But buybacks occur at huge losses for investors. Today it bought back a 1.25% 20-year bond for 66 cents on the dollar.

By Wolf Richter for WOLF STREET.

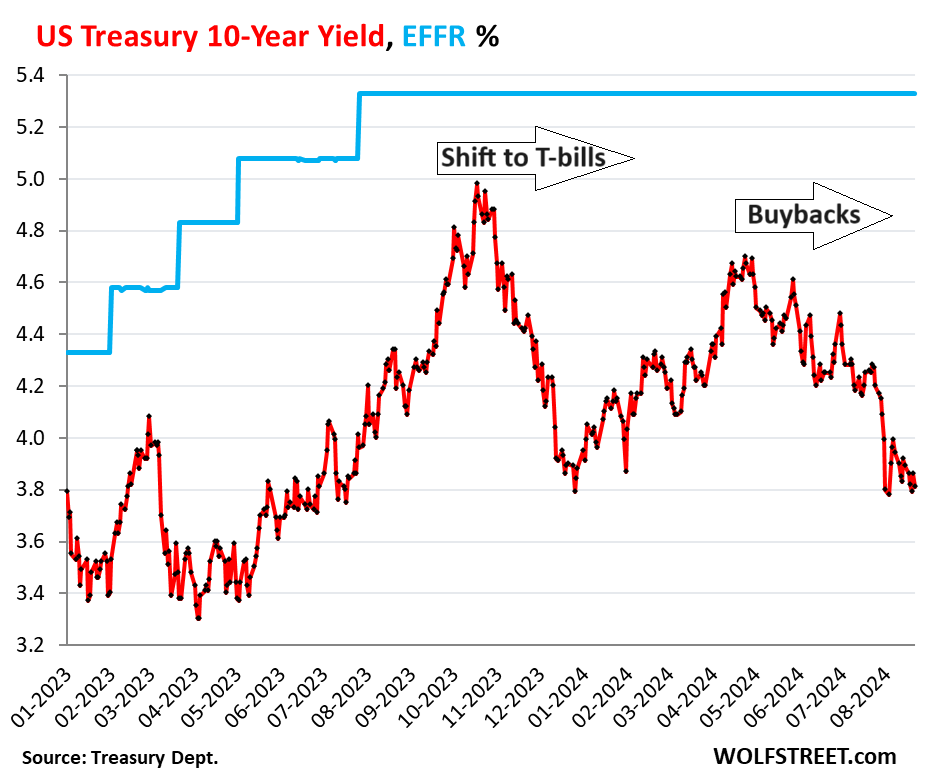

The US Treasury Department has been doing two major things to aggressively push down long-term yields on US government debt, and thereby long-term interest rates in the economy, such as for corporate bonds and mortgages:

- Shifting a larger portion of issuance of new debt to short-term Treasury bills, instead of longer-term notes and bonds, thereby increasing the proportion of T-bills outstanding.

- Buying back older longer-term Treasury securities with the proceeds from issuing new Treasury securities, so essentially replacing old securities with new securities, which doesn’t involve money creation and is not QE, but a swap of securities. It does put a big regular buyer into the harder-to-trade end of the bond market.

We can see the effects of those two policies on the 10-year yield. The increased portion of T-bill issuance starting in the second half of 2023 took pressure off the 10-year yield, which had been spiking into October 2023 and briefly kissed 5%. The buybacks, which started in April, coincided with a decline in the 10-year yield of nearly 100 basis points, even as the Fed was pushing back against rate-cut mania.

Adding more inflationary fuel to the economy.

Since the Treasury Department started this shift last year, T-bills – bracketed by expectations of the Fed’s policy rates – have yielded above 5%, substantially higher than the 10-year yield, which has ranged from 3.8% to just under 5% over this period.

So short-term, this strategy costs the government and taxpayers more money, but long term, if the bet works out, Treasury would reduce the effects of locking in the higher interest rates (interest expense!) on its incredibly ballooning debt for many years to come. But we doubt that saving the taxpayer money years in the future after this administration is long gone is the objective here. No one ever tries to save the taxpayer money.

The primary objective is clearly to manipulate long-term interest rates lower to stimulate the economy since long-term interest rates matter to the economy much more than short-term interest rates.

These lower long-term yields contribute inflationary fuel to the economy. They reduce mortgage rates. They encourage corporate leverage. They loosen financial conditions. This comes on top of the vast deficit spending, which also adds inflationary fuel to the economy.

These efforts by Treasury to push down long-term interest rates are in direct conflict with what the Fed has been trying to accomplish since it began hiking its policy rates.

The shift to T-bills.

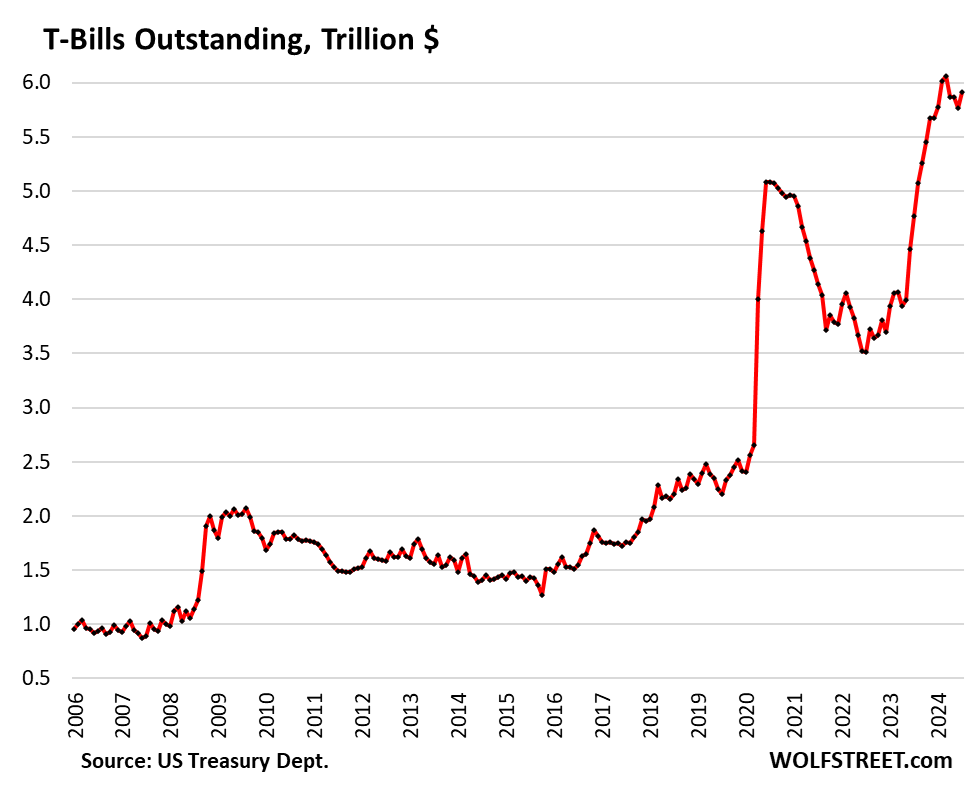

T-bill issuance has exploded since the debt ceiling was suspended in June 2023, and total T-bills outstanding spiked in 12 months by $2 trillion, or by 50%, from $4.0 trillion in March 2023, to over $6 trillion in March 2024.

