Majority of construction spending goes into nonresidential, dominated now by a spending spree on factories.

By Wolf Richter for WOLF STREET.

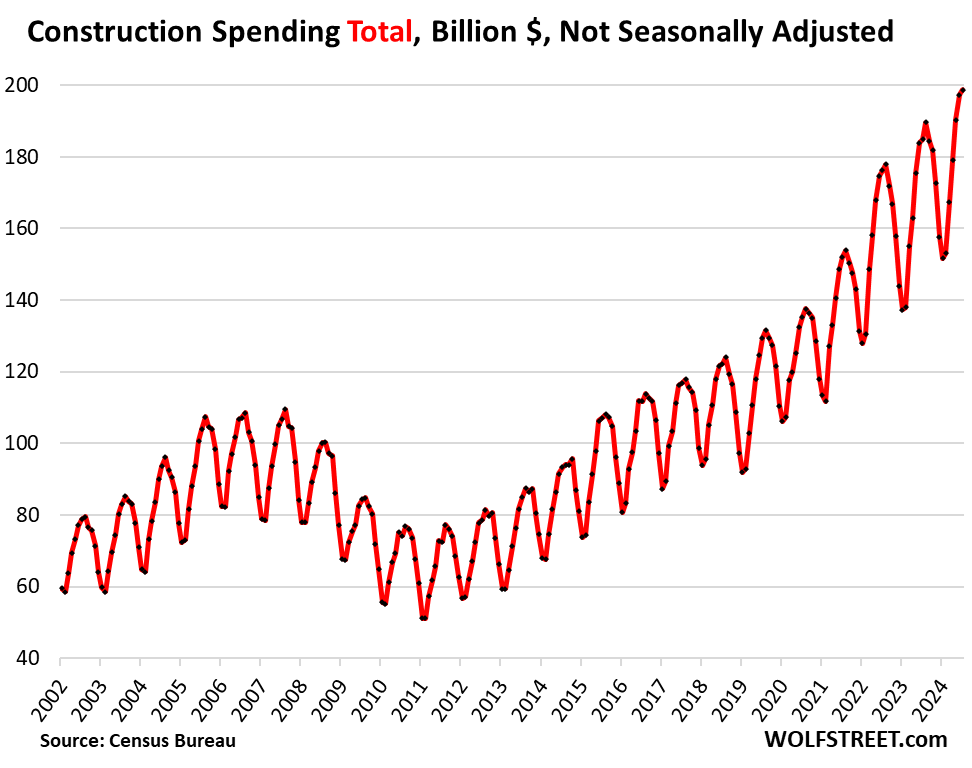

Total construction spending ticked up to a record of $199 billion in July, up by 7.5% from a year ago, driven by record spending in both residential and nonresidential construction, according to data released by the Census Bureau today.

But there had been a pronounced slump in residential construction spending from mid-2022 through mid-2023, and the sector is now trying to dig out of it.

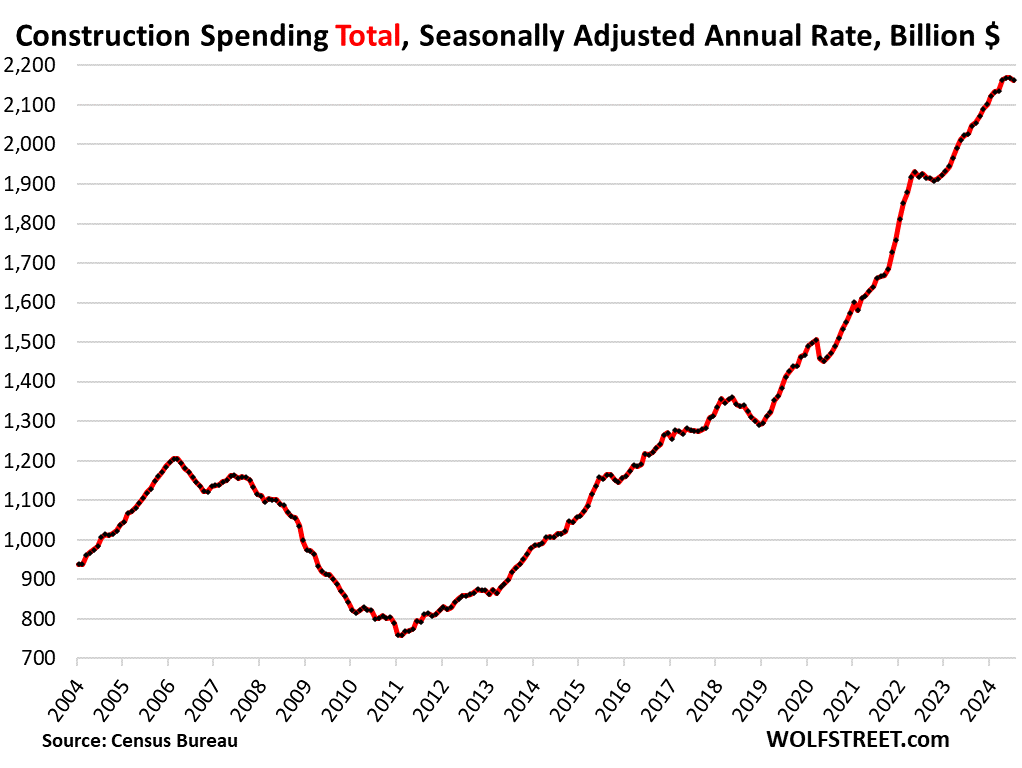

The seasonally adjusted annual rate in July, at $2.16 trillion, was up by 6.7% year-over-year, and down a hair from the records in the prior three months that had topped off a massive construction spending boom starting in 2021.

