play. RE is dirty like that

Tell that acquaintance he better get good at a different kind of service industry, hey at least in some states, minimal wages for food workers are better now.

Used to work at a place that was right next to New Century Mortgage back in 2008, one day plenty of fancy cars in their lot, next day, people were crying carrying out boxes, and looking for any jobs they could get..I am sure your acquaintance thinks this time is different…maybe he is right if I were him, I would keep that hubris in check

“frequently bragging”

Considering that annual national home sales are down 33% from their latest idiot peak, discount everything he says by a third.

When housing prices fall at least 80% then some demand from potential purchasers will likely return to the housing markets.

Never said never but as much I pray that will happen, I put that at the probability of the general public meeting aliens from out space within the next 2-3 years.

Can only imagine even if existing prices collapse by 50%, what kind of chaos it will cause in this whole wealth effect and the funny part is that even at 50% crash, this will just barely bring SoCal back to “normal” fundamental value. 80% is perhaps maybe just a slight bargain..

“Phed’s Phantom Wealth Effects 2.0”

guess I’m lucky as I closed yesterday(Tucson) at FULL PRICE

of course move in ready, etc. and I did FSBO – paid buyer commission

now I’m not in hurry but starting to scout next one

of course I’m not looking to flip but might

want to add another rental – not like stocks/bonds are very good ‘investments’ ie gambles

“not like stocks/bonds are very good ‘investments’ ie gambles”

I dunno – earning 10% annally with Treasuries & corporate credit isn’t a bad deal. And none of the work of landlording.

Of course you did.

Ever see a depredssion 88% drop and still can’t sell

Oh no…not precise San Diego on this list, then again median price of $1M and even higher than SF is a bit of a joke in itself especially when comparing the average income between these two areas….disappointing not to see LA or OC markets in the first table, hopefully this is just the start and RE industries and sellers don’t end up getting even lower mortgage rate, maybe at below 5% they might get what they are waiting for even at these high prices…once again crossing my fingers I am dead wrong in this assumption.

On a different note, wife did show me a listing of a house in Orange, CA, decent sq footage and all fixed up (probably flipper special) went from listing of $2M just 6 months ago to now asking just $1 below $1M. Not sure what to make of it, it’s pretty funny though, seeing how much of these initial asking price is out of where the sun doesn’t shine and there are a lot of games being played on Zillow, Redfin with more pending, contingent to back on the market popping up based on my very limited anecdotal evidence.

Thanks for the article.

I always laugh when I see a home in San Diego listed for $1.5M when it sold in 2019 for $750K. Then it goes pending and back on market a few times over the next few weeks before they take it off to relist a few months later.

The big shocker will be what happens when mortgage rates don’t drop a lot. Many people I know are expecting sub 4.0% rates and I don’t think that will never happen again.

My experience after buying an selling multiple homes is purchases are made on payment. And high rates and high prices makes that impossible for buyers.

“The big shocker will be what happens when mortgage rates don’t drop a lot. Many people I know are expecting sub 4.0% rates and I don’t think that will never happen again.”

I agree.

Housing market could go from temporarily frozen to a new ice age.

For Median listing price it sort of looks like we are seeing a sawtooth sideways pattern in a range between $410k to $450k? Most likely we will head back down to $410k going into January. I guess then we need to see if we have another bounce back up or will it break lower.

I guess buy then we will or will not have had a rate cut.

A measure of just how much the Fed has been able to warp economic reality over the last 24 years.

In 2000,

Federal Debt-to-GDP ratio was 56% and the 10 year Treasury was 6.7%

By 2013,

Federal Debt-to-GDP ratio was 100% and the 10 year was…1.9% (the power of money printing used to incestuously buy Treasuries)

By 2018,

Federal Debt-to-GDP ratio was 105% and the 10 year was…2.6%

By 2023,

Federal Debt-to-GDP ratio was 123% and the 10 year was 4%.

It will be interesting how these comments will change once the prices correct a little. I suspect a lot of people like to “pile on” the bubble narrative just to buy up RE at better prices. I bet lots of people here own RE and want to buy more, as does the general public. Sure, we had unprecedented stimulus but people underestimate underlying demand. The RE loans now are also in a different world compared to the NINJa loans pre-gfc. And with the migrant flows, there will be a shortage of housing, as rents go up, people will want to buy just to lock in the price as the dollar looses value.