Tax Day this year brought in a record amount of cash by mid-April, so T-bill issuance slowed in April through July. The outstanding amount in T-bills at the end of July was $5.9 trillion.

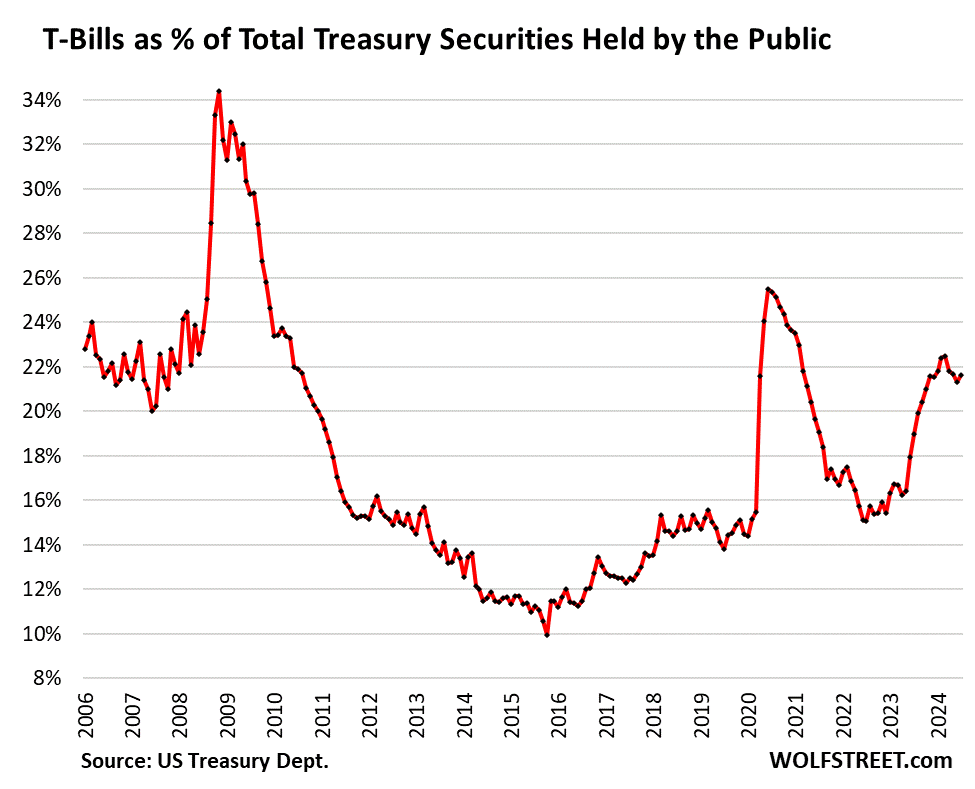

T-bills yields are bracketed by expectations of Fed’s policy rates and are not much influenced by issuance. There has been huge demand for T-bills.

Between March 2023 and May 2024, the share of T-bills outstanding jumped from 16.7% of total marketable Treasury securities to 22.5% in March 2024. The record receipts around Tax Day relieved some of the pressure. But in July, the share started ticking up again. This is the shift to T-bills:

The shift to T-bill issuance is a bet that long-term interest rates would be lower over the next few years than they’d been in 2023 and 2024, and that the government could refinance those T-bills with lower-rate long-term debt. It’s thereby a (courageous?) bet that inflation will just quietly go back to 2%.

Treasury Secretary Yellen was infamously wrong about these inflation bets before, including in January 2022, when she said that she expected inflation to go back to 2% by the end of 2022. But 12 months later, the December 2022 reading of the core PCE price index, the Fed’s preferred measure for its 2% target, came in at 4.9% and core CPI at 5.7%. Inflation is hard to just wish away.

Buybacks are an even more aggressive move.

Under the buyback program, Treasury is buying back older “off-the-run” securities with the proceeds from issuing new securities, so swapping off-the-run securities for new on-the-run securities. This is essentially a swap of securities and doesn’t involve money creation and is not QE.

But it does add a big relentless bid to a portion of the Treasury market where liquidity can be thin, and where an investor that needs to unload a pile of off-the-run securities could do so only at a substantial discount compared to on-the-run securities.

By Treasury stepping into this end of the market, it is adding liquidity and its relentless weekly bid has the effect of lowering long-term yields. It started discussing this last fall and kicked it off in April, at first with smaller weekly auctions (on Wednesdays) that then increased in size. In recent weekly auctions it bought back between $2 billion and $4 billion.

Investors lock in massive losses.

At today’s auction, Treasury bought back $2 billion in bonds. All bonds it bought back today have maturity dates between 2040 and 2042.

For example: 66 cents on the dollar. One of the eight bond issues that Treasury bought back today was $110 million of 20-year bonds (CUSIP 912810SR0), with a 1.25% coupon. The bonds had been issued in June 2020 when long-term yields had hit rock bottom.

Today, the 20-year yield is 4.22%. A 20-year bond that was issued four years ago, and has therefore 16 years left before maturity, trades like a 16-year bond, not a 20-year bond, and the 16-year yield would be lower than the 20-year yield.

Treasury bought back this 20-year bond at 65.64 cents on the dollar, in other words, at a discount of 34.36% to face value. Alternatively, the investor could have held it to maturity, collect 1.25% in coupon interest per year for 16 years, and then get 100 cents on the dollar.

For example, 77 cents on the dollar. Another of the eight bond issues that Treasury bought back today was $599 million of a 20-year bond with a 2.375% coupon, issued in March 2022. The price: 77.376 cents on the dollar, or a discount of 22.64% of face value.

The bonds that the government repurchased are then retired. The cash used to purchase those bonds has to be raised from selling new bonds, and so effectively, these older bonds are replaced by new securities.

These buybacks allow big investors, such as banks, to sell off-the-run long-term bonds at massive losses, but without further pushing down prices and pushing up yields, and without therefore further increasing their losses. This has the effect of propping up long-term bond prices and pushing down their yields – which then translates into lower interest rates in the economy.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

And lower tax receipts for the government as investors can use the losses to reduce their tax payments…

Not that simple.

That loss would be a capital loss, against long-term capital gains.

But investors get the cash, so maybe $66 for that $100 in 1.25% bonds, and then they invest that $66 in T-bills at 5.2%, and make more interest income, $3.43 a year, instead of $1.25 a year ($100 at 1.25%), and pay higher taxes (nearly 3x) on that interest income.

From the government’s point of view, the transaction lowered its total debt by $34. So some of that $34 would be given back to the selling investors via the capital loss tax reduction, but then it would pick up the income taxes on the much higher interest income from the investor — and for years to come.

But these bonds are being bought at market, not called. So the investors who choose to sell will be the ones who most benefit from the upfront capital loss. Probably corporations whose capital gains are taxed at the same rate as ordinary income…

Like a big clearinghouse bank, for example?

A dark view of reality. I just assume everyone else is as dumb as me.

Love is my bet. So far it’s ahead by a nose, since the first written word six centuries ago.