Note the 35% plunge in construction spending from 2007 into 2011, mostly driven by the collapse in spending for residential construction during the Housing Bust, and to a lesser extent by the drop in nonresidential construction during that time.

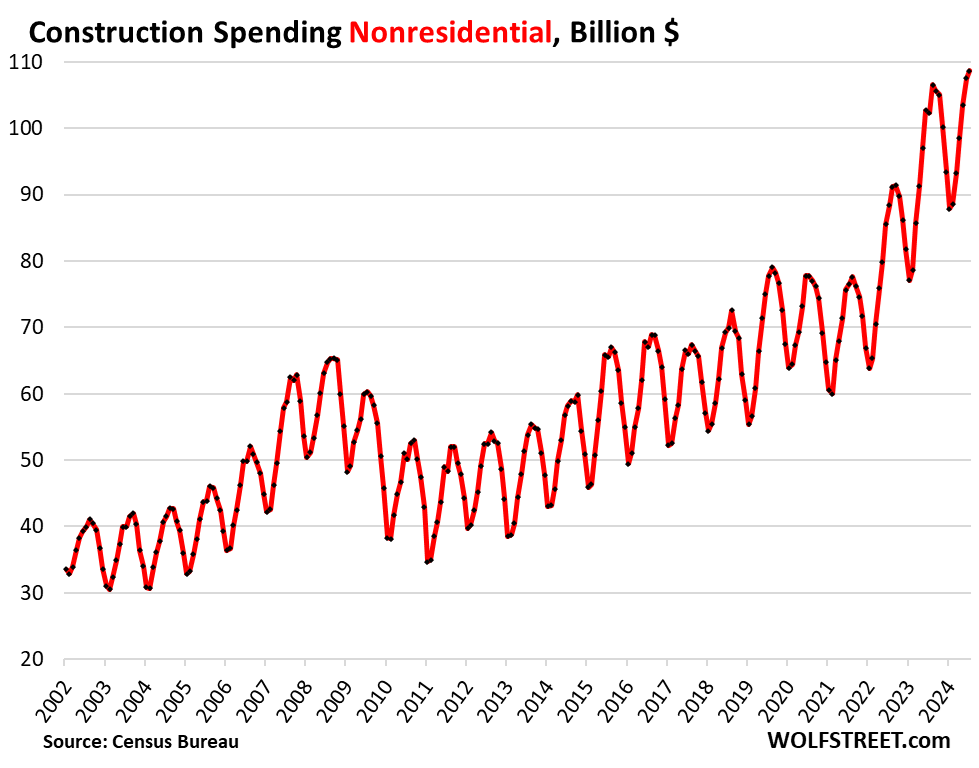

Nonresidential construction spending, which accounts for the majority (56%) of total construction spending, ticked up to a record $109 billion in July, up by 6.1% from a year ago.