Prices are way too high. The middle class is priced out. The bulk of the RE market is the middle class.

Both days on the market and active listings were all higher in 2017-2019.

I guess the difference now being low volume and high rate of change?

Volume collapsed, compared to 2017-2019. So there are fewer active listings but a lot less demand.

Wolf,

Do you frequently post annual/quarterly closed SFH sales charts?

I don’t remember any recently but perhaps I just missed/forgot them.

As you allude to, they are a pretty important number.

It is one thing to have a $450k median sale price with 6.5 million sales and quite another to have a $450k median sale price with 4.2 million sales.

The latter being strongly suggestive of evaporating demand (in all probability due to evaporating affordability, in turn due to the evaporating falsehood of ZIRP).

“Do you frequently post annual/quarterly closed SFH sales charts?”

I report monthly on closed sales of existing SFH and condos and on contract sales of new SFH. I track annual close sales of existing SFH and condos, but I don’t post charts because no one cares about annual sales, and they only happen once a year. In 2023, 4.09 million existing homes sold, down by 33% from 2021. My monthly charts have been saying that also.

What kind of event could trigger a mass realization from buyers that they have to drop prices now to still capture any of the gains before they vanish?

That is the kind of event that will result in a rapid decline in house prices.

For now, the sellers with active listings do not perceive any looming threat that could knock them off their perch. It is as if they are waiting for the next round of price increases to kick off.

Could be a good opportunity for a perceptive seller to lower his price, move his house, and still capture most of the gains before the decline begins—what the smartest sellers would have done in 2005.

I struggle with this one too, outside of major shifts in government policy or monetary policy that will shift the balance dramatically back to buyers, it’s hard to imagine the mindset will be broken and force sellers to all run for the exit.

Look at China, it took major action from the government to change things rapidly and this is with the government for the most part staying on course and being ok with home prices going down despite mass unrest…etc, hard to see it happening here

On the other hand, if there’s a sudden major turn in the economy and mass and long-lasting unemployment is a thing, then it’s probably likely the dynamic will shift rather quickly.

Most “homeowners” own a home as a “place to live” and never even think about “capturing gains before they vanish” (or even check Zillow).

Sustained deflation. First sellers realize that prices aren’t going up any more. Then they notice prices are dropping in small increments 3% – 5%. Then they notice their listing is at the high end of the market. Then they start making small price cuts themselves. The cycle repeats a few times until panic starts to set in. Then the kicker: flippers who bought at the peak of the market start turning the keys into the banks. Poorly managed banks start looking like they’re going belly up and the banking industry stops making loans to each other and the RE market. That’s when prices collapse. But it will only happen with sustained deflation, the banks are much better regulated now than in 2008.

10% unemployment or 70% drop in stock market. Or both.

While we don’t have the data for August yet, sales of existing homes went up from June to July and the supply went down. Of course it varies region to region, but looking at the nation as a whole, there’s no reason to believe a price collapse is imminent. Maybe the August data will tell another story.

The timing of collapses is often mysterious. I remember in Fall of 2007, things seemed to breakdown all at once from my perspective. A small builder that was asking $850k for new luxury home dropped his price to $600k in a week.

Around that time, I went to a car dealer to buy a new car. Bought a new 2008 Honda Accord EX for $17K. The dealer said this was the first sale that occurred in many days.

One month people are spending like crazy with greed or FOMO in their eyes, then a month or two later things seem to quietly fall through the floor, all at once for some reason.

Same thing happens on the upside. The homes in my neighborhood seemed to go up relentlessly for many years straight, even before the pandemic. I never understood why until I pulled the RE property records to identify a pattern with the buyers. Nearly 100% of the buyers were Asian. Because I wasn’t part of that group and didn’t communicate with that group, I had no clue there was a buying frenzy going on.

No wonder I was receiving cold calls and recorded messages from people speaking an Asian language. They were probably talking about the great RE opportunities in my neighborhood!!

Those who identified the trend early made a lot of money. If you want to identify trends early, you have to do your own homework. By the time general media starts talking about it, it’s already too late.