Not even considering that nature has no compunction toward any existing human understanding. The San Andreas is overdue.

I don’t know what the current capital ratio for insurance companies is, but a couple years back about 2/3 of their capital was Bonds. I suspect that is one major reason for rising premiums across the board. Based on your examples, they must be a hurtin’…

Or am i missing something?

Yes, I would say that you may be missing the trees in the forest.

The implication here is the Treasury has been stimulating the economy with cash like issuance of short term debt to fund the excessive debt taken on by the US government without proper oversight.

Stay short, it’s still going to pay a reasonable rate of interest for the next six months without risk.

I wonder if you’re being a bit uncharitable to the Fed, in ascribing their motivations for this set of moves.

Fed are clearly aware that there is no appetite to control spending from anyone in Washington. It seems like a very smart move to cut future interest expenses.

I have no idea where you got that. I don’t think I said anything about the Fed other than:

“These efforts by Treasury to push down long-term interest rates are in direct conflict with what the Fed has been trying to accomplish since it began hiking its policy rates.”

You also said it wasn’t their primary motivation. It very well could be the case that this was a plan of theirs all along.

The way the Fed has navigated this landing has impressed me very much. It obviously isn’t done yet, but I don’t know anyone who predicted things would go this smoothly after the orgy of money printing over the last decade.

Things have gone smoothly up to this point in time.

There is no start and finish, just a continuum of events with associated time lagged consequences.

a soft landing with many TRILLIONS of new debt???

U can’t be serious, that’s no landing at all,,, just more kicking the can farther and further down the road and onto the shoulders of the young folks

Pardon me, but I respectively disagree with your admonition of the Fed’s delft handling of their extrication from a shit pile of their own making.

The economy is clearly being stimulated by former Fed officials who now work for the Treasury enough without the idiots at the FOMC, remarkably famous for their fuck ups going back to the great depression, to feel the urge too cut interest rates. A knee jerk genuflection too the invisible hand.

The problem is the Fed has in effect been sandbagging the American worker/consumer. It is not trying to keep a lid on inflation at all. It is merely paying lip service to some sort of nebulous inflation fight. In actual fact it is actively trying to stimulate and overheat the economy as usual. Powel is not in any way mystified that things haven’t rolled over. He never wanted anything to break. The Fed has been easy more or less the entire time and when the bond guys get ansy about the lack of inflation fighting and back the curve up the Fed and Treasury find a way to get the massive inversion back on track. In all honesty Wolf it is just sad.

re: “He never wanted anything to break.”

He’s watching the fluctuations in the market making portfolios rise and fall with big movements. Makes a lot of people nervous.

Kind of like the “war on terror” where the government first had to create their own terrorists and then spent a lot of money through the military and contractors and weapons, ect…. on fighting terrorists they pretend they never knew they created. I’m not joking. If they can physically kill people for money, inflating away your savings ‘ain’t shit’. No conscience, no accountability, no positive leadership, and no good results for the future of the average person……. but great for the puppet masters who run this show.

Sorry, I get you now. My mistake.

Wow. I buy three year Notes and short bills. Got a 4-week rollover this week at 5.33%. The notes are coming in at about 4.3.

I can’t imagine sitting on a 1.25% bond and having to sell. Maybe the Treasury does have an opportunity now to buy those up at 66-77 cents or whatever and retire a few hundred billion (trillion?) of debt. Then, during the next recession when the ten year is at 1.5 or 1.75% again they sell long bonds to the chumps and pay off those 5+% bills.

Yes, it’s tough. People are sitting on TLT that’s down 41% since June 2020, and that thing trades every second of the day at this price.

Thanks for posting the treasury buyback link….that seems like a windfall for the Treasury.

What I find fascinating is about 3/4 of the 2 billion were at 2% or higher rates, 2.75% bonds and higher were offered but rejected, and there were even 4.75% bonds in the offer pool.

Oh goody…so does this mean the RE industry and all the people waiting for the mortgage rates to fall further will get what they wish for with 10 years yield being pushed down? I am sure this will do wonders to support the pricing will only go up narrative..

The funny thing is, with the timing, even though not related, people will probably assume the upcoming Sept FED rate cut is what drove the mortgage rate down…maybe that’s enough to illicit another round of FOMO in certain RE markets..

The problem is that price has to fall in the absence of a massive wage inflation that made the affordability attractive. Which is considered a problem for our corporate oriented government who have been instructed by their lobbyist sugar daddies to vote against American workers.

All the while, it was the general population that made it all possible. A classic tale of the naive fool being taken advantage by the huckster.

What’s left of America since the industrial migration to the desperate communist party labor force allowed the American companies to sell their Chinese products at the same price as the domestically produced products.

It’s been so much better since the Ivy League took over.

The Aristocracy is so much better at making decisions as are the hoi polloi.

Wait, I thought American workers elected our politicians who are representing our interests. Are you suggesting the greatest democracy to ever exist is a complete illusion and sham? After owning people to produce goods at a low cost the only option when that ended was to find other ripe places for exploitation.

@Glen: Let’s see if anyone who has less than a few million dollars in the bank can run for office. That is the test of a real democracy. And can someone owning a few million dollars really represent the interests of the middle class and the poor?

As George Carlin says – we have the illusion of choice. Because the interests of 330 million people cannot be represented by 2 parties who are mostly in the control of PACs and lobbyists. Sorry if I shattered your illusion.

Sean Shasta,

I was being sarcastic as especially fun to poke fun during political season where people think either party cares and are quite passionate about it.

Inflation results in more money in circulation, reserves, etc. The result is an injection of dollars into the economy. QE 2.0

Phase 3 will be when they further suppress longer yields by letting the T-bills mature and issuing more in the long end of the curve.

If you are investing in bonds, its hard to see any reason to buy the long end of the curve.

Unless you are a life insurer or have other predictable future liabilities.

Hence maybe why this time is different. Inverted yield curve don’t mean jack when it comes to predicting the next recession

Only if they can keep the charade going forever. At some point, something is likely to break. It’s just a matter of knowing when to make it investible.

I cannot think of a single reason to go longer than six months at this point.

So, is, what we’re saying is that the treasury scheduling was the ultimate cause of the inverted yield curve. By starving the long end, they conspired to manipulate the world’s currency markets for the purpose of electing their candidate, who at the time had been drooling in his corn flakes for quite sometime. One hopes they protect the nuclear launch button.

The risk of staying on the short end is that government could try to restart the financial repression regime. They needed financial repression to avoid a deep recession in the pre-COVID period. Why would this need suddenly evaporate, absent any structural changes in the economy? If anything, our structural problems seem worse now (higher debts, higher wealth concentration, more fragile geopolitics, higher societal strife and discontent, etc.)

Perhaps the financial repression has already begun. We see rate reductions coming on the short end. We see forced reductions on the long end (as described in this article). Powell stood proudly on the tracks for a bit, but now he’s shaking as the freight train comes into view.

I bought a nice chunk of TLT many months ago when LT rates were pushing the 5% range, and that has been a nice hedge against Fed dovishness of late (including the recent policy pivot).

Regarding bond funds, short term funds currently benefit from a higher yield and less risk if interest rates go up.