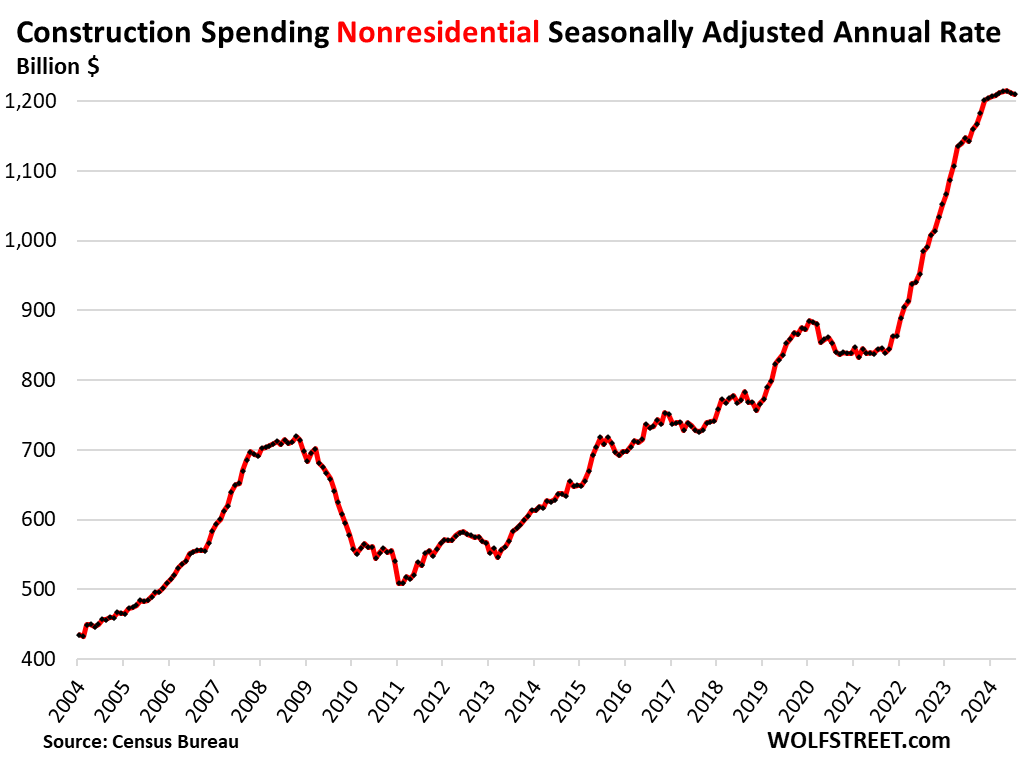

The seasonally adjusted annual rate of nonresidential construction spending in July, at $1.21 trillion, was down a hair from the records in the prior three months, and up by 5.9% year-over-year.

The 45% two-year spike in 2022 and 2023 was in part a result of the eyepopping boom in spending on manufacturing plants, by far the largest segment of nonresidential construction (more in a moment); and in part the result of inflation (more in a moment).

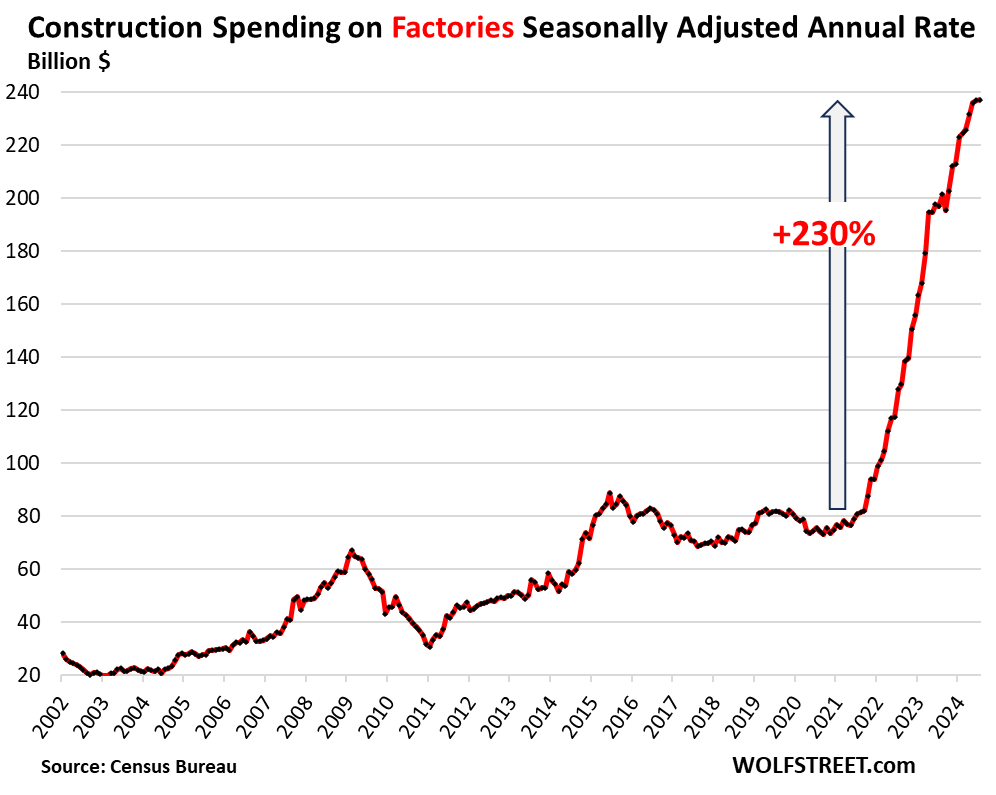

Construction spending on manufacturing plants in July, at $19.7 billion, repeated the June record.

On the basis of the seasonally adjusted annual rate, spending rose to a record of $237 billion in July, up by 20.4% year-over-year.

The eyepopping boom of 230% since early 2021 was driven by the investments in semiconductor plants, EV plants, battery plants, and many other high-value products. We’ve discussed this phenomenon in detail, including causes, for over a year, most recently a month ago:

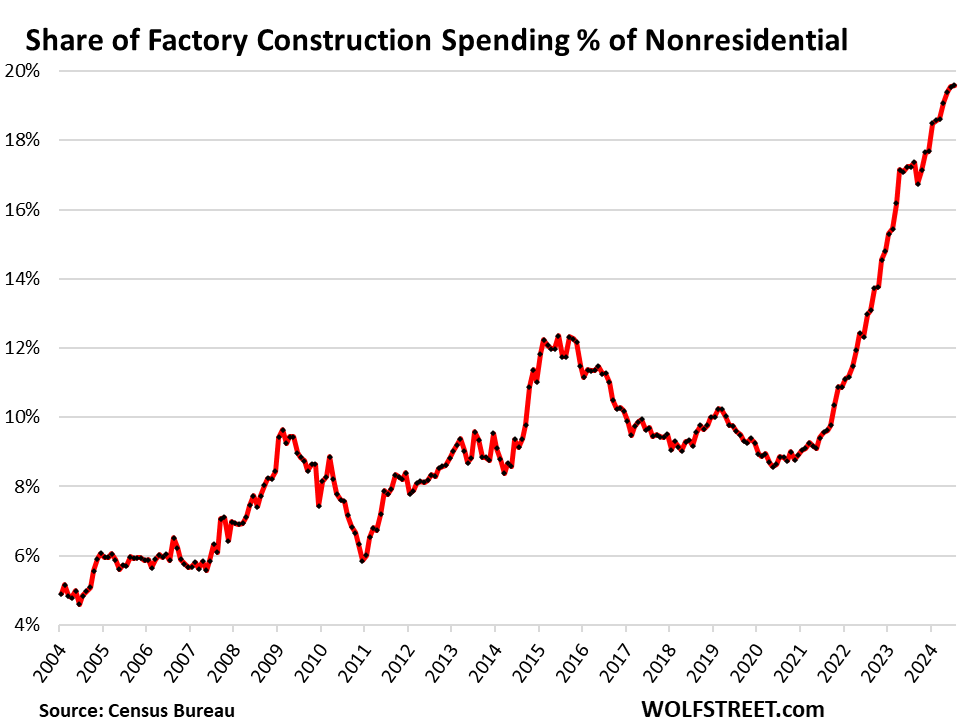

The share of spending on factories rose to a record of 19.6% of nonresidential construction spending, having doubled over the past four years. This is now by far the biggest segment of nonresidential construction:

The top 10 segments of nonresidential construction, in seasonally adjusted annual rates, with year-over-year growth rates:

- Manufacturing: $237 billion (+20.4%)

- Power: $143 billion (+10.0%)

- Highway and street: $141 billion (+3.6%)

- Commercial (warehouses, auto dealers & service, supermarkets, malls, restaurants, farm buildings): $125 billion (-13.3%)

- Office (incl. data centers of which construction is booming, while office building construction has hit the skids): $100 billion (+3.0%)

- Transportation (airports, rail, marine terminals, docks): $69 billion (+7.1%)

- Healthcare: $66 billion (+1.9%)

- Sewage and waste disposal: $46 billion (+10.7%)

- Amusement & recreation: $40 billion (+8.5%)

- Water supply: $32 billion (+16.5%)

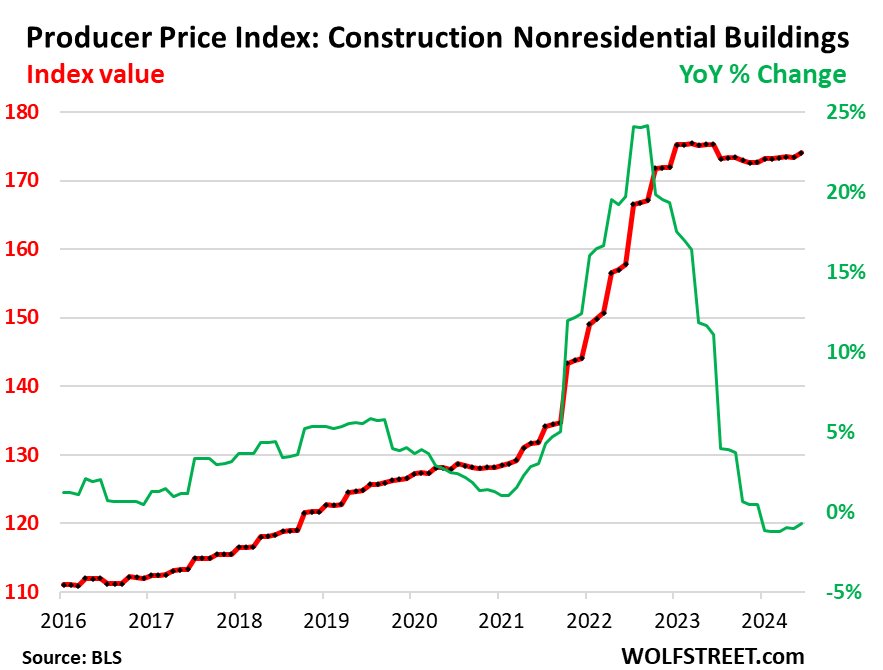

The role of inflation in this boom in nonresidential construction spending essentially ended in early 2023, according to the Producer Price Index for construction costs of nonresidential buildings, after the two-year 35% spike from early 2021 through early 2023 (red).