Asians have deep belief that real estate never goes down. If you go to any expensive areas of any western block countries ( e.g. Vancouver, Sydney, OC CA, San Diego etc ), you’d find Asians owning lot of homes.

So far, they have been right due to govt policies.

Yeah these folks should ask people in their home country like China how true that is…I am sure they will come up with an excuse like it’s only true over there, this time is different…blah blah..

Are these Asian buyers foreign citizens or immigrants? If it is the former and they buy houses here purely for investment purposes, the government needs to step in and create disincentives for such purchases.

However, if they are immigrants (and some are likely to be second or third or nth generation), we cannot just complain just because they are Asian. They are entitled to buy just like any other American citizen.

You likely are referring to SoCal or maybe NorCal as Asian buyers from China and India are dominant in the market and even before this recent crazy from Covid, you often hear stories of them buying cash and screwing over local buyers.

I truly loathe and despise these buyers, foreign money buying at all costs to park their money, taking up available housing for locals, and driving up prices to crazy levels. As much as I despise them, I probably blame our government policy more for turning a blind eye and instead shift the blame to needing to build more affordable housing. Hmm, why do you think our houses are so unaffordable now? It’s certainly not due to a lack of available housing units per household but if you treat housing as another speculative investment, I don’t care how many “affordable” housing you build, it will NEVER fix the root cause.

Phoenix_Ikki,

I don’t have numbers but would guess foreign cash buyers aren’t significant to local cash buyers who own multiple properties. From my perspective it is equally bad but it is the collective economic system our country mostly worships. Profit, profit, profit. There are of course solutions but not that would be possible here. Promising government assistance is just an empty November election promise to try to get a certain demographic of voters. Same you know, different day.

Yes you are correct. My brother who is in San Jose and has been his whole life. All of his neighbors that have sold in the last few years have left San Jose for northern Nevada. All eight new neighbors are Asian. Yes our government is to blame. Welcome to Nevada now go home lol. I have been in Northern Nevada since the mid 80s its crazy up here.

Bash Immigrants for all the problems in US.. How classic.. Same BS all time.

Legal Immigrants come here, contribute to society/economy, pay taxes and live like any other American would live.

As Indian, I can tell you USD is very strong with INR specially in last 3-4 years. So it doesn’t make any sense to buy US properties with Indian money. First of all India has strong democracy and Indians are no afraid Govt will take their money away. Second why would Indian would buy property when its very clear to have 50% negative cash-flow after taking taxes, insurance and rents into consideration. Indians can earn 8% without any risk on Bank deposits itself.

So stop blaming Indians for all your problems. Go screw your Congress Reps and Govt who created the Bubble with ZIRP and massive debts.

There are enough Idiots Locals/Non-Immigrants who made this bubble happen.

Remember Rockefeller Center. The Japanese lost their kimonos on that one…

Totally agree. The ’08 crash was sudden and vicious where I live. The timeframe from “everything is hunky-dory!” to seller desperation with slash and burn prices happened really, really quick. Sellers would bring checks to closing for $50,000, $100,000 just to get out from under the house mortgage. Almost overnight.

Oh but this time is different…at least that’s the gospel that’s been going around for the better part of a decade now. To them, 2008 is a once in lifetime event similar to the extinction trigger for the dinosaurs

There usually are a fair number of advanced warnings – but they are ignored/discounted.

Do you really mean Fall of 2008 rather than 2007? Fall of 2008 was really when things fell off a cliff in a panic.

But 6 months earlier, Bear Stearns (a key player in RRE CDOs) had blown up.

And six months before that, there were reports of deep trouble at Bear Stearns.

And my faint recollection is that Idiot Boom 1.0 peaked in early/mid 2006 in terms of prices/volume – maybe 30 months before things fell off the cliff as panic finally caught fire.

The problem is that sales/volume declines from a peak happen all the time (otherwise history would be nothing more than a “permanently high…permanent high”) so that alone ain’t a great signal.

*But* a broad (albeit retrospective) reading of *many* macro indicators were suggestive that Boom 1.0 was a Phony Boom, with foundations of sand and fraud.

Most simply – the US had shown really, really crappy employment growth from 2001-2006 even as home prices were magically doubling in many huge metros.

Sound familiar?