You made a good move buying buying TLT at the peak, but your return is being driven by the FED’s effort to suppress long term rates. Staying in the fund my be a good idea or not, if long rates stay the same, you are not getting enough yield to compensate for the risks in my opinion, and we’ve already seen what happens when long rates go up.

It is now in the public record via numerous previous staffers that it was the former occupant who had them worried about the button. There is the newly released book by McMaster, but that just one.

In his blistering, insightful account of his time in the Trump White House, McMaster describes meetings in the Oval Office as “exercises in competitive sycophancy” during which Trump’s advisers would flatter the president by saying stuff like, “Your instincts are always right” or, “No one has ever been treated so badly by the press.” Meanwhile, Trump would say “outlandish” things like, “Why don’t we just bomb the drugs?” in Mexico or, “Why don’t we take out the whole North Korean Army during one of their parades?”

Inflation is hard to just wish away. 😂

But inflation has come down form 9% to less than 3 % in last 2years or so.

Yes, the 40% to 100% inflation of prices over a 3 or 4 year period is forgotten now. I know, it’s not the official ‘inflation rate’ for that time frame, but if you’re in a store buying food or other stuff, that’s what it is.

You forgot the “/s”. I’ll never forget.

SOL: If you haven’t noticed that in the last 4 years, somebody else must be doing the buying for you and not mentioning it.

No /s needed.

“But inflation has come down form 9% to less than 3 % in last 2years or so.”

So everything we need went up about 30% over 2 years (1980 truthful CPI) and none of it will be given back. So now we add 3% or more to that every 12 months. How nice

Prices of all major durable goods categories — motor vehicles, electronics, furniture, appliances, etc. — have come down, and some like used cars, have plunged. Prices of gasoline have plunged. These things really are a lot cheaper than they were two years ago.

What hasn’t come down are food and services. Insurance continues to roar higher.

LOL!!! That is still a 3% rate of change ON TOP OF prices people cannot afford. So, the unaffordable is becoming more unaffordable.

“So, the unaffordable is becoming more unaffordable.”

🤣 People can afford it just fine, it seems: GDP growth for Q2 was revised up today to 3.0% because inflation-adjusted consumer spending jumped by 2.9% (revised up from +2.3%).

People who think that consumers are tapped out and don’t have anything and cannot pay for a $400 emergency and are way over their heads in debt will never understand the US economy and will always be surprised by it.

not at the grocery store, not for services and restaurants, not for those who live in reality

Quote:

“These lower long-term yields contribute inflationary fuel to the economy. They reduce mortgage rates. They encourage corporate leverage. They loosen financial conditions. This comes on top of the vast deficit spending, which also adds inflationary fuel to the economy.”

“Vast defcit spending” isn’t inflationary because a government always borrows “already existing money” (except when e.g. the FED “creates money out of thin air”.)

It’s very inflationary because the government borrows from investors who sit on cash and don’t spend it, and then spends and distributes that cash directly in the economy. That cash went from sitting somewhere to circulating in the economy and driving up demand.

– Yes, in that one case but how much cash is there “floating around” right now ?

Keynesian governments hate “idle savings” more than anything – especially when the “idleness” is the result of investor uncertainty/dismay at the perpetual f-ups of Keynesian governments.

It is a problem caused by huge income inequality that sits idle and very little makes it back to the productive sectors of the economy. This super rich class is a drag on the economy. Forcing them to inject spending lessens the drag, I suppose. But how much of the spending will be productive? Maybe it all just churns in the stock markets. Said markets getting a nice big “Vig” as a result.

Yes, it’s a problem, a surfeit of savings over real investment outlets.

Link: “Changes in Wealth and the Velocity of Money”

https://files.stlouisfed.org/files/htdocs/publications/review/87/03/Changes_Mar1987.pdf

It results in a cessation of the circuit income velocity of funds.

I am not in a position to know but the super rich, let’s say 50 million+) can simply spend their investment gains without touching any of their base money. It’s like you could buy much of the Midwest and only increase your wealth and those land purchases might distribute wealth to other land owners but are of no productive value. Ideally money spent would have decent productive value.

“Inflation is always and everywhere a monetary phenomenon.”

-Milton Friedman

That simplistic line keeps getting regurgitated because it’s simplistic. But it’s was wrong.

Consumer price inflation is a complex phenomenon, a big component of which is mass psychology — the inflationary mindset, where consumers pay whatever, and where companies know they can rise prices without gutting their sales, confident that their customers will pay whatever. And this is exactly what happened in 2021-2023.

Nobody borrows money they don’t intend to spend into the real economy. They also promise added production to pay it back, with interest, in the future. That’s all inflationary. The federal government is spending 6+% of GDP in deficit and it’s all inflationary.

I have often borrowed money I do not intend to spend into the real economy. I often borrow (usually through getting an unneeded mortgage on a house I fully own) and then invest the money for a greater return than the loan.

Mortgages are great for borrowing because they are uncallable leverage at fairly low rates.

You seem to be saying that govt borrowing crowds out other borrowing and thus does not cause inflation. This seems right to me.

Well, that is the conventional, conservative argument against government deficits cited by every budget busting politician since at least the shining city on the hill was floated.

Since you seem to have a different POV about the cause of inflation and the current excessive Fed balance sheet unlikely to run out of money anytime soon.

I admire your public admission of an incorrect operational imperative in the same sense of watching a small puppy wandering onto the highway.

I would guess that your second quotation was said during the drama of the great depression. Years and tears after his first comment.

I’m often wrong, thank goodness.

But this game of “rate manipulation” will, somehwere in the (near/distant) future come to bite the US government in the “rear end”.

have been hearing this for last two decades. Nothing would happen to USA govt since it can print $$ ad infinitum and there is demand for USD all over world.

Yup, the cleanest dirty shirt in a closet full of even dirtier or torn-up shirts is still the best option. Looking around in the world, hard to see any of them supersede US’s cleanest shirt title for the next couple of decades…the next big hope before China? Yeah not going to happen…

But outside of those in government goon type jobs you have the country being overrun with crime, drugs and homelessness as people can’t afford housing, healthcare, education, insurance, gas or even food.

What a great plan! Historians will call it depression v2.0.

Only in your fevered imagination. Maybe you should get off the sofa and check out the real world? None of your statements are supported by the facts.

One man’s and woman’s depression is never shared. The shadow of the inequality that haunts our society. You have not overstated your personal experience, I assume, for those who are not wealthy.

I have no other cheer to offer other than to remember the warmth of growing up in a place where nobody really had a pot to pee in.

Escierto, interesting to call it imaginary…

Generally, crime in the US peaked in the early 90s and has steadily declined. However, there has been a very recent uptick in crime rates. More concerning is that the rate of crimes being solved has declined while the crimes being committed increased. Case clearance rates are lower than in the 90s. Those issues combined are probably contributing to people’s perception of crime.

Regarding drugs, drug overdose deaths have massively increased since the 90s.

Same with the number of homeless people.

Uh, cost of housing, healthcare, education, insurance, gas, food… do you even read the articles on this site???

What color is the sky in the world you live in? Your description does not match the real world we live in now.