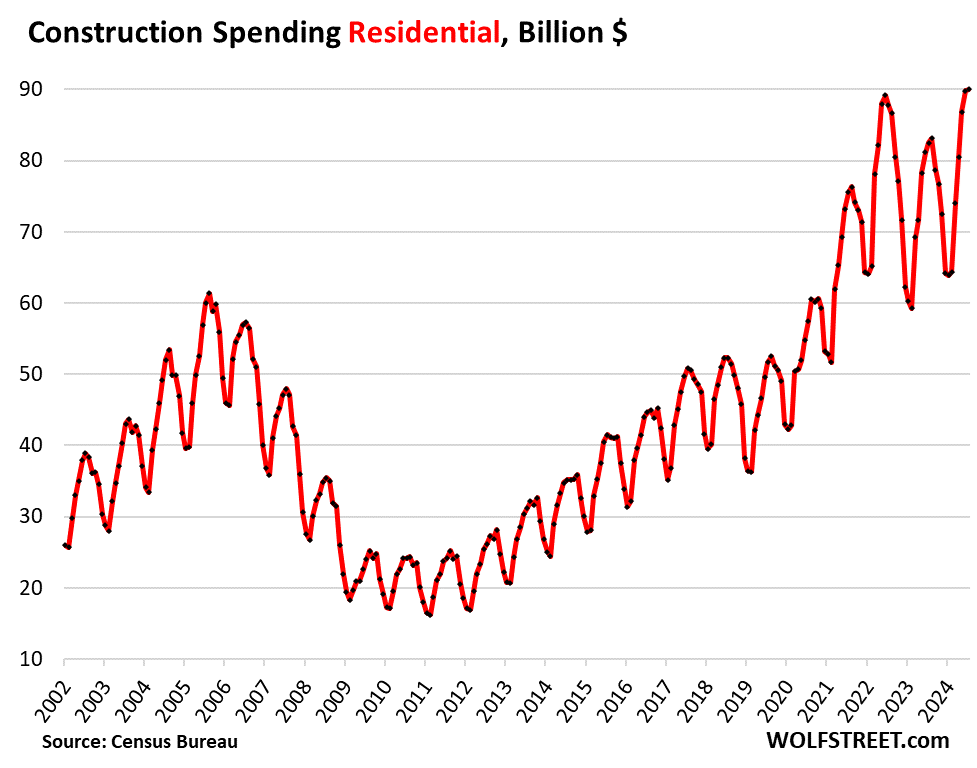

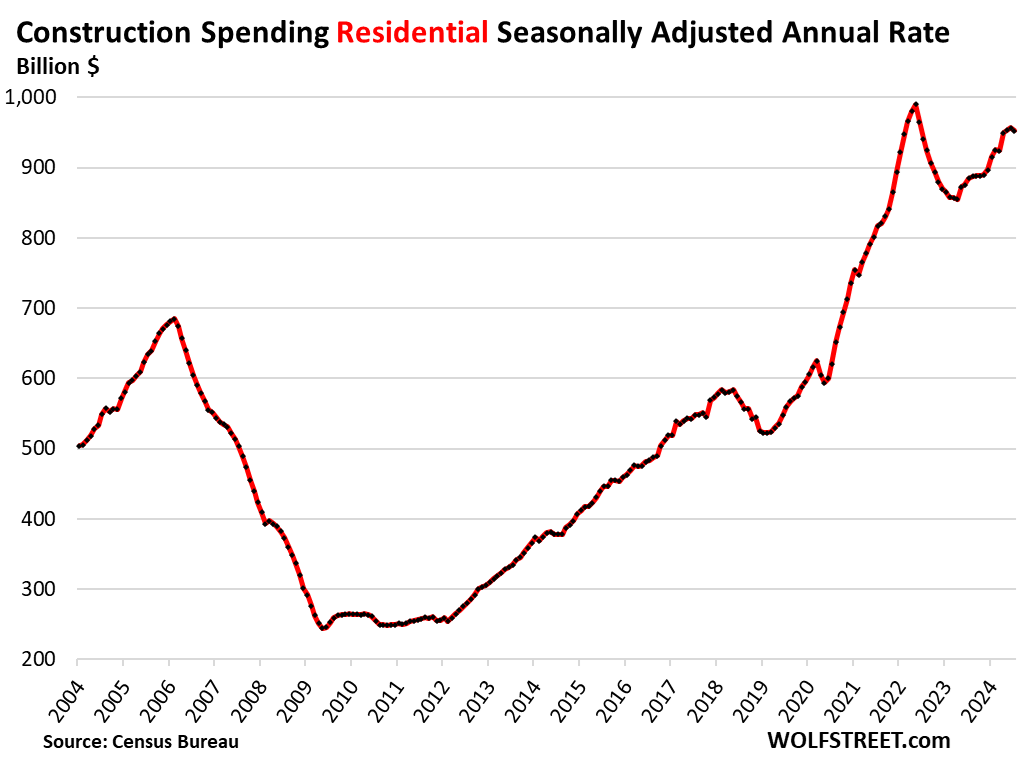

Digging out of the slump: residential construction.

Residential construction spending has been recovering from the slump in mid-2022 through April 2023. That slump had come off the spike in prior years.

In July, residential construction spending edged up to a record $90 billion, from the record in June, and both squeaked past the prior record of June 2022 ($89 billion). Year-over-year, spending was up 9.1%:

The seasonally adjusted annual rate of residential construction spending in July ticked down to $952 billion.