Anytime some big macro factors are saying the exact opposite of what other big macro factors are saying…there is danger underfoot. Either something is being measured wrong or there is a variable (proto ZIRP or ZIRP) distorting one of those macro factors.

My family began looking recently and got preapproved for a 5.75% fixed rate mortgage. Even at that “great” rate all the houses we have looked at have been more like investor specials. I don’t mind fixing up a bit of a rough place but those aren’t really available for that long. The only ones we can find in our price range would take a major overhaul and there’s no way that’s going to happen when we buy at the top of our budget.

At this point we just figure that if we are going to pay more per month for something, we at least better like it better than the place we’re renting now. So far that’s not in our range. So we wait.

Thanks for the info. I appreciate the in depth analysis on this stuff.

“The median number of days a property sits on the market for sale before it sells or before it is pulled off the market rose to 53 days”

This is the hedonic adjustment for how much new technology has reduced friction time in home sale. Maybe this is equivalent to 68 days, old school?

Yes, there’s that too. All the processes have shrunk. Some that used to take weeks are now near-instantly, such as listing a property and presenting the listing to buyers. In the olden days, this was done in print and took weeks, and it didn’t reach global buyers but only local buyers.

Active listings/ new listings : Tampa and San Diego are flooded. Austin

and Minneapolis (at the bottom) are getting better. The most constrictive areas are below Boston. PGH and DC are the worse for buyers.

Austin is getting “better” how, compared to what and for whom?

When home valuations are far, far in excess of what employment numbers (numbers/salaries) can support, a return to rational valuation is really in almost everybody’s best interest.

Except for speculators whose entire investment rationale was rooted in interest rate gutting (ZIRP, powered by government money printing) and attempted, highly levered quasi cornering of various metro markets.

In any event, phony financing fundamentals pre-ordain valuation collapses.

Just to say — Austin went from outbloodyrageous to just outrageous. I guess that’s technically better. I’m still seeing flippers, of all things. How many more barn doors, journeyman stone hearths slathered in warship gray and bistro bathrooms is enough? How much more luxuriating in vinyl tile does one generation of homebuyers need to indulge in before we amble back toward something like normal?

Wolf, another great article. What about the inventory of Airbnb houses. Are they starting to come back on the market with the rentals slowing down?

Is there any data available on the numbers of Airbnb rentals in each market?

Thanks.

@W K Foster the majority of “AirBnB Houses” are “vacation homes” owned by the “working rich” (the “really rich” don’t “need” to rent their “vacation homes”) who rent the places a liittle when they are not using them to get some extra cash. There will be “some” AirBnB homes that hit the market because the negative cash flow got too bit, but it is a small percentage of vacation homes and an even smaller percantage of the overall SFH market.

This is profoundly incorrect.

An outside analysis in 2023 shows that 3/4 of all Airbnb properties are owned by people or business entities that own more than one property.

In fact, 30% of Airbnb properties are owned by landlords with more than 21 properties. This is a very big business and very sensitive to the tourist economy, more akin to hotels than traditional rentals. If there is a downturn, you can imagine how it could be very ugly.

@Happy1 I’m pretty sure that “3/4 of all AirB properties are MANAGED by business entities that MANAGE more than one property (I don’t “manage” my AirBnB property and since my CPA is the managing member and agent for service of the LLC nobody knows who actually “OWNS” the property). Running an AirBnB is harder and MORE capital intensive and costs WAY more to manage than a hotel that typically has a 50-60% expense ratio (think how much more is costs to have someone drive two miles throught the snow to strip the sheets off beds and wait for them to wash in a residential washer than it takes for a lady to push a cart to the next room to strip the sheets and take them in an elevator down to a huge commercial washer). We have low prop 13 taxes and no debt on our cabin, but on year we have negative cash flow about half the years.

Seems like we will hit a magic point where investors jump on and buy up houses and turn them into rentals, thus reducing home ownership, which is already fairly low compared to most developed countries. Feels like a repeat of just a few decades ago. Nothing wrong with having rentals as I will want that in a few years but it would be nice for those that desire it to have the opportunity. Seems like potentially a lot of lifelong renters.