CHS,

You say recently there was an uptick in crime. That is no longer a true statement. Like many other things, COVID had a huge distortion on crime. There was a jump in crime due to COVID effects, but that has recently declined. 2023 crime stats are generally below 2021 and 2024 will be even lower.

Escierto has to disagree with anything said by someone on the right, it’s how the NPC Karen model is programmed, lol. If I said water was wet hed have a fit and deny it. They really are that deranged.

I wonder if identity theft is a crime, what about credit card theft.

Lots of crime everywhere.

Letting fentanyl into the country to kill all the weak and undesirable is a crime. Letting unvetted migrants into the country is a crime.

JimL, maybe things will trend down, maybe not. Violent crime rates were higher in 2023 than 2019, so the uptick still exists.

Regardless, I was speaking to why people might perceive crime as being out of control.

If it not the US government that prints money, it is the Fed. Right now, with QT, they’re unprinting money.

Of course, they would go back to QE if things got bad.

The Fed is a US government agency, performing services as the government’s central banker. It receives is authority from the 1913 Federal Reserve Act (12 U.S.C. §§ 221 et seq.), funds itself from operations and, as required by the statute, credits all net revenue not needed for operations to the account of the US Treasury.

Re: cleanest shirt. The Swedish, Norwegian and especially the Swiss currencies are much ‘cleaner’ or in the usual term, harder, but there are not enough of them to form a universal medium of exchange.

Back in the day of the US dollar crisis, when American ownership of gold was made illegal, the old West German D- Mark was a prime currency store of value with much more depth. German auto exporters were quoted at one point at being ‘in despair’ at the refusal of the Bundesbank to weaken the D-Mark.

The perennial problem of Swiss industry is the strength of the Swiss Franc. Solution: Join the euro zone. That solved Germany’s overly hard D- Mark problem. But sometimes solving one problem creates another. Not sure of the number but believe the ECB owes Germany 2 trillion euros for its help in bailing out other euro zone members.

According to Economic Times, Germany was owed 1.23 trillion euros as of 2022.

As long as the dollar is the gold standard. Not one of the countries cited has the capacity to support a world economy and are derivative currencies.

Actually, part of the problem of a defunct relative currency valuation system. The Japanese carry trade is a good example.

The currency system auto adjusted too accommodate the excess issuance of the Japan Central Bank QE program, and maintain the agreed upon conversion ratio.

Derivative of what?

A lot of folks commenting about a possible US$ crisis forget, or never knew, there’s already been one. Volker had more than inflation to deal with, he had a currency crisis. Americans were flocking to gold, D Mark, Swiss Frank. A US couple on a long stay in Italy were asked if they could please pay in lira instead of US$ , which had fallen during their stay. The US$ was crashing.

Back then btw the Swiss franc was still gold backed, so in a way you could say it was derived. It was defined as as set amount of gold.

It no longer is. If they decoupled to weaken the SF, it hasn’t worked. There has never been a Swiss currency crisis, except, its ongoing problem of being too high.

Thanks a lot WR for putting this article.

Nothing new here as we all knew that Treasury/FED is manipulating the rates in various ways to support low rates but still keeping the charade going.

You’re wrong in with “Treasury/FED”: the Fed hiked a bunch and kept rates there for 14 months, and rates a still there, while the government is fighting the Fed to push down long-term rates. RTGDFA

Why do you think this isn’t a bigger scandal?

It’s not a “scandal.” The White House is trying to stimulate the economy, every White House is trying to stimulate the economy, which is what the White House always does. You can see that in the campaign promises on both sides now. They just have different approaches. They hate the fact that the Fed cracks down on inflation by raising rates to slow the economy. Congress is the same. They all want to borrow endless amounts of money for free or nearly free and stimulate the economy with it.

That’s a lot of initials to RTFA but entertaining nonetheless

What do you see in short term treasury bill and note interest rates? Like 26 week to two-year maturities?

Is this a new thing? I can’t remember ever reading about a debt swap program like this before.

What I don’t understand is why any entity that had borrowed money for 20 years at bargain-basement prices (in this case, the Treasury) wouldn’t want to keep the loan all the way to maturity. They must immediately replace any money they return early — and at a much higher price. Seems like there ought to be ways suppressing long-term rates without taking this dreadful hit…? Isn’t this really just covert bank recapitalization at taxpayer cost? It would hardly be the first time.

That $110 million in 1.25% 20-year bonds that the Treasury bought back today at a discount of 34% reduced the national debt by $37 million ($110 million times 34%).

It goes like this:

1. to get the cash, issue $73 million in new debt: national debt +$73 million

2. use that $73 million in cash to buy back $110 million in 20-year bonds at a 34% discounts and retire them: national debt -$110 million

Net reduction in the national debt from this buyback: $37 million ($110 million – 73 million)

Cash out refis are back!

Well yes, but there’s a sleight of hand here.

Say the $110 million of debt to be retired early INCLUDES all future coupon obligations over X years. Doesn’t it? That gives us the 34% discount to retire the debt now, because now those coupon payments won’t have to be paid.

But then, to be consistent, the $73 million value used to fund the debt retirement must ALSO include all future coupon payments over the same X years. The only way that works out as a net win for the borrower is if the interest rate has gone down. But in fact it has gone up.

Now, if the $73 million value used to fund the debt retirement is over a shorter duration? Why yes, that does create the appearance of lower cost for the same debt. But — unless the government magically stops needing to borrow after that shorter duration elapses (ha!) then that debt must be rolled over again, and again, and again. Once we get out to the original X years’ worth of debt that was retired, the accumulated coupon payments will likely be MORE than they were if the government had just held on to the long-duration bonds.

Early repayment of long-duration cheap loans using short-duration expensive loans simply gives the instantaneous numerical appearance of a decrease in debt. But extending coupon payments out over the original long timeframe, not so much.

I think so too.

Kinda like a payday loan ?

Yes, this is why it amounts to a bet that long-term yields in the future will be lower than they are now. If that happens, Treasury can re-issue some of the debt it’s buying back via long-term bonds without having swapped 1.25% debt for debt at a much higher rate.

What I’m curious about is what happens if (when?) they aren’t. Does Treasury just keep issuing more and more bills to keep up with the expanding debt? And if so, does the demand for short-term debt keep up with that or is there a limit somewhere? If so, and short-term yields rise while long-term yields are also unappealing to it, what does Treasury do then? Surely they’ve thought these contingencies through and have a plan for them…

I think you need to factor in the increase in the cost of interest payments, though:

$110M in principal at 1.25% over 20 years = $1.37M in interest cost per year, times 20 years – 27.5M in interest cost over the duration of this bond.

$73M in principal at 4% over 20 years = $2.92M in interest cost per year, times 20 years = $58M in interest costs over the duration.

Overall, that’s $20.5M in additional interest that treasury will need to pay.

So, the net reduction in debt is $37M – $20.5M = $16.5M

Still a reduction but not as much. And the yearly increase in interest costs will affect the budget and increase the deficit in the short term.

So, the auction is targeting bonds that were at less than 2.5%. It’s a good deal for the Treasury, that’s for sure. But what impact that would have on higher yielding bonds that are still outstanding. Would that make those more valuable or have no real effect?