The record occurred in May 2022 ($990 billion), driven by a boom in multifamily construction, with annual multifamily construction starts (in the number of housing units) hitting multi-decade highs in 2021, 2022, and 2023.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

All those factories will require input commodities and energy…

…position accordingly.

Good thing this country is awash in cheap hydrocarbons,

Omg, a single stock just lost $0.3 Trillion in a single day. Quickly, cut the rates!!

Oh mine..Nvidia down close to 10%? Unacceptable, I am sure Siegel is already scheduling MSM interviews and scream about emergency rate cut now..the man can’t wait another 2 weeks and .25 cut is just too little now we’re dealing with depression cliff…/S

Bet you by tomorrow, BTFD squad will be back to full force. Today’s action is simply because PPT is currently still on an extended labor day holiday drinking spree..

You’d figure Nvidia would have used their AI to predict this.

1:04 PM 9/3/2024

Dow 40,936.93 -626.15 -1.51%

S&P 500 5,528.93 -119.47 -2.12%

Nasdaq 17,136.30 -577.33 -3.26%

VIX 21.34 6.34 42.27%

Gold 2,523.60 -4.00 -0.16%

Oil 70.34 -3.21 -4.36%

Why are more manufacturing facilities being built at a time when manufacturing in the US is significantly contracting?

1. what you saw today was a sentiment survey of executives (the ISM Purchasing Managers Index or PMI), which asks questions of this type:

Was your production up, the same, or down in this period compared to LAST MONTH. So this is month-to-month sentiment, not numbers. Up = +1, same = 0; down = -1. The whole thing is averaged out. 50% = same number of executives said up as down; less than 50% = more executives said down than up; over 50% = more executives said up than down.

ISM: “A Manufacturing PMI above 42.5% over a period of time, generally indicates an expansion of the overall economy.”

Today’s ISM number was 47.2%, well above the 42.5% line.

After the boom in 2021 through late 2022, the PMI has been below 50% for nearly the entire time, and nothing bad happened, though ZH made it sound like everything was collapsing, LOL.

A small company executive weighs the same as a giant-company executive, so that’s another problem. Executives get in a bad mood, and a few more say down than up, and you’ve got your below-50% number. Enjoy with care.

2. NO ONE is going to make a long-term strategic decision (building a factory) based on a PMI sentiment survey. PMIs are just supplementary info for short-term fun. They have zero long-term significance.

3. Building factories in the US is not to meet new demand, but to shift production from foreign countries to the US to make US companies less dependent on China. Dependence on China produced catastrophic results for US manufacturers during the era of shortages. It seems everyone learned a lesson.

4. US dependence of foreign countries for semiconductors has taken on scary proportions, and also led to catastrophic shortages, including for automakers – and resulted in a big bout of inflation – and addressing it has strategic importance for the US economy. No semis, no economy.

42.5 as the threshold. I was thinking it was 50.

What this says is: If manufacturing PMI is at 42.5%, the OVERALL economy stall.

Work in Construction near Raleigh. A lot of manufacturing facilities coming online. But they are Pharma-manufacturing, so they aren’t the metal bashing, or even electronic component assembly that most associate with manufacturing. Manufacturing usually swings hard with the economy. I am assuming this is your typical late-cycle activity – maybe even beyond late cycle Wile E. Coyote running off the cliff and waiting for gravity to take hold activity.

The WSJ had (Sept 3) a long piece online about Biotech and pharma buildings being in a huge glut. They seem to be talking about lab/research spaces. And I agree, these have dried up considerably around here.

The glut in “life sciences” you’re talking about are more or less special office buildings that are used for research, labs, administrative stuff, etc. It’s part of the office building glut.

Because this is either direct and/or government induced spending and most economists would classify these investments as adjacent to government spending. I don’t know why Wolf doesn’t emphasize this more.

The funds from the CHIPS act haven’t even been disbursed yet. Some have been “awarded” and “announced,” but it will take years for all the funds to be disbursed, and it hasn’t even started. This is still to come.

The huge impetus behind this factory construction boom are the catastrophic shortages that US companies experienced during Covid, including semiconductor shortages that brought the automakers and other high-value manufacturers to a near-halt. No one wants to go through that again. It has shown that the US has become scarily dependent on supply chains running through China, and they understood that China could choke the US economy. It finally sank in, after decades of globalization, that globalization comes with huge risks and costs. That realization – which spans across industry and government – is what you’re looking at here. Trump was on the right track with his tariffs, and Biden kept them largely in place, but it took Covid to bring out the true and scary dependence of US companies (and consumers!) on foreign manufacturers.

In most cases, US companies ARE the ‘foreign manufacturers’ who simply have facilities located abroad, and the entire CHIPS act should be rescinded and the funds clawed back.

But semiconductor manufacturers aren’t investing in the low-dollar components that actually caused the shortages. They’re shoving their money and CHIPS funding into high-margin fire breathing GPUs and CPUs for server farms. They’re not going to be onshoring the small/simple low margin $0.05-$10 ICs and microcontrollers that go into mudane devices like your car’s control modules or your coffee maker. Nobody is making pc board capacitors or resistors or any the neccesary passive components stateside. And even those high dollar GPUs and CPUs are useless without low dollar support components. Basically the money being showered on U.S. semiconductor manufacturing isn’t going to address future shortages at all. It’s just blowing up the second coming of the .com bubble rebadged for AI.