LOL, if you buy houses at these prices and turn them into rentals at the current rents you will lose lots of money and you will be cash-flow negative and you will bleed to death and the bank will get the house. The biggest single-family landlords have turned into sellers of the homes they bought in 2012 because prices are so high. They’re now building their own rental homes, entire subdivisions of rental homes with a central leasing office because it’s cheaper than buying individual houses.

Homeowners who pull their for-sale house off the market to then rent it out give up after a few months of trying because the rents they could get won’t even cover the mortgage payment. You can see this all over Zillow.

It’s a whole lot cheaper today to rent than to buy an equivalent house. Which tells you that new landlords will bleed to death trying.

Not sure I buy your comment that US home ownership is “fairly low compared to most developed countries”. There are really large differences in tax and mortgage regulations country to country, and poor countries tend to have higher home ownership rates generally. The US rate is just slightly less than Canada and Australia, probably the two countries most similar to the US economically and culturally, and just slightly higher than the UK, which is probably the next most similar country. And our rates are substantially higher than France, Germany, and Switzerland. But it’s a weird mixed bag, we are higher than South Korea but lower than China, Japan, Taiwan, and Singapore.

I buy houses in Massachusetts and either flip or rent them out.

When people call me and want say $700k for an already fixed up house that they are desperate to sell. I look at the numbers as an investor, if it will only rent for $3500 per month but the typical mortgage for this would be around $3946 per month before insurance that’s putting 20 percent down.

Prices are too high for numbers to work as a rental. I have to tell them call me back when your ready to drop the price about 200k.

It’s the flipping and the specu-vesting that serves as part of the pox on residential real estate.

I’m surprised a realtor can’t sell it for market value.

Miami has been one of the craziest markets, but something is changing very quickly.

Updated 09/01

All Redfin metro areas (months of supply) 14.5 weeks

Miami area (months of supply) 34.4 weeks

The market continues to soften in Austin, both in residential and commercial sectors.

The big disconnect is Covid pricing is not sustainable. Sellers and agents don’t want to let go of that once in a lifetime fever dream.

In my central Austin neighborhood there’s a $2.35 million spec home with a “just listed” sign sitting above the “for sale” sign. It was “just listed” 5 months ago.

How’s the area around Liberty Hill doing? Someone I used to work with bought a new build there during Covid, been riding high on equity, last time I checked Redfin still showing mid 500k, above $400K she paid back then, seem like that market is still holding?

@Wolf curious about these already ‘priced in’ rate cuts with respect to mortgage rates. Does that mean mortgage rates likely won’t go much lower in the next 12 months assuming we enter a normal rate cutting cycle of .25 per meeting until we get the ‘neutral rate’ (not a crisis where rates go to zero)?

Which in that case the only thing left to revamp the housing would be price cuts?

My friend is a realtor and keeps going on and on about buy now because inventory is up so I’ll actually have some options and can get an inspection, before spring when the market is just going to sky rocket again because of rate cuts. If we’re already at those mortgage rates though, there definitely hasn’t been any sky rocketing….

She truly believes this, not just realtor hype. Her face went pretty pale when I told her Airbnbs last earning report indicated travel was down all the CO mountain towns nights booked are down 10-15% yoy and more compared to 2022. I can’t find Denver stats but what hits the mountains tends to also hit Denver eventually and Denver has one of the highest rates of Airbnb listings of any major city in the US. I said I think we’ll see some price decreases if tourism continues to cool. She was quiet for a minute and seemed to be processing some cognitive dissonance and then told me housing never goes down, it’s great a investment. I also asked how many homes she thought were vacant, she said oh tons of people moved away during COVID and held onto their properties for price appreciation because housing is such a good investment. Then she suggested I do an interest only loan to just have something for the price appreciation.

I’m curious because I know what I think, but thus far the realtors have been right and I’ve been wrong. Buying would have been significantly cheaper in 2021, paying 100k over asking than waiting out the mania that to me so obviously looked like a bubble. Got quoted 5.875 on a 30yr from my lender two weeks ago, I can’t imagine rates going much lower than that.

Correction. Airbnbs earnings report indicated travel was slowing down, the nights booked in Colorado mountain towns data came from local news sources.

MM1: Anecdotally, yes CO tourism is down in all ways. Volume, prices etc. This is in comparison to absolutely insane times of the past few years.

Our property lowered our nightly rates, after doubling them summer pf 2022.