What kind of effect would this have on the current bonds? Reduction of supply, would necessarily increase price if the demand remains the same, right? So, the newer bonds would effectively have lower yield. Is that right?

Conversely, if more Bill are put into the market, there would need to be a higher (?) yield that would try to drain the supply that Treasury is putting onto the market. What does that mean when the Fed starts to cut rates, but Treasury still has to borrow this massive amount. I guess the question is really, what would have more of an impact, Treasury’s supply that has to be taken by someone, or the Fed chopping interest rates. Wonder which side of the boat is more loaded at that point, whether there are still more people piling into Bills because is risk free asset (force yield on these new Bills to go up) or there is more supply because the Treasury has to finance the government somehow due to deficits, so in the latter case supply would outstrip demand, and drive a lower auction price.

@Wolf Richter

So, we got this additional financial engineering (I am assuming this technique is new) — with Janet at the helms, what else can happen — to bring the LT IR down. Folks use this number (but forget this new wrinkle) to claim recession indicators are flashing.

As I have been thinking, too many financial engineering in different sectors (today NVDA said, they will spent 15B in 2 quarters for stock buyback – they included their one cent a share dividend in the same sentence but that is miniscule), the internet and apps that opened our markets for the world average Joe are all distorting and making all the old rules useless.

I guess, there is connection to inflation and LT interest rates. /Sarc

This is this kind of engineering as us selling some stock and getting MM. :)

Treasury did buybacks before a few times, including in 2002-2003.

…at long last, universal ‘next-quarter thinking’ reducto ad absurdium?.

may we all find a better day.

“For example: 66 cents on the dollar. $110 million of 20-year bonds (CUSIP 912810SR0), with a 1.25% coupon.

Today, the 20-year yield is 4.22%. 16-year yield little less.

So, instead of paying the 1.25% coupon rate, they are going to pay the T-bill rate which is much higher”.

I forgot, there was article / controversy on this — talking about manipulation of economy for political reasons — by two well known economists – one Raghuram Rajan?

A newly published white paper is causing a stir on Wall Street and in Washington by accusing the Treasury Department of conspiring to boost the economy for political ends, and of risking a revival of inflation in the process.

The paper, published last week, claims that the Treasury Department’s decision to continue financing an outsize chunk of the U.S. debt with short-term Treasury bills is tantamount to deliberate manipulation of the economy.

co-authors Stephen Miran and Nouriel Roubini

Over the past nine months, the Treasury’s excess issuance of bills has had an impact similar to roughly $800 billion in quantitative easing, the Fed’s postcrisis bond-buying program, Miran and Roubini contend.

This is equivalent to lopping 25 basis points off the 10-year yield, or a full percentage point from the federal-funds rate.

That white paper called it “backdoor QE,” which is stupid-ass manipulative bullshit; and that’s where I stopped reading. People who put that kind of BS into a paper to get attention don’t deserve attention.

QE involves money creation. This here is essentially just a swap of bonds since the Treasury cannot create money (it has to sell new bonds to get the cash to buy back the old bonds).

One of the effect of qe is loose financial conditions as fed buys long term bonds thus pressing down yields.

Treasury is effectively doing the same by doing these tricks ..

Stupid BS. The effect of QE is creation of money that then chases after assets forever until QT destroys it. The Fed creates $10 billion and buys $10 billion in bonds from a primary dealer, so now the primary dealer has $10 billion in cash and no bonds, so they use that cash to buy $10 billion in securities, maybe bonds, maybe stocks, maybe whatever. So now the sellers of those securities have that $10 billion, and they have to do something with it, and so they buy real estate and derivates and stocks and what not, and now THOSE sellers have the $10 billion and they buy something with it, ad infinitum. And with this new demand endlessly chasing after assets, prices rise. QE creates money that then chases after assets forever until QT destroys this money. That’s the effect of QE.

Financial conditions tighten and loosen for all kinds of reasons — and we have seen that.

Obviously, the FED isn’t “tight”. But changing the mix in its SOMA portfolio didn’t cause 2nd qtr gDp to reach 3%

Nice. So the FED is about to reinstate the punishment of savers. And the Treasury is doing all they can to make sure they are not only punished, but comatose. Or dead.

Spend as little as possible and work against the system. If only I could get the greedy, materialistic in this country to do exactly that. I think our (meaning this corrupt country) time is coming. I fully believe it will backfire eventually. When, I don’t know, but it will happen.

Only those foolish enough to buy long term debt from the USG a sketchy borrower with increasingly lower trustworthiness.

The wealthy cannot be allowed to lose their shirt even when they bet wrong. It would disrupt the functioning of capitalism that would occur during a messy bankruptcy of a scion of capitalism.

“T-bill and chill”, love it!

– a “moderately well-behaved” commenter

Interesting reading: that there is a market so peeps can take losses now is amazing. Why would people/corporations sell their treasuries at a loss unless there is a gun to their heads? They must be making some money on their investment.

There is a mountain of debt out there. Do they expect everybody to retire it at a loss? Will there be holdouts for full value?

The sheer incompetence is astounding

It’s pretty competent, I think, for what they’re trying to do because it’s working.

It’s kinda like buying and selling peaks and valleys when you control the wave machine. Not bad work if you can get it.

This technique has ”worked” for construction contractors for eva, but only short term.

It was called, ”Borrowing from Peter to pay Paul.” by the old timers when I first heard of it in the 1950s, and they were advising me never to do it because it always ended in bankruptcy.

While it seems BK will NOT result from this being done by USA GUV MINT, the inevitable result then must be inflation and resulting loss of value of OUR $$$s.

When using the official BLS inflation calculator, we have already lost value so that it takes $32.38 2024USDs to equal $1.00 1913USD.

Other sources seen in past, but nowhere to be found these days, indicate it’s more likely $100 to$1.

Makes me very happy to be a ”short timer,” that’s far damn shore.

The last thing the government wants is price discovery. Stocks, Real Estate or Bonds.

Probably more complicated and nuances but from a simple man’s optic, this certainly looks that way.

Maybe too simplistic of a view but if short-term will be driven down from rate cuts soon and long-term is suppressed….it sure does look like they are putting us on the path to reaping fixed income low risk returns and forcing people to either buy overpriced assets or back to the stock market it goes…

“….it sure does look like they are putting us on the path to reaping fixed income low risk returns and forcing people to either buy overpriced assets or back to the stock market it goes…”

That’s exactly what they are doing. It’s disgusting. With any luck, it will backfire on this corrupt country.

How is this destroying price discovery? The treasury is buying the 16 year bonds at market prices?

Yep. Cat’s out of the bag here.

The market price fluctuates based demand. If a single buyer steps in and consistently buys 4 times as many bonds as all other buyers for a period of time, the price of bonds will drop. That’s exactly what has happened and it is the clear intention of this action. It’s directly contradictory to the Fed’s QE, which drives prices up.

If the Fed had an ounce of integrity, they would ramp up QE to offset this action with more bond sales. But they have no integrity.

Huh? The price of the bonds isn’t dropping. It is rising, that is why rates are staying low.

The rate of a bond move opposite of its price.