The US got very lucky. That dependence was only going to get worse, and at some point China would have tightened the screws.

Nothing is moving in L.A.

I’m struggling with the continued inclusion of Data Centers in “Office” rather than a more appropriate category that reflects the other dimensions of such buildings (occupancy, commute impacts, need for nearby retail etc).

If it gets big enough — and it might — it should be in its own category.

20 years ago, data centers were nearly nada. Companies had their own servers in their own office buildings and factories. The movement to “cloud computing” and now AI in the cloud has fueled the rise of the data centers.

This is a landmark achievement of Biden’s administration, which it rarely receives credit for: re-onshoring. The real benefits will come in the next years and decades as those factories start producing.

Other than the CHIPS act, what has the current administration done to promote return of manufacturing to the US? It seems more like a pragmatic decision by businesses than something politicians have done.

The Inflation Reduction Act &Bipartisan Infrastructure Law with its requirements on materials & products being made in America.

The creation of the Made in America Office at the White House Office of Management and Budget.

The elimination of the Reagan-era Buy America waiver for manufactured products in federal-aid highway projects.

Updating the Buy American Act to increase the domestic content requirements for Made in America for federal procurement from 55 percent of the value of their component parts that are manufactured here to a threshold of 60 percent in 2022, 65 percent in 2024, and 75 percent in 2029.

The Executive Order on Amending Regulations Relating to the Safeguarding of Vessels, Harbors, Ports, and Waterfront Facilities of the United States.

The Broadband Equity, Access, and Deployment (BEAD) Program.

The Make PPE in America Act.

But, other than that, nothing.

Every administration has a slew of “Made in America” bills. Biden, Trump, Obama, Bush etc. That is just politics as usual. The next administration whether it is Harris or Trump will have the same.

Clearly, the lessons learned from extended supply and manufacturing lines during Covid is the real cause.

So what.

The previous administration tried tariffs, renegotiating trade deals, tax policy to encourage repatriation of corporate profits, etc. and the trade deficit has continued to get worse under both administrations. Much worse today than 2016 or 2020.

What part of that 230% growth was due to any of these policies?

“Give me of examples of what has been done.” … “Well other administrations have done things too!” “So what?” lol these responses, how embarrassing. Thanks for the specifics WGH

Hey Ben, I guess I should have asked what has the administration “actually” accomplished, so maybe you partisans will actually stop and think. What has the Made in America Office actually accomplished? You know, backed by data, not just your feelings.

For better or worse, government subsidized enterprises are usually stimulating. Tariffs, government set targets, price controls, etc are not stimulating, just more bureaucracy or worse.

Not one of the damn things this administration or the previous or the previous has done has improved the trade deficit.

BTW, if dumb ass Trump gets back in the white house and the CHIPS act money kicks in, are you gonna give him credit or are you gonna give credit to Biden’s Made in America Office?

BABA = Buy American, Build American and is a requirement of BIL grant recipients for certain components.

Ya ok, but besides that overwhelming barrage of examples

Don’t forget the “Inflation Reduction Act” successfully dumping trillions into the inflation braking systems. [sarc]

@Wolf

You pointed there was some 35% inflation between 2021-2023. So, I am trying to figure out if the higher spending (or what percentage) on non-residential (factories) is a result of this inflation combined with Inflation Reduction act dollar give aways OR real re-shoring efforts. It is clear if the re-shoring would would keep the inflation higher (Boing union wanting to strike!)

we hear German economy is slowing down, China in doldrums; would the new constructions be really be used or go the way of Amazon spending spree on warehousing? When I see Temu offering great prices, I wonder if they got all those Amazon warehouses for free to ship the stuff from locally!

Construction spending on factories is up 230%. Inflation for nonresidential construction was up 35% over the same period. The rest is increased net construction.

Some of the CHIPS Act funds have been “awarded” but due diligence etc. still needs to be done, and the funds have not been disbursed yet. Government moves slowly. So that’s still to come.

you can read the details here:

https://wolfstreet.com/2024/08/01/eyepopping-factory-construction-boom-in-the-us-reaches-new-highs-amid-big-corporate-strategic-rethink/

and here

https://wolfstreet.com/2024/06/03/eyepopping-factory-construction-boom-in-the-us-semiconductors-auto-industry-and-everyone-else/

which includes this excerpt:

“The first grants and loans under the CHIPS act were awarded only in March 2024, spearheaded by the announcement that Intel would get up to $23 billion in grants and loans, plus up to $25 billion in tax credits. This was followed by announcements that TSMC (the world’s largest contract chip maker), Samsung, and Micron each would get over $6 billion in grants, and that Global Foundries would get $1.5 billion in grants. Smaller announcements followed.

But the deals will take time to finalize, and disbursement will be spread out over phases.