On the other hand, we are selling our units like hotcakes at very high prices.

I read this as the bifurcated economy. Average people are doing the less expensive trips. The wealthy are repositioning their assets and would rather have a condo that will hold value than the depreciating cash or a potential collapsing stock market.

Yeah that makes sense. I’d heard the $5M plus market was doing great in Vail. I’m sure other mountain towns are similar. I’d heard the lower end of the market in Avon and similar areas where non- multi-millionaire Denverites bought trying to get rich or at least pay for their ski house with Airbnb is suffering and that a lot of those people aren’t getting what they need income wise anymore. Anecdotal but I know a number of locals and I saw more fore sale signs then I’ve ever seen up there this summer.

My advice, get a different friend and if this is an acquaintance then just do a Homer Simpson walk backward into the bush with her. This “friend” sure so sound a lot like those friends that are trying to convince you why MLM is a good way to make some side hustle money…

“My friend is a realtor and keeps going on and on about buy now because inventory is up so I’ll actually have some options and can get an inspection, before spring when the market is just going to sky rocket again because of rate cuts.”

” I also asked how many homes she thought were vacant, she said oh tons of people moved away during COVID and held onto their properties for price appreciation because housing is such a good investment. Then she suggested I do an interest only loan to just have something for the price appreciation”

Haha. The mlm thing is good comparison. Most realtors I know truly believe what they’re saying and they’re in an echo chamber from everyone else in their industry. They could be right though….who knows at this point.

Also tbh if prices started to decline it would probably benefit realtors because it would probably up transaction volumes. The race to the door on the sell side and buyers finally being willing to come off the side lines.

There is another dire possibility I haven’t seen mentioned here. And that is steeply rising insurance rates caused by global warming weather changes cause a huge swath of homes to not qualify for mortgage loans. In these areas insurance is not (or will not be) available at any price. For example, in California (wild fires and mudslides), in Florida, Mississippi and Louisiana (hurricanes and torrential rain), in the Midwest (tornadoes and torrential rain). This will essentially leave only cash buyers who are willing to self insure for these homes, probably reducing demand by up to 90%.

I’ve wondered about this. There’s a lot of homes for sale in mountains right now (CO), way more than I ever remember seeing. I was think return to office and decrease in tourism – but a friend corrected me and said it’s probably property taxes and insurance costs with home values jumping the way they did and wildfire risks becoming a bigger issue for insurers. So that’s pretty valid depending on the area.

This bubble is different. The current absurd pricing is being maintained by the real estate cartels who are backed by Wall Street and pumped by Redfin/zillow universal overpricing. My north county coastal town is controlled by the re cartel. They continue to immediately buy anything reasonable and turn it over to their flippers to pump. Problem is their prices now exceed the town next door that is much nicer. Will Wall Street decide to move on once they see we aren’t going to buy their overpriced homes?

Zillow ruined housing now that everyone can see what their Zillow value was last year and they don’t want to sell for less. It gives people a perceived sense of loss they never had before. Not only that your neighbors and everyone can see what your house sold for. How embarrassing if you had to go $50k less than your neighbor who sold at the peak.

Zillow values were always high from what I’ve been told, because what site gets more traffic, the one that tells you the highest number. I was told anyone who pays Zillow value is a sucker (back pre -2020).

What’s interesting lately is a house will have a certain Zillow value up until it’s listed, then Zillow value suddenly jumps up to the listing price, sometimes this just is $100-150k.

I think prices will be far more stubborn until there’s some sort of event that makes people realize they need to sell. Then the race to the door will be faster.

People won’t sell unless they are forced to.

Real estate is also a phycological game.

Once it starts going down, you’d find lot of sellers coming out and selling even if they don’t need to.

What is needed is a initial trigger, which may come form high un employment if ever it happens

Colorado has the traffic shit show to get to the mountain towns these days. Hiking and biking trails all trashed by the various visitors and new unlikely residents. The value will be in commercial property downtown as bars, restaurants, and boutiques stores as all pack up and leave due to crime and homeless. Go get mugged on 16th street mall or light rail when it is operating. Outside the beltway is where you want to be. The great delusion best places and towns 2 live in CO have ran it course. Denver #1 for car theft and drugs.