So from all this data here, does one still believe that Yellen and Powell do not talk to each other? Not to mention the political power that got them elected. Not to make this into anything political but really guys, no wonder the bottom 50% is mad at Washington.

They weren’t elected.

I wouldn’t be so sure that it’s just the bottom 50%…

So maybe some banks are holding capital losses on these bonds, what happens when they take them? If this was generous stimulative Fed they would roll them at PAR. Or do a QE. This is being done for liquidity purposes, to take liquidity out of the system. Buying a bond is like driving a new car off the lot, they’re all old run bonds. They are offering you 66 cents on the dollar b/c next week it will be worth even less and so will the crap they sell you. We are getting close to another credit downgrade, and risk premia gets the last word.

SPX [1M] plunged from its Jan 2022 high to Oct 2022 low. In Oct 2022 the 10Y spiked and cont up to 5% in Apr 2024 in diversion with the stock markets. The Fed accumulate bonds and 10Y bc rate cuts are coming in

2024/25. The Fed will ease the cost of debt until the gov will be able to significantly cut debt, if they are fully committed to cutting debt, instead of spending on pet projects.

5% in Oct 2023.

Mr. Wolf wrote: “But buybacks occur at huge losses for investors. Today it bought back a 1.25% 20-year bond for 66 cents on the dollar.” This looks like a great bargain for investors, about the rate at the end in the movie; “Margin Call.” Imagine 1.25% exposed for 20 years to the possibility of 1970s style inflation = 0 cents.

Yeah… it is hard for me to imagine that the purpose here isn’t for short-term political gain. As Wolf says, there are a LOT of moving parts that need to happen “just so” in order for this bond swap to come close to breaking even.

The government (ANY government) has to offer some rate of return to get people to buy their bonds. 1.25% for thirty years is a GREAT deal for the federal government. Much as a 3 to 4% mortgage for 30 years is a great deal for homeowners… who are rightfully slow to refinance or move. So dumping a CERTAIN good deal for the government in exchange for a POSSIBLE good deal… just doesn’t make much sense to the grown-ups in the room… unless they have an ulterior motive.

Wolf-

Any feel for how federal debt service as a percent of government outlays or tax receipts will be effected by this Treasury maturity transformation operation?

Also, what happens to rates along the yield curve in that year where Treasury discontinues the operation and recedes from actively manipulating the U.S. treasury markets, or is this more of a perpetual operation?

Thanks for any thoughts you can offer on this mind-bending subject.

So they’re reducing the debt by the discounts, but they’re issuing smaller amounts of more expensive debt to pay for it. So theoretically, over the long term, depending on what rates will do, that could be a wash in terms of interest expense. But it also pushes down long-term yields, making ALL newly-issued long term debt less expensive. So this would be some savings. But right now, they’re funding this with T-bills, which are more expensive than long-term debt, so that would make it more expensive. And lower interest rates reduce tax receipts from income taxes on interest. So there are a lot of moving parts, and I’m not sure as to how this washes out overall. I’m pretty sure, they don’t know either, and I’m certain they don’t really care about that part.

So what happens when they discontinue? Well, if inflation has just fallen totally asleep by then, probably not much happens. But if inflation is alive and well and thriving, I think the next administration is going to have their hands full dealing with this.

More expensive but for a shorter time. So eventually when rates going down, this seems a solid accounting move on their part.

Intuitively, it seems that if a long-tern borrower funds operations with shorter term borrowing, she (Yellen) increases our exposure to (and potential fiscal damage from) a rise in Tbill rates.

Didn’t we learn in the S&L crisis that interest rate mismatches are tantamount to playing with fire. I suppose though, that the move from 12% of bonds outstanding in Tbills 10 years ago to 22% now is “only”incremental… it’s not the entire portfolio.

Funny that if this “operation twist” works as planned by treasury, it thwarts Powell’s effort’s to dampen inflation. As commented above, very “bad optics.”

John H,

“Didn’t we learn in the S&L crisis that interest rate mismatches are tantamount to playing with fire”

Exactly.

Seems to me that the Treasury is placing bets that by the time thier “new” short term T Bills come due (the ones created and sold to raise the funds to purchase existing Notes at discounts), that interest rates will be lower.

One has to wonder if Ms. Yellen would be willing to place the same trade (bet?) with her own $kin in the game?

The S&L crisis was made when Congress turned the thrifts into banks.

Seems like the Fed has done it’s homework and is pretty confident that long-term Treasury rates will not be able to go back to 0.2 -0.3% above inflation again anytime soon-

https://www.richmondfed.org/publications/research/economic_brief/2024/eb_24-28

I have been promoting the concept, a hypothesis, that asset price inflation is the native inflation. That we measure, consumer inflation, is a derivative of the cost of higher asset prices.

Monetary policy was designed too support higher asset prices.

Money is an often abused privilege, that has an undefined role in the course of human events.

If they issue enough short-term securities, eventually the rates on those will go up, especially if QT continues. These securities are mostly held by money market funds, and if interest rates dip, then some holder of MMFs will take their money and buy stocks, forcing the MMF to sell short-term Treasury bills.

So we could see a situation where the yield curve rises sharply from the overnight rate, and then falls sharply for the one-year bills and beyond. A $1.7 trillion deficit is bound to break something somewhere.

It sounds wrong to buy back any debt held at fixed negative real interest rates, but that’s because we never get the option of paying only 70% of face value and then re-issuing short term debt to fund it. It must be nice to be the Treasury.

There are other issuers of debt: corpos, munis. Would be interesting to know if they have been doing it.

The so called market interest rate is being subsidized lower by the USG for the benefit of a class of people that could care less about the other 97% of Americans.

This reduces not only country debt payments (less taxing?), but also mortgages, auto loans.

Who they are? 97% of Americans are rather not major TLT holders, but people trying to buy a home and a car.

T-bills accumulation phase : between 2009 and Q4 2015. The Re –accumulation phase : 2021 and 2022. The jump : Oct 2022. The Fed currently own $6T T-bills. Rate cuts are coming. They will send it higher.

On the way up the Fed will take profit. They already did.

Most impotantly, it is a pressure release preventing a catastrophic banking crisis down the road. I think Janet is still working for the Fed while over at the Treasury.

I am guessing this has to do with helping cover the banks of their bad bets on long term securities from the past couple of years. Banks are holding a lot more long term debt at extremely low rates than they are comfortable holding. If all of them dumped as much as they wanted to prices would plummet and all of the banks would suffer.

So the treasury is buying up these bonds at market prices. They are not subsidizing the banks because the banks are having to sell at big discounts, but they (the treasury) are supporting the liquidity of those markets with their constant buying.

The banks are still taking pain by having to sell at big discounts, but the market isn’t locking up and it is clear there won’t be a liquidity crisis.

“These lower long-term yields contribute inflationary fuel to the economy. They reduce mortgage rates. They encourage corporate leverage. They loosen financial conditions. This comes on top of the vast deficit spending, which also adds inflationary fuel to the economy.”

Psychopaths at the helm. There is a place in h e l l for them. I so pray it all backfires on this corrupt country.

Wolf, it seems you have become convinced by Nouriel Roubini et al’s recent argument that the Treasury is intentionally driving down long-term rates to achieve short-term political goals around the economy.

Have you reviewed any of the pushback to Roubini et al by other commentators and Treasury officials? If so, why were you still convinced by Roubini?

“to achieve short-term political goals around the economy.”

I didn’t say that kind of idiotic bullshit. What I said was that they’re doing this to lower long-term rates to stimulate the economy (which also stimulates inflation), that’s what I said.

Don’t try to put political bullshit into my mouth.

Can you explain the difference between “short-term political goals around the economy” and “lower long-term rates to stimulate the economy (which also stimulates inflation)”?

@Wolf: Based on this comment as well as the paragraph in the article [“These efforts by Treasury to push down long-term interest rates are in direct conflict with what the Fed has been trying to accomplish since it began hiking its policy rates.”], can we anticipate that this Treasury action may in fact cause higher-for-longer short term interest rates – that is, interest rate cuts may continue to be pushed out?

Today’s Q2 GDP revision from 2.8% to 3.0%, improved consumer sentiment and spending seem to indicate that the Fed should hold fast and not keel over to the demands of the interest rate cut maniacs.

Treasury can obfuscate and do their dirty tricks – and get away with it. It is the Fed that will be held accountable if inflation flares up again.

When one can borrow long term at 1 per cent and then buy their loan back at 6o cents on the dollar, that makes sense.

Unless one needs to borrow the “new” money at 5 per cent.

Just another example of how our government is manipulating monetary and fiscal policy.

Shakespeare said it best in Puck: “What fools these mortals be!”.

B

Rate cut mania is raging again. May 2-Year auction: 4.875%. August 2-Year auction 3.75%.

Wolf – do you happen to know what duration of T bill the Treasury is selling, eg 4 week bills or more like 52 week?

Second, how much have they bought back YTD in long term bonds, out of curiosity? I’m a bit surprised that you think their bid for those securities is having an impact on yields given the size of those buybacks, although I’ll admit that you didn’t claim that it’s having a 25 bps impact or whatever, just that it’s moving the yield by *some* amount given the thin trading.

The Treasury is selling every kind of T-bill, note, and bond. It’s selling huge amount of them to fund the huge deficits and replace maturing securities.

Here are the auction results for August. It includes, 30-year, 20-year, 10-year, 7-year… etc. securities, and lots of T-bills. Look at both tabs, “Upcoming Auctions” and “Auction Results”:

https://www.treasurydirect.gov/auctions/upcoming/

MW: Dollar General’s stock heads for record plunge after a triple miss for earnings

DG -26.64%

I saw that also. Some MSM commentators are saying that is because DG’s best(poorest) customers are running out of money.

I’m not an expert, but I’ve noticed WalMart’s prices are now often cheaper than DG. Walmart stock is up almost 15%.

IMHO, Walmart is stealing customers from DG.

Even the Dollar Store is getting squeezed. Since they raised prices from $1, to $1.25, our local store has been empty.

I used to buy some canned items at the Dollar Store which are now $1.25. Walmart has most of them at less than $1 now.

Walmart had a blowout quarter because it knows that it’s doing, unlike some of the other retailers. It’s not the consumers; it’s dumb retailers that then blame the consumers for their iniquities. I’ve called this the Brick-and-Mortar Meltdown since 2016.

And consumers are doing well, consumer spending adjusted for inflation jumped by 2.8% in Q2, people sit on cash and have gotten the biggest pay increases in decades, esp. at the lower income spectrum. So why would they go a junk-retailer when they can afford to go to Walmart that has everything in one place?

MW: US Treasury yields rise after latest batch of US economic data

Wolf nailed this and NOT enough people are talking about this. Thank you….

Great explanation.

“These efforts by Treasury to push down long-term interest rates are in direct conflict with what the Fed has been trying to accomplish since it began hiking its policy rates.”

So in effect the Treasury is creating the conditions for another wave of inflation, or at least continued elevated inflation, which will negate the FED’s ability to cut very much without a re-ignition?

Lets just watch and see if the Fed can lower interest rates and if the Treasury can sell all its required issuance at the new lower rates.

If they can, then it’s party on. 6% of GDP fiscal deficits can become 7% or 8% and it wont matter. Nobody’s horizons are more than a year or 3 forward anyway (and probably growing shorter).

If they can’t, then it’s some sort of signal that dedollarization is slowly happening and/or the Fed is losing it’s grip or something else.

Or maybe market for Debt is one area where the normal rules of supply and demand don’t matter ?

In the meantime I see that there are no available aircraft carriers to deploy to the pacific and the Navy is mothballing 17 supply support ships because they can’t come up with crews to man them. Clearly the productive economy is firing on all cylinders.

Maybe get rid of carriers and all the related costs? Out of about 47 in the world, the US has twenty of them with even adding in NATO countries. Russia has 1 and China has 5.

Well, thank goodness the Fed is pushing back against this obvious attempt by the Treasury Department to undo its tightening by…clearly signaling its intent to begin loosening soon!

Is there any way to know if any of the sellers of these bonds back to the govt at a loss are investment funds such as blackrock or vanguard, selling bonds held in peoples 401ks/retirement accounts?

Is it fair to say that the US Treasury (UST) is front-running Wall St by buying long UST bonds for cheap, ahead of the Fed’s announced interest rate cuts?

I mean, usually it is Wall St front-running the Fed by buying long bonds ahead for cheap ahead of upcoming interest rate cuts, but this time it is the UST doing it, for the benefit of the taxpayer citizen !!??

I think it is this exactly. The treasury is front running. I think it has been clear for a very, very long time that rates were going to go down before they went up, but that they weren’t going to go down right away.

So there has been a hidden opportunity for the treasury to buy bonds from stupid investors who thought rates were going to stay low 3 – 5 years ago and finance it with shirt term bonds knowing that eventually rates were going to drop.

It was a genius move. Even better, it doesn’t take advantage of anyone who wasn’t gambling anyway or require taxpayer money.

Thanks for this review, sent to me by John Mauldin.

Lots of comments here about Treasury manipulating interest rates, and mistakenly Fed. I suspect this is much more two things – 1) providing liquidity to investors who need the cash and 2) doing the very intelligent move of buying back long term debt to improve the US balance sheet. If T buys back $1T in debt for $660B, the US balance sheet debt drops by $340B. Cash flow doesn’t change today, but long term, flexibility is achieved.

The Fed is mandated to “promote effectively……. moderate long term rates”, so it shouldn’t be doing things like QE of long term bonds to drive down rates, but it did. The Treasury has no such mandate. )For those who question Fed mandate, read amended 1978 Federal Reserve Employment Act, same document that was morphed into the dual mandate by disingenuous economists 16 years ago.)

Highly appreciated Wolf !!!

This is one of my top articles that I have read on internet. Even learned something new and it instantly cleared my head. Clicked like a charm.

Would be interesting to know who submited bids to sell their government securities. Some speculative investment bank looking for short term goal, or distressed sell? It’s either not publicly disclosed or am not able to find it anywhere.

$35 Trillion divided by 350 million residents in USA = $100,000 each.

Just print and hand out $200,000 to each resident, and tax the windfall 50%.

Debt solved.

Hyper… INFLATION!