The total costs of building a fab, to equip it, and to get it up and running are huge. TSMC has announced over $65 billion in investments, including $40 billion for two fabs that are now under construction near Phoenix. Despite assorted delays and issues, TSMC said that its first fab “is on track to begin production leveraging 4nm technology” in the first half of 2025.

Intel has rolled out $100 billion in investment plans, including $43 billion for facilities in Ohio, New Mexico, Oregon, and Arizona. Texas Instruments is investing $30 billion in Texas. Samsung is investing about $45 billion in Texas. Micron is talking about $125 billion, with new plants in New York and Idaho. These numbers are gigantic, but only a smallish part of it all will be construction costs of the building and will be tracked here.

New factories beyond semiconductors: Chip plants are written all over this boom in factory construction because the plans are huge and costly, heavily government subsidized, and get all the publicity. But there’s more going on.

Here is a sampling of announcements beyond semiconductors over just the past few weeks:

Toyota announced a $1.4-billion investment in its Princeton, Indiana, facility to assemble its new three-row battery electric SUV, bringing total investment in Indiana to $8 billion. “This investment will not only provide plant infrastructure to build the all-new BEV, it will add a new battery pack assembly line using lithium-ion batteries supplied by Toyota Battery Manufacturing North Carolina, a $13.9 billion facility slated to begin production in 2025,” Toyota said on April 25.

Kohler Co., maker of kitchen and bath products, inaugurated a 1-million-square-foot manufacturing facility in Casa Grande, Arizona.

Crystal Window & Door Systems announced a new manufacturing facility in Johnston County, North Carolina, to specialize in aluminum and vinyl extrusion, and window and door fabrication.

ION Storage Systems commissioned a solid-state battery manufacturing plant in the US, in Beltsville, Maryland.

GAF Energy inaugurated its 450,000-square-foot Timberline Solar manufacturing facility in Georgetown, Texas.

GF Casting Solutions AG, a division of Georg Fischer AG, headquartered in Switzerland, announced a new manufacturing facility in Augusta, Georgia, to produce large structural cast-aluminum components for the automotive industry.

Boviet Solar announced a 1-million-square-foot manufacturing facility for solar panels in Greenville, North Carolina.

Green New Energy Materials, a battery component manufacturer, announced a $140 million lithium-ion battery separator manufacturing facility in Denver, North Carolina.

Intel should simply sell itself off to the PRC and shut all fabs and other facilities in the US by the end of 2024.

Never bet against the USA!

We certainly do not need or want any more factories in the US and we need to close around 50% of those that are presently operating and source manufacturing to the best lowest cost producers globally.

🤣❤️

1) China’s RE was enabled by overcapacities in the steel, coal and other industries. The Chinese gov will order those sectors to cut prices in order to avoid a glut.

2) When our national factories will be completed demand for highly skilled workers will rise. The US gov raised tariffs to protect those jobs and those factories. In other sectors, not protected, consumers will benefit from deflating prices. Wages will rise. Consumption fall. Speculations will explode.

3) Higher gov revenues from tariffs and taxes will fill the gov coffer without raising taxes. If the Fed cut rates to ease debt payments the budget deficit might flip to a surplus. The Fed will give the gov a chance to be frugal in order to cut its debt. After a few years the Fed will have to raise rates above the sticky CPI, selling short Dow speculators to prevent an 1929 event.

In order to be competitive, these factories will be filled with robotics, not skilled Americans demanding triple the wages paid to workers outside the country.

When the iPad went into production, TSMC built the facility, hired 3,000 engineers and a hundred thousand workers, and did it in one year. Eventually providing employment in the city for a million people.

Apple attempted to manufacture the Mac Pro in Austin Texas. It was delayed almost 2 years, and was the most expensive desktop in the world.

What most of you don’t realize is that less than 20% of Chinese manufacturing production is imported into the USA. Any manufactured product in the world can be taken to China and they will replicate it in 90 days, quality determined by how much you are willing to pay.

You go into a store outside North America and USA manufactured products are literally nonexistent. Outside the tourist areas, of course.

In the last 15 years more than 100products I brought in from Amazon are now available off the shelf. Not a single one is manufactured in the USA.

Have you bought a car recently in the US, such as a Toyota Tundra pickup, a Tesla, a Honda, etc.? They’re all made in the USA.

Have you bought any of the equipment needed for oil and gas production in the US? The US is the largest oil and natural gas producer in the world, and the technology is American, and most of the equipment is made in the USA.

The USA is the second largest manufacturing country in the world, behind China, and bigger than the next three combined.

But yes, lots of cheap consumer products are made overseas. There are not a lot of reasons for the US to be making T-shirts.

MW: These semiconductor ETFs just had their worst performances in four years

MW: Intel’s stock hasn’t been this cheap in at least 30 years.

That’s what many years financial engineering, rather than actual engineering, inevitably lead to.

If Intel hadn’t wasted and incinerated $94 billion in cash on share buybacks instead of investing it in research, development, and manufacturing plants, it wouldn’t be so far behind now.

All I know in my little piece of flyover heaven

Is the breaks are smoking.

From residential construction, local truckers,

And our industrial parks.

I would have to assume our slow down it will felt nation wide at some